Financial Accounting 1 Assignment: Detailed Solutions Provided

VerifiedAdded on 2022/12/16

|18

|2500

|205

Homework Assignment

AI Summary

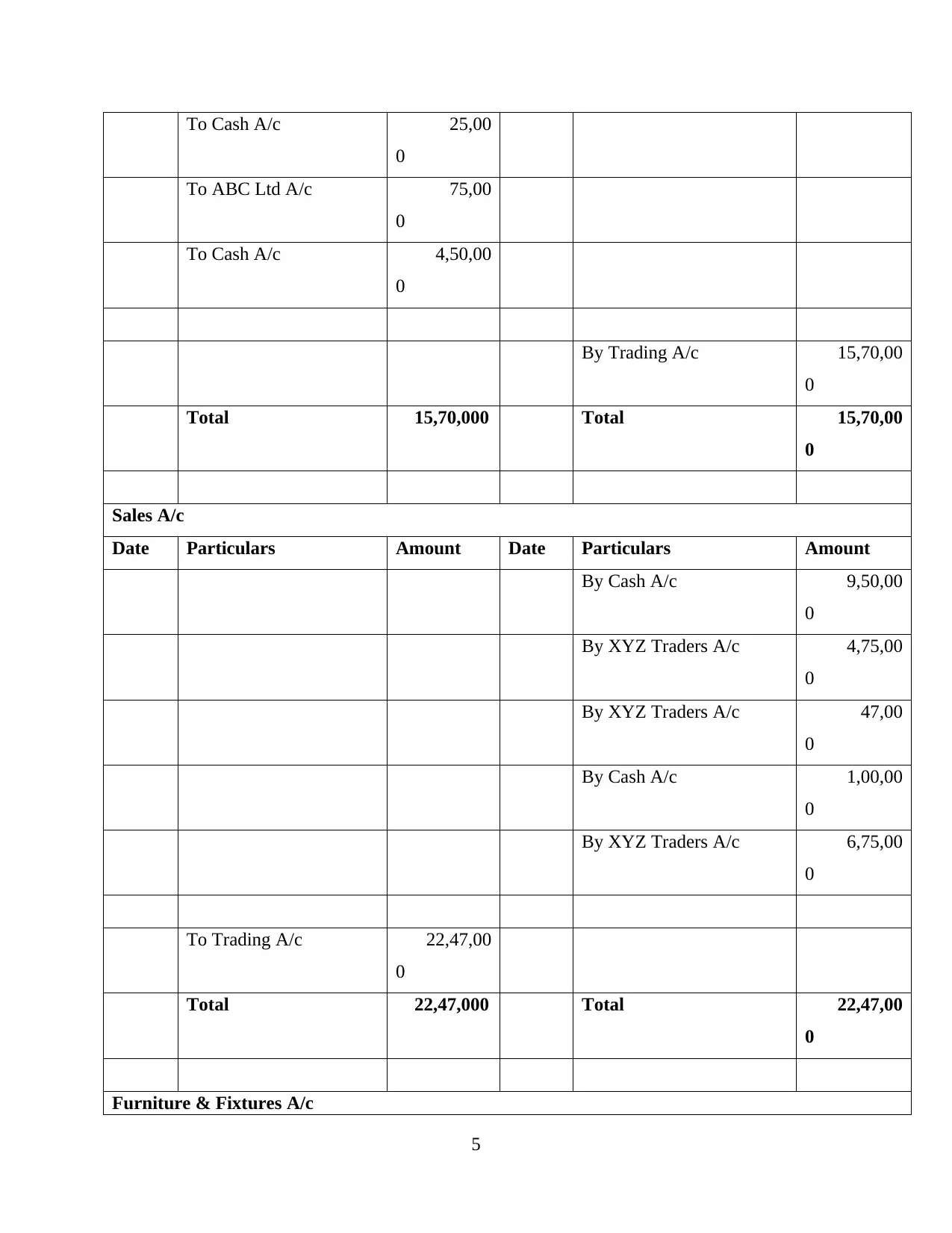

