Financial Accounting: Business Transactions and Financial Statements

VerifiedAdded on 2022/11/24

|17

|3882

|169

Report

AI Summary

This report provides a comprehensive overview of financial accounting, covering various aspects such as business transactions, single and double-entry bookkeeping, and the importance of a trial balance. It differentiates between financial statements and financial reporting, elaborates on accounting principles like accrual and consistency, and discusses bank reconciliation and control accounts. The report also includes practical applications with journal entries, income statement preparation, balance sheet analysis, and cash flow statement interpretation. Scenario-based questions are addressed to illustrate the concepts, providing a thorough understanding of financial accounting principles and their application in real-world business scenarios. Desklib offers students access to similar solved assignments and resources for further study.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

Scenario 1........................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................4

Question 3....................................................................................................................................5

Question 4....................................................................................................................................6

Question 5....................................................................................................................................7

Question 6....................................................................................................................................8

Question 7....................................................................................................................................9

Scenario 2......................................................................................................................................10

Question 1..................................................................................................................................10

Question 4..................................................................................................................................12

Question 5..................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

1

Introduction......................................................................................................................................2

Scenario 1........................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................4

Question 3....................................................................................................................................5

Question 4....................................................................................................................................6

Question 5....................................................................................................................................7

Question 6....................................................................................................................................8

Question 7....................................................................................................................................9

Scenario 2......................................................................................................................................10

Question 1..................................................................................................................................10

Question 4..................................................................................................................................12

Question 5..................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

1

Introduction

Financial accounting as a particular branch of accounting and it represents to an ongoing

procedure of recording identifying and analysing summarising all the transactions which has

been taken place in the business operations for an accounting period (Yerznkyan and et.al 2020).

All these transactions are further categorised and summarised and different financial statements

such as balance sheet income statement and cash flow which records all the operating

performance of the company for specified time duration. This report further demonstrate about

various types of business transactions and it also includes single entry and double entry

bookkeeping. Importance of trial balance has also been defined in this report. Key difference

between financial statement and financial reporting has also been elaborated in this report.

Different principle of accounting it is also being jotted in this report. Bank reconciliation and its

importance has also been discussed in this report. Role of control account in financial

management has also been defined in this report along with this suspense account and reason for

drafting suspense account is also been mentioned in this report.

Scenario 1

Question 1

Different types of business transaction

There are number of business transactions held in the organisation such as:

Purchase of raw material and goods

Every organisation needed various goods and raw material so that they can produce

quality goods. Purchase can be categorised into cash or credit (Types of Business Transactions

and Documentation., 2020). Those organisation which go for cash purchase then they need to

make payment immediately on the other hand when they go for credit then they will not need to

take immediately to the supplier so most of the organisation works on credit purchase.

Sales

Sales also divided into two parts such as cash sales and credit sales. In the credit scenes

organisation gets the payment after some time but in cash saves the get immediate payment by

selling goods and services.

Wages and salary

2

Financial accounting as a particular branch of accounting and it represents to an ongoing

procedure of recording identifying and analysing summarising all the transactions which has

been taken place in the business operations for an accounting period (Yerznkyan and et.al 2020).

All these transactions are further categorised and summarised and different financial statements

such as balance sheet income statement and cash flow which records all the operating

performance of the company for specified time duration. This report further demonstrate about

various types of business transactions and it also includes single entry and double entry

bookkeeping. Importance of trial balance has also been defined in this report. Key difference

between financial statement and financial reporting has also been elaborated in this report.

Different principle of accounting it is also being jotted in this report. Bank reconciliation and its

importance has also been discussed in this report. Role of control account in financial

management has also been defined in this report along with this suspense account and reason for

drafting suspense account is also been mentioned in this report.

Scenario 1

Question 1

Different types of business transaction

There are number of business transactions held in the organisation such as:

Purchase of raw material and goods

Every organisation needed various goods and raw material so that they can produce

quality goods. Purchase can be categorised into cash or credit (Types of Business Transactions

and Documentation., 2020). Those organisation which go for cash purchase then they need to

make payment immediately on the other hand when they go for credit then they will not need to

take immediately to the supplier so most of the organisation works on credit purchase.

Sales

Sales also divided into two parts such as cash sales and credit sales. In the credit scenes

organisation gets the payment after some time but in cash saves the get immediate payment by

selling goods and services.

