Financial Accounting Report: Ratio Analysis, Giorgio Plc Statements

VerifiedAdded on 2023/06/07

|12

|2108

|358

Report

AI Summary

This financial accounting report provides a comprehensive analysis of financial performance and position. It includes a ratio analysis of ASOS Plc, evaluating profitability, working capital, liquidity, and long-term financing through metrics like return on capital employed, net profit margin, asset turnover, inventory days, accounts receivable/payable days, and current/acid-test ratios. The report also features the preparation of financial statements for Giorgio Plc, including an income statement, statement of changes in equity, and statement of financial position. Furthermore, it includes a cash budget and profit budget for Grazyna Ltd, offering insights into cash flow management and projected financial performance. This detailed analysis is essential for understanding the financial health and operational efficiency of the companies involved.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Section A .........................................................................................................................................3

Question – 1 ....................................................................................................................................3

Ratio analysis .............................................................................................................................3

Part B ..............................................................................................................................................7

Question B1: ...................................................................................................................................7

1) Income statement of Giorgio Plc ...........................................................................................7

2) Statement of changes in equity: .............................................................................................7

3) Statement of Financial position: ............................................................................................8

Question B2: ...............................................................................................................................9

1) Grazyna Ltd cash budget .......................................................................................................9

2. Grazyna Ltd profit budget.....................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Section A .........................................................................................................................................3

Question – 1 ....................................................................................................................................3

Ratio analysis .............................................................................................................................3

Part B ..............................................................................................................................................7

Question B1: ...................................................................................................................................7

1) Income statement of Giorgio Plc ...........................................................................................7

2) Statement of changes in equity: .............................................................................................7

3) Statement of Financial position: ............................................................................................8

Question B2: ...............................................................................................................................9

1) Grazyna Ltd cash budget .......................................................................................................9

2. Grazyna Ltd profit budget.....................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial accounting refers to the process of presenting the financial reports to the

internal or external users. It is utilized in big company for measuring the monetary performance.

It aids to evaluate the difficulties that is faced by the businesses enterprises. This report is about

the ASOS Plc company to measure the financial position. The ASOS Plc company is an retail

organisation which indulge such as investment related business. It is a multinational fashion and

beauty retailer. It was established in the year 2000 in UK (Allen, Aselta, and Engel, 2019) . It

has several branches in many countries and includes 850 brands deals in garments and

accessories. In the first section company has done deep study on the accounting ratios and their

impact on the organisation. Further, company has made the financial statements from the trial

balance of the organisation.

MAIN BODY

Section A

Question – 1

Ratio analysis

Profitability ratio

1. Return on capital employed: This ratio show that how organisation is able to generate its

revenue by using the capital efficiently. It denotes how organisation is managing its profit from

the mixture of the debt and equity

In 2020 Return on capital employed= Profit before interest and tax / capital employed *100

= 151/1621*100

= 9.31%

In 2021 = 190/2068*100

= 9.18%

Comments: From the analysis it is determined that the return on capital employed in 2020 is

9.31% which is more as compared to the year 2021. It means in the present year company is

getting less returns from the investment. It means company debts is much higher as compared to

owners equity(Astuty, and Pasaribu, 2021).

Financial accounting refers to the process of presenting the financial reports to the

internal or external users. It is utilized in big company for measuring the monetary performance.

It aids to evaluate the difficulties that is faced by the businesses enterprises. This report is about

the ASOS Plc company to measure the financial position. The ASOS Plc company is an retail

organisation which indulge such as investment related business. It is a multinational fashion and

beauty retailer. It was established in the year 2000 in UK (Allen, Aselta, and Engel, 2019) . It

has several branches in many countries and includes 850 brands deals in garments and

accessories. In the first section company has done deep study on the accounting ratios and their

impact on the organisation. Further, company has made the financial statements from the trial

balance of the organisation.

MAIN BODY

Section A

Question – 1

Ratio analysis

Profitability ratio

1. Return on capital employed: This ratio show that how organisation is able to generate its

revenue by using the capital efficiently. It denotes how organisation is managing its profit from

the mixture of the debt and equity

In 2020 Return on capital employed= Profit before interest and tax / capital employed *100

= 151/1621*100

= 9.31%

In 2021 = 190/2068*100

= 9.18%

Comments: From the analysis it is determined that the return on capital employed in 2020 is

9.31% which is more as compared to the year 2021. It means in the present year company is

getting less returns from the investment. It means company debts is much higher as compared to

owners equity(Astuty, and Pasaribu, 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Net profit margin: It identifies the relationship between the sales and the net profit of the

organisation. It indicates the how much revenue can be earned from the sales.

In 2020 Net profit ratio= Net profit/ sales

= 151/3264*100

= 4.62%

In 2021 = 190/3911*100

= 4.85%

Comments: The net profit ratio in 2021 is 4.85 % and it is quite higher than the net profit ratio

of 2020. It shows the company has generate more sales which increases the profit of the

company and minimize the direct or indirect expenses (Banker, Huang, and Zhao, 2021)

(,Bertuzi, and Silva, 2020). Higher the net profit ratio is good for the organisation it indicates the

ability of the company to improve the cost efficiency of the product.

3. Asset turnover ratio: It is the accounting relativity between the total assets of the enterprise

and the sales of the organisation.

In 2020 Asset turnover ratio = Total assets / sales *100

= 1990/3264

= 60.96%

In 2021 = 2885/3911*100

= 73.76 %

Comments : The assets turnover ratio of the organisation in 2021 is 73.6 % and it is 10% higher

from the ratio in 2020. It shows that organisation has employed the assets to earn the profit. In

this the ratio has increased it indicates that organisation is utilizing the assets more effectively to

produce the income(.Cagle, 2020). If the company has high ratio it means organisation is

performing better as against with the lower assets turnover ratio. This information is used by the

external users or investors for getting the idea about the assets.

Working capital ratio

1. Inventory days: In 2021 = Average inventory * 365 / cost of goods sold

= 699.5*365/2134

= 115 days

organisation. It indicates the how much revenue can be earned from the sales.

