Financial Accounting Report: IAS, Concepts, and Sole Traders

VerifiedAdded on 2020/12/10

|10

|2802

|179

Report

AI Summary

This report provides a comprehensive overview of financial accounting, encompassing various aspects such as financial statements, regulations, and key concepts. The report is divided into two parts, with the first part covering financial accounting and its purpose, regulations, accounting rules, and principles. The second part delves into sole traders, their advantages and disadvantages, capital, and the application of the accounting equation (Assets = Liabilities + Equity). The report further explores International Accounting Standards (IAS) like IAS 1 (Financial Statements) and IAS 2 (Inventory), along with concepts such as accrual, consistency, and prudence. Additionally, it examines depreciation, bank reconciliation statements, control accounts, and suspense accounts. The report provides insights into statement formats for sole traders and companies, offering a detailed analysis of financial accounting principles and their practical applications.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.Financial accounting and its purpose..................................................................................1

2. Regulations relating to financial accounting......................................................................1

3. Accounting rules and principles:........................................................................................2

4. Consistency and material disclosure convention and concepts:.........................................3

PART 2............................................................................................................................................3

1. Sole traders and its advantages and disadvantages.............................................................3

2. Capital for sole traders........................................................................................................4

3. ASSETS=LIABILITIES+EQUITY...................................................................................4

4. IAS 1: Financial statement and its purpose with need.......................................................4

5. Statement of sole trader and company................................................................................5

6. IAS 2- Inventory and evaluation........................................................................................5

7. Accrual concept..................................................................................................................6

8. Accounting Consistency and Prudence concept:................................................................6

9. Depreciation and its purpose in formulating accounting statements..................................6

10.Purpose of preparing Bank Reconciliation Statements.....................................................6

11. Control account................................................................................................................6

12. Suspense account..............................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.Financial accounting and its purpose..................................................................................1

2. Regulations relating to financial accounting......................................................................1

3. Accounting rules and principles:........................................................................................2

4. Consistency and material disclosure convention and concepts:.........................................3

PART 2............................................................................................................................................3

1. Sole traders and its advantages and disadvantages.............................................................3

2. Capital for sole traders........................................................................................................4

3. ASSETS=LIABILITIES+EQUITY...................................................................................4

4. IAS 1: Financial statement and its purpose with need.......................................................4

5. Statement of sole trader and company................................................................................5

6. IAS 2- Inventory and evaluation........................................................................................5

7. Accrual concept..................................................................................................................6

8. Accounting Consistency and Prudence concept:................................................................6

9. Depreciation and its purpose in formulating accounting statements..................................6

10.Purpose of preparing Bank Reconciliation Statements.....................................................6

11. Control account................................................................................................................6

12. Suspense account..............................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

The report comprises of two parts. The first part includes sole trader and company's financial

statement, inventory accounting standard, accrual, consistency, prudence concept, purpose of

calculation depreciation and creating bank reconciliation statement, use of control account,

suspense account and the second part consist of financial accounting regulation and its purpose,

accounting rules and principles, materiality and consistency conventions and concepts (Beatty,

2014).

PART 1

1.Financial accounting and its purpose

It is the field of accounting related to the concise description, investigation and recording

of financial transactions happening in a business. These transactions are recorded in financial

statements, including balance sheet, income statement, cash flow statement etc. These statements

are used to show financial position of the company. It is a part of accounting that uses money to

measure system execution rather than as an element of production.

Purpose of Financial Accounting

The purpose of financial accounting is to provide such information that is facilitative for

good economical decision making. The main purpose of it is to prepare financial statements that

provide accurate information about the performance of the organisation to the outer parties like

investors, stakeholders, suppliers and taxation department. There are various statements prepared

in financial accounting such as income statement, balance sheet, cash flow statement etc. There

are different purposes for each statement, income statement is used to determine the profit

capacity of the organisation, balance sheet is prepared to show the current status of the

organisation to the reader. Cash flow statement is helpful in determining the liquid strength of

the organisation. Its object is to effectively manage the material resources accessible. It is also

helpful in facilitating social functions and control.

