Financial Accounting: Brooks City Firm Case Study and Analysis

VerifiedAdded on 2023/01/10

|22

|4853

|86

Homework Assignment

AI Summary

This document provides a comprehensive solution to a financial accounting assignment, focusing on the operations of Brooks City accounting firm in London. The assignment covers core concepts such as single and double-entry bookkeeping, detailing the processes of sales, purchases, receipts, and payments. It includes journal entries, ledger accounts, and a trial balance, demonstrating the recording and summarization of financial transactions. Furthermore, the assignment differentiates between financial statements and financial reports, highlighting their uses for various stakeholders like owners, management, employees, clients, and investors. Scenario-based questions explore various accounting practices. The solution provides detailed explanations and analyses to aid in understanding financial accounting principles and their practical application within a business context.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3 (Difference between financial statement and financial report)............................................10

Question 4.............................................................................................................................................11

Question 5.............................................................................................................................................12

SCENARIO 2............................................................................................................................................13

Question 1.............................................................................................................................................13

Question 2.............................................................................................................................................14

Question 3.............................................................................................................................................14

Question 4.............................................................................................................................................15

(b) Explain the following terms.............................................................................................................16

Question 5.............................................................................................................................................16

CONCLUSION.........................................................................................................................................18

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3 (Difference between financial statement and financial report)............................................10

Question 4.............................................................................................................................................11

Question 5.............................................................................................................................................12

SCENARIO 2............................................................................................................................................13

Question 1.............................................................................................................................................13

Question 2.............................................................................................................................................14

Question 3.............................................................................................................................................14

Question 4.............................................................................................................................................15

(b) Explain the following terms.............................................................................................................16

Question 5.............................................................................................................................................16

CONCLUSION.........................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the process by which a company's operations information is

recorded, summarized and reported via financial reports. Those reports are: the report of profits,

the cash flow, the financial statement and the report of borrowed capital. Financial accounting is

primarily focused on producing such statements, based on gathered facts and implementing

"Generally Accepted Accounting Principles" (anything else recognized as GAAP). GAAP

establishes accounting guidelines on a broad variety of subjects in the United States, namely

financial statements of the company (Pelz, 2019). To better understand the concept of financial

accounting selected Brooks’ city accounting firm which is established in London. In this report

consist of various tasks of reporting business operations in terms of reports, ledger, trial balance,

and accounting records for different forms of company. This study also included a bank audit in

order to determine whether financial records are right or not.

SCENARIO 1

Question 1

There are different individual and double entry bookkeeping, there are many forms of

business activities that occurred. It has essentially four main types that are as follows:

Sales: This sale is carried out by company wherein they market their goods & payment systems

to any other organization and return the money to the client or may buy things on loan. Both

sales exchanges identified in accounting records but instead rendering publications and other

documents has been further evaluated for external reporting. During this contract, customers are

debited, and selling reports are paid.

Purchase: When an entity or individual purchases some products, the quickly went under

purchases. If the corporation is buying things, and the transaction is publicized as the debit of the

financial planning and the personal or lender to which the acquired person would be attributed.

This activity is mostly carried out in cash or on a credit-based basis. In addition, this expenditure

was registered for accounting purposes in the accounting records (Fang and et.al, 2016).

Receipts: If a corporation charges for selling products or services to some other organization,

such payments extend to other businesses or individuals. These same transactions are recorded in

publications where vendors are paid as credit and debit or card payments to exchange retained

earnings.

Payment: It involves corporate practices where companies are expected to lend on credit or

money rates to other entities. It will be reported in the financial accounts and are often published

by newspapers for accounting purposes. Spending is debt and profits owed to some other party.

Financial accounting is the process by which a company's operations information is

recorded, summarized and reported via financial reports. Those reports are: the report of profits,

the cash flow, the financial statement and the report of borrowed capital. Financial accounting is

primarily focused on producing such statements, based on gathered facts and implementing

"Generally Accepted Accounting Principles" (anything else recognized as GAAP). GAAP

establishes accounting guidelines on a broad variety of subjects in the United States, namely

financial statements of the company (Pelz, 2019). To better understand the concept of financial

accounting selected Brooks’ city accounting firm which is established in London. In this report

consist of various tasks of reporting business operations in terms of reports, ledger, trial balance,

and accounting records for different forms of company. This study also included a bank audit in

order to determine whether financial records are right or not.

SCENARIO 1

Question 1

There are different individual and double entry bookkeeping, there are many forms of

business activities that occurred. It has essentially four main types that are as follows:

Sales: This sale is carried out by company wherein they market their goods & payment systems

to any other organization and return the money to the client or may buy things on loan. Both

sales exchanges identified in accounting records but instead rendering publications and other

documents has been further evaluated for external reporting. During this contract, customers are

debited, and selling reports are paid.