Wages and salary

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

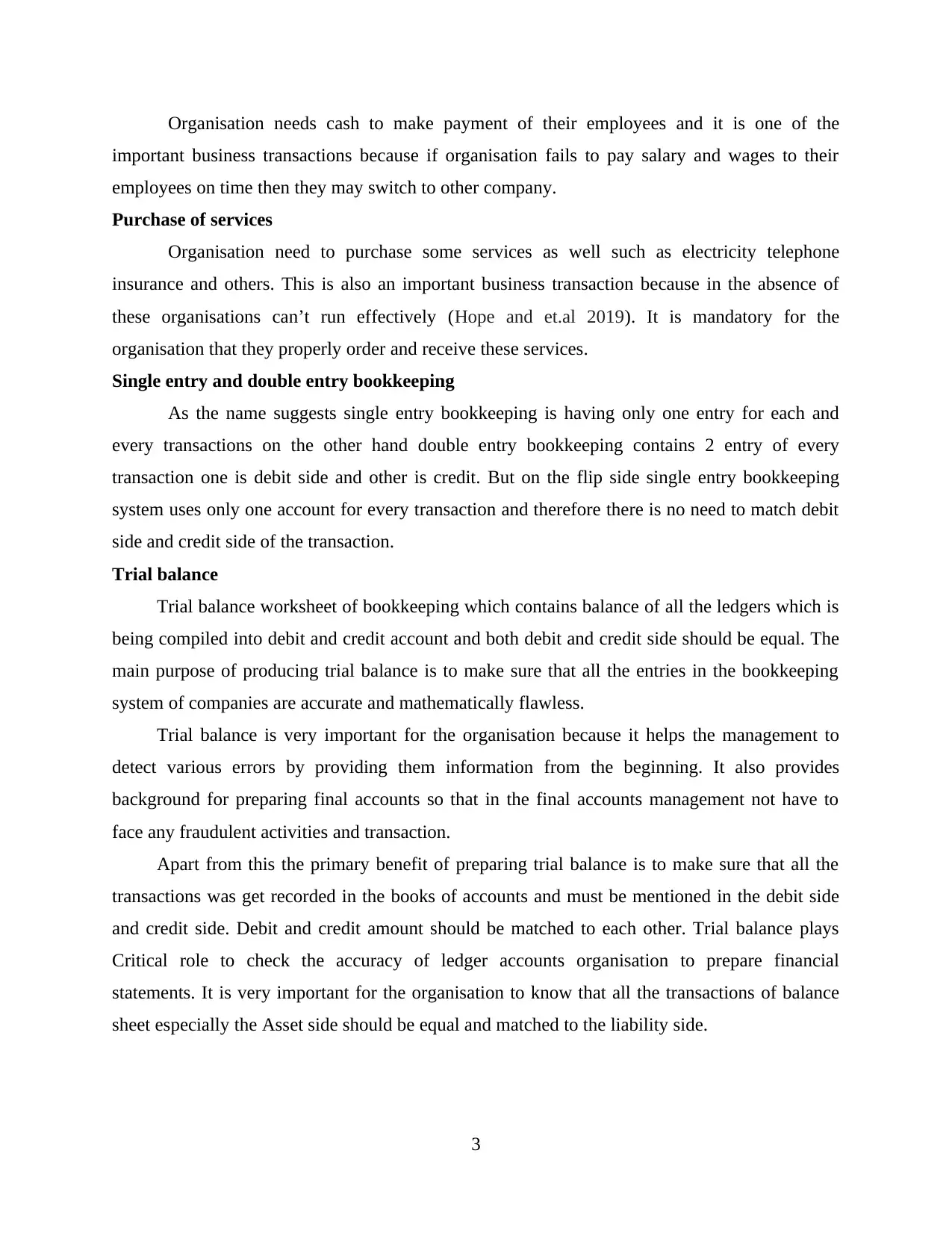

Organisation needs cash to make payment of their employees and it is one of the

important business transactions because if organisation fails to pay salary and wages to their

employees on time then they may switch to other company.

Purchase of services

Organisation need to purchase some services as well such as electricity telephone

insurance and others. This is also an important business transaction because in the absence of

these organisations can’t run effectively (Hope and et.al 2019). It is mandatory for the

organisation that they properly order and receive these services.

Single entry and double entry bookkeeping

As the name suggests single entry bookkeeping is having only one entry for each and

every transactions on the other hand double entry bookkeeping contains 2 entry of every

transaction one is debit side and other is credit. But on the flip side single entry bookkeeping

system uses only one account for every transaction and therefore there is no need to match debit

side and credit side of the transaction.

Trial balance

Trial balance worksheet of bookkeeping which contains balance of all the ledgers which is

being compiled into debit and credit account and both debit and credit side should be equal. The

main purpose of producing trial balance is to make sure that all the entries in the bookkeeping

system of companies are accurate and mathematically flawless.

Trial balance is very important for the organisation because it helps the management to

detect various errors by providing them information from the beginning. It also provides

background for preparing final accounts so that in the final accounts management not have to

face any fraudulent activities and transaction.

Apart from this the primary benefit of preparing trial balance is to make sure that all the

transactions was get recorded in the books of accounts and must be mentioned in the debit side

and credit side. Debit and credit amount should be matched to each other. Trial balance plays

Critical role to check the accuracy of ledger accounts organisation to prepare financial

statements. It is very important for the organisation to know that all the transactions of balance

sheet especially the Asset side should be equal and matched to the liability side.

3

important business transactions because if organisation fails to pay salary and wages to their

employees on time then they may switch to other company.

Purchase of services

Organisation need to purchase some services as well such as electricity telephone

insurance and others. This is also an important business transaction because in the absence of

these organisations can’t run effectively (Hope and et.al 2019). It is mandatory for the

organisation that they properly order and receive these services.

Single entry and double entry bookkeeping

As the name suggests single entry bookkeeping is having only one entry for each and

every transactions on the other hand double entry bookkeeping contains 2 entry of every

transaction one is debit side and other is credit. But on the flip side single entry bookkeeping

system uses only one account for every transaction and therefore there is no need to match debit

side and credit side of the transaction.

Trial balance

Trial balance worksheet of bookkeeping which contains balance of all the ledgers which is

being compiled into debit and credit account and both debit and credit side should be equal. The

main purpose of producing trial balance is to make sure that all the entries in the bookkeeping

system of companies are accurate and mathematically flawless.

Trial balance is very important for the organisation because it helps the management to

detect various errors by providing them information from the beginning. It also provides

background for preparing final accounts so that in the final accounts management not have to

face any fraudulent activities and transaction.

Apart from this the primary benefit of preparing trial balance is to make sure that all the

transactions was get recorded in the books of accounts and must be mentioned in the debit side

and credit side. Debit and credit amount should be matched to each other. Trial balance plays

Critical role to check the accuracy of ledger accounts organisation to prepare financial

statements. It is very important for the organisation to know that all the transactions of balance

sheet especially the Asset side should be equal and matched to the liability side.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

