Financial Accounting Report: Analysis of ANZ and Westpac Banks

VerifiedAdded on 2020/03/23

|20

|1321

|243

Report

AI Summary

This financial accounting report analyzes the annual reports of ANZ and Westpac banks, focusing on the effectiveness of communication and information disclosure. The report, written from an investor's perspective, evaluates areas for improvement in financial reporting, including segmental analysis, disclosure of credit and liquidity risks, and adherence to Basel regulations. It compares the two banks' practices, highlighting differences in segmental analysis and the presentation of Basel information. The report recommends improvements in line with IASB principles, emphasizing the need for entity-specific information, proper formatting, and the use of graphical representations to aid investor decision-making. The author suggests that effective communication is crucial for investors to make informed financial decisions and recommends that organizations incorporate forward-looking information and quantitative targets. The report concludes with specific recommendations for enhancing the clarity and usefulness of financial reports, advocating for a more standardized and investor-focused approach.

Running head: FINANCIAL ACCOUNTING

Financial accounting

Name of the University

Name of the student

Authors note

Financial accounting

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................6

Answer to Question 3:.....................................................................................................................8

Requirement i:.............................................................................................................................8

Requirement ii:..........................................................................................................................10

Requirement iii:.........................................................................................................................11

Answer to Question 4:...................................................................................................................14

Answer to Question 5:...................................................................................................................15

References:....................................................................................................................................18

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................6

Answer to Question 3:.....................................................................................................................8

Requirement i:.............................................................................................................................8

Requirement ii:..........................................................................................................................10

Requirement iii:.........................................................................................................................11

Answer to Question 4:...................................................................................................................14

Answer to Question 5:...................................................................................................................15

References:....................................................................................................................................18

2

FINANCIAL ACCOUNTING

Answer to Question 1:

To,

Chairperson

International standard accounting board

30 cannon street, London- EC4M 6XH, United Kingdom

Date: 15th September, 2017

Subject: Recommendation and guidance for improving the effectiveness of communication and

information in the financial report.

Sir,

As an investor, I intend to make some plan regarding the IASB proposition regarding the

effectiveness of information contained in the financial report. I have been considering

undertaking investments in two organizations listed on ASX that is Westpac and ANZ. With this

interest, I have compared and reviewed annual report of current year of both organizations.

While going through the report, I have discovered some areas that can be improved for better

presented and disclosure of relevant information. Preparation of financial report is regarded as

complex task by the preparers and sometimes it is considered by investors or users that

information’s have not been sufficiently depicted. There has been overall improvement in the

quality of corporate reporting, even though there exist opportunities for making further

improvement. Creation of good linkage of information in annual report goes beyond the

explanation of nature of linkage and highlighting the related disclosure location (Pacter, 2017).

FINANCIAL ACCOUNTING

Answer to Question 1:

To,

Chairperson

International standard accounting board

30 cannon street, London- EC4M 6XH, United Kingdom

Date: 15th September, 2017

Subject: Recommendation and guidance for improving the effectiveness of communication and

information in the financial report.

Sir,

As an investor, I intend to make some plan regarding the IASB proposition regarding the

effectiveness of information contained in the financial report. I have been considering

undertaking investments in two organizations listed on ASX that is Westpac and ANZ. With this

interest, I have compared and reviewed annual report of current year of both organizations.

While going through the report, I have discovered some areas that can be improved for better

presented and disclosure of relevant information. Preparation of financial report is regarded as

complex task by the preparers and sometimes it is considered by investors or users that

information’s have not been sufficiently depicted. There has been overall improvement in the

quality of corporate reporting, even though there exist opportunities for making further

improvement. Creation of good linkage of information in annual report goes beyond the

explanation of nature of linkage and highlighting the related disclosure location (Pacter, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

Poor presentation of financial data drowns the valuable information contained in the

annual report and that is sometimes not understood by investors. All this prevent investors and

make it difficult to take any feasible financial decisions. I have been able to ascertain the need

for making effective communication of information after going through the annual report of

ANZ bank and Westpac. However, there exist some differences in the presentation of

information of both the organization. It’s been disclosed that in terms of both preparing financial

report and information disclosure, there is a need for standardization. I have well acquainted

myself with the set of seven principles in section 2 of discussion paper that involves clear and

simple, entity specific, comparable, in an appropriate format, free from unnecessary duplication

and organized to highlight important matters (Luke, 2016). It has been ascertained after doing the

analysis of annual report for both the organizations that they comply with few principles and

lacks on most of parts.