Purchase: When an entity or individual purchases some products, the quickly went under

purchases. If the corporation is buying things, and the transaction is publicized as the debit of the

financial planning and the personal or lender to which the acquired person would be attributed.

This activity is mostly carried out in cash or on a credit-based basis. In addition, this expenditure

was registered for accounting purposes in the accounting records (Fang and et.al, 2016).

Receipts: If a corporation charges for selling products or services to some other organization,

such payments extend to other businesses or individuals. These same transactions are recorded in

publications where vendors are paid as credit and debit or card payments to exchange retained

earnings.

Payment: It involves corporate practices where companies are expected to lend on credit or

money rates to other entities. It will be reported in the financial accounts and are often published

by newspapers for accounting purposes. Spending is debt and profits owed to some other party.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Single entry book keeping: Single-entry bookkeeping is a simple and obvious recordkeeping

process, where expenditure is documented as a single item in a document. This is really a cash-

based form of book - keeping that records inbound and outbound cash in a document. They often

document financial transactions and payable accounts using the singular-entry bookkeeping

system. They will report money-book input and output cash. The financial assets are typically

tracked independently. Single-entry bookkeeping is characterized, as in the check ledger, by the

fact that one report on each operation is produced. Records are listed whether as a favorable or as

a specific value in one row. They would clearly retain a two-column ledger for singular-entry

bookkeeping, one section for revenue and one section for expenses. This is also called single-

entry, and there's only a row for every operation (Morales-Díaz and Zamora-Ramírez, 2018).

Double entry book keeping: Most companies, like the majority of small enterprises, have

double-entry bookkeeping to fulfill the financial obligations. Two book-keeping functions with

double entry in which each ledger has two sections, and then every transaction is in two

accounts. For each selling two activities are processed in one fund as just a reduction while in

other as an addition. When the company has to spend on investors, a double-entry payment will

be one instance. The amount of the corporation owing the lender should slash the balance of the

money market fund where the accounts payable is debited. Rather, double entry excludes the

money that the company starts paying to the creditor account as it received the firm's credit sum

and the corporation is enhancing and account will be credited.

Trial Balance and its importance

A trial balance is essentially a summary of the account transactions together with their

corresponding amount of debt or credit. The trial balance is not a structured financial statement

but instead a personality-check in order to decide whether debits are equivalent to balances.

Different entries in numerous items form a transaction. Taking all the ledger balances and

displaying them in a particular worksheet as at a particular date is Trial Balance. Team is

reviewing its month-end money transfers and classifying them into distinct areas. Presently they

make a sheet and divide the organizations into efficient / semi-effective ones (Kanodia and

Sapra, 2016).

The importance of a trial balance is to ensure that all expenditures reported in a firm's

cash book are properly accounted for. A trial balance shows the beginning equilibrium within

each general ledger account. The exact figure of the debits and credits amounts will suit it in

every other accounting point of view.

Question 2

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

process, where expenditure is documented as a single item in a document. This is really a cash-

based form of book - keeping that records inbound and outbound cash in a document. They often

document financial transactions and payable accounts using the singular-entry bookkeeping

system. They will report money-book input and output cash. The financial assets are typically

tracked independently. Single-entry bookkeeping is characterized, as in the check ledger, by the

fact that one report on each operation is produced. Records are listed whether as a favorable or as

a specific value in one row. They would clearly retain a two-column ledger for singular-entry

bookkeeping, one section for revenue and one section for expenses. This is also called single-

entry, and there's only a row for every operation (Morales-Díaz and Zamora-Ramírez, 2018).

Double entry book keeping: Most companies, like the majority of small enterprises, have

double-entry bookkeeping to fulfill the financial obligations. Two book-keeping functions with

double entry in which each ledger has two sections, and then every transaction is in two

accounts. For each selling two activities are processed in one fund as just a reduction while in

other as an addition. When the company has to spend on investors, a double-entry payment will

be one instance. The amount of the corporation owing the lender should slash the balance of the

money market fund where the accounts payable is debited. Rather, double entry excludes the

money that the company starts paying to the creditor account as it received the firm's credit sum

and the corporation is enhancing and account will be credited.

Trial Balance and its importance

A trial balance is essentially a summary of the account transactions together with their

corresponding amount of debt or credit. The trial balance is not a structured financial statement

but instead a personality-check in order to decide whether debits are equivalent to balances.

