Financial Accounting Assignment: Superstore Ltd Financial Analysis

VerifiedAdded on 2023/01/06

|16

|1687

|75

Homework Assignment

AI Summary

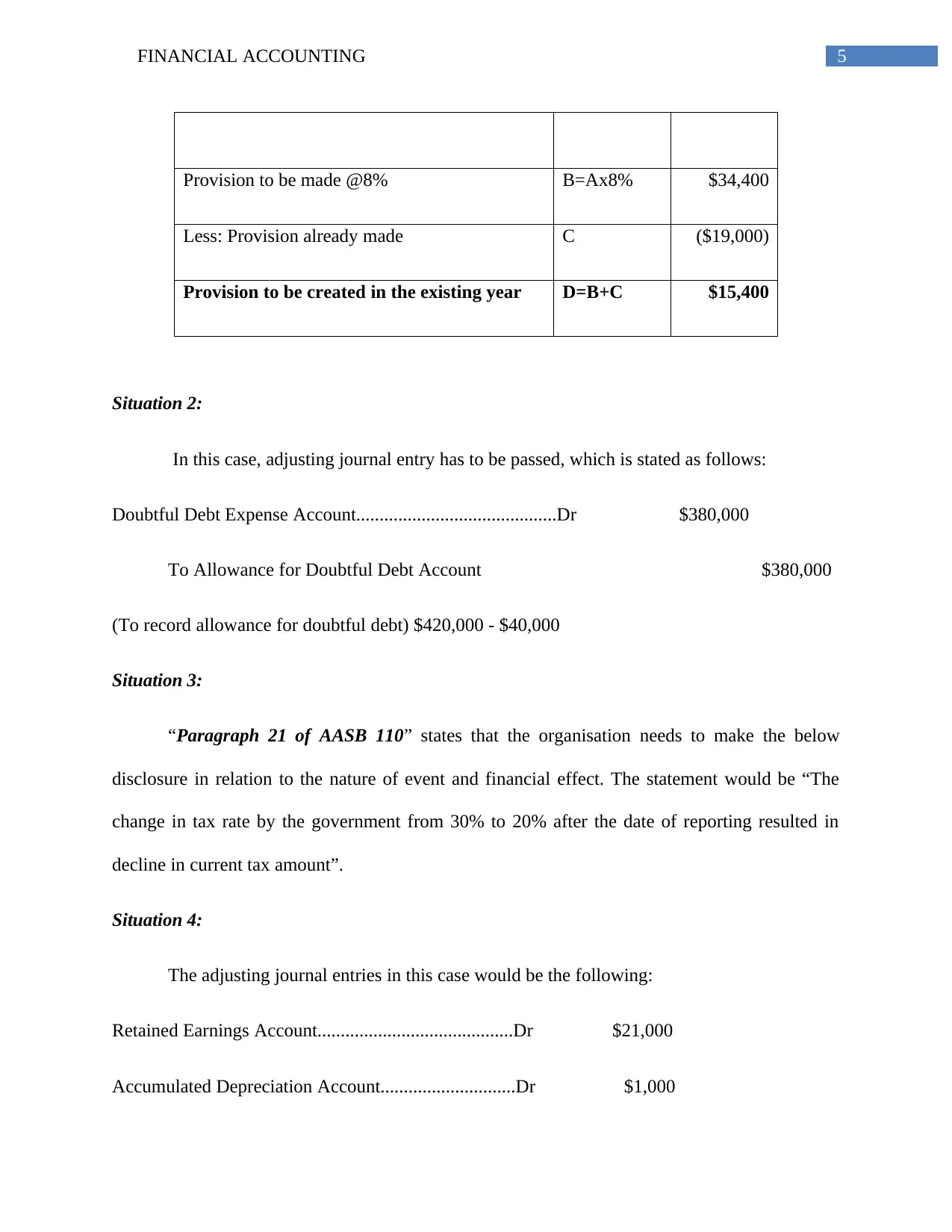

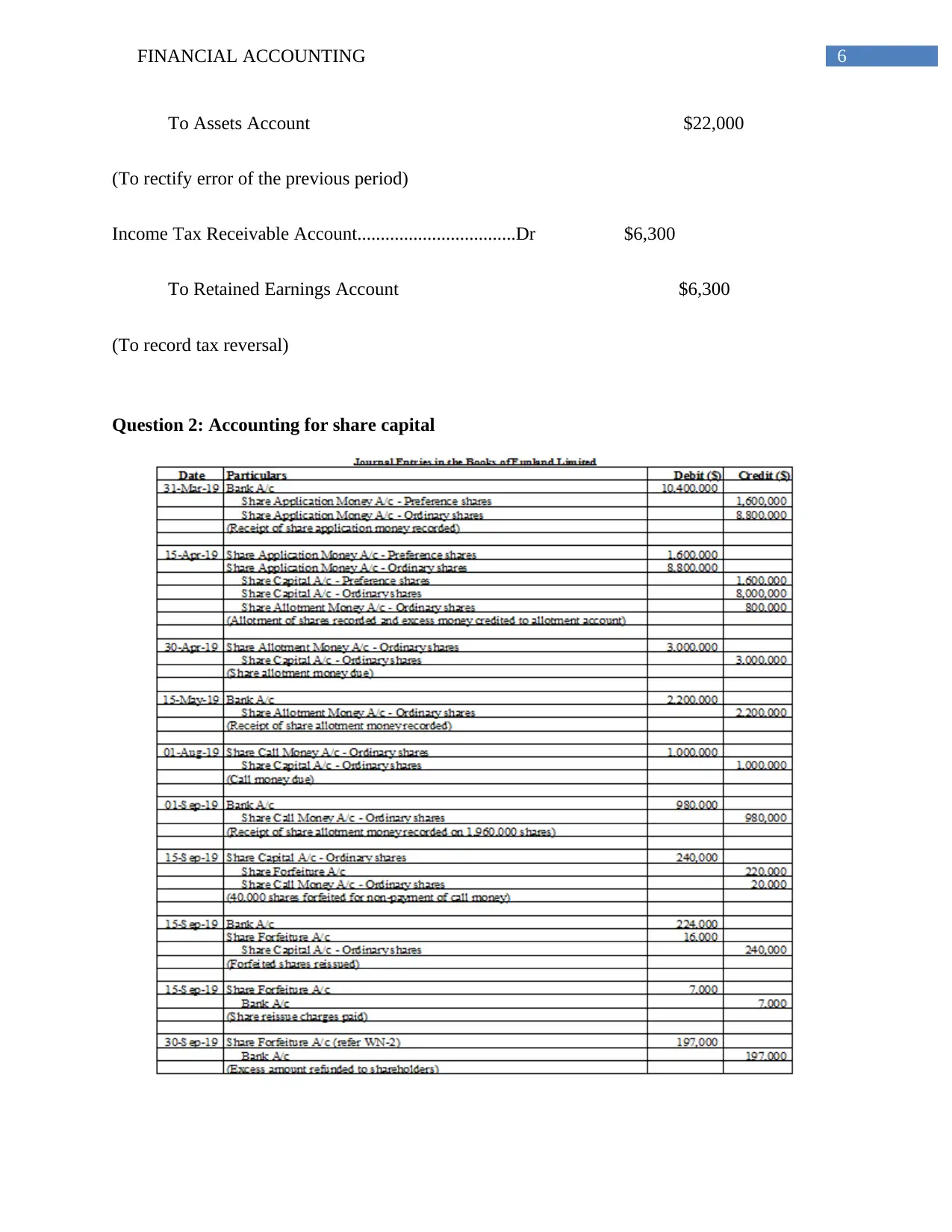