In 2020 Net profit ratio= Net profit/ sales

= 151/3264*100

= 4.62%

In 2021 = 190/3911*100

= 4.85%

Comments: The net profit ratio in 2021 is 4.85 % and it is quite higher than the net profit ratio

of 2020. It shows the company has generate more sales which increases the profit of the

company and minimize the direct or indirect expenses (Banker, Huang, and Zhao, 2021)

(,Bertuzi, and Silva, 2020). Higher the net profit ratio is good for the organisation it indicates the

ability of the company to improve the cost efficiency of the product.

3. Asset turnover ratio: It is the accounting relativity between the total assets of the enterprise

and the sales of the organisation.

In 2020 Asset turnover ratio = Total assets / sales *100

= 1990/3264

= 60.96%

In 2021 = 2885/3911*100

= 73.76 %

Comments : The assets turnover ratio of the organisation in 2021 is 73.6 % and it is 10% higher

from the ratio in 2020. It shows that organisation has employed the assets to earn the profit. In

this the ratio has increased it indicates that organisation is utilizing the assets more effectively to

produce the income(.Cagle, 2020). If the company has high ratio it means organisation is

performing better as against with the lower assets turnover ratio. This information is used by the

external users or investors for getting the idea about the assets.

Working capital ratio

1. Inventory days: In 2021 = Average inventory * 365 / cost of goods sold

= 699.5*365/2134

= 115 days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

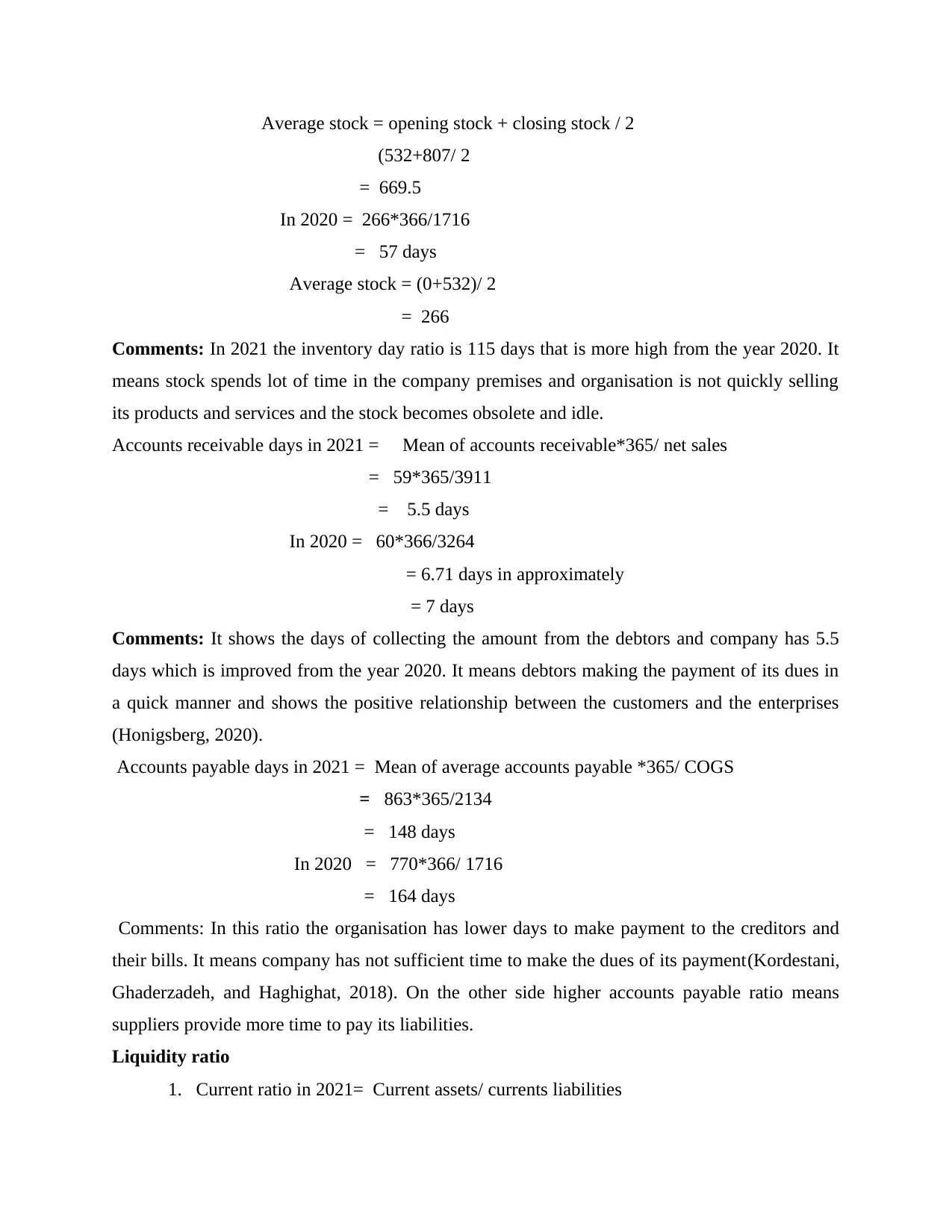

Average stock = opening stock + closing stock / 2

(532+807/ 2

= 669.5

In 2020 = 266*366/1716

= 57 days

Average stock = (0+532)/ 2

= 266

Comments: In 2021 the inventory day ratio is 115 days that is more high from the year 2020. It

means stock spends lot of time in the company premises and organisation is not quickly selling

its products and services and the stock becomes obsolete and idle.

Accounts receivable days in 2021 = Mean of accounts receivable*365/ net sales

= 59*365/3911

= 5.5 days

In 2020 = 60*366/3264

= 6.71 days in approximately

= 7 days

Comments: It shows the days of collecting the amount from the debtors and company has 5.5

days which is improved from the year 2020. It means debtors making the payment of its dues in

a quick manner and shows the positive relationship between the customers and the enterprises

(Honigsberg, 2020).