Different entries in numerous items form a transaction. Taking all the ledger balances and

displaying them in a particular worksheet as at a particular date is Trial Balance. Team is

reviewing its month-end money transfers and classifying them into distinct areas. Presently they

make a sheet and divide the organizations into efficient / semi-effective ones (Kanodia and

Sapra, 2016).

The importance of a trial balance is to ensure that all expenditures reported in a firm's

cash book are properly accounted for. A trial balance shows the beginning equilibrium within

each general ledger account. The exact figure of the debits and credits amounts will suit it in

every other accounting point of view.

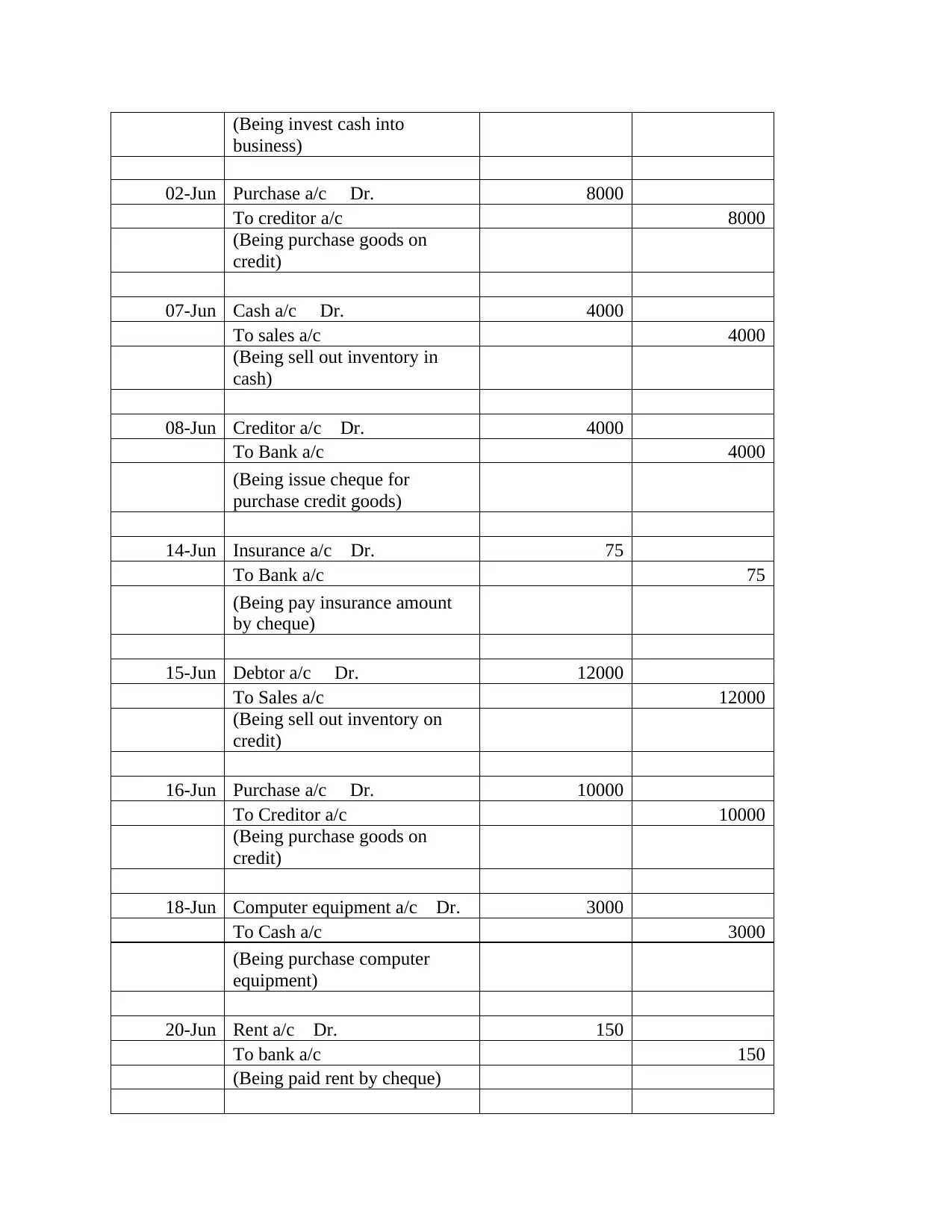

Question 2

Date Particulars Debit Credit

01-Jun Cash a/c Dr. 65000

To capital a/c 65000

(Being invest cash into

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

08-Jun Creditor a/c Dr. 4000

To Bank a/c 4000

(Being issue cheque for

purchase credit goods)

14-Jun Insurance a/c Dr. 75

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

business)

02-Jun Purchase a/c Dr. 8000

To creditor a/c 8000

(Being purchase goods on

credit)

