Financial Accounting Report: Amstel D. and Sierra Laurent Analysis

VerifiedAdded on 2020/12/10

|40

|4007

|130

Report

AI Summary

This report delves into the core principles and practices of financial accounting. It begins with an introduction to the field, explaining its purpose, regulations, and the importance of adhering to accounting standards like GAAP and IFRS. The report then examines key accounting principles, including the monetary unit, going concern, historical cost, and conservatism principles, among others. It also explores concepts like consistency and material disclosure. The practical application of these principles is demonstrated through the analysis of journal entries, ledger accounts, and trial balances for multiple clients (Amstel D., Sierra Laurent, and LMS Ltd.), culminating in the preparation of financial statements, including profit and loss accounts and statements of financial position. The report also covers topics like bank reconciliation statements, control accounts, and suspense accounts, providing a holistic view of financial accounting procedures. The report concludes with a discussion of depreciation methods and the application of accounting concepts in real-world scenarios.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A......................................................................................................................................................1

1. Report to Line Manager explaining accounting regulations....................................................1

2. Financial Accounting Regulations...........................................................................................2

3. Accounting Principles and Rules.............................................................................................3

4.Concepts relating to consistency and material disclosure........................................................4

CLIENT 1........................................................................................................................................5

1. Preparation of journal entries for Amstel D............................................................................5

2. Creating leader accounts for Amstel D....................................................................................6

3. Extracting Trail Balance by compiling accounts...................................................................22

CLIENT 2......................................................................................................................................23

1. Preparation of Statement of Profit and loss for Sierra Laurent.............................................23

2. Preparing Statement of Financial Position............................................................................24

CLIENT 3......................................................................................................................................27

1. Profit and Loss account of LMS Ltd....................................................................................27

2. Statement of financial position of company..........................................................................28

3. Explanation of consistency and prudency concept................................................................30

4. Description of purpose of depreciation and explaining methods of charging it....................30

CLIENT 4......................................................................................................................................31

1. Purpose of preparing Bank Reconciliation Statement of Kendal Ltd....................................31

2. Causes of varying accounting records with bank statements................................................31

3. Preparation of cash book and Bank Reconciliation Statement..............................................31

CLIENT 5......................................................................................................................................34

1. Producing sales and purchase ledger control account of Tom Higher..................................34

2. Defining control account.......................................................................................................35

CLIENT 6......................................................................................................................................35

1. Suspense account and outlining its rain features...................................................................35

2. Constructing trial balance......................................................................................................36

3. Differentiating between clearing and suspense account........................................................36

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................38

INTRODUCTION...........................................................................................................................1

A......................................................................................................................................................1

1. Report to Line Manager explaining accounting regulations....................................................1

2. Financial Accounting Regulations...........................................................................................2

3. Accounting Principles and Rules.............................................................................................3

4.Concepts relating to consistency and material disclosure........................................................4

CLIENT 1........................................................................................................................................5

1. Preparation of journal entries for Amstel D............................................................................5

2. Creating leader accounts for Amstel D....................................................................................6

3. Extracting Trail Balance by compiling accounts...................................................................22

CLIENT 2......................................................................................................................................23

1. Preparation of Statement of Profit and loss for Sierra Laurent.............................................23

2. Preparing Statement of Financial Position............................................................................24

CLIENT 3......................................................................................................................................27

1. Profit and Loss account of LMS Ltd....................................................................................27

2. Statement of financial position of company..........................................................................28

3. Explanation of consistency and prudency concept................................................................30

4. Description of purpose of depreciation and explaining methods of charging it....................30

CLIENT 4......................................................................................................................................31

1. Purpose of preparing Bank Reconciliation Statement of Kendal Ltd....................................31

2. Causes of varying accounting records with bank statements................................................31

3. Preparation of cash book and Bank Reconciliation Statement..............................................31

CLIENT 5......................................................................................................................................34

1. Producing sales and purchase ledger control account of Tom Higher..................................34

2. Defining control account.......................................................................................................35

CLIENT 6......................................................................................................................................35

1. Suspense account and outlining its rain features...................................................................35

2. Constructing trial balance......................................................................................................36

3. Differentiating between clearing and suspense account........................................................36

CONCLUSION..............................................................................................................................37

REFERENCES..............................................................................................................................38

INTRODUCTION

The process of recording, summarizing and reporting business transactions that occur

over a specific period of time, is known as financial accounting. It includes the preparation of

financial and income statements, cash flow and balance sheets (Flores and Braunbeck, 2017).

This report will cover purpose of financial accounting and its meaning. Explanation of

accounting rules, regulations and governing principles that aid in preparing financial statements

as well as consistency and material disclosure conventions and concepts will be elaborated.

Double entry book keeping by recording of business transactions and creation of trial balance

will be done and analysed. Bank reconciliation statement's purpose and application, control and

suspense accounts will be explained as well.

A

1. Report to Line Manager explaining accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms and regulations useful for organisation to comply with

Respected Sir,

The recording, measuring and summarizing of daily financial transactions in a business

operation is described as accounting. It is both an art and a science because there is requirement

of judgements and skills, as well as a body of knowledge that has rules and principles that

constantly changes. Accounts are only expressed in monetary terms and accountants are to be

trained with proper discipline in order to perform various accounting functions. Financial

accounting is a field of accountancy (Gebhardt, Mora and Wagenhofer, 2014). It helps in

controlling and keeping track of a business' assets and liabilities, while providing methods for

money deduction and cost control. Company is able to determine economic data, policies for its

business and aid in fixation of tax. Trail balance helps in testing the arithmetical accuracy of

accounts which assists in capital borrowing, when needed.

Interpretation of amounts, figures and data is done through the summarization of

recorded information, in order to create financial reports and analyse their results. Management

ascertains positive and negative aspects and take proper measures to correct any problems that

comes forward. The main purpose of accounting is to accumulate and report fiscal information

1

The process of recording, summarizing and reporting business transactions that occur

over a specific period of time, is known as financial accounting. It includes the preparation of

financial and income statements, cash flow and balance sheets (Flores and Braunbeck, 2017).

This report will cover purpose of financial accounting and its meaning. Explanation of

accounting rules, regulations and governing principles that aid in preparing financial statements

as well as consistency and material disclosure conventions and concepts will be elaborated.

Double entry book keeping by recording of business transactions and creation of trial balance

will be done and analysed. Bank reconciliation statement's purpose and application, control and

suspense accounts will be explained as well.

A

1. Report to Line Manager explaining accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms and regulations useful for organisation to comply with

Respected Sir,

The recording, measuring and summarizing of daily financial transactions in a business

operation is described as accounting. It is both an art and a science because there is requirement

of judgements and skills, as well as a body of knowledge that has rules and principles that

constantly changes. Accounts are only expressed in monetary terms and accountants are to be

trained with proper discipline in order to perform various accounting functions. Financial

accounting is a field of accountancy (Gebhardt, Mora and Wagenhofer, 2014). It helps in

controlling and keeping track of a business' assets and liabilities, while providing methods for

money deduction and cost control. Company is able to determine economic data, policies for its

business and aid in fixation of tax. Trail balance helps in testing the arithmetical accuracy of

accounts which assists in capital borrowing, when needed.

Interpretation of amounts, figures and data is done through the summarization of

recorded information, in order to create financial reports and analyse their results. Management

ascertains positive and negative aspects and take proper measures to correct any problems that

comes forward. The main purpose of accounting is to accumulate and report fiscal information

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with regard to performances, financial position and cash flows of a company's business. It helps

in keeping track of operations. These statements provide qualitative and quantitative information

that is used while making decisions about investments and business management. Owners are

able to find out their entity's stability, profitability and ability to pay obligations (Wagenhofer,

2015). The information is useful for 3rd parties such as creditors, investors, stakeholders, lenders,

employees and government.

2. Financial Accounting Regulations

Financial regulators impart guidelines that are to be followed by various businesses in

order to get rid of manipulation of accounting records which can affect its fairness and reliability

to a large extent. This can help users of financial accounting gain correct information and 3rd

parties do not get misguided by inaccurate information (Ijiri, 2018). International Accounting

Standards Boards or IAS has created International financial reporting standards (IFRS) and

FASB set various accounting standards which have been issues by GAAP that has to be followed

by businesses while preparation of their books of accounts.

Financial reporting council or FRC, is a body that is formed by guarantee and regulates

corporate and government businesses. It is beneficial as proper principles are followed which

leads to preparation of true financials. Accountants have ease while preparing various statements

with regard to IASB prescribed regulations as it helps them in determining correct position of

company. IFRS also helps and guides preparation of financial reports in the best possible way

and aids in following policies and rules so that information is clear and precise for those who

have to make important decisions.

Financial statements are made according to GAAP, which is beneficial for fiscal market

investors as they require information of companies for making decisions. Revenue recognition

helps in improvement of financial reports that includes income and comparability of various

statements. The disclosure of debt securities and purchased financial assets are to be done in

order to help investors understand estimates. Securities and exchange commission body

regulates financial markets and accounting standard setting bodies (Kim and et.al., 2016). Audit

boards are reviewed by Public Company accounting oversight board and auditing standards are

determined by them.

2

in keeping track of operations. These statements provide qualitative and quantitative information

that is used while making decisions about investments and business management. Owners are

able to find out their entity's stability, profitability and ability to pay obligations (Wagenhofer,

2015). The information is useful for 3rd parties such as creditors, investors, stakeholders, lenders,

employees and government.

2. Financial Accounting Regulations

Financial regulators impart guidelines that are to be followed by various businesses in

order to get rid of manipulation of accounting records which can affect its fairness and reliability

to a large extent. This can help users of financial accounting gain correct information and 3rd

parties do not get misguided by inaccurate information (Ijiri, 2018). International Accounting

Standards Boards or IAS has created International financial reporting standards (IFRS) and

FASB set various accounting standards which have been issues by GAAP that has to be followed

by businesses while preparation of their books of accounts.

Financial reporting council or FRC, is a body that is formed by guarantee and regulates

corporate and government businesses. It is beneficial as proper principles are followed which

leads to preparation of true financials. Accountants have ease while preparing various statements

with regard to IASB prescribed regulations as it helps them in determining correct position of

company. IFRS also helps and guides preparation of financial reports in the best possible way

and aids in following policies and rules so that information is clear and precise for those who

have to make important decisions.

Financial statements are made according to GAAP, which is beneficial for fiscal market

investors as they require information of companies for making decisions. Revenue recognition

helps in improvement of financial reports that includes income and comparability of various

statements. The disclosure of debt securities and purchased financial assets are to be done in

order to help investors understand estimates. Securities and exchange commission body

regulates financial markets and accounting standard setting bodies (Kim and et.al., 2016). Audit

boards are reviewed by Public Company accounting oversight board and auditing standards are