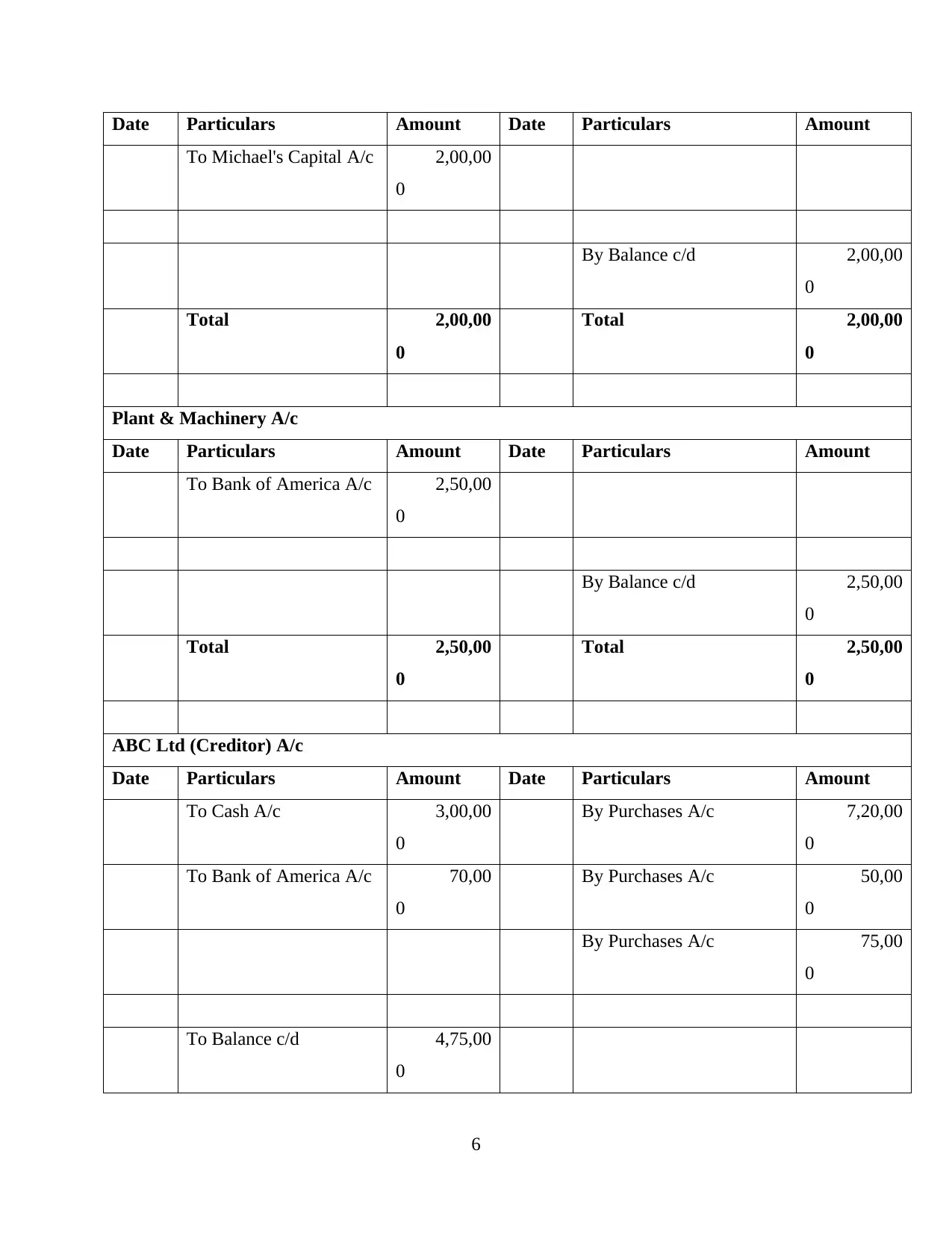

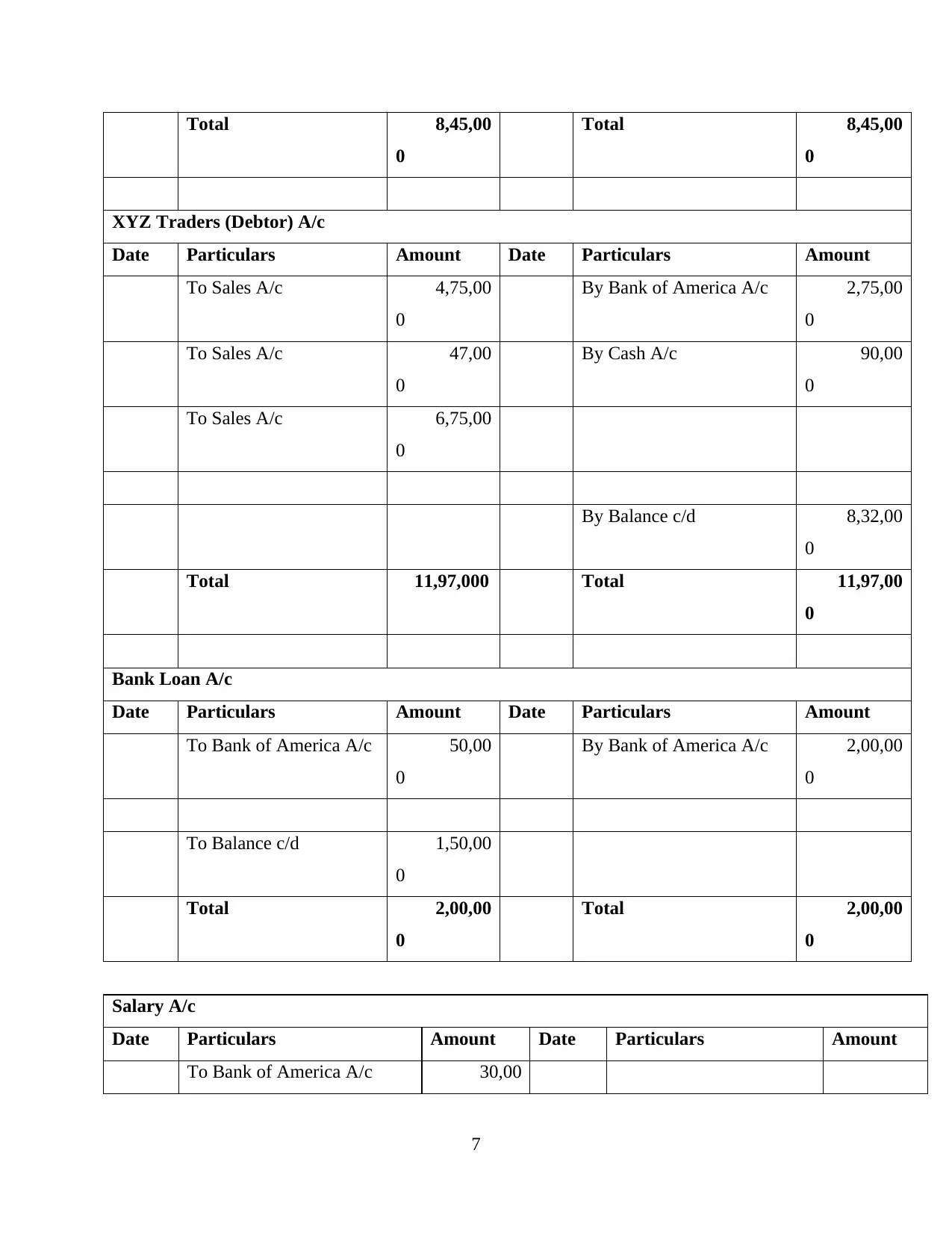

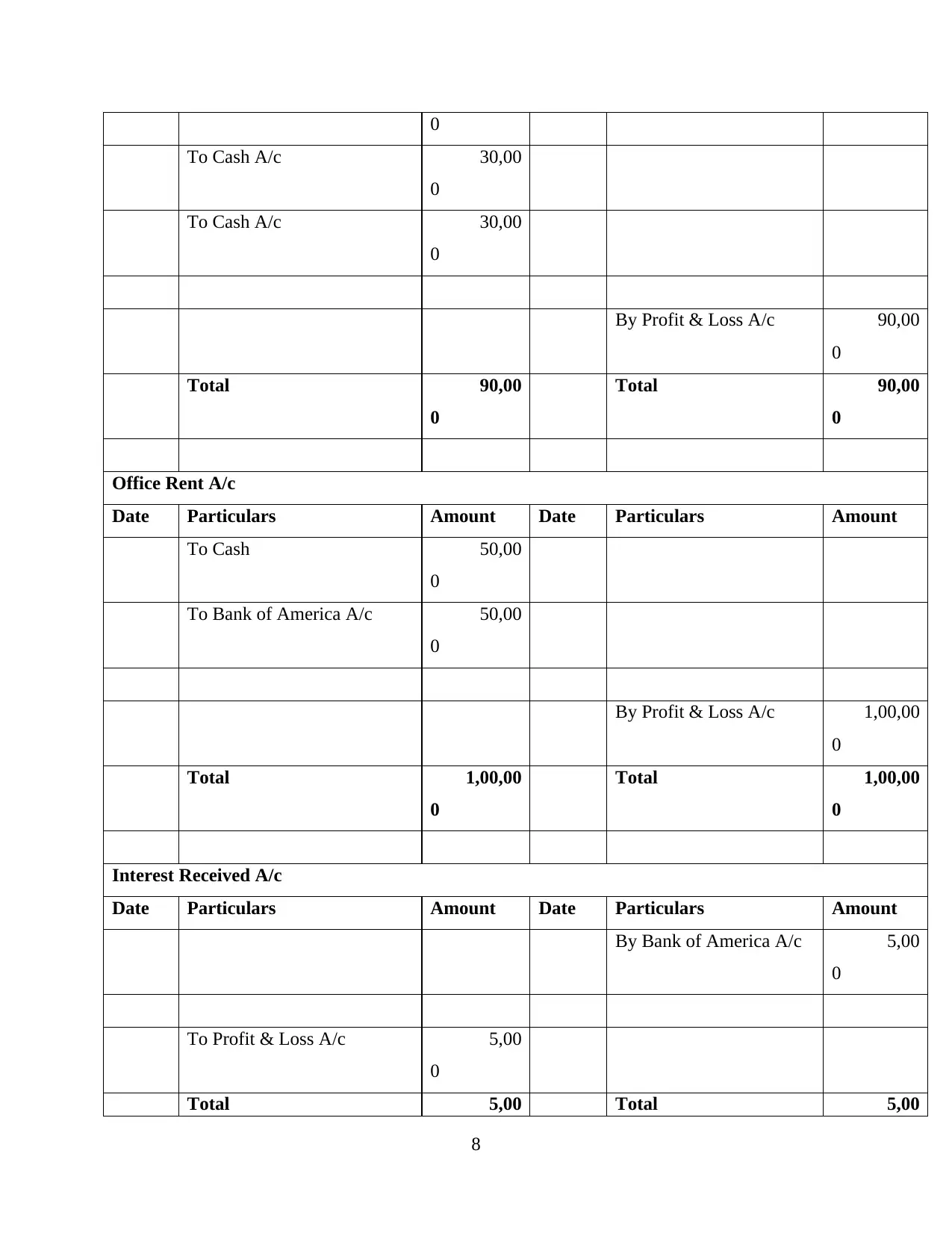

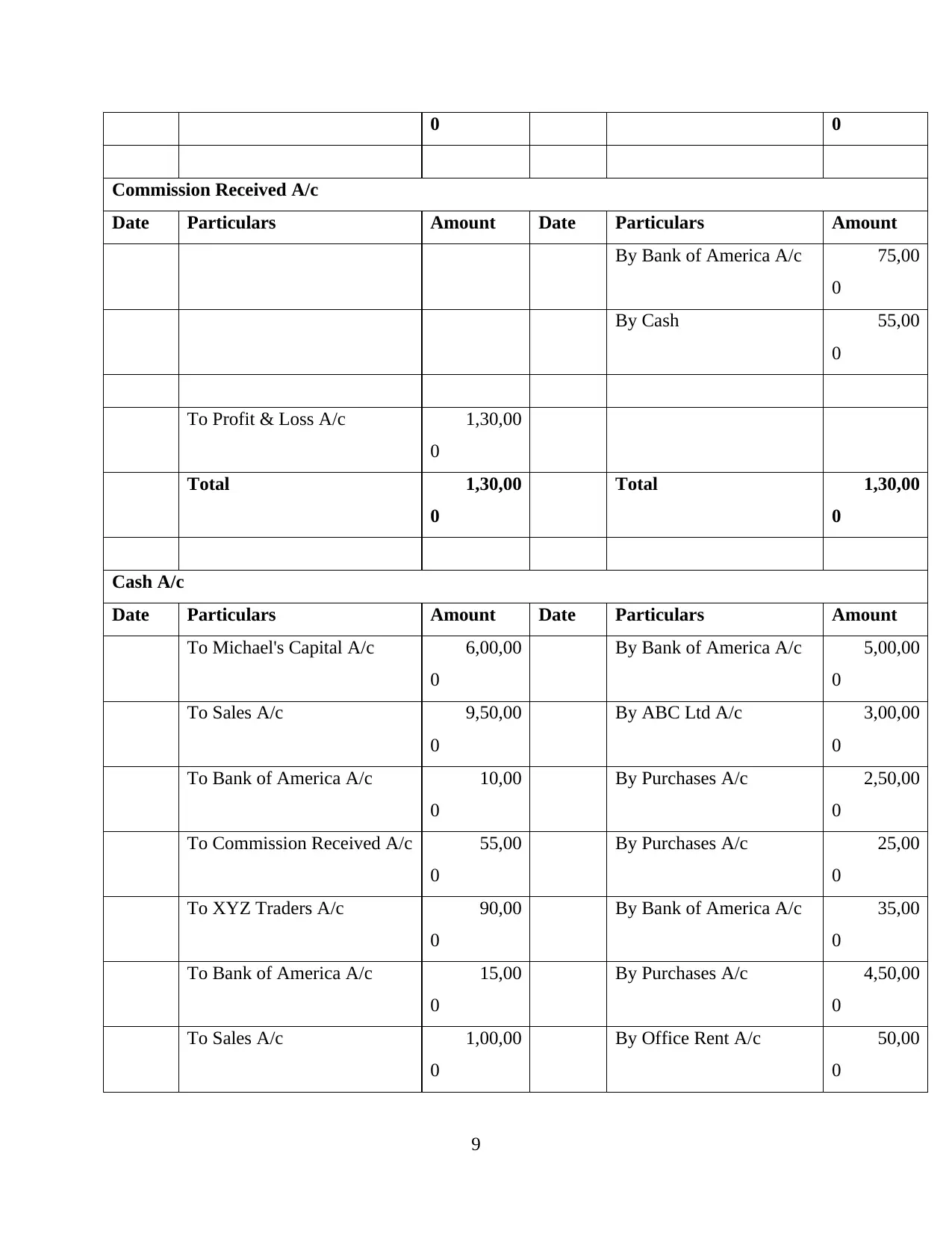