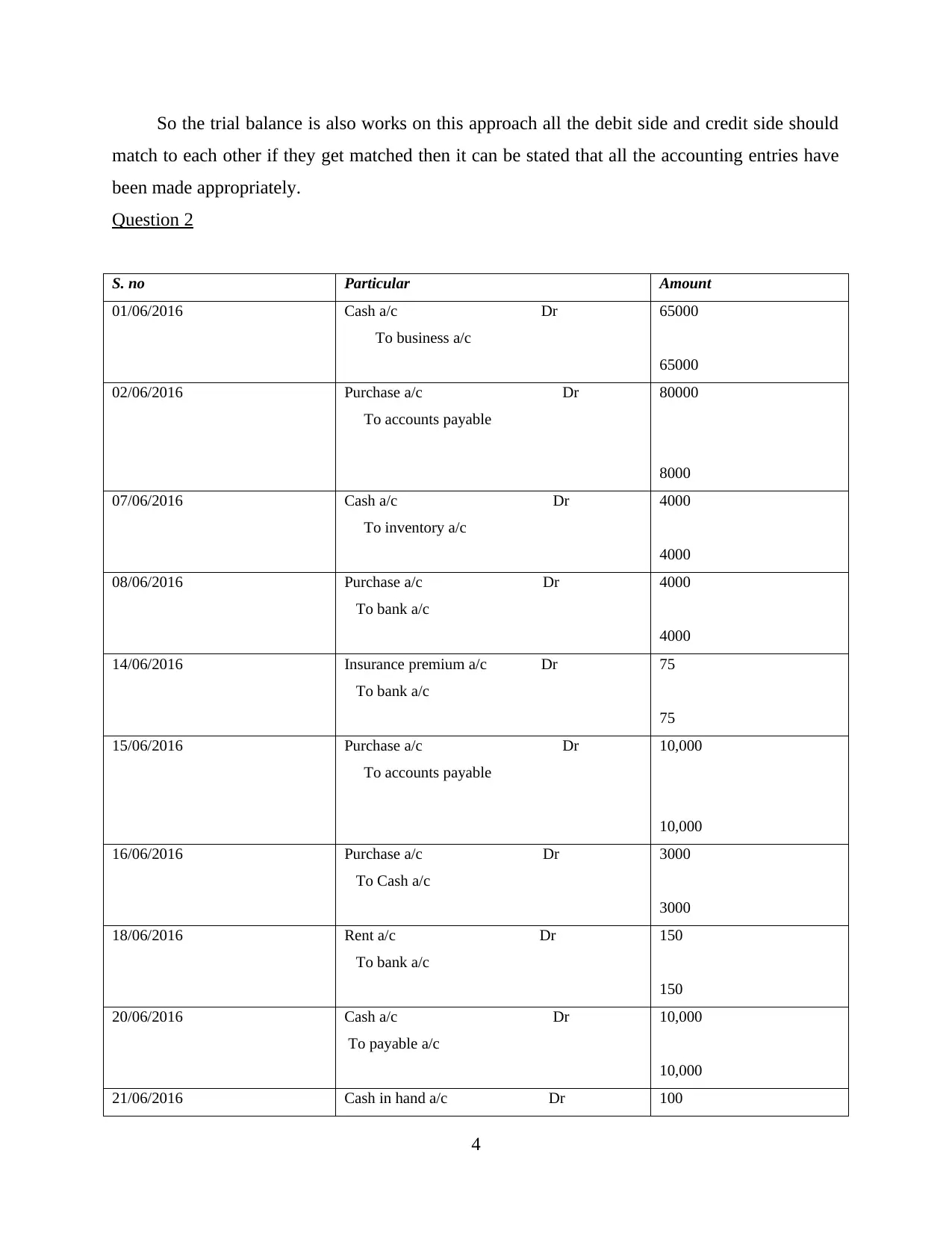

So the trial balance is also works on this approach all the debit side and credit side should

match to each other if they get matched then it can be stated that all the accounting entries have

been made appropriately.

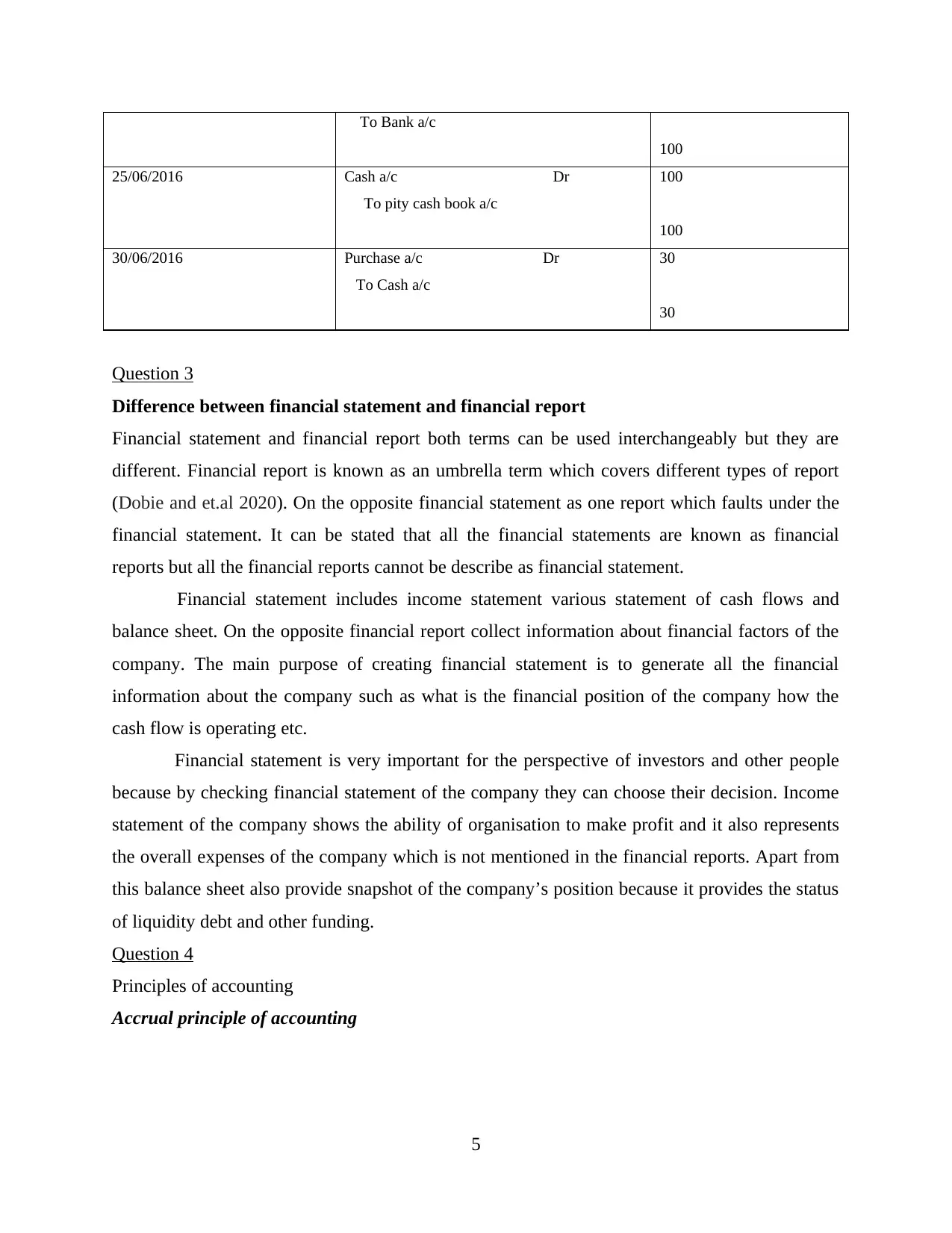

Question 2

S. no Particular Amount

01/06/2016 Cash a/c Dr

To business a/c

65000

65000

02/06/2016 Purchase a/c Dr

To accounts payable

80000

8000

07/06/2016 Cash a/c Dr

To inventory a/c

4000

4000

08/06/2016 Purchase a/c Dr

To bank a/c

4000

4000

14/06/2016 Insurance premium a/c Dr

To bank a/c

75

75

15/06/2016 Purchase a/c Dr

To accounts payable

10,000

10,000

16/06/2016 Purchase a/c Dr

To Cash a/c

3000

3000

18/06/2016 Rent a/c Dr

To bank a/c

150

150

20/06/2016 Cash a/c Dr

To payable a/c

10,000

10,000

21/06/2016 Cash in hand a/c Dr 100

4

match to each other if they get matched then it can be stated that all the accounting entries have

been made appropriately.

