Financial Accounting Assignment: Scenario Analysis and Solutions

VerifiedAdded on 2022/11/29

|26

|4721

|263

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment. It begins with an introduction to financial accounting, defining its core processes of recording, evaluating, and reporting financial transactions, including the preparation of financial statements like the balance sheet and cash flow report. The solution then delves into two scenarios, addressing questions on various accounting operations, including sales, acquisitions, and cash transactions. It differentiates between single-entry and double-entry bookkeeping systems and explains the importance of trial balances in ensuring the accuracy and reliability of financial data. The assignment also explores journal entries, providing examples and ledger accounts, and discusses the income statement and balance sheet, outlining their components and the requirements of financial reports for different users, such as management, creditors, and employees. Finally, the document includes profit and loss accounts and a balance sheet for the year ended 31st December 2017, offering a complete overview of the financial accounting concepts and their practical application.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SCENARIO 1..................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................5

Question 3.................................................................................................................................11

Question 4.................................................................................................................................12

SCENARIO 2................................................................................................................................13

Question 1.................................................................................................................................13

Question 2.................................................................................................................................14

Question 3.................................................................................................................................15

Question 4.................................................................................................................................15

Question 5.................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

SCENARIO 1..................................................................................................................................3

Question 1...................................................................................................................................3

Question 2...................................................................................................................................5

Question 3.................................................................................................................................11

Question 4.................................................................................................................................12

SCENARIO 2................................................................................................................................13

Question 1.................................................................................................................................13

Question 2.................................................................................................................................14

Question 3.................................................................................................................................15

Question 4.................................................................................................................................15

Question 5.................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION

Financial accounting seems to be the process of recording, evaluating, and reporting

financial transactions and occurrences which are at some largely financial in character, as well as

interpreting the outcomes in a meaningful way. Financial accounting is really a professional

sector of accounting which measures cash flow inside a corporation (Aifuwa, Embele and Saidu,

2018). Expenses are recorded, summarised, and income tax as well as financial statements, such

as with a cash flow report or a balance sheet, are prepared according to predefined rules. The

many chores of recording company activity in the form of documents, reports, trial balances, as

well as the development of yearly reports for business entities determine this assessment.This

research also included a bank examination to see if the financial records were accurate.

SCENARIO 1

Question 1

Various types of company operations have been documented in accounting records, and the

amount from which it is founded was further defined. The following are some of them:

1. Sales transactions entail the selling of a commodity to a consumer in exchange for money

or credit.

2. Acquisitions are the events that somehow a business employs to acquire the items or

resources necessary to achieve the company's goals, as well as they are a negative to cash

or receivable accounts as well as a crediting to the revenue connected accounts

throughout the sales data.

3. Money purchases resulting in such a debit throughout the financial statements as well as a

problem of financial. Unless the products were purchased on credit, the purchase will be

completed, the debit accrued income, as well as the reimbursements put into the chaining

accounts.

4. Accounts receivable were documentation that show that a firm has paid for the delivery

of the product to some other firm. The invoicing interchange is recorded in the merchant's

reporting as a cash debit balances to the prepayments.

5. Payment comprise transactions in which monies are sent to a firm that is getting funds in

exchange for goods or services. Persons are recorded in the company's accounting log,

Financial accounting seems to be the process of recording, evaluating, and reporting

financial transactions and occurrences which are at some largely financial in character, as well as

interpreting the outcomes in a meaningful way. Financial accounting is really a professional

sector of accounting which measures cash flow inside a corporation (Aifuwa, Embele and Saidu,

2018). Expenses are recorded, summarised, and income tax as well as financial statements, such

as with a cash flow report or a balance sheet, are prepared according to predefined rules. The

many chores of recording company activity in the form of documents, reports, trial balances, as

well as the development of yearly reports for business entities determine this assessment.This

research also included a bank examination to see if the financial records were accurate.

SCENARIO 1

Question 1

Various types of company operations have been documented in accounting records, and the

amount from which it is founded was further defined. The following are some of them:

1. Sales transactions entail the selling of a commodity to a consumer in exchange for money

or credit.

2. Acquisitions are the events that somehow a business employs to acquire the items or

resources necessary to achieve the company's goals, as well as they are a negative to cash

or receivable accounts as well as a crediting to the revenue connected accounts

throughout the sales data.

3. Money purchases resulting in such a debit throughout the financial statements as well as a

problem of financial. Unless the products were purchased on credit, the purchase will be

completed, the debit accrued income, as well as the reimbursements put into the chaining

accounts.

4. Accounts receivable were documentation that show that a firm has paid for the delivery

of the product to some other firm. The invoicing interchange is recorded in the merchant's

reporting as a cash debit balances to the prepayments.

5. Payment comprise transactions in which monies are sent to a firm that is getting funds in

exchange for goods or services. Persons are recorded in the company's accounting log,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

allowing the transaction to be recorded as a sum received as well as a decrease from

accounts receivable.

Single entry bookkeeping

Single-entry accounting is unlikely to work for a business even if it is small, simple, and

has a low volume of transactions. It's typically similar to having your own private account. When

you use single-entry accountancy, you may keep track of things like money, income expenses,

and taxable income(Bishop, DeZoort and Hermanson, 2017).