2. Regulations relating to financial accounting

There are various regulation that an organisation is needed to follow few of those

regulations are explained below:

1

The report comprises of two parts. The first part includes sole trader and company's financial

statement, inventory accounting standard, accrual, consistency, prudence concept, purpose of

calculation depreciation and creating bank reconciliation statement, use of control account,

suspense account and the second part consist of financial accounting regulation and its purpose,

accounting rules and principles, materiality and consistency conventions and concepts (Beatty,

2014).

PART 1

1.Financial accounting and its purpose

It is the field of accounting related to the concise description, investigation and recording

of financial transactions happening in a business. These transactions are recorded in financial

statements, including balance sheet, income statement, cash flow statement etc. These statements

are used to show financial position of the company. It is a part of accounting that uses money to

measure system execution rather than as an element of production.

Purpose of Financial Accounting

The purpose of financial accounting is to provide such information that is facilitative for

good economical decision making. The main purpose of it is to prepare financial statements that

provide accurate information about the performance of the organisation to the outer parties like

investors, stakeholders, suppliers and taxation department. There are various statements prepared

in financial accounting such as income statement, balance sheet, cash flow statement etc. There

are different purposes for each statement, income statement is used to determine the profit

capacity of the organisation, balance sheet is prepared to show the current status of the

organisation to the reader. Cash flow statement is helpful in determining the liquid strength of

the organisation. Its object is to effectively manage the material resources accessible. It is also

helpful in facilitating social functions and control.

2. Regulations relating to financial accounting

There are various regulation that an organisation is needed to follow few of those

regulations are explained below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AS 2 Valuation of inventories: This standard set guideline for the organisation to

regulate the worth at which inventories are shown in the financial statement. It justifies different

ways of recording the closing stock which has a vast outcome on the business and the assets.

AS 3 Cash flow statement: It sets the regulation for the organisation to prepare a

statement that shows the balance of cash and cash equivalents at the end of financial year. It

shows the flow of incoming and outgoing cash of the organisation.

AS 25 Interim financial reporting: Main objective of this standard is to prepare interim

financial report in precise way so that investors will have accurate information of the

organisation and they can take right decision to invest in the organisation. These reports are also

helpful for the creditors and stakeholders to keep a record of their money they have invested in

the organisation (Bertoni, 2012).

3. Accounting rules and principles:

There are certain accounting rules and principles which an organisation follows while

preparing financial statements. These rules are referred to basic accounting principles and

guidelines which are given below:

Debit what comes in, credit what goes out: This rule is applied on real accounts like

tangible assets which have default debit balances when they come in business. Therefore,

debit what comes in means we add this balance into respective accounts by debited

amount and credit what goes out means we are deducting account balances when these

assets goes out of the business.

Debit the receiver, credit the giver: This rule is used in case of personal accounts that

means when we receive something from person i.e. inflows are debited and person who

gives is credited and vice versa.

Debit all expenses and losses, credit all incomes and gain: This rule is applied to

nominal account. Company's capital is a liability with credit balance. So when all

incomes and gain are credited it increases capital and all expenses and losses are debited

it decreases capital.

Principles:

Monetary unit principle: This principle implies only monetary transactions are recorded

which can be measured in terms of money.

2

regulate the worth at which inventories are shown in the financial statement. It justifies different

ways of recording the closing stock which has a vast outcome on the business and the assets.

AS 3 Cash flow statement: It sets the regulation for the organisation to prepare a

statement that shows the balance of cash and cash equivalents at the end of financial year. It

shows the flow of incoming and outgoing cash of the organisation.

AS 25 Interim financial reporting: Main objective of this standard is to prepare interim

financial report in precise way so that investors will have accurate information of the

organisation and they can take right decision to invest in the organisation. These reports are also

helpful for the creditors and stakeholders to keep a record of their money they have invested in

the organisation (Bertoni, 2012).

