Superstore Ltd Financial Accounting Homework - Year Ended June 2018

VerifiedAdded on 2023/03/17

|26

|2344

|100

Homework Assignment

AI Summary

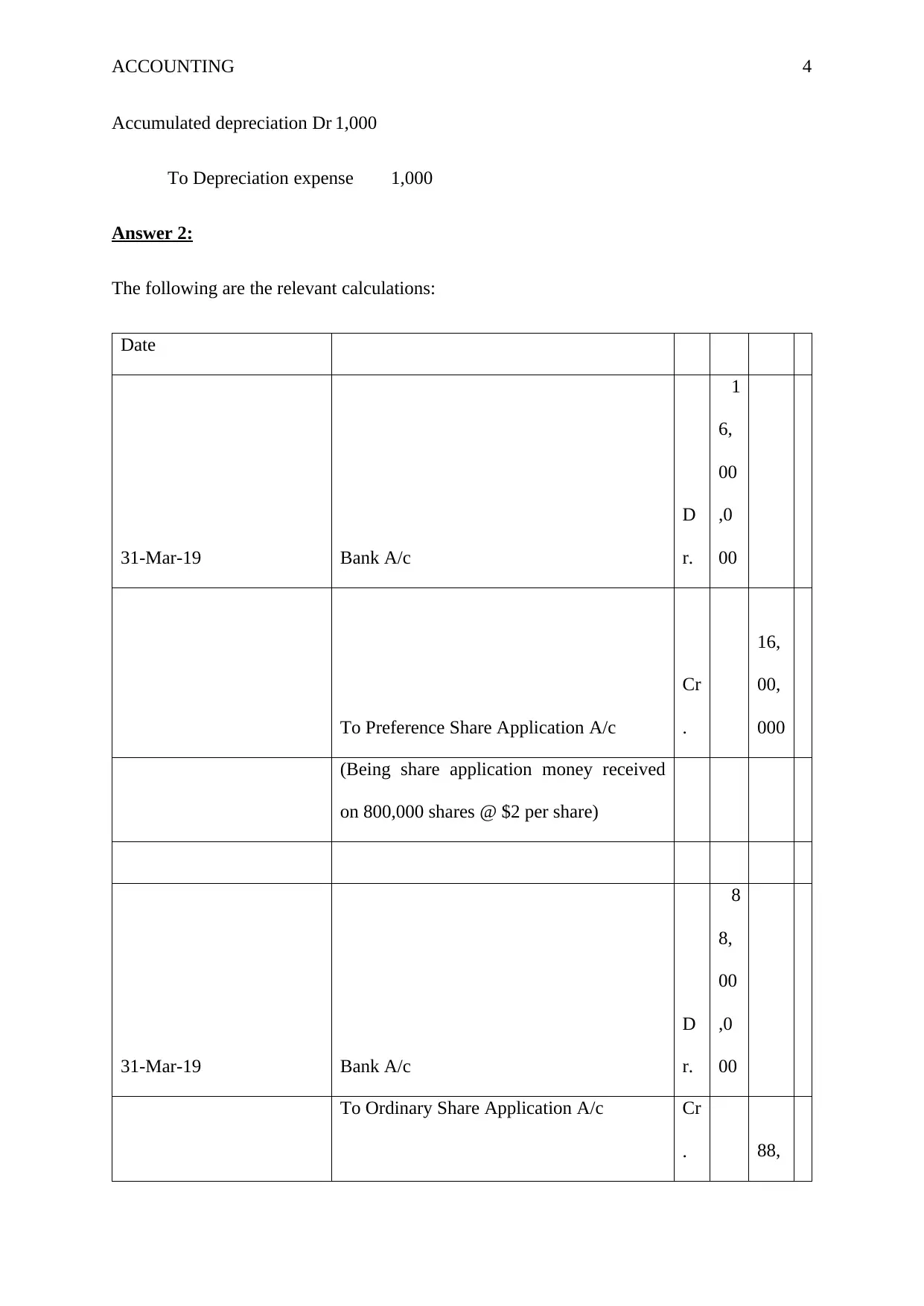