Double entry bookkeeping

Many businesses, particularly start-ups, use double-entry accounting to maintain track of

their finances. The fact that each checkbook contains two sections yet expenditures are on

opposite sides is one of the hallmarks of double accounting system. The payment generates two

transfers: one deduction through one bank or each crediting from another (Ayres, Huang and

Myring, 2017).

Trial balance and its importance

The trial balance is really a spreadsheet where all accounting balances are incorporated

further into contactless payment component amounts, and the total is balanced. The business

used to make preparations trial balances on a regular basis, generally at the conclusion of each

financial month. The following are the doctoral programs of the financial statement:

Checking for reliability: This might indicate that the settlement agreement was being utilised

to validate the real figure gathered on the proper side of that equation ledger when transferring

data from many other sources like purchase records, written documents, cash books, and so on.

Aside from financial accounting considerations, the legitimacy of a specific economic industry

by improving.

Aids in the preparation of financial reports: The financial statements, capital structure, and

capital expenditures must all be revised at the conclusion of each financial reporting year. The

trial chapter also covers the total amount of all monies utilised to compile the accounting

statements, making financial facts simple to produce and comprehend.

Rectifying errors: The total deficit of both financial statements must match the total credit

including its financial statement. It is really a examination of the had therefore in the pamphlet. If

this isn't the case, the auditor will catch the mistake and correct it. Accounting professionals are

also happy when the overall debt balance as well as the overall amount owing are equal.

accounts receivable.

Single entry bookkeeping

Single-entry accounting is unlikely to work for a business even if it is small, simple, and

has a low volume of transactions. It's typically similar to having your own private account. When

you use single-entry accountancy, you may keep track of things like money, income expenses,

and taxable income(Bishop, DeZoort and Hermanson, 2017).

Double entry bookkeeping

Many businesses, particularly start-ups, use double-entry accounting to maintain track of

their finances. The fact that each checkbook contains two sections yet expenditures are on

opposite sides is one of the hallmarks of double accounting system. The payment generates two

transfers: one deduction through one bank or each crediting from another (Ayres, Huang and

Myring, 2017).

Trial balance and its importance

The trial balance is really a spreadsheet where all accounting balances are incorporated

further into contactless payment component amounts, and the total is balanced. The business

used to make preparations trial balances on a regular basis, generally at the conclusion of each

financial month. The following are the doctoral programs of the financial statement:

Checking for reliability: This might indicate that the settlement agreement was being utilised

to validate the real figure gathered on the proper side of that equation ledger when transferring

data from many other sources like purchase records, written documents, cash books, and so on.

Aside from financial accounting considerations, the legitimacy of a specific economic industry

by improving.

Aids in the preparation of financial reports: The financial statements, capital structure, and

capital expenditures must all be revised at the conclusion of each financial reporting year. The

trial chapter also covers the total amount of all monies utilised to compile the accounting

statements, making financial facts simple to produce and comprehend.

Rectifying errors: The total deficit of both financial statements must match the total credit

including its financial statement. It is really a examination of the had therefore in the pamphlet. If

this isn't the case, the auditor will catch the mistake and correct it. Accounting professionals are

also happy when the overall debt balance as well as the overall amount owing are equal.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adjustment assistance: During the verdict balance building process, adjustments programs

including such payroll costs, retention bonds, closure needs to share, and so on must be altered.

This helps make modifications that are only noticeable in the relevant accounting year. There at

conclusion of the fiscal year, companies typically throw out readjustment news pieces. When

people occurs, there really is no constraint on initiating new shift activities (Bolvar and et al,

2018).

