Financial Accounting Assignment Solution - Finance Module

VerifiedAdded on 2020/05/16

|11

|1167

|257

Homework Assignment

AI Summary

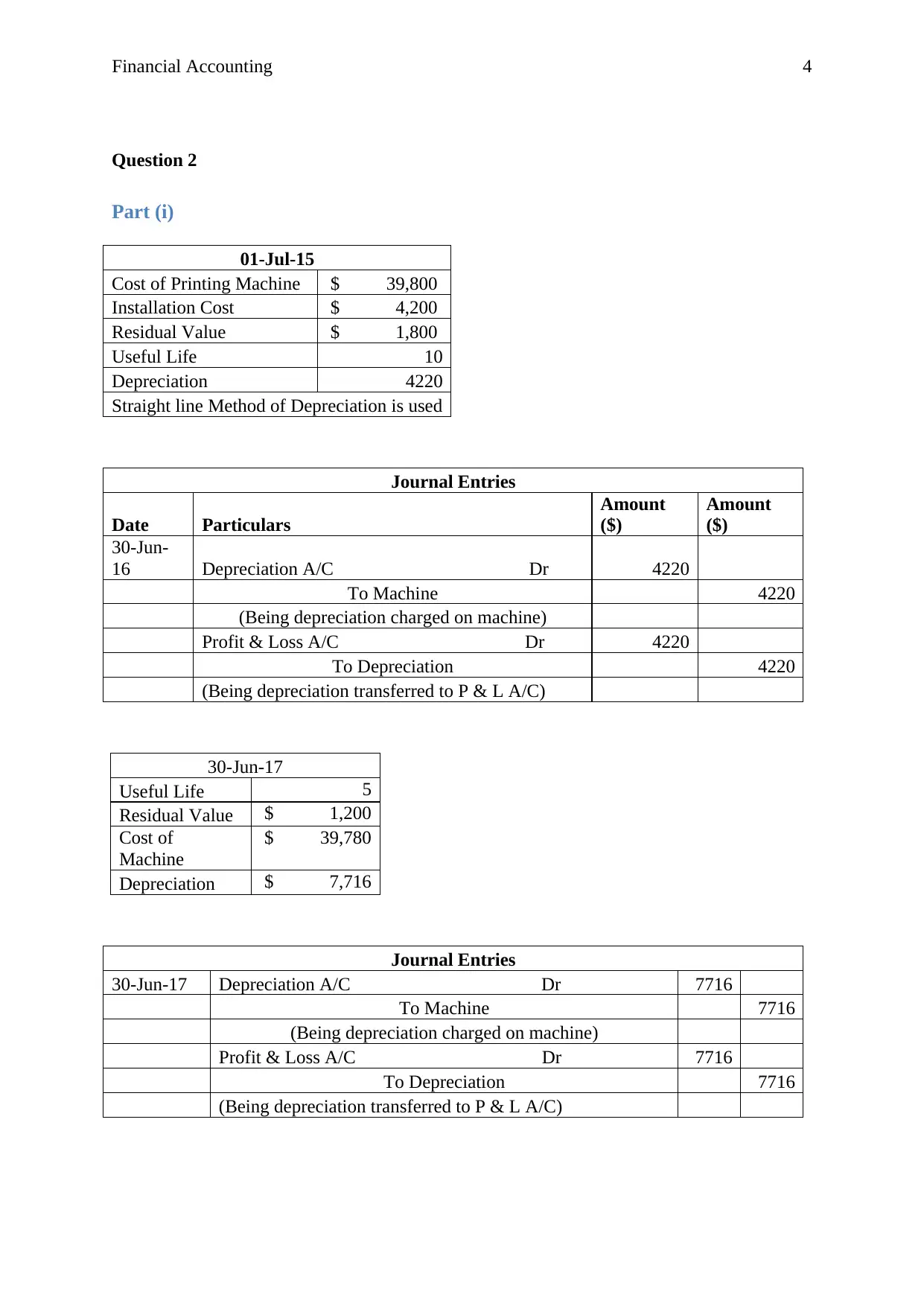