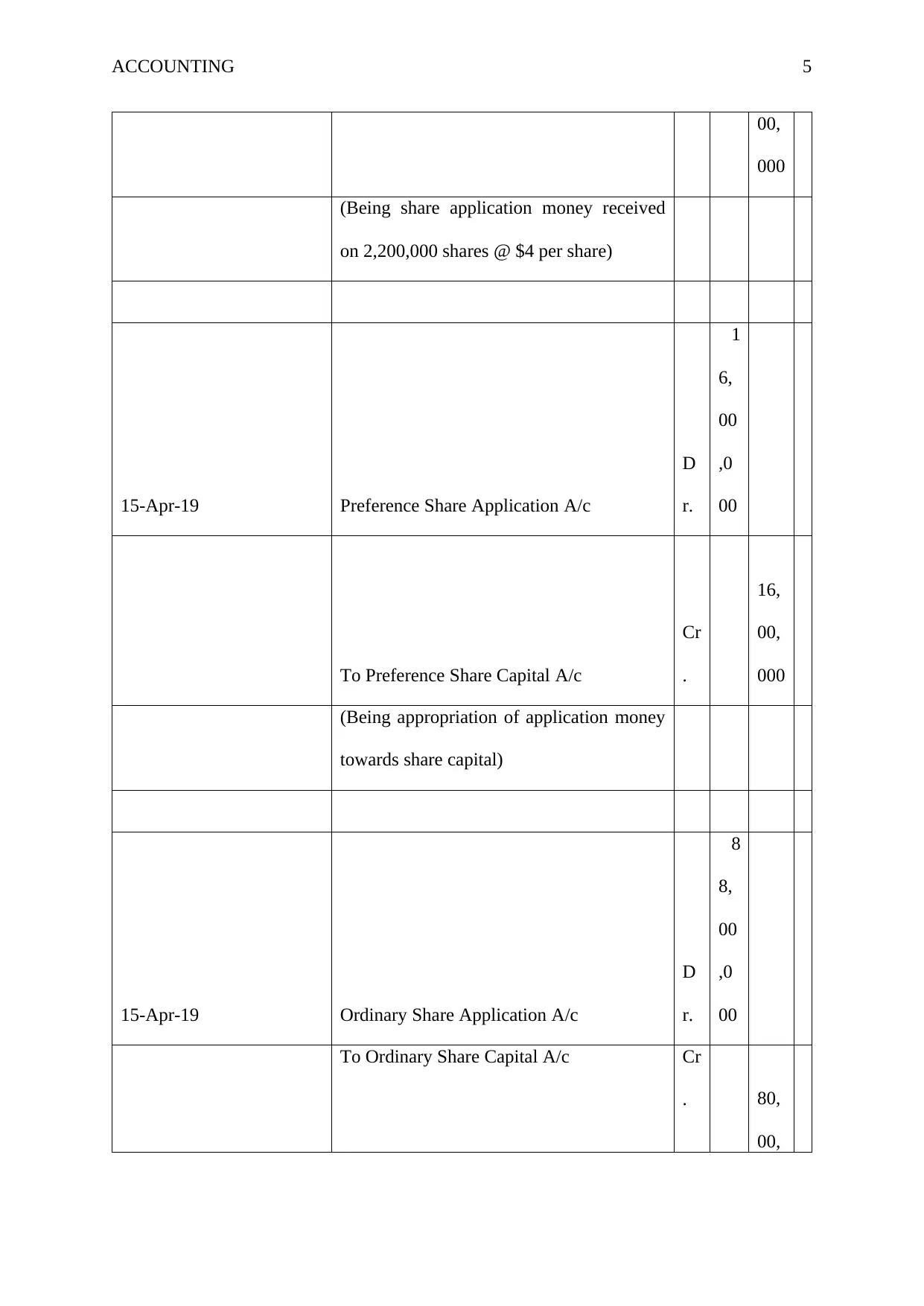

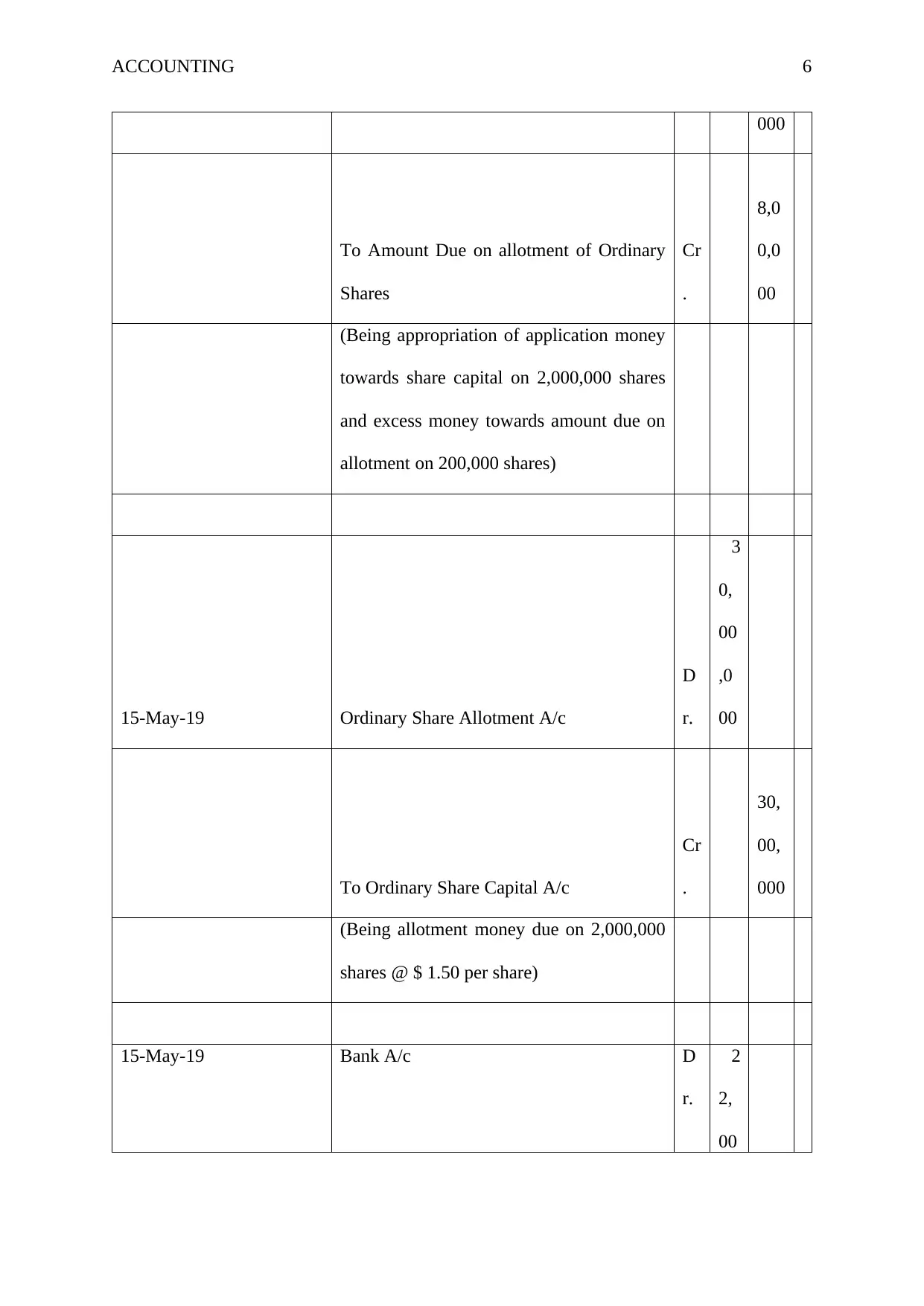

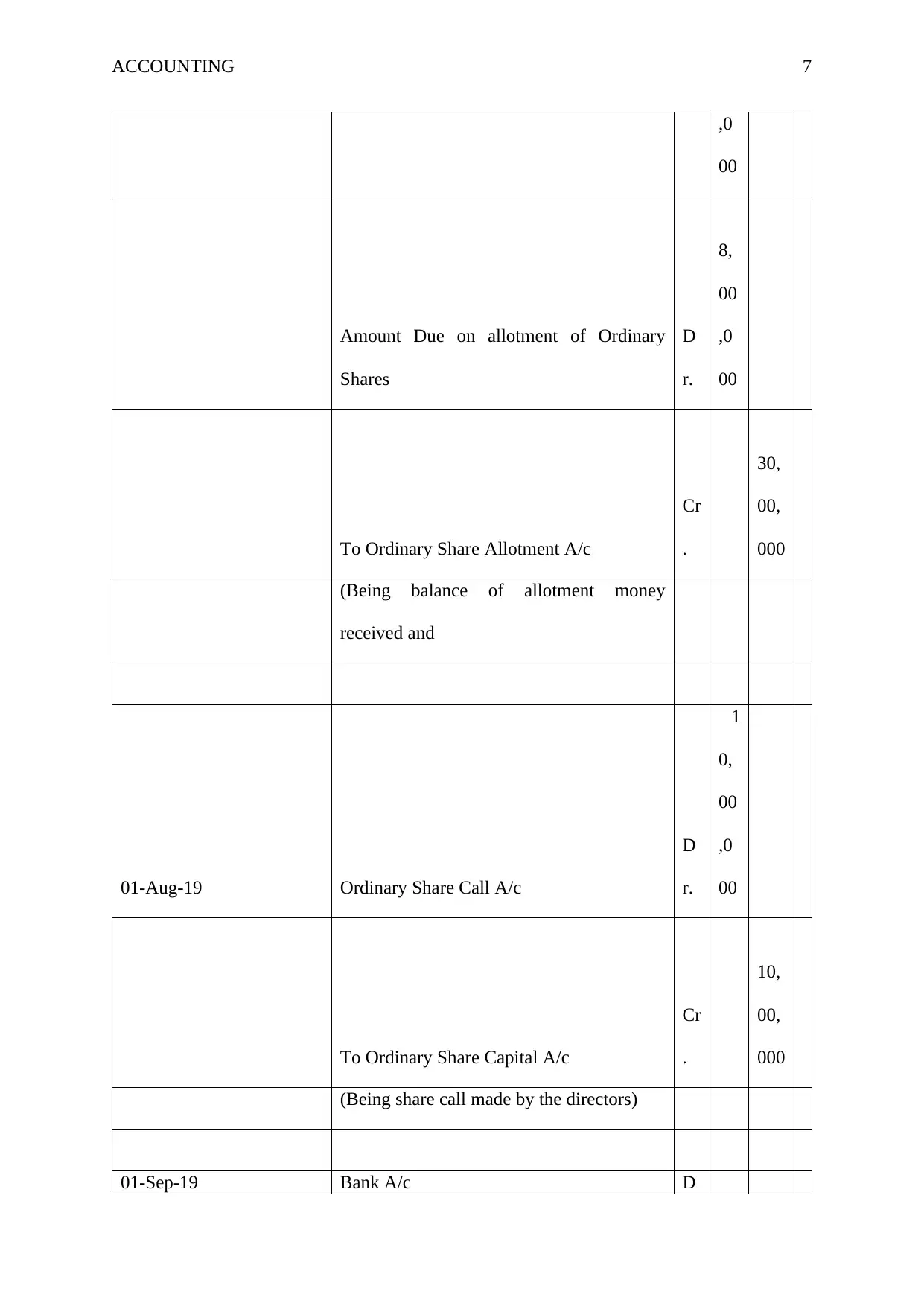

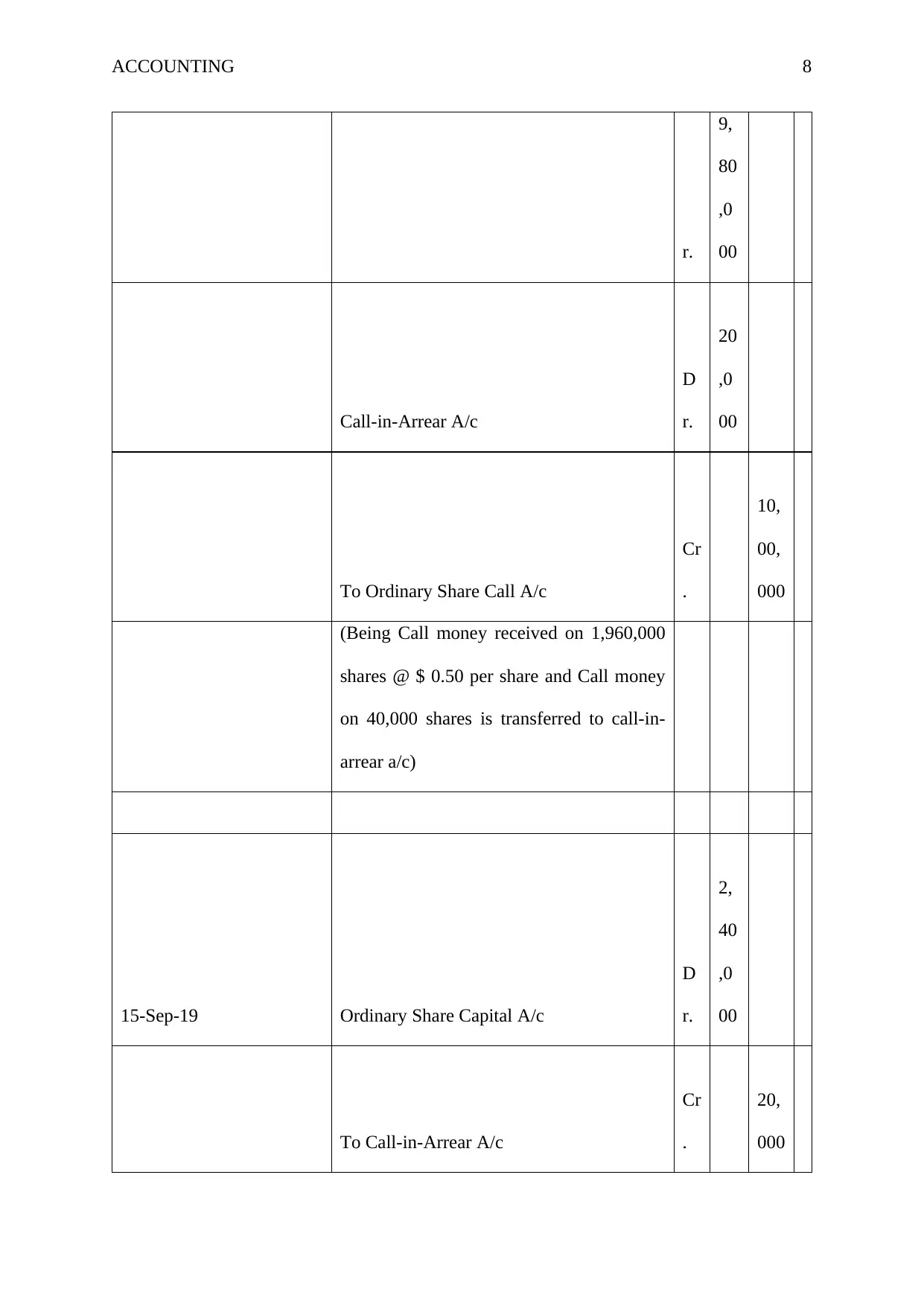

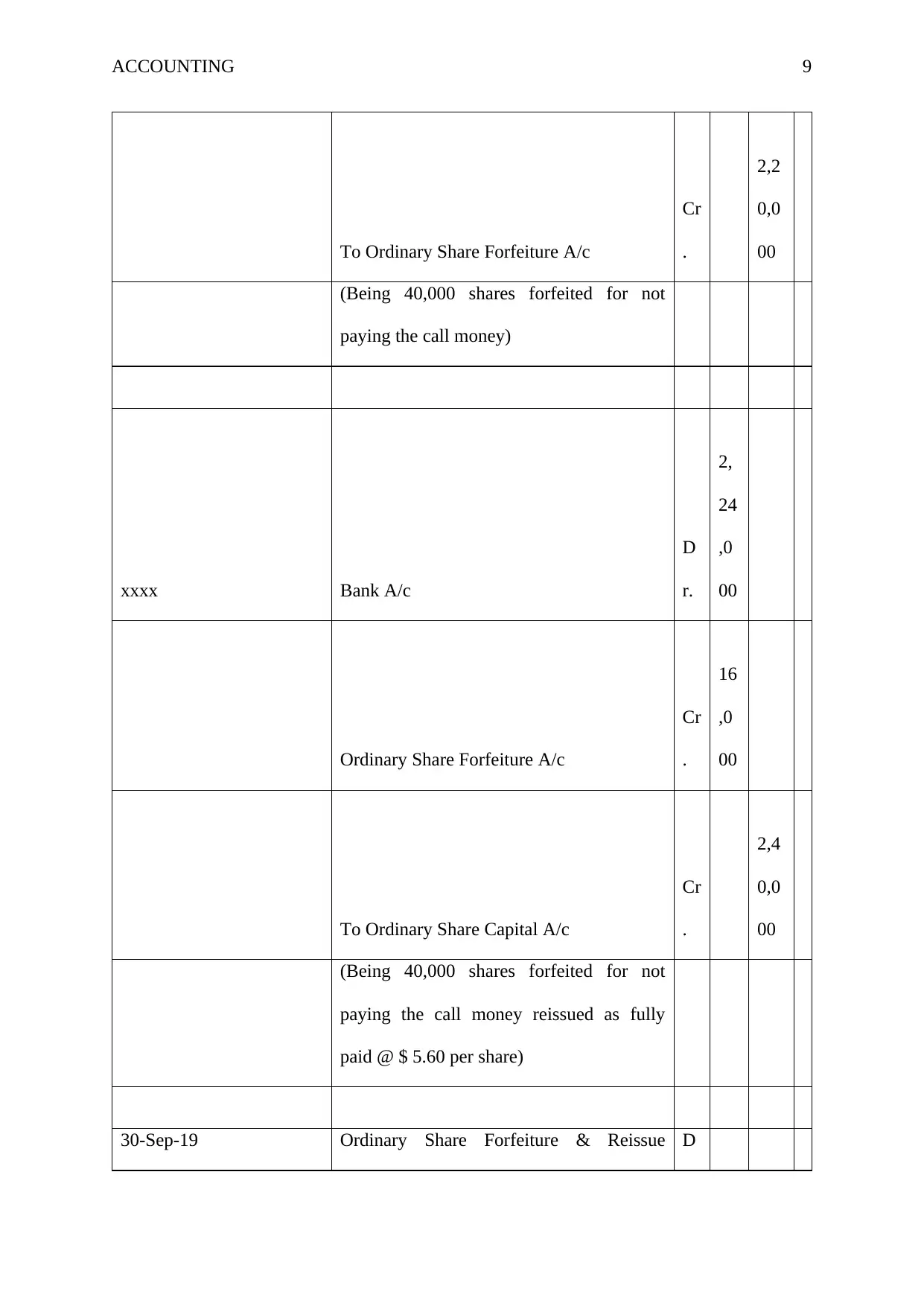