3. Accounting rules and principles:

There are certain accounting rules and principles which an organisation follows while

preparing financial statements. These rules are referred to basic accounting principles and

guidelines which are given below:

Debit what comes in, credit what goes out: This rule is applied on real accounts like

tangible assets which have default debit balances when they come in business. Therefore,

debit what comes in means we add this balance into respective accounts by debited

amount and credit what goes out means we are deducting account balances when these

assets goes out of the business.

Debit the receiver, credit the giver: This rule is used in case of personal accounts that

means when we receive something from person i.e. inflows are debited and person who

gives is credited and vice versa.

Debit all expenses and losses, credit all incomes and gain: This rule is applied to

nominal account. Company's capital is a liability with credit balance. So when all

incomes and gain are credited it increases capital and all expenses and losses are debited

it decreases capital.

Principles:

Monetary unit principle: This principle implies only monetary transactions are recorded

which can be measured in terms of money.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Matching principle: When revenues are recorded business should also record all related

expenses of the same accounting period.

Going concern: Entity of business will remain same in future accounting period.

Company is going to carry out its objectives and will not liquidate in future.

Cost principle: Business should record a transaction at its original acquisition cost.

Reliability principle: Recording of only those transactions that are evidenced which

means proven transactions.

Accrual principle: Transaction are recorded in same accounting period when they are

actually occurring not when money is received.

Business entity principle: Transaction of business are recorded separately from its

owner and other businesses.

4. Consistency and material disclosure convention and concepts:

Consistency concepts defines that accounting principles which are once adopted should

be followed consistently in future accounting periods also. Alternation in principles is only

possible when they change methods on reasonable ground or it's innovation improves financial

reports and such changes are disclosing in financial statements of the same accounting year. For

example, if company previously using declining balance depreciation method and at last quarter

they want to change it to straight line, then they must have disclosed it in financial statements

(Edwards, 2013).

Material disclosure convention refers to all material i.e. necessary information that may

impact on readers in understanding financial statement must be clearly disclosed and immaterial

items are ignored while preparing profit and loss a/c, balance sheet. Such disclosure includes

supplementary schedules and footnotes in financial statements and quarterly earnings reports.

Footnotes includes that significant accounting policies like how assets is depreciated, inventory

valuation method, when revenue is recognised and many more.

PART 2

1. Sole traders and its advantages and disadvantages

Sole traders: These are the owners of the company and they are liable to bear all the

losses and to keep all the profits after interest and tax. They have many liabilities to manage and

control their business.

3

expenses of the same accounting period.

Going concern: Entity of business will remain same in future accounting period.

Company is going to carry out its objectives and will not liquidate in future.

Cost principle: Business should record a transaction at its original acquisition cost.

Reliability principle: Recording of only those transactions that are evidenced which

means proven transactions.

Accrual principle: Transaction are recorded in same accounting period when they are

actually occurring not when money is received.

Business entity principle: Transaction of business are recorded separately from its

owner and other businesses.

4. Consistency and material disclosure convention and concepts:

Consistency concepts defines that accounting principles which are once adopted should

be followed consistently in future accounting periods also. Alternation in principles is only

possible when they change methods on reasonable ground or it's innovation improves financial

reports and such changes are disclosing in financial statements of the same accounting year. For

example, if company previously using declining balance depreciation method and at last quarter

they want to change it to straight line, then they must have disclosed it in financial statements

(Edwards, 2013).

Material disclosure convention refers to all material i.e. necessary information that may

impact on readers in understanding financial statement must be clearly disclosed and immaterial

items are ignored while preparing profit and loss a/c, balance sheet. Such disclosure includes

supplementary schedules and footnotes in financial statements and quarterly earnings reports.

Footnotes includes that significant accounting policies like how assets is depreciated, inventory

valuation method, when revenue is recognised and many more.

PART 2

1. Sole traders and its advantages and disadvantages

Sole traders: These are the owners of the company and they are liable to bear all the

losses and to keep all the profits after interest and tax. They have many liabilities to manage and

control their business.

