Financial Accounting Homework: Comprehensive Case Study Analysis

VerifiedAdded on 2021/02/20

|25

|4368

|24

Homework Assignment

AI Summary

This document presents a comprehensive financial accounting homework assignment solution, covering a range of topics. It begins with an introduction to financial accounting, defining its purpose and objectives, and exploring the interests of internal and external stakeholders in financial statements. The solution then delves into practical applications, including journal entries, trial balances, income statements, balance sheets, and bank reconciliation statements. It includes explanations of accounting concepts like depreciation, control accounts, and suspense accounts. The assignment analyzes different clients, providing detailed solutions for each, from recording transactions to preparing financial statements. The document offers a complete overview of financial accounting principles and practices, making it a valuable resource for students seeking to understand and apply accounting concepts.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

a. ......................................................................................................................................................1

1.Defining financial accounting and its objectives.....................................................................1

2.Explaining the internal and the external stakeholders and their in interest in the company's

financial statements.....................................................................................................................2

b........................................................................................................................................................3

Client 1.............................................................................................................................................3

I. Recording and classification of the journal entries..................................................................3

ii. Preparation of the trial balance...............................................................................................3

Client 2.............................................................................................................................................3

a. Preparation of the income statement.......................................................................................3

b. Statement of balance sheet......................................................................................................3

c. Explaining the concepts of accounting....................................................................................3

d. Describing the purpose of charging depreciation and various methods used by the

organization for evaluating depreciation.....................................................................................4

e. Evaluating the difference in between the financial statements of sole trader and the limited

company......................................................................................................................................4

Client 3.............................................................................................................................................5

a. Explaining the objective of formulating the bank reconciliation statement............................5

b...................................................................................................................................................5

c. Explaining the concept of imprest in the system of petty cash...............................................5

d. Preparation of bank reconciliation statement..........................................................................5

Client 4.............................................................................................................................................5

a. Preparing sales and the purchase ledger account....................................................................5

b. Explaining the meaning of control account ...........................................................................5

Client 5.............................................................................................................................................5

a. Explaining the meaning and the features of suspense account ..............................................5

b. Drafting a trial balance ...........................................................................................................5

INTRODUCTION...........................................................................................................................1

a. ......................................................................................................................................................1

1.Defining financial accounting and its objectives.....................................................................1

2.Explaining the internal and the external stakeholders and their in interest in the company's

financial statements.....................................................................................................................2

b........................................................................................................................................................3

Client 1.............................................................................................................................................3

I. Recording and classification of the journal entries..................................................................3

ii. Preparation of the trial balance...............................................................................................3

Client 2.............................................................................................................................................3

a. Preparation of the income statement.......................................................................................3

b. Statement of balance sheet......................................................................................................3

c. Explaining the concepts of accounting....................................................................................3

d. Describing the purpose of charging depreciation and various methods used by the

organization for evaluating depreciation.....................................................................................4

e. Evaluating the difference in between the financial statements of sole trader and the limited

company......................................................................................................................................4

Client 3.............................................................................................................................................5

a. Explaining the objective of formulating the bank reconciliation statement............................5

b...................................................................................................................................................5

c. Explaining the concept of imprest in the system of petty cash...............................................5

d. Preparation of bank reconciliation statement..........................................................................5

Client 4.............................................................................................................................................5

a. Preparing sales and the purchase ledger account....................................................................5

b. Explaining the meaning of control account ...........................................................................5

Client 5.............................................................................................................................................5

a. Explaining the meaning and the features of suspense account ..............................................5

b. Drafting a trial balance ...........................................................................................................5

c. Rectification of errors .............................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting refers to the process that involve the collection and the processing

of the financial information in order to meet the need of internal and the external parties relating

to their decision making. The present study is based on several aspects of the financial

accounting that include its purpose and interest of the users in the accounting information of the

organization. Journal, ledger and trial balance is been under the study for recording and reporting

the results of the financial transactions. Various accounting concepts and the methods of

depreciation are also been described under the report. Furthermore, income statement and

balance sheet are also formulated. Moreover, Bank reconciliation statement with the description

of its purpose is been mentioned and concept and features of control and the suspense account is

also included.

a.