Question 2

S. no Particular Amount

01/06/2016 Cash a/c Dr

To business a/c

65000

65000

02/06/2016 Purchase a/c Dr

To accounts payable

80000

8000

07/06/2016 Cash a/c Dr

To inventory a/c

4000

4000

08/06/2016 Purchase a/c Dr

To bank a/c

4000

4000

14/06/2016 Insurance premium a/c Dr

To bank a/c

75

75

15/06/2016 Purchase a/c Dr

To accounts payable

10,000

10,000

16/06/2016 Purchase a/c Dr

To Cash a/c

3000

3000

18/06/2016 Rent a/c Dr

To bank a/c

150

150

20/06/2016 Cash a/c Dr

To payable a/c

10,000

10,000

21/06/2016 Cash in hand a/c Dr 100

4

To Bank a/c

100

25/06/2016 Cash a/c Dr

To pity cash book a/c

100

100

30/06/2016 Purchase a/c Dr

To Cash a/c

30

30

Question 3

Difference between financial statement and financial report

Financial statement and financial report both terms can be used interchangeably but they are

different. Financial report is known as an umbrella term which covers different types of report

(Dobie and et.al 2020). On the opposite financial statement as one report which faults under the

financial statement. It can be stated that all the financial statements are known as financial

reports but all the financial reports cannot be describe as financial statement.

Financial statement includes income statement various statement of cash flows and

balance sheet. On the opposite financial report collect information about financial factors of the

company. The main purpose of creating financial statement is to generate all the financial

information about the company such as what is the financial position of the company how the

cash flow is operating etc.

Financial statement is very important for the perspective of investors and other people

because by checking financial statement of the company they can choose their decision. Income

statement of the company shows the ability of organisation to make profit and it also represents

the overall expenses of the company which is not mentioned in the financial reports. Apart from

this balance sheet also provide snapshot of the company’s position because it provides the status

of liquidity debt and other funding.

Question 4

Principles of accounting

Accrual principle of accounting

5

100

25/06/2016 Cash a/c Dr

To pity cash book a/c

100

100

30/06/2016 Purchase a/c Dr

To Cash a/c

30

30

Question 3

Difference between financial statement and financial report

Financial statement and financial report both terms can be used interchangeably but they are

different. Financial report is known as an umbrella term which covers different types of report

(Dobie and et.al 2020). On the opposite financial statement as one report which faults under the

financial statement. It can be stated that all the financial statements are known as financial

reports but all the financial reports cannot be describe as financial statement.

Financial statement includes income statement various statement of cash flows and

balance sheet. On the opposite financial report collect information about financial factors of the

company. The main purpose of creating financial statement is to generate all the financial

information about the company such as what is the financial position of the company how the

cash flow is operating etc.

Financial statement is very important for the perspective of investors and other people

because by checking financial statement of the company they can choose their decision. Income

statement of the company shows the ability of organisation to make profit and it also represents

the overall expenses of the company which is not mentioned in the financial reports. Apart from

this balance sheet also provide snapshot of the company’s position because it provides the status

of liquidity debt and other funding.

Question 4

Principles of accounting

Accrual principle of accounting

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This principle states that all the accounting transactions of the organisation must be

recorded in the accounting period and the duration in which this transaction occurs instead of

recording them as per the cash flow statement.

This is one of the oldest form of accounting (Renes, 2020). This principle is also useful for the

financial statements because by using this principle, financial statement can provide accurate

result to the organisation.

Consistency principle

This principle represent that once an organisation adopt any accounting principle then

they should use the same principle for long. If the organisation is not following consistent

principal then it can be stated that organisation is jumping between different and various

accounting treatments it can become difficult for the organisation to can long-term result.

Cost principle

This is one of the oldest principle which emphasize night business must record all the

Asset liabilities and equity at exact purchase cost. But this principle is not popular nowadays

because it is very difficult for the organisation to adjust their asset and liabilities on the fair

value.

Going Concern principle

According to this principle business will remain for so long in the market and never stop

their operations. Every organisation has this objective that they will serve their customers for

long duration and earn profit.

Monetary unit principle

This principle of accounting emphasise that organisation must record their transactions

which can be defined in the terms of currency. It becomes easy for the organisation to calculate

all the revenues and expenses for the accounting period if the transactions are being recorded in

the units of money.