Banks being financial institutions are required to make clear disclosure of credit and

liquidity risks and perform the segmental analysis for easing investors in taking investment

decisions. Renowned and reputed banks should disclose information in way that gives a clear

picture of their financial heath at glance that can only be obtained by adopting some

effectiveness principles that are lacking. There is no segmental analysis done by ANZ banks in

their annual report. On other hand, segmental analysis has been done by Westpac with

consistently defining segments. Segmental analysis has not been done by ANZ bank and there is

no separate analysis. Furthermore, for strengthening the banking industry regulation, Basel is

incorporated that is a inclusive set of reform measures. I have seen that there are separate

disclosures of requirements of Basel in the financial report. Credit risk and liquidity risks have

not been disclosed separately. However, little information regarding same was mentioned in the

FINANCIAL ACCOUNTING

Poor presentation of financial data drowns the valuable information contained in the

annual report and that is sometimes not understood by investors. All this prevent investors and

make it difficult to take any feasible financial decisions. I have been able to ascertain the need

for making effective communication of information after going through the annual report of

ANZ bank and Westpac. However, there exist some differences in the presentation of

information of both the organization. It’s been disclosed that in terms of both preparing financial

report and information disclosure, there is a need for standardization. I have well acquainted

myself with the set of seven principles in section 2 of discussion paper that involves clear and

simple, entity specific, comparable, in an appropriate format, free from unnecessary duplication

and organized to highlight important matters (Luke, 2016). It has been ascertained after doing the

analysis of annual report for both the organizations that they comply with few principles and

lacks on most of parts.

Banks being financial institutions are required to make clear disclosure of credit and

liquidity risks and perform the segmental analysis for easing investors in taking investment

decisions. Renowned and reputed banks should disclose information in way that gives a clear

picture of their financial heath at glance that can only be obtained by adopting some

effectiveness principles that are lacking. There is no segmental analysis done by ANZ banks in

their annual report. On other hand, segmental analysis has been done by Westpac with

consistently defining segments. Segmental analysis has not been done by ANZ bank and there is

no separate analysis. Furthermore, for strengthening the banking industry regulation, Basel is

incorporated that is a inclusive set of reform measures. I have seen that there are separate

disclosures of requirements of Basel in the financial report. Credit risk and liquidity risks have

not been disclosed separately. However, little information regarding same was mentioned in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

notes to financial statement. With respect to Westpac, there has been appropriate disclosure of

requirements and information about Basel and risk information of banking industry. However,

annual report of ANZ bank does not have any information regarding Tier I and tier II. Westpac

on other hand have made disclosure about Tiers. Divisional performance of Westpac has been

properly presented in their annual report compared to ANZ bank that did not disclose this

specific area.

Annual reports of organization should make use of graphical representation for

presenting their financial data that would ease investors in performance analysis. Using the

graphs would be appropriate in spite of using some narrative disclosure as sometimes such

information becomes redundant (Hussey & Ong, 2017). After conducting the analysis of annual

report and in lights of all facts regarding disclosure identified above, it is considered that

communication of information in annual report requires significant improvement. Some of the

principles of effective communications that IASB is required to put the most to work are capable

to making it comparable and entity specific.

For ensuring that communication is targeted, organizations sometimes consider investors

combination. Investors seek to identify value entity specific information and providing sufficient

and development of each segment, core product range is of particular helpful. Organizations

should incorporate forward looking information and quantitative targets for measuring the

performance against set strategic objectives. The principle of being entity specific and way the

information are presented should be incorporated by organization. Information presented in the

financial report is modified in accordance to entity circumstances rather than being general by

adopting the principle of entity specific. It would be suitable and preferred by investors to view

specific information as they can easily access general information about organization from

FINANCIAL ACCOUNTING

notes to financial statement. With respect to Westpac, there has been appropriate disclosure of

requirements and information about Basel and risk information of banking industry. However,

annual report of ANZ bank does not have any information regarding Tier I and tier II. Westpac

on other hand have made disclosure about Tiers. Divisional performance of Westpac has been

properly presented in their annual report compared to ANZ bank that did not disclose this

specific area.