1.Defining financial accounting and its objectives

Financial accounting is the practice that records, analyse, summarize and report the

business transactions resultant from the operations of the business over the time period. It utilizes

a set of the accounting conventions and the principles at the time of financial accounting. These

accounting principles are formulated and established for the purpose of facilitating consistent

information to the investors, regulators, tax authorities and the creditors. Financial accounting is

been performed using the accrual and the cash method (Mullinova, 2016). It results in the

reporting of the income by preparing the income statement and financial position by formulating

the balance sheet. There are various purposes of the financial accounting as follows-

The main purpose or objective of financial accounting is to facilitate the information which is

required for making the suitable decisions and to frame the financial reports which results in

providing the information relating to the performance of the company to the internal as well as

the external users. Other objectives include-

Relevancy- The foremost purpose of financial accounting is to provide the relevant

information to the users which helps them in making the decisions regarding their financial well

being. It helps in making the investment decisions for the investors.

Reliability- Accounting information that is recorded been entered in the financial

statements must be reliable which means free from bias and does not contain any misleading

statement. Reliability can be attained by the organization through the verification of the

1

Financial accounting refers to the process that involve the collection and the processing

of the financial information in order to meet the need of internal and the external parties relating

to their decision making. The present study is based on several aspects of the financial

accounting that include its purpose and interest of the users in the accounting information of the

organization. Journal, ledger and trial balance is been under the study for recording and reporting

the results of the financial transactions. Various accounting concepts and the methods of

depreciation are also been described under the report. Furthermore, income statement and

balance sheet are also formulated. Moreover, Bank reconciliation statement with the description

of its purpose is been mentioned and concept and features of control and the suspense account is

also included.

a.

1.Defining financial accounting and its objectives

Financial accounting is the practice that records, analyse, summarize and report the

business transactions resultant from the operations of the business over the time period. It utilizes

a set of the accounting conventions and the principles at the time of financial accounting. These

accounting principles are formulated and established for the purpose of facilitating consistent

information to the investors, regulators, tax authorities and the creditors. Financial accounting is

been performed using the accrual and the cash method (Mullinova, 2016). It results in the

reporting of the income by preparing the income statement and financial position by formulating

the balance sheet. There are various purposes of the financial accounting as follows-

The main purpose or objective of financial accounting is to facilitate the information which is

required for making the suitable decisions and to frame the financial reports which results in

providing the information relating to the performance of the company to the internal as well as

the external users. Other objectives include-

Relevancy- The foremost purpose of financial accounting is to provide the relevant

information to the users which helps them in making the decisions regarding their financial well

being. It helps in making the investment decisions for the investors.

Reliability- Accounting information that is recorded been entered in the financial

statements must be reliable which means free from bias and does not contain any misleading

statement. Reliability can be attained by the organization through the verification of the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting treatments and the transactions based on the audits. This in turn enable the end users

in taking the best decisions by using the financial information.

Consistency- It is also one of the most important objective of financial accounting to gain

consistency in recording and communicating the financial information (Dutta and Patatoukas,

2016). This help the users in comparing the financial results of various periods with appropriate

disclosures.

Comparability- Facilitating the information that comprises the quality of comparison is

also a main purpose of the financial accounting. An organization uses the established system in

case of recording and reporting the financial information of the business so that investors can

compare the data for making the relative judgements for availing various investment

opportunities.

Thus, these are the major purpose for which the organization opts for financial

accounting in order to provide the adequate information to the users with compliance of all

standards and the concept of accounting as provided by IFRS and GAAP.

2.Explaining the internal and the external stakeholders and their in interest in the company's

financial statements.

Business organization functions in the large environment which involves many factors

that directly or indirectly affects the financial wealth of the enterprise. Stakeholders are

considered as one of the major factor that influences the activities of the organization.

Stakeholders are categorised into two segments that is internal and the external stakeholders.

Internal stakeholders means the individual or the parties that are present within the

enterprise. For example- Employees, owners, managers and investors.

Owners- For assessing the performance of their organization, they seek for the financial

statements that facilitate the useful information relating to the profitability and the position of

overall business organization across the globe (Barth, 2015). They show the keen interest in the

financial information as it helps in determining the stability level and the extent to which the

economic factors has affected their business. Financial information assist the owners in deciding

for making the further investment in the existing or the new business ventures that generates

large profits.

Managers- They require the financial information for planning, monitoring and in

making the relevant decisions for the business. Accounting information provides for allocating

2

in taking the best decisions by using the financial information.

Consistency- It is also one of the most important objective of financial accounting to gain

consistency in recording and communicating the financial information (Dutta and Patatoukas,

2016). This help the users in comparing the financial results of various periods with appropriate

disclosures.

Comparability- Facilitating the information that comprises the quality of comparison is

also a main purpose of the financial accounting. An organization uses the established system in

case of recording and reporting the financial information of the business so that investors can

compare the data for making the relative judgements for availing various investment

opportunities.

Thus, these are the major purpose for which the organization opts for financial

accounting in order to provide the adequate information to the users with compliance of all

standards and the concept of accounting as provided by IFRS and GAAP.