3

Advantages Disadvantages

They have right to retain all the profit

of the business.

They are not bound to share

information to the public like

companies, all the information remain

private.

As they are the owners of the they have

many liabilities related to the company,

if there are so many debts in the

company then they are liable for the

same.

2. Capital for sole traders

A sole trader has to put own money in the business that is the capital for sole trader. They

can use own savings, money from family or friends, loans from banks if they have security to

pay back the loan. These are the ways to invest money in the business that is capital (Horngren,

2012).

3. ASSETS=LIABILITIES+EQUITY

It is an equation that shows the relation between these three different terms, those are

assets, liabilities and equity.

Assets are the company's resources the company owns like cash, stocks, account

receivables and fixed assets.

Liabilities are the obligations of the company it is the amount that is payable by the

company such as creditors, account payables, loans etc.

Equity is the owners fund or capital which have been invested by the owner of the

company. Equities and liabilities are recorded in left side of balance sheet and assets are recorded

in right side of the balance sheet. When all the transactions are recorded accurately then total of

right and left side of balance sheet will be the same.

4. IAS 1: Financial statement and its purpose with need

These are the written format of all financial activities that happen in an accounting year.

There are three types of financial statements explained below:

Income statement: It shows the revenue generated and expenses faced by the organisation

within a year and results with net profit or loss for the organisation.

Purpose: The purpose of income statement is to show the accurate information regarding

profit or loss to the investors, creditors and stakeholders of the organisation.

4

They have right to retain all the profit

of the business.

They are not bound to share

information to the public like

companies, all the information remain

private.

As they are the owners of the they have

many liabilities related to the company,

if there are so many debts in the

company then they are liable for the

same.

2. Capital for sole traders

A sole trader has to put own money in the business that is the capital for sole trader. They

can use own savings, money from family or friends, loans from banks if they have security to

pay back the loan. These are the ways to invest money in the business that is capital (Horngren,

2012).

3. ASSETS=LIABILITIES+EQUITY

It is an equation that shows the relation between these three different terms, those are

assets, liabilities and equity.

Assets are the company's resources the company owns like cash, stocks, account

receivables and fixed assets.

Liabilities are the obligations of the company it is the amount that is payable by the

company such as creditors, account payables, loans etc.

Equity is the owners fund or capital which have been invested by the owner of the

company. Equities and liabilities are recorded in left side of balance sheet and assets are recorded

in right side of the balance sheet. When all the transactions are recorded accurately then total of

right and left side of balance sheet will be the same.

4. IAS 1: Financial statement and its purpose with need

These are the written format of all financial activities that happen in an accounting year.

There are three types of financial statements explained below:

Income statement: It shows the revenue generated and expenses faced by the organisation

within a year and results with net profit or loss for the organisation.

Purpose: The purpose of income statement is to show the accurate information regarding

profit or loss to the investors, creditors and stakeholders of the organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Need: It is required to record all the incomes and expenses of the business in an

accounting year.

Balance sheet: All the assets and liabilities are recorded in balance sheet to analyse the

financial condition and market position of the business.

Purpose: The purpose of preparing balance sheet is to supply faithful information of

business's performance to the investors.

Need: Balance sheet is important to maintain by the company because it is used to

maintain the record of assets and liabilities of an organisation.

Cash flow statement: It shows all the cash related transactions within a specific period

of time, and shows the closing balance of cash remaining in the organisation.

Purpose: The purpose of cash flow statement is to keep a record of each transaction

which is related to cash such as cash payments and cash receipts of an organisation.

Need: It is required to maintain because it covers all the important information of cash

and cash equivalents that are required for the management to take decisions (Khan, 2015).

5. Statement of sole trader and company

Statement of sole trader: A sole trader prepares financial statements in horizontal

format that is a traditional method, in sole trader organisation there is only one member who is

the owner of the company, and the amount of transaction is comparatively lower than company.

Statement of a company: A company uses modern method of financial statement that is

vertical format of financial statement, there is many members in a company to take decisions

they are called shareholders, and the amount of transactions is very high (Financial Accounting

Foundations, 2018).