Annual reports of organization should make use of graphical representation for

presenting their financial data that would ease investors in performance analysis. Using the

graphs would be appropriate in spite of using some narrative disclosure as sometimes such

information becomes redundant (Hussey & Ong, 2017). After conducting the analysis of annual

report and in lights of all facts regarding disclosure identified above, it is considered that

communication of information in annual report requires significant improvement. Some of the

principles of effective communications that IASB is required to put the most to work are capable

to making it comparable and entity specific.

For ensuring that communication is targeted, organizations sometimes consider investors

combination. Investors seek to identify value entity specific information and providing sufficient

and development of each segment, core product range is of particular helpful. Organizations

should incorporate forward looking information and quantitative targets for measuring the

performance against set strategic objectives. The principle of being entity specific and way the

information are presented should be incorporated by organization. Information presented in the

financial report is modified in accordance to entity circumstances rather than being general by

adopting the principle of entity specific. It would be suitable and preferred by investors to view

specific information as they can easily access general information about organization from

5

FINANCIAL ACCOUNTING

external source. Furthermore, presented financial information and other relevant information

should be able to make easy comparison between different reporting periods that should not

compromise the information usefulness in decision making.

Effectiveness of communication of information can be improved by using proper

formatting as perceived by many stakeholders (Burca et al., 2015). Various reports are published

by financial institutions regarding using tables and graphs for presentation of financial data.

However, uncertainty exists about using format and therefore, I would recommend to make

effective use of formatting for effective information communication. I think that investors would

have ease in making financial decision if they are able to compare data and analyze the trend of

financial performance over different periods. Format developments should rely and dependant on

entity specific factors. International Standards are required to develop in depth guidance on

usage of appropriate format.

I would recommend as an investor that some principles of making effective

communication should be incorporated by organizations. After the proper analysis of financial

report of both organizations, some of the most effective principle that should be incorporated are

entity specific and using proper formatting.

Yours sincerely,

ABC

FINANCIAL ACCOUNTING

external source. Furthermore, presented financial information and other relevant information

should be able to make easy comparison between different reporting periods that should not

compromise the information usefulness in decision making.

Effectiveness of communication of information can be improved by using proper

formatting as perceived by many stakeholders (Burca et al., 2015). Various reports are published

by financial institutions regarding using tables and graphs for presentation of financial data.

However, uncertainty exists about using format and therefore, I would recommend to make

effective use of formatting for effective information communication. I think that investors would

have ease in making financial decision if they are able to compare data and analyze the trend of

financial performance over different periods. Format developments should rely and dependant on

entity specific factors. International Standards are required to develop in depth guidance on

usage of appropriate format.

I would recommend as an investor that some principles of making effective

communication should be incorporated by organizations. After the proper analysis of financial

report of both organizations, some of the most effective principle that should be incorporated are

entity specific and using proper formatting.

Yours sincerely,

ABC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

Answer to Question 2:

Dr. Cr.

Date Amount Amount

31/03/2017 Bank A/c. Dr. $8,200,000

To.

Preference Share Application A/c. $1,600,000

To. Ordinary Share Application A/c. $6,600,000

15/4/2017

Preference Share Application

A/c. Dr. $1,600,000

To. Preference Share Capital A/c. $1,600,000

Ordinary Share Application

A/c. Dr. $6,600,000

To. Ordinary Share Capital A/c. $6,000,000

To. Ordinary Share Allotment A/c. $600,000

Ordinary Share Allotment A/c. Dr. $3,000,000

To. Ordinary Share Capital A/c. $3,000,000

In the books of Harriette Ltd.

Journal Entries

Particulars

(Being application money received for 2,000,000 ordinary shares

and 1,000,000 preference shares)

(Being application money received for pf. Shares transferred to Pf.