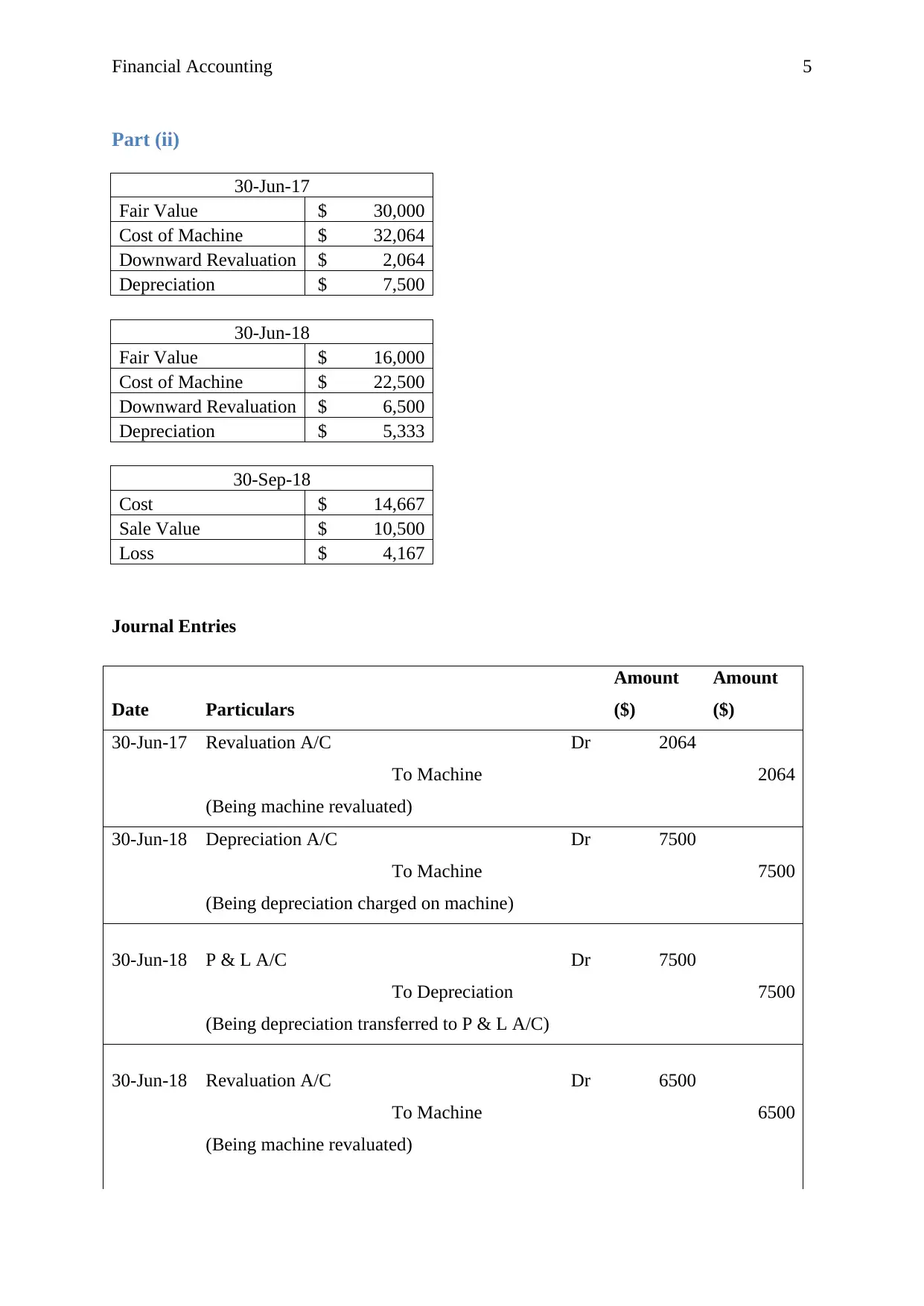

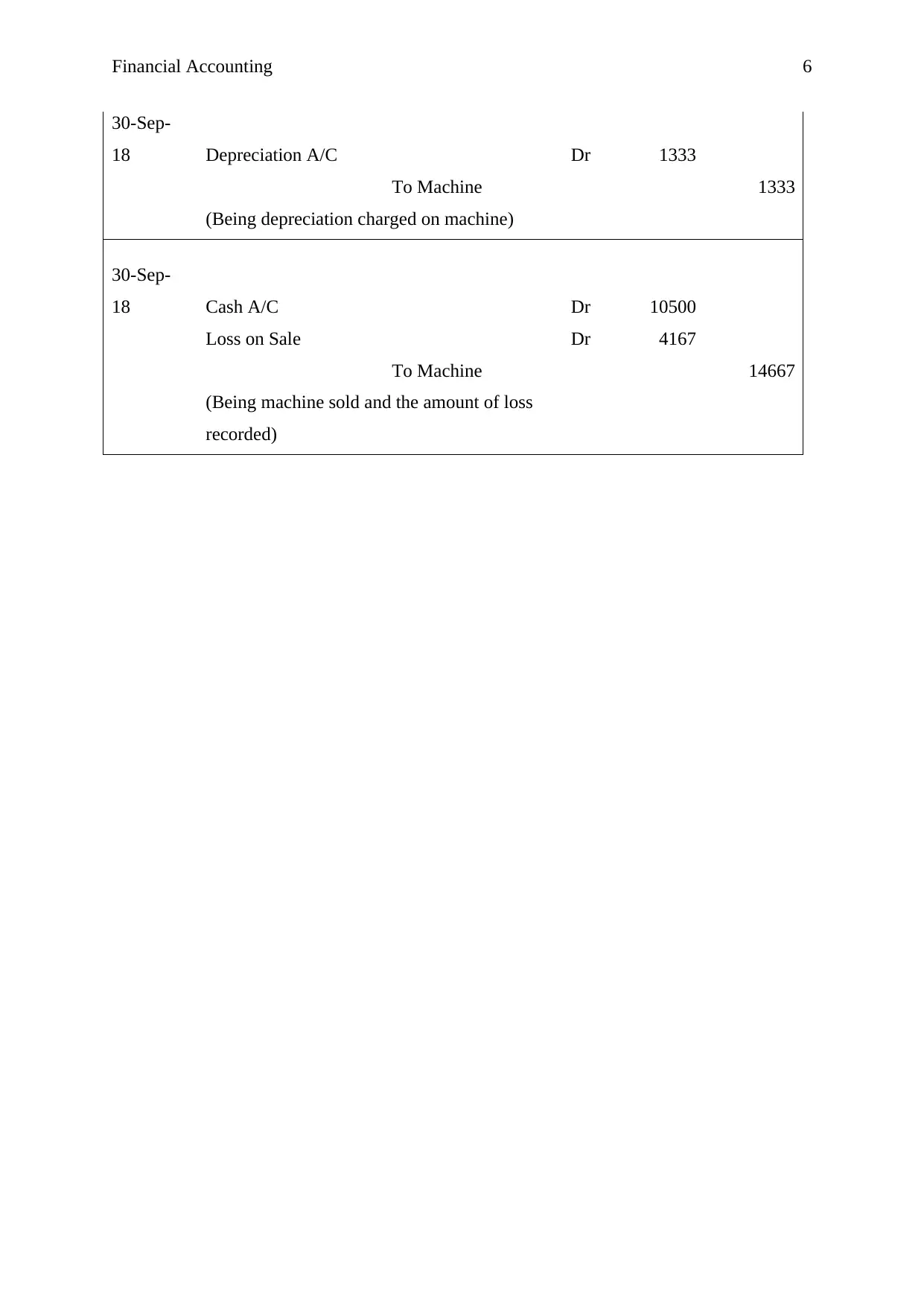

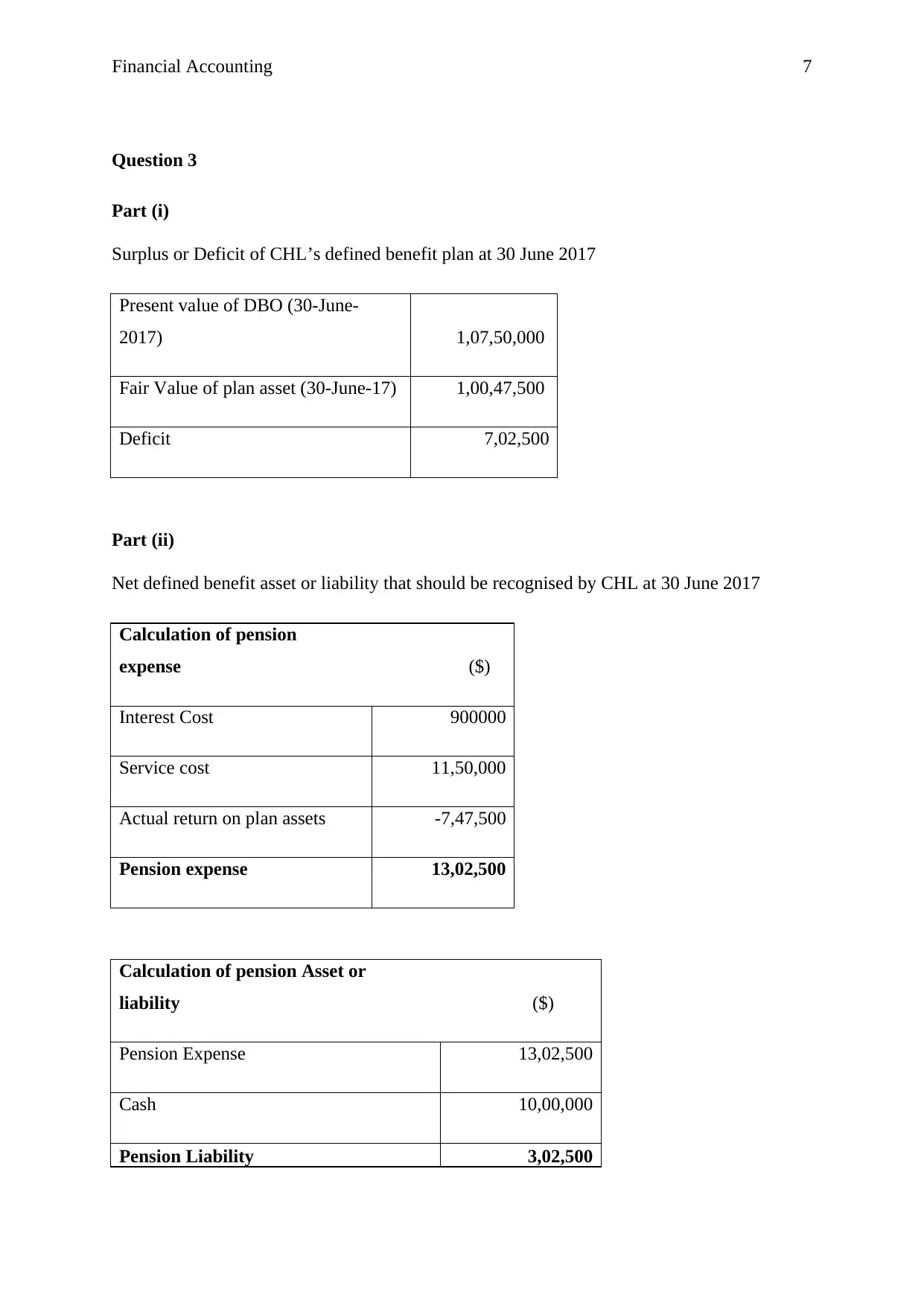

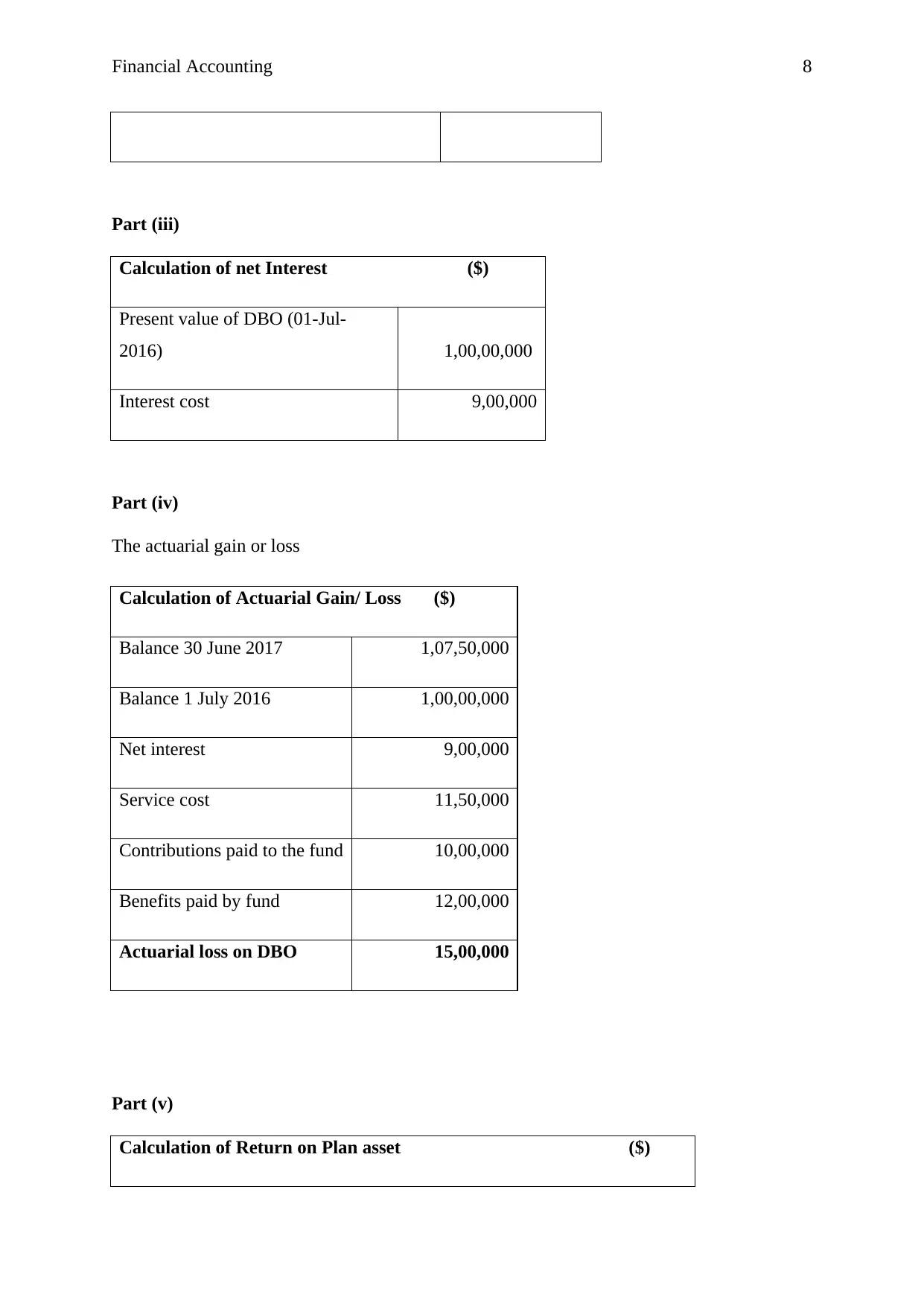

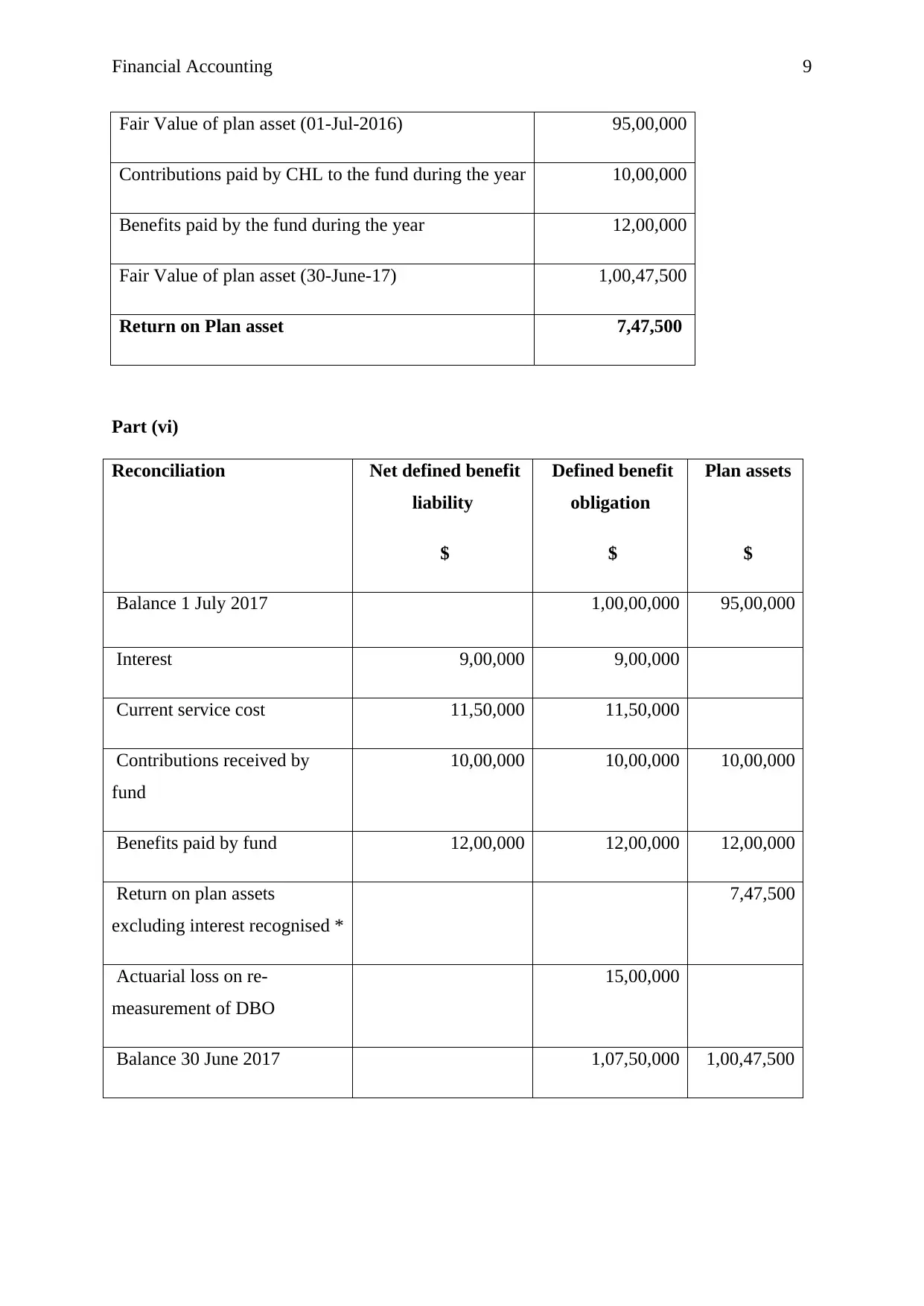

