Analysis of Financial Accounting for Saracen Mineral: A Report

VerifiedAdded on 2023/04/03

|14

|3057

|359

Report

AI Summary

This report presents an evaluation of the accounting concepts, measurement issues, and qualitative criteria of financial reporting, using Saracen Mineral, an ASX-listed entity, as a case study. It demonstrates the company's adherence to standard accounting concepts, including going concern, business entity, accounting period, money measurement, accounting cost, realization, dual aspect, and accrual concepts. The analysis explores Saracen Mineral's application of a mixed model of accounting, balancing historical cost and fair value, to address measurement issues within the conceptual framework. The report examines the importance of relevance and representational faithfulness in financial information, highlighting the strengths and limitations of various measurement methods. It discusses the shift towards fair value accounting and the adoption of mixed models to maintain reliability and relevance. The report uses Saracen Mineral's financial reports to illustrate these concepts, including the application of AASB 13 for financial asset and liability valuation, providing a comprehensive overview of the company's financial reporting practices.

Advanced Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has presented an evaluation of the accounting concepts, measurement issues

and understanding of qualitative criteria of financial reporting provided by the conceptual

framework. This has been done by providing examples from a selected ASX listed entity, that is,

Saracen Mineral. It has been illustrated that the company has prepared the financial reports as per

the standard accounting concepts. Also, it has adopted a missed model of accounting for

resolving the measurement issue and also tried to attain congruence between relevance and

representational faithfulness of financial information.

2

This report has presented an evaluation of the accounting concepts, measurement issues

and understanding of qualitative criteria of financial reporting provided by the conceptual

framework. This has been done by providing examples from a selected ASX listed entity, that is,

Saracen Mineral. It has been illustrated that the company has prepared the financial reports as per

the standard accounting concepts. Also, it has adopted a missed model of accounting for

resolving the measurement issue and also tried to attain congruence between relevance and

representational faithfulness of financial information.

2

Contents

Introduction......................................................................................................................................4

Part 1: Accounting concepts description.........................................................................................4

Part 2: Measurement Issue as per the Conceptual Framework of Accounting Discussed in

Context of Selected Company.........................................................................................................6

Part 3: Understanding of Relevance and Representational Faithfulness Qualitative Characteristics

of Conceptual Accounting Framework in Context of Selected Company......................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction......................................................................................................................................4

Part 1: Accounting concepts description.........................................................................................4

Part 2: Measurement Issue as per the Conceptual Framework of Accounting Discussed in

Context of Selected Company.........................................................................................................6

Part 3: Understanding of Relevance and Representational Faithfulness Qualitative Characteristics

of Conceptual Accounting Framework in Context of Selected Company......................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The business entities across the world are required to develop their financial reports in a

manner to provide useful information to the end-users and thus meeting the varying needs of the

different stakeholder groups. As such, there has been the emergence of various contemporary

issues in accounting related to improving the quality of financial reporting systems. In this

context, this report has emphasized on the need for business entities to comply with accounting

concepts and conceptual accounting framework qualitative principles for enhancing the integrity

in their financial reports. The overall analysis has been carried out in context of a selected ASX

listed entity, that is, Saracen Mineral, an ASX listed company involved in exploration and

production of gold.

Part 1: Accounting concepts description

Methods of accounting and techniques of valuation of accounts are present in different forms. To

make the data comparable it is significant for the accountant to record the accounting

transactions with some consistency and uniformity. For maintaining uniformity and consistency,

certain principles and rules are developed by the international bodies of accounting which are

considered as accounting concepts. Basic assumptions for accounting and the guiding principles

for developing financial statements are provided by the accounting concepts (Wolk, Dodd and

Rozycki, 2016). Some significant concepts of accounting which are compulsory for the company

to follow while financial reporting are discussed below:

Going concern concept

As per this concept, the company will continue to exist for an indefinite period of time

and its liquidation can only take place if in case there is an extreme requirement to do so. Based

on this concept, the assets and liabilities values of a company are calculated. One such example

is the charging the value of plant and machinery on depreciated amount instead of treating it as

an expense in the first year (Wahlen, Baginski and Bradshaw, 2017). For example, Saracen

Mineral has depicted in its financial report that it measures the subsequent costs related with its

fixed assets in the carrying amount on the basis of probability of realizing future economic

4

The business entities across the world are required to develop their financial reports in a

manner to provide useful information to the end-users and thus meeting the varying needs of the

different stakeholder groups. As such, there has been the emergence of various contemporary

issues in accounting related to improving the quality of financial reporting systems. In this

context, this report has emphasized on the need for business entities to comply with accounting

concepts and conceptual accounting framework qualitative principles for enhancing the integrity

in their financial reports. The overall analysis has been carried out in context of a selected ASX

listed entity, that is, Saracen Mineral, an ASX listed company involved in exploration and

production of gold.