Share capital)

(Being application money received for ordinary share capital

transferred to ordinary share capital and excess amount adjusted

with due allotment)

(Being allotment money due on alloted shares)

15/5/2017 Bank A/c. Dr. $2,400,000

To. Ordinary Share Allotment A/c. $2,400,000

1/8/2017 Ordinary Share Call A/c. Dr. $1,000,000

To. Ordinary Share Capital A/c. $1,000,000

1/9/2017 Bank A/c. Dr. $975,000

Calls-in-Arrear A/c. Dr. $25,000

To. Ordinary Share Call A/c. $1,000,000

(Being due allotment money received)

(Being call money due on alloted shares)

(Being due call money received except for 50000 shares)

FINANCIAL ACCOUNTING

Answer to Question 2:

Dr. Cr.

Date Amount Amount

31/03/2017 Bank A/c. Dr. $8,200,000

To.

Preference Share Application A/c. $1,600,000

To. Ordinary Share Application A/c. $6,600,000

15/4/2017

Preference Share Application

A/c. Dr. $1,600,000

To. Preference Share Capital A/c. $1,600,000

Ordinary Share Application

A/c. Dr. $6,600,000

To. Ordinary Share Capital A/c. $6,000,000

To. Ordinary Share Allotment A/c. $600,000

Ordinary Share Allotment A/c. Dr. $3,000,000

To. Ordinary Share Capital A/c. $3,000,000

In the books of Harriette Ltd.

Journal Entries

Particulars

(Being application money received for 2,000,000 ordinary shares

and 1,000,000 preference shares)

(Being application money received for pf. Shares transferred to Pf.

Share capital)

(Being application money received for ordinary share capital

transferred to ordinary share capital and excess amount adjusted

with due allotment)

(Being allotment money due on alloted shares)

15/5/2017 Bank A/c. Dr. $2,400,000

To. Ordinary Share Allotment A/c. $2,400,000

1/8/2017 Ordinary Share Call A/c. Dr. $1,000,000

To. Ordinary Share Capital A/c. $1,000,000

1/9/2017 Bank A/c. Dr. $975,000

Calls-in-Arrear A/c. Dr. $25,000

To. Ordinary Share Call A/c. $1,000,000

(Being due allotment money received)

(Being call money due on alloted shares)

(Being due call money received except for 50000 shares)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

15/9/2017 Ordinary Share Capital A/c. Dr. $250,000

To. Calls-in-Arrear A/c. $25,000

To. Ordinary Share Forfeiture A/c. $225,000

Bank A/c. Dr. $210,000

Ordinary Share Forfeiture A/c. Dr. $40,000

To. Ordinary Share Capital A/c. $250,000

Cost of Forfeiture & Reissue

A/c. Dr. $7,500

To. Bank A/c. $7,500

Ordinary Share Forfeiture A/c. Dr. $185,000

To.

Cost of Forfeiture & Reissue A/c. $7,500

To. Capital Reserve A/c. $177,500

(Being the balance of share forfeiture a/c. after adjusting with cost

of forfeiture and reissue transferred to capital reserve)

(Being the 50000 shares, for which call money is due, forfeited

accordingly)

(Being the forfeited shares reissued for $4.20 per shares)

(Being cost of forfeiture and reissue of shares paid)

Workings:

Particulars Nos. Of Shares Value per Share Amount

Pf. Share Application Received A 800000 $2 $1,600,000

Ordinary Share Application Received B 2200000 $3 $6,600,000

Ordinary Share Application Alloted C 2000000 $3 $6,000,000

Ordinary Share Application Adjsuted D=B-C 200000 $3 $600,000

Ordinary Share Allotment Due E 2000000 $1.50 $3,000,000

Ordinary Share Allotment Received F=E-D 1800000 $2,400,000

Ordinary Share Call Due G 2000000 $0.50 $1,000,000

Ordinary Share Call Received H 1950000 $0.50 $975,000

FINANCIAL ACCOUNTING

15/9/2017 Ordinary Share Capital A/c. Dr. $250,000

To. Calls-in-Arrear A/c. $25,000

To. Ordinary Share Forfeiture A/c. $225,000

Bank A/c. Dr. $210,000

Ordinary Share Forfeiture A/c. Dr. $40,000

To. Ordinary Share Capital A/c. $250,000

Cost of Forfeiture & Reissue

A/c. Dr. $7,500

To. Bank A/c. $7,500

Ordinary Share Forfeiture A/c. Dr. $185,000

To.