Accounts payable days in 2021 = Mean of average accounts payable *365/ COGS

= 863*365/2134

= 148 days

In 2020 = 770*366/ 1716

= 164 days

Comments: In this ratio the organisation has lower days to make payment to the creditors and

their bills. It means company has not sufficient time to make the dues of its payment(Kordestani,

Ghaderzadeh, and Haghighat, 2018). On the other side higher accounts payable ratio means

suppliers provide more time to pay its liabilities.

Liquidity ratio

1. Current ratio in 2021= Current assets/ currents liabilities

(532+807/ 2

= 669.5

In 2020 = 266*366/1716

= 57 days

Average stock = (0+532)/ 2

= 266

Comments: In 2021 the inventory day ratio is 115 days that is more high from the year 2020. It

means stock spends lot of time in the company premises and organisation is not quickly selling

its products and services and the stock becomes obsolete and idle.

Accounts receivable days in 2021 = Mean of accounts receivable*365/ net sales

= 59*365/3911

= 5.5 days

In 2020 = 60*366/3264

= 6.71 days in approximately

= 7 days

Comments: It shows the days of collecting the amount from the debtors and company has 5.5

days which is improved from the year 2020. It means debtors making the payment of its dues in

a quick manner and shows the positive relationship between the customers and the enterprises

(Honigsberg, 2020).

Accounts payable days in 2021 = Mean of average accounts payable *365/ COGS

= 863*365/2134

= 148 days

In 2020 = 770*366/ 1716

= 164 days

Comments: In this ratio the organisation has lower days to make payment to the creditors and

their bills. It means company has not sufficient time to make the dues of its payment(Kordestani,

Ghaderzadeh, and Haghighat, 2018). On the other side higher accounts payable ratio means

suppliers provide more time to pay its liabilities.

Liquidity ratio

1. Current ratio in 2021= Current assets/ currents liabilities

= 1560/998

= 1.56

In 2020 = 1020 / 818

= 1.24

Comments : In the recent year the current ratio is 1.56 times which has increased as compared

to previous year. It means company has more current assets to meet out its short term

obligations. It indicates the position of the company to pay its short term liabilities from the

current assets. The perfect current ratio is 2:1 if it is more from the 2 than it will not be the good

sign for the company (Mălăescu, and Avram, 2018).

2. Acid test ratio in 2021 = Quick assets / current liabilities

Quick assets = Current assets – inventory – Prepaid expenses

= (1560-807) / 998

= 0.75

In 2020 = (1020-532) / 818

= 0.60

Comments: The company has 0.75 quick ratio in 2021 which is little bit higher as compared to

the 2020. It denotes company does not have enough assets to meet its liquidity. The best quick

ratio is 1:1 (Naranjo, Ripoll Feliu, 2021).

Long term financing

Gearing ratio in 2021 = Equity / debt

= 1034 / 1034

= 1 times

In 2020 = 810 / 810

= 1 times

Comments: In this it has same gearing ratio for both the years it company has equal debts and

liabilities which shows the good position of the business (Mutha, Bansal, and Guide, 2021). It is

related with the liquidity of the business. It concentrates the long term monetary stability of the

company. It analyses the potion of the assets which is funded by the long term sources of the

business.

= 1.56

In 2020 = 1020 / 818

= 1.24

Comments : In the recent year the current ratio is 1.56 times which has increased as compared

to previous year. It means company has more current assets to meet out its short term

obligations. It indicates the position of the company to pay its short term liabilities from the

current assets. The perfect current ratio is 2:1 if it is more from the 2 than it will not be the good

sign for the company (Mălăescu, and Avram, 2018).

2. Acid test ratio in 2021 = Quick assets / current liabilities

Quick assets = Current assets – inventory – Prepaid expenses

= (1560-807) / 998

= 0.75

In 2020 = (1020-532) / 818

= 0.60

Comments: The company has 0.75 quick ratio in 2021 which is little bit higher as compared to

the 2020. It denotes company does not have enough assets to meet its liquidity. The best quick

ratio is 1:1 (Naranjo, Ripoll Feliu, 2021).

Long term financing

Gearing ratio in 2021 = Equity / debt

= 1034 / 1034

= 1 times

In 2020 = 810 / 810

= 1 times

Comments: In this it has same gearing ratio for both the years it company has equal debts and

liabilities which shows the good position of the business (Mutha, Bansal, and Guide, 2021). It is

related with the liquidity of the business. It concentrates the long term monetary stability of the

company. It analyses the potion of the assets which is funded by the long term sources of the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part B

Question B1:

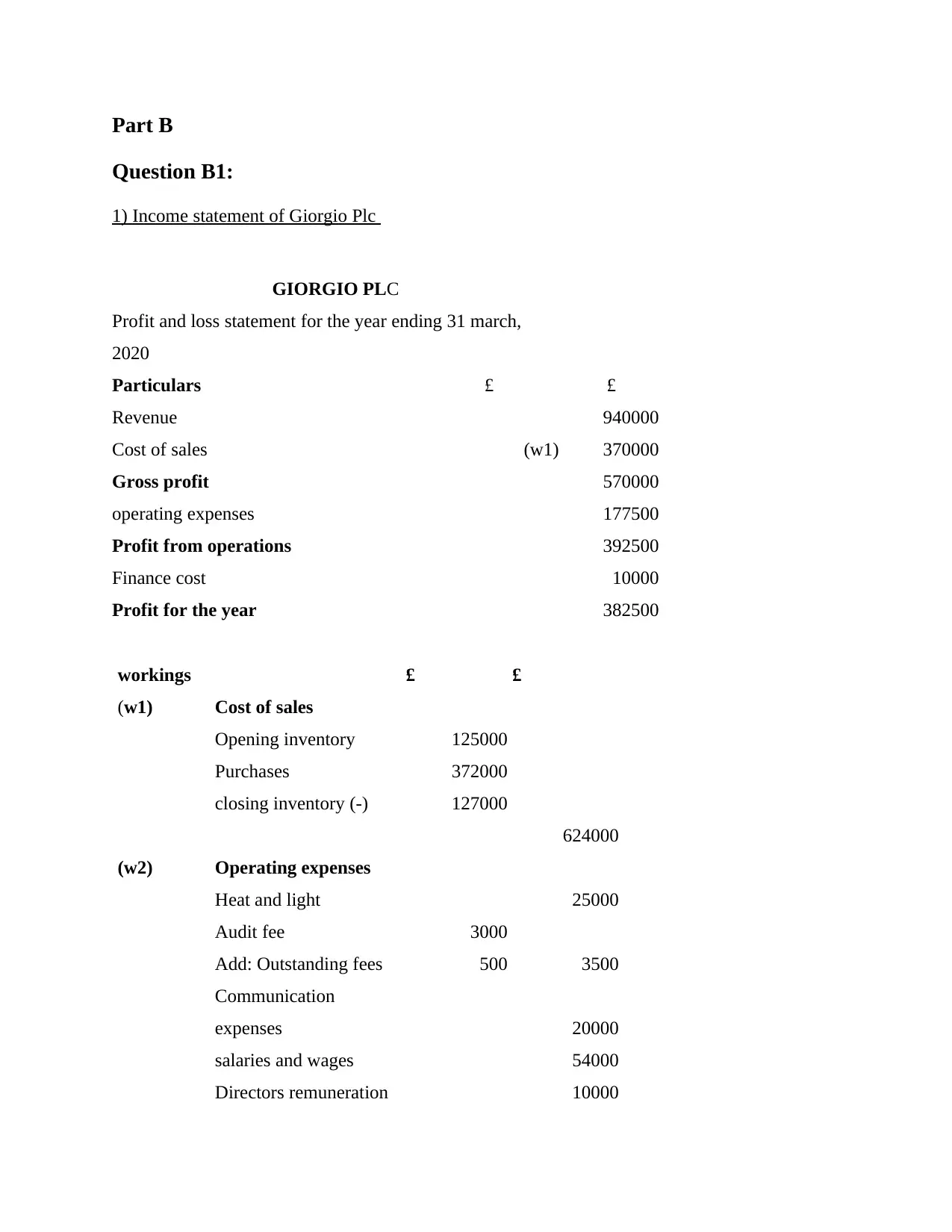

1) Income statement of Giorgio Plc

GIORGIO PLC

Profit and loss statement for the year ending 31 march,

2020

Particulars £ £

Revenue 940000

Cost of sales (w1) 370000

Gross profit 570000

operating expenses 177500

Profit from operations 392500

Finance cost 10000

Profit for the year 382500

workings £ £

(w1) Cost of sales

Opening inventory 125000

Purchases 372000

closing inventory (-) 127000

624000

(w2) Operating expenses

Heat and light 25000

Audit fee 3000

Add: Outstanding fees 500 3500

Communication

expenses 20000

salaries and wages 54000

Directors remuneration 10000

Question B1:

1) Income statement of Giorgio Plc

GIORGIO PLC

Profit and loss statement for the year ending 31 march,

2020

Particulars £ £

Revenue 940000

Cost of sales (w1) 370000

Gross profit 570000

operating expenses 177500

Profit from operations 392500

Finance cost 10000

Profit for the year 382500

workings £ £

(w1) Cost of sales

Opening inventory 125000

Purchases 372000

closing inventory (-) 127000

624000

(w2) Operating expenses

Heat and light 25000

Audit fee 3000

Add: Outstanding fees 500 3500

Communication

expenses 20000

salaries and wages 54000

Directors remuneration 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

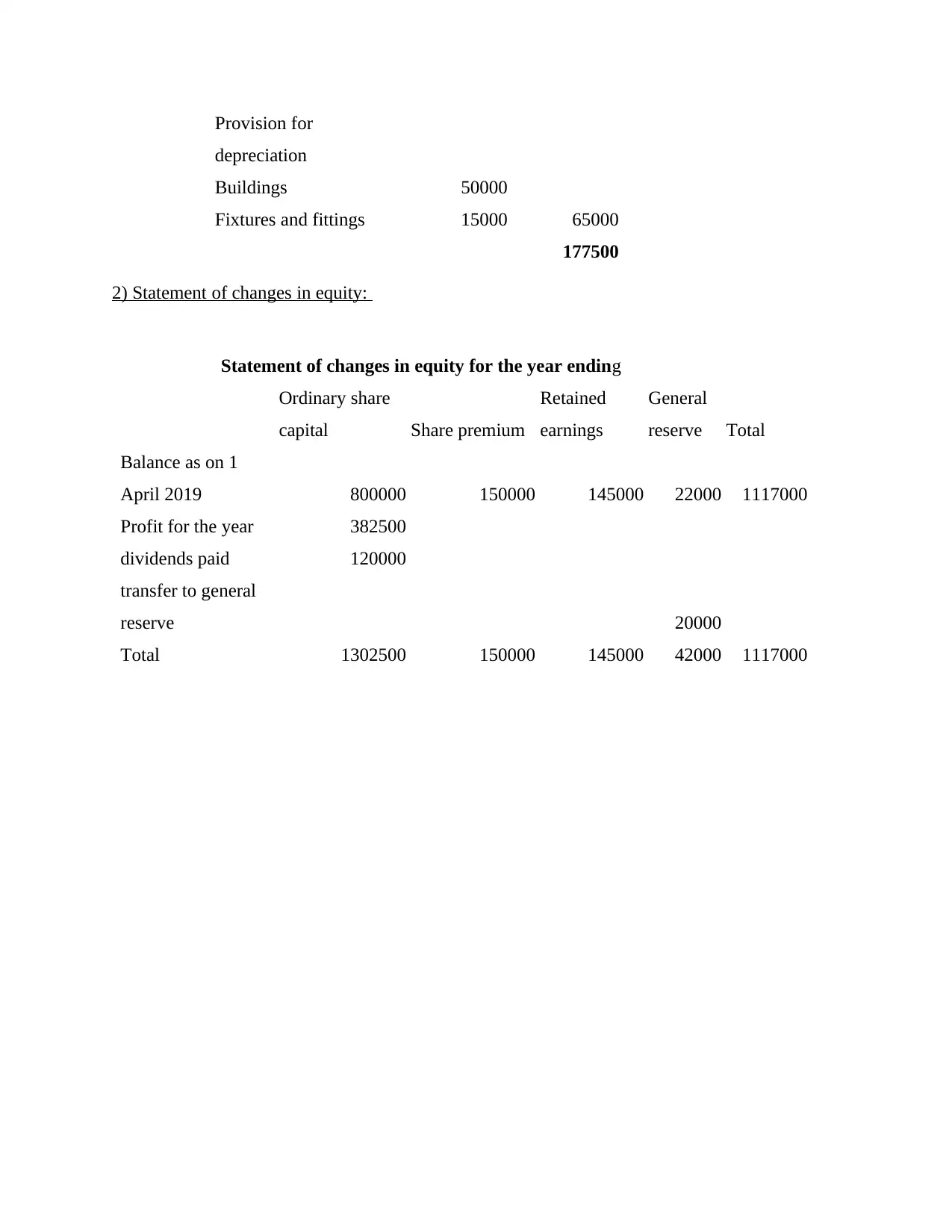

Provision for

depreciation

Buildings 50000

Fixtures and fittings 15000 65000

177500

2) Statement of changes in equity:

Statement of changes in equity for the year ending

Ordinary share

capital Share premium

Retained

earnings

General

reserve Total

Balance as on 1

April 2019 800000 150000 145000 22000 1117000

Profit for the year 382500

dividends paid 120000

transfer to general

reserve 20000

Total 1302500 150000 145000 42000 1117000

depreciation

Buildings 50000

Fixtures and fittings 15000 65000

177500

2) Statement of changes in equity:

Statement of changes in equity for the year ending

Ordinary share

capital Share premium

Retained

earnings

General

reserve Total

Balance as on 1

April 2019 800000 150000 145000 22000 1117000

Profit for the year 382500

dividends paid 120000

transfer to general

reserve 20000

Total 1302500 150000 145000 42000 1117000

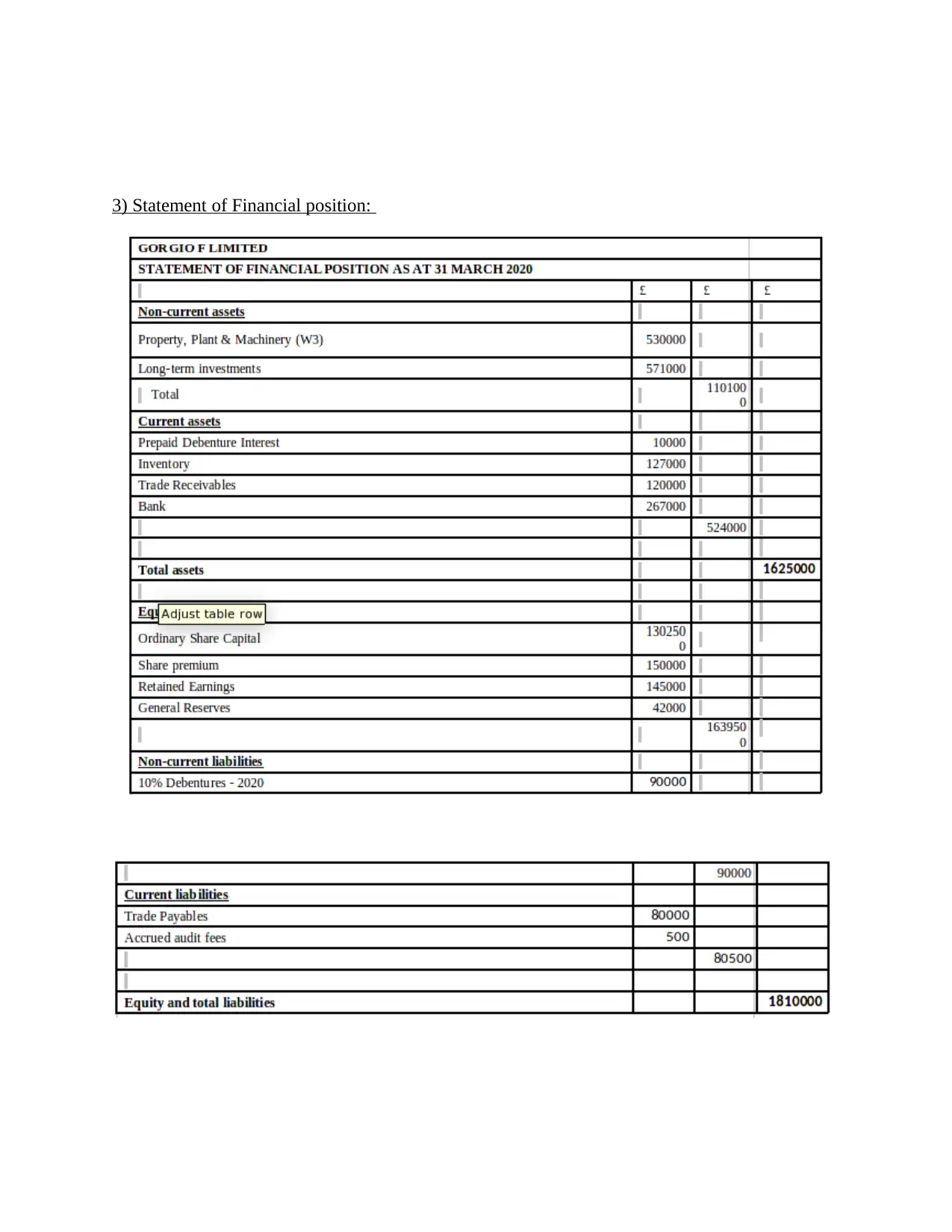

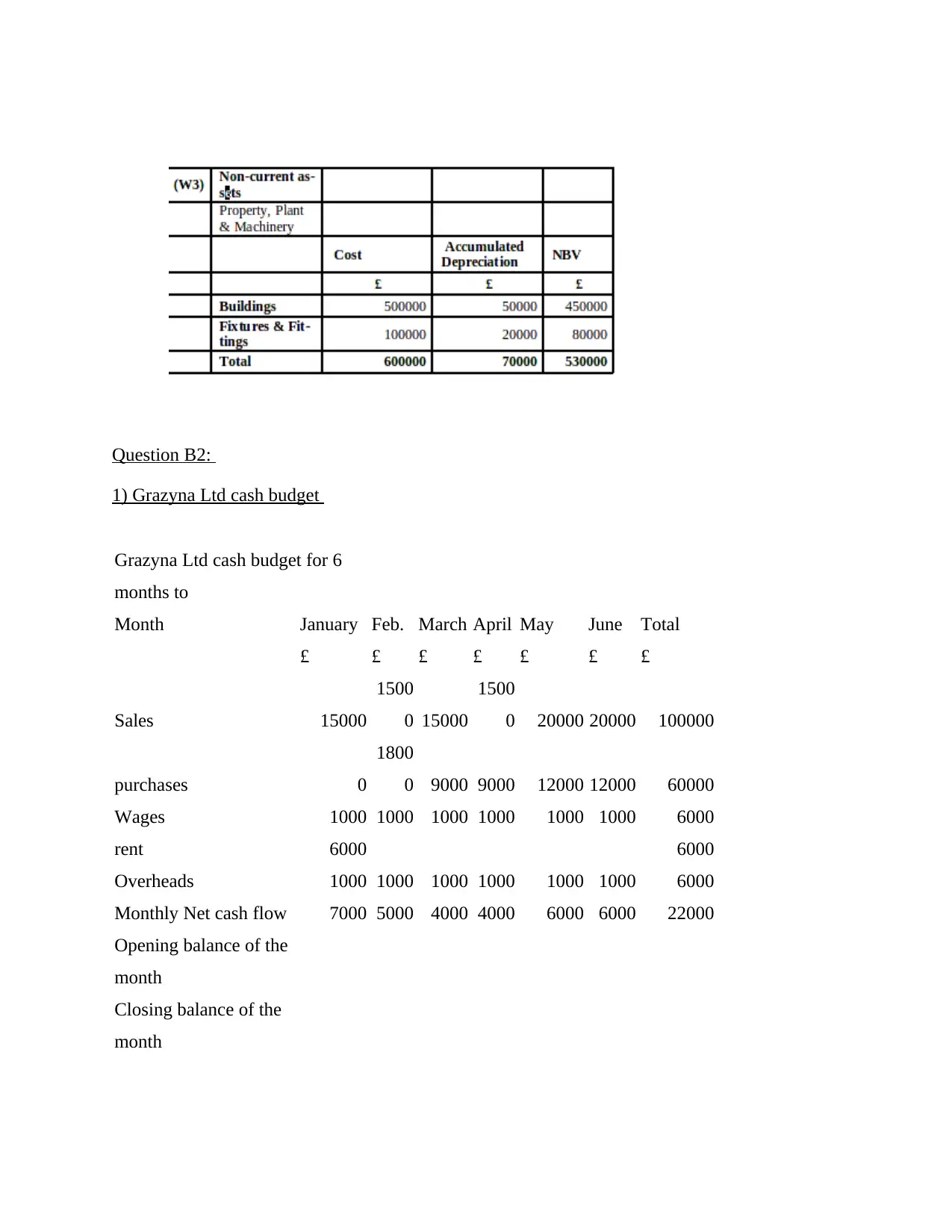

3) Statement of Financial position:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question B2:

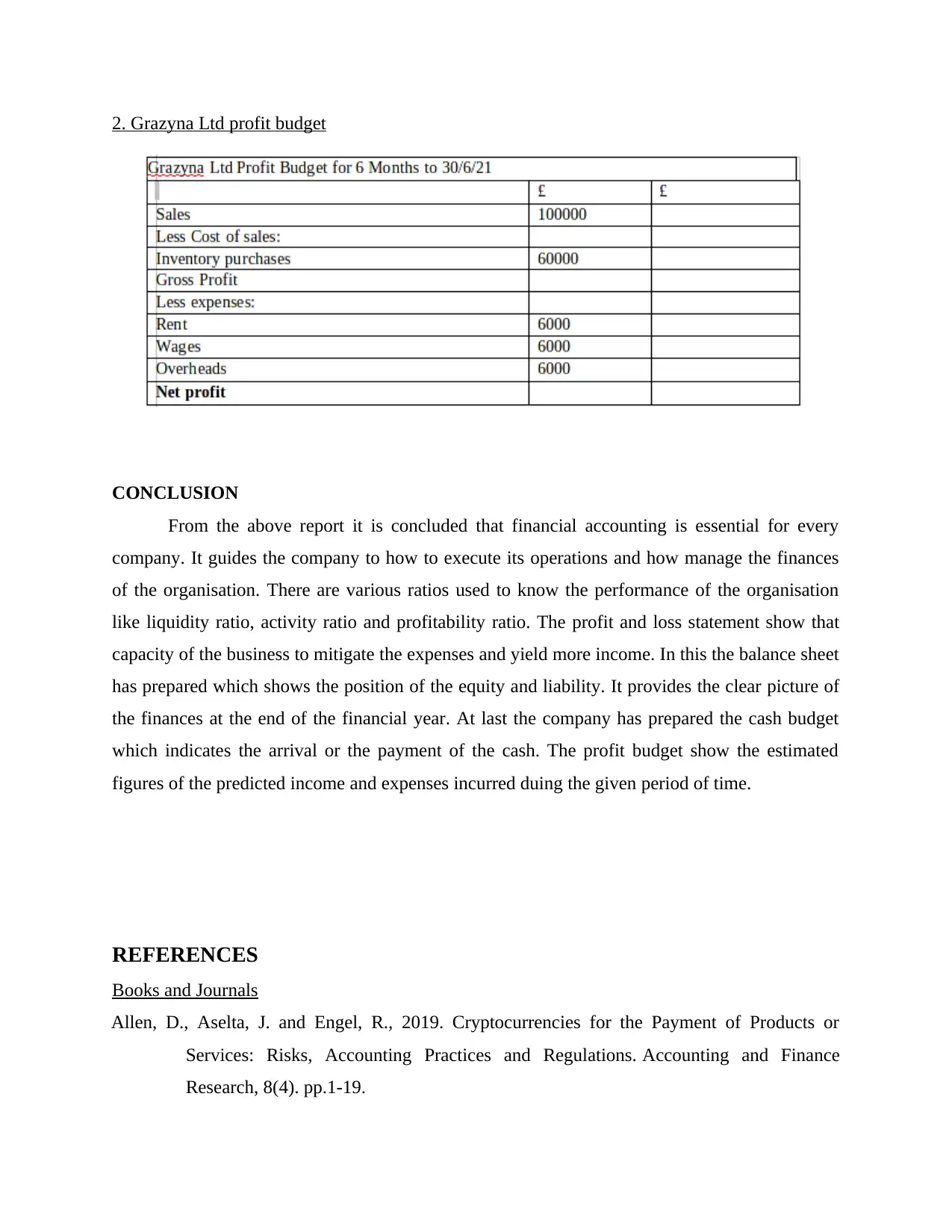

1) Grazyna Ltd cash budget

Grazyna Ltd cash budget for 6

months to

Month January Feb. March April May June Total

£ £ £ £ £ £ £

Sales 15000

1500

0 15000

1500

0 20000 20000 100000

purchases 0

1800

0 9000 9000 12000 12000 60000

Wages 1000 1000 1000 1000 1000 1000 6000

rent 6000 6000

Overheads 1000 1000 1000 1000 1000 1000 6000

Monthly Net cash flow 7000 5000 4000 4000 6000 6000 22000

Opening balance of the

month

Closing balance of the

month

1) Grazyna Ltd cash budget

Grazyna Ltd cash budget for 6

months to

Month January Feb. March April May June Total

£ £ £ £ £ £ £

Sales 15000

1500

0 15000

1500

0 20000 20000 100000

purchases 0

1800

0 9000 9000 12000 12000 60000

Wages 1000 1000 1000 1000 1000 1000 6000

rent 6000 6000

Overheads 1000 1000 1000 1000 1000 1000 6000

Monthly Net cash flow 7000 5000 4000 4000 6000 6000 22000

Opening balance of the

month

Closing balance of the

month

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

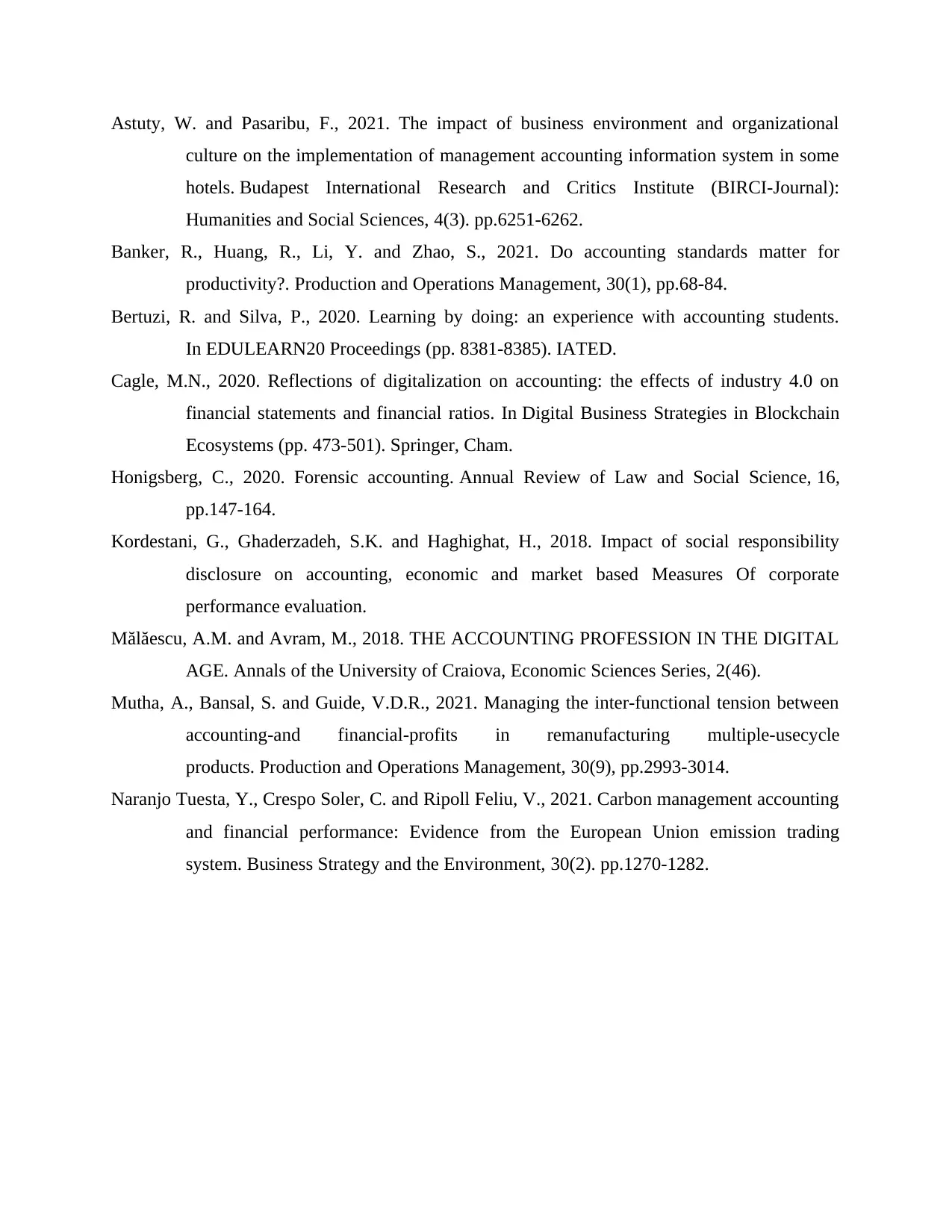

2. Grazyna Ltd profit budget

CONCLUSION

From the above report it is concluded that financial accounting is essential for every

company. It guides the company to how to execute its operations and how manage the finances

of the organisation. There are various ratios used to know the performance of the organisation

like liquidity ratio, activity ratio and profitability ratio. The profit and loss statement show that

capacity of the business to mitigate the expenses and yield more income. In this the balance sheet

has prepared which shows the position of the equity and liability. It provides the clear picture of

the finances at the end of the financial year. At last the company has prepared the cash budget

which indicates the arrival or the payment of the cash. The profit budget show the estimated

figures of the predicted income and expenses incurred duing the given period of time.

REFERENCES

Books and Journals

Allen, D., Aselta, J. and Engel, R., 2019. Cryptocurrencies for the Payment of Products or

Services: Risks, Accounting Practices and Regulations. Accounting and Finance

Research, 8(4). pp.1-19.

CONCLUSION

From the above report it is concluded that financial accounting is essential for every

company. It guides the company to how to execute its operations and how manage the finances

of the organisation. There are various ratios used to know the performance of the organisation

like liquidity ratio, activity ratio and profitability ratio. The profit and loss statement show that

capacity of the business to mitigate the expenses and yield more income. In this the balance sheet

has prepared which shows the position of the equity and liability. It provides the clear picture of

the finances at the end of the financial year. At last the company has prepared the cash budget

which indicates the arrival or the payment of the cash. The profit budget show the estimated

figures of the predicted income and expenses incurred duing the given period of time.

REFERENCES

Books and Journals

Allen, D., Aselta, J. and Engel, R., 2019. Cryptocurrencies for the Payment of Products or

Services: Risks, Accounting Practices and Regulations. Accounting and Finance

Research, 8(4). pp.1-19.

Astuty, W. and Pasaribu, F., 2021. The impact of business environment and organizational

culture on the implementation of management accounting information system in some

hotels. Budapest International Research and Critics Institute (BIRCI-Journal):

Humanities and Social Sciences, 4(3). pp.6251-6262.

Banker, R., Huang, R., Li, Y. and Zhao, S., 2021. Do accounting standards matter for

productivity?. Production and Operations Management, 30(1), pp.68-84.

Bertuzi, R. and Silva, P., 2020. Learning by doing: an experience with accounting students.

In EDULEARN20 Proceedings (pp. 8381-8385). IATED.

Cagle, M.N., 2020. Reflections of digitalization on accounting: the effects of industry 4.0 on

financial statements and financial ratios. In Digital Business Strategies in Blockchain

Ecosystems (pp. 473-501). Springer, Cham.

Honigsberg, C., 2020. Forensic accounting. Annual Review of Law and Social Science, 16,

pp.147-164.

Kordestani, G., Ghaderzadeh, S.K. and Haghighat, H., 2018. Impact of social responsibility

disclosure on accounting, economic and market based Measures Of corporate

performance evaluation.

Mălăescu, A.M. and Avram, M., 2018. THE ACCOUNTING PROFESSION IN THE DIGITAL

AGE. Annals of the University of Craiova, Economic Sciences Series, 2(46).

Mutha, A., Bansal, S. and Guide, V.D.R., 2021. Managing the inter‐functional tension between

accounting‐and financial‐profits in remanufacturing multiple‐usecycle

products. Production and Operations Management, 30(9), pp.2993-3014.

Naranjo Tuesta, Y., Crespo Soler, C. and Ripoll Feliu, V., 2021. Carbon management accounting

and financial performance: Evidence from the European Union emission trading

system. Business Strategy and the Environment, 30(2). pp.1270-1282.

culture on the implementation of management accounting information system in some

hotels. Budapest International Research and Critics Institute (BIRCI-Journal):

Humanities and Social Sciences, 4(3). pp.6251-6262.

Banker, R., Huang, R., Li, Y. and Zhao, S., 2021. Do accounting standards matter for

productivity?. Production and Operations Management, 30(1), pp.68-84.

Bertuzi, R. and Silva, P., 2020. Learning by doing: an experience with accounting students.

In EDULEARN20 Proceedings (pp. 8381-8385). IATED.

Cagle, M.N., 2020. Reflections of digitalization on accounting: the effects of industry 4.0 on

financial statements and financial ratios. In Digital Business Strategies in Blockchain

Ecosystems (pp. 473-501). Springer, Cham.

Honigsberg, C., 2020. Forensic accounting. Annual Review of Law and Social Science, 16,

pp.147-164.

Kordestani, G., Ghaderzadeh, S.K. and Haghighat, H., 2018. Impact of social responsibility

disclosure on accounting, economic and market based Measures Of corporate

performance evaluation.

Mălăescu, A.M. and Avram, M., 2018. THE ACCOUNTING PROFESSION IN THE DIGITAL

AGE. Annals of the University of Craiova, Economic Sciences Series, 2(46).

Mutha, A., Bansal, S. and Guide, V.D.R., 2021. Managing the inter‐functional tension between

accounting‐and financial‐profits in remanufacturing multiple‐usecycle

products. Production and Operations Management, 30(9), pp.2993-3014.

Naranjo Tuesta, Y., Crespo Soler, C. and Ripoll Feliu, V., 2021. Carbon management accounting

and financial performance: Evidence from the European Union emission trading

system. Business Strategy and the Environment, 30(2). pp.1270-1282.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.