Part 1: Accounting concepts description

Methods of accounting and techniques of valuation of accounts are present in different forms. To

make the data comparable it is significant for the accountant to record the accounting

transactions with some consistency and uniformity. For maintaining uniformity and consistency,

certain principles and rules are developed by the international bodies of accounting which are

considered as accounting concepts. Basic assumptions for accounting and the guiding principles

for developing financial statements are provided by the accounting concepts (Wolk, Dodd and

Rozycki, 2016). Some significant concepts of accounting which are compulsory for the company

to follow while financial reporting are discussed below:

Going concern concept

As per this concept, the company will continue to exist for an indefinite period of time

and its liquidation can only take place if in case there is an extreme requirement to do so. Based

on this concept, the assets and liabilities values of a company are calculated. One such example

is the charging the value of plant and machinery on depreciated amount instead of treating it as

an expense in the first year (Wahlen, Baginski and Bradshaw, 2017). For example, Saracen

Mineral has depicted in its financial report that it measures the subsequent costs related with its

fixed assets in the carrying amount on the basis of probability of realizing future economic

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

benefits. Also, deprecation is charged by the use of straight-line method on the useful lives of

assets measuring that is not charged in a single reporting period but will be incurred in the future

financial periods.

Business entity concept

According to this concept, the company and its owner are two separate entities and

therefore the business and personal transactions shall be treated separately. As such, the financial

report of Saracen Mineral has represented share capital in equity section of the balance sheet

which represents that both owners and entity are treated as separately by the company(Saracen

Mineral: Annual Report, 2018).

Accounting period concept

This concept signifies that accounting transactions for a specific time period are

considered for evaluation of company’s financial performance. Also, the accounting transactions

which do not have any relation with the specific time shall be adjusted by using adjusting entries

and should not be mentioned in the balance sheet for any reference in future. Through this

concept, the company’s actual performance or a specific period of time can be evaluated as well

as the tax for specified period can also be ascertained. As such, the company has reported the

transactions such as prepaid expenses, unrealized income and other items within the balance

sheet and not in the income statement (Sadowska, 2016).

Money measurement concept

According to this concept of accounting, it is compulsory on all companies to record only

monetary transactions and in the form of currency of the nation only. For instance, if a company

is established in USA then the transaction shall be recorded in the US dollar only. Saracen

Mineral has recorded the business transactions in Australian dollar only.

Accounting cost concept

Under this concept, the assets of the company shall be recorded at cost instead of market

value. For instance, the purchase price of plant and machinery shall only include transportation,

acquisition, and cost of installation. The market value of property and equipment and plant

5

assets measuring that is not charged in a single reporting period but will be incurred in the future

financial periods.

Business entity concept

According to this concept, the company and its owner are two separate entities and

therefore the business and personal transactions shall be treated separately. As such, the financial

report of Saracen Mineral has represented share capital in equity section of the balance sheet

which represents that both owners and entity are treated as separately by the company(Saracen

Mineral: Annual Report, 2018).

Accounting period concept

This concept signifies that accounting transactions for a specific time period are

considered for evaluation of company’s financial performance. Also, the accounting transactions

which do not have any relation with the specific time shall be adjusted by using adjusting entries

and should not be mentioned in the balance sheet for any reference in future. Through this

concept, the company’s actual performance or a specific period of time can be evaluated as well

as the tax for specified period can also be ascertained. As such, the company has reported the

transactions such as prepaid expenses, unrealized income and other items within the balance

sheet and not in the income statement (Sadowska, 2016).

Money measurement concept

According to this concept of accounting, it is compulsory on all companies to record only

monetary transactions and in the form of currency of the nation only. For instance, if a company

is established in USA then the transaction shall be recorded in the US dollar only. Saracen

Mineral has recorded the business transactions in Australian dollar only.

Accounting cost concept

Under this concept, the assets of the company shall be recorded at cost instead of market

value. For instance, the purchase price of plant and machinery shall only include transportation,

acquisition, and cost of installation. The market value of property and equipment and plant

5

cannot be recorded by the company in the balance sheet (Needles, Powers and Crosson, 2013).

As such, Saracen Mineral has recorded its buildings, plant and machinery on the cost basis with

the deduction of deprecation or amortization.

Realization concept

As per this concept, the company, Saracen Mineral, has recorded revenue in the books of

accounts post its realization instead of recording it at the time of transaction(Saracen Mineral:

Annual Report, 2018). The legal right for receiving the money is known as realization. For

instance, the goods sold are money realization but the receiving the orders cannot be considered

as realization.

Dual aspect concept

This can be known as complete process of accounting. As per this concept, two accounts

shall be impacted when a transaction takes place. This means that for every transaction, entries

shall be made in two different accounts (Wahlen, Baginski and Bradshaw, 2017). One account

will be debited and other will be credited. This concept is applied by Saracen Mineral in

recording of all its financial transactions including those for income, assets, expenses, liabilities

or any other account(Saracen Mineral: Annual Report, 2018).

Accrual concept

As per the concept, Saracen Mineral has accrued all the expenses and revenues which do

not have any significance in the current period and are outstanding in the current time period.

This concept is helpful in maintaining balance in the accounting books and also aid in recording

the financial transactions that have significance only for the current financial period (Mirza and

Knorr, 2011).