Cost of Forfeiture & Reissue A/c. $7,500

To. Capital Reserve A/c. $177,500

(Being the balance of share forfeiture a/c. after adjusting with cost

of forfeiture and reissue transferred to capital reserve)

(Being the 50000 shares, for which call money is due, forfeited

accordingly)

(Being the forfeited shares reissued for $4.20 per shares)

(Being cost of forfeiture and reissue of shares paid)

Workings:

Particulars Nos. Of Shares Value per Share Amount

Pf. Share Application Received A 800000 $2 $1,600,000

Ordinary Share Application Received B 2200000 $3 $6,600,000

Ordinary Share Application Alloted C 2000000 $3 $6,000,000

Ordinary Share Application Adjsuted D=B-C 200000 $3 $600,000

Ordinary Share Allotment Due E 2000000 $1.50 $3,000,000

Ordinary Share Allotment Received F=E-D 1800000 $2,400,000

Ordinary Share Call Due G 2000000 $0.50 $1,000,000

Ordinary Share Call Received H 1950000 $0.50 $975,000

8

FINANCIAL ACCOUNTING

Calls-in-Arrear I 50000 $0.50 $25,000

Share Capital Forfeited J 50000 $5 $250,000

Share Forfeiture K=I-J 50000 $225,000

Share Capital received fro Reissue L 50000 $4.20 $210,000

Share forfeiture adusted with reissue M=J-L 50000 $40,000

