Financial Accounting Homework - Depreciation, Assets, and Receivables

VerifiedAdded on 2022/12/27

|5

|617

|41

Homework Assignment

AI Summary

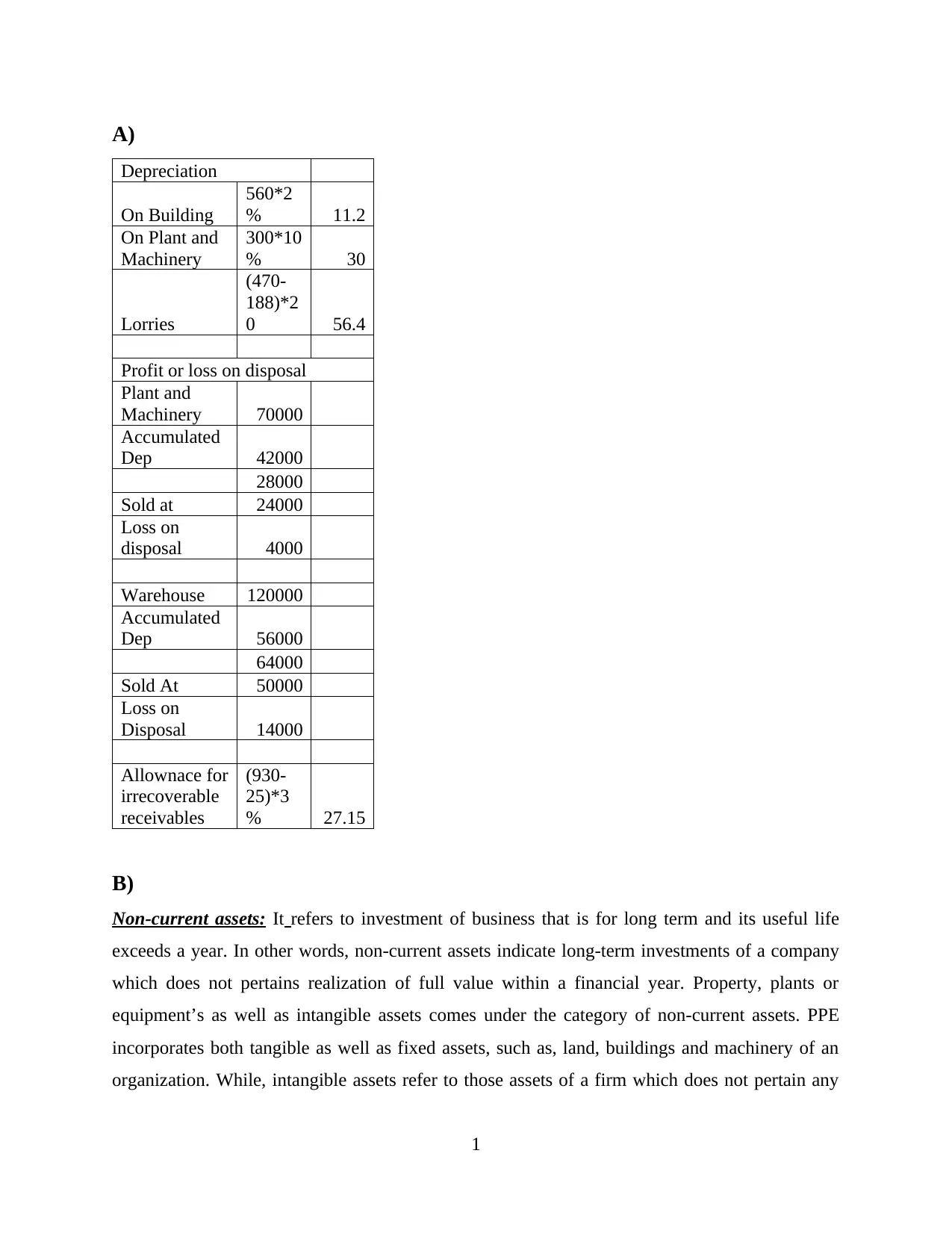

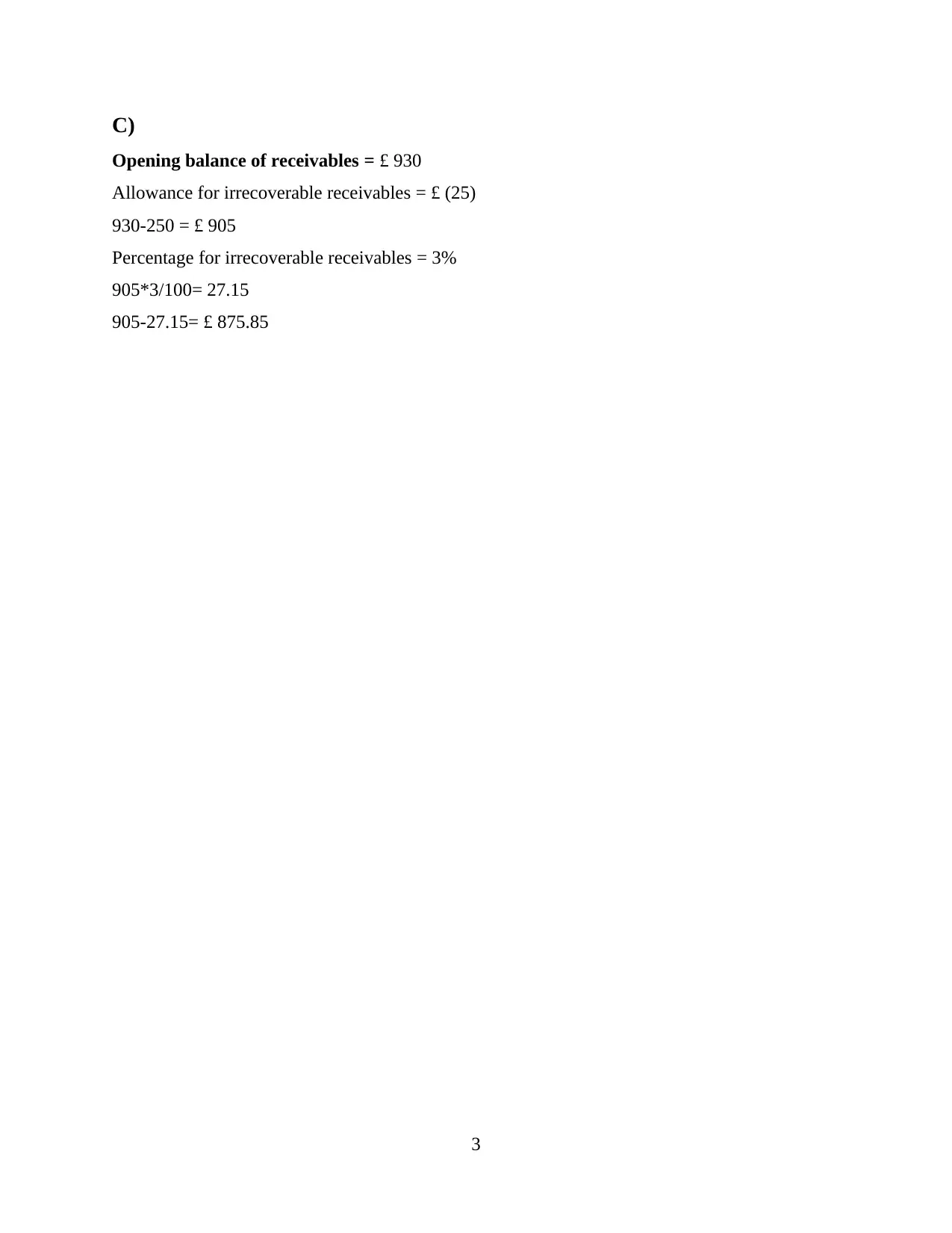

This document presents a detailed solution to a financial accounting homework assignment, covering several key areas. The solution includes calculations for depreciation on buildings, plant and machinery, and lorries, along with the profit or loss on the disposal of assets. It also explains the concept of non-current assets, their classification (property, plant, equipment, and goodwill), and the adjustments involved in their valuation. Furthermore, the assignment addresses the calculation of allowance for irrecoverable receivables, providing a step-by-step breakdown of the process. This resource from Desklib offers students a comprehensive understanding of these critical accounting principles.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.