2.Explaining the internal and the external stakeholders and their in interest in the company's

financial statements.

Business organization functions in the large environment which involves many factors

that directly or indirectly affects the financial wealth of the enterprise. Stakeholders are

considered as one of the major factor that influences the activities of the organization.

Stakeholders are categorised into two segments that is internal and the external stakeholders.

Internal stakeholders means the individual or the parties that are present within the

enterprise. For example- Employees, owners, managers and investors.

Owners- For assessing the performance of their organization, they seek for the financial

statements that facilitate the useful information relating to the profitability and the position of

overall business organization across the globe (Barth, 2015). They show the keen interest in the

financial information as it helps in determining the stability level and the extent to which the

economic factors has affected their business. Financial information assist the owners in deciding

for making the further investment in the existing or the new business ventures that generates

large profits.

Managers- They require the financial information for planning, monitoring and in

making the relevant decisions for the business. Accounting information provides for allocating

2

the financial, capital and the human resources adequately through the process of budgeting.

Financial accounting helps the manager in monitoring the business performance by making the

comparison against the past results, competitor analysis through benchmarking and key

performance tool (Libby, 2017). Managers can form the business decisions like financing,

pricing and the investment appropriately by using the accounting information.

External stakeholders refers to the parties that are present outside the organization and

highly affects the activities of the business. For instance- investors, customers, lenders, tax

authorities, suppliers, Auditors and the government.

Investors- They need accounting information in order to analyse or assess the

performance of the organization in which the investment has been made by them. Primarily they

use the financial statements that are published by the organization for evaluating the profitability,

risk and the valuation in respect of their investment. Investors uses the financial information for

identifying that the investment made be them is good or in deciding whether to hold, decrease or

increase the portion of their investment from the organization.

Lenders- They utilise the accounting information in order to know the credit-worthiness

of the organization that means whether the enterprise capable of paying back the loan. They offer

the loans or the other credit facilities on the basis of financial health of the organization.

Government- They require accounting information for ensuring that the organization has

presented all the disclosures in accordance with the rules and the regulations as provided in the

accounting standards (De Waegenaere, Sansing and Wielhouwer, 2015). Government prevents

the stakeholders interest by ensuring that the statements is been providing a true and the fair

view. Government defines the thresholds like sales revenue, net profit etc. in context of

determining the size and the scope of each business.

Auditors- External auditors makes the examination of the financial statements and the

recording of the accounting information for the purpose of forming an opinion. The other

external user rely on the opinion provided by the auditors relating to the financial well-being of

the organization as the accuracy of the information increases by conducting the audit

appropriately.

3

Financial accounting helps the manager in monitoring the business performance by making the

comparison against the past results, competitor analysis through benchmarking and key

performance tool (Libby, 2017). Managers can form the business decisions like financing,

pricing and the investment appropriately by using the accounting information.

External stakeholders refers to the parties that are present outside the organization and

highly affects the activities of the business. For instance- investors, customers, lenders, tax

authorities, suppliers, Auditors and the government.

Investors- They need accounting information in order to analyse or assess the

performance of the organization in which the investment has been made by them. Primarily they

use the financial statements that are published by the organization for evaluating the profitability,

risk and the valuation in respect of their investment. Investors uses the financial information for

identifying that the investment made be them is good or in deciding whether to hold, decrease or

increase the portion of their investment from the organization.

Lenders- They utilise the accounting information in order to know the credit-worthiness

of the organization that means whether the enterprise capable of paying back the loan. They offer

the loans or the other credit facilities on the basis of financial health of the organization.

Government- They require accounting information for ensuring that the organization has

presented all the disclosures in accordance with the rules and the regulations as provided in the

accounting standards (De Waegenaere, Sansing and Wielhouwer, 2015). Government prevents

the stakeholders interest by ensuring that the statements is been providing a true and the fair

view. Government defines the thresholds like sales revenue, net profit etc. in context of

determining the size and the scope of each business.

Auditors- External auditors makes the examination of the financial statements and the

recording of the accounting information for the purpose of forming an opinion. The other

external user rely on the opinion provided by the auditors relating to the financial well-being of

the organization as the accuracy of the information increases by conducting the audit

appropriately.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B.