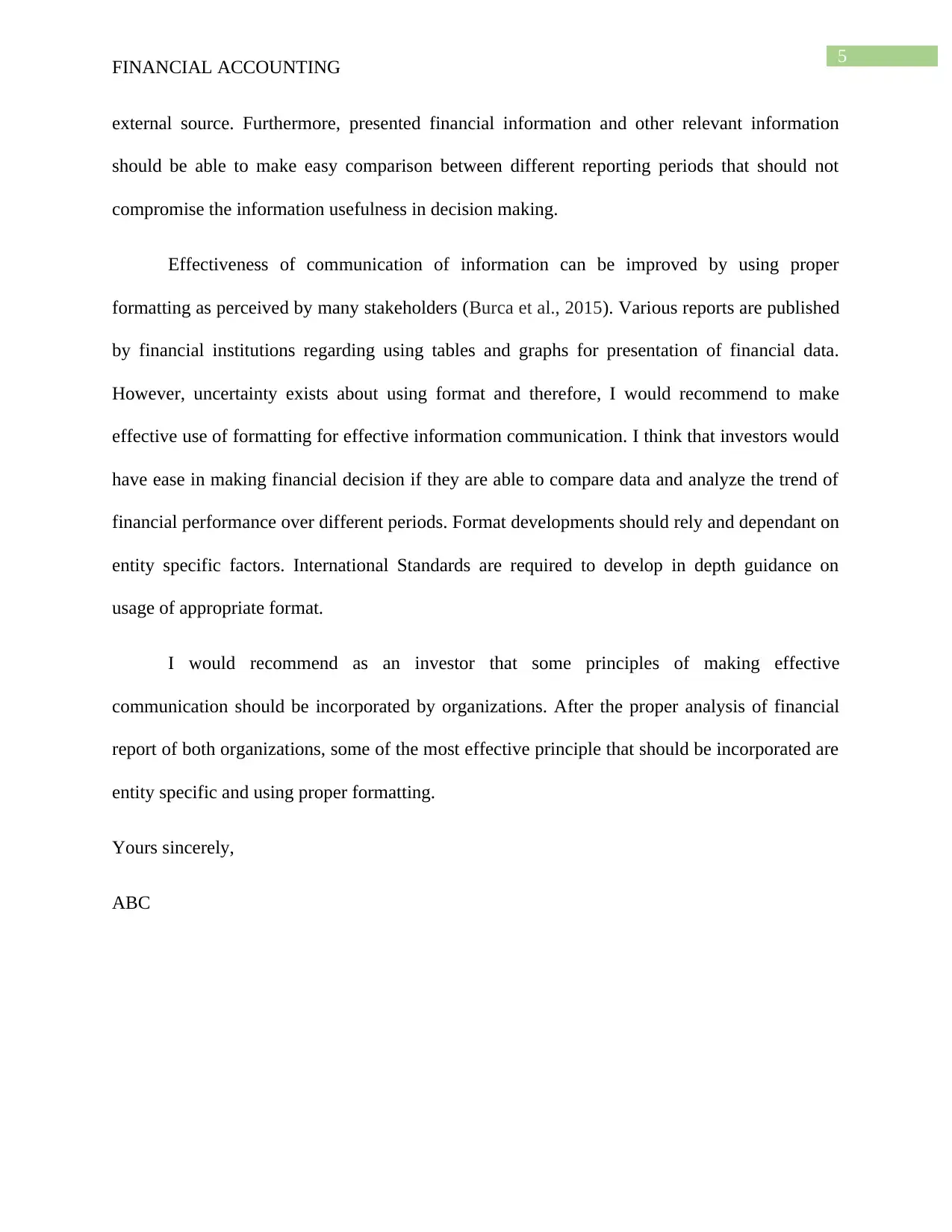

Answer to Question 3:

Requirement i:

Particulars Amount Amount

Accounting profit before tax $66,000

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$206,000

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income $80,000

Tax on taxable income @30% $24,000

Less: 30% Tax paid on Sales Revenue $205,800

Income Tax Refundable ($181,800)

Worksheet for Curret Tax Liability/(Refundable):

FINANCIAL ACCOUNTING

Calls-in-Arrear I 50000 $0.50 $25,000

Share Capital Forfeited J 50000 $5 $250,000

Share Forfeiture K=I-J 50000 $225,000

Share Capital received fro Reissue L 50000 $4.20 $210,000

Share forfeiture adusted with reissue M=J-L 50000 $40,000

Answer to Question 3:

Requirement i:

Particulars Amount Amount

Accounting profit before tax $66,000

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$206,000

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income $80,000

Tax on taxable income @30% $24,000

Less: 30% Tax paid on Sales Revenue $205,800

Income Tax Refundable ($181,800)

Worksheet for Curret Tax Liability/(Refundable):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

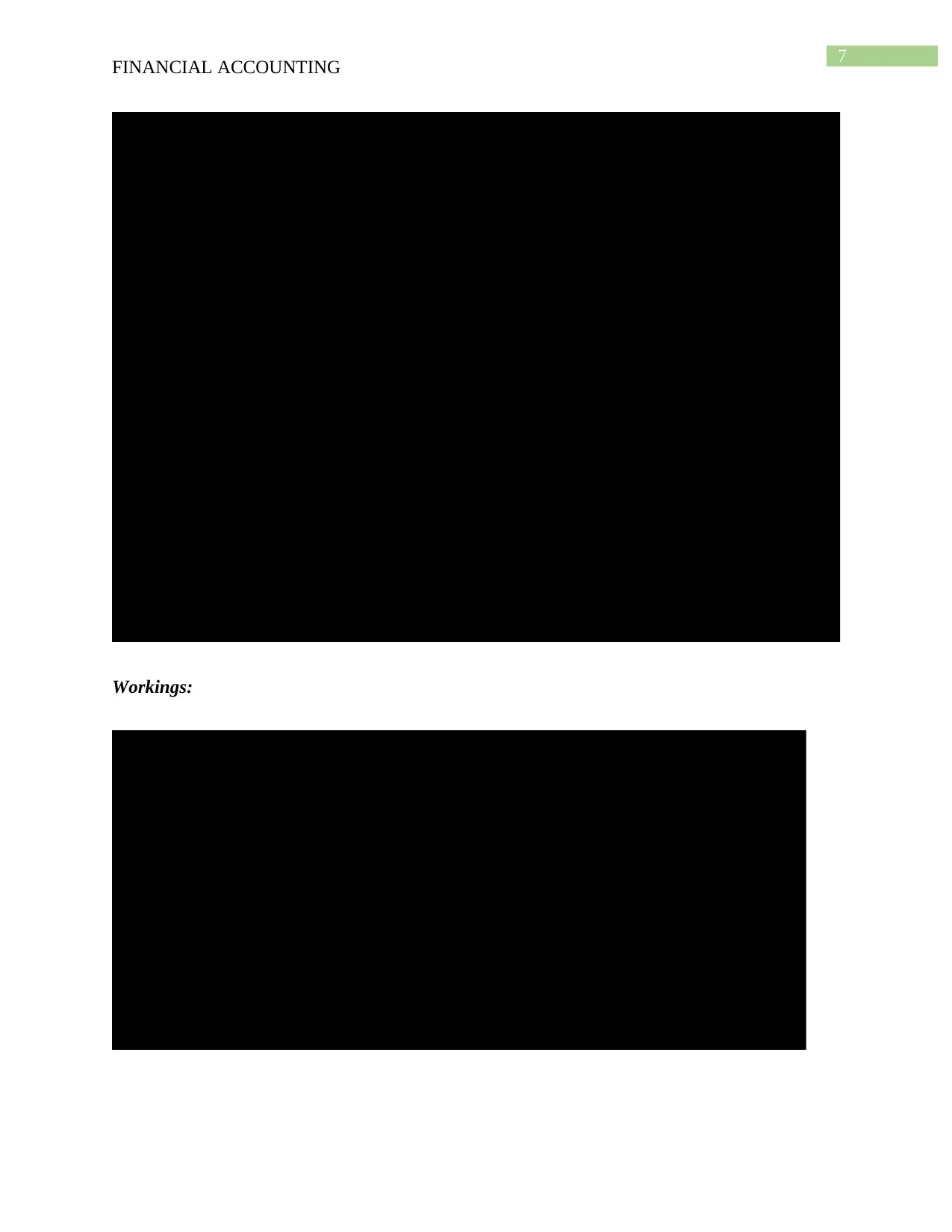

FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $10,000 $10,000

Trade Receivables $125,000 $125,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

Inventories $60,000 $60,000

Prepaid Insurance $10,000 $10,000

Goodwill $20,000 $20,000

Equipment $300,000 $300,000

Accumulated Depreciation ($60,000) ($50,000) $10,000

Liabilities

Trade Payables $35,000 $35,000

Provision for Warranties $10,000 $10,000

Provision for Annual Leave $20,000 $20,000

Loan Payable $90,000 $90,000

Total Temporary differences $10,000 $44,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $13,200

Deferred Tax Worksheet:

FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $10,000 $10,000

Trade Receivables $125,000 $125,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

Inventories $60,000 $60,000

Prepaid Insurance $10,000 $10,000

Goodwill $20,000 $20,000

Equipment $300,000 $300,000

Accumulated Depreciation ($60,000) ($50,000) $10,000

Liabilities

Trade Payables $35,000 $35,000

Provision for Warranties $10,000 $10,000

Provision for Annual Leave $20,000 $20,000

Loan Payable $90,000 $90,000

Total Temporary differences $10,000 $44,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $13,200