07-Jun Cash a/c Dr. 4000

To sales a/c 4000

(Being sell out inventory in

cash)

08-Jun Creditor a/c Dr. 4000

To Bank a/c 4000

(Being issue cheque for

purchase credit goods)

14-Jun Insurance a/c Dr. 75

To Bank a/c 75

(Being pay insurance amount

by cheque)

15-Jun Debtor a/c Dr. 12000

To Sales a/c 12000

(Being sell out inventory on

credit)

16-Jun Purchase a/c Dr. 10000

To Creditor a/c 10000

(Being purchase goods on

credit)

18-Jun Computer equipment a/c Dr. 3000

To Cash a/c 3000

(Being purchase computer

equipment)

20-Jun Rent a/c Dr. 150

To bank a/c 150

(Being paid rent by cheque)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

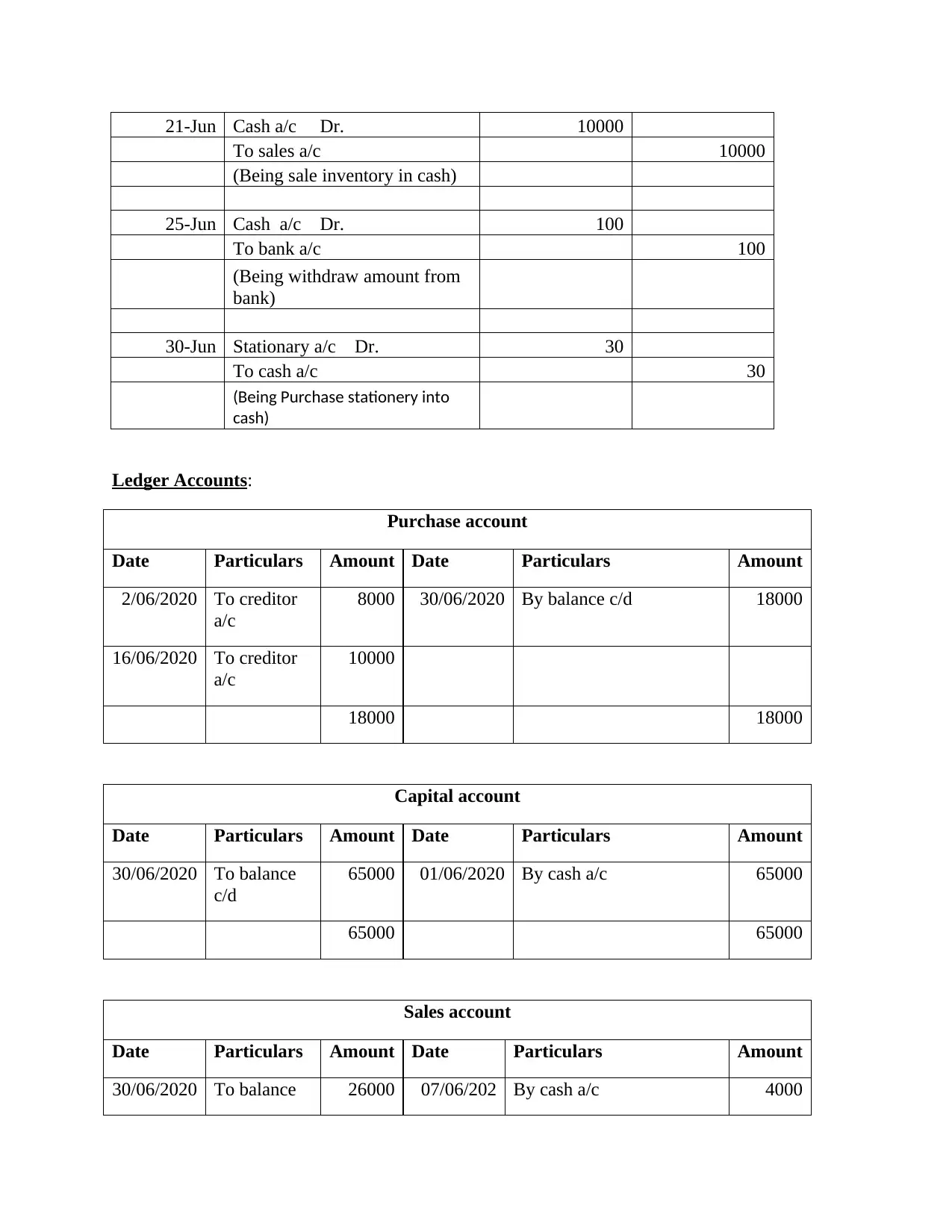

21-Jun Cash a/c Dr. 10000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

To cash a/c 30

(Being Purchase stationery into

cash)