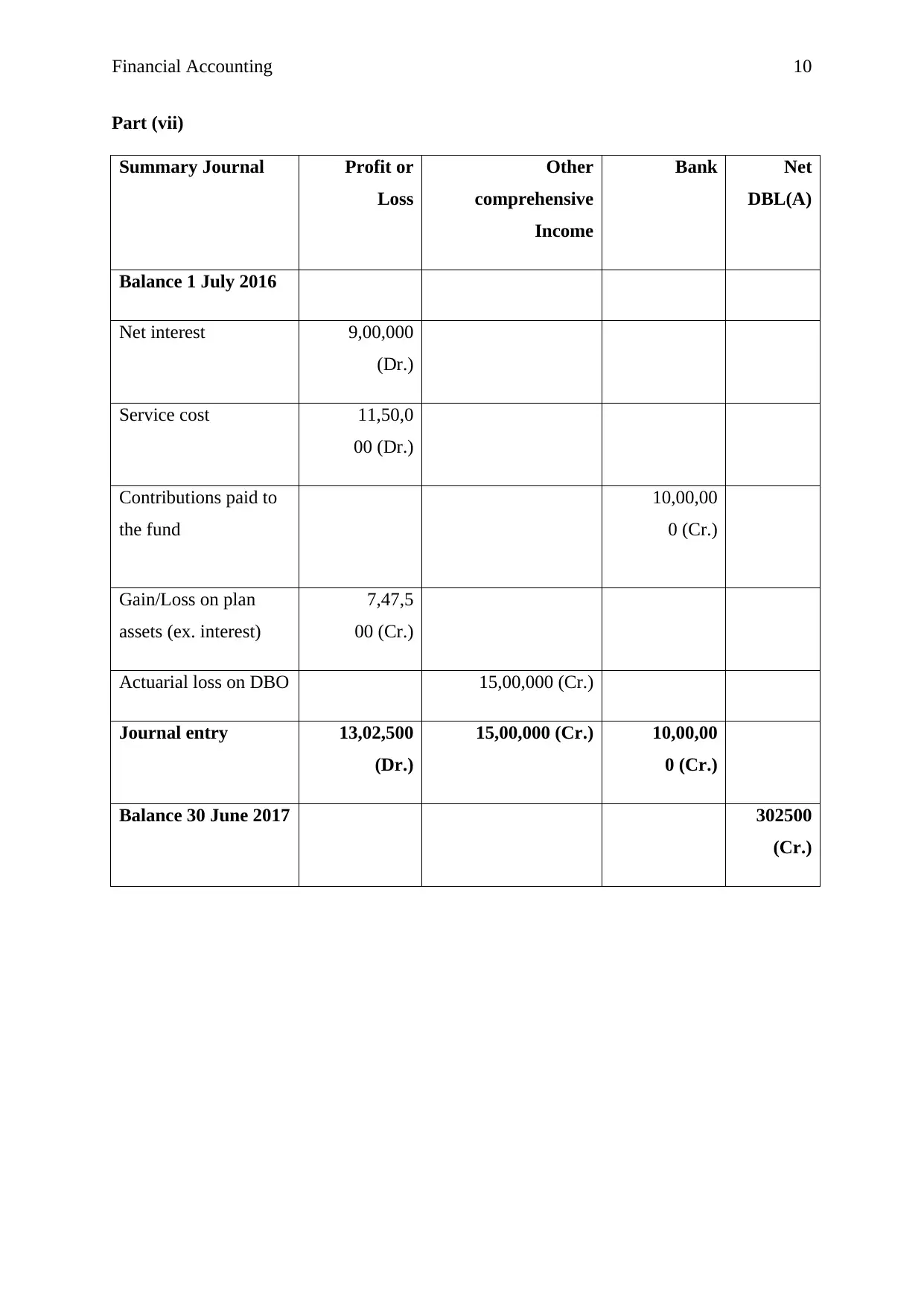

This document is a comprehensive solution to a financial accounting assignment, addressing key concepts and practical applications. The assignment covers three main questions: the fair value method of accounting, depreciation calculations and journal entries, and the accounting for a defined benefit pension plan. The solution provides detailed explanations, calculations, and journal entries for each part, including straight-line depreciation, downward revaluation, and the reconciliation of pension assets and liabilities. It also includes calculations for pension expense, net interest, actuarial gains/losses, and the return on plan assets. The document concludes with a summary of the journal entries. This assignment provides a valuable resource for students studying financial accounting and seeking to understand complex accounting principles and their practical application.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.