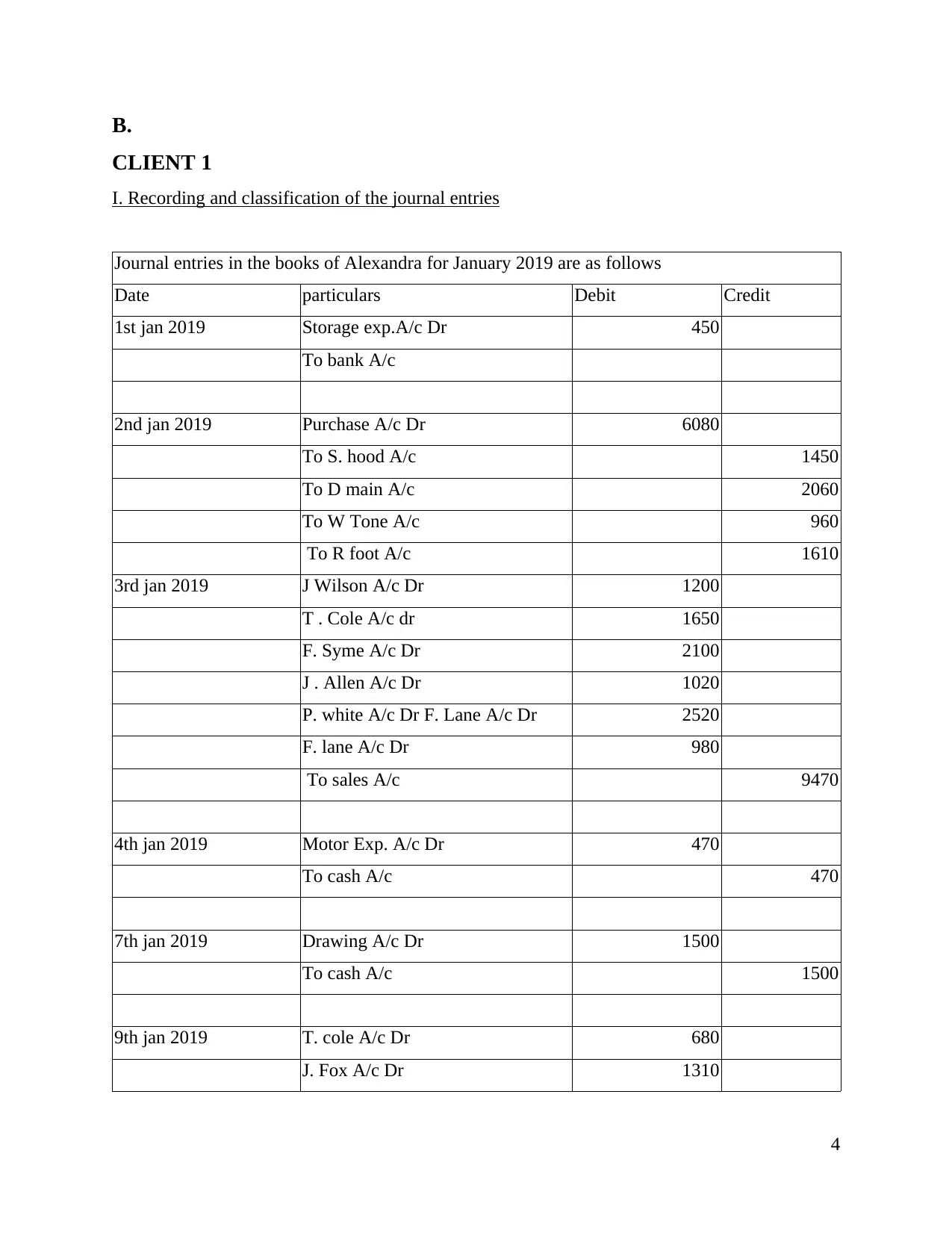

CLIENT 1

I. Recording and classification of the journal entries

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