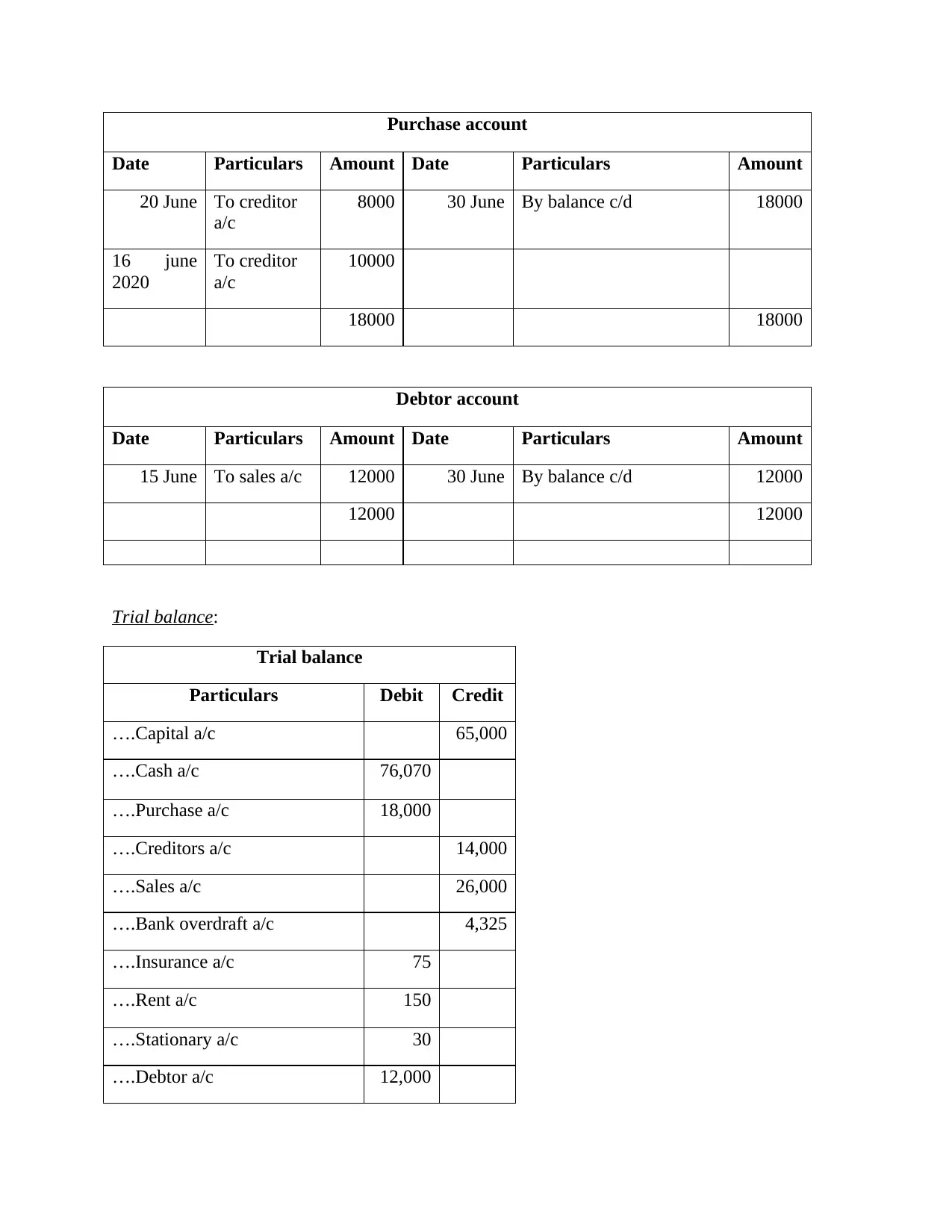

Ledger Accounts:

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Capital account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

65000 01/06/2020 By cash a/c 65000

65000 65000

Sales account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance 26000 07/06/202 By cash a/c 4000

To sales a/c 10000

(Being sale inventory in cash)

25-Jun Cash a/c Dr. 100

To bank a/c 100

(Being withdraw amount from

bank)

30-Jun Stationary a/c Dr. 30

To cash a/c 30

(Being Purchase stationery into

cash)

Ledger Accounts:

Purchase account

Date Particulars Amount Date Particulars Amount

2/06/2020 To creditor

a/c

8000 30/06/2020 By balance c/d 18000

16/06/2020 To creditor

a/c

10000

18000 18000

Capital account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance

c/d

65000 01/06/2020 By cash a/c 65000

65000 65000

Sales account

Date Particulars Amount Date Particulars Amount

30/06/2020 To balance 26000 07/06/202 By cash a/c 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c/d 0

