Financial Reporting Newsletter for Financial Accounting Course

VerifiedAdded on 2022/10/11

|9

|1075

|14

Report

AI Summary

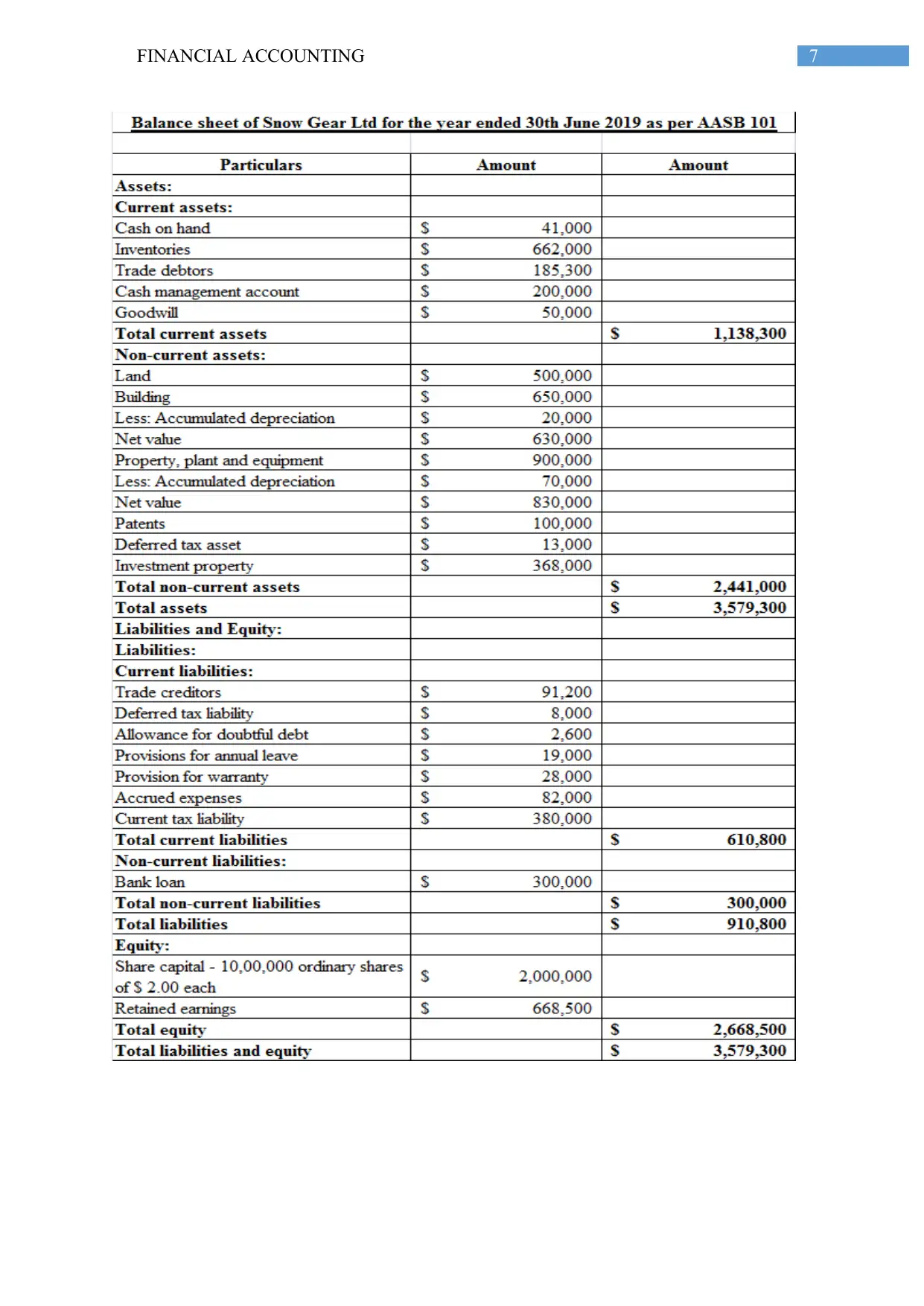

This financial reporting newsletter, prepared for accounting professionals, summarizes key developments in the financial reporting environment from April 1, 2019, to July 31, 2019. It covers significant updates, including the establishment of an independent review board by CPA Australia, annual improvements to IFRS Standards 2018-2020, amendments to AASB 112, changes to the guidance and definition of not-for-profit companies, pre-meeting summaries for the June meeting of IASB, and disclosures in special purpose financial statements. The newsletter provides concise summaries of each update, along with links to further information, enabling accounting staff to stay informed about changes in standards and their potential impact. The report also includes advice on presenting expenses in the income statement, either by nature or function, referencing relevant accounting standards such as AASB 101.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.