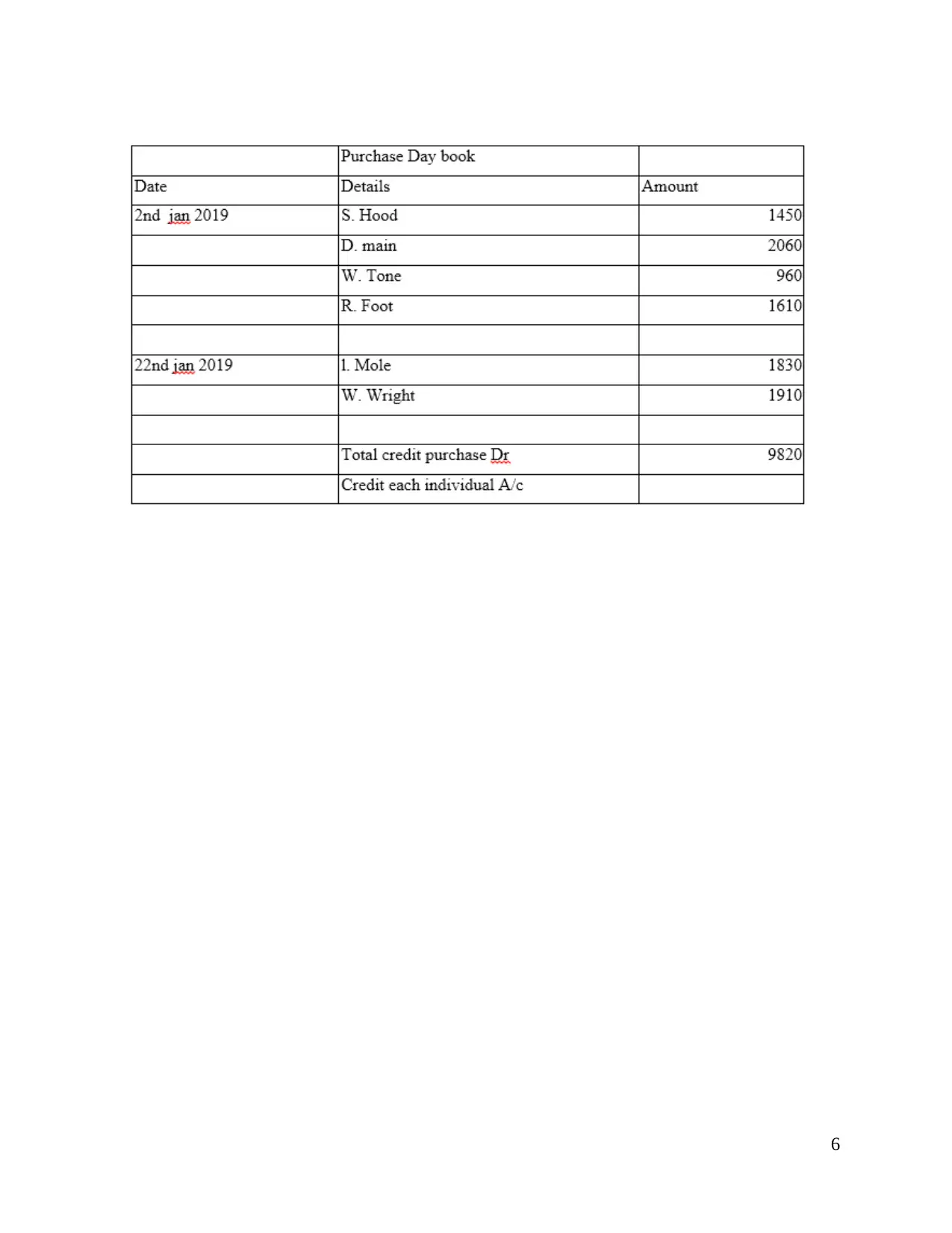

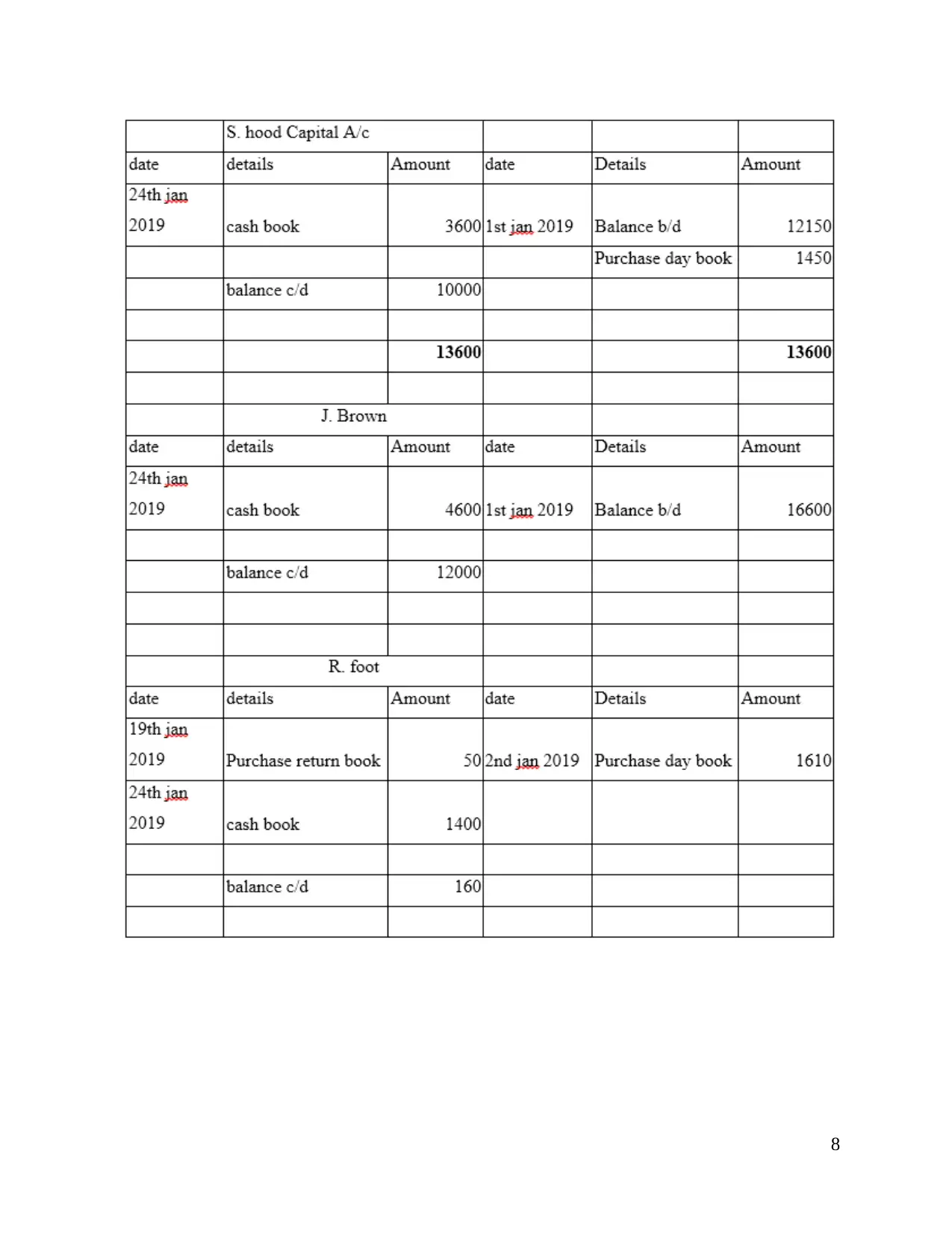

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