15/06/202

0

By debtor a/c 12000

21/06/202

0

By cash a/c 10000

26000 26000

Computer equipment account

Date Particulars Amount Date Particulars Amount

18/06/2020 To cash a/c 3,000 30/06/2020 By balance c/d 3,000

3,000 3,000

Bank account

Date Particulars Amount Date Particulars Amount

30 June To balance

c/d

4325 8 June By creditor a/c 4000

14 June By insurance a/c 75

20 June By rent a/c 150

25 June By cash a/c 100

4325 4325

Cash account

Date Particulars Amount Date Particulars Amount

1 June To capital

a/c

65000 18 June By computer equipment

a/c

3000

7 June To sales a/c 4000 30 June By stationary a/c 30

21 June To sales a/c 10000 30 June By balance c/d 76070

15/06/202

0

By debtor a/c 12000

21/06/202

0

By cash a/c 10000

26000 26000

Computer equipment account

Date Particulars Amount Date Particulars Amount

18/06/2020 To cash a/c 3,000 30/06/2020 By balance c/d 3,000

3,000 3,000

Bank account

Date Particulars Amount Date Particulars Amount

30 June To balance

c/d

4325 8 June By creditor a/c 4000

14 June By insurance a/c 75

20 June By rent a/c 150

25 June By cash a/c 100

4325 4325

Cash account

Date Particulars Amount Date Particulars Amount

1 June To capital

a/c

65000 18 June By computer equipment

a/c

3000

7 June To sales a/c 4000 30 June By stationary a/c 30

21 June To sales a/c 10000 30 June By balance c/d 76070

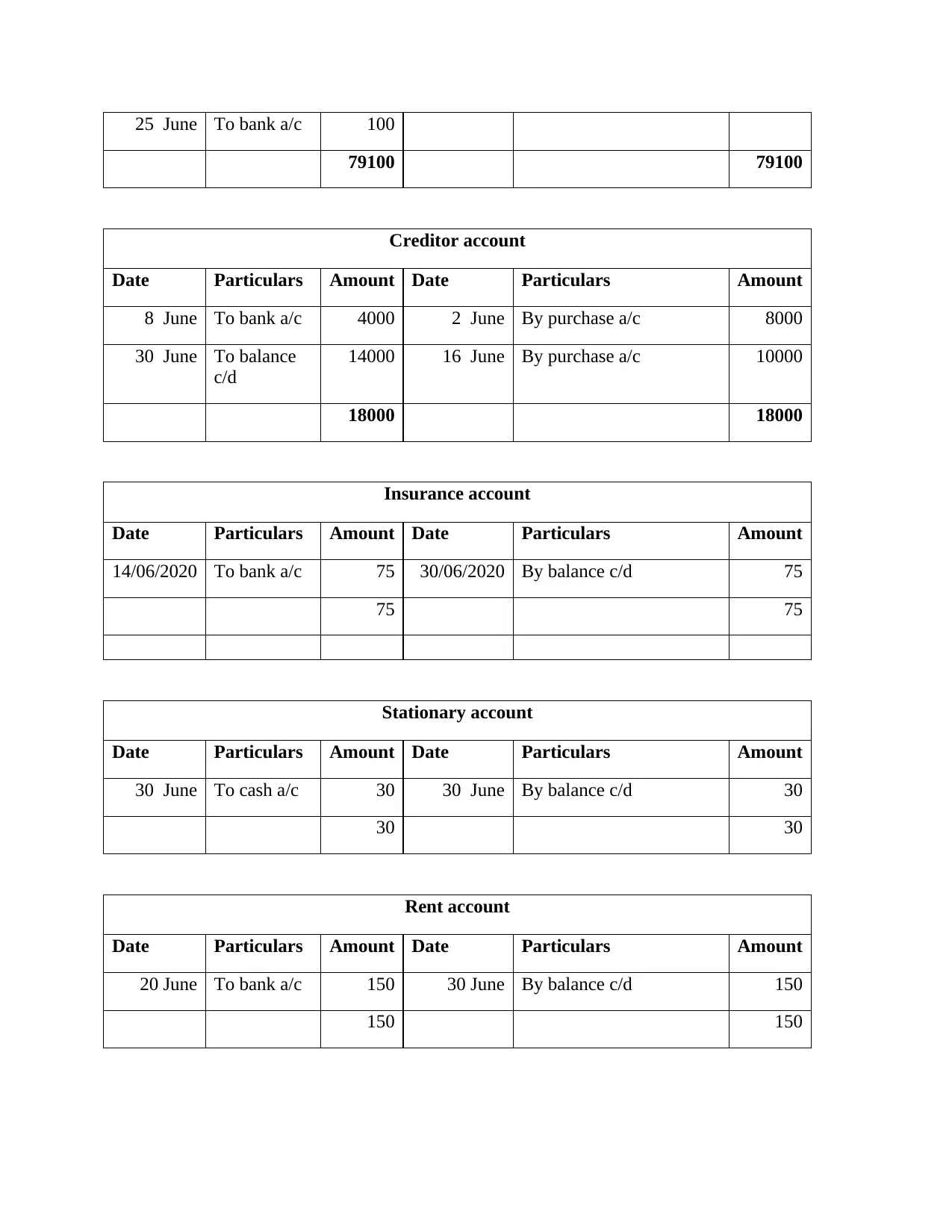

25 June To bank a/c 100

79100 79100

Creditor account

Date Particulars Amount Date Particulars Amount

8 June To bank a/c 4000 2 June By purchase a/c 8000

30 June To balance

c/d

14000 16 June By purchase a/c 10000

18000 18000

Insurance account

Date Particulars Amount Date Particulars Amount

14/06/2020 To bank a/c 75 30/06/2020 By balance c/d 75

75 75

Stationary account

Date Particulars Amount Date Particulars Amount

30 June To cash a/c 30 30 June By balance c/d 30

30 30

Rent account

Date Particulars Amount Date Particulars Amount

20 June To bank a/c 150 30 June By balance c/d 150

150 150

79100 79100

Creditor account

Date Particulars Amount Date Particulars Amount

8 June To bank a/c 4000 2 June By purchase a/c 8000

30 June To balance

c/d

14000 16 June By purchase a/c 10000

18000 18000

Insurance account

Date Particulars Amount Date Particulars Amount

14/06/2020 To bank a/c 75 30/06/2020 By balance c/d 75

75 75

Stationary account

Date Particulars Amount Date Particulars Amount

30 June To cash a/c 30 30 June By balance c/d 30

30 30

Rent account

Date Particulars Amount Date Particulars Amount

20 June To bank a/c 150 30 June By balance c/d 150