determined by them.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

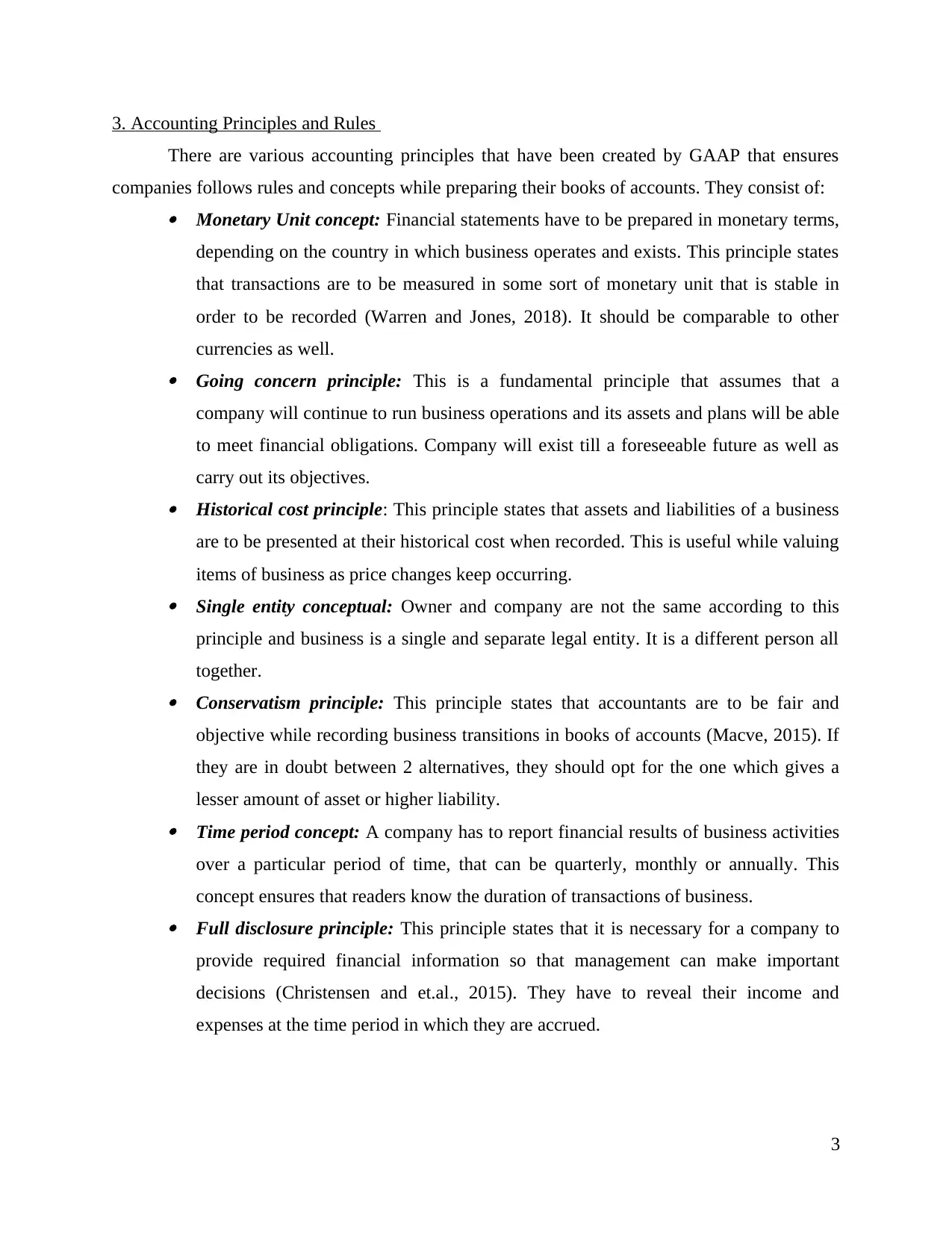

3. Accounting Principles and Rules

There are various accounting principles that have been created by GAAP that ensures

companies follows rules and concepts while preparing their books of accounts. They consist of:

Monetary Unit concept: Financial statements have to be prepared in monetary terms,

depending on the country in which business operates and exists. This principle states

that transactions are to be measured in some sort of monetary unit that is stable in

order to be recorded (Warren and Jones, 2018). It should be comparable to other

currencies as well.

Going concern principle: This is a fundamental principle that assumes that a

company will continue to run business operations and its assets and plans will be able

to meet financial obligations. Company will exist till a foreseeable future as well as

carry out its objectives.

Historical cost principle: This principle states that assets and liabilities of a business

are to be presented at their historical cost when recorded. This is useful while valuing

items of business as price changes keep occurring.

Single entity conceptual: Owner and company are not the same according to this

principle and business is a single and separate legal entity. It is a different person all

together.

Conservatism principle: This principle states that accountants are to be fair and

objective while recording business transitions in books of accounts (Macve, 2015). If

they are in doubt between 2 alternatives, they should opt for the one which gives a

lesser amount of asset or higher liability.

Time period concept: A company has to report financial results of business activities

over a particular period of time, that can be quarterly, monthly or annually. This

concept ensures that readers know the duration of transactions of business.

Full disclosure principle: This principle states that it is necessary for a company to

provide required financial information so that management can make important

decisions (Christensen and et.al., 2015). They have to reveal their income and

expenses at the time period in which they are accrued.

3

There are various accounting principles that have been created by GAAP that ensures

companies follows rules and concepts while preparing their books of accounts. They consist of:

Monetary Unit concept: Financial statements have to be prepared in monetary terms,

depending on the country in which business operates and exists. This principle states

that transactions are to be measured in some sort of monetary unit that is stable in

order to be recorded (Warren and Jones, 2018). It should be comparable to other

currencies as well.

Going concern principle: This is a fundamental principle that assumes that a

company will continue to run business operations and its assets and plans will be able

to meet financial obligations. Company will exist till a foreseeable future as well as

carry out its objectives.

Historical cost principle: This principle states that assets and liabilities of a business

are to be presented at their historical cost when recorded. This is useful while valuing

items of business as price changes keep occurring.

Single entity conceptual: Owner and company are not the same according to this

principle and business is a single and separate legal entity. It is a different person all

together.

Conservatism principle: This principle states that accountants are to be fair and

objective while recording business transitions in books of accounts (Macve, 2015). If

they are in doubt between 2 alternatives, they should opt for the one which gives a

lesser amount of asset or higher liability.

Time period concept: A company has to report financial results of business activities

over a particular period of time, that can be quarterly, monthly or annually. This

concept ensures that readers know the duration of transactions of business.

Full disclosure principle: This principle states that it is necessary for a company to

provide required financial information so that management can make important

decisions (Christensen and et.al., 2015). They have to reveal their income and

expenses at the time period in which they are accrued.

