Financial Accounting Homework: Detailed Client Solutions Analysis

VerifiedAdded on 2020/06/05

|30

|3307

|315

Homework Assignment

AI Summary

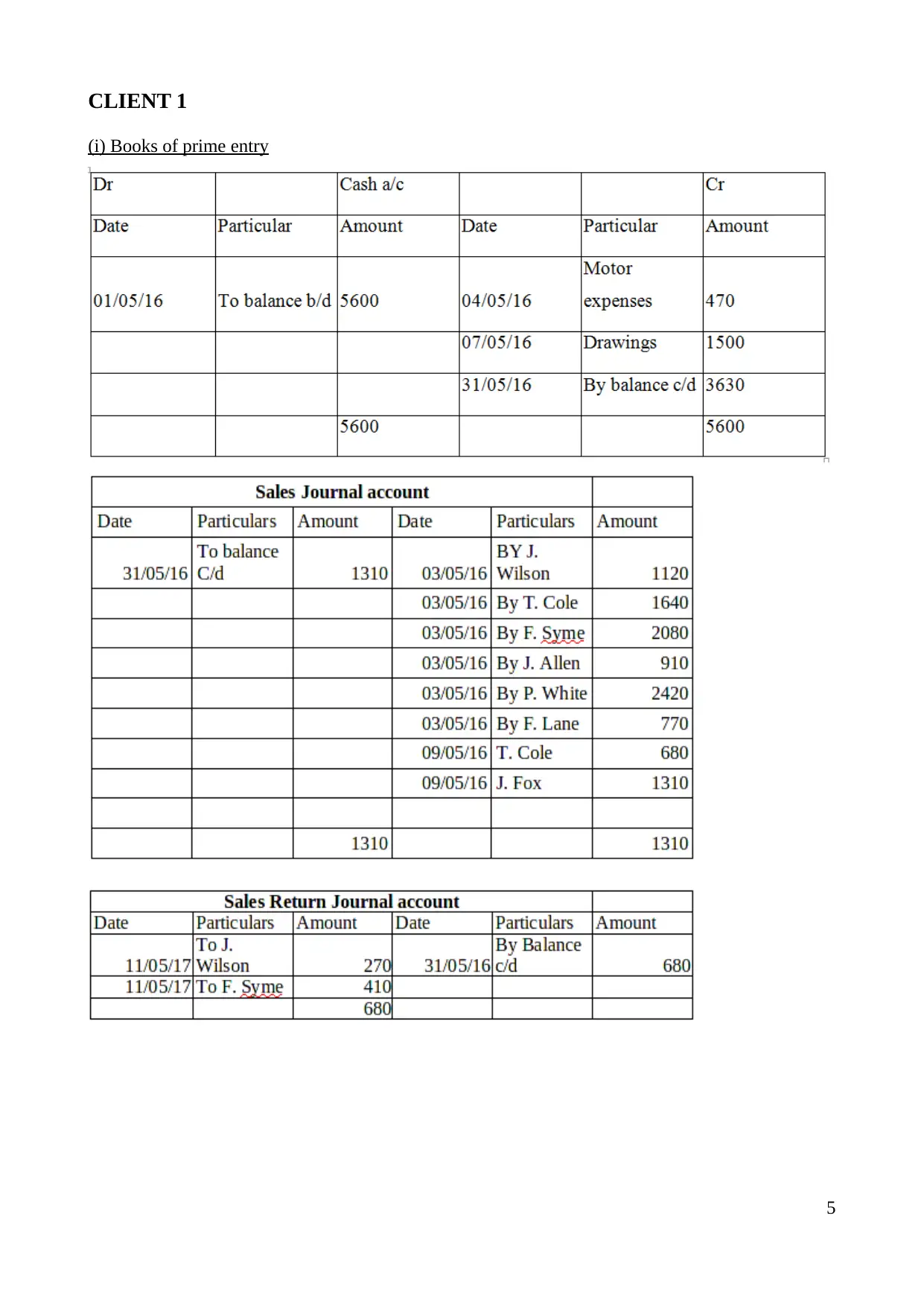