150 150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase account

Date Particulars Amount Date Particulars Amount

20 June To creditor

a/c

8000 30 June By balance c/d 18000

16 june

2020

To creditor

a/c

10000

18000 18000

Debtor account

Date Particulars Amount Date Particulars Amount

15 June To sales a/c 12000 30 June By balance c/d 12000

12000 12000

Trial balance:

Trial balance

Particulars Debit Credit

….Capital a/c 65,000

….Cash a/c 76,070

….Purchase a/c 18,000

….Creditors a/c 14,000

….Sales a/c 26,000

….Bank overdraft a/c 4,325

….Insurance a/c 75

….Rent a/c 150

….Stationary a/c 30

….Debtor a/c 12,000

Date Particulars Amount Date Particulars Amount

20 June To creditor

a/c

8000 30 June By balance c/d 18000

16 june

2020

To creditor

a/c

10000

18000 18000

Debtor account

Date Particulars Amount Date Particulars Amount

15 June To sales a/c 12000 30 June By balance c/d 12000

12000 12000

Trial balance:

Trial balance

Particulars Debit Credit

….Capital a/c 65,000

….Cash a/c 76,070

….Purchase a/c 18,000

….Creditors a/c 14,000

….Sales a/c 26,000

….Bank overdraft a/c 4,325

….Insurance a/c 75

….Rent a/c 150

….Stationary a/c 30

….Debtor a/c 12,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

….Computer equipment a/c 3,000

109,32

5

109,32

5

Question 3

Financial statement: Investors, industry observers and lenders should use financial

statements to determine the financial stability and financial returns of an enterprise. The three

main sections in the financial statements are the cash flow, sales report and income statement.

Monetary assertions are published documents of the financial position of a company. This

included regular reports such as the balance sheet, report of sales or profits and losses, and

financial statement. These are one of the most critical aspects of business records and the

primary means of transmitting financial data with third parties about such an organization.

Financial Reporting includes reporting detailed information for different key

stakeholders the company's monetary results and financial status for a specific period of time.

Such participants are investors, lenders, the community, debt suppliers, government departments

and legislatures. The intensity of the financial reporting is weekly & yearly for public firms.

Financial reporting is normally regarded a bookkeeping end commodity. Offer insight into the

financial situation, results and adjustments in the economic situations of a business which is

important for a variety of economic interest to the miner (Lara and et.al, 2017).