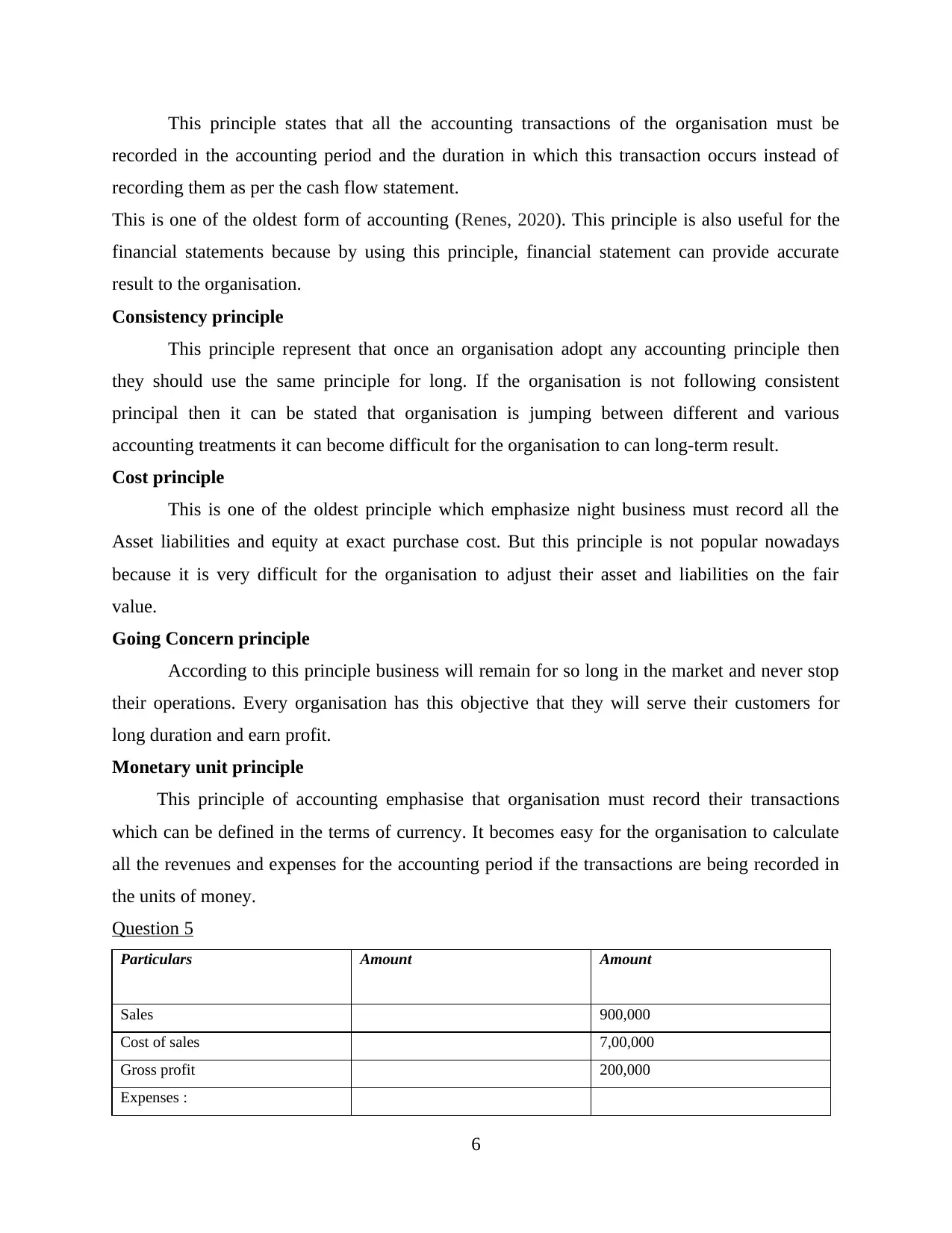

Question 5

Particulars Amount Amount

Sales 900,000

Cost of sales 7,00,000

Gross profit 200,000

Expenses :

6

recorded in the accounting period and the duration in which this transaction occurs instead of

recording them as per the cash flow statement.

This is one of the oldest form of accounting (Renes, 2020). This principle is also useful for the

financial statements because by using this principle, financial statement can provide accurate

result to the organisation.

Consistency principle

This principle represent that once an organisation adopt any accounting principle then

they should use the same principle for long. If the organisation is not following consistent

principal then it can be stated that organisation is jumping between different and various

accounting treatments it can become difficult for the organisation to can long-term result.

Cost principle

This is one of the oldest principle which emphasize night business must record all the

Asset liabilities and equity at exact purchase cost. But this principle is not popular nowadays

because it is very difficult for the organisation to adjust their asset and liabilities on the fair

value.

Going Concern principle

According to this principle business will remain for so long in the market and never stop

their operations. Every organisation has this objective that they will serve their customers for

long duration and earn profit.

Monetary unit principle

This principle of accounting emphasise that organisation must record their transactions

which can be defined in the terms of currency. It becomes easy for the organisation to calculate

all the revenues and expenses for the accounting period if the transactions are being recorded in

the units of money.

Question 5

Particulars Amount Amount

Sales 900,000

Cost of sales 7,00,000

Gross profit 200,000

Expenses :

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

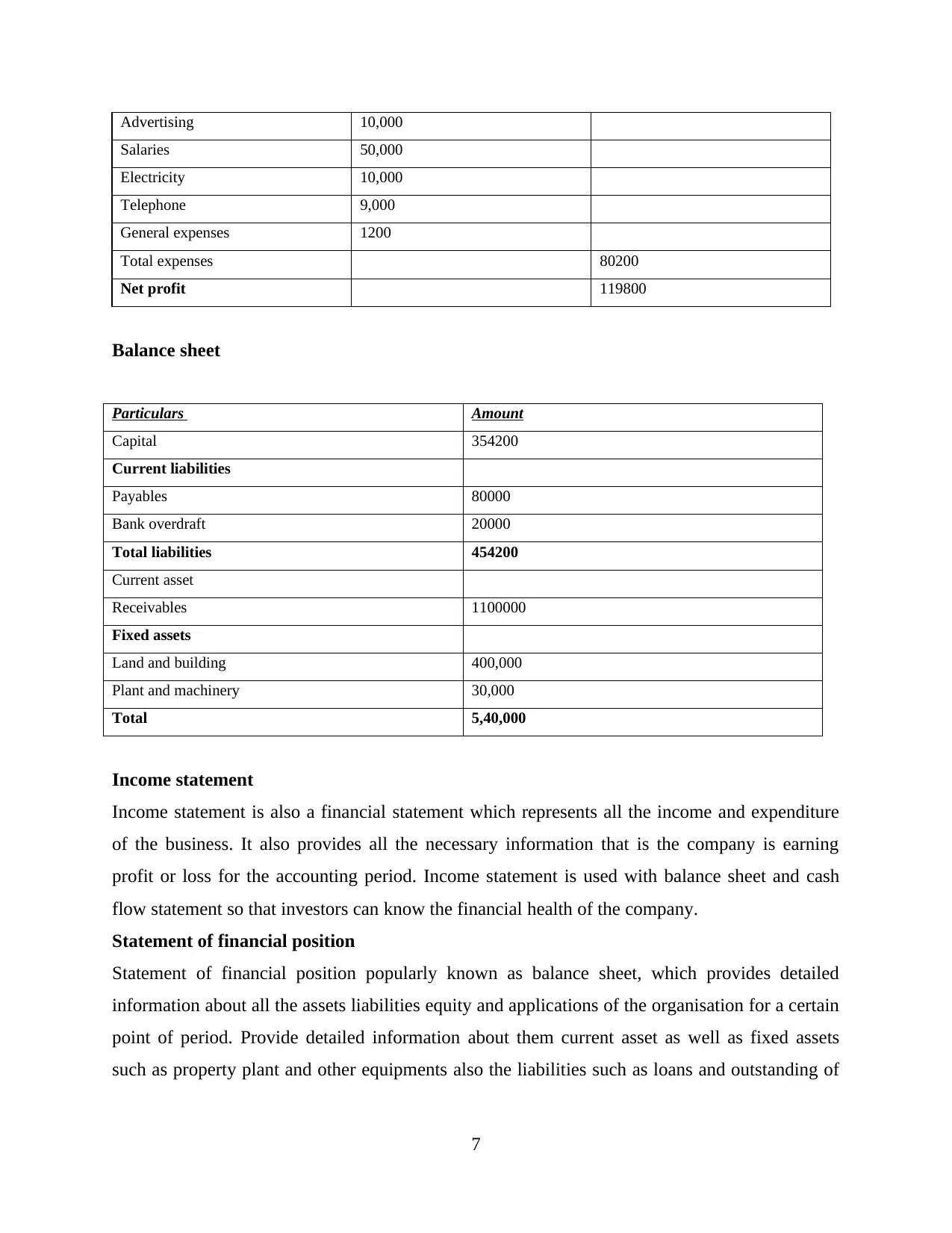

Advertising 10,000

Salaries 50,000

Electricity 10,000

Telephone 9,000

General expenses 1200

Total expenses 80200

Net profit 119800

Balance sheet

Particulars Amount

Capital 354200

Current liabilities

Payables 80000

Bank overdraft 20000

Total liabilities 454200

Current asset

Receivables 1100000

Fixed assets

Land and building 400,000

Plant and machinery 30,000

Total 5,40,000

Income statement

Income statement is also a financial statement which represents all the income and expenditure

of the business. It also provides all the necessary information that is the company is earning

profit or loss for the accounting period. Income statement is used with balance sheet and cash

flow statement so that investors can know the financial health of the company.