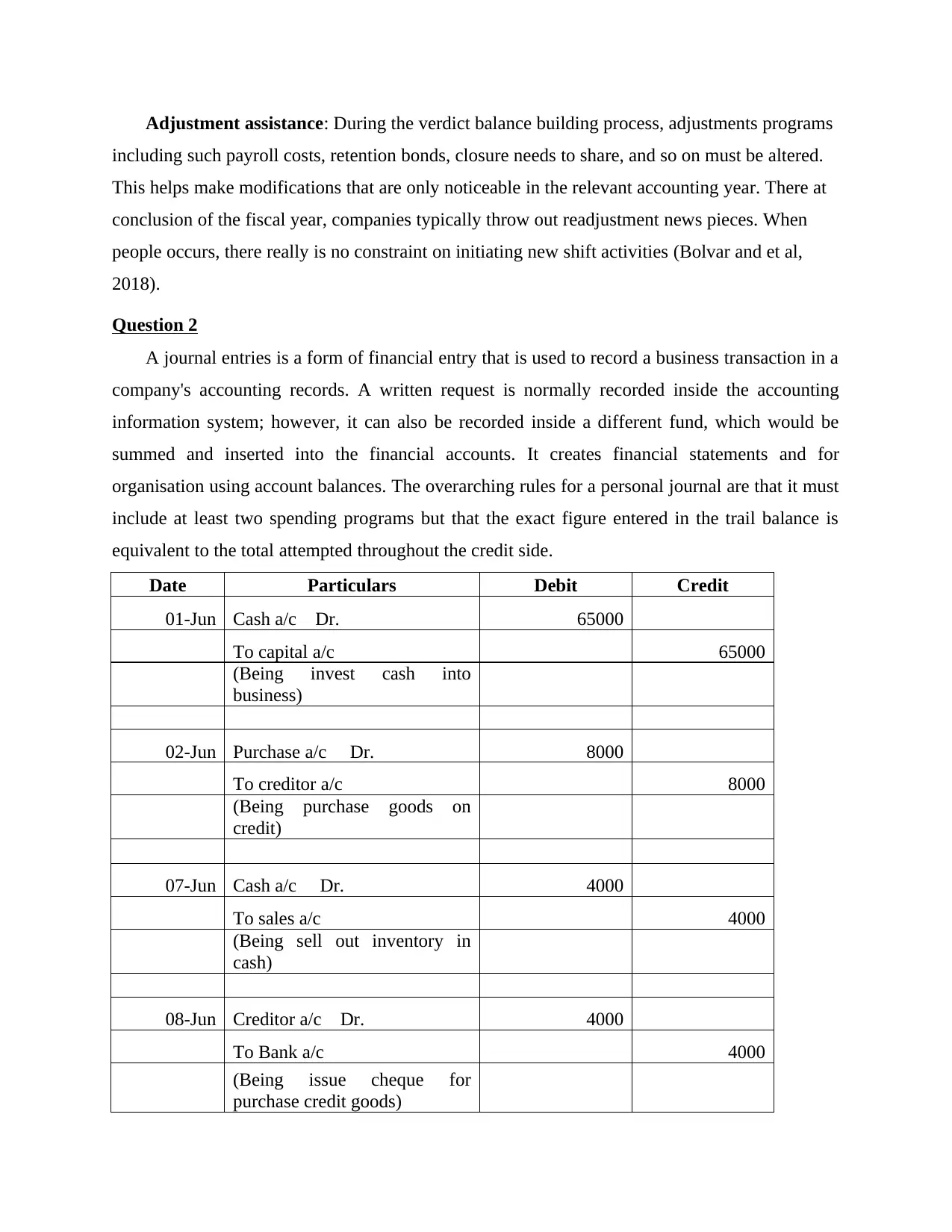

Question 2

A journal entries is a form of financial entry that is used to record a business transaction in a

company's accounting records. A written request is normally recorded inside the accounting

information system; however, it can also be recorded inside a different fund, which would be

summed and inserted into the financial accounts. It creates financial statements and for

organisation using account balances. The overarching rules for a personal journal are that it must

include at least two spending programs but that the exact figure entered in the trail balance is

equivalent to the total attempted throughout the credit side.

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

(Being invest cash into

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

08-Jun Creditor a/c Dr. 4000

To Bank a/c 4000

(Being issue cheque for

purchase credit goods)

including such payroll costs, retention bonds, closure needs to share, and so on must be altered.

This helps make modifications that are only noticeable in the relevant accounting year. There at

conclusion of the fiscal year, companies typically throw out readjustment news pieces. When

people occurs, there really is no constraint on initiating new shift activities (Bolvar and et al,

2018).

Question 2

A journal entries is a form of financial entry that is used to record a business transaction in a

company's accounting records. A written request is normally recorded inside the accounting

information system; however, it can also be recorded inside a different fund, which would be

summed and inserted into the financial accounts. It creates financial statements and for

organisation using account balances. The overarching rules for a personal journal are that it must

include at least two spending programs but that the exact figure entered in the trail balance is

equivalent to the total attempted throughout the credit side.

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

(Being invest cash into

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

08-Jun Creditor a/c Dr. 4000

To Bank a/c 4000

(Being issue cheque for

purchase credit goods)

