Financial Accounting Homework: Stakeholders and Statements

VerifiedAdded on 2021/02/22

|25

|2659

|436

Homework Assignment

AI Summary

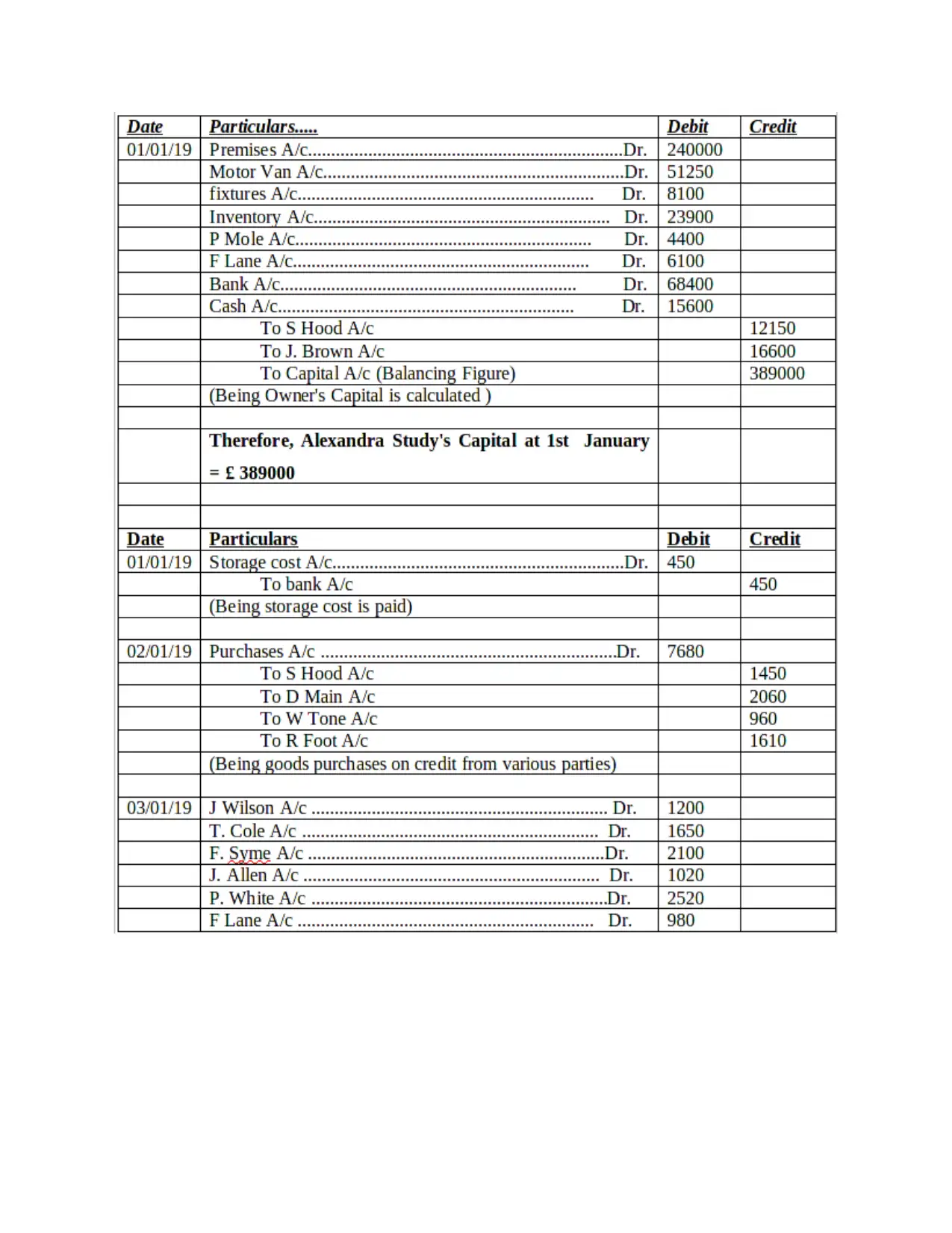

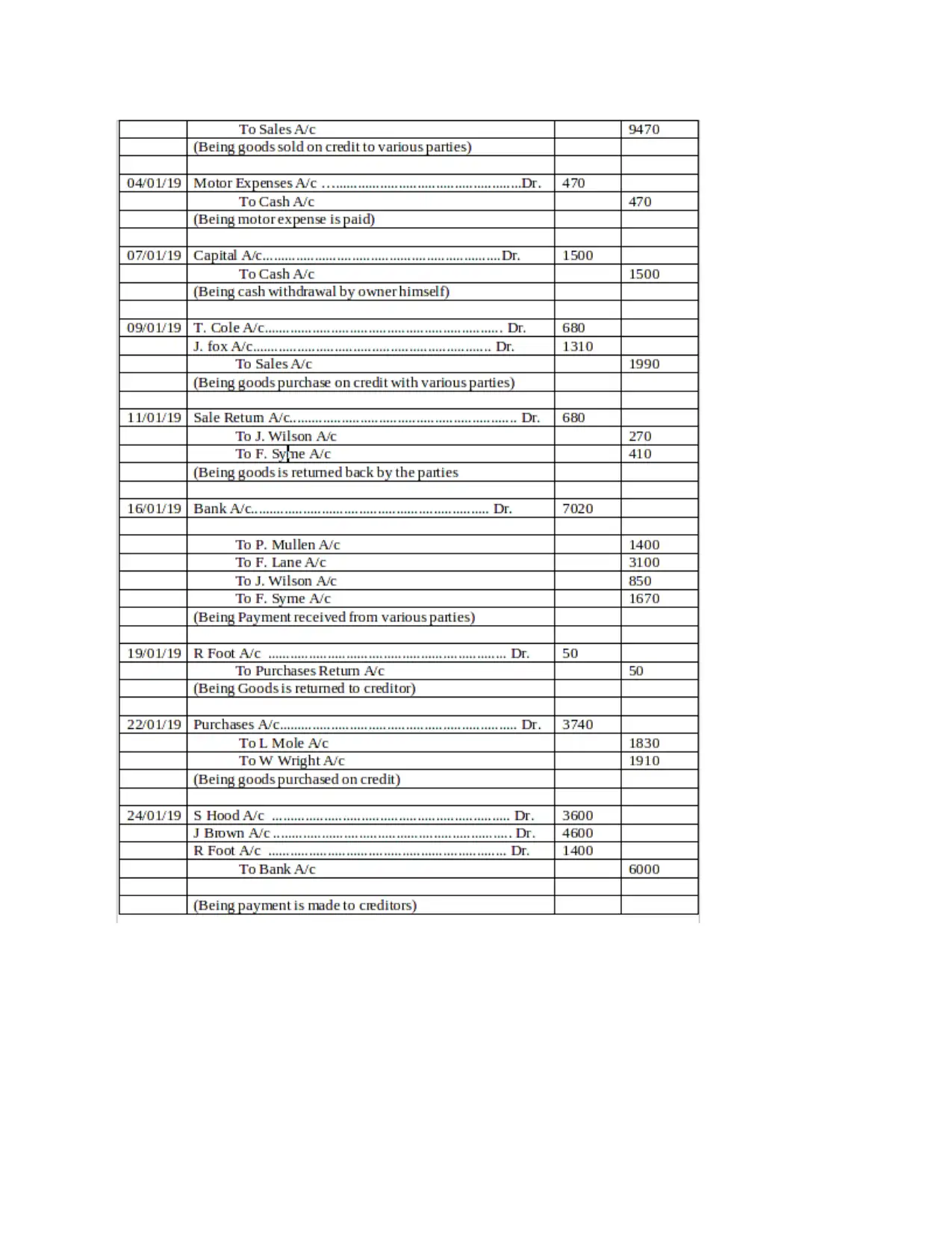