Part 2: Measurement Issue as per the Conceptual Framework of

Accounting Discussed in Context of Selected Company

The measurement method used in financial reporting have a large impact on the type of

financial information disclosed within the financial statements that is made available to the end-

users. The conceptual accounting framework has generally provided two major methods to be

6

As such, Saracen Mineral has recorded its buildings, plant and machinery on the cost basis with

the deduction of deprecation or amortization.

Realization concept

As per this concept, the company, Saracen Mineral, has recorded revenue in the books of

accounts post its realization instead of recording it at the time of transaction(Saracen Mineral:

Annual Report, 2018). The legal right for receiving the money is known as realization. For

instance, the goods sold are money realization but the receiving the orders cannot be considered

as realization.

Dual aspect concept

This can be known as complete process of accounting. As per this concept, two accounts

shall be impacted when a transaction takes place. This means that for every transaction, entries

shall be made in two different accounts (Wahlen, Baginski and Bradshaw, 2017). One account

will be debited and other will be credited. This concept is applied by Saracen Mineral in

recording of all its financial transactions including those for income, assets, expenses, liabilities

or any other account(Saracen Mineral: Annual Report, 2018).

Accrual concept

As per the concept, Saracen Mineral has accrued all the expenses and revenues which do

not have any significance in the current period and are outstanding in the current time period.

This concept is helpful in maintaining balance in the accounting books and also aid in recording

the financial transactions that have significance only for the current financial period (Mirza and

Knorr, 2011).

Part 2: Measurement Issue as per the Conceptual Framework of

Accounting Discussed in Context of Selected Company

The measurement method used in financial reporting have a large impact on the type of

financial information disclosed within the financial statements that is made available to the end-

users. The conceptual accounting framework has generally provided two major methods to be

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sued during measurement of financial items such as assets and liabilities. These are historical

cost and fair value basis that has been provided by the accounting framework to be used for

identification, recognition and measuring of monetary values of different financial items

(International Accounting Standards Board, 2016). The decision taken by the preparers of

accounting statements regarding the measurement approach is dependent on the perceived costs

and benefits of different measurement bases. The use of mixed measurement approach for

measuring the value of different financial items has resulted in causing the problem related to

lack of consistency within the financial reports. This is because certain items are measured at fair

values and others at historical cost which can result in making the financial information less

comparable over the subsequent years (ICAEW, 2016). Also, the financial information lacks

comparability in case of competitors due to difference in measurement basis selected by them.

Thus, it can be said that selection of an adequate method of measurement to be used in

developing the financial reports is a key issue for business entities. The business entities tend to

differ from each other on basis of type of industry, ownership and governance structure. This

result in causing variability among the measurement approaches selected by different business

entities for financial reporting and makes the information less comparable (IFRS, 2017).

The measurement methods used in financial reporting as provided by the conceptual

accounting framework are associated with different strengths and limitations. The selection of

measurement approach is dependent on the legitimacy theory of accounting which has stated that

businesses need to disclose financial information in a regular manner for ensuring relevance and

reliability of the resulting measurements (Yip and Young, 2012). This is required to ensure that

businesses provide legitimate information to the end-users that is both relevance for some

purpose and reliable in other situations. This leads to improving legitimacy in the financial

reporting and thus protecting the interests of the end-users. The current measurement practices

provided by the conceptual framework are rather complex, diverse and inconsistent. As such,

there is increasing need for development of a single set of accounting standards to be used for

measurement during financial reporting to overcome the issue of inconsistency and uniformity in

reporting the value of different financial assets and liabilities (Anwer, Neel and Wang, 2013).

The accountants are gradually shifting from the use of traditional basis of measurement used,

that is, historical cost, towards the adoption of fair value measure of accounting. This is mainly

due to the limitations of historical cost basis for depicting actual profits or expenses incurred by

7

cost and fair value basis that has been provided by the accounting framework to be used for

identification, recognition and measuring of monetary values of different financial items

(International Accounting Standards Board, 2016). The decision taken by the preparers of

accounting statements regarding the measurement approach is dependent on the perceived costs

and benefits of different measurement bases. The use of mixed measurement approach for

measuring the value of different financial items has resulted in causing the problem related to

lack of consistency within the financial reports. This is because certain items are measured at fair

values and others at historical cost which can result in making the financial information less

comparable over the subsequent years (ICAEW, 2016). Also, the financial information lacks

comparability in case of competitors due to difference in measurement basis selected by them.

Thus, it can be said that selection of an adequate method of measurement to be used in

developing the financial reports is a key issue for business entities. The business entities tend to

differ from each other on basis of type of industry, ownership and governance structure. This

result in causing variability among the measurement approaches selected by different business

entities for financial reporting and makes the information less comparable (IFRS, 2017).

The measurement methods used in financial reporting as provided by the conceptual

accounting framework are associated with different strengths and limitations. The selection of

measurement approach is dependent on the legitimacy theory of accounting which has stated that

businesses need to disclose financial information in a regular manner for ensuring relevance and

reliability of the resulting measurements (Yip and Young, 2012). This is required to ensure that

businesses provide legitimate information to the end-users that is both relevance for some

purpose and reliable in other situations. This leads to improving legitimacy in the financial

reporting and thus protecting the interests of the end-users. The current measurement practices

provided by the conceptual framework are rather complex, diverse and inconsistent. As such,

there is increasing need for development of a single set of accounting standards to be used for

measurement during financial reporting to overcome the issue of inconsistency and uniformity in

reporting the value of different financial assets and liabilities (Anwer, Neel and Wang, 2013).