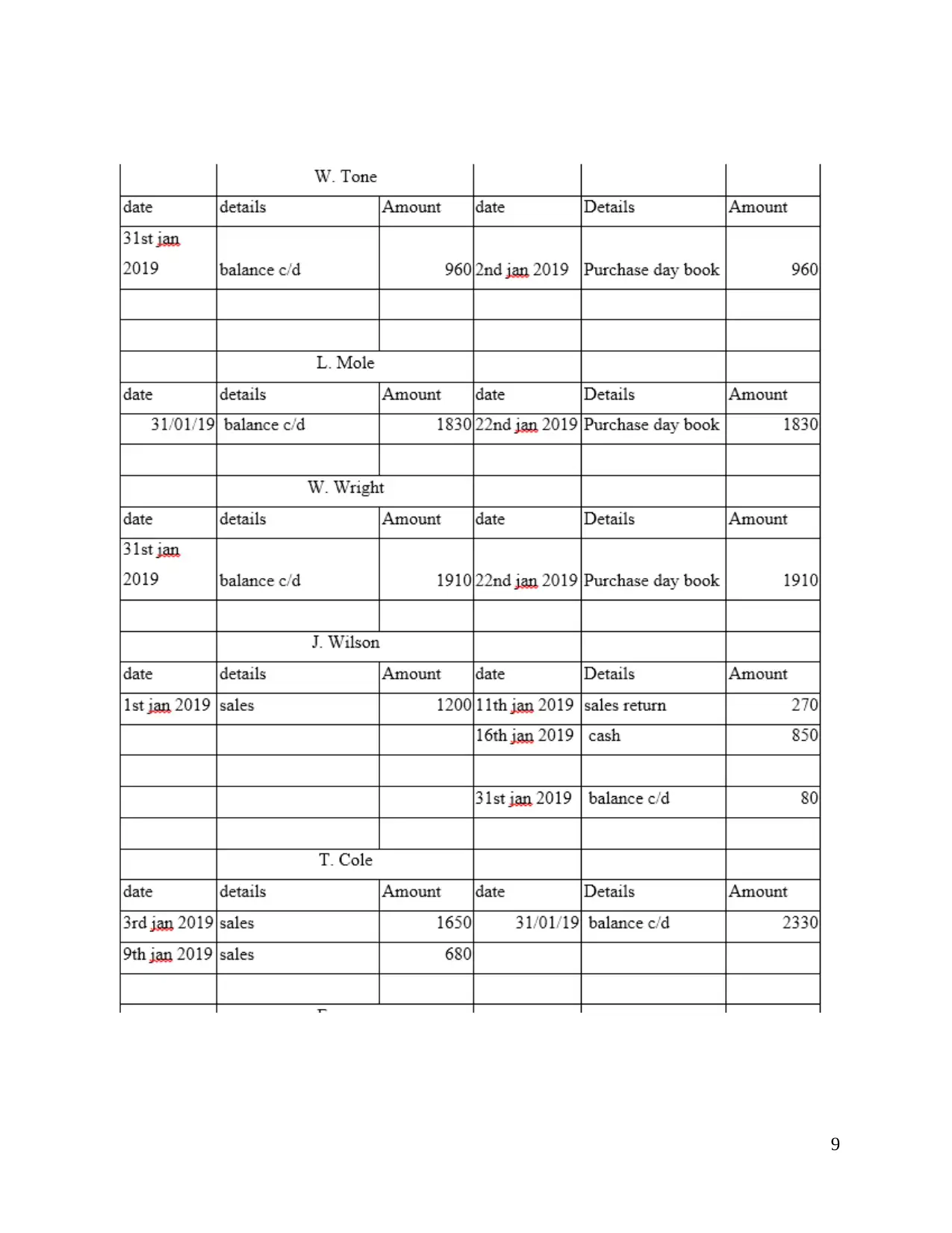

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

4

CLIENT 1

I. Recording and classification