University Financial Accounting: Consolidated Balance Sheet Analysis

VerifiedAdded on 2022/08/25

|8

|898

|24

Homework Assignment

AI Summary

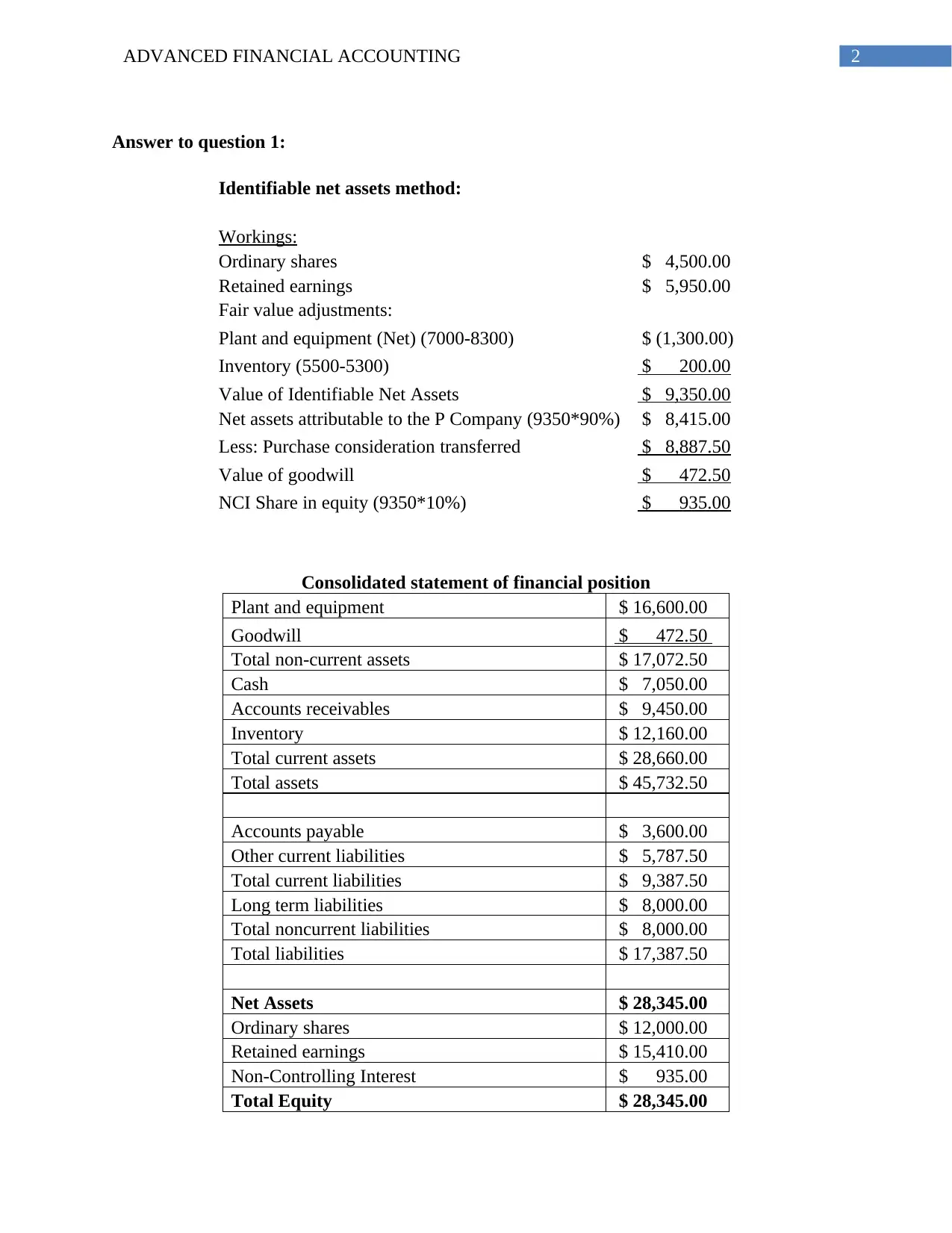

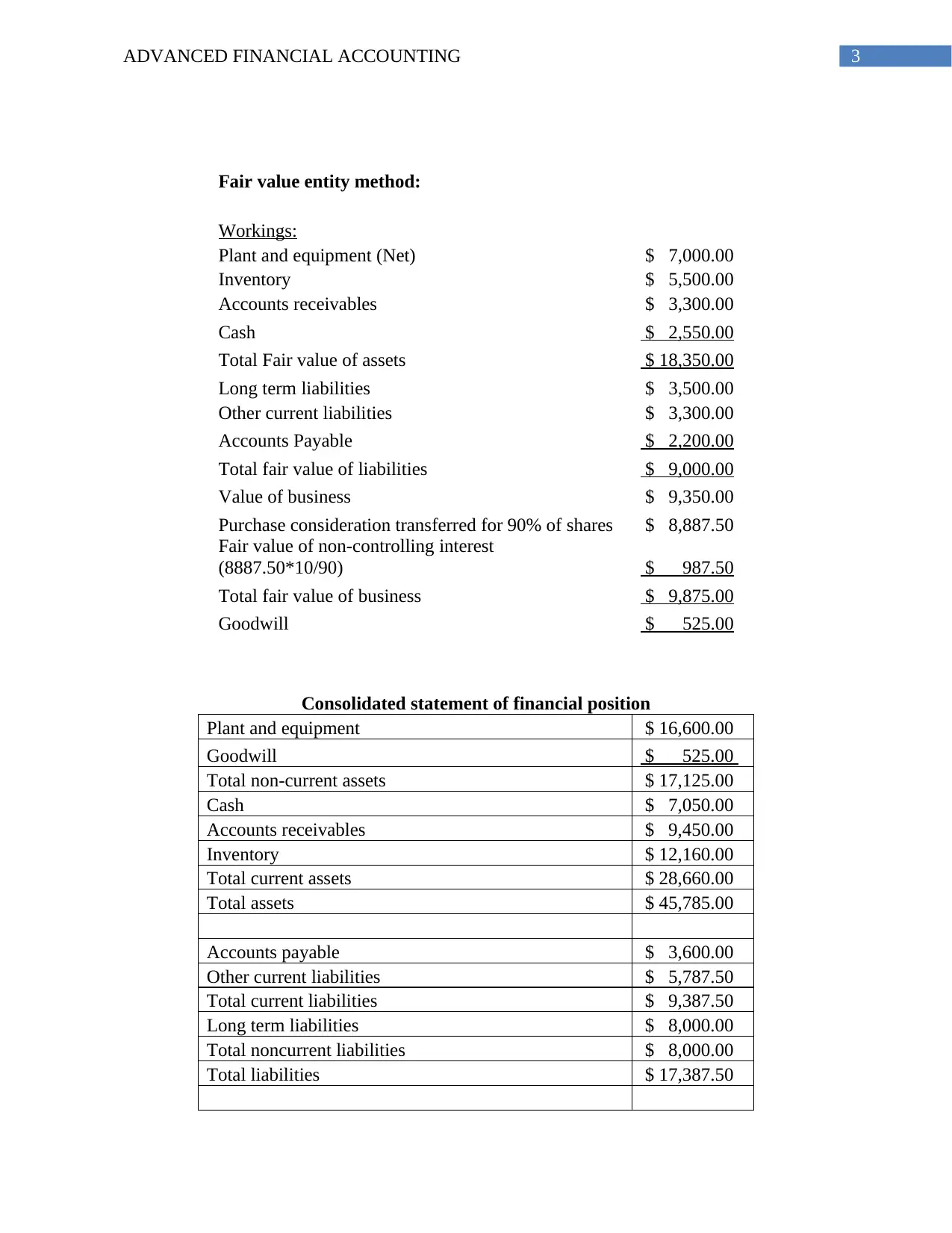