The accountants are gradually shifting from the use of traditional basis of measurement used,

that is, historical cost, towards the adoption of fair value measure of accounting. This is mainly

due to the limitations of historical cost basis for depicting actual profits or expenses incurred by

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

an entity over a selected time-period (Riedl, 2010). The method is not appropriate for providing

relevant information to the end-users as it is mainly based on measuring and interpreting the past

financial information. As such, the method fails to provide a depiction of the future cash flow

position of an entity and therefore not very useful for the end-users (Yuan and Brown, 2014).

This is causing the shift towards the use of fair value method of accounting which

provides a depiction of the actual value of assets and liabilities as per the active market. It

provides relevant information to the users that are able to provide an estimation of the future

financial performance of an entity on the basis of current market price of assets and liabilities.

However, the method of fair value of accounting is also associated with significant limitations as

has been illustrated during the occurrence of global financial crisis (Taplin, 2011). The method

of fair value accounting fails to depict the actual value of assets and liabilities during the

conditions of market volatility. The fluctuations in the market conditions can result in

manipulating the fair value of assets and liabilities and therefore inaccurate depiction of the

financial position of an entity that has resulted in causing the occurrence of global breakdown of

financial system during the time of financial crisis. Therefore, this has resulted in causing the

need for development of a unified system of measurement that records the value of assets and

liabilities in both reliable and relevant manner (Kythreotis, 2014).

At present, the developers are integrating the use of mixed model of accounting that is

integrating the use of historical method for financial items whose active market is not present

and fair value for the financial items that have the presence of active market. This is necessary

for maintaining reliability and relevancy in the financial reports. The same can be illustrated

from the financial reports of the selected company that is Saracen Mineral. The company has

accounted fixed assets such as building, plant and equipment at the historical cost which includes

expenses that are incurred during the acquisition of financial items. This is largely due to

inability to determine their fair value in the absence of their market. On the other hand, the

significant financial items such as ordinary share capital, financial assets and liabilities. The

items of income statement such as expenses and gains are realized at fair value less costs of

selling an asset (Saracen Mineral: Annual Report, 2018). The fair value system of measurement

