Financial Accounting Homework: Statements & Assumptions

VerifiedAdded on 2022/12/28

|7

|761

|51

Homework Assignment

AI Summary

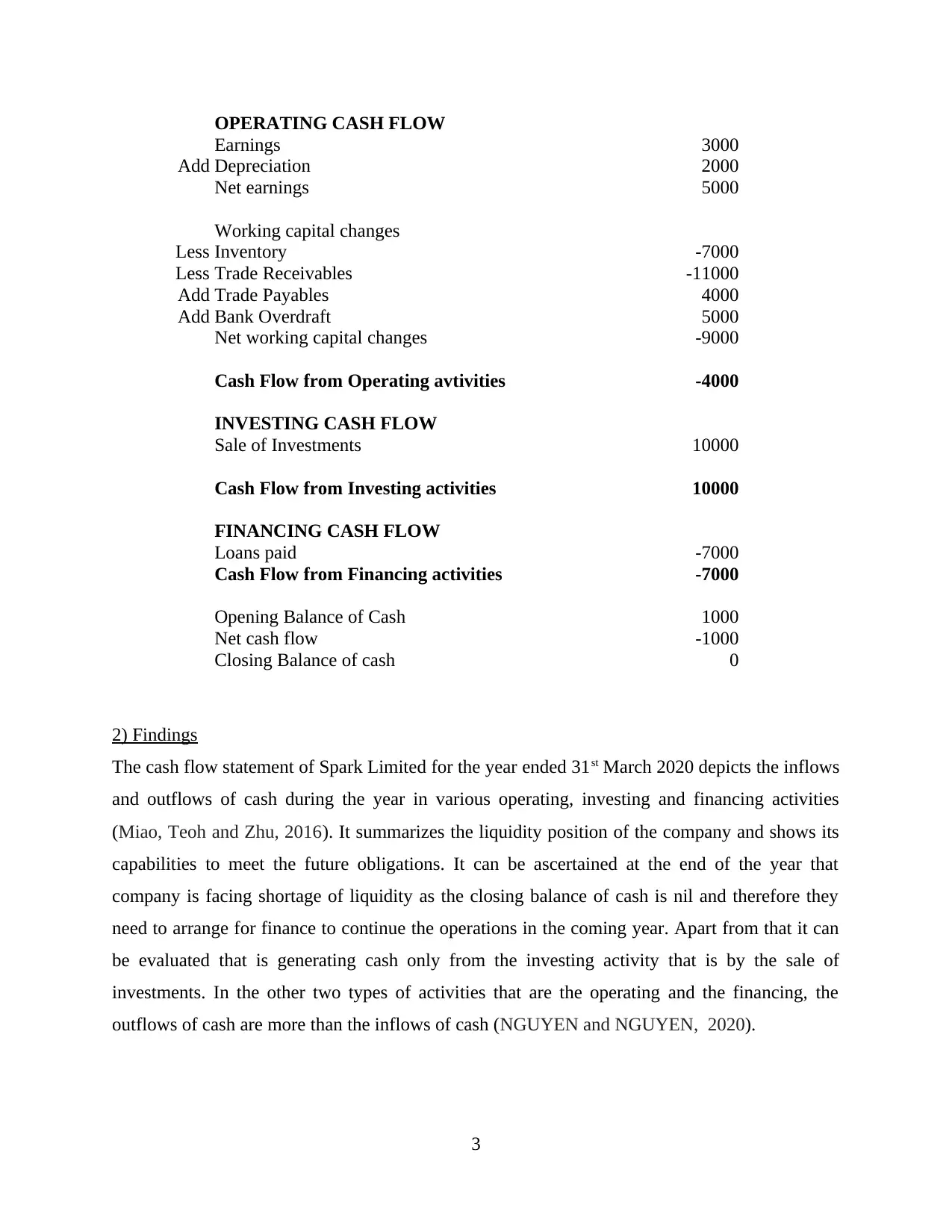

This financial accounting assignment presents a comprehensive solution, including an income statement for the year 2021, a statement of financial position, and a cash flow statement for the year ended March 31, 2020. The assignment identifies and explains six key assumptions underlying the preparation of financial statements. The solution details the calculations for net profit, assets, liabilities, and shareholder's equity, as well as an analysis of cash flow from operating, investing, and financing activities. The findings highlight the company's liquidity position and its reliance on investing activities for cash generation. The document references relevant academic sources to support the analysis and findings.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.