Financial Accounting Report: Stakeholders and Financial Statements

VerifiedAdded on 2021/02/20

|8

|1824

|35

Report

AI Summary

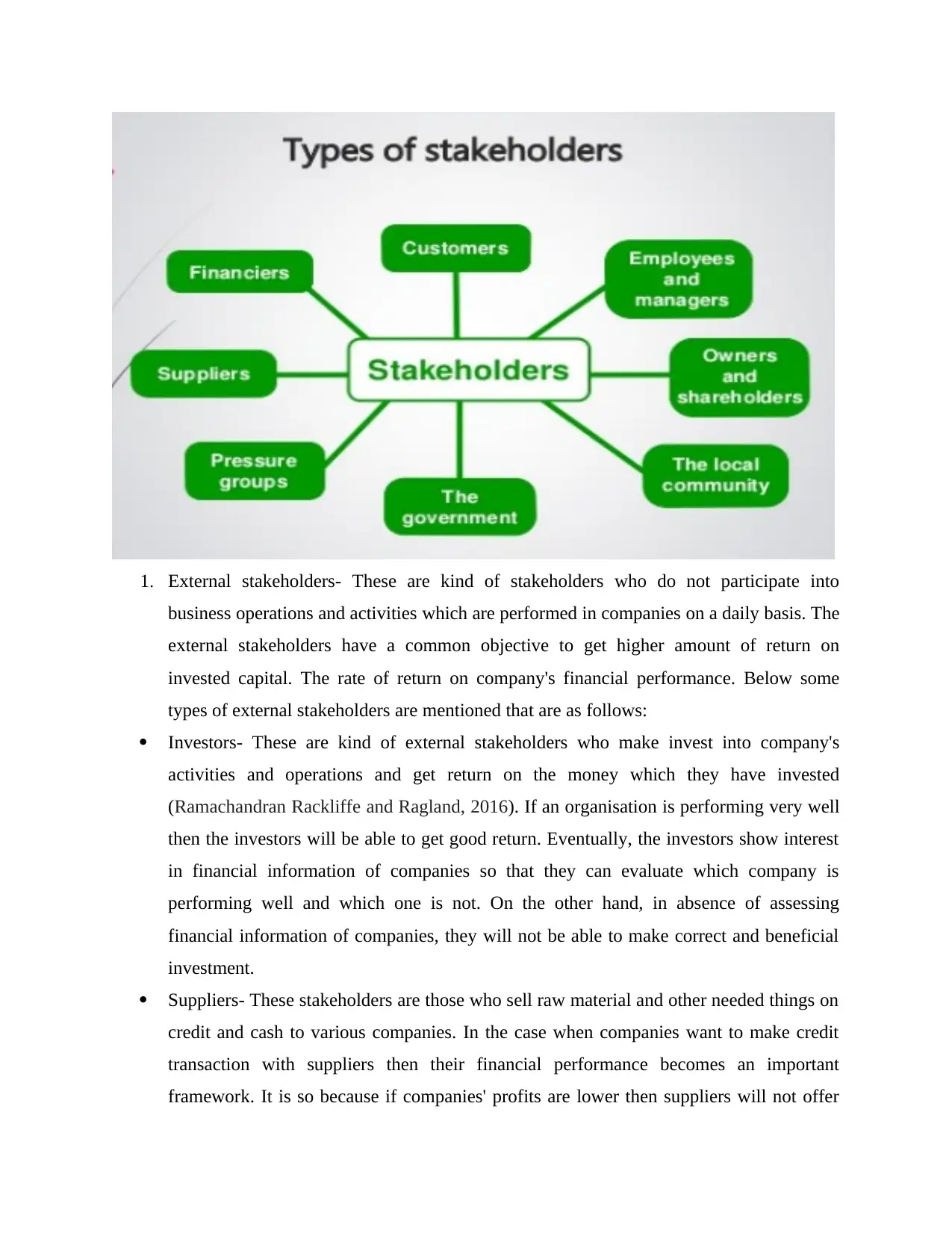

This report delves into the realm of financial accounting, emphasizing its crucial role in gathering and analyzing financial information to produce financial statements. The report explores the purpose of financial accounting, which includes presenting financial statements to stakeholders, summarizing financial events, recording financial transactions, estimating financial resources, and aiding in the decision-making process. The study uses the Broad head accountancy firm as a case study to illustrate these concepts. Furthermore, the report differentiates between internal and external stakeholders, defining stakeholders as those with an interest in a company's activities. Internal stakeholders, like managers and the board of directors, are actively involved in daily operations, while external stakeholders, such as investors, suppliers, government, and customers, assess financial performance for investment and other decisions. The report concludes that financial accounting is vital for companies, providing essential information for decision-making and stakeholder assessment. The financial statements are important for both internal and external users of the financial information.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.