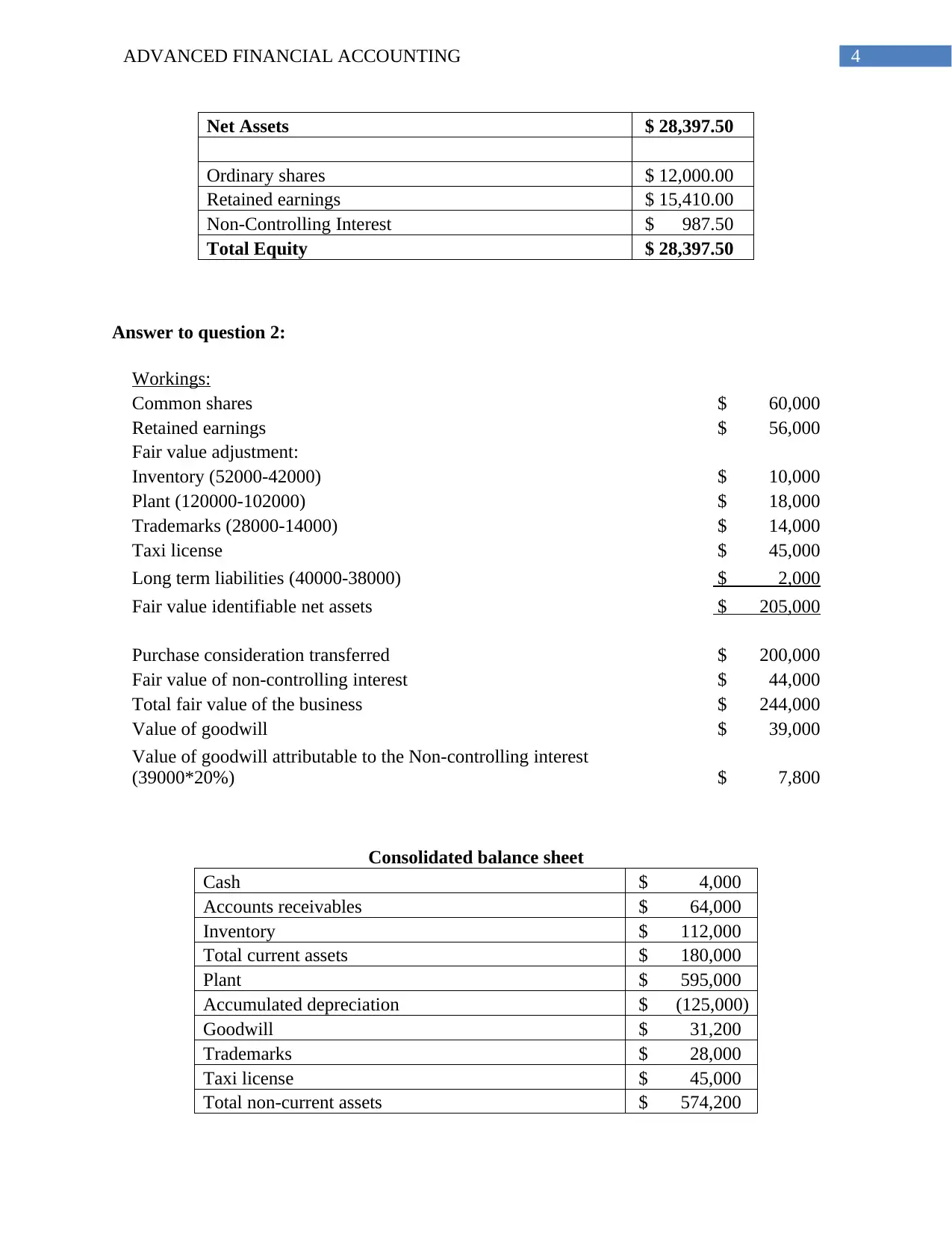

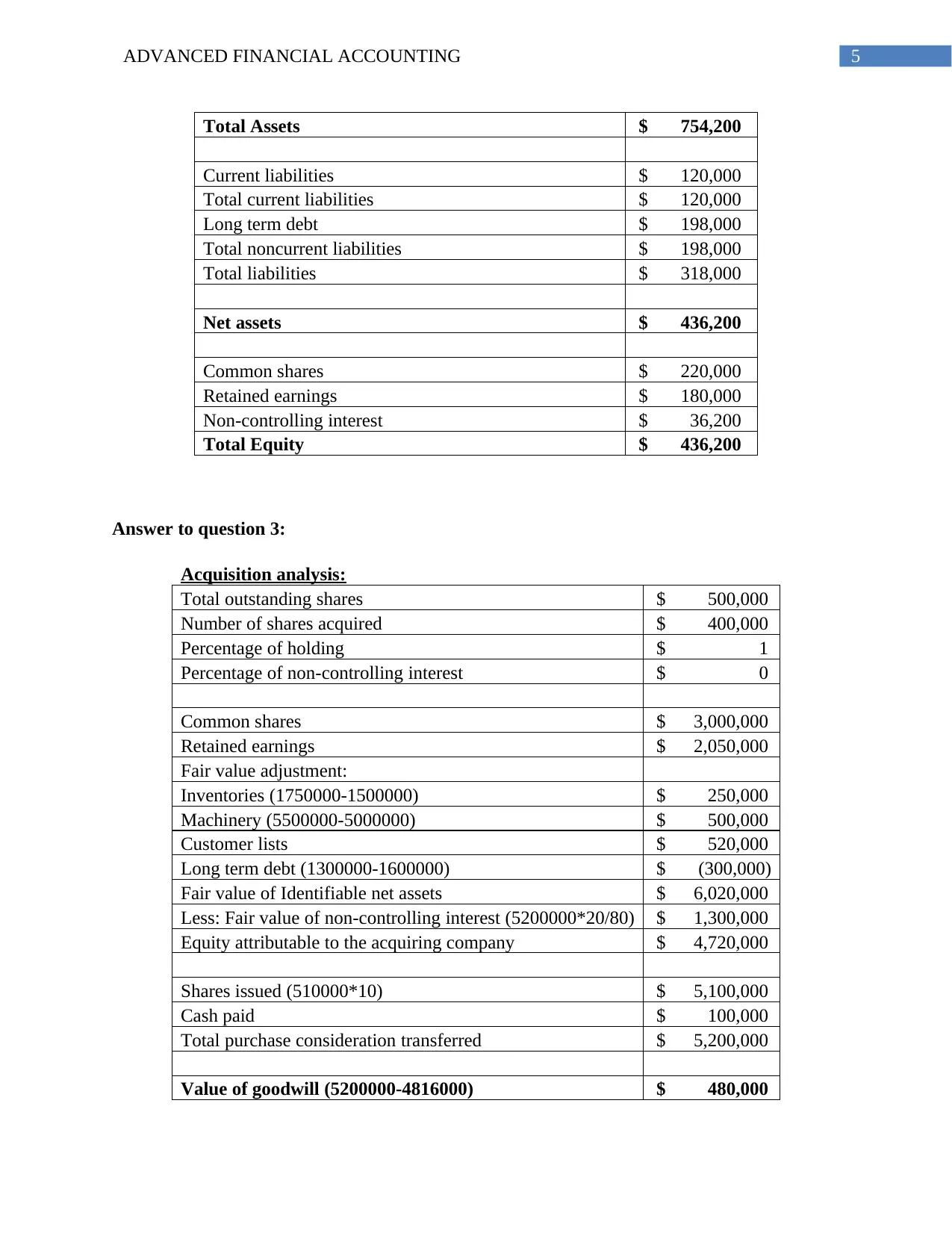

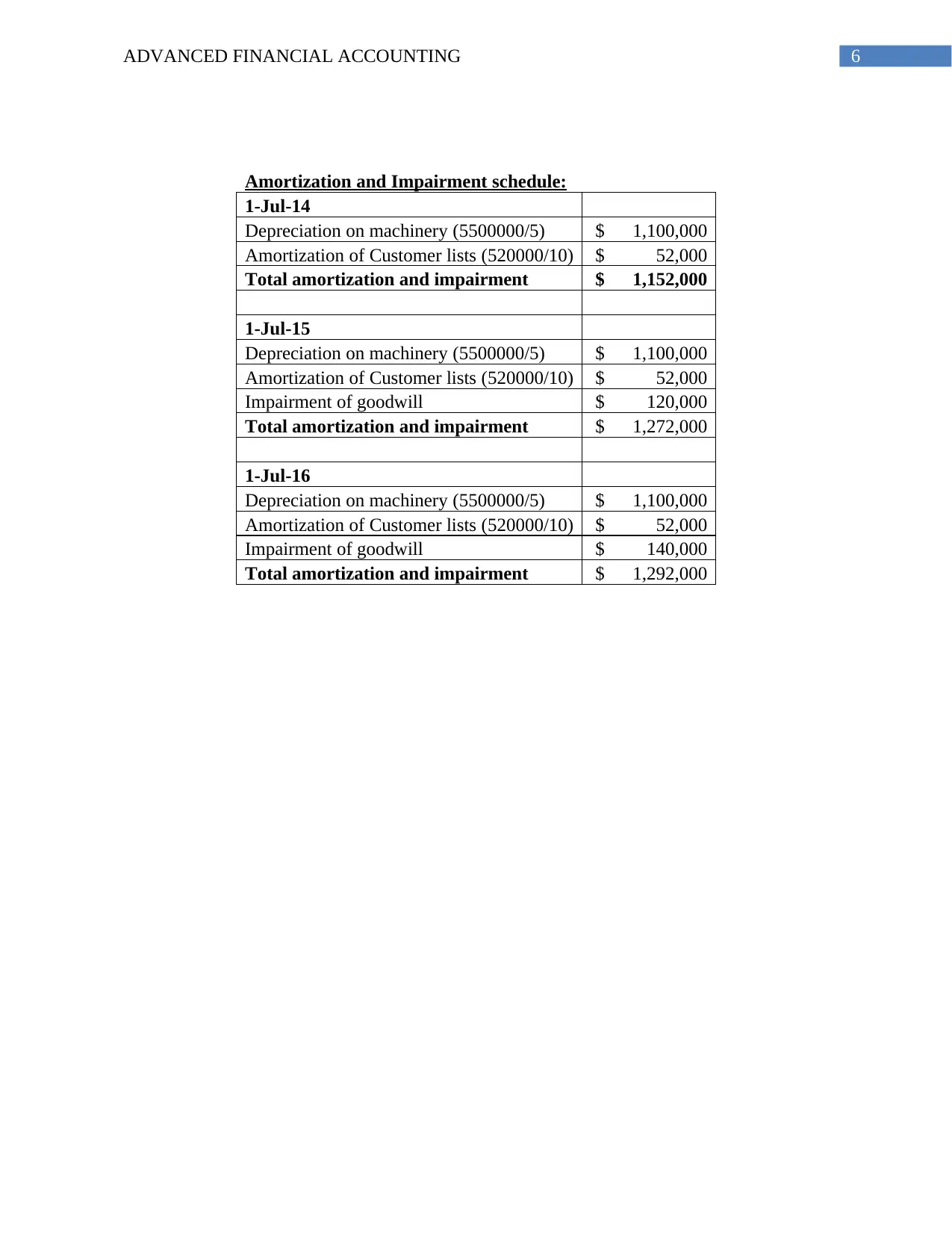

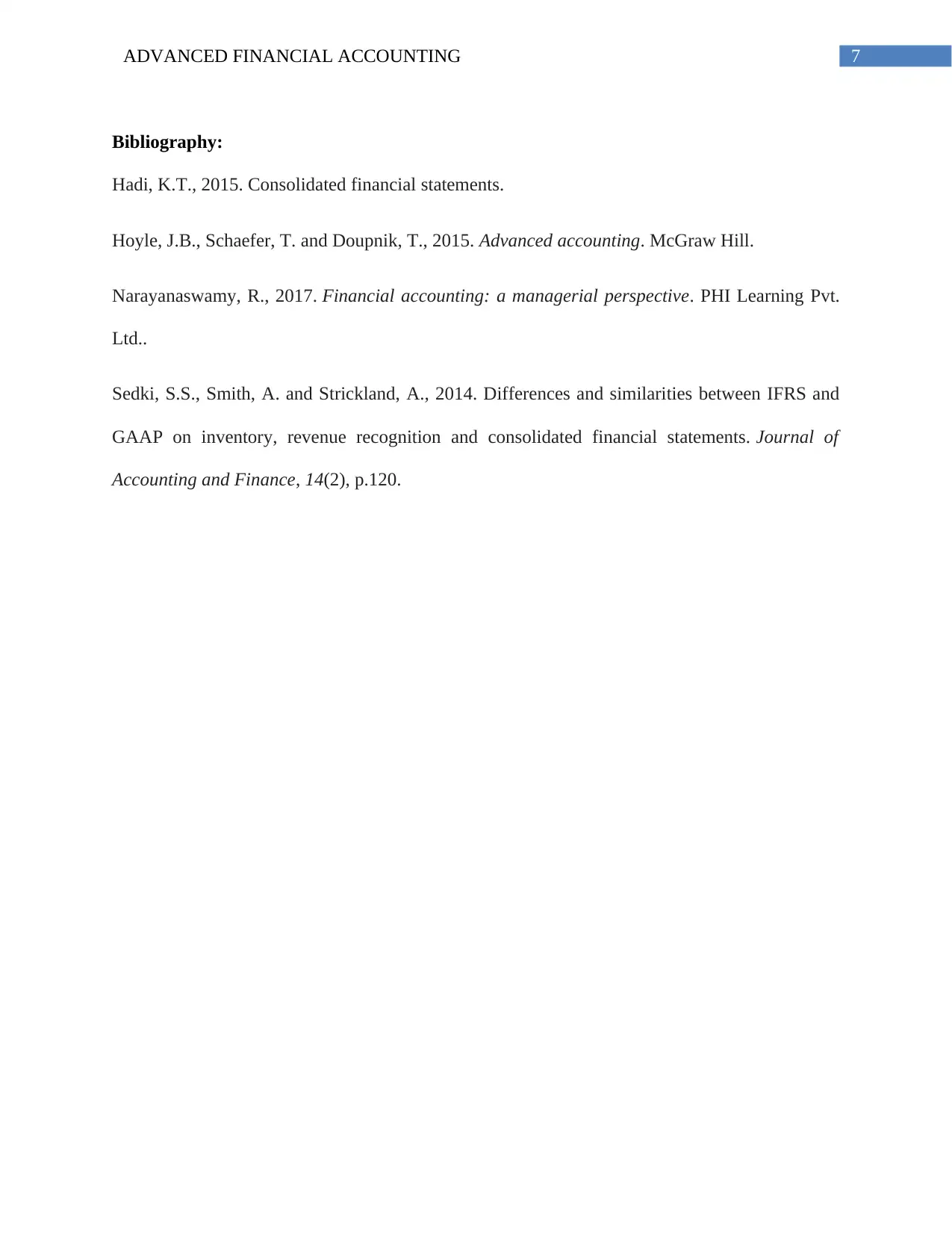

This assignment provides a comprehensive solution to advanced financial accounting problems, specifically focusing on the preparation of consolidated financial statements. The solution addresses three key questions: The first question involves preparing a consolidated statement of financial position using both the identifiable net assets method and the fair value entity method, demonstrating the calculation of goodwill and non-controlling interest. The second question requires the preparation of a consolidated balance sheet, incorporating fair value adjustments for various assets and liabilities, and calculating goodwill. The third question analyzes an acquisition scenario, including the calculation of equity attributable to the acquiring company, amortization schedules, and impairment of goodwill. The assignment covers key concepts such as consolidation methods, fair value adjustments, goodwill calculations, non-controlling interest, and balance sheet preparation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.