of the journal entries

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

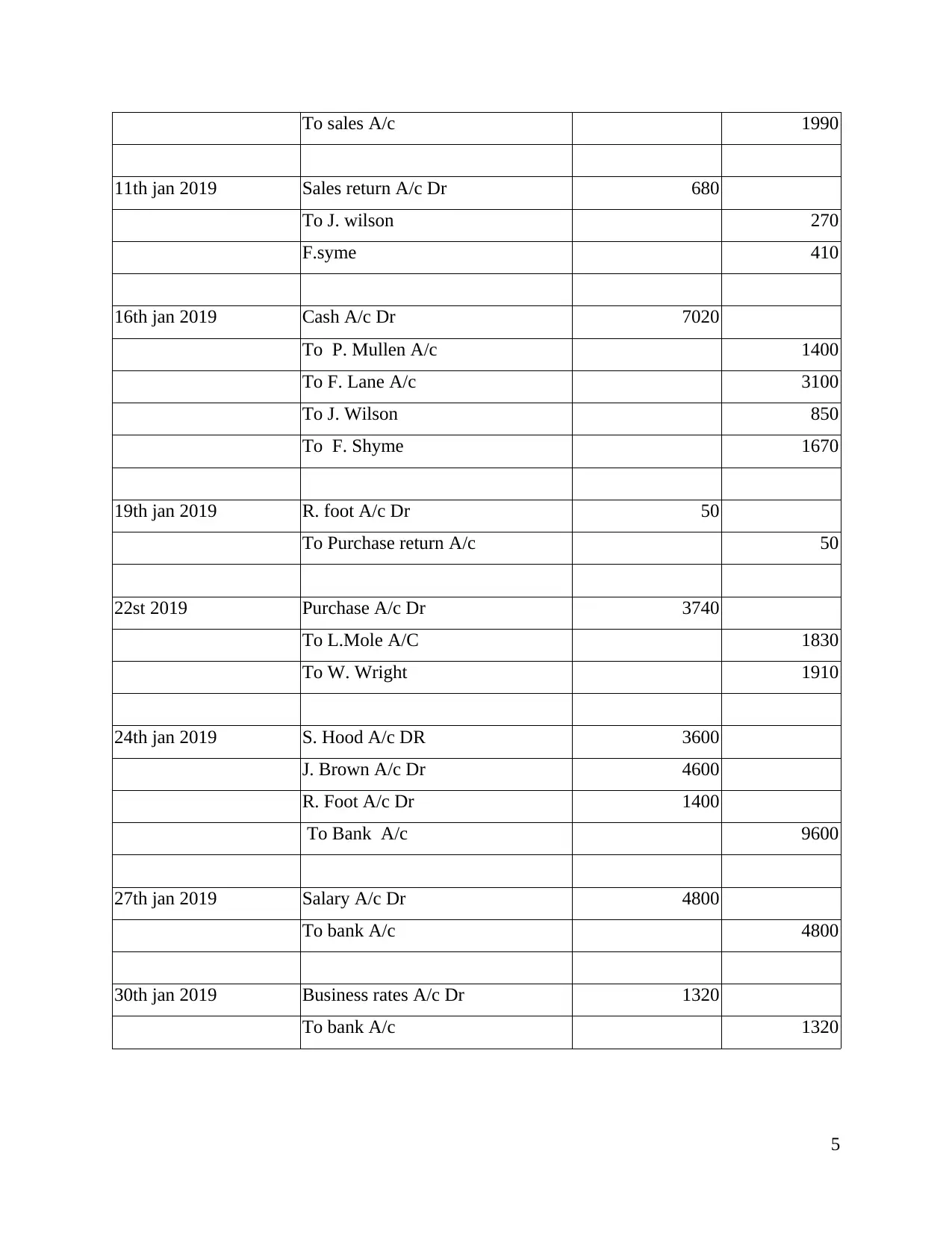

To sales A/c 1990