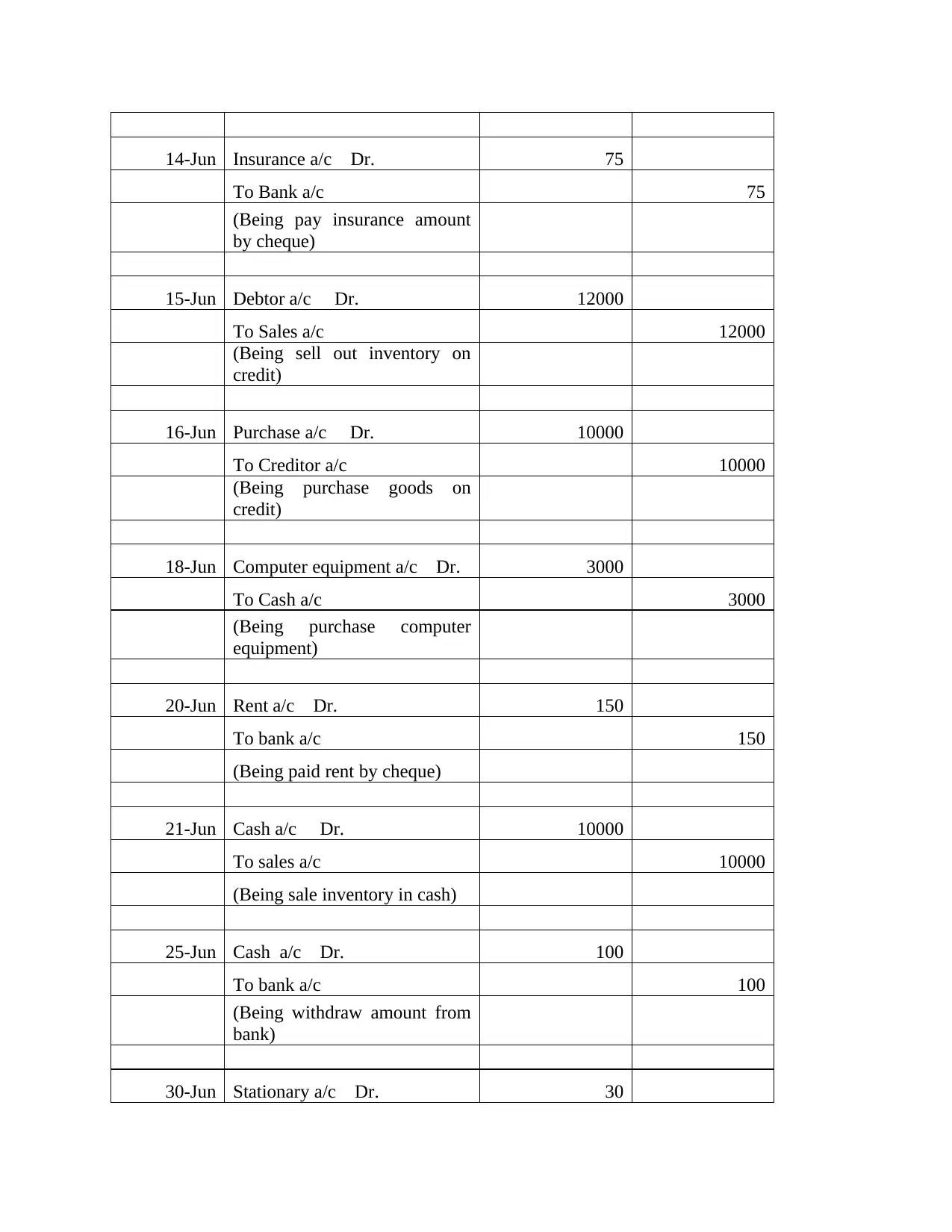

14-Jun Insurance a/c Dr. 75

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

21-Jun Cash a/c Dr. 10000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

21-Jun Cash a/c Dr. 10000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

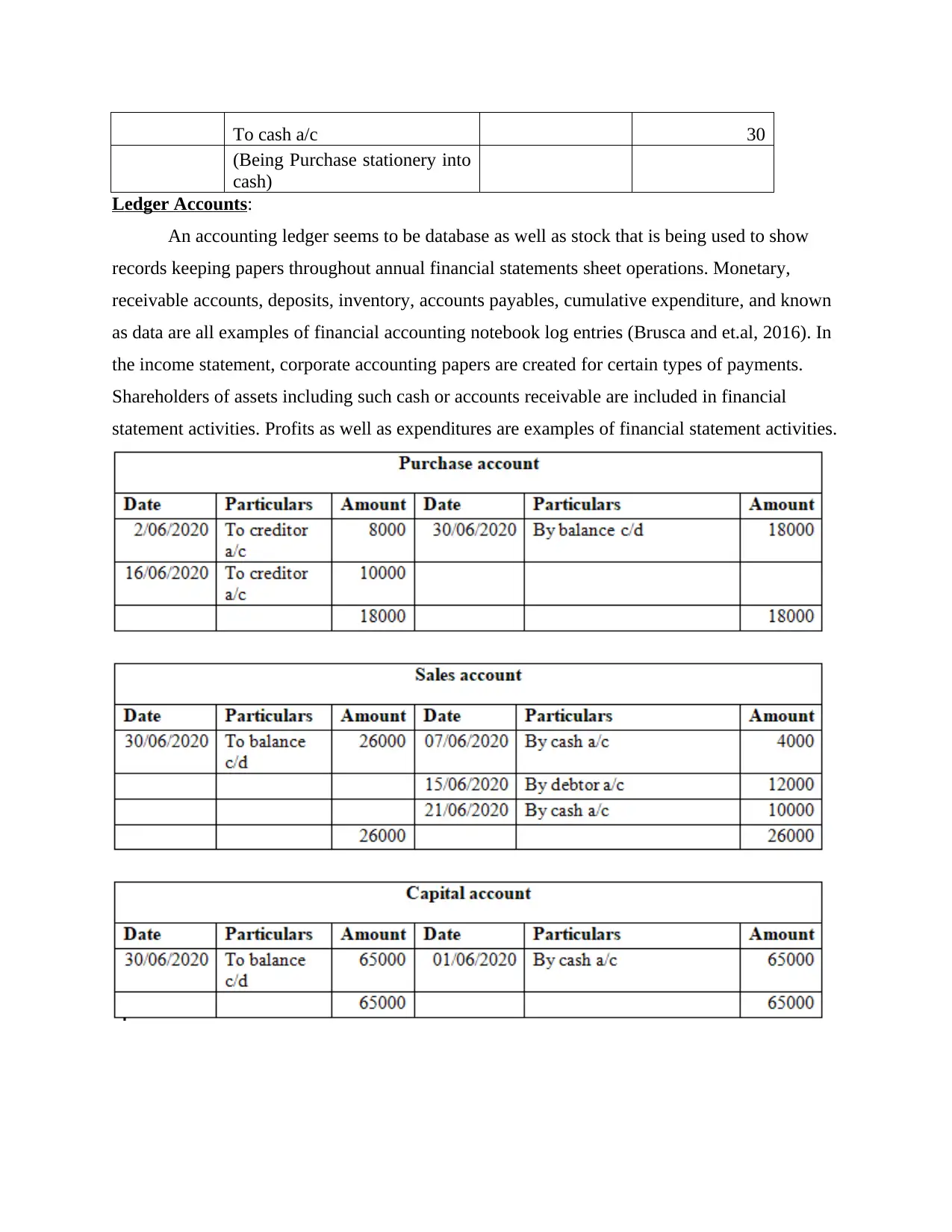

To cash a/c 30

(Being Purchase stationery into

cash)

