Accounting Solutions: Journal Entries, Statement of Financial Position

VerifiedAdded on 2020/04/07

|9

|1550

|181

Homework Assignment

AI Summary

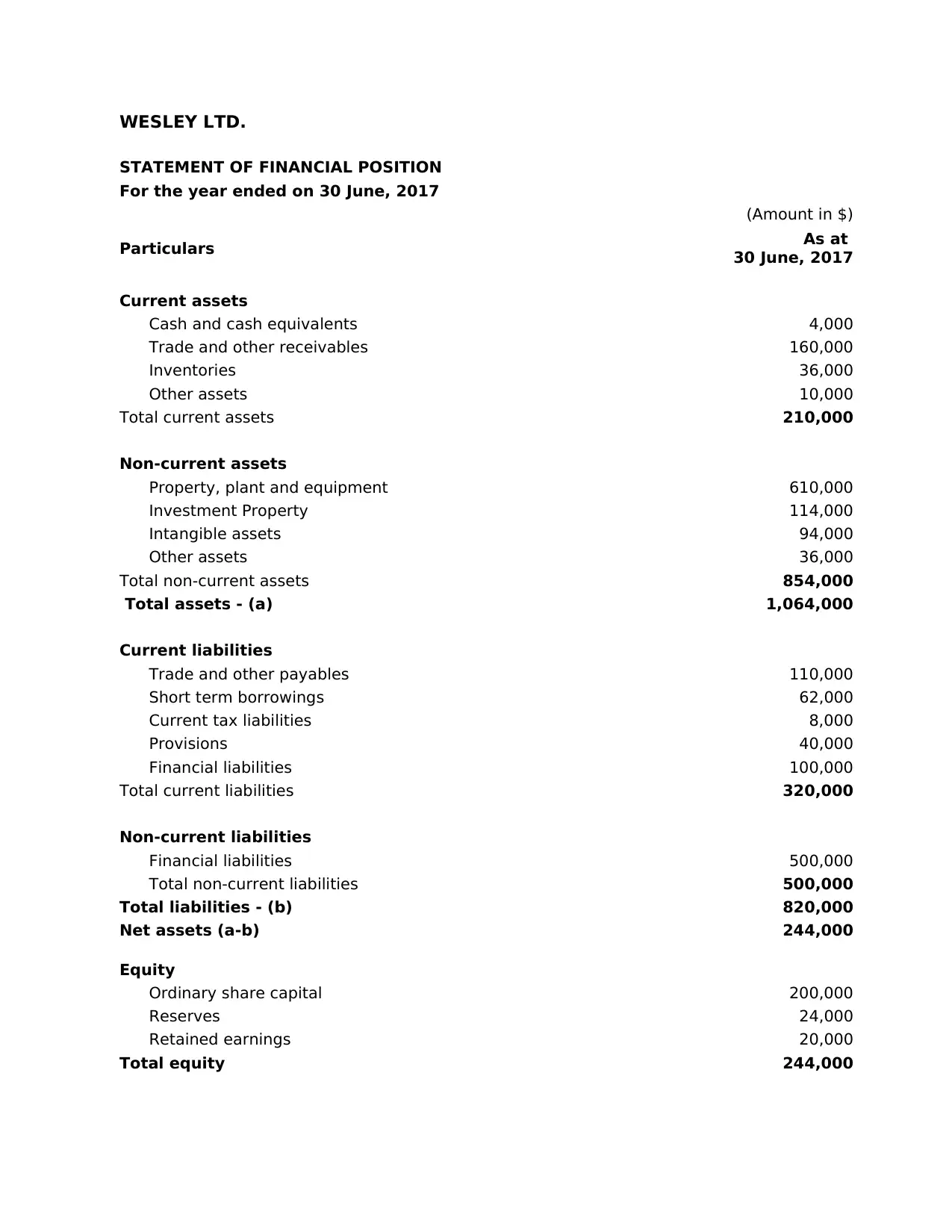

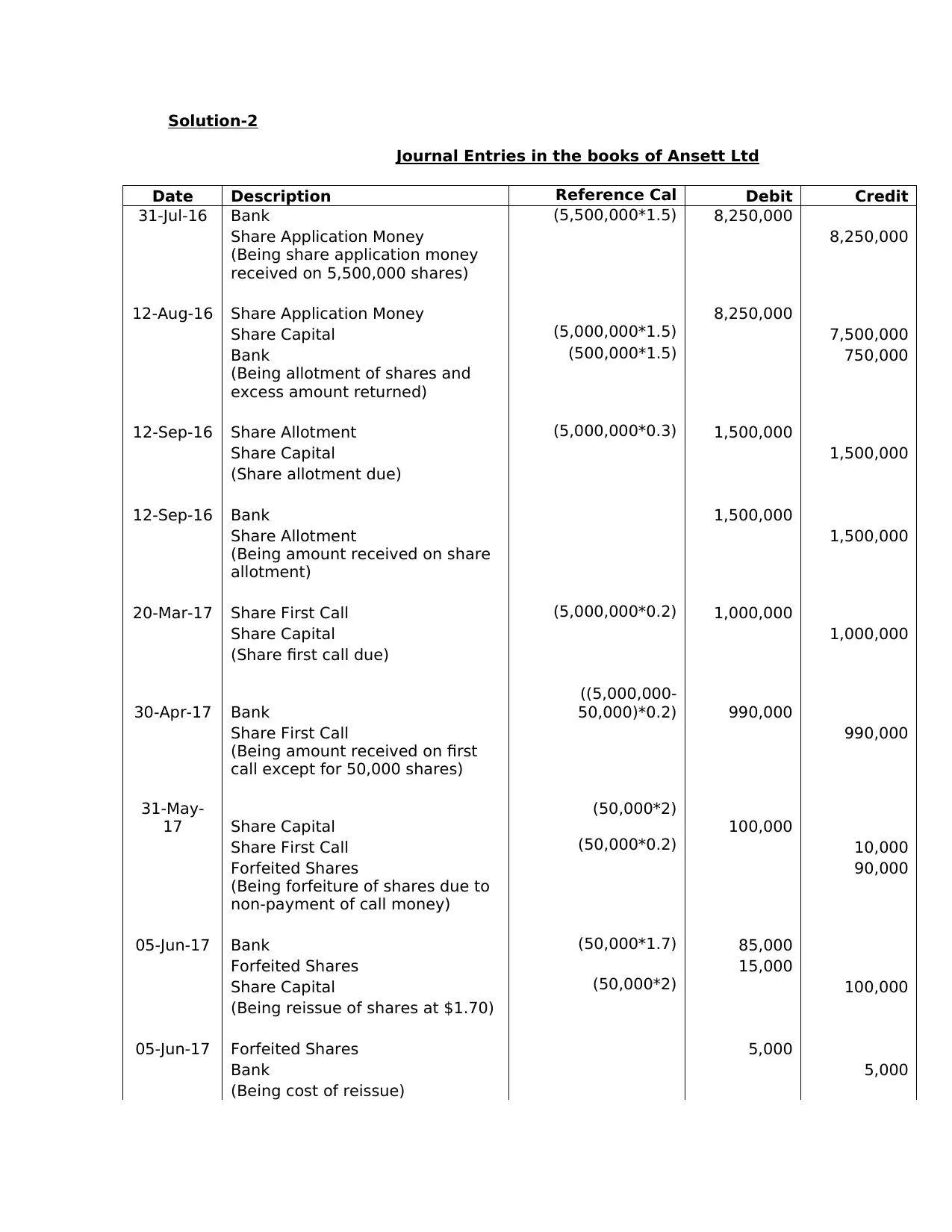

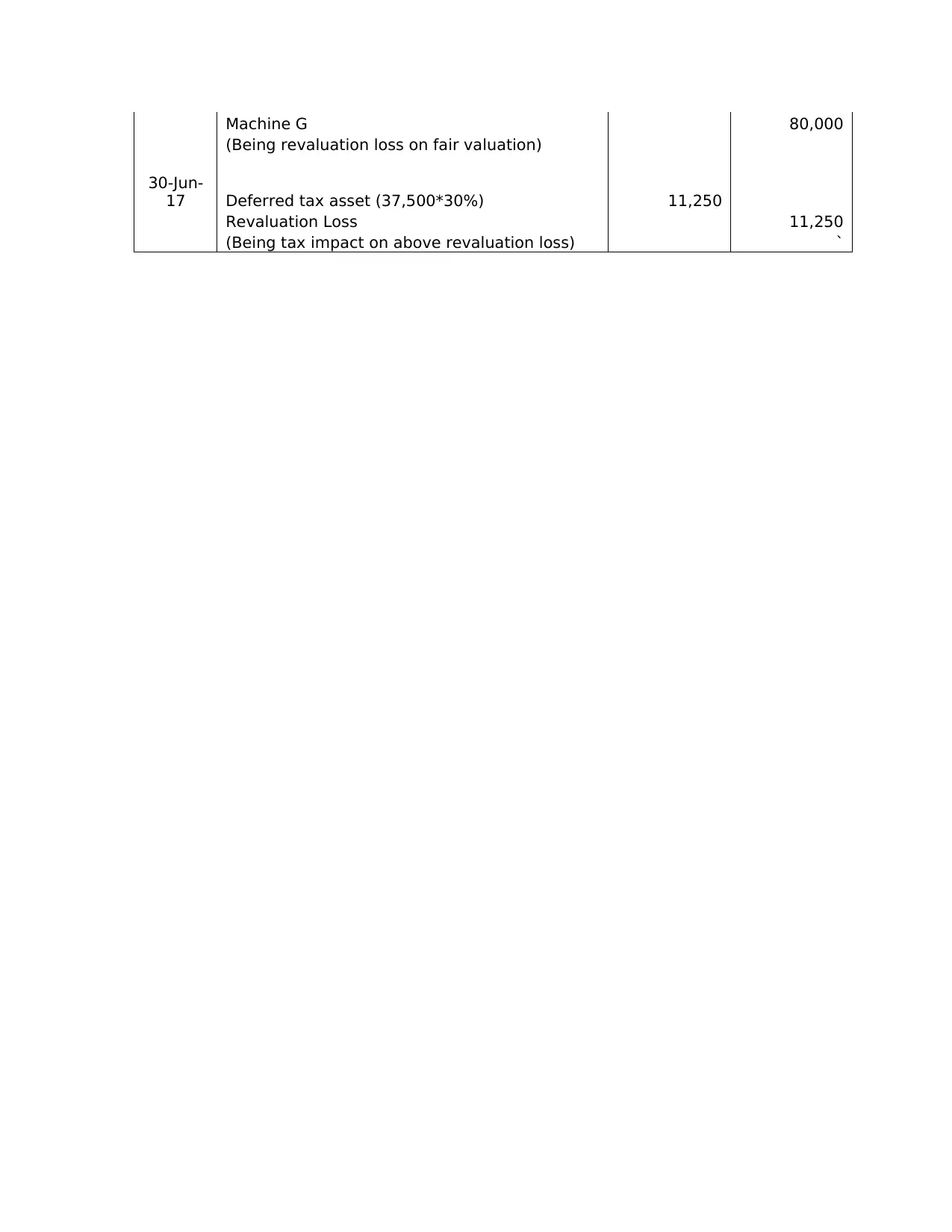

