Financial Accounting Principles Report - Finance, University of ABC

VerifiedAdded on 2020/10/05

|27

|4402

|498

Report

AI Summary

This report delves into the core principles of financial accounting, encompassing the concepts, regulations, rules, and conventions that govern the field. It begins with an introduction to financial accounting, outlining its purpose and the various regulations associated with it, such as those from the IASB and IFRS. The report then explores key accounting rules, including personal, real, and nominal accounts, along with fundamental accounting principles like materiality, revenue recognition, and the going concern concept. It also examines conventions related to consistency and material disclosure, and the accrual concept. The report includes detailed examples and ledger accounts for multiple clients to illustrate these principles in practice, covering aspects like sales, purchases, and bank transactions. The preparation of profit and loss statements and concepts of bank reconciliation statements are also included, providing a comprehensive overview of financial accounting practices.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

BUSINESS REPORT......................................................................................................................3

(a): Concept of financial accounting and their purpose..........................................................3

(b): Regulations associated with financial accounting...........................................................4

(c): Accounting rules and principles.......................................................................................5

(d): Convention and concepts associated with consistency and material disclosure..............7

CLIENT 1........................................................................................................................................7

CLIENT 2......................................................................................................................................18

CLIENT 3......................................................................................................................................20

CLIENT 4......................................................................................................................................22

CLIENT 5......................................................................................................................................24

CLIENT 6......................................................................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................28

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................3

BUSINESS REPORT......................................................................................................................3

(a): Concept of financial accounting and their purpose..........................................................3

(b): Regulations associated with financial accounting...........................................................4

(c): Accounting rules and principles.......................................................................................5

(d): Convention and concepts associated with consistency and material disclosure..............7

CLIENT 1........................................................................................................................................7

CLIENT 2......................................................................................................................................18

CLIENT 3......................................................................................................................................20

CLIENT 4......................................................................................................................................22

CLIENT 5......................................................................................................................................24

CLIENT 6......................................................................................................................................25

CONCLUSION..............................................................................................................................26

REFERENCES..............................................................................................................................28

INTRODUCTION

Finance is a wider term that provide information about two associated activities such as

the study of managing money and actual process of acquiring required capital. It has been

analysed that individual or government both need funds to operate their business. It is an

economic activity that would assist commercial entities to generate maximum profitability for an

organisation for short period of time. Financial accounting can refer as management of

recording, summarising and evaluating various transactions that are incurred by the company

during an accounting period of time. This project is all about providing specific information

about regulations those are associated with the accountancy. Apart from this, rules, principles

and conventions related with the accounting which is being discussed under this report. Further,

this project consists of prime entry and ledger accounts. Preparation of profit and loss statement

of LMS Ltd is also being given below. Concepts of bank reconciliation statement and associated

recording of transaction by Kendal Ltd is mentioned under this report effectively (Edwards,

2013).

BUSINESS REPORT

(a): Concept of financial accounting and their purpose

Finance is said to be one of the specific art and ability to managing overall funds that are

generated by the company within an accounting period of time. It consists of financial services

and instruments. It consists of capital, funds and money that are generated within an

organisation. Financial accounting is one of the reliable aspects of recording, classifying and

evaluating overall management of various transaction as well as capital that are invested in

different projects of the company. On the other hand, it is also associated with preparation of

various statements or reports such as incomes statements and balance sheet of an organisation.

The role of financial manager is to make proper availability of essential aspects that are useful

for the company to organise their entire business operations in well manner (Zeff, 2016). There

are various types of information that are associated with finance and non-finance on continuous

basis. That would lead to make use of automatic system to record each entries. There are various

types of accounting statements which are prepared by the finance officers. Some of them are

mentioned underneath:

3

Finance is a wider term that provide information about two associated activities such as

the study of managing money and actual process of acquiring required capital. It has been

analysed that individual or government both need funds to operate their business. It is an

economic activity that would assist commercial entities to generate maximum profitability for an

organisation for short period of time. Financial accounting can refer as management of

recording, summarising and evaluating various transactions that are incurred by the company

during an accounting period of time. This project is all about providing specific information

about regulations those are associated with the accountancy. Apart from this, rules, principles

and conventions related with the accounting which is being discussed under this report. Further,

this project consists of prime entry and ledger accounts. Preparation of profit and loss statement

of LMS Ltd is also being given below. Concepts of bank reconciliation statement and associated

recording of transaction by Kendal Ltd is mentioned under this report effectively (Edwards,

2013).

BUSINESS REPORT

(a): Concept of financial accounting and their purpose

Finance is said to be one of the specific art and ability to managing overall funds that are

generated by the company within an accounting period of time. It consists of financial services

and instruments. It consists of capital, funds and money that are generated within an

organisation. Financial accounting is one of the reliable aspects of recording, classifying and

evaluating overall management of various transaction as well as capital that are invested in

different projects of the company. On the other hand, it is also associated with preparation of

various statements or reports such as incomes statements and balance sheet of an organisation.

The role of financial manager is to make proper availability of essential aspects that are useful

for the company to organise their entire business operations in well manner (Zeff, 2016). There

are various types of information that are associated with finance and non-finance on continuous

basis. That would lead to make use of automatic system to record each entries. There are various

types of accounting statements which are prepared by the finance officers. Some of them are

mentioned underneath:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit and loss statement: It is one of the main report that will be prepared to record

every income earn by the company and total expenses given to get that particular profits.

Managers are responsible for analysing net profit and loss generated during the period of time.

Purpose:

The primary objective of preparing income statement is done to analyse total earning a

company is generating from the entire sale of product and services.

It would be further evaluated for the purpose of attaining certain loan from financial

institution to organise their projects (Alver, Alver and Talpas, 2013).

Balance sheet: It is said to be effective financial statement that displays company’s total assets

and liabilities of the company. It has been found that a standard format followed within an

organisation consists of two sides.

Purpose:

To examine necessary changes in an individual goods recorded into the balance sheet so

that upcoming decision can be made effectively.

To determine owner funds as well as indicate certain chance of growth in coming period

of time.

Cash flow statement: It is known as one of the reliable statement that can provide overall

analysis about the total cash inflow and outflow incurred by the company within an accounting

period. It can be collected from various activities such as operating, financing and investing.

Purpose:

The primary purpose of this statement is to deliver information regarding cash receipts,

payments and net changes in cash outcomes from various activities.

To deliver statements to the investors in order to analyse position of cash they are having

to plan their upcoming projects.

(b): Regulations associated with financial accounting

In every business organisation, accountant used to follow necessary rules and regulation

that are made by the concern agencies of board to record each and every transaction in correct

manner. This will provide certain base to remain away from any kind of mistakes that are

generally occurs while recording (Fourie and et. al., 2015). For the purpose of managing and

controlling the financial results at large scale is little tough task. It should not be simple to

evaluate the results, whether transactions are posted accurately in their concern format. In

4

every income earn by the company and total expenses given to get that particular profits.

Managers are responsible for analysing net profit and loss generated during the period of time.

Purpose:

The primary objective of preparing income statement is done to analyse total earning a

company is generating from the entire sale of product and services.

It would be further evaluated for the purpose of attaining certain loan from financial

institution to organise their projects (Alver, Alver and Talpas, 2013).

Balance sheet: It is said to be effective financial statement that displays company’s total assets

and liabilities of the company. It has been found that a standard format followed within an

organisation consists of two sides.

Purpose:

To examine necessary changes in an individual goods recorded into the balance sheet so

that upcoming decision can be made effectively.

To determine owner funds as well as indicate certain chance of growth in coming period

of time.

Cash flow statement: It is known as one of the reliable statement that can provide overall

analysis about the total cash inflow and outflow incurred by the company within an accounting

period. It can be collected from various activities such as operating, financing and investing.

Purpose:

The primary purpose of this statement is to deliver information regarding cash receipts,

payments and net changes in cash outcomes from various activities.

To deliver statements to the investors in order to analyse position of cash they are having

to plan their upcoming projects.

(b): Regulations associated with financial accounting

In every business organisation, accountant used to follow necessary rules and regulation

that are made by the concern agencies of board to record each and every transaction in correct

manner. This will provide certain base to remain away from any kind of mistakes that are

generally occurs while recording (Fourie and et. al., 2015). For the purpose of managing and

controlling the financial results at large scale is little tough task. It should not be simple to

evaluate the results, whether transactions are posted accurately in their concern format. In

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accordance to face with such kind of problems, most of the company are following essential

rules and standards. Moreover, the idea is just to become more valuable to take into account

every decision at major superiority.

IASB (International accounting standard board): It is known as international body

that is made for the purpose of controlling and management for recording of necessary records.

These are formed in order to regulate essential rules in respect to get accurate results in coming

period of time. They use to provide necessary rules and standards in order to record data in

proper manner.

IFRS (International financial reporting standard): It is effective set of accounting

standard that is made by an independent body called as IASB. It is associated with quality

management of bookkeeping so that every transaction is being recorded in proper manner. There

are various regulations that can be needed to be followed within an organisation. Some of them

are:

IFRS 1 (First-time approval of the standards of international financial reporting): It

used to permit early application of new IFRS that is not yet essential but allows early

application. This is the starting point for their accounting in respect with IFRSs.

IFRS 2 (Shared Based Payment): It is made to specify the financial reporting an entity

when it undertakes a shared based payment (Mullinova, 2016).

There are many other regulation standards that are requisite to consider while developing

the file. An organisation need to carry out operations on the grounds of those criteria or

regulation to work ethically.

(c): Accounting rules and principles

There are different types of accounting norms and principles are available through which

an organise can record effective transaction in reliable manner. Some rules are mentioned below:

Accounting rules: It is said to be systematic rules and strategies which will be used to

analyse different accounting transactions. Some of them are given underneath:

Personal account: This is one of the effective rules that are associated with an

individual, organisation or a company. it is more simple to analyse every transaction that

are having the capability to deal with every kind of issues. Example, Debtors, creditors

and consideration for products suppliers.

5

rules and standards. Moreover, the idea is just to become more valuable to take into account

every decision at major superiority.

IASB (International accounting standard board): It is known as international body

that is made for the purpose of controlling and management for recording of necessary records.

These are formed in order to regulate essential rules in respect to get accurate results in coming

period of time. They use to provide necessary rules and standards in order to record data in

proper manner.

IFRS (International financial reporting standard): It is effective set of accounting

standard that is made by an independent body called as IASB. It is associated with quality

management of bookkeeping so that every transaction is being recorded in proper manner. There

are various regulations that can be needed to be followed within an organisation. Some of them

are:

IFRS 1 (First-time approval of the standards of international financial reporting): It

used to permit early application of new IFRS that is not yet essential but allows early

application. This is the starting point for their accounting in respect with IFRSs.

IFRS 2 (Shared Based Payment): It is made to specify the financial reporting an entity

when it undertakes a shared based payment (Mullinova, 2016).

There are many other regulation standards that are requisite to consider while developing

the file. An organisation need to carry out operations on the grounds of those criteria or

regulation to work ethically.

(c): Accounting rules and principles

There are different types of accounting norms and principles are available through which

an organise can record effective transaction in reliable manner. Some rules are mentioned below:

Accounting rules: It is said to be systematic rules and strategies which will be used to

analyse different accounting transactions. Some of them are given underneath:

Personal account: This is one of the effective rules that are associated with an

individual, organisation or a company. it is more simple to analyse every transaction that

are having the capability to deal with every kind of issues. Example, Debtors, creditors

and consideration for products suppliers.

5

Real account: The financial accountant of an organisation is needed to categories every

items as per their impacts of nature. The rules say that “debits what comes in” and “credit

what goes out”. Example, fixed assets and cash.

Nominal account: Under this rules, accountant need to debits all expenditure & losses

and credit all income and earnings. Like for examples, Purchase, sales and commission

earned (Agasisti and Catalano, 2013).

Accounting principles:

Materiality: This seems to be one of the effective accounting principles that finance

manager must be liable to record only material facts or transaction into various statements of the

company.

Revenue recognition: Basically, earning is recognised in only those situations when any

critical event occurs and the amount of earning can be measurable. It is associated with

accounting period under which earning and expenses would easily be analysed effectively.

Conservation: According to this principles, an accountant will use to do in advance or

disclose losses, but it cannot allow same actions for coming future profits. This policy tends to

determine rather than overemphasize net effects and net earnings.

Matching principle: Under this, the data recorded by the accountant must be use for

accrual basis. It is generally associated with the certain aspects that all expenses must be matched

with earning those are generated within the period (Barth, 2015).

Going concern: As, it has been seen that business is continuous process that it is

operated for long time. There accountant believes that companies should not be able to

commence the account until all the statements are not disclosed.

Full disclosure principles: It is crucial for the external or internal parties to make

evaluation of various financial statement. The role of manager to disclose all essential reports in

front of investors so that they can make necessary decision.

Cost principles: As per the accounting principles that every financial and non-financial

information can be recorded only n cash basis.

Time period assumption: This seems to be effective accounting concepts that a business

would report that financial outcome of their activities over a usual time period. It is usually

prepared on monthly, quarterly and yearly basis (Tschopp and Nastanski, 2014).

6

items as per their impacts of nature. The rules say that “debits what comes in” and “credit

what goes out”. Example, fixed assets and cash.

Nominal account: Under this rules, accountant need to debits all expenditure & losses

and credit all income and earnings. Like for examples, Purchase, sales and commission

earned (Agasisti and Catalano, 2013).

Accounting principles:

Materiality: This seems to be one of the effective accounting principles that finance

manager must be liable to record only material facts or transaction into various statements of the

company.

Revenue recognition: Basically, earning is recognised in only those situations when any

critical event occurs and the amount of earning can be measurable. It is associated with

accounting period under which earning and expenses would easily be analysed effectively.

Conservation: According to this principles, an accountant will use to do in advance or

disclose losses, but it cannot allow same actions for coming future profits. This policy tends to

determine rather than overemphasize net effects and net earnings.

Matching principle: Under this, the data recorded by the accountant must be use for

accrual basis. It is generally associated with the certain aspects that all expenses must be matched

with earning those are generated within the period (Barth, 2015).

Going concern: As, it has been seen that business is continuous process that it is

operated for long time. There accountant believes that companies should not be able to

commence the account until all the statements are not disclosed.

Full disclosure principles: It is crucial for the external or internal parties to make

evaluation of various financial statement. The role of manager to disclose all essential reports in

front of investors so that they can make necessary decision.

Cost principles: As per the accounting principles that every financial and non-financial

information can be recorded only n cash basis.

Time period assumption: This seems to be effective accounting concepts that a business

would report that financial outcome of their activities over a usual time period. It is usually

prepared on monthly, quarterly and yearly basis (Tschopp and Nastanski, 2014).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Money unit’s assumptions: It is one of the effective measurement principles that used to

analyse only those transactions that are occurs or express in monetary term. Accounting ignore

the effects of inflation during the time entering the amount.

Economic entity principles: The accountant can have used to record each transaction as

per the length of operation of the company. According objectives as they used to take into

account as two separate entities.

(d): Convention and concepts associated with consistency and material disclosure

Consistency concepts: According to this particular concepts, a financial manager can

assume that various business is having more consistent in nature in regard to various standards

and norms. In accordance to different kind of rules, the accountant required to post transactions

continuously into their format so that mistakes can be overcome and base for future benefits can

be rise.

Material disclosure: Accounting to this particular convention is used by the manager to

record all transaction by using legal rules and regulation according to the request of the company

(Stice and Stice, 2013).

Accrual concepts: This is known as fundamental concepts that would provide specific

information to the accountant to keep recording of all expenditure and earning at the time they

occur.

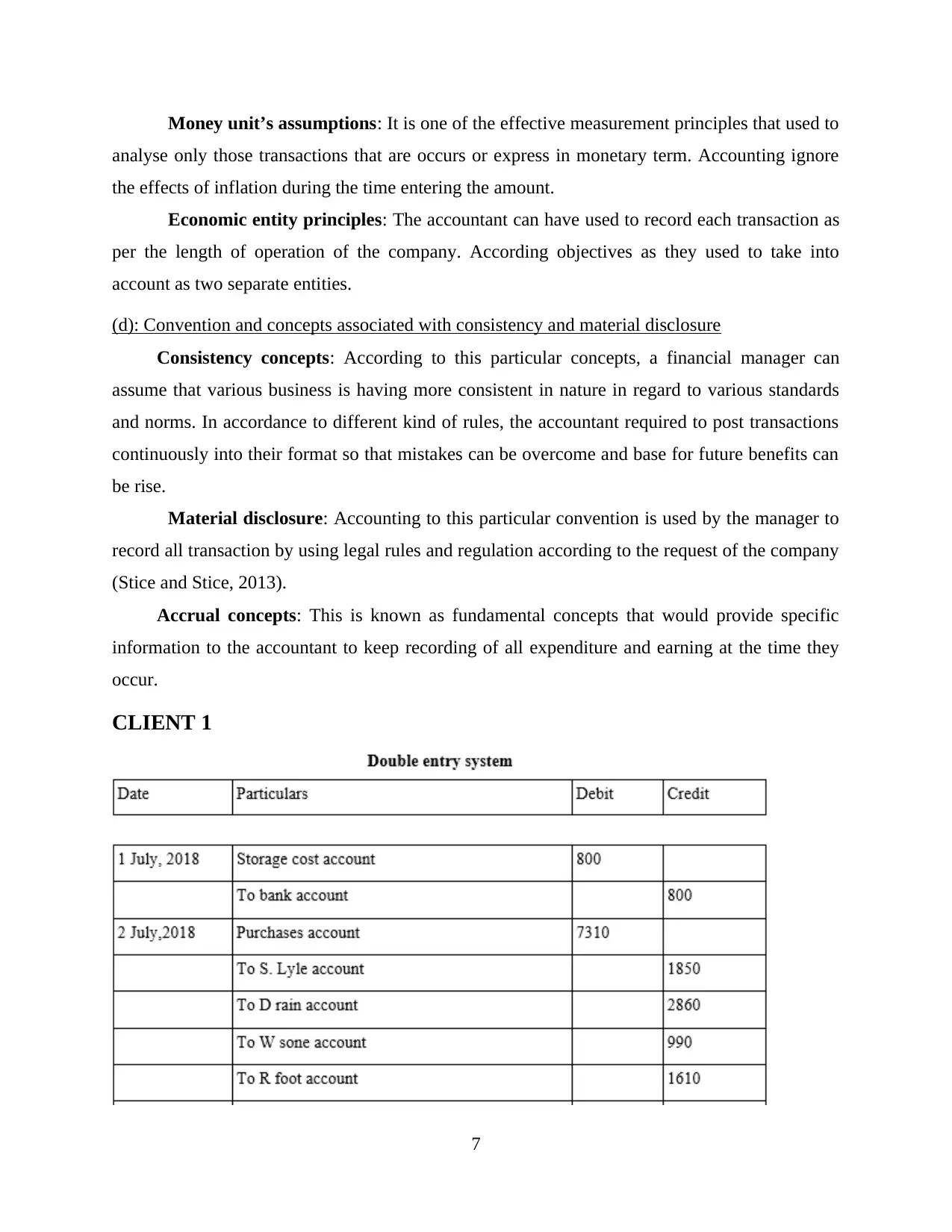

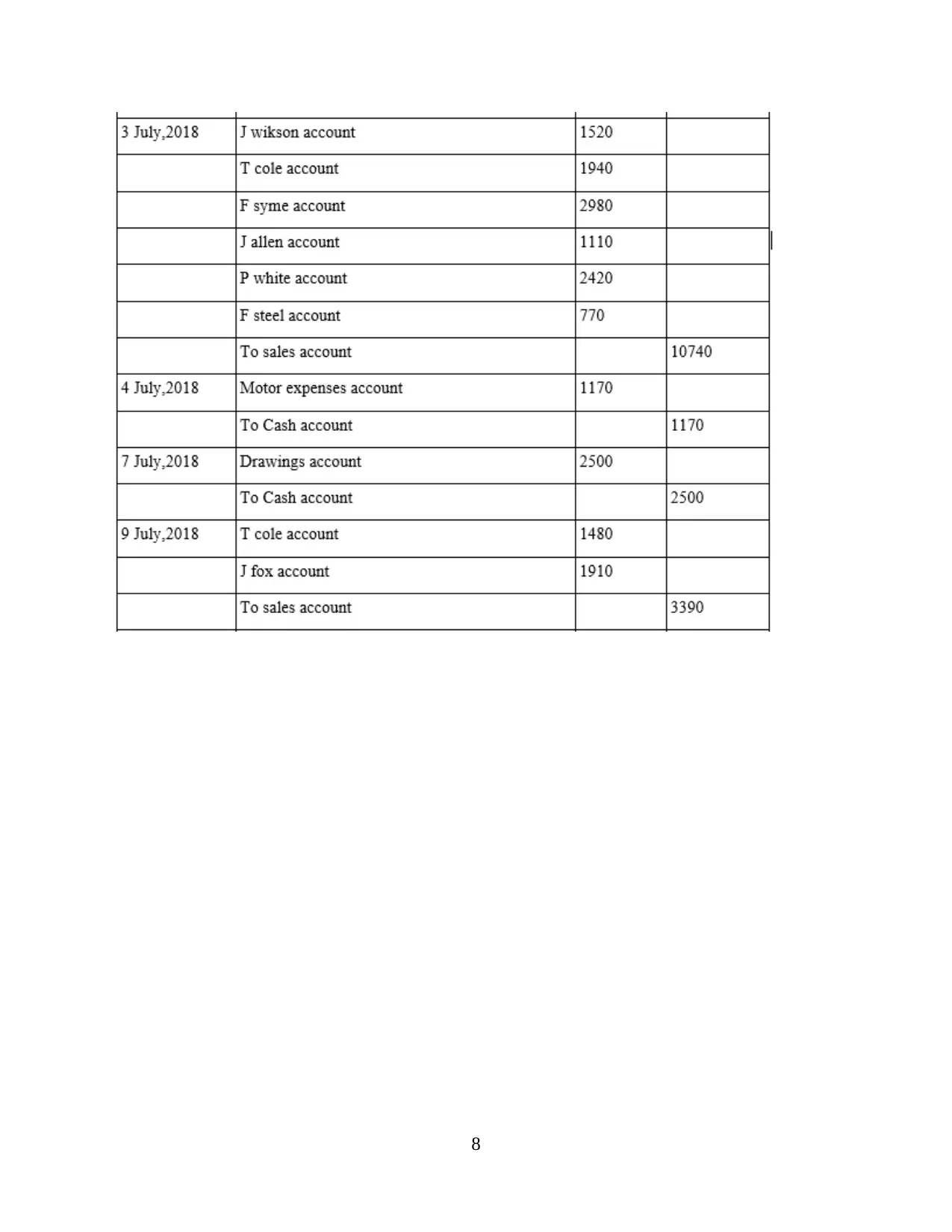

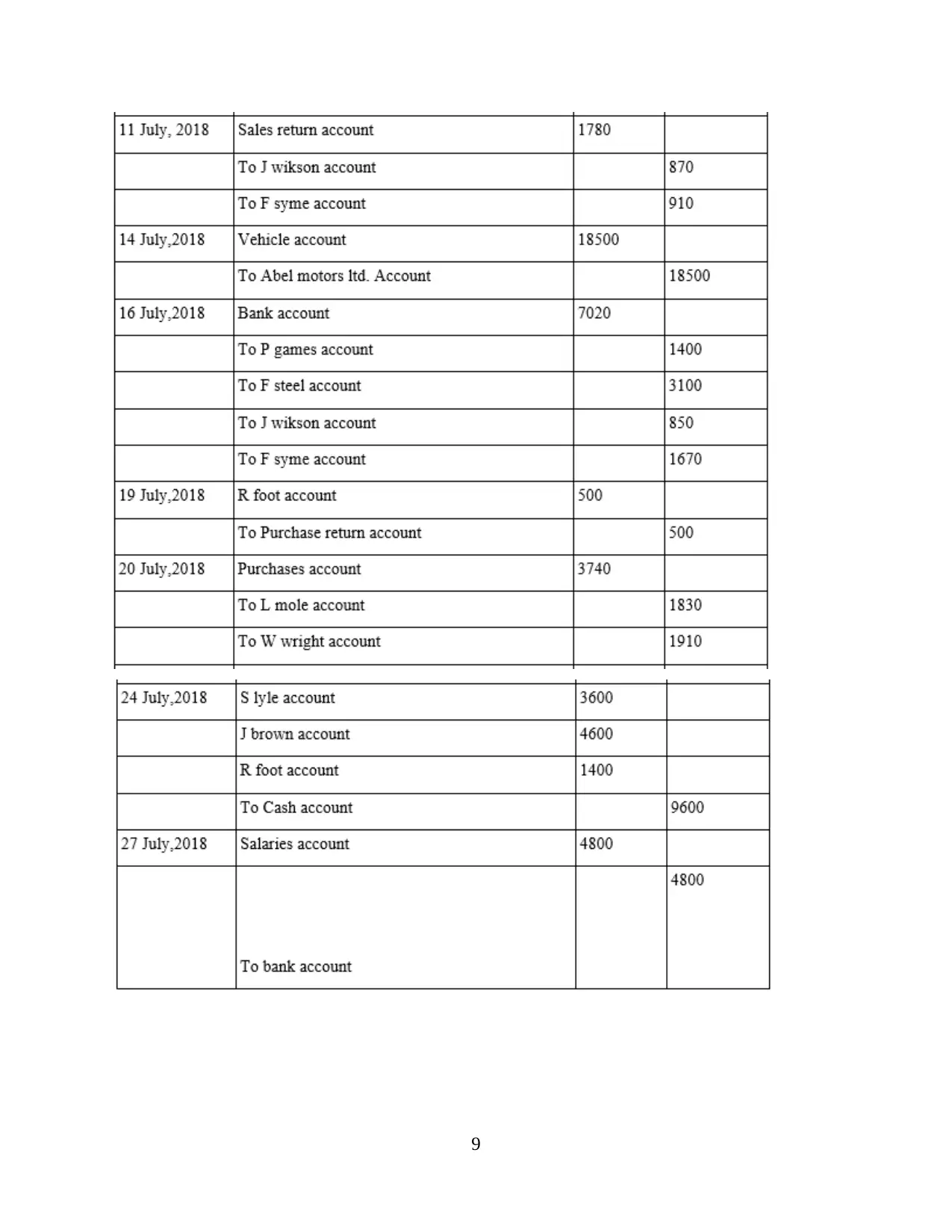

CLIENT 1

7

analyse only those transactions that are occurs or express in monetary term. Accounting ignore

the effects of inflation during the time entering the amount.

Economic entity principles: The accountant can have used to record each transaction as

per the length of operation of the company. According objectives as they used to take into

account as two separate entities.

(d): Convention and concepts associated with consistency and material disclosure

Consistency concepts: According to this particular concepts, a financial manager can

assume that various business is having more consistent in nature in regard to various standards

and norms. In accordance to different kind of rules, the accountant required to post transactions

continuously into their format so that mistakes can be overcome and base for future benefits can

be rise.

Material disclosure: Accounting to this particular convention is used by the manager to

record all transaction by using legal rules and regulation according to the request of the company

(Stice and Stice, 2013).

Accrual concepts: This is known as fundamental concepts that would provide specific

information to the accountant to keep recording of all expenditure and earning at the time they

occur.

CLIENT 1

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

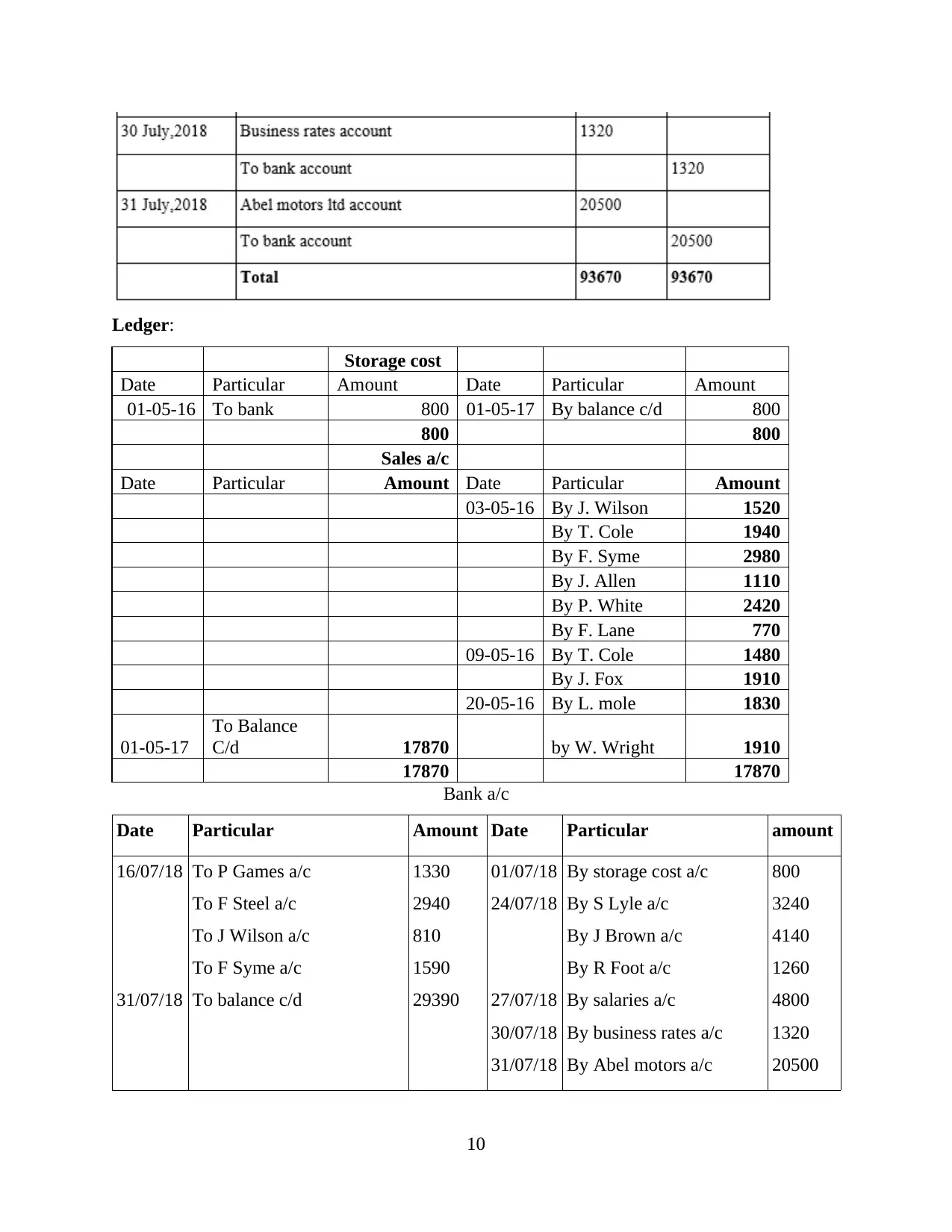

Ledger:

Storage cost

Date Particular Amount Date Particular Amount

01-05-16 To bank 800 01-05-17 By balance c/d 800

800 800

Sales a/c

Date Particular Amount Date Particular Amount

03-05-16 By J. Wilson 1520

By T. Cole 1940

By F. Syme 2980

By J. Allen 1110

By P. White 2420

By F. Lane 770

09-05-16 By T. Cole 1480

By J. Fox 1910

20-05-16 By L. mole 1830

01-05-17

To Balance

C/d 17870 by W. Wright 1910

17870 17870

Bank a/c

Date Particular Amount Date Particular amount

16/07/18

31/07/18

To P Games a/c

To F Steel a/c

To J Wilson a/c

To F Syme a/c

To balance c/d

1330

2940

810

1590

29390

01/07/18

24/07/18

27/07/18

30/07/18

31/07/18

By storage cost a/c

By S Lyle a/c

By J Brown a/c

By R Foot a/c

By salaries a/c

By business rates a/c

By Abel motors a/c

800

3240

4140

1260

4800

1320

20500

10

Storage cost

Date Particular Amount Date Particular Amount

01-05-16 To bank 800 01-05-17 By balance c/d 800

800 800

Sales a/c

Date Particular Amount Date Particular Amount

03-05-16 By J. Wilson 1520

By T. Cole 1940

By F. Syme 2980

By J. Allen 1110

By P. White 2420

By F. Lane 770

09-05-16 By T. Cole 1480

By J. Fox 1910

20-05-16 By L. mole 1830

01-05-17

To Balance

C/d 17870 by W. Wright 1910

17870 17870

Bank a/c

Date Particular Amount Date Particular amount

16/07/18

31/07/18

To P Games a/c

To F Steel a/c

To J Wilson a/c

To F Syme a/c

To balance c/d

1330

2940

810

1590

29390

01/07/18

24/07/18

27/07/18

30/07/18

31/07/18

By storage cost a/c

By S Lyle a/c

By J Brown a/c

By R Foot a/c

By salaries a/c

By business rates a/c

By Abel motors a/c

800

3240

4140

1260

4800

1320

20500

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

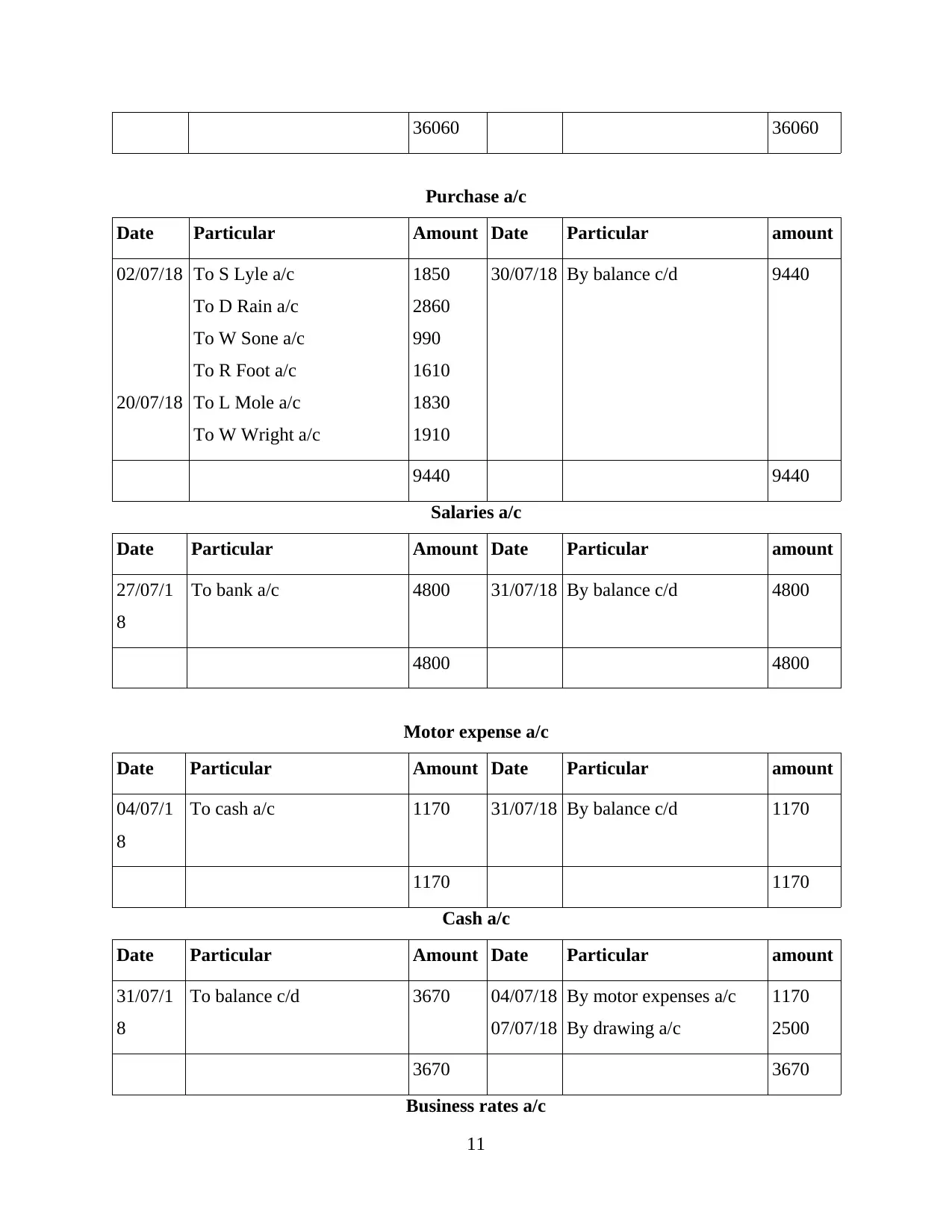

36060 36060

Purchase a/c

Date Particular Amount Date Particular amount

02/07/18

20/07/18

To S Lyle a/c

To D Rain a/c

To W Sone a/c

To R Foot a/c

To L Mole a/c

To W Wright a/c

1850

2860

990

1610

1830

1910

30/07/18 By balance c/d 9440

9440 9440

Salaries a/c

Date Particular Amount Date Particular amount

27/07/1

8

To bank a/c 4800 31/07/18 By balance c/d 4800

4800 4800

Motor expense a/c

Date Particular Amount Date Particular amount

04/07/1

8

To cash a/c 1170 31/07/18 By balance c/d 1170

1170 1170

Cash a/c

Date Particular Amount Date Particular amount

31/07/1

8

To balance c/d 3670 04/07/18