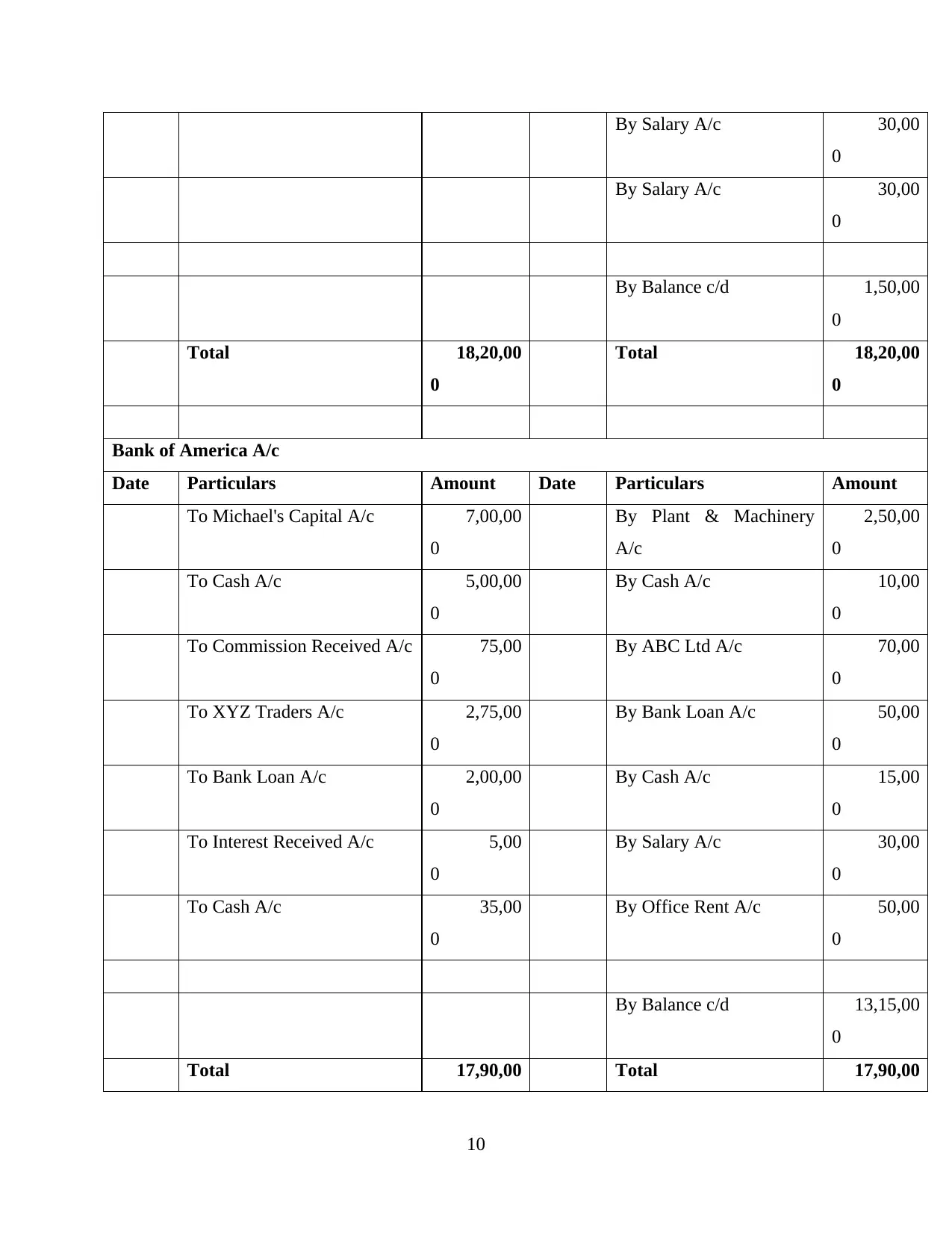

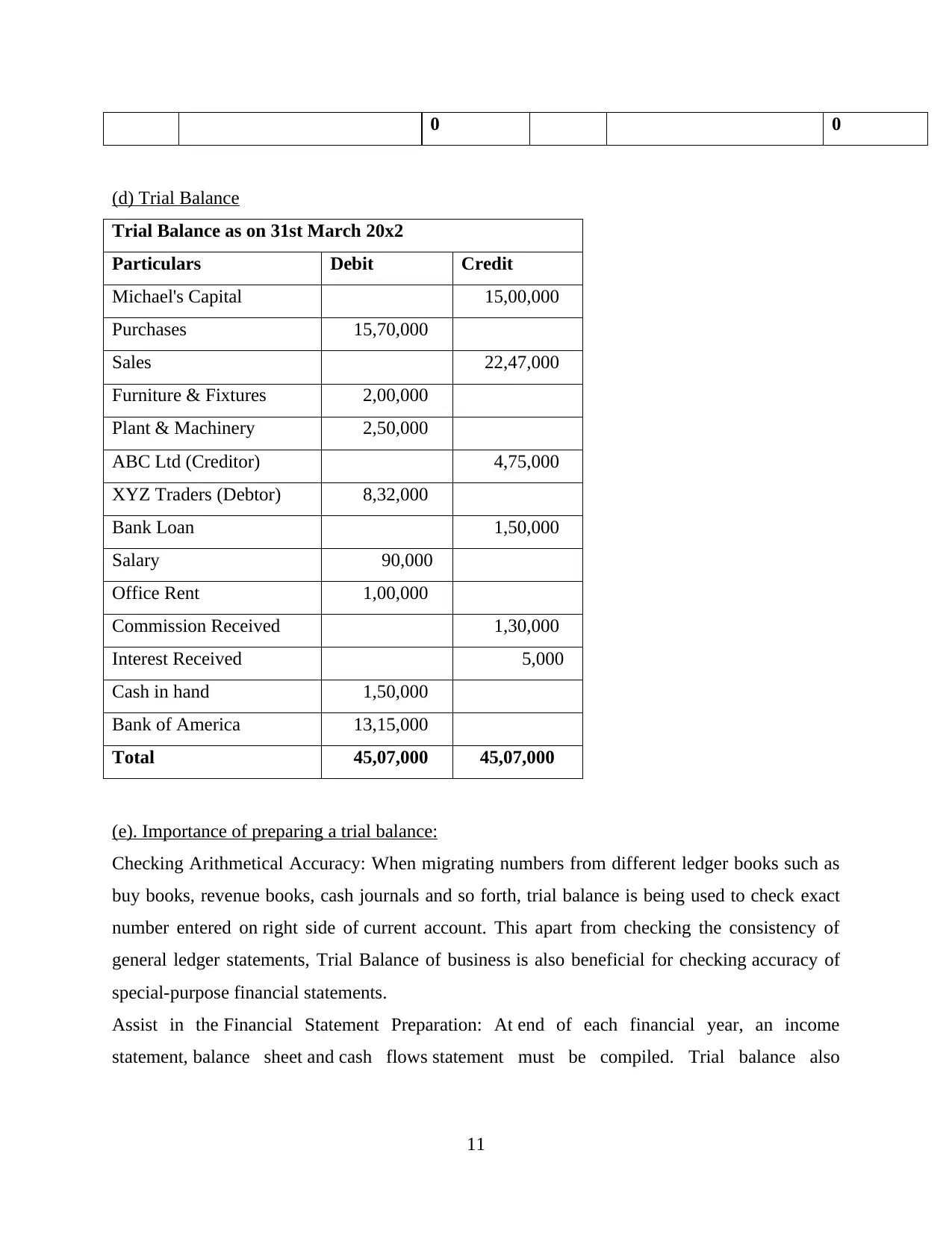

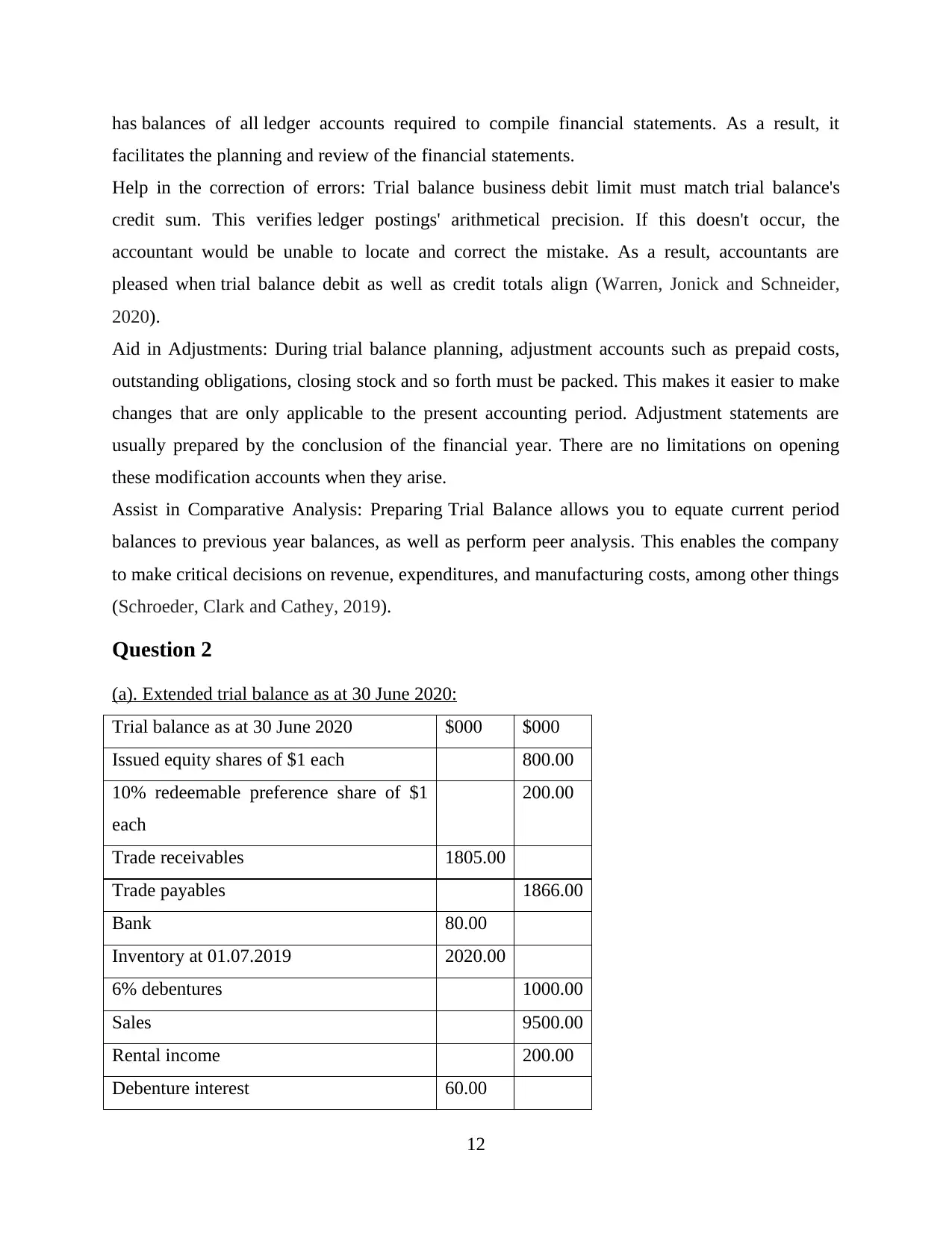

This assignment solution for Financial Accounting 1 encompasses three main questions addressing fundamental accounting principles and practices. Question 1 delves into the recording of transactions, the creation of ledger accounts (including capital, purchases, sales, and others), and the preparation and importance of a trial balance. Question 2 focuses on the preparation of financial statements, specifically the statement of profit or loss and the statement of financial position, adhering to IAS 1, and also explores key accounting concepts such as consistency and materiality. Question 3 provides a sales ledger control account and explores how control accounts support effective financial management. The solution provides detailed workings and explanations for each question, making it a valuable resource for students studying financial accounting.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.