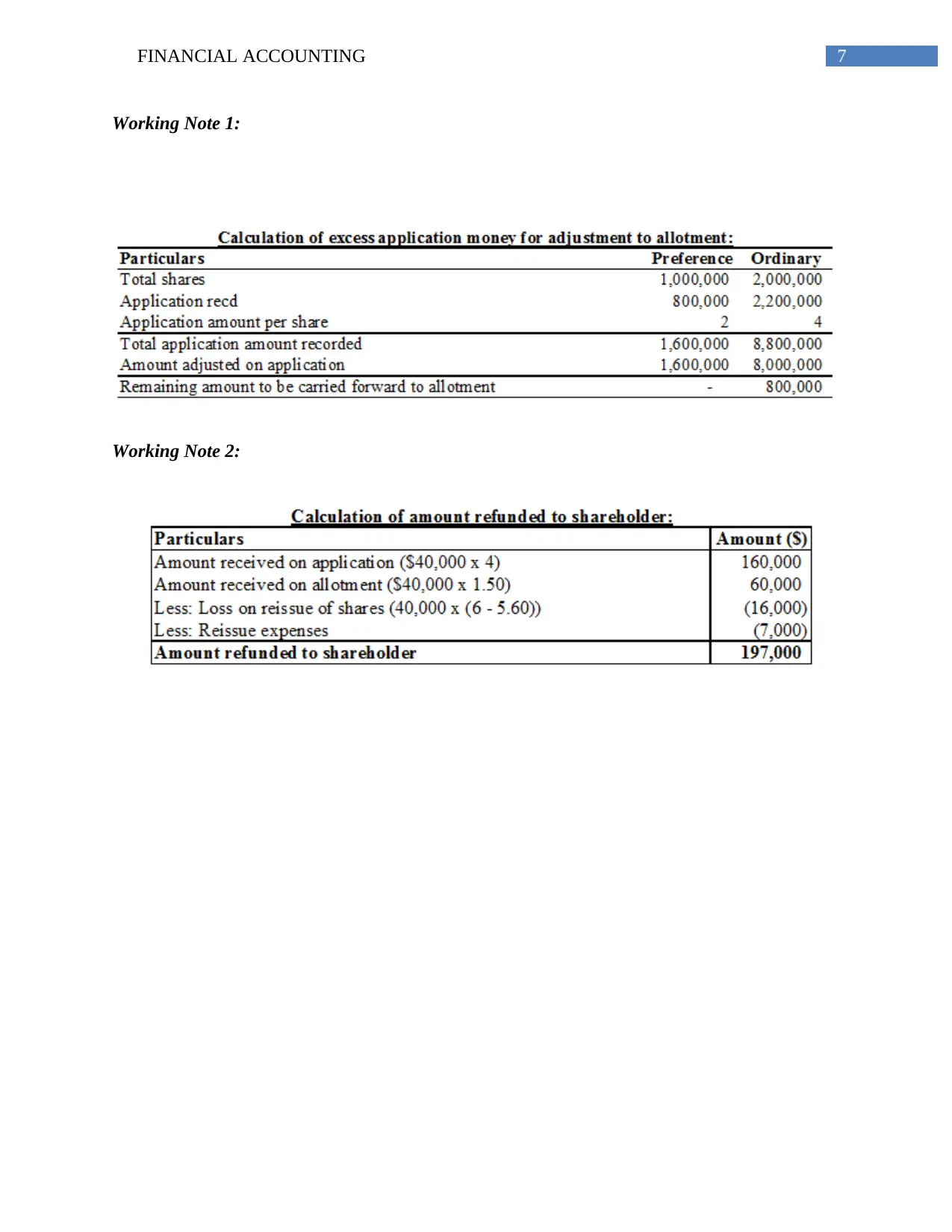

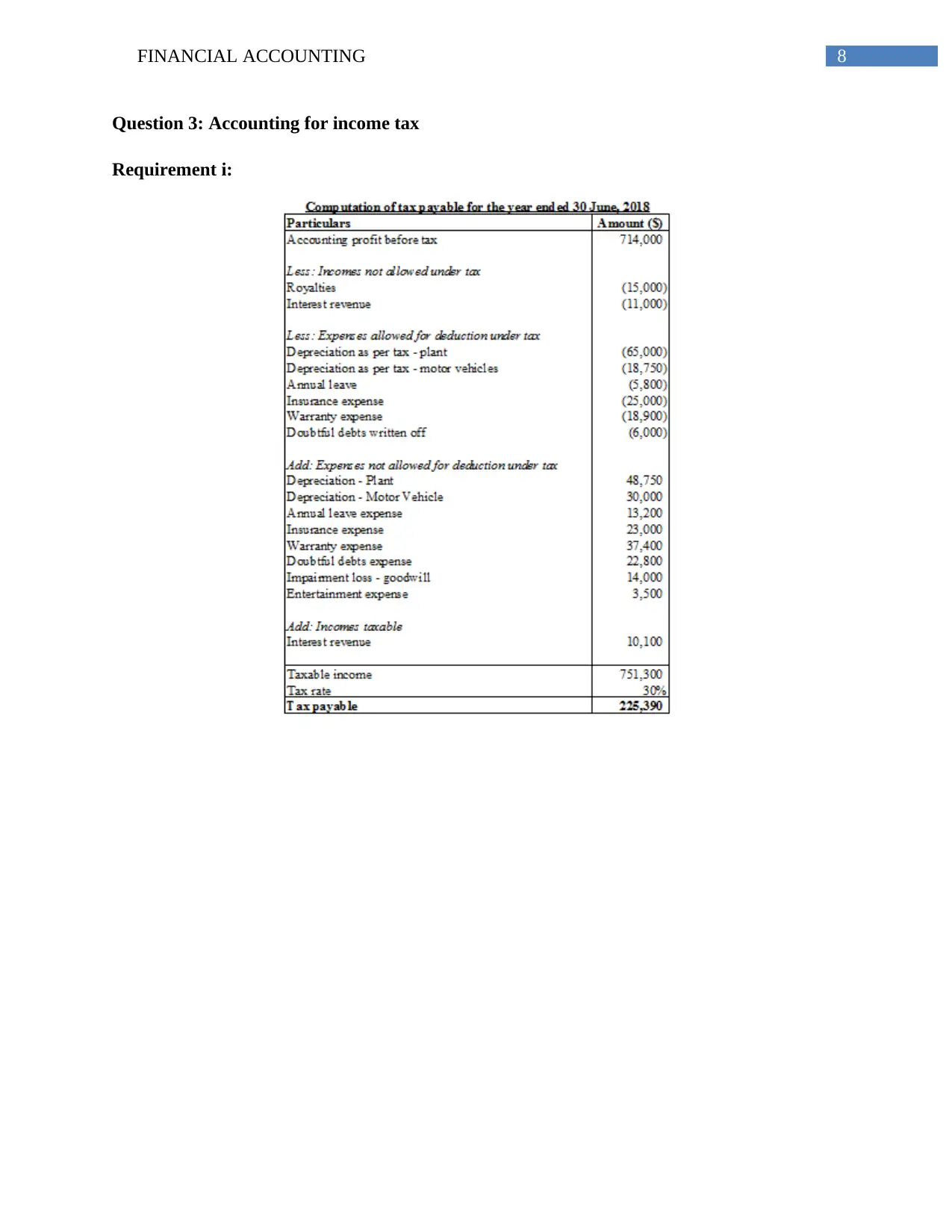

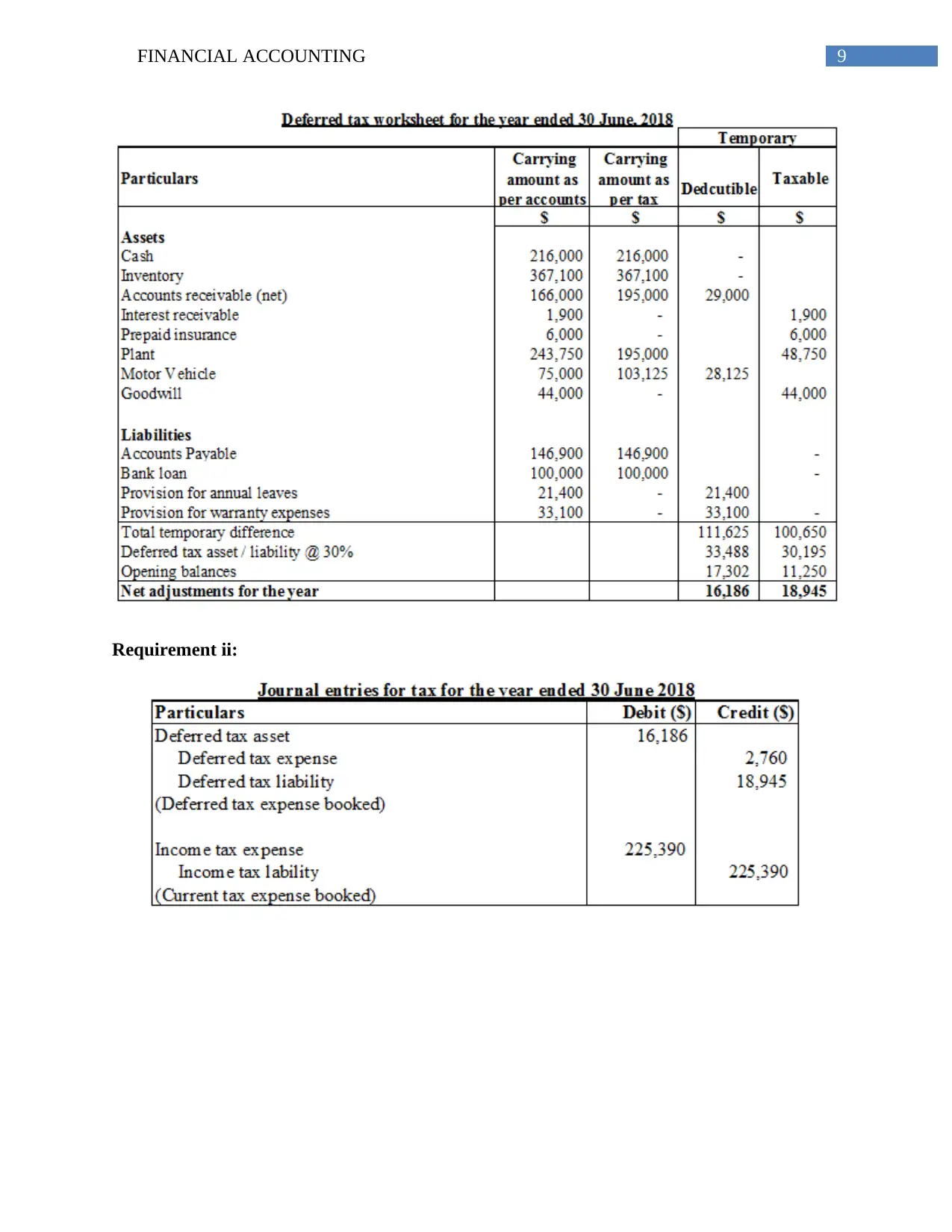

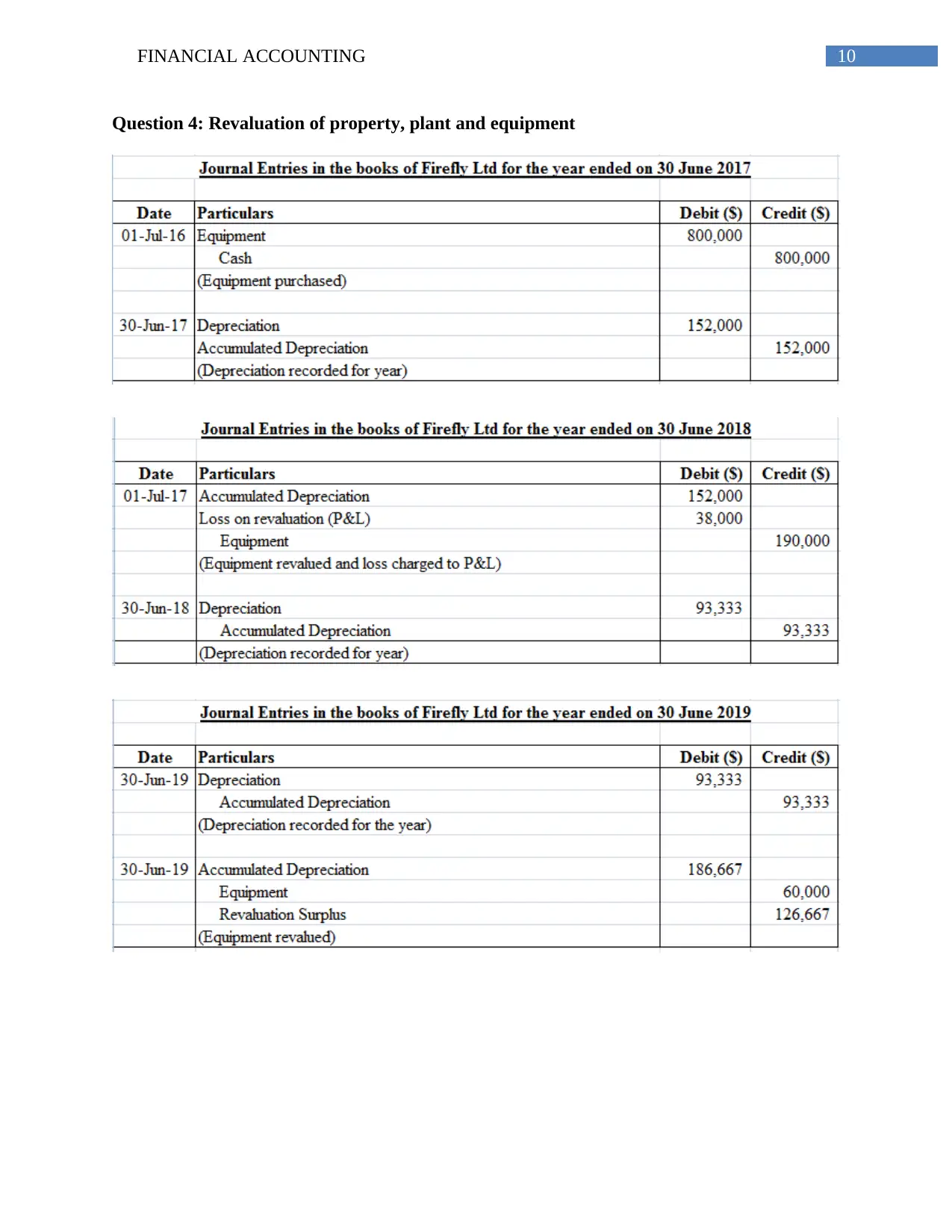

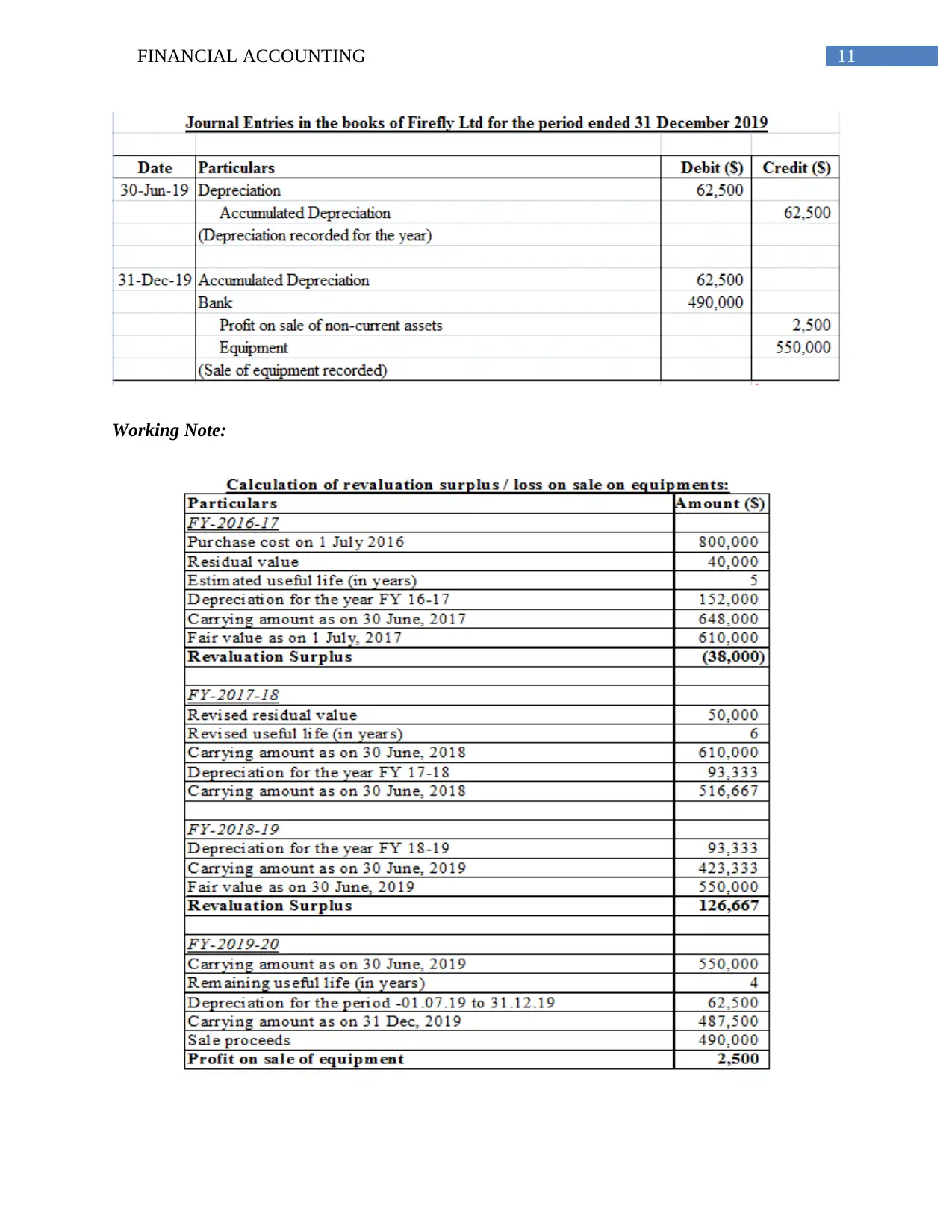

This financial accounting assignment analyzes various aspects of financial reporting and accounting practices. The assignment begins with an examination of financial statement disclosures, covering topics such as changes in accounting estimates, events after the reporting date, and error corrections. It then delves into the accounting treatment for share capital, followed by an in-depth analysis of income tax accounting, including both current and deferred tax calculations. The assignment continues with a focus on asset valuation, specifically addressing the revaluation of property, plant, and equipment, including the necessary journal entries and working notes. Finally, the assignment concludes with a detailed exploration of asset impairment, encompassing the computation of impairment losses, the allocation of these losses, and the subsequent reversal of impairment losses. The assignment utilizes real-world scenarios and case studies to illustrate key accounting concepts and principles.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.