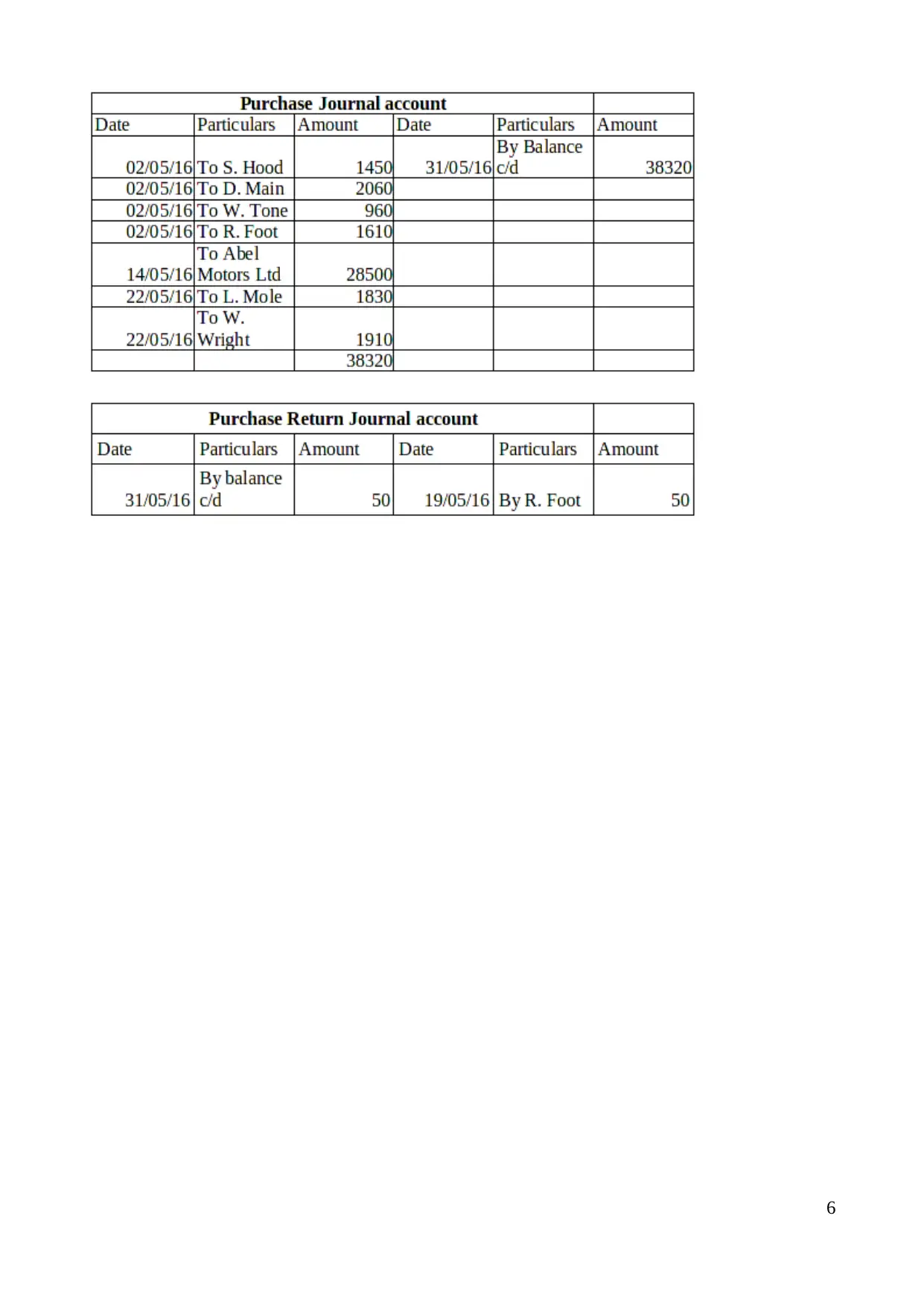

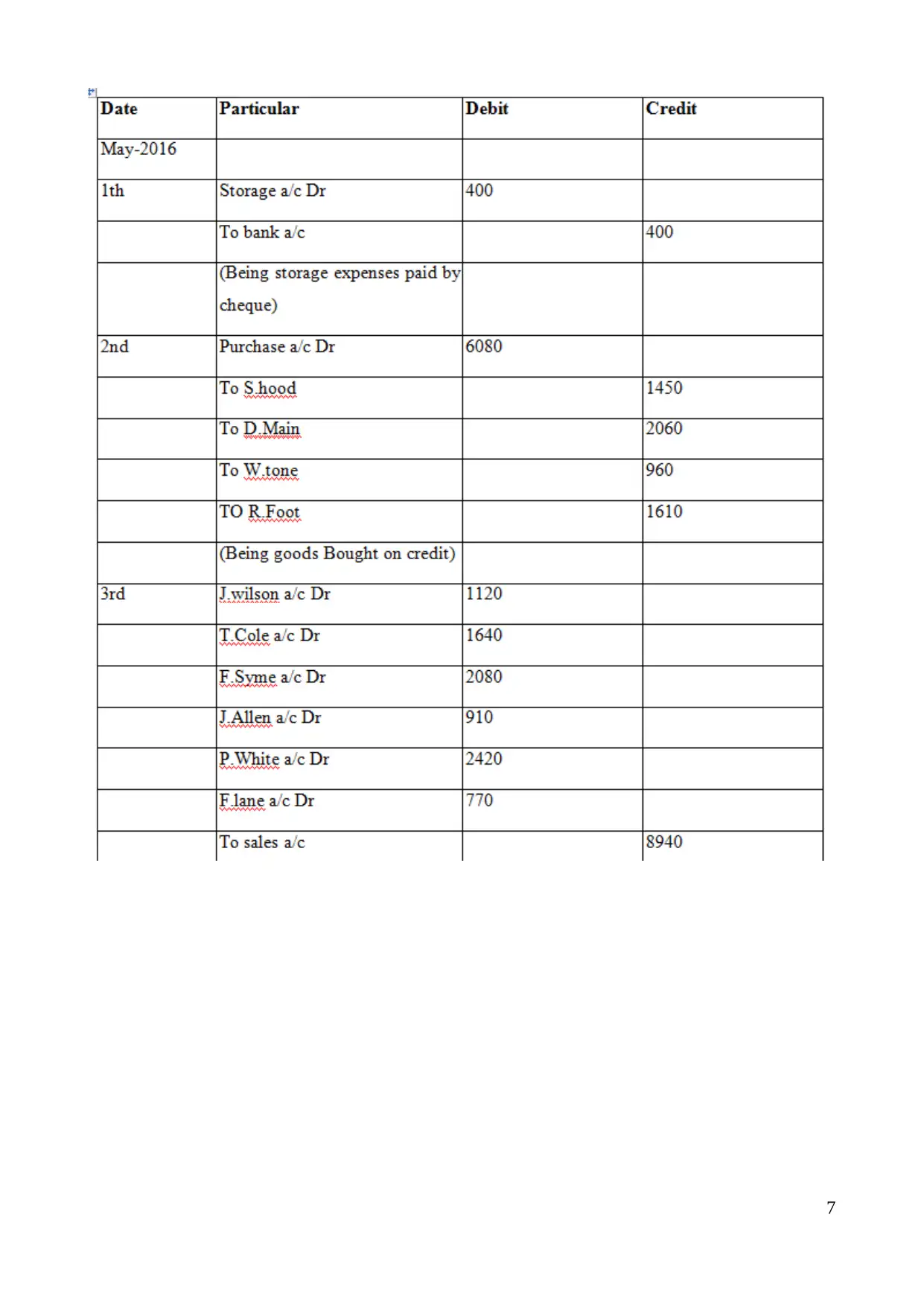

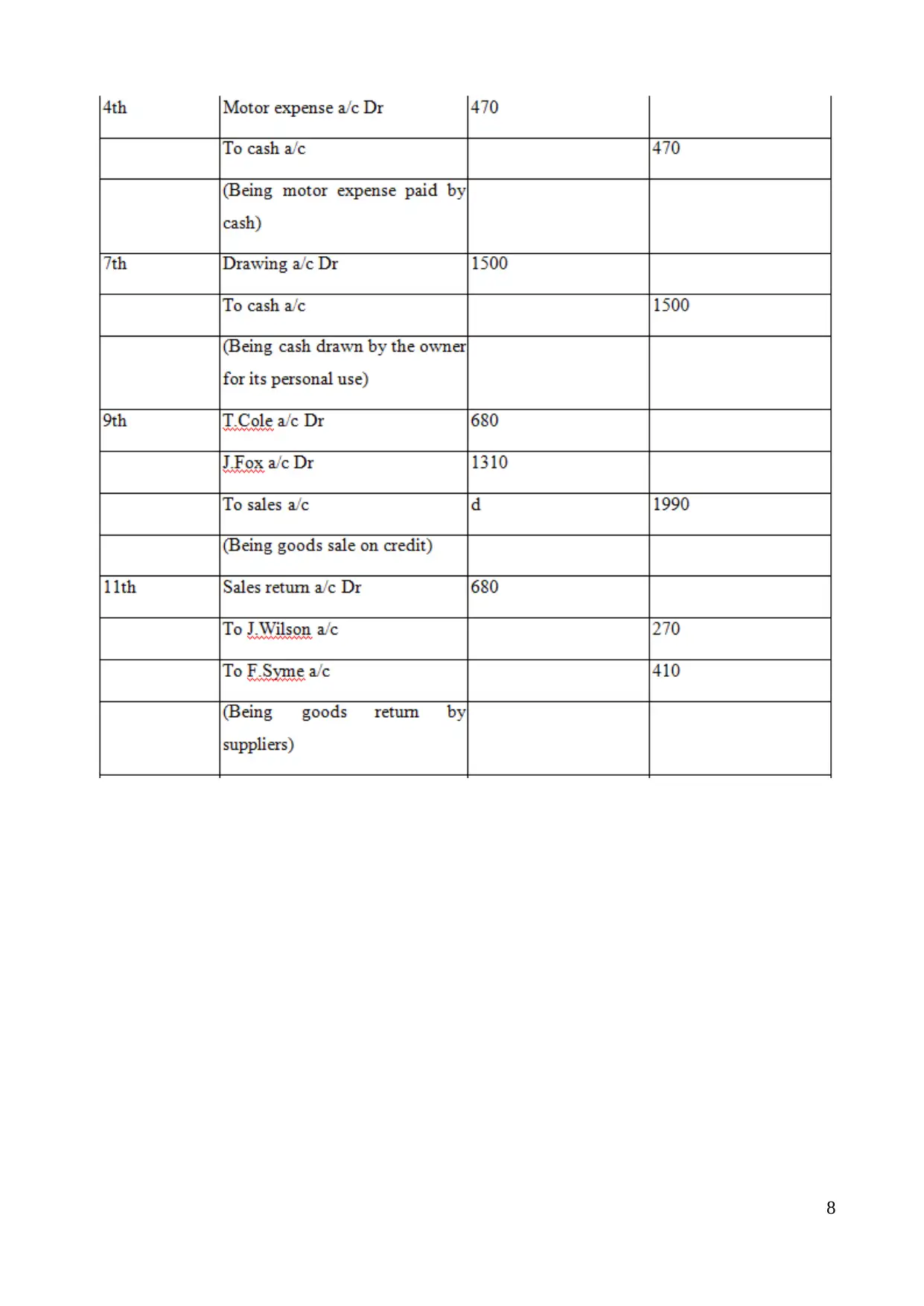

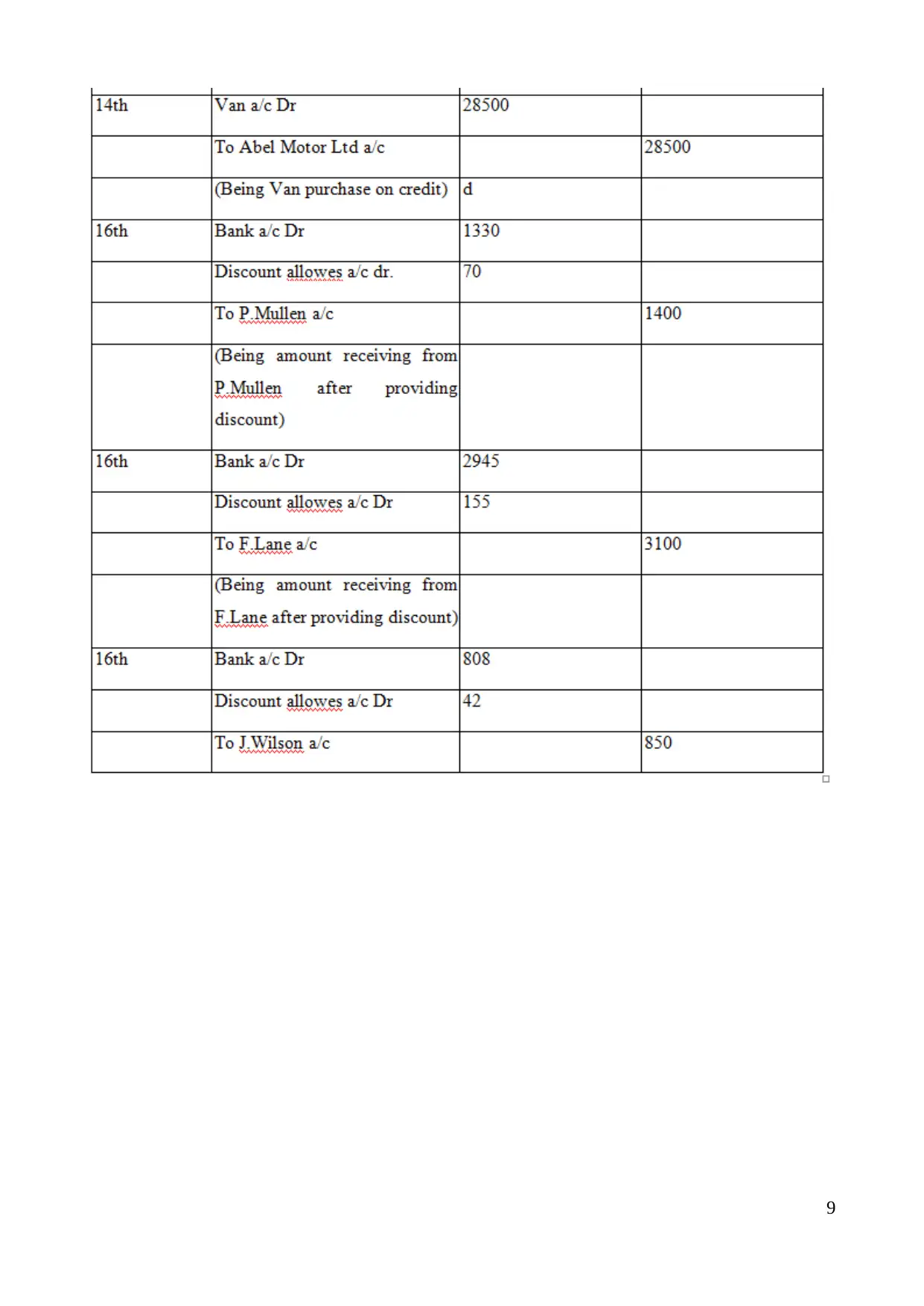

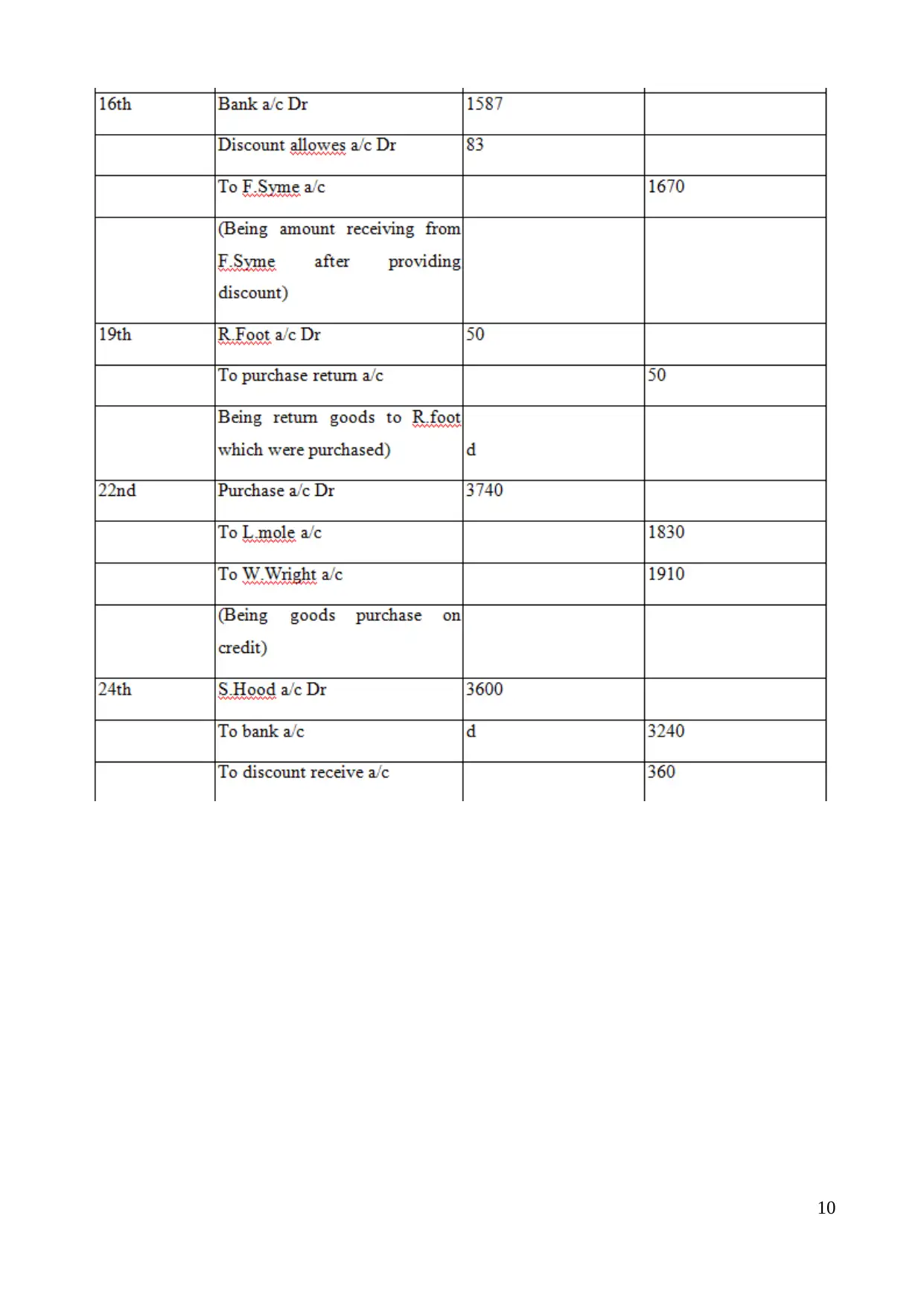