3

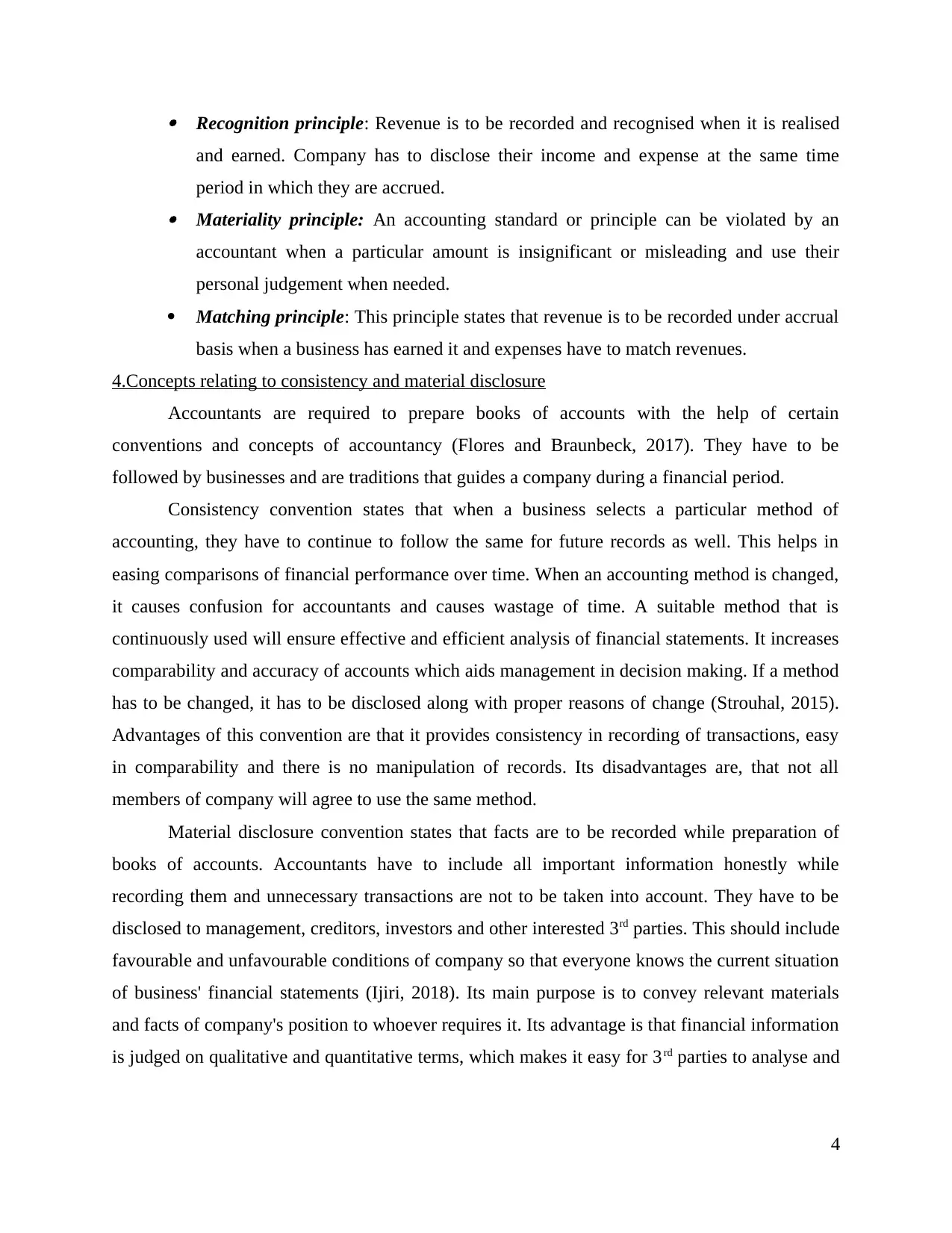

Recognition principle: Revenue is to be recorded and recognised when it is realised

and earned. Company has to disclose their income and expense at the same time

period in which they are accrued.

Materiality principle: An accounting standard or principle can be violated by an

accountant when a particular amount is insignificant or misleading and use their

personal judgement when needed.

Matching principle: This principle states that revenue is to be recorded under accrual

basis when a business has earned it and expenses have to match revenues.

4.Concepts relating to consistency and material disclosure

Accountants are required to prepare books of accounts with the help of certain

conventions and concepts of accountancy (Flores and Braunbeck, 2017). They have to be

followed by businesses and are traditions that guides a company during a financial period.

Consistency convention states that when a business selects a particular method of

accounting, they have to continue to follow the same for future records as well. This helps in

easing comparisons of financial performance over time. When an accounting method is changed,

it causes confusion for accountants and causes wastage of time. A suitable method that is

continuously used will ensure effective and efficient analysis of financial statements. It increases

comparability and accuracy of accounts which aids management in decision making. If a method

has to be changed, it has to be disclosed along with proper reasons of change (Strouhal, 2015).

Advantages of this convention are that it provides consistency in recording of transactions, easy

in comparability and there is no manipulation of records. Its disadvantages are, that not all

members of company will agree to use the same method.

Material disclosure convention states that facts are to be recorded while preparation of

books of accounts. Accountants have to include all important information honestly while

recording them and unnecessary transactions are not to be taken into account. They have to be

disclosed to management, creditors, investors and other interested 3rd parties. This should include

favourable and unfavourable conditions of company so that everyone knows the current situation

of business' financial statements (Ijiri, 2018). Its main purpose is to convey relevant materials

and facts of company's position to whoever requires it. Its advantage is that financial information

is judged on qualitative and quantitative terms, which makes it easy for 3rd parties to analyse and

4

and earned. Company has to disclose their income and expense at the same time

period in which they are accrued.

Materiality principle: An accounting standard or principle can be violated by an

accountant when a particular amount is insignificant or misleading and use their

personal judgement when needed.

Matching principle: This principle states that revenue is to be recorded under accrual

basis when a business has earned it and expenses have to match revenues.

4.Concepts relating to consistency and material disclosure

Accountants are required to prepare books of accounts with the help of certain

conventions and concepts of accountancy (Flores and Braunbeck, 2017). They have to be

followed by businesses and are traditions that guides a company during a financial period.

Consistency convention states that when a business selects a particular method of

accounting, they have to continue to follow the same for future records as well. This helps in

easing comparisons of financial performance over time. When an accounting method is changed,

it causes confusion for accountants and causes wastage of time. A suitable method that is

continuously used will ensure effective and efficient analysis of financial statements. It increases

comparability and accuracy of accounts which aids management in decision making. If a method

has to be changed, it has to be disclosed along with proper reasons of change (Strouhal, 2015).

Advantages of this convention are that it provides consistency in recording of transactions, easy

in comparability and there is no manipulation of records. Its disadvantages are, that not all

members of company will agree to use the same method.

Material disclosure convention states that facts are to be recorded while preparation of

books of accounts. Accountants have to include all important information honestly while

recording them and unnecessary transactions are not to be taken into account. They have to be

disclosed to management, creditors, investors and other interested 3rd parties. This should include

favourable and unfavourable conditions of company so that everyone knows the current situation

of business' financial statements (Ijiri, 2018). Its main purpose is to convey relevant materials

and facts of company's position to whoever requires it. Its advantage is that financial information

is judged on qualitative and quantitative terms, which makes it easy for 3rd parties to analyse and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine whether or not the company will be a good investment. Disclosing too much

information is a disadvantage as it weakens a business's competition.

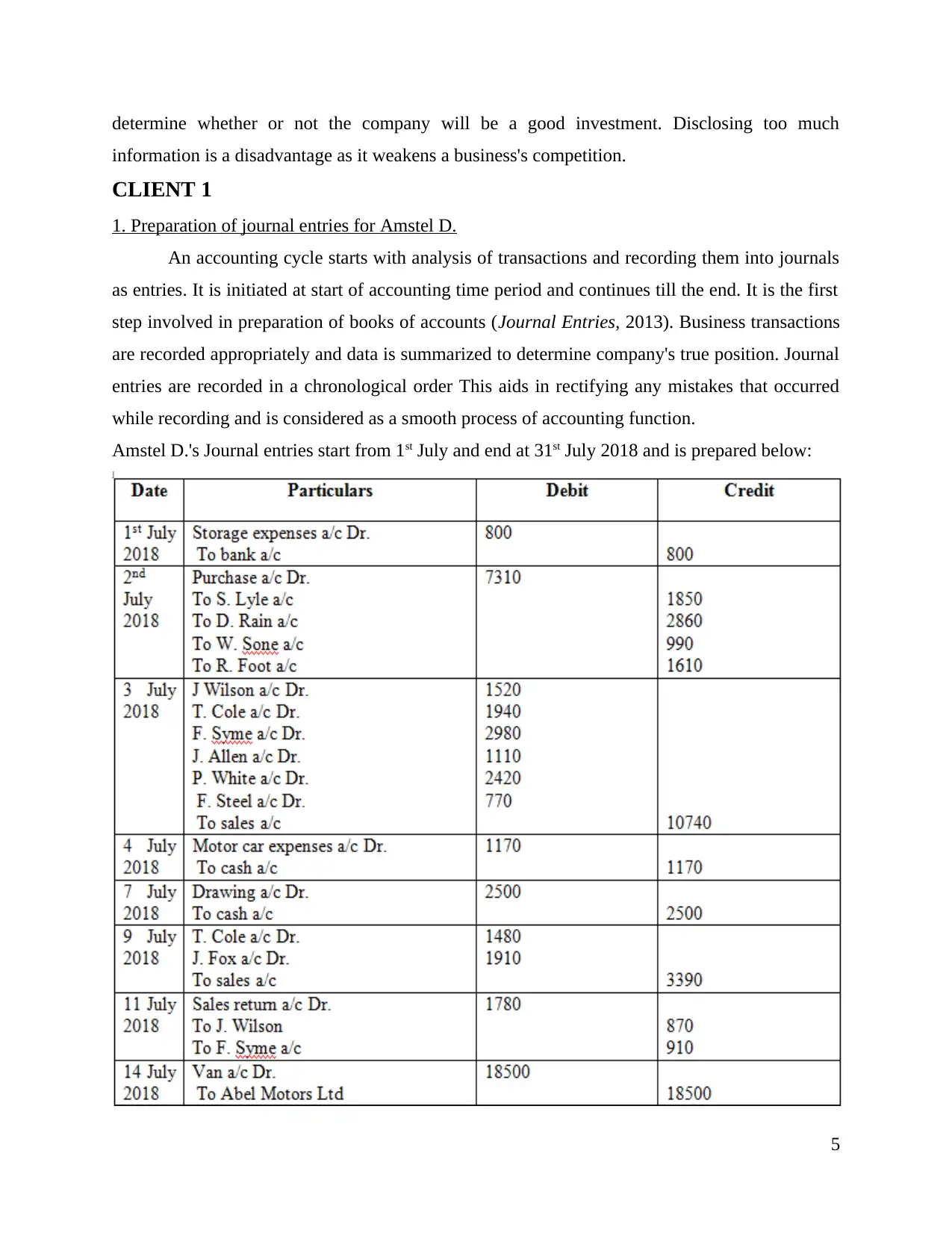

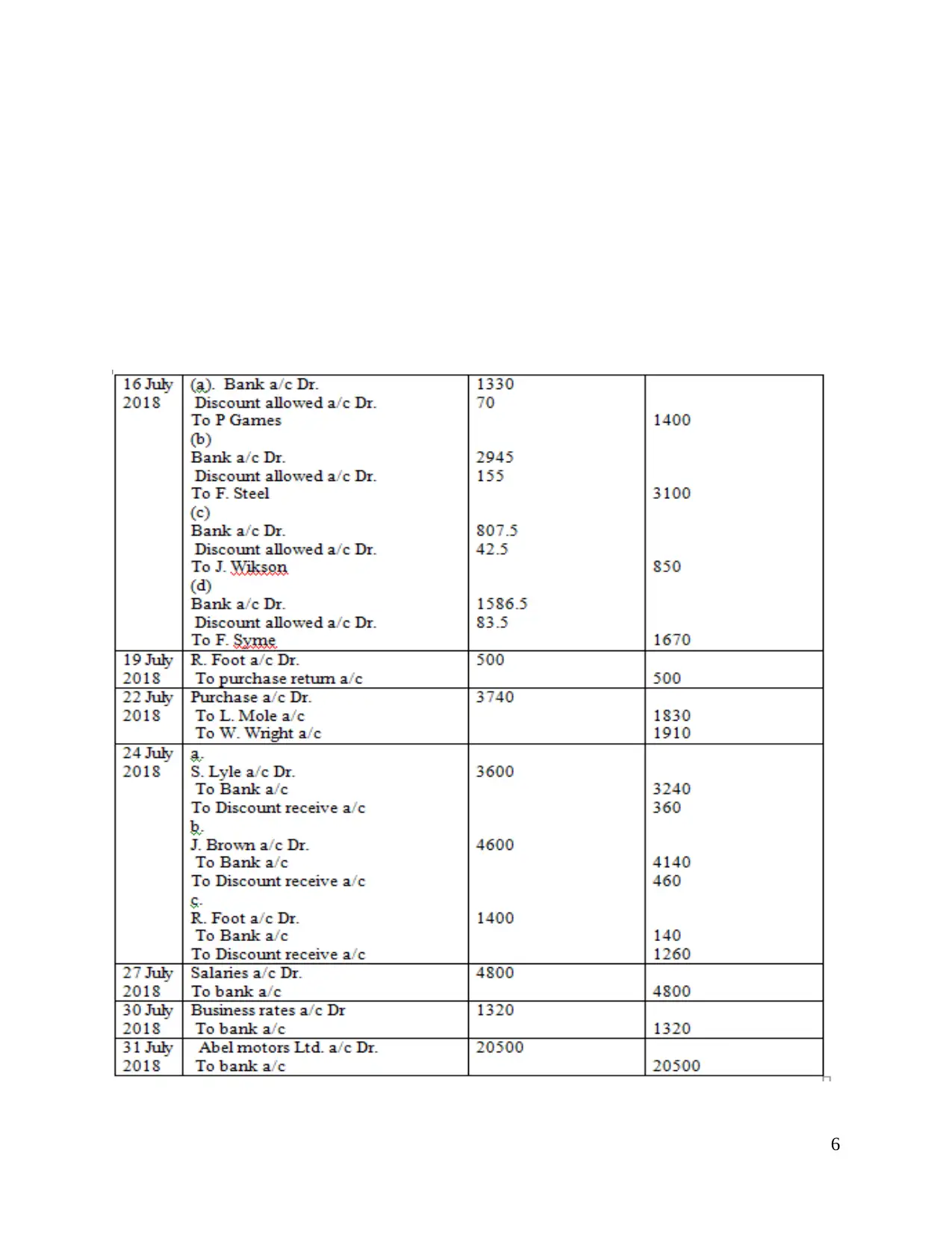

CLIENT 1

1. Preparation of journal entries for Amstel D.

An accounting cycle starts with analysis of transactions and recording them into journals

as entries. It is initiated at start of accounting time period and continues till the end. It is the first

step involved in preparation of books of accounts (Journal Entries, 2013). Business transactions

are recorded appropriately and data is summarized to determine company's true position. Journal

entries are recorded in a chronological order This aids in rectifying any mistakes that occurred

while recording and is considered as a smooth process of accounting function.

Amstel D.'s Journal entries start from 1st July and end at 31st July 2018 and is prepared below:

5

information is a disadvantage as it weakens a business's competition.

CLIENT 1

1. Preparation of journal entries for Amstel D.

An accounting cycle starts with analysis of transactions and recording them into journals

as entries. It is initiated at start of accounting time period and continues till the end. It is the first

step involved in preparation of books of accounts (Journal Entries, 2013). Business transactions

are recorded appropriately and data is summarized to determine company's true position. Journal

entries are recorded in a chronological order This aids in rectifying any mistakes that occurred

while recording and is considered as a smooth process of accounting function.

Amstel D.'s Journal entries start from 1st July and end at 31st July 2018 and is prepared below:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