Statement of financial position

Statement of financial position popularly known as balance sheet, which provides detailed

information about all the assets liabilities equity and applications of the organisation for a certain

point of period. Provide detailed information about them current asset as well as fixed assets

such as property plant and other equipments also the liabilities such as loans and outstanding of

7

Salaries 50,000

Electricity 10,000

Telephone 9,000

General expenses 1200

Total expenses 80200

Net profit 119800

Balance sheet

Particulars Amount

Capital 354200

Current liabilities

Payables 80000

Bank overdraft 20000

Total liabilities 454200

Current asset

Receivables 1100000

Fixed assets

Land and building 400,000

Plant and machinery 30,000

Total 5,40,000

Income statement

Income statement is also a financial statement which represents all the income and expenditure

of the business. It also provides all the necessary information that is the company is earning

profit or loss for the accounting period. Income statement is used with balance sheet and cash

flow statement so that investors can know the financial health of the company.

Statement of financial position

Statement of financial position popularly known as balance sheet, which provides detailed

information about all the assets liabilities equity and applications of the organisation for a certain

point of period. Provide detailed information about them current asset as well as fixed assets

such as property plant and other equipments also the liabilities such as loans and outstanding of

7

the organisation. So that company can certain positions to repay their applications with the help

of assets.

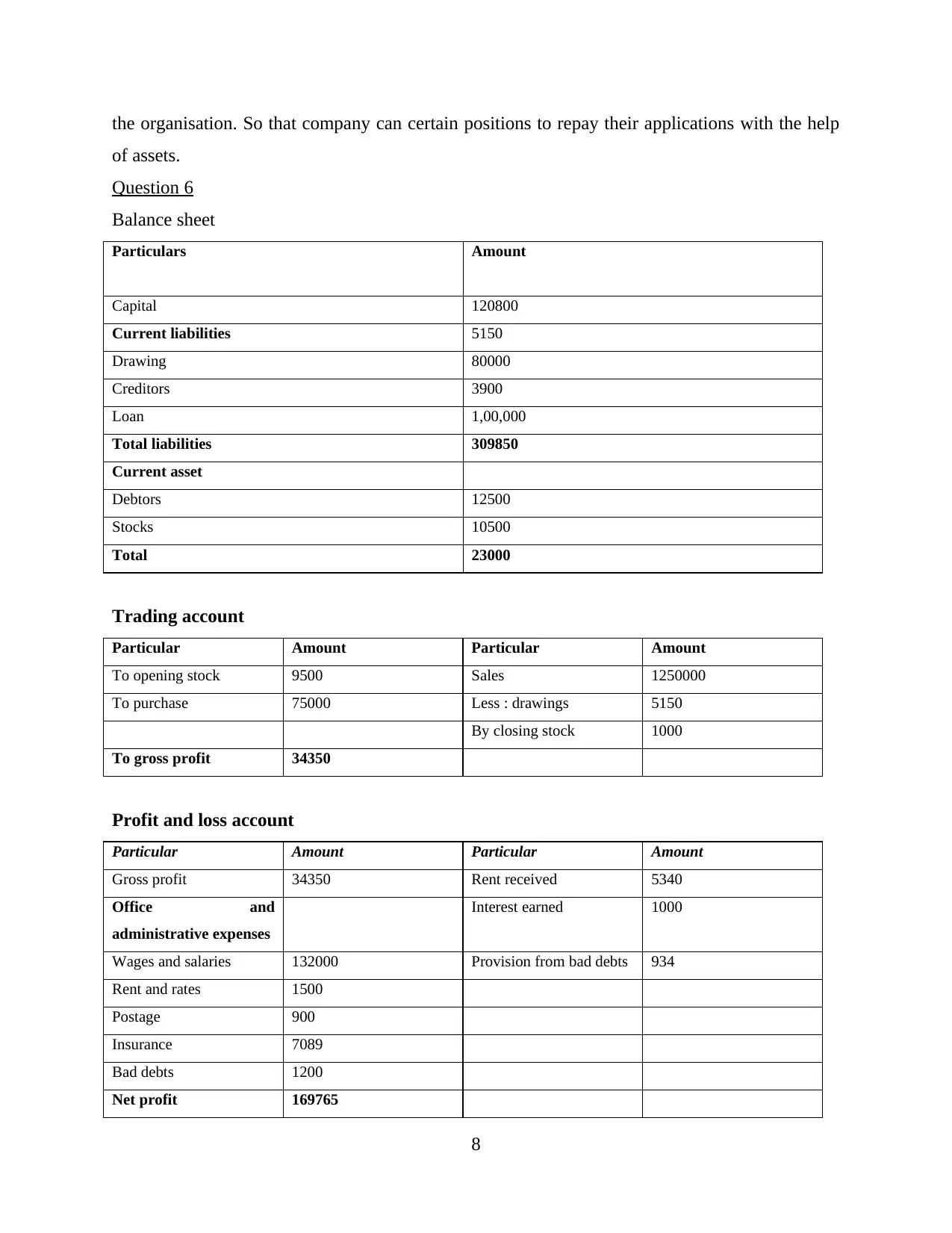

Question 6

Balance sheet

Particulars Amount

Capital 120800

Current liabilities 5150

Drawing 80000

Creditors 3900

Loan 1,00,000

Total liabilities 309850

Current asset

Debtors 12500

Stocks 10500

Total 23000

Trading account

Particular Amount Particular Amount

To opening stock 9500 Sales 1250000

To purchase 75000 Less : drawings 5150

By closing stock 1000

To gross profit 34350

Profit and loss account

Particular Amount Particular Amount

Gross profit 34350 Rent received 5340

Office and

administrative expenses

Interest earned 1000

Wages and salaries 132000 Provision from bad debts 934

Rent and rates 1500

Postage 900

Insurance 7089

Bad debts 1200

Net profit 169765

8

of assets.