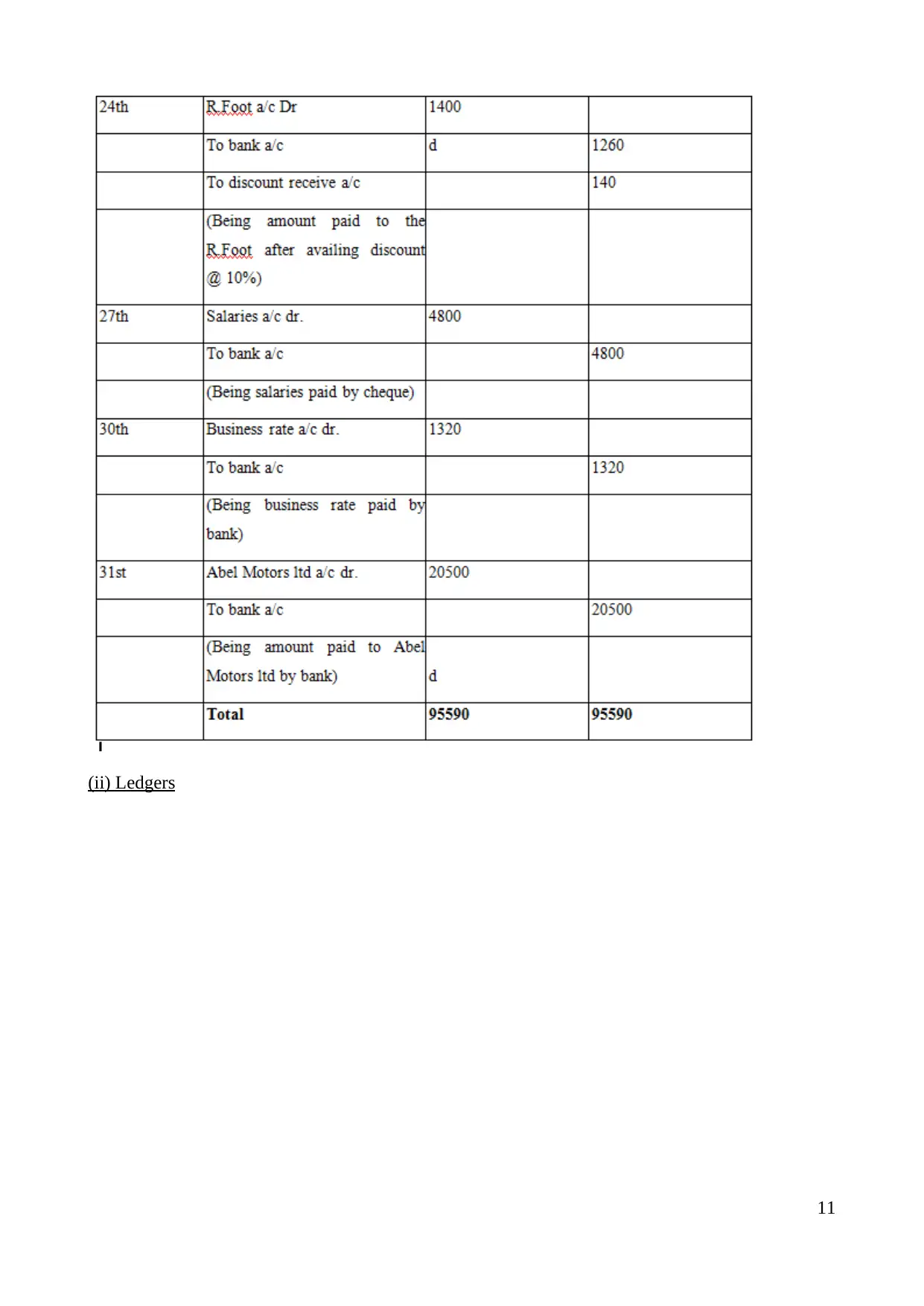

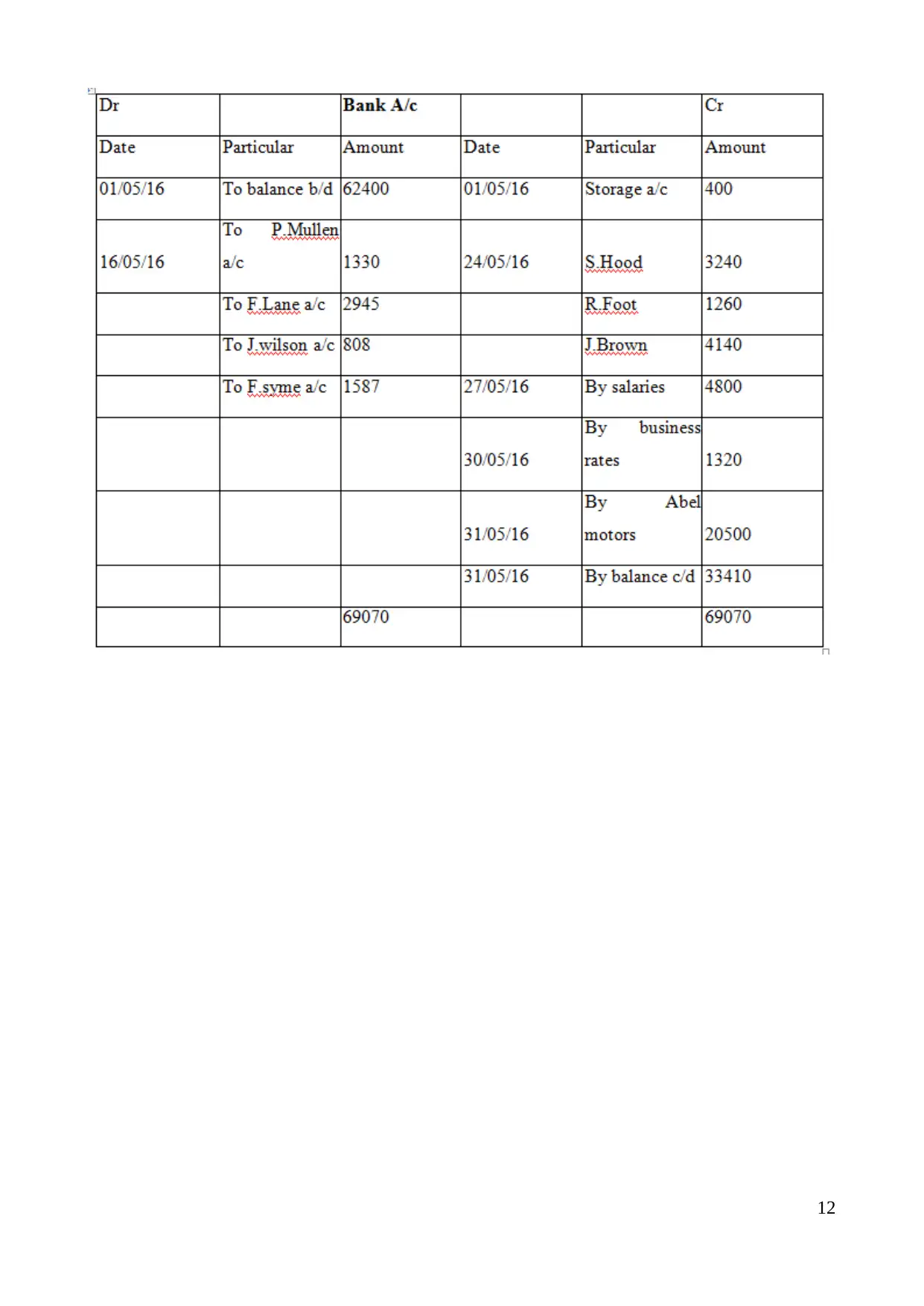

This financial accounting assignment solution provides a comprehensive overview of various accounting concepts and their practical application through multiple client scenarios. The solution covers the definition of financial accounting, relevant regulations, accounting rules, and principles like accrual and going concern. It includes detailed examples of books of prime entry, ledgers, and trial balances for Client 1. Client 2 and 3 solutions feature the preparation of profit and loss accounts and statements of financial position, along with explanations of consistency, prudence, and depreciation methods. Client 4 focuses on bank reconciliation statements, updated cash books, and the reasons for balance variations. Client 5 covers sales and purchase ledger control accounts, explaining their purpose. Finally, Client 6 addresses suspense accounts and journal entries for rectification. The assignment comprehensively demonstrates the application of accounting principles and practices in real-world scenarios.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.