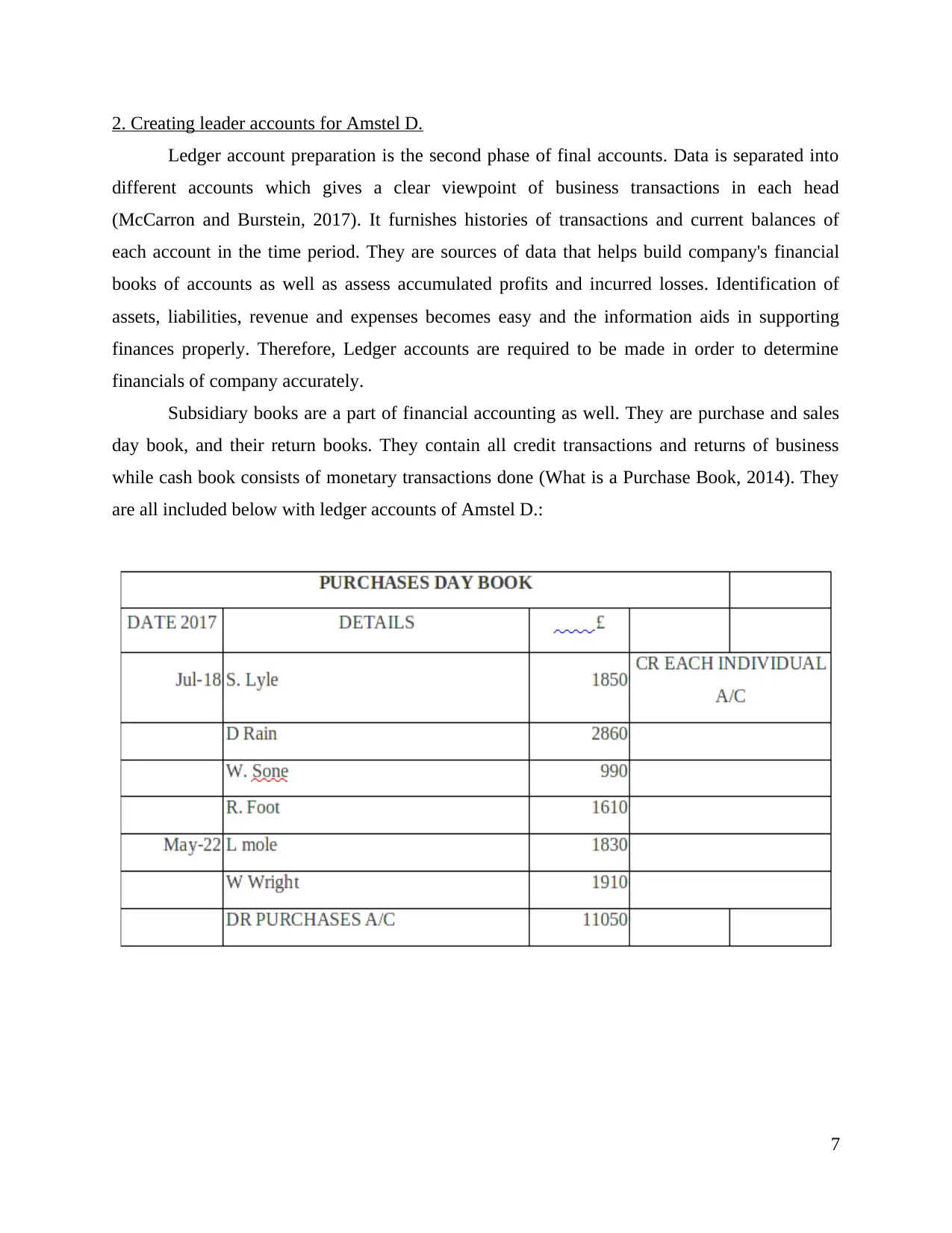

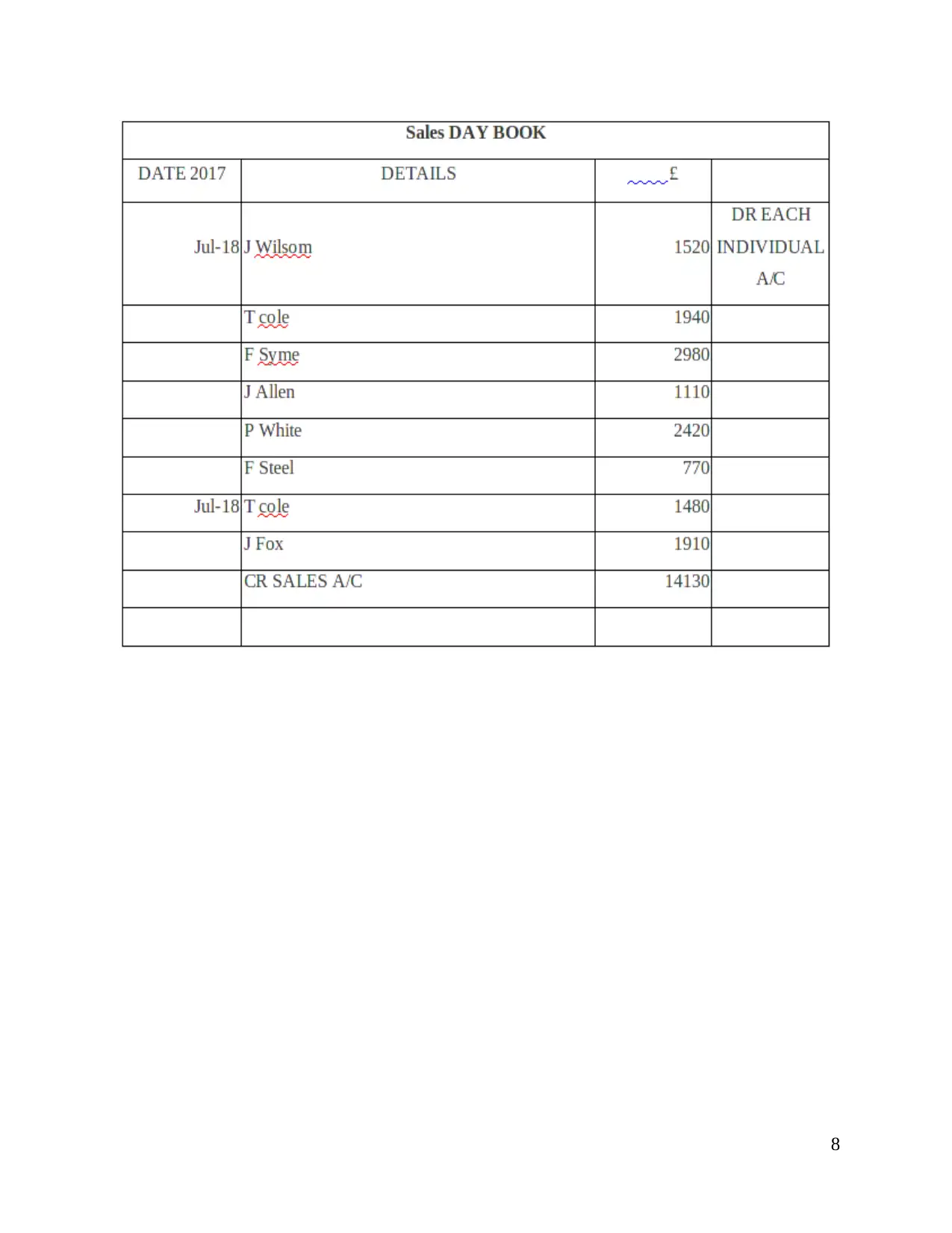

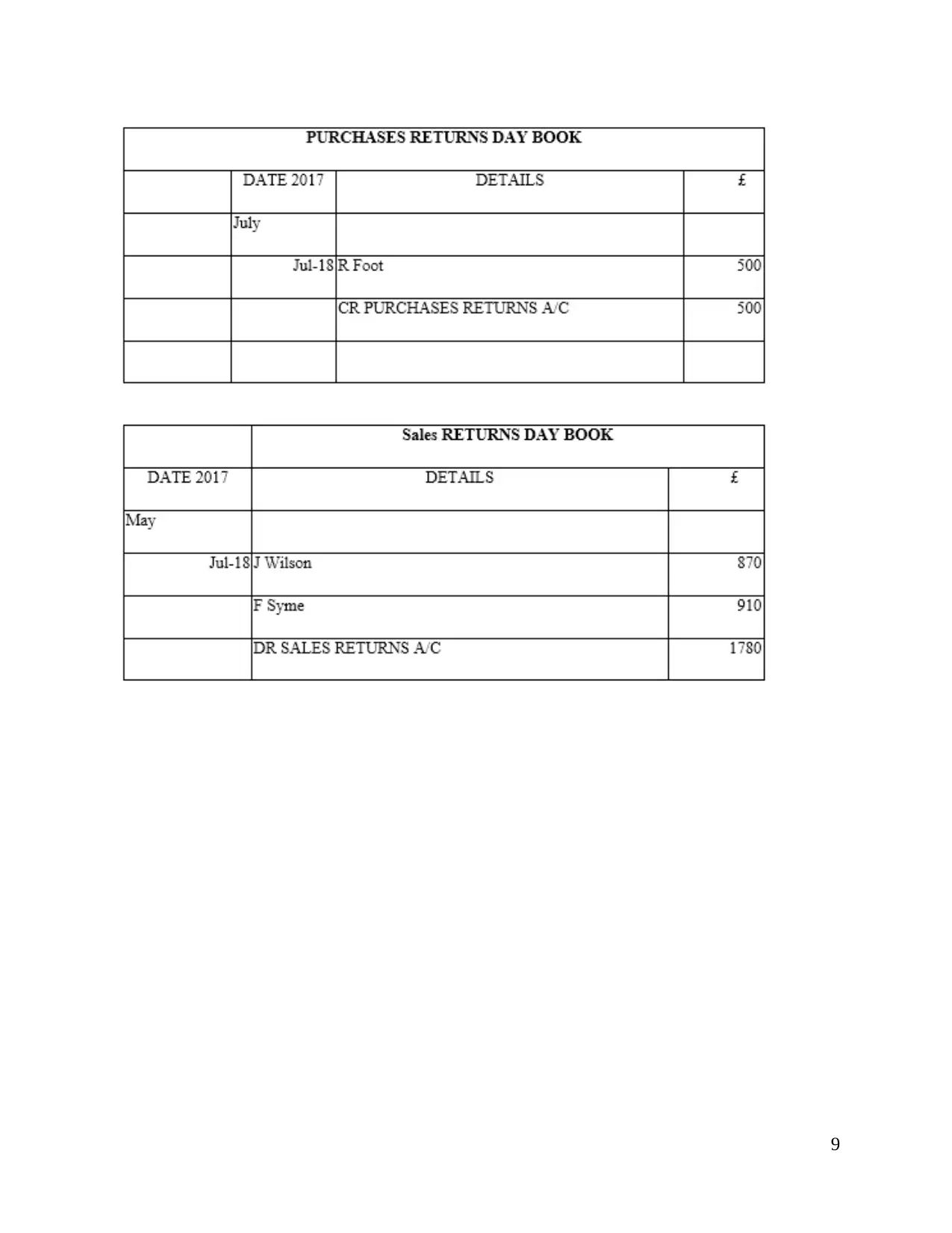

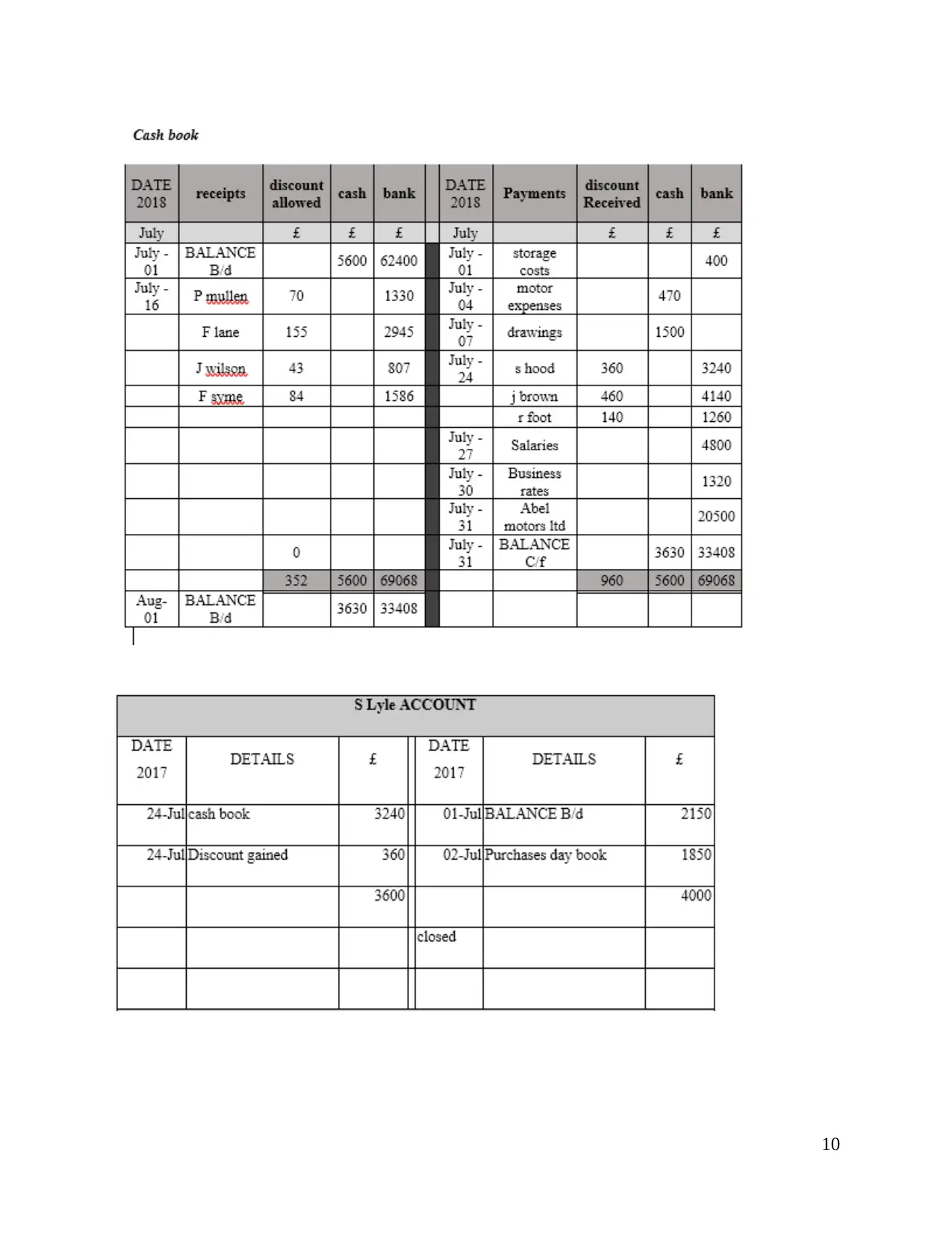

2. Creating leader accounts for Amstel D.

Ledger account preparation is the second phase of final accounts. Data is separated into

different accounts which gives a clear viewpoint of business transactions in each head

(McCarron and Burstein, 2017). It furnishes histories of transactions and current balances of

each account in the time period. They are sources of data that helps build company's financial

books of accounts as well as assess accumulated profits and incurred losses. Identification of

assets, liabilities, revenue and expenses becomes easy and the information aids in supporting

finances properly. Therefore, Ledger accounts are required to be made in order to determine

financials of company accurately.

Subsidiary books are a part of financial accounting as well. They are purchase and sales

day book, and their return books. They contain all credit transactions and returns of business

while cash book consists of monetary transactions done (What is a Purchase Book, 2014). They

are all included below with ledger accounts of Amstel D.:

7

Ledger account preparation is the second phase of final accounts. Data is separated into

different accounts which gives a clear viewpoint of business transactions in each head

(McCarron and Burstein, 2017). It furnishes histories of transactions and current balances of

each account in the time period. They are sources of data that helps build company's financial

books of accounts as well as assess accumulated profits and incurred losses. Identification of

assets, liabilities, revenue and expenses becomes easy and the information aids in supporting

finances properly. Therefore, Ledger accounts are required to be made in order to determine

financials of company accurately.

Subsidiary books are a part of financial accounting as well. They are purchase and sales

day book, and their return books. They contain all credit transactions and returns of business

while cash book consists of monetary transactions done (What is a Purchase Book, 2014). They

are all included below with ledger accounts of Amstel D.:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.