6. IAS 2- Inventory and evaluation

International accounting standard board sets a guideline for inventory valuation and its

classification. Valuation of inventory are based on its write down value and net realisable value.

The cost of inventories consists of cost of production, conversion and distribution. When

inventories are sold its carrying amount and difference between the amount of write down and

net realisable value of inventory and all losses of inventory are recognised as expenses is treated

as an expenses of that particular period in which revenue recorded (May, 2013).

5

accounting year.

Balance sheet: All the assets and liabilities are recorded in balance sheet to analyse the

financial condition and market position of the business.

Purpose: The purpose of preparing balance sheet is to supply faithful information of

business's performance to the investors.

Need: Balance sheet is important to maintain by the company because it is used to

maintain the record of assets and liabilities of an organisation.

Cash flow statement: It shows all the cash related transactions within a specific period

of time, and shows the closing balance of cash remaining in the organisation.

Purpose: The purpose of cash flow statement is to keep a record of each transaction

which is related to cash such as cash payments and cash receipts of an organisation.

Need: It is required to maintain because it covers all the important information of cash

and cash equivalents that are required for the management to take decisions (Khan, 2015).

5. Statement of sole trader and company

Statement of sole trader: A sole trader prepares financial statements in horizontal

format that is a traditional method, in sole trader organisation there is only one member who is

the owner of the company, and the amount of transaction is comparatively lower than company.

Statement of a company: A company uses modern method of financial statement that is

vertical format of financial statement, there is many members in a company to take decisions

they are called shareholders, and the amount of transactions is very high (Financial Accounting

Foundations, 2018).

6. IAS 2- Inventory and evaluation

International accounting standard board sets a guideline for inventory valuation and its

classification. Valuation of inventory are based on its write down value and net realisable value.

The cost of inventories consists of cost of production, conversion and distribution. When

inventories are sold its carrying amount and difference between the amount of write down and

net realisable value of inventory and all losses of inventory are recognised as expenses is treated

as an expenses of that particular period in which revenue recorded (May, 2013).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7. Accrual concept

This accounting concept requires to record all incomes and gain in the accounting period

when they are earned not when they are received in monetary basis. Similarly, all expenses and

losses are recorded when they incurred not when they are paid.

8. Accounting Consistency and Prudence concept:

Consistency concept: This concept means company should continue with the accounting

principles which they adopt in the beginning of financial year and continue it consistently in

coming accounting years.

Prudence concept: This accounting concept defines that company should record its

liabilities and expenses immediately when incurred but revenues are recorded in the financial

year only when they are realized (Weil, 2013).

9. Depreciation and its purpose in formulating accounting statements

Depreciation is a decrease in the value of an asset after a period of time due to normal

wear and tear. It systematically moves asset's cost from balance sheet to expense on income

statement over asset's life. The purpose of calculating depreciation is to match asset cost with its

use. Straight line and Declining balance are two types of methods works for calculation of

depreciation.

Straight line depreciation estimates the useful life of the asset. This method reflects the

consumption pattern of the inherent asset.

Declining balance depreciation results in reducing depreciation charges in each

accounting period. This method is useful when asset productivity is higher i.e. in the beginning

of its life.

10.Purpose of preparing Bank Reconciliation Statements

BRS is used to compare company's bank statement with balances of bank. Company

prepare this statement on monthly basis so that they can verify their transactions are properly

recorded in company and bank books or not (Sharma, 2013).

11. Control account

This account is used in recording and cross checking the balances on a various subsidiary

accounts. It is a summary account in the general ledger. The purpose of creating those account is

to keep the general ledger neat which shows accurate balances.

6

This accounting concept requires to record all incomes and gain in the accounting period

when they are earned not when they are received in monetary basis. Similarly, all expenses and

losses are recorded when they incurred not when they are paid.

8. Accounting Consistency and Prudence concept:

Consistency concept: This concept means company should continue with the accounting

principles which they adopt in the beginning of financial year and continue it consistently in

coming accounting years.