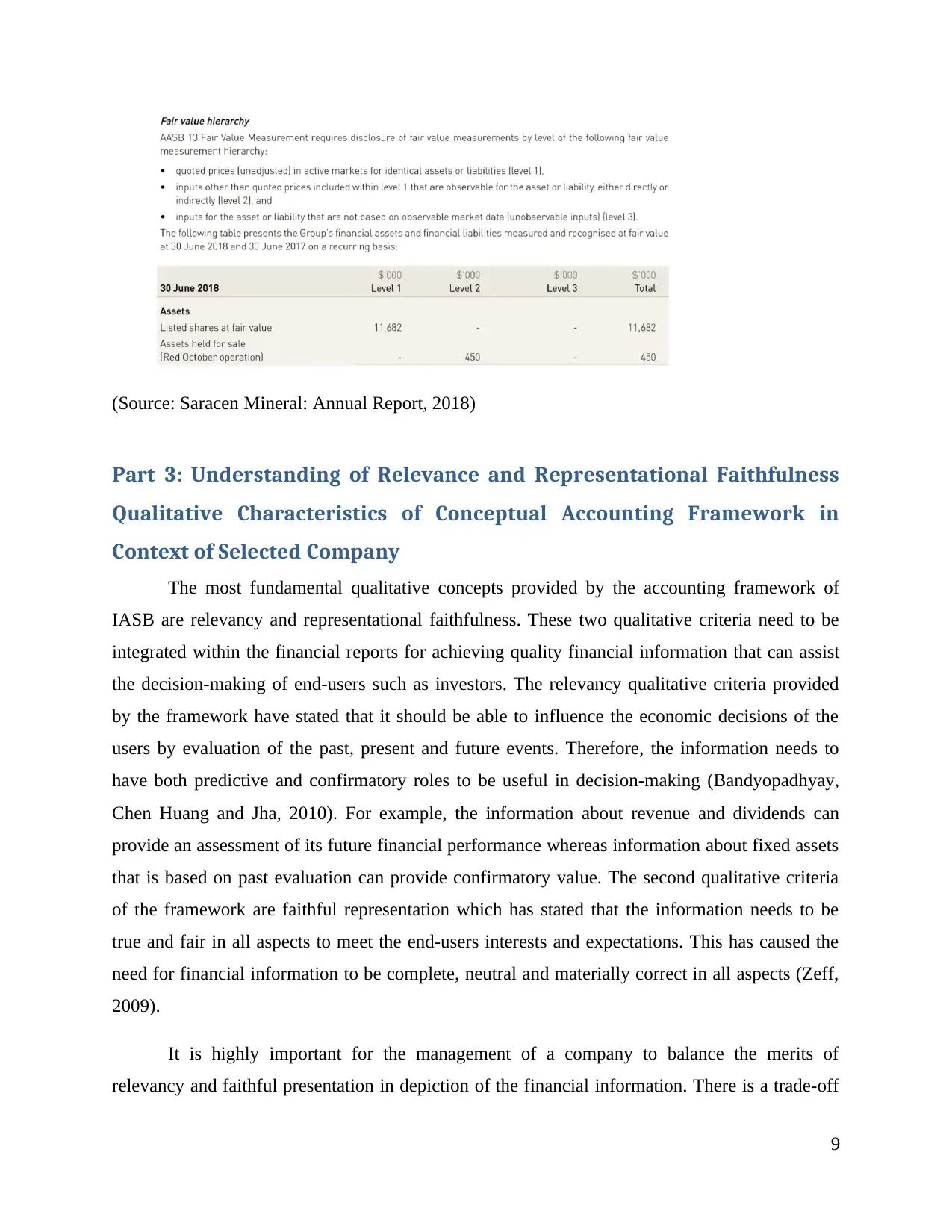

has been applied as per the AASB 13 accounting standard for reporting the financial assets and

liabilities value as depicted below:

8

relevant information to the end-users as it is mainly based on measuring and interpreting the past

financial information. As such, the method fails to provide a depiction of the future cash flow

position of an entity and therefore not very useful for the end-users (Yuan and Brown, 2014).

This is causing the shift towards the use of fair value method of accounting which

provides a depiction of the actual value of assets and liabilities as per the active market. It

provides relevant information to the users that are able to provide an estimation of the future

financial performance of an entity on the basis of current market price of assets and liabilities.

However, the method of fair value of accounting is also associated with significant limitations as

has been illustrated during the occurrence of global financial crisis (Taplin, 2011). The method

of fair value accounting fails to depict the actual value of assets and liabilities during the

conditions of market volatility. The fluctuations in the market conditions can result in

manipulating the fair value of assets and liabilities and therefore inaccurate depiction of the

financial position of an entity that has resulted in causing the occurrence of global breakdown of

financial system during the time of financial crisis. Therefore, this has resulted in causing the

need for development of a unified system of measurement that records the value of assets and

liabilities in both reliable and relevant manner (Kythreotis, 2014).

At present, the developers are integrating the use of mixed model of accounting that is

integrating the use of historical method for financial items whose active market is not present

and fair value for the financial items that have the presence of active market. This is necessary

for maintaining reliability and relevancy in the financial reports. The same can be illustrated

from the financial reports of the selected company that is Saracen Mineral. The company has

accounted fixed assets such as building, plant and equipment at the historical cost which includes

expenses that are incurred during the acquisition of financial items. This is largely due to

inability to determine their fair value in the absence of their market. On the other hand, the

significant financial items such as ordinary share capital, financial assets and liabilities. The

items of income statement such as expenses and gains are realized at fair value less costs of

selling an asset (Saracen Mineral: Annual Report, 2018). The fair value system of measurement

has been applied as per the AASB 13 accounting standard for reporting the financial assets and

liabilities value as depicted below:

8

(Source: Saracen Mineral: Annual Report, 2018)

Part 3: Understanding of Relevance and Representational Faithfulness

Qualitative Characteristics of Conceptual Accounting Framework in

Context of Selected Company

The most fundamental qualitative concepts provided by the accounting framework of

IASB are relevancy and representational faithfulness. These two qualitative criteria need to be

integrated within the financial reports for achieving quality financial information that can assist

the decision-making of end-users such as investors. The relevancy qualitative criteria provided

by the framework have stated that it should be able to influence the economic decisions of the

users by evaluation of the past, present and future events. Therefore, the information needs to

have both predictive and confirmatory roles to be useful in decision-making (Bandyopadhyay,

Chen Huang and Jha, 2010). For example, the information about revenue and dividends can

provide an assessment of its future financial performance whereas information about fixed assets

that is based on past evaluation can provide confirmatory value. The second qualitative criteria

of the framework are faithful representation which has stated that the information needs to be

true and fair in all aspects to meet the end-users interests and expectations. This has caused the

need for financial information to be complete, neutral and materially correct in all aspects (Zeff,

2009).

It is highly important for the management of a company to balance the merits of

relevancy and faithful presentation in depiction of the financial information. There is a trade-off

9

Part 3: Understanding of Relevance and Representational Faithfulness

Qualitative Characteristics of Conceptual Accounting Framework in

Context of Selected Company

The most fundamental qualitative concepts provided by the accounting framework of

IASB are relevancy and representational faithfulness. These two qualitative criteria need to be

integrated within the financial reports for achieving quality financial information that can assist

the decision-making of end-users such as investors. The relevancy qualitative criteria provided

by the framework have stated that it should be able to influence the economic decisions of the

users by evaluation of the past, present and future events. Therefore, the information needs to

have both predictive and confirmatory roles to be useful in decision-making (Bandyopadhyay,

Chen Huang and Jha, 2010). For example, the information about revenue and dividends can

provide an assessment of its future financial performance whereas information about fixed assets

that is based on past evaluation can provide confirmatory value. The second qualitative criteria

of the framework are faithful representation which has stated that the information needs to be

true and fair in all aspects to meet the end-users interests and expectations. This has caused the

need for financial information to be complete, neutral and materially correct in all aspects (Zeff,

2009).