Question 6

Balance sheet

Particulars Amount

Capital 120800

Current liabilities 5150

Drawing 80000

Creditors 3900

Loan 1,00,000

Total liabilities 309850

Current asset

Debtors 12500

Stocks 10500

Total 23000

Trading account

Particular Amount Particular Amount

To opening stock 9500 Sales 1250000

To purchase 75000 Less : drawings 5150

By closing stock 1000

To gross profit 34350

Profit and loss account

Particular Amount Particular Amount

Gross profit 34350 Rent received 5340

Office and

administrative expenses

Interest earned 1000

Wages and salaries 132000 Provision from bad debts 934

Rent and rates 1500

Postage 900

Insurance 7089

Bad debts 1200

Net profit 169765

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

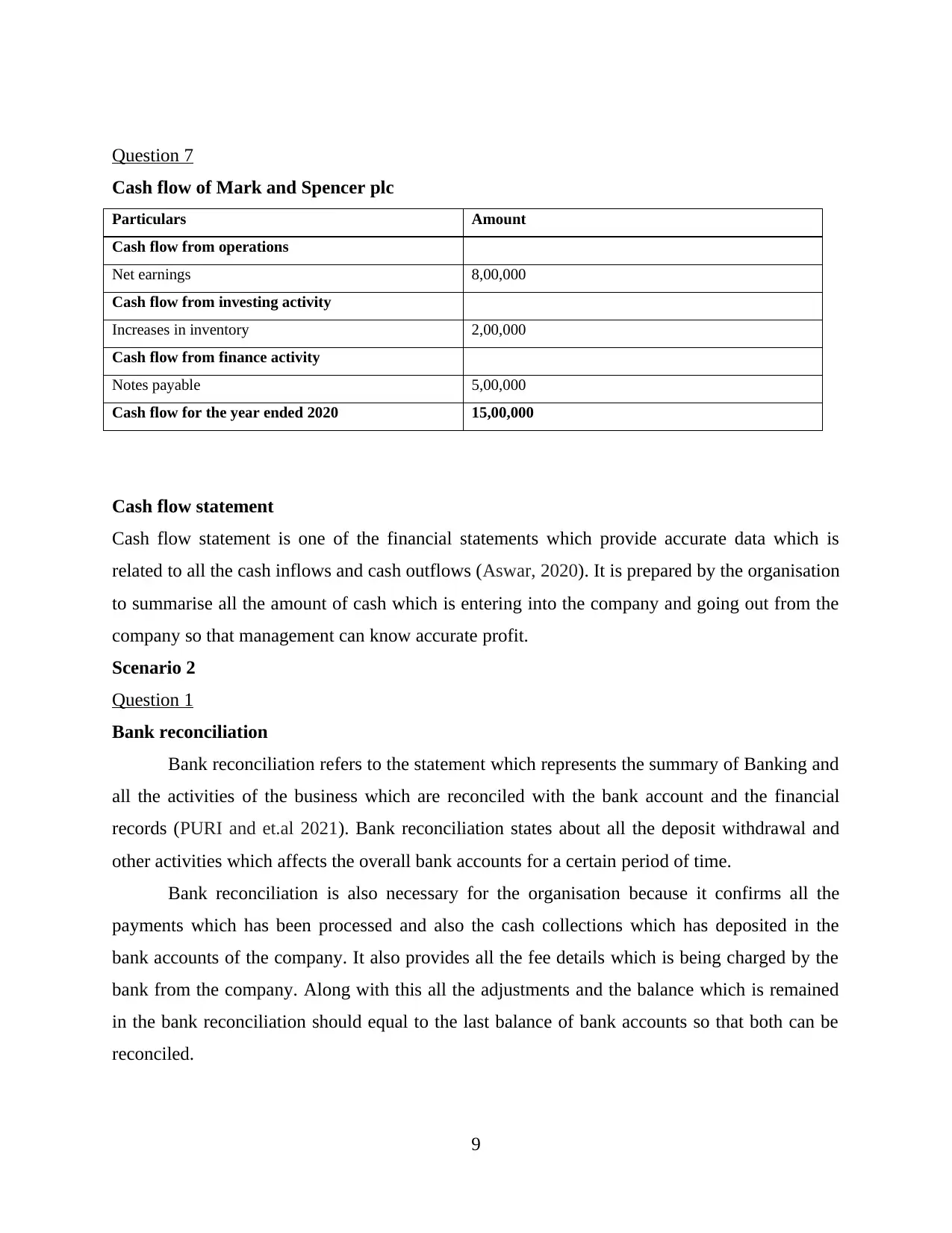

Question 7

Cash flow of Mark and Spencer plc

Particulars Amount

Cash flow from operations

Net earnings 8,00,000

Cash flow from investing activity

Increases in inventory 2,00,000

Cash flow from finance activity

Notes payable 5,00,000

Cash flow for the year ended 2020 15,00,000

Cash flow statement

Cash flow statement is one of the financial statements which provide accurate data which is

related to all the cash inflows and cash outflows (Aswar, 2020). It is prepared by the organisation

to summarise all the amount of cash which is entering into the company and going out from the

company so that management can know accurate profit.

Scenario 2

Question 1

Bank reconciliation

Bank reconciliation refers to the statement which represents the summary of Banking and

all the activities of the business which are reconciled with the bank account and the financial

records (PURI and et.al 2021). Bank reconciliation states about all the deposit withdrawal and

other activities which affects the overall bank accounts for a certain period of time.

Bank reconciliation is also necessary for the organisation because it confirms all the

payments which has been processed and also the cash collections which has deposited in the

bank accounts of the company. It also provides all the fee details which is being charged by the

bank from the company. Along with this all the adjustments and the balance which is remained

in the bank reconciliation should equal to the last balance of bank accounts so that both can be

reconciled.

9

Cash flow of Mark and Spencer plc

Particulars Amount

Cash flow from operations

Net earnings 8,00,000

Cash flow from investing activity

Increases in inventory 2,00,000

Cash flow from finance activity

Notes payable 5,00,000

Cash flow for the year ended 2020 15,00,000

Cash flow statement

Cash flow statement is one of the financial statements which provide accurate data which is

related to all the cash inflows and cash outflows (Aswar, 2020). It is prepared by the organisation

to summarise all the amount of cash which is entering into the company and going out from the

company so that management can know accurate profit.

Scenario 2

Question 1

Bank reconciliation

Bank reconciliation refers to the statement which represents the summary of Banking and

all the activities of the business which are reconciled with the bank account and the financial

records (PURI and et.al 2021). Bank reconciliation states about all the deposit withdrawal and

other activities which affects the overall bank accounts for a certain period of time.

Bank reconciliation is also necessary for the organisation because it confirms all the

payments which has been processed and also the cash collections which has deposited in the

bank accounts of the company. It also provides all the fee details which is being charged by the

bank from the company. Along with this all the adjustments and the balance which is remained

in the bank reconciliation should equal to the last balance of bank accounts so that both can be

reconciled.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To prepare accurate bank reconciliation statement it requires current and last month

statement apart from this it also required closing balance of the accounts that angry conciliation

can show exact result to the organisation. Bank reconciliation is very important because it

provides all the internal records of the company and matches such records with the statement of

bank so that discrepancies can be found.