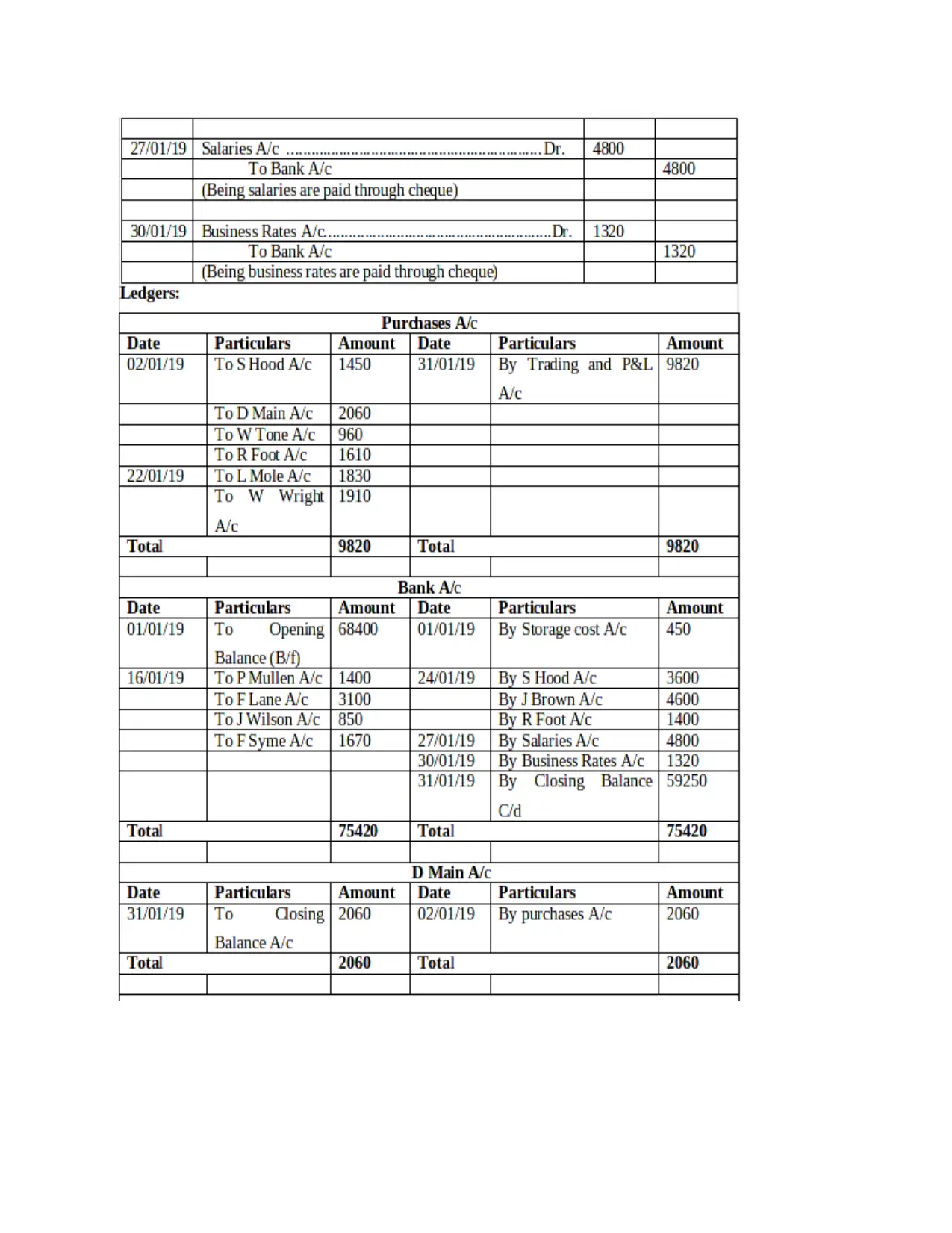

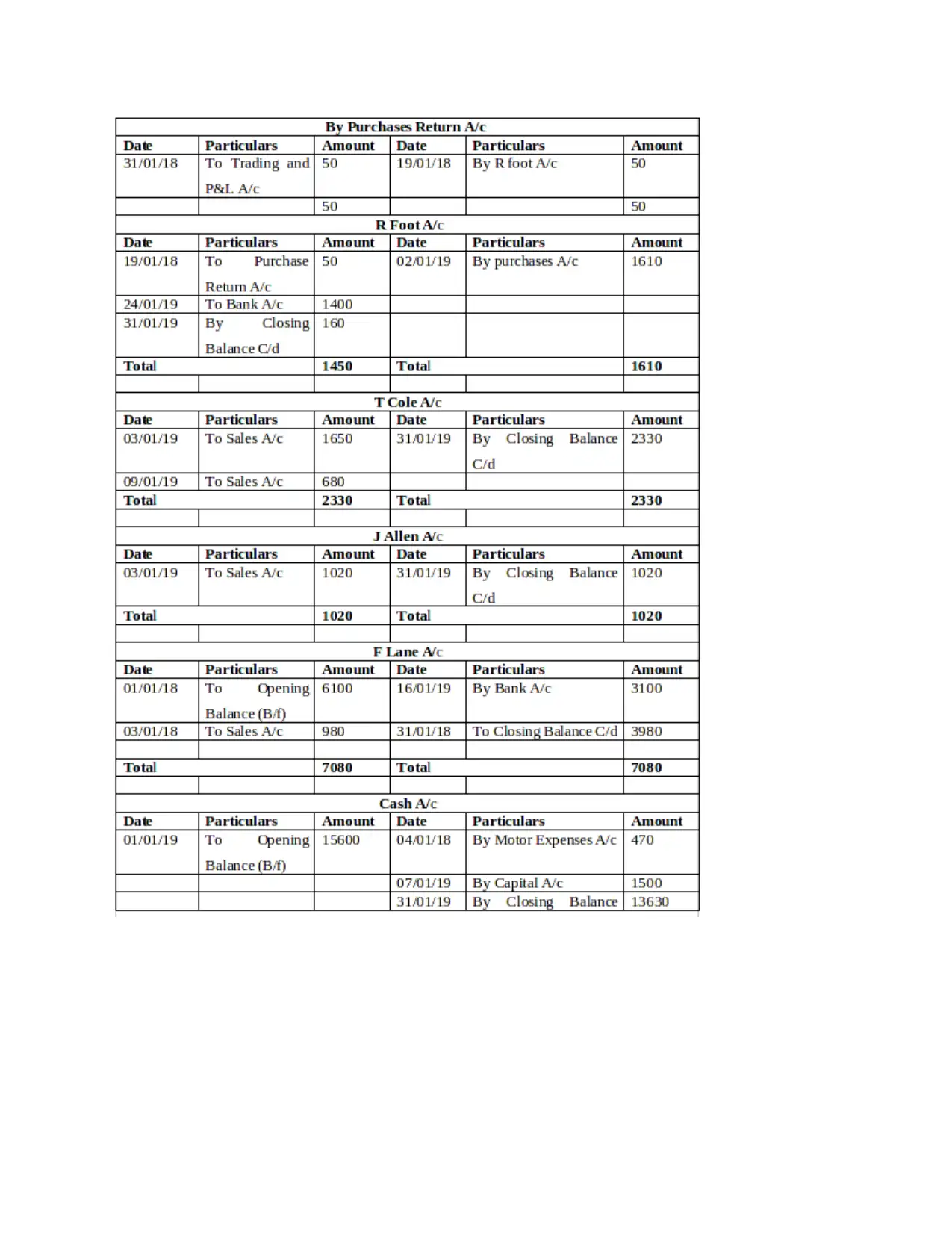

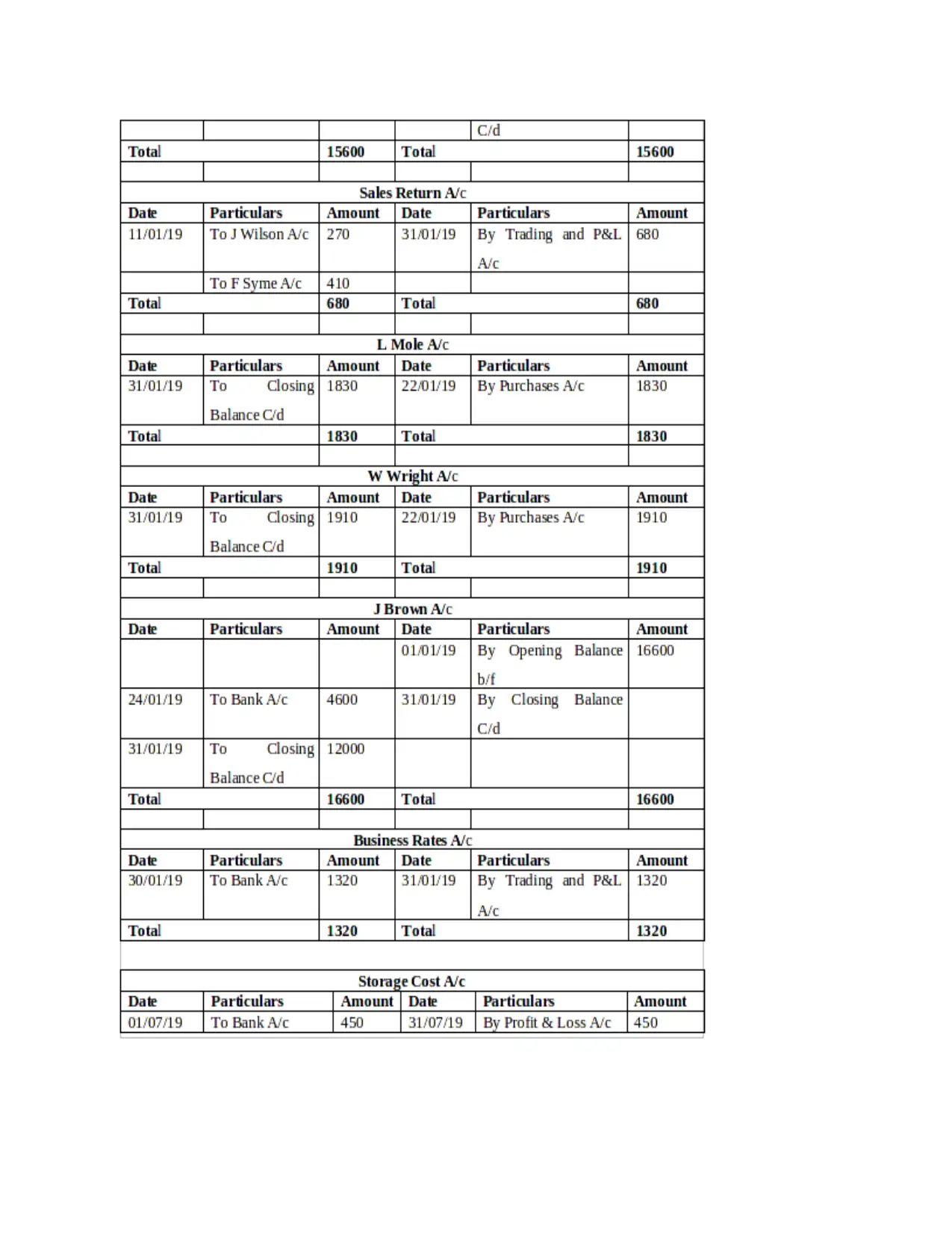

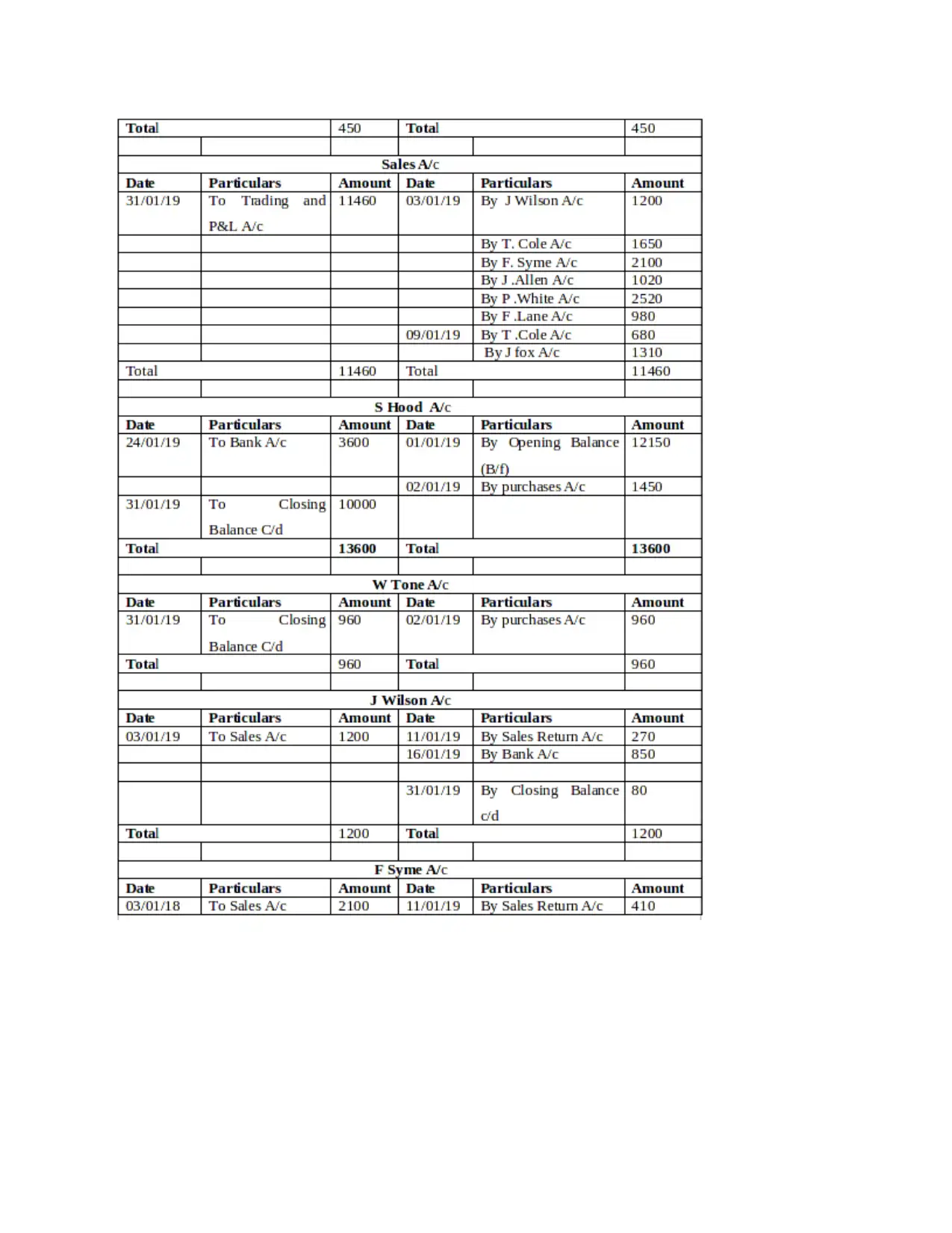

This financial accounting assignment solution covers various aspects of financial accounting, including the definition and purpose of financial accounting, internal and external stakeholders, and the preparation of financial statements. The assignment delves into journal entries and ledgers for different clients, demonstrating the application of accounting concepts such as consistency and prudence. It also explains depreciation methods (straight-line and reducing balance), differences between sole traders and limited companies' financial statements, bank reconciliation statements, control accounts, and suspense accounts. The solution provides detailed examples and calculations to illustrate these concepts, making it a comprehensive resource for understanding financial accounting principles and practices. The assignment also provides a practical understanding of how financial accounting is applied in real-world scenarios, such as in the context of a financial marketing consultancy company.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.