It is highly important for the management of a company to balance the merits of

relevancy and faithful presentation in depiction of the financial information. There is a trade-off

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between the two qualitative criteria’s provided by the conceptual framework that requires that

information should be reliable in some aspects and relevant in others. This is because increasing

reliability of information can result in undermining its relevancy and vice-versa (Anwer, Neel

and Wang, 2013). For example, the use of fair value method of accounting can result in making

financial information to be more relevant whereas historical method of accounting will make it

more reliable. Therefore, it is necessary to achieve a trade-off between the qualitative

characteristics for meeting the objective of financial statement preparation. The importance of

one concept over another cannot be stated as both are important in ensuring that the needs and

expectations of different users are adequately met. The accountants are therefore integrating the

use of mixed method approach that ensures the presence of both relevance and faithful

presentation within the financial information (Horton and Serafeim, 2010).

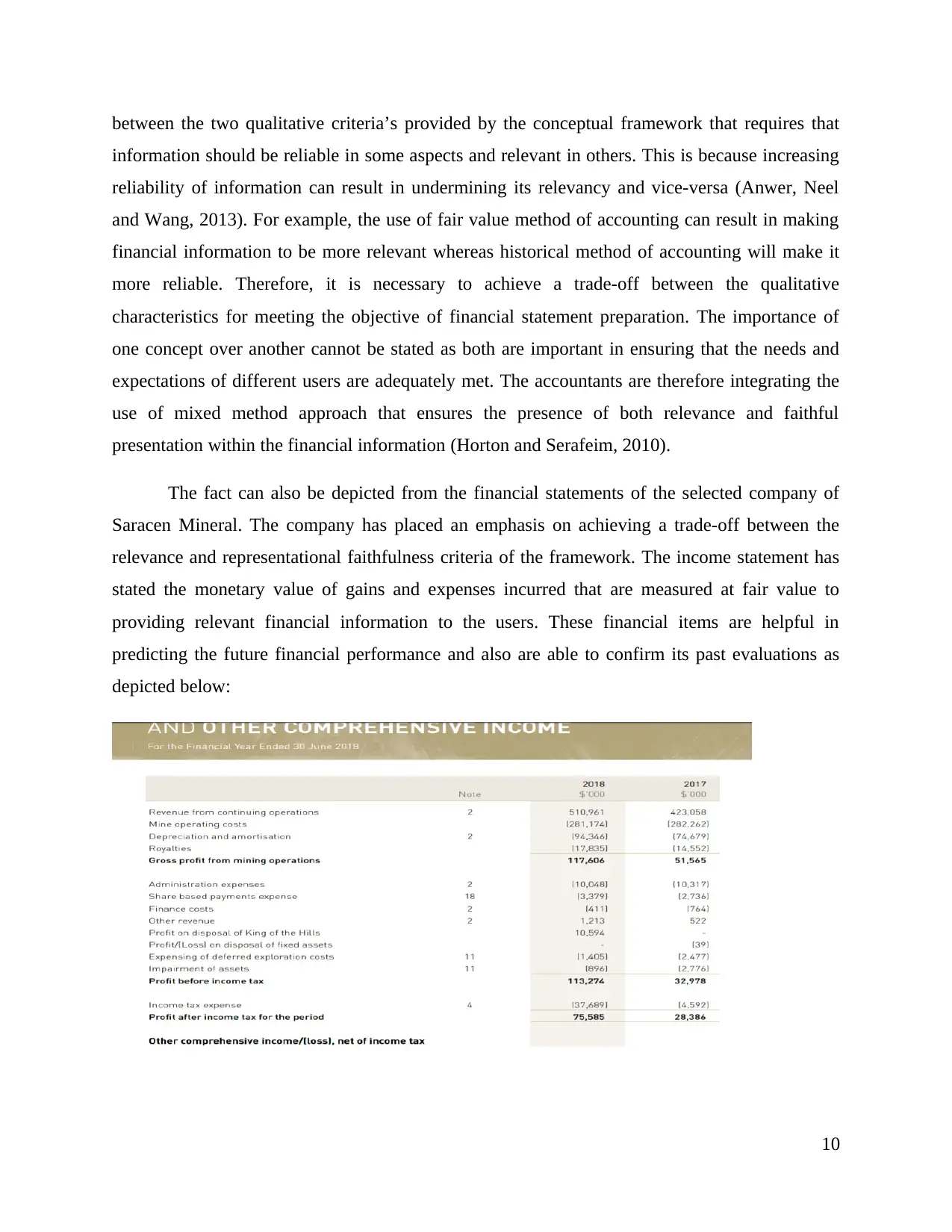

The fact can also be depicted from the financial statements of the selected company of

Saracen Mineral. The company has placed an emphasis on achieving a trade-off between the

relevance and representational faithfulness criteria of the framework. The income statement has

stated the monetary value of gains and expenses incurred that are measured at fair value to

providing relevant financial information to the users. These financial items are helpful in

predicting the future financial performance and also are able to confirm its past evaluations as

depicted below:

10

information should be reliable in some aspects and relevant in others. This is because increasing

reliability of information can result in undermining its relevancy and vice-versa (Anwer, Neel

and Wang, 2013). For example, the use of fair value method of accounting can result in making

financial information to be more relevant whereas historical method of accounting will make it

more reliable. Therefore, it is necessary to achieve a trade-off between the qualitative

characteristics for meeting the objective of financial statement preparation. The importance of

one concept over another cannot be stated as both are important in ensuring that the needs and

expectations of different users are adequately met. The accountants are therefore integrating the

use of mixed method approach that ensures the presence of both relevance and faithful

presentation within the financial information (Horton and Serafeim, 2010).

The fact can also be depicted from the financial statements of the selected company of

Saracen Mineral. The company has placed an emphasis on achieving a trade-off between the

relevance and representational faithfulness criteria of the framework. The income statement has

stated the monetary value of gains and expenses incurred that are measured at fair value to

providing relevant financial information to the users. These financial items are helpful in

predicting the future financial performance and also are able to confirm its past evaluations as

depicted below:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

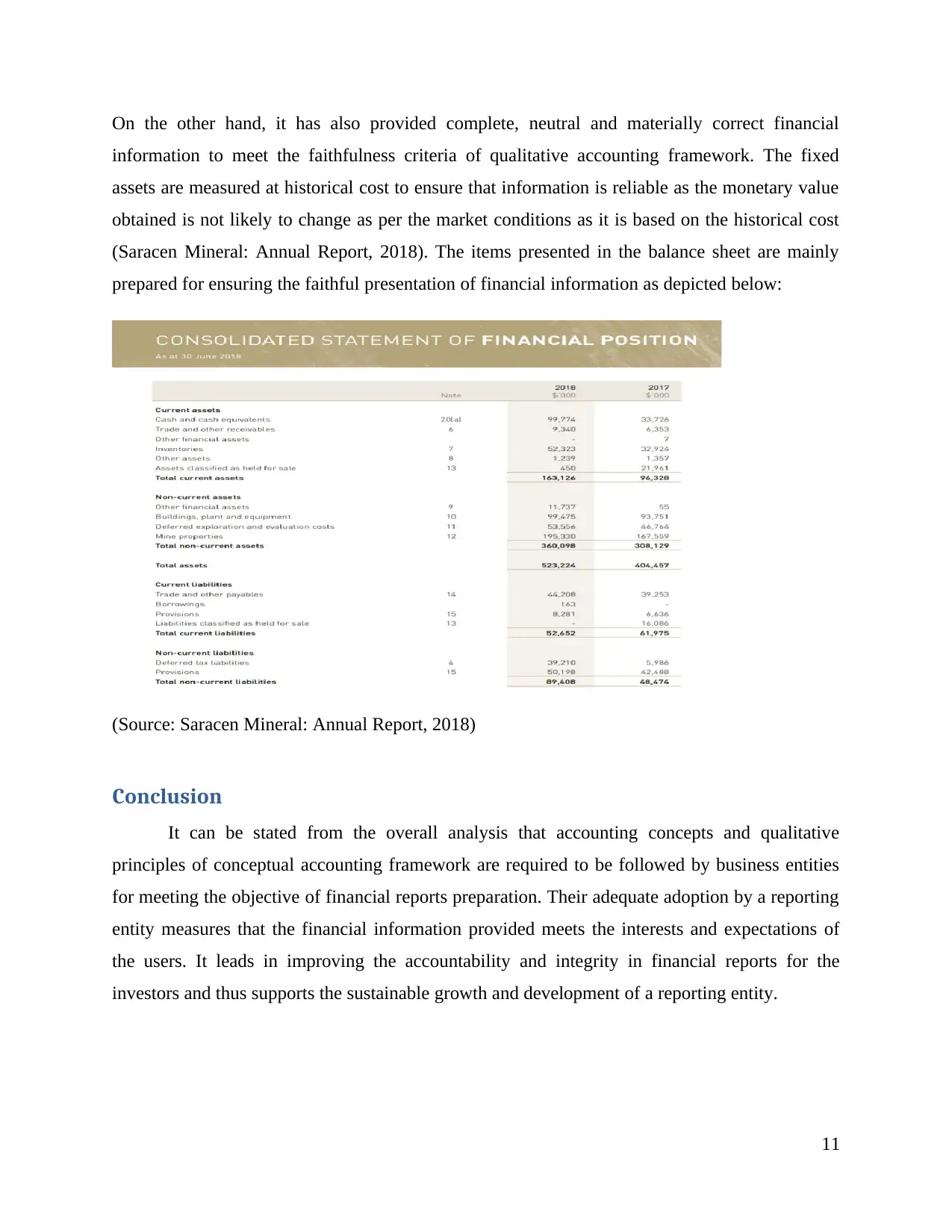

On the other hand, it has also provided complete, neutral and materially correct financial

information to meet the faithfulness criteria of qualitative accounting framework. The fixed

assets are measured at historical cost to ensure that information is reliable as the monetary value

obtained is not likely to change as per the market conditions as it is based on the historical cost

(Saracen Mineral: Annual Report, 2018). The items presented in the balance sheet are mainly

prepared for ensuring the faithful presentation of financial information as depicted below:

(Source: Saracen Mineral: Annual Report, 2018)

Conclusion

It can be stated from the overall analysis that accounting concepts and qualitative

principles of conceptual accounting framework are required to be followed by business entities

for meeting the objective of financial reports preparation. Their adequate adoption by a reporting

entity measures that the financial information provided meets the interests and expectations of

the users. It leads in improving the accountability and integrity in financial reports for the

investors and thus supports the sustainable growth and development of a reporting entity.

11

information to meet the faithfulness criteria of qualitative accounting framework. The fixed

assets are measured at historical cost to ensure that information is reliable as the monetary value

obtained is not likely to change as per the market conditions as it is based on the historical cost

(Saracen Mineral: Annual Report, 2018). The items presented in the balance sheet are mainly

prepared for ensuring the faithful presentation of financial information as depicted below:

(Source: Saracen Mineral: Annual Report, 2018)

Conclusion

It can be stated from the overall analysis that accounting concepts and qualitative

principles of conceptual accounting framework are required to be followed by business entities

for meeting the objective of financial reports preparation. Their adequate adoption by a reporting

entity measures that the financial information provided meets the interests and expectations of

the users. It leads in improving the accountability and integrity in financial reports for the

investors and thus supports the sustainable growth and development of a reporting entity.

11

References

Anwer S. A., Neel, M. and Wang, D. 2013. Does Mandatory Adoption of IFRS improve

Accounting Quality? Preliminary Evidence. Contemporary Accounting Research 30 (4), pp.

1344–1372.

Bandyopadhyay, S., Chen, C., Huang, A. and Jha, R. 2010. Accounting Conservatism and the

Temporal Trends in Current Earnings’ Ability to Predict Future Cash Flows Versus Future

Earnings: Evidence on the Trade-Off Between Relevance and Reliability. Contemporary

Accounting Research, 27 (2), pp. 413-460.

Horton, J. and Serafeim, G. 2010. Market Reaction to and Valuation of IFRS Reconciliation

Adjustments: First Evidence from the UK. Review of Accounting Studies 15 (4), pp. 725-751.

ICAEW. 2016. Measurement in financial reporting. [Online]. Available at:

https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-

better-markets/ifbm-reports/measurement-in-financial-reporting.ashx [Accessed on: 31 May

2018].

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 31 May 2019].

International Accounting Standards Board. 2016. Measurement Bases for Financial Accounting.

[Online]. Available at: https://www.efrag.org/Assets/Download?assetUrl=%2Fsites

%2Fwebpublishing%2FProject%20Documents%2F53%2FDP%20Measurement%20on

%20Initial%20Recognition.pdf [Accessed on: 31 May 2018].

Kythreotis, A. 2014. Measurement Of Financial Reporting Quality Based On IFRS Conceptual

Framework’s Fundamental Qualitative Characteristics. European Journal of Accounting,

Finance & Business, 2(3), pp. 4-29.

12

Anwer S. A., Neel, M. and Wang, D. 2013. Does Mandatory Adoption of IFRS improve

Accounting Quality? Preliminary Evidence. Contemporary Accounting Research 30 (4), pp.

1344–1372.

Bandyopadhyay, S., Chen, C., Huang, A. and Jha, R. 2010. Accounting Conservatism and the

Temporal Trends in Current Earnings’ Ability to Predict Future Cash Flows Versus Future

Earnings: Evidence on the Trade-Off Between Relevance and Reliability. Contemporary

Accounting Research, 27 (2), pp. 413-460.

Horton, J. and Serafeim, G. 2010. Market Reaction to and Valuation of IFRS Reconciliation

Adjustments: First Evidence from the UK. Review of Accounting Studies 15 (4), pp. 725-751.

ICAEW. 2016. Measurement in financial reporting. [Online]. Available at:

https://www.icaew.com/-/media/corporate/files/technical/financial-reporting/information-for-

better-markets/ifbm-reports/measurement-in-financial-reporting.ashx [Accessed on: 31 May

2018].

IFRS. 2017. Measurement uncertainty and the fundamental qualitative characteristics of useful

financial information. [Online]. Available at:

https://www.ifrs.org/-/media/feature/meetings/2017/september/iasb/cf/ap10-conceptual-

framework.pdf[Accessed on: 31 May 2019].

International Accounting Standards Board. 2016. Measurement Bases for Financial Accounting.

[Online]. Available at: https://www.efrag.org/Assets/Download?assetUrl=%2Fsites

%2Fwebpublishing%2FProject%20Documents%2F53%2FDP%20Measurement%20on

%20Initial%20Recognition.pdf [Accessed on: 31 May 2018].

Kythreotis, A. 2014. Measurement Of Financial Reporting Quality Based On IFRS Conceptual

Framework’s Fundamental Qualitative Characteristics. European Journal of Accounting,

Finance & Business, 2(3), pp. 4-29.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.