Financial reports and statements are often used synonymously. There are several

differences in the financial statement and the fiscal audit and analyses. Documentation can be

used to endorse details about decision-making. The monitoring of financial matters is much more

formal. They are using reporting to get another-party entities to convey financial wellness. The

annual accounts are filed for every fiscal year. Throughout the financial reports involves the

study of the factors used to assess the financial position of the organisation in regard of

profitability, liquidity and effectiveness. In comparison, the financial statements contain the

capital structure, income and loss and other comprehensive income, cash flow, report of cash

budget etc.

In the sense of Brooks’ city Financial Group there are many applications of financial

statements but those are mentioned elsewhere here:

Owner: investors and investors need financial experience to help them decide what to do about

their properties, including such keeping, purchasing or selling more.

Leadership: Land owners and administrators may be involved. The local business planning,

though, is usually comprised of recruited specialists who have now been granted the duty to run

the enterprise or an economic side. They serve as representatives of secret sources.

109,32

5

109,32

5

Question 3

Financial statement: Investors, industry observers and lenders should use financial

statements to determine the financial stability and financial returns of an enterprise. The three

main sections in the financial statements are the cash flow, sales report and income statement.

Monetary assertions are published documents of the financial position of a company. This

included regular reports such as the balance sheet, report of sales or profits and losses, and

financial statement. These are one of the most critical aspects of business records and the

primary means of transmitting financial data with third parties about such an organization.

Financial Reporting includes reporting detailed information for different key

stakeholders the company's monetary results and financial status for a specific period of time.

Such participants are investors, lenders, the community, debt suppliers, government departments

and legislatures. The intensity of the financial reporting is weekly & yearly for public firms.

Financial reporting is normally regarded a bookkeeping end commodity. Offer insight into the

financial situation, results and adjustments in the economic situations of a business which is

important for a variety of economic interest to the miner (Lara and et.al, 2017).

Financial reports and statements are often used synonymously. There are several

differences in the financial statement and the fiscal audit and analyses. Documentation can be

used to endorse details about decision-making. The monitoring of financial matters is much more

formal. They are using reporting to get another-party entities to convey financial wellness. The

annual accounts are filed for every fiscal year. Throughout the financial reports involves the

study of the factors used to assess the financial position of the organisation in regard of

profitability, liquidity and effectiveness. In comparison, the financial statements contain the

capital structure, income and loss and other comprehensive income, cash flow, report of cash

budget etc.

In the sense of Brooks’ city Financial Group there are many applications of financial

statements but those are mentioned elsewhere here:

Owner: investors and investors need financial experience to help them decide what to do about

their properties, including such keeping, purchasing or selling more.

Leadership: Land owners and administrators may be involved. The local business planning,

though, is usually comprised of recruited specialists who have now been granted the duty to run

the enterprise or an economic side. They serve as representatives of secret sources.

Employees: such people are so keen on enterprise sustainable development and ability to survive.

They're so much about the business being able to afford wages and also offering workplace

opportunities. They may also be interested in financial position and effects to assess market

development prospects and career progression.

Clients: Once a lengthy-term engagement or partnership has been reached between both the

business and its customers, buyers become interested in the capability of the firm to immediately

follow its existence and sustain operating consistency. Its use is even enhanced in situations

where the organization is also dependent on the customers (Rezaee and Tuo, 2017).

Investors: Future investors need financial reporting to determine the company's efficiency and

future for productivity. Likewise, smaller businesses require personal and financial information

to make sure that the project is worthwhile or even if it must proceed, be enhanced or go down.

The information provided in the financial reporting mentioned above are restricted, there are

much more still who needed the data to make their judgments. They can be both internally and

externally financial statements consumers. Likewise, Brooks’ city organization provides detailed

statements for its customers' use.

Question 4

There are many basic principles that are very crucial for investment companies to

implement in order to preserve their account balances and display information as per the

concepts. These are as follows:

Monetary transactions: Accounting intends to measure all the true economic entity values. It is

not possible because as barter system cannot be given for this. Therefore, applying definitions to

entities and items is a question, since it is subjective. Nevertheless, reporting has suggested

standards for working with exactly the very same (Demerjian and Owens, 2016).

Going concern: This term indicates the business will proceed to do its usual life during the next

going to make money is given up and the reverse is not stated. Because of the principle of viable

business, businesses will operate on loans, pay for additional payments and deferred revenue that

they intend to receive or repay over their lifespan, and experience impairment if the process has

been used for centuries to come.

Conservatism principle: specialists are generally seen to be very radical. They want to keep

optimistic, and start preparing for something worse. The regulations they produced for their

professional life show this. Constancy concept is also another core element of financial

reporting. Regardