ACCT6003: Financial Accounting Case Study on Asset Valuation Methods

VerifiedAdded on 2022/09/14

|13

|1200

|20

Report

AI Summary

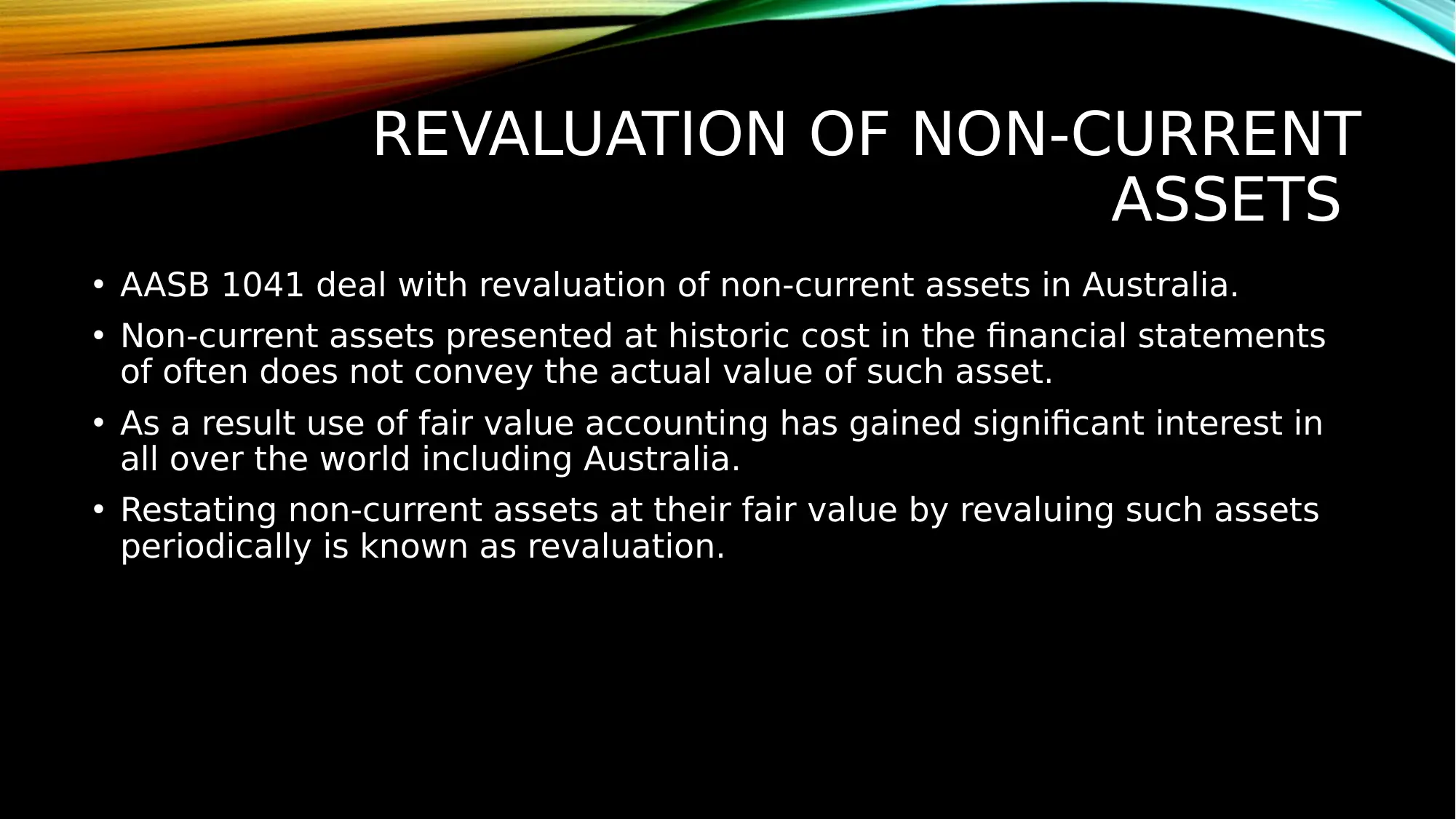

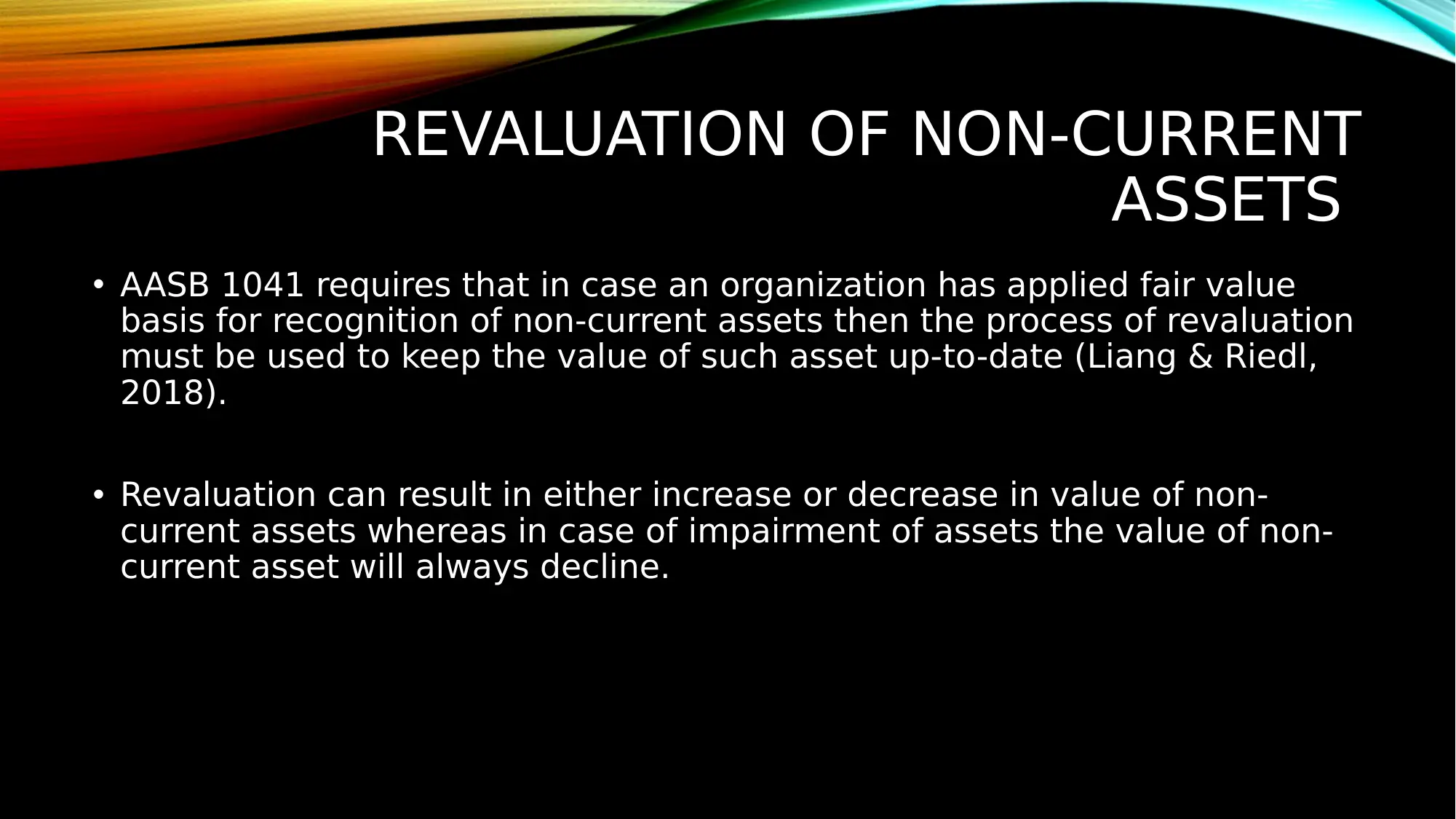

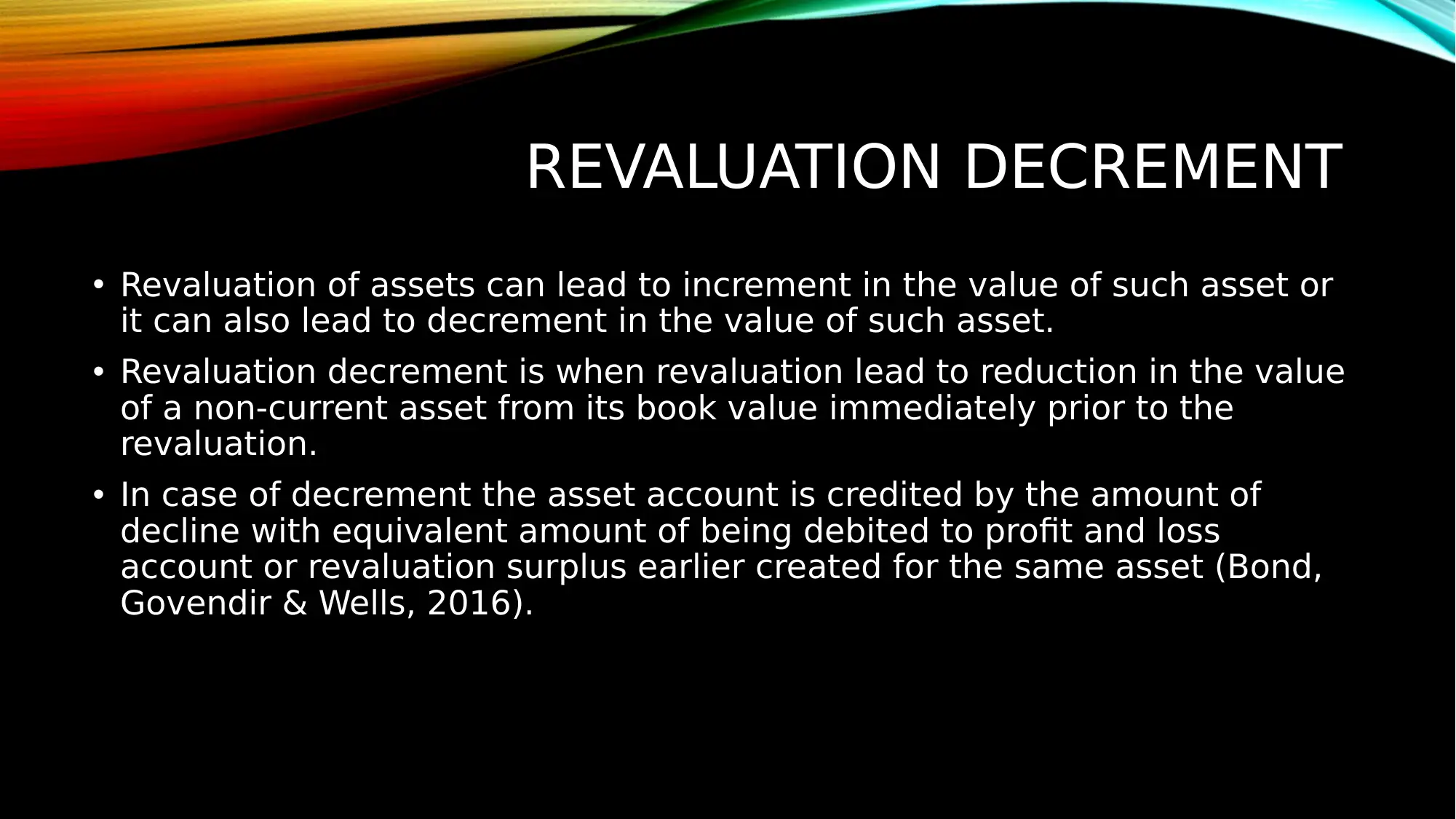

This report delves into the intricacies of accounting principles and policies, particularly focusing on the revaluation and impairment of non-current assets. It examines the application of AASB 1041 for revaluation, highlighting the shift towards fair value accounting and the concepts of revaluation increments and decrements. The report contrasts revaluation with impairment losses under AASB 136, emphasizing their distinct treatments. Furthermore, it provides a comparative analysis of the cost model and revaluation (fair value) model, discussing their implications for financial statement presentation. The report concludes with a recommendation for Jasper Ltd., suggesting the adoption of the revaluation model to ensure a true and fair representation of its financial position. The report is supported by several references to academic literature.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.