Deferred Tax Worksheet:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

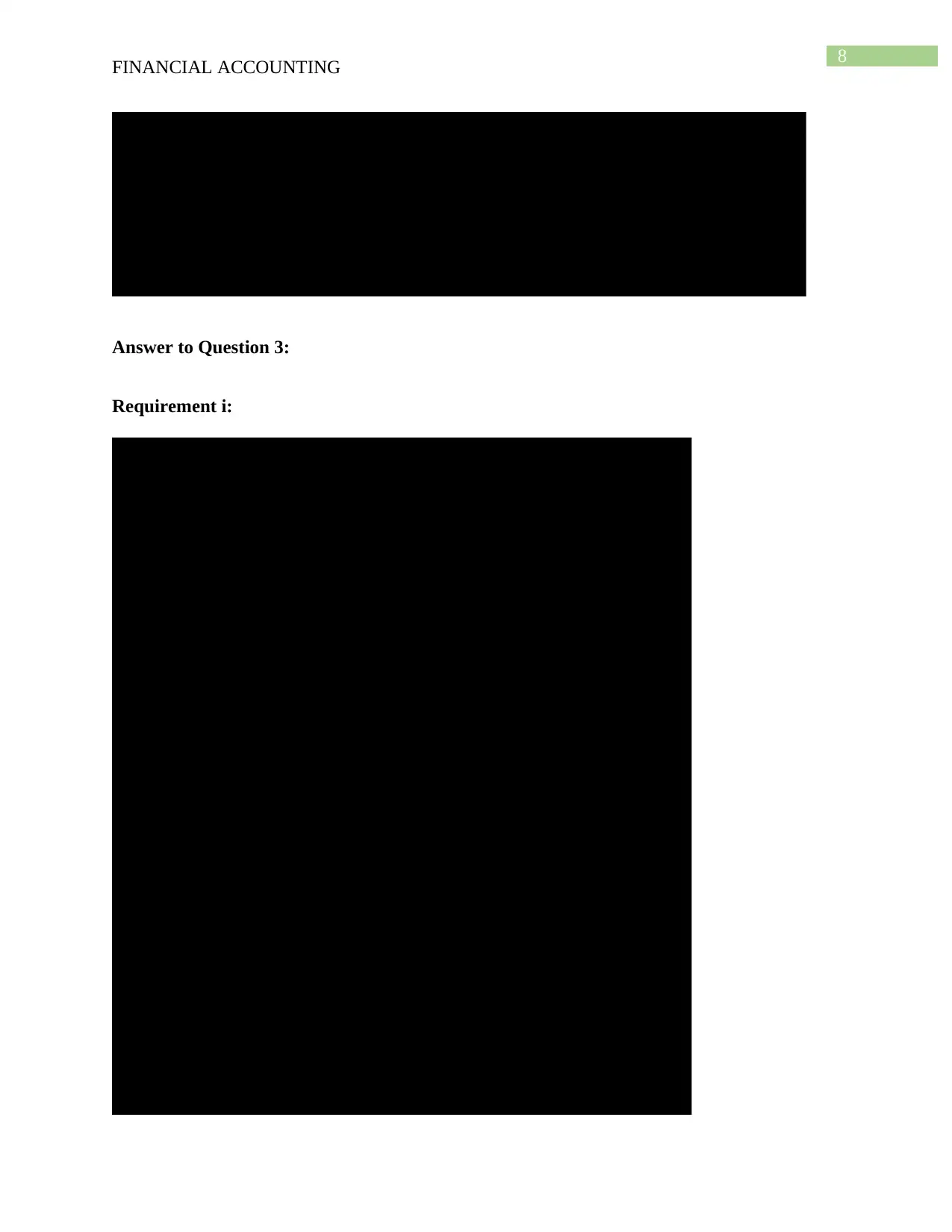

FINANCIAL ACCOUNTING

Requirement ii:

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $24,000

Income Tax Refundable A/c. Dr. $181,800

To, Advance Tax Paid A/c. $205,800

$13,200

Deferred Tax Assets A/c. Dr. $3,000

To, Deferred Tax Liability A/c. $10,200

To, Income Tax Expense A/c.

Profit & loss A/c. $21,000

To, Income Tax Expense A/c. $21,000

(Being deferred tax assets and deferred tax liabilities

recorded)

Particulars

(Being Income tax expenses adjusterd with advance tax paid

and income tax refundable recorded)

(Being income tax expense transferred to P/L A/c.)

FINANCIAL ACCOUNTING

Requirement ii:

Dr. Cr.

Date Amount Amount

30/06/2017 Income Tax Expense A/c. Dr. $24,000

Income Tax Refundable A/c. Dr. $181,800

To, Advance Tax Paid A/c. $205,800

$13,200

Deferred Tax Assets A/c. Dr. $3,000

To, Deferred Tax Liability A/c. $10,200

To, Income Tax Expense A/c.

Profit & loss A/c. $21,000

To, Income Tax Expense A/c. $21,000

(Being deferred tax assets and deferred tax liabilities

recorded)

Particulars

(Being Income tax expenses adjusterd with advance tax paid

and income tax refundable recorded)

(Being income tax expense transferred to P/L A/c.)

11

FINANCIAL ACCOUNTING

Requirement iii:

Particulars Amount Amount

Accounting profit before tax ($44,000)

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$96,000

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income ($30,000)

Tax on taxable income @30% $0

Less: 30% Tax paid on Sales Revenue $172,800

Income Tax Refundable ($172,800)

Worksheet for Curret Tax Liability/(Refundable):

FINANCIAL ACCOUNTING

Requirement iii:

Particulars Amount Amount

Accounting profit before tax ($44,000)

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$96,000

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income ($30,000)

Tax on taxable income @30% $0

Less: 30% Tax paid on Sales Revenue $172,800

Income Tax Refundable ($172,800)

Worksheet for Curret Tax Liability/(Refundable):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.