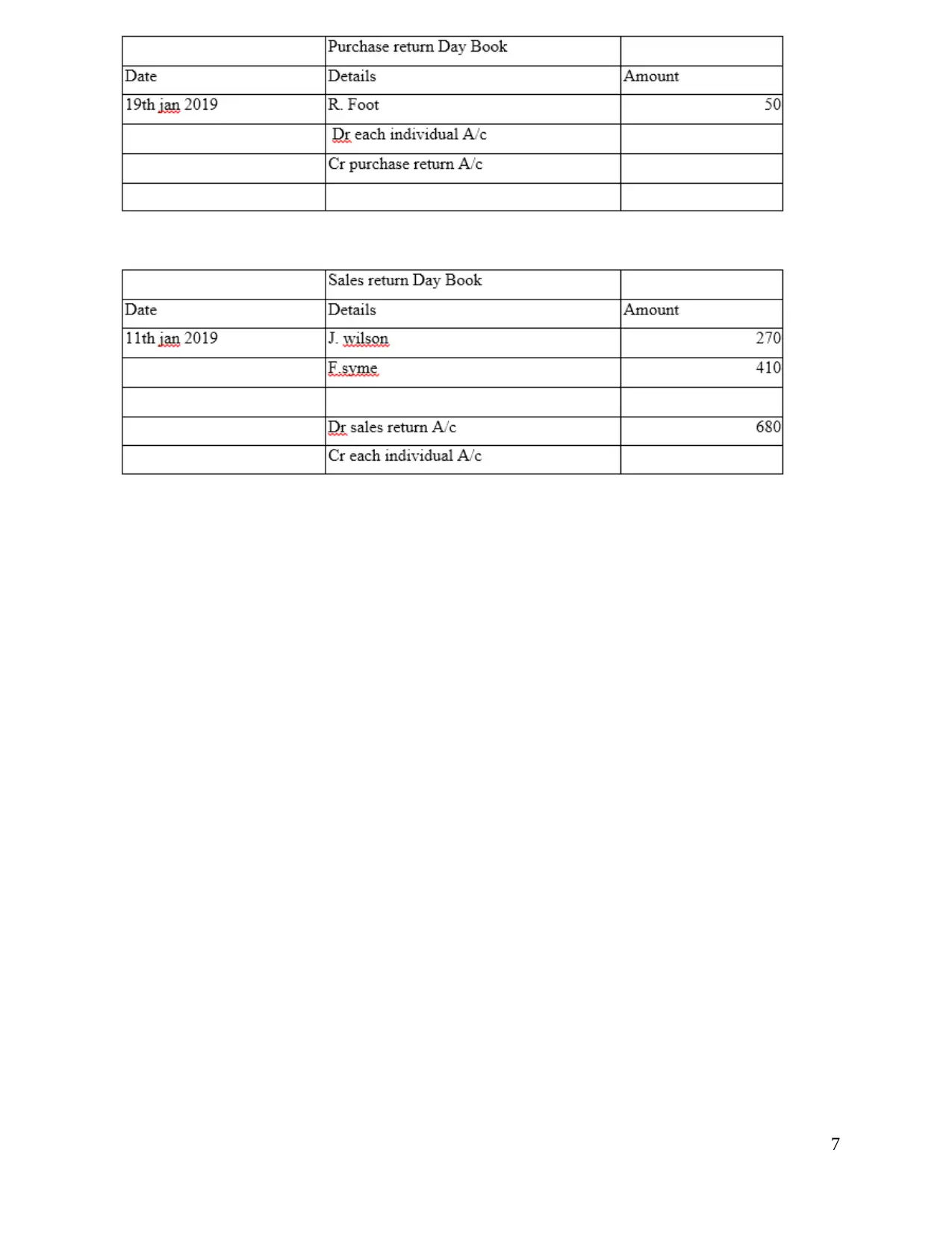

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

5

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.