Prudence concept: This accounting concept defines that company should record its

liabilities and expenses immediately when incurred but revenues are recorded in the financial

year only when they are realized (Weil, 2013).

9. Depreciation and its purpose in formulating accounting statements

Depreciation is a decrease in the value of an asset after a period of time due to normal

wear and tear. It systematically moves asset's cost from balance sheet to expense on income

statement over asset's life. The purpose of calculating depreciation is to match asset cost with its

use. Straight line and Declining balance are two types of methods works for calculation of

depreciation.

Straight line depreciation estimates the useful life of the asset. This method reflects the

consumption pattern of the inherent asset.

Declining balance depreciation results in reducing depreciation charges in each

accounting period. This method is useful when asset productivity is higher i.e. in the beginning

of its life.

10.Purpose of preparing Bank Reconciliation Statements

BRS is used to compare company's bank statement with balances of bank. Company

prepare this statement on monthly basis so that they can verify their transactions are properly

recorded in company and bank books or not (Sharma, 2013).

11. Control account

This account is used in recording and cross checking the balances on a various subsidiary

accounts. It is a summary account in the general ledger. The purpose of creating those account is

to keep the general ledger neat which shows accurate balances.

6

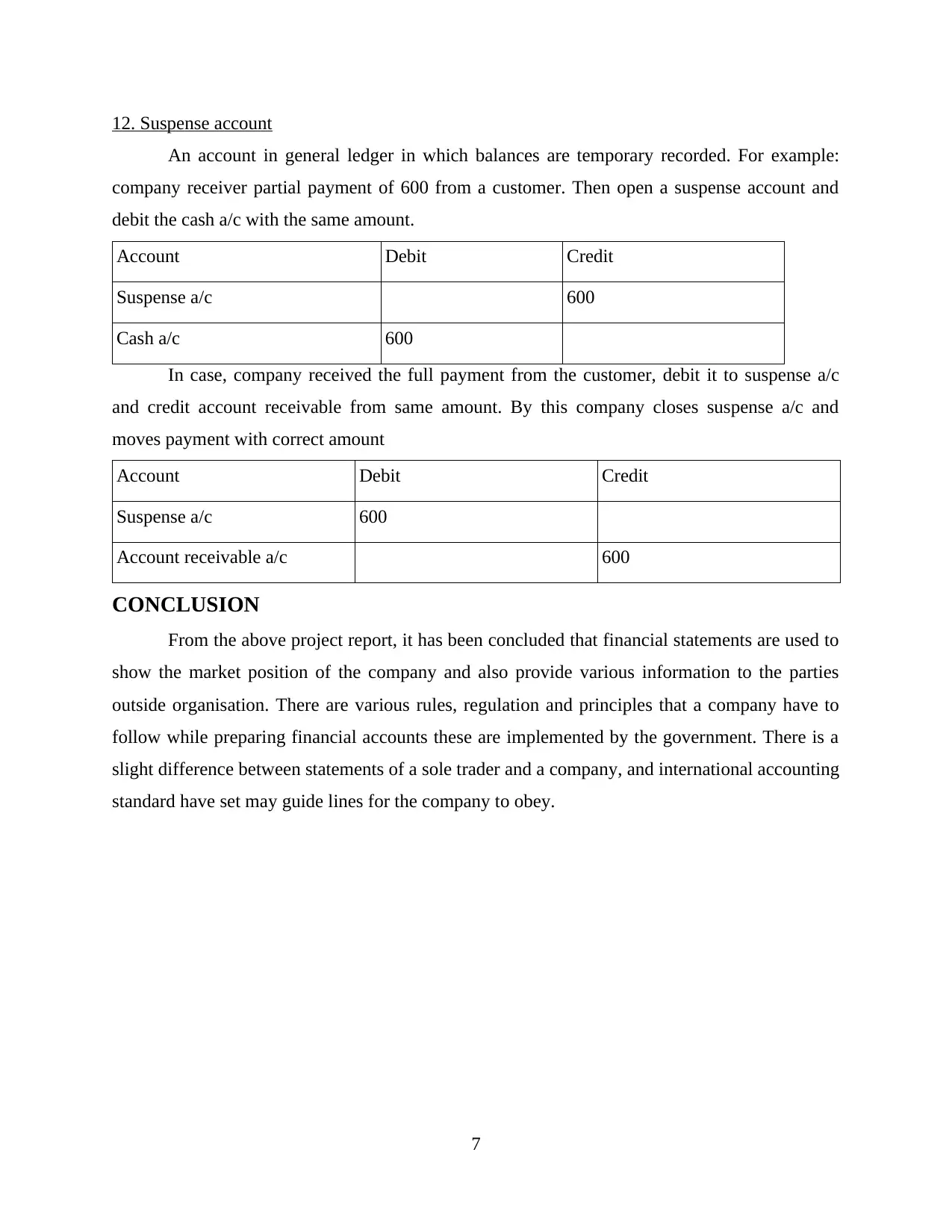

12. Suspense account

An account in general ledger in which balances are temporary recorded. For example:

company receiver partial payment of 600 from a customer. Then open a suspense account and

debit the cash a/c with the same amount.

Account Debit Credit

Suspense a/c 600

Cash a/c 600

In case, company received the full payment from the customer, debit it to suspense a/c

and credit account receivable from same amount. By this company closes suspense a/c and

moves payment with correct amount

Account Debit Credit

Suspense a/c 600

Account receivable a/c 600

CONCLUSION

From the above project report, it has been concluded that financial statements are used to

show the market position of the company and also provide various information to the parties

outside organisation. There are various rules, regulation and principles that a company have to

follow while preparing financial accounts these are implemented by the government. There is a

slight difference between statements of a sole trader and a company, and international accounting

standard have set may guide lines for the company to obey.

7

An account in general ledger in which balances are temporary recorded. For example:

company receiver partial payment of 600 from a customer. Then open a suspense account and

debit the cash a/c with the same amount.

Account Debit Credit

Suspense a/c 600

Cash a/c 600

In case, company received the full payment from the customer, debit it to suspense a/c

and credit account receivable from same amount. By this company closes suspense a/c and

moves payment with correct amount

Account Debit Credit

Suspense a/c 600

Account receivable a/c 600

CONCLUSION

From the above project report, it has been concluded that financial statements are used to

show the market position of the company and also provide various information to the parties

outside organisation. There are various rules, regulation and principles that a company have to

follow while preparing financial accounts these are implemented by the government. There is a

slight difference between statements of a sole trader and a company, and international accounting

standard have set may guide lines for the company to obey.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Bertoni, M. P. G. V. A. G. and De Rosa, B., 2012. Green accounting: an alternative approach to

reporting emission trading allowances in financial statements.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Horngren, C., and et. al., 2012. Financial accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

May, G. O., 2013. Financial accounting. Read Books Ltd.

Sharma, A. and Panigrahi, P. K., 2013. A review of financial accounting fraud detection based

on data mining techniques. arXiv preprint arXiv:1309.3944.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Online

Financial Accounting: Foundations. 2018. [Online]. Available through:

<https://www.coursera.org/learn/financial-accounting-basics>.

8

Books and Journals

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Bertoni, M. P. G. V. A. G. and De Rosa, B., 2012. Green accounting: an alternative approach to

reporting emission trading allowances in financial statements.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Horngren, C., and et. al., 2012. Financial accounting. Pearson Higher Education AU.

Khan, M., 2015. Accounting: Financial. In Encyclopedia of Public Administration and Public

Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

May, G. O., 2013. Financial accounting. Read Books Ltd.

Sharma, A. and Panigrahi, P. K., 2013. A review of financial accounting fraud detection based

on data mining techniques. arXiv preprint arXiv:1309.3944.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Online

Financial Accounting: Foundations. 2018. [Online]. Available through:

<https://www.coursera.org/learn/financial-accounting-basics>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.