This process is important because it can easily recognise all the fruits and accounting

mistakes. Reconciliation make sure that actual amount of money should match with the available

balance of bank account for a fiscal period. Company scan conductor conciliation on regular

intervals so that they may identify all the frauds and errors. Conciliation can take place on

monthly quarterly and yearly basis. Typically there are 2 methods suggest documentation review

and analytical review. Those businesses which are small in nature the main objective is to

reconcile the bank statement so that they can make sure all the recorded balance is matching up

with the bank balance.

Question 2

Control accounts

Control account refers to the summary account which is being prepared in the general

ledger. This account contains all the totals for each and every transaction which are individually

mentioned in the subsidiary level ledger (Azam, 2019). The main purpose of forming control

accounts is to summarise of the country symbols and account payable because these two contains

use number of transactions that is very necessary to separate them into subsidiary lasers instead

of merging them into general ledger with ample of information.

The last balance of control account should get matched with the ending total of subsidiary

ledger. If the balance of both will not get match then there is high chances that general entries in

the ledger account has not been mention accurately. Apart from this it is helpful for those who

want to check the details of account payable and account receivable then they can simply

checkout control accounts so that they may get all the necessary information.

All the transactions and activities take place in the control account on daily basis such as

all the accounts payable entered on the same day when the transaction take place and it’s also

posted summary level. But all the transactions must be mentioned in different accounts before

the closing of box and it should be maintained before the reporting period.

10

statement apart from this it also required closing balance of the accounts that angry conciliation

can show exact result to the organisation. Bank reconciliation is very important because it

provides all the internal records of the company and matches such records with the statement of

bank so that discrepancies can be found.

This process is important because it can easily recognise all the fruits and accounting

mistakes. Reconciliation make sure that actual amount of money should match with the available

balance of bank account for a fiscal period. Company scan conductor conciliation on regular

intervals so that they may identify all the frauds and errors. Conciliation can take place on

monthly quarterly and yearly basis. Typically there are 2 methods suggest documentation review

and analytical review. Those businesses which are small in nature the main objective is to

reconcile the bank statement so that they can make sure all the recorded balance is matching up

with the bank balance.

Question 2

Control accounts

Control account refers to the summary account which is being prepared in the general

ledger. This account contains all the totals for each and every transaction which are individually

mentioned in the subsidiary level ledger (Azam, 2019). The main purpose of forming control

accounts is to summarise of the country symbols and account payable because these two contains

use number of transactions that is very necessary to separate them into subsidiary lasers instead

of merging them into general ledger with ample of information.

The last balance of control account should get matched with the ending total of subsidiary

ledger. If the balance of both will not get match then there is high chances that general entries in

the ledger account has not been mention accurately. Apart from this it is helpful for those who

want to check the details of account payable and account receivable then they can simply

checkout control accounts so that they may get all the necessary information.

All the transactions and activities take place in the control account on daily basis such as

all the accounts payable entered on the same day when the transaction take place and it’s also

posted summary level. But all the transactions must be mentioned in different accounts before

the closing of box and it should be maintained before the reporting period.

10

The primary role of control account screenshot that the accuracy of subsidiary account

must be clear and sorry check the individual accounts and transactions before mentioning them

into the subsidiary ledger.

Apart from this it also provides up to date balance of each and every account on a given

time duration and therefore it is essential for the organisation to prepare control accounts.

Control accounts are kind of the general ledger accounts which summarises all the large number

of accounting transactions and therefore it is being maintained by most of the business so that

they can know their cash flow management is well and they can easily report each and every

transaction.

Question 3

Suspense account

Suspense account is a part of general ledger all the records and entries of the organisation I been

ancient improper classification and accurately (Firawati 2017). Suspense account papers to

brokerage account where investors can temporary there cash which is not getting used. Such cash

can be used to buy new investments.

Suspense account can be clear out once the discrepancies of the transaction can be find

out and the records and transactions can be shuffle to other accounts so that at the end of

accounting period organisation can get to know the accurate and exact transaction and amount as

well. Suspense account should be returned routinely check so that discrepancies can be resold

and it can be shuffle to other accounts.

Suspense account is being used by the mortgage lenders in which the borrower

accidentally make any monthly payment and if the borrower selects any kind of breakup to

monthly payment (Aisyah, and et.al 2017). The main purpose of creating suspense account is to

know the trial balance and unidentified transactions.

As the suspense account is being listed on the trial balance it is being maintained to know

the imbalance of the transactions. Another purpose of preparing suspense account is to receive

the payments which are not correctly identified whether they have received earlier or not so with

the help of suspense account such payments can be identified.

Apart from this it also helps the organisation in management to know who made the

payment the overall invoices. Along with this it is also beneficial for the organisation because

they can we check with their clients before posting any payment so that they may get to know the

11

must be clear and sorry check the individual accounts and transactions before mentioning them

into the subsidiary ledger.

Apart from this it also provides up to date balance of each and every account on a given

time duration and therefore it is essential for the organisation to prepare control accounts.

Control accounts are kind of the general ledger accounts which summarises all the large number

of accounting transactions and therefore it is being maintained by most of the business so that

they can know their cash flow management is well and they can easily report each and every

transaction.

Question 3

Suspense account

Suspense account is a part of general ledger all the records and entries of the organisation I been

ancient improper classification and accurately (Firawati 2017). Suspense account papers to

brokerage account where investors can temporary there cash which is not getting used. Such cash

can be used to buy new investments.

Suspense account can be clear out once the discrepancies of the transaction can be find

out and the records and transactions can be shuffle to other accounts so that at the end of

accounting period organisation can get to know the accurate and exact transaction and amount as

well. Suspense account should be returned routinely check so that discrepancies can be resold

and it can be shuffle to other accounts.

Suspense account is being used by the mortgage lenders in which the borrower

accidentally make any monthly payment and if the borrower selects any kind of breakup to

monthly payment (Aisyah, and et.al 2017). The main purpose of creating suspense account is to

know the trial balance and unidentified transactions.

As the suspense account is being listed on the trial balance it is being maintained to know

the imbalance of the transactions. Another purpose of preparing suspense account is to receive

the payments which are not correctly identified whether they have received earlier or not so with

the help of suspense account such payments can be identified.

Apart from this it also helps the organisation in management to know who made the

payment the overall invoices. Along with this it is also beneficial for the organisation because

they can we check with their clients before posting any payment so that they may get to know the

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.