07/07/18

By motor expenses a/c

By drawing a/c

1170

2500

3670 3670

Business rates a/c

11

Purchase a/c

Date Particular Amount Date Particular amount

02/07/18

20/07/18

To S Lyle a/c

To D Rain a/c

To W Sone a/c

To R Foot a/c

To L Mole a/c

To W Wright a/c

1850

2860

990

1610

1830

1910

30/07/18 By balance c/d 9440

9440 9440

Salaries a/c

Date Particular Amount Date Particular amount

27/07/1

8

To bank a/c 4800 31/07/18 By balance c/d 4800

4800 4800

Motor expense a/c

Date Particular Amount Date Particular amount

04/07/1

8

To cash a/c 1170 31/07/18 By balance c/d 1170

1170 1170

Cash a/c

Date Particular Amount Date Particular amount

31/07/1

8

To balance c/d 3670 04/07/18

07/07/18

By motor expenses a/c

By drawing a/c

1170

2500

3670 3670

Business rates a/c

11

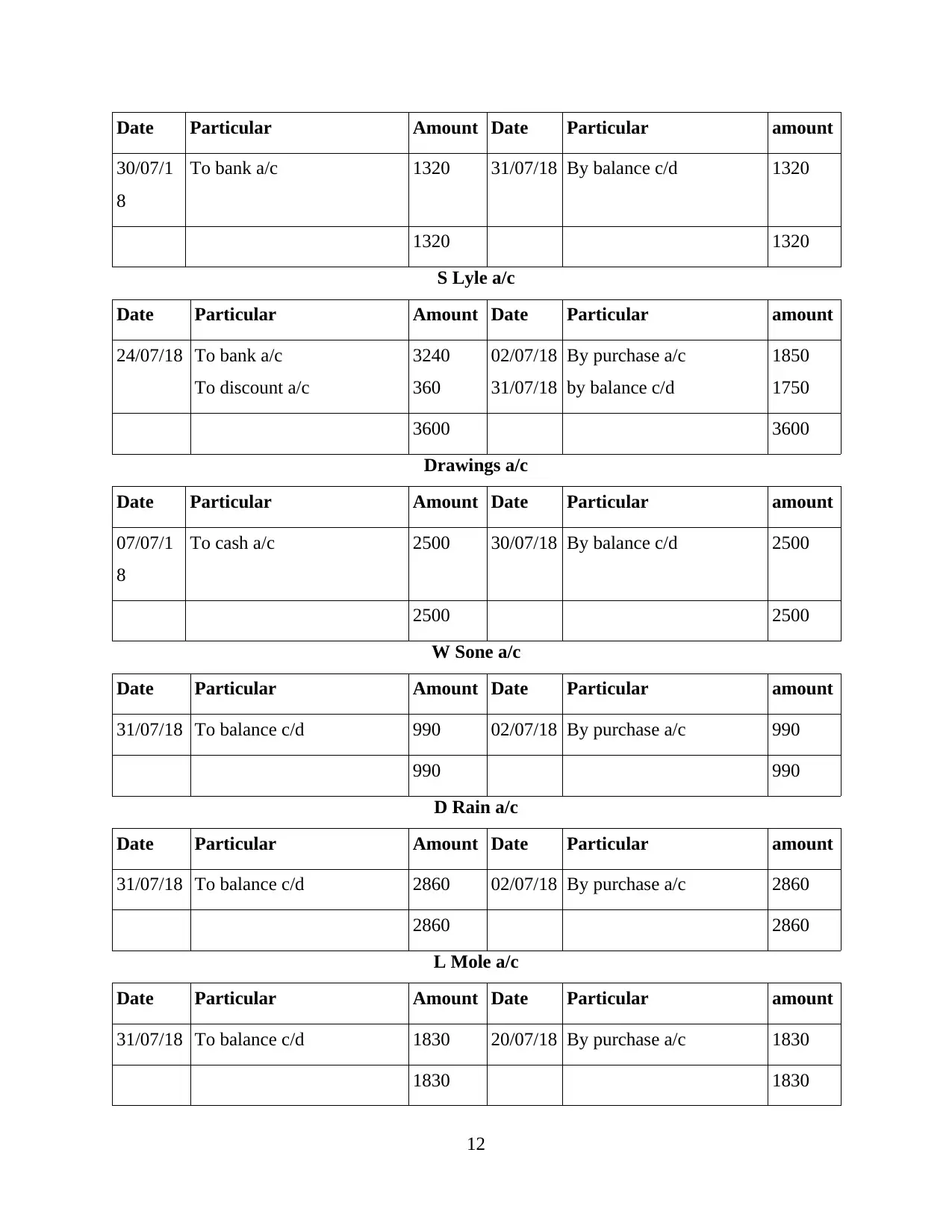

Date Particular Amount Date Particular amount

30/07/1

8

To bank a/c 1320 31/07/18 By balance c/d 1320

1320 1320

S Lyle a/c

Date Particular Amount Date Particular amount

24/07/18 To bank a/c

To discount a/c

3240

360

02/07/18

31/07/18

By purchase a/c

by balance c/d

1850

1750

3600 3600

Drawings a/c

Date Particular Amount Date Particular amount

07/07/1

8

To cash a/c 2500 30/07/18 By balance c/d 2500

2500 2500

W Sone a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 990 02/07/18 By purchase a/c 990

990 990

D Rain a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 2860 02/07/18 By purchase a/c 2860

2860 2860

L Mole a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 1830 20/07/18 By purchase a/c 1830

1830 1830

12

30/07/1

8

To bank a/c 1320 31/07/18 By balance c/d 1320

1320 1320

S Lyle a/c

Date Particular Amount Date Particular amount

24/07/18 To bank a/c

To discount a/c

3240

360

02/07/18

31/07/18

By purchase a/c

by balance c/d

1850

1750

3600 3600

Drawings a/c

Date Particular Amount Date Particular amount

07/07/1

8

To cash a/c 2500 30/07/18 By balance c/d 2500

2500 2500

W Sone a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 990 02/07/18 By purchase a/c 990

990 990

D Rain a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 2860 02/07/18 By purchase a/c 2860

2860 2860

L Mole a/c

Date Particular Amount Date Particular amount

31/07/18 To balance c/d 1830 20/07/18 By purchase a/c 1830

1830 1830

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.