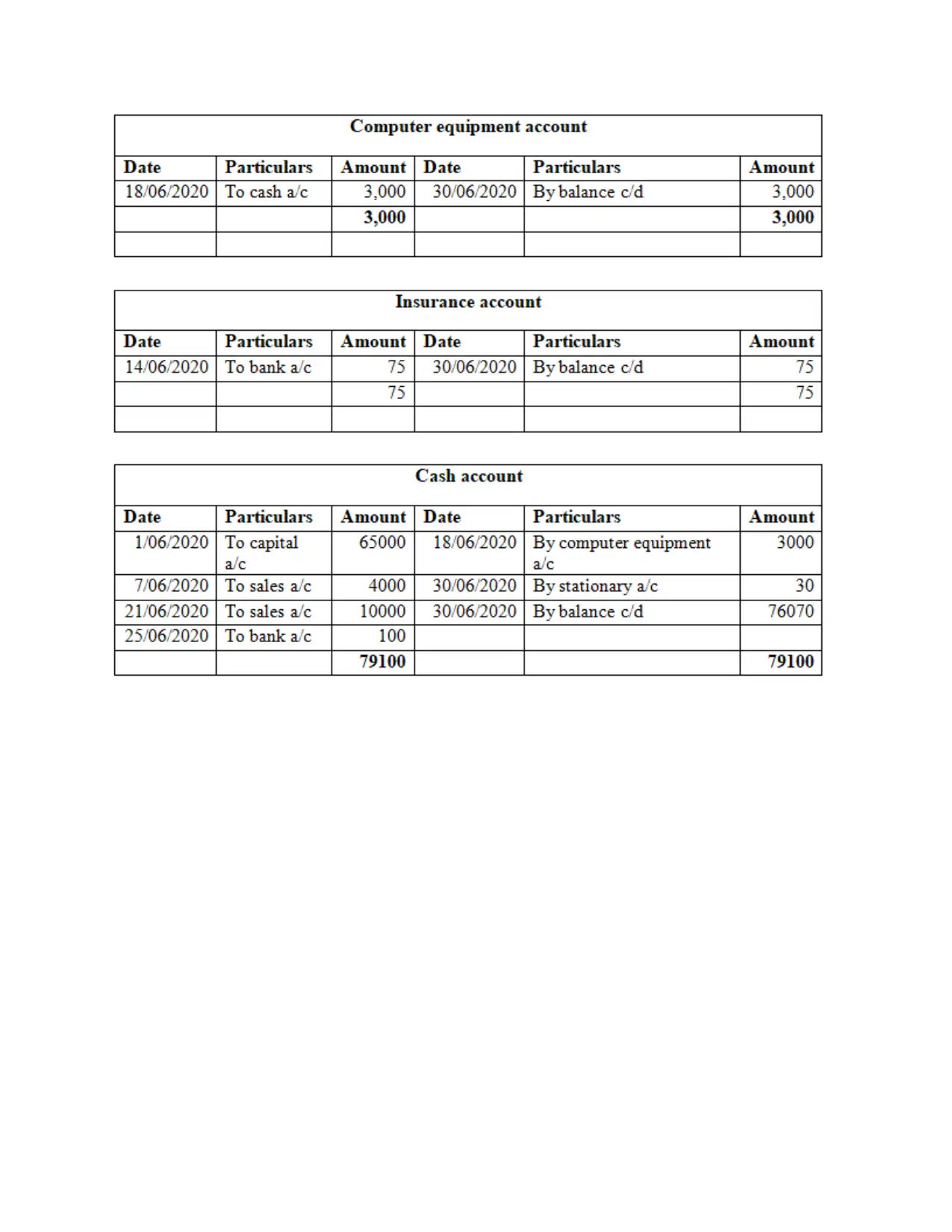

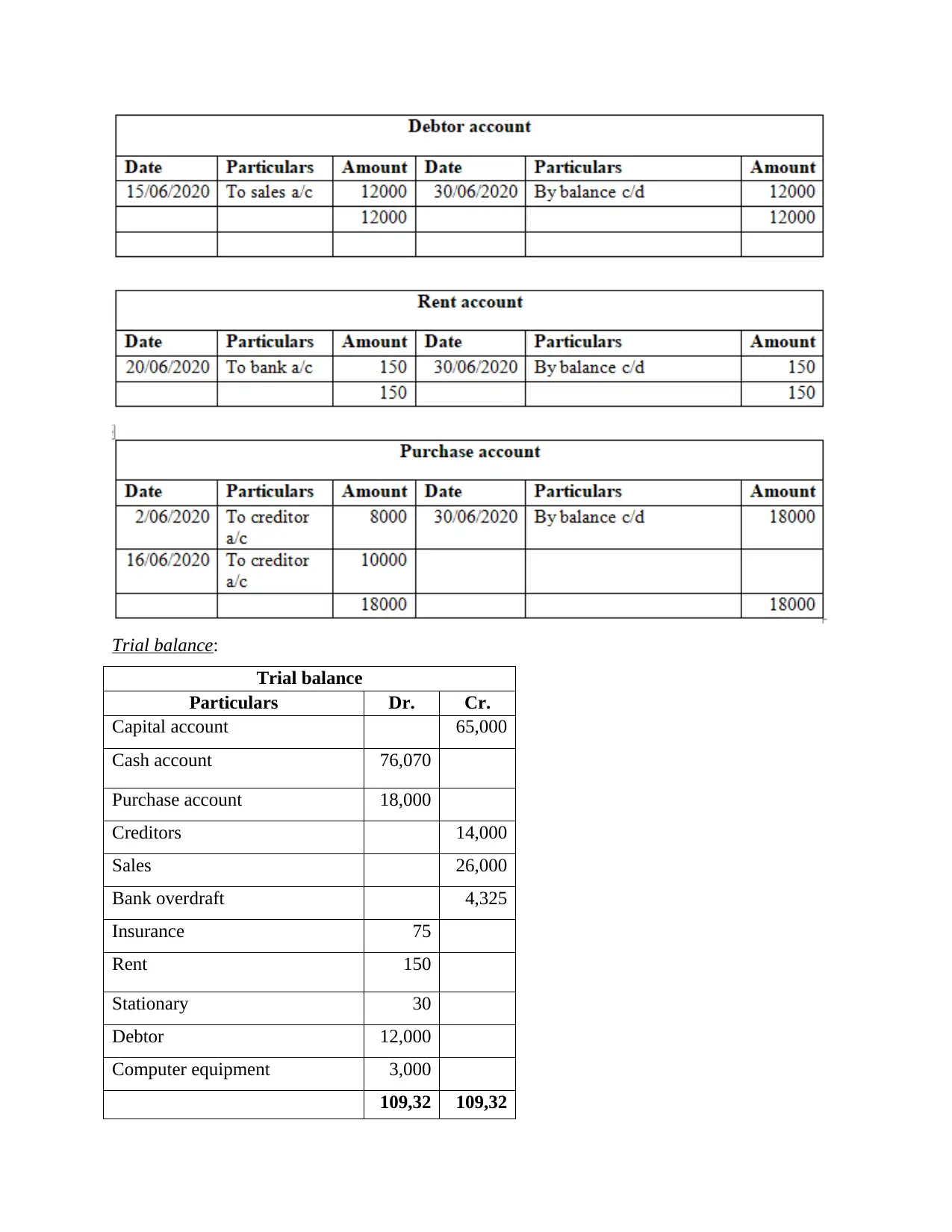

Ledger Accounts:

An accounting ledger seems to be database as well as stock that is being used to show

records keeping papers throughout annual financial statements sheet operations. Monetary,

receivable accounts, deposits, inventory, accounts payables, cumulative expenditure, and known

as data are all examples of financial accounting notebook log entries (Brusca and et.al, 2016). In

the income statement, corporate accounting papers are created for certain types of payments.

Shareholders of assets including such cash or accounts receivable are included in financial

statement activities. Profits as well as expenditures are examples of financial statement activities.

(Being Purchase stationery into

cash)

Ledger Accounts:

An accounting ledger seems to be database as well as stock that is being used to show

records keeping papers throughout annual financial statements sheet operations. Monetary,

receivable accounts, deposits, inventory, accounts payables, cumulative expenditure, and known

as data are all examples of financial accounting notebook log entries (Brusca and et.al, 2016). In

the income statement, corporate accounting papers are created for certain types of payments.

Shareholders of assets including such cash or accounts receivable are included in financial

statement activities. Profits as well as expenditures are examples of financial statement activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trial balance:

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Debtor 12,000

Computer equipment 3,000

109,32 109,32

Trial balance

Particulars Dr. Cr.

Capital account 65,000

Cash account 76,070

Purchase account 18,000

Creditors 14,000

Sales 26,000

Bank overdraft 4,325

Insurance 75

Rent 150

Stationary 30

Debtor 12,000

Computer equipment 3,000

109,32 109,32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 5

Question 3

The income report presents the results of financial reporting, which is a process of providing

primary contact employees the information required to make good decisions. The major

difference among financial statements and accounting is this. Financial reports are generated for

a given accounting period, which is generally a year. So because balance sheet may fluctuate

based on the records of the person or company, this accounting term is referred to as a 'fiscal

year.' It differs from a scheduled term (Gotti, 2016). Financial reports are also intended to offer

information about the company's financial status, cash flow, as well as operating

performance. The consumers of such remarks were aided in formulating appropriate decisions as

a result of this procedure. These assessments look for patterns in commodity usage, cash flow,

employee morale, as well as financial health. This enables merchants and people to make more

informed judgments about how the business must be run for better results.The terms "financial

report" as well as "financial statement" are used interchangeably but not interchangeably. The

notion of a "financial statement" is a basic notion that underpins many other types of reporting.

The revenue reports are one research that falls within the accounting records category. All

financial reports are accounting standards in several ways, although not all revenue accounts

seem to be best for company.

Requirement of financial reports and its users:

Organizations incur a price for attempting to report upon its capital gains, profit-making

profitability economic strategies, as per GAAPs. The next three primary financial reports,

comprising the income statements, balance sheet, and summary of cash flow, should be produced

in accordance with GAAP. Financial statement systems may be coupled with the present general

ledger, delivering robust and current integrated analytics, but without the high cost of upgrading

their GL or ERP. Holders might expect economic development after the company has established

the suitable long-term cooperation (Honggowati and et.al, 2017). While integrating data sources,

locations, and exchange rates, production, packaging, and marketing evaluations may be

completed with uniformity and dependability. The similar control guarantees that reports are

tailored to the subcommittee's as well as the SEC's requirements.

Question 3

The income report presents the results of financial reporting, which is a process of providing

primary contact employees the information required to make good decisions. The major

difference among financial statements and accounting is this. Financial reports are generated for

a given accounting period, which is generally a year. So because balance sheet may fluctuate

based on the records of the person or company, this accounting term is referred to as a 'fiscal

year.' It differs from a scheduled term (Gotti, 2016). Financial reports are also intended to offer

information about the company's financial status, cash flow, as well as operating

performance. The consumers of such remarks were aided in formulating appropriate decisions as

a result of this procedure. These assessments look for patterns in commodity usage, cash flow,

employee morale, as well as financial health. This enables merchants and people to make more

informed judgments about how the business must be run for better results.The terms "financial

report" as well as "financial statement" are used interchangeably but not interchangeably. The

notion of a "financial statement" is a basic notion that underpins many other types of reporting.

The revenue reports are one research that falls within the accounting records category. All

financial reports are accounting standards in several ways, although not all revenue accounts

seem to be best for company.

Requirement of financial reports and its users:

Organizations incur a price for attempting to report upon its capital gains, profit-making

profitability economic strategies, as per GAAPs. The next three primary financial reports,

comprising the income statements, balance sheet, and summary of cash flow, should be produced

in accordance with GAAP. Financial statement systems may be coupled with the present general

ledger, delivering robust and current integrated analytics, but without the high cost of upgrading

their GL or ERP. Holders might expect economic development after the company has established

the suitable long-term cooperation (Honggowati and et.al, 2017). While integrating data sources,

locations, and exchange rates, production, packaging, and marketing evaluations may be

completed with uniformity and dependability. The similar control guarantees that reports are

tailored to the subcommittee's as well as the SEC's requirements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The revenues obtained by the business throughout the financial quarter should be addressed in

the interest expense, along with the associated operational expenditures. It includes both

operational and non-operating income, giving creditors as well as debtors the ability to set

profitability. Financial reports as well as losses statements are common terms used to describe it.

Similarly, the cost of borrowing and liabilities indicated in the financial report, as well as the

consequent cash flow, are represented in the balance sheet. Workers who seem to have a major

impact on the business outcomes of the company utilise this information. The following is a list

of everything:

Management: The firm's productivity, adaptability, and capital expenditures should be

recognised on a regular basis so that commodity accountancy and strategic analyses may

be completed.

Creditors: Because they are the company's proprietors and want to recognise their

money's growth, they will demand that financial reports be examined (Khoja, Chipulu

and Jayasekera, 2019).

Competitors: Businesses might anticipate competitors to also have accessibility to their

banking records in order to assess their financial situation. Their dominating advantage

may change as a result of the expert information they learn.

Customers: When deciding which manufacturer to hire for a major contract, the buyer

must first review his finance analysis to show the business's surplus funds to stay

profitable long enough to provide the activities or commodities required by the contract.

Employees: A business might choose to begin giving financial statements towards its

employees, including a detailed description of the systems in place. It might be used to

build relationships with people and understanding of the market.