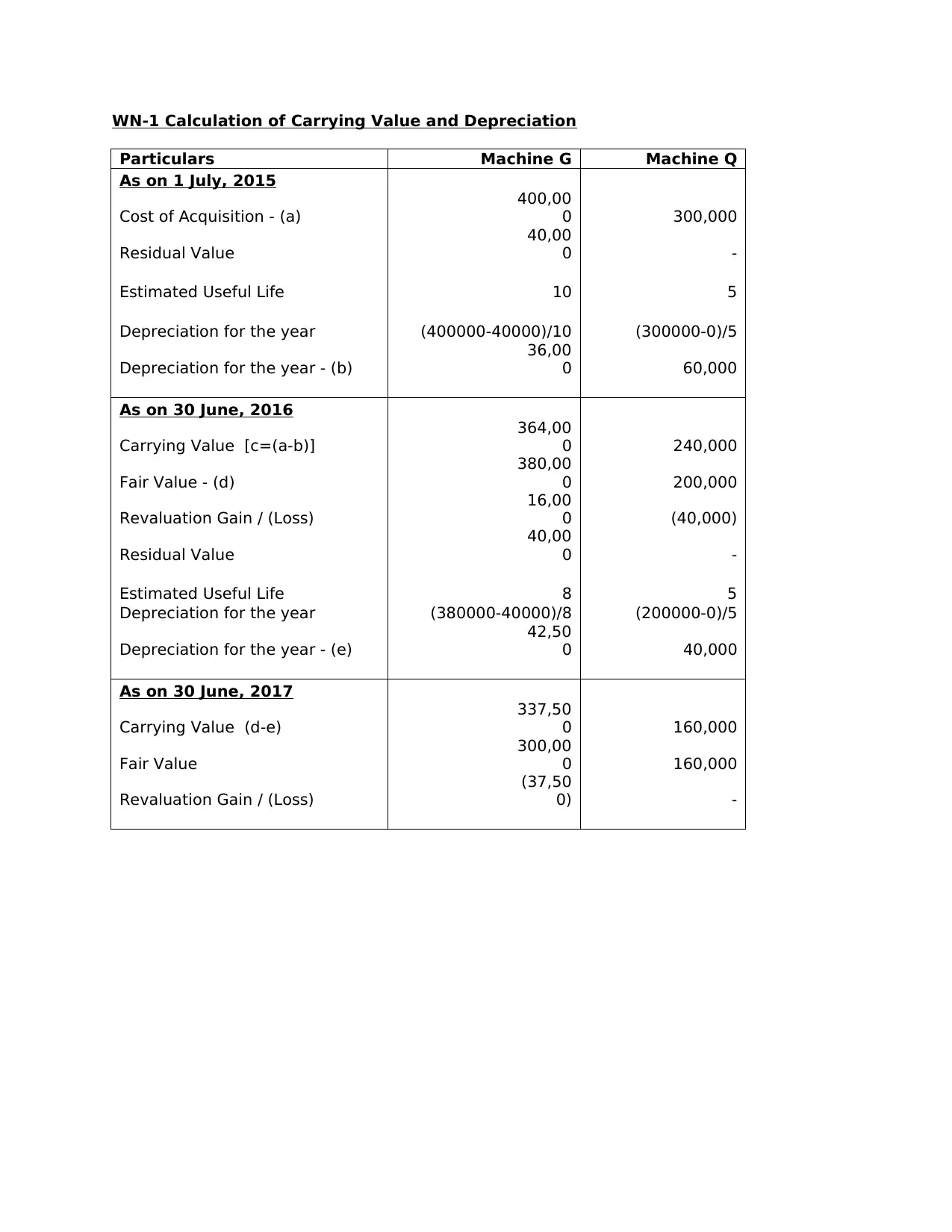

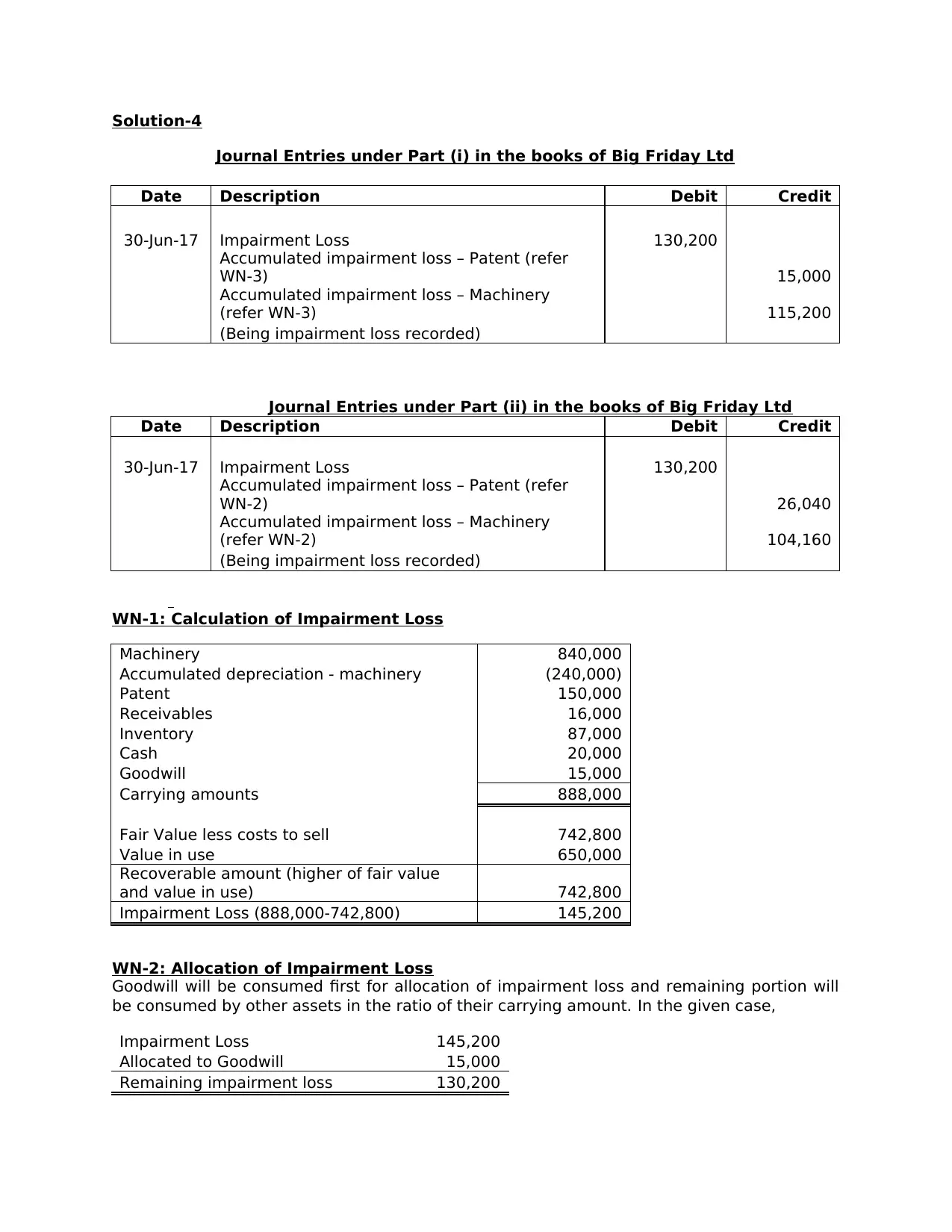

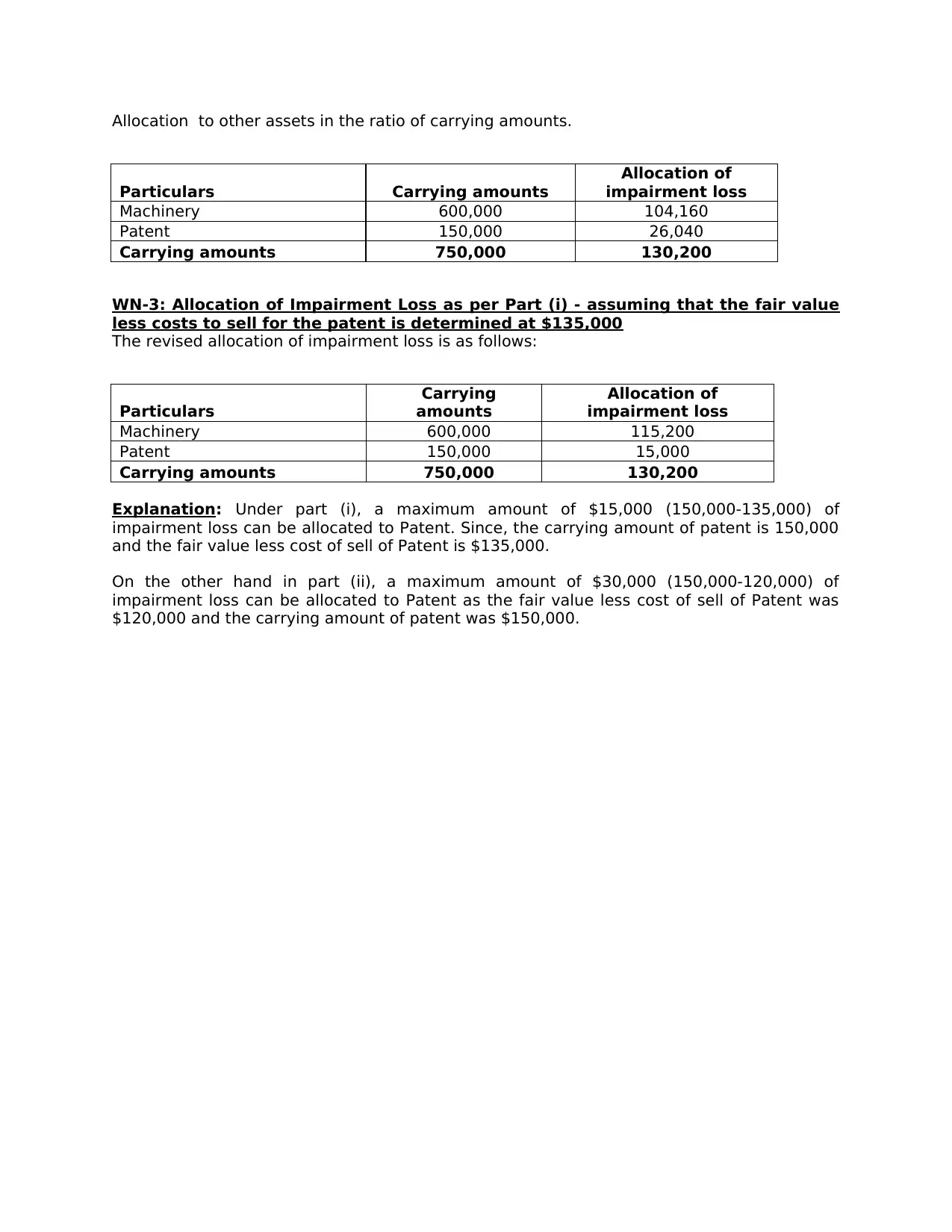

This document presents a series of financial accounting solutions, addressing key concepts such as the statement of financial position, journal entries, and impairment loss calculations. The first solution critiques a statement of financial position, highlighting issues related to current/non-current asset and liability classifications, presentation formats, and grouping errors, providing a revised statement as an enclosure. The second solution provides detailed journal entries for share transactions, including share application, allotment, and calls, along with the forfeiture and reissue of shares. The third solution focuses on accounting for machine revaluation and depreciation, including the journal entries for initial purchase, depreciation, and revaluation gains/losses, as well as the associated deferred tax implications. The fourth solution addresses impairment loss, including the calculation and allocation of impairment losses for both machinery and patents under different scenarios with varied fair values less costs to sell. These solutions offer a comprehensive guide to various financial accounting problems.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.