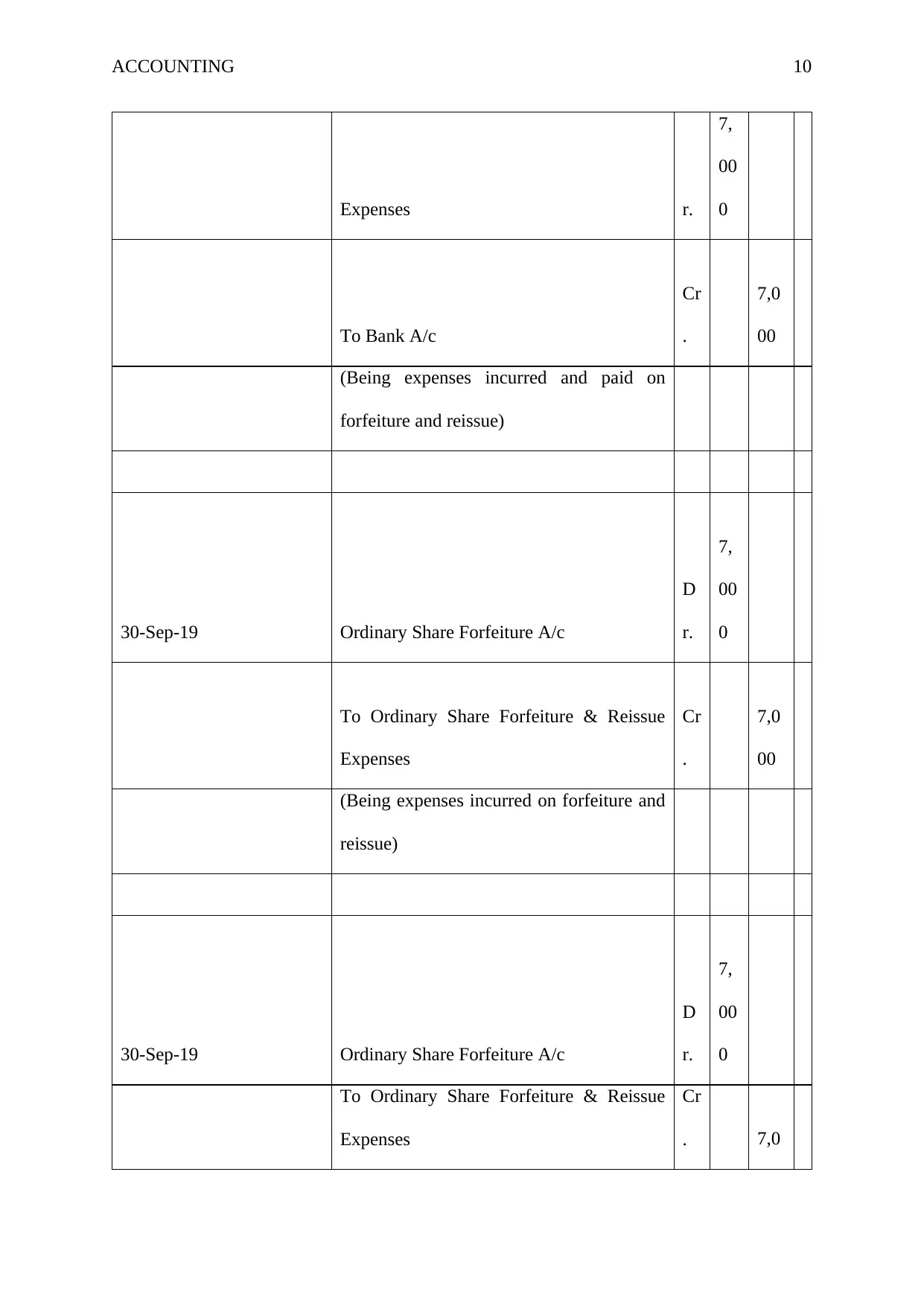

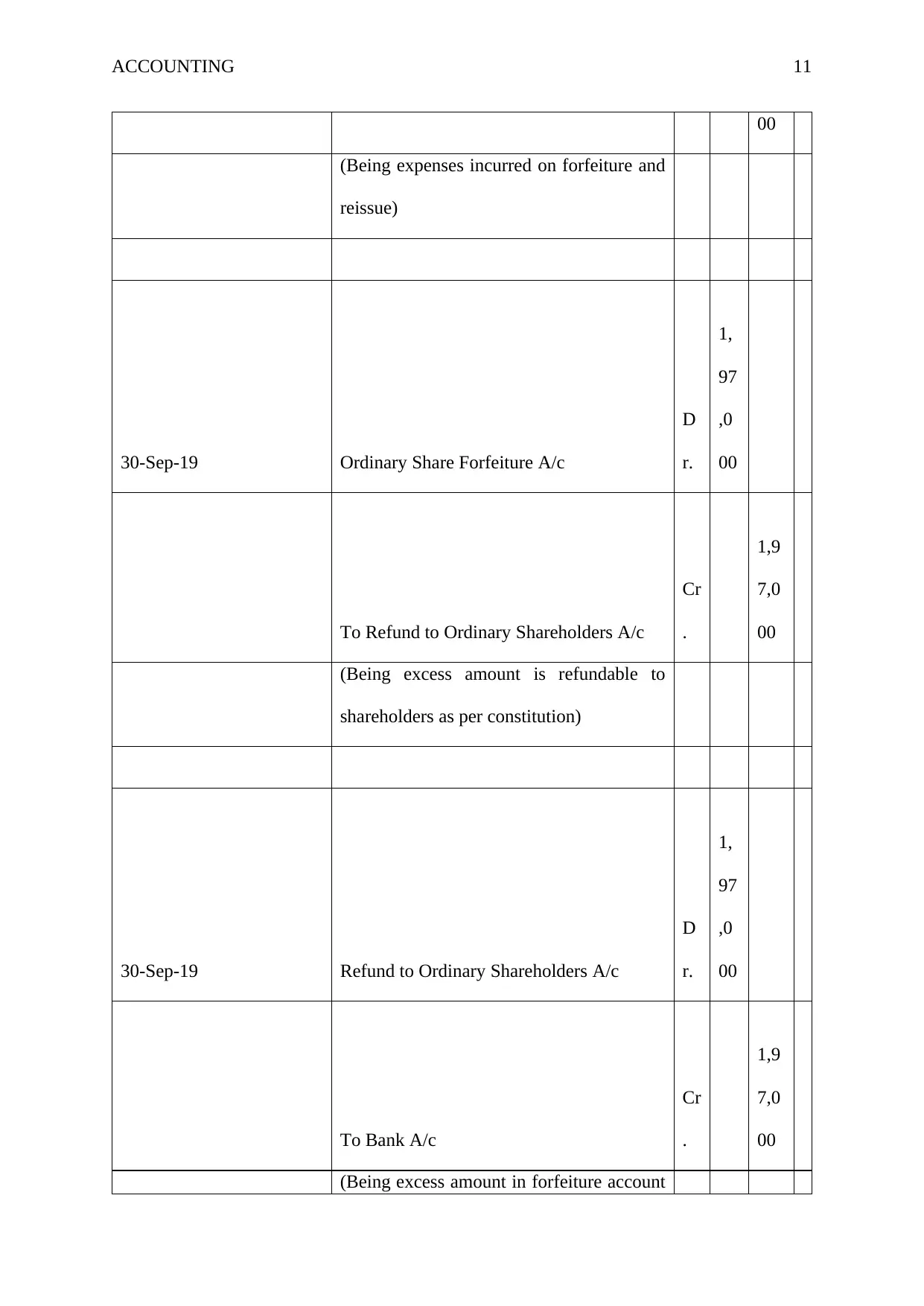

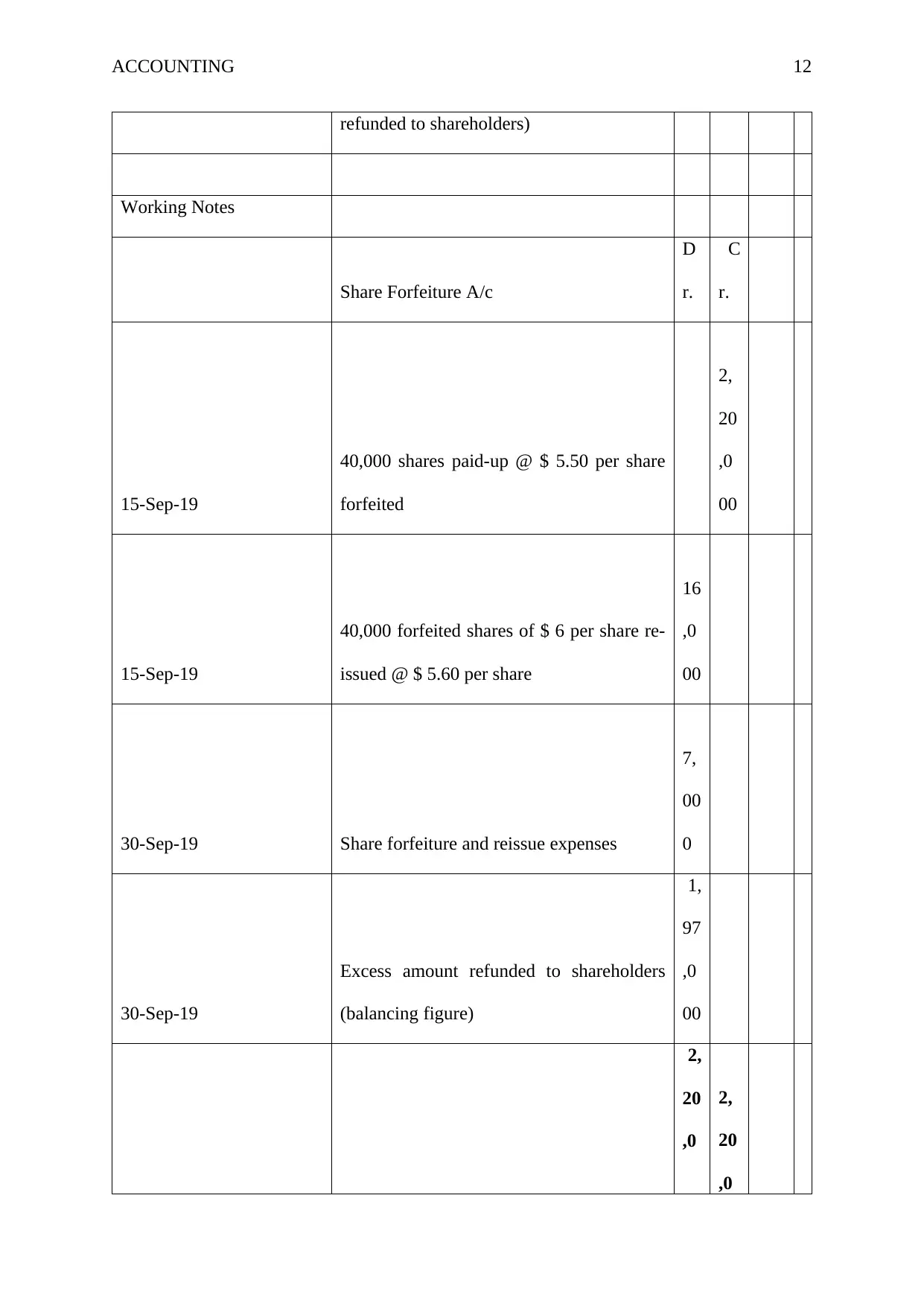

This assignment provides a comprehensive solution to a financial accounting problem centered on Superstore Ltd's financial statements for the year ended June 30, 2018. The solution addresses several key accounting concepts, including the recognition and disclosure of liabilities, specifically focusing on warranties, bad debts, and the impact of changing tax rates. It also covers depreciation calculations, journal entries related to share capital, and the handling of impairment losses on assets. Furthermore, the assignment delves into detailed calculations for share issuance, allotment, calls, and forfeitures, alongside relevant journal entries and working notes. The solution also includes the computation of current and deferred tax, with accompanying journal entries, and analyzes revaluation and disposal of assets. Finally, the assignment encompasses the preparation of impairment loss calculations and associated accounting treatments.

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.