Question 4

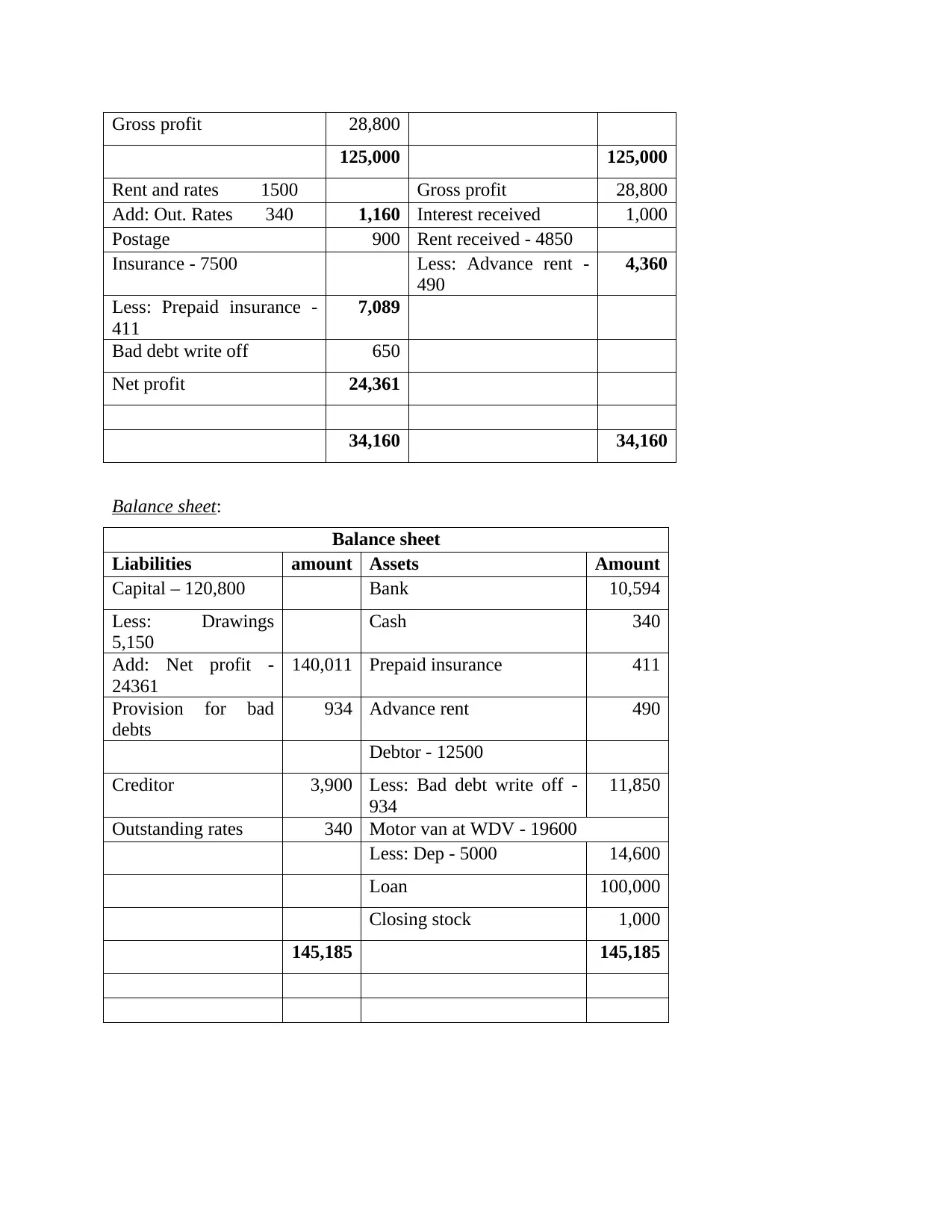

Profit and loss account for the year ended 31st December 2017:

Profit and loss account

Particulars Amount Particulars amount

Opening stock 9,500 Sales 125,000

Purchase 75000 Less: Return (1000) 124,000

Less: Return (1500) 73,500 Closing stock 1,000

Wages and salaries 13,200

the interest expense, along with the associated operational expenditures. It includes both

operational and non-operating income, giving creditors as well as debtors the ability to set

profitability. Financial reports as well as losses statements are common terms used to describe it.

Similarly, the cost of borrowing and liabilities indicated in the financial report, as well as the

consequent cash flow, are represented in the balance sheet. Workers who seem to have a major

impact on the business outcomes of the company utilise this information. The following is a list

of everything:

Management: The firm's productivity, adaptability, and capital expenditures should be

recognised on a regular basis so that commodity accountancy and strategic analyses may

be completed.

Creditors: Because they are the company's proprietors and want to recognise their

money's growth, they will demand that financial reports be examined (Khoja, Chipulu

and Jayasekera, 2019).

Competitors: Businesses might anticipate competitors to also have accessibility to their

banking records in order to assess their financial situation. Their dominating advantage

may change as a result of the expert information they learn.

Customers: When deciding which manufacturer to hire for a major contract, the buyer

must first review his finance analysis to show the business's surplus funds to stay

profitable long enough to provide the activities or commodities required by the contract.

Employees: A business might choose to begin giving financial statements towards its

employees, including a detailed description of the systems in place. It might be used to

build relationships with people and understanding of the market.

Question 4

Profit and loss account for the year ended 31st December 2017:

Profit and loss account

Particulars Amount Particulars amount

Opening stock 9,500 Sales 125,000

Purchase 75000 Less: Return (1000) 124,000

Less: Return (1500) 73,500 Closing stock 1,000

Wages and salaries 13,200

Gross profit 28,800

125,000 125,000

Rent and rates 1500 Gross profit 28,800

Add: Out. Rates 340 1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24,361

34,160 34,160

Balance sheet:

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings

5,150

Cash 340

Add: Net profit -

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off -

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

125,000 125,000

Rent and rates 1500 Gross profit 28,800

Add: Out. Rates 340 1,160 Interest received 1,000

Postage 900 Rent received - 4850

Insurance - 7500 Less: Advance rent -

490

4,360

Less: Prepaid insurance -

411

7,089

Bad debt write off 650

Net profit 24,361

34,160 34,160

Balance sheet:

Balance sheet

Liabilities amount Assets Amount

Capital – 120,800 Bank 10,594

Less: Drawings

5,150

Cash 340

Add: Net profit -

24361

140,011 Prepaid insurance 411

Provision for bad

debts

934 Advance rent 490

Debtor - 12500

Creditor 3,900 Less: Bad debt write off -

934

11,850

Outstanding rates 340 Motor van at WDV - 19600

Less: Dep - 5000 14,600

Loan 100,000

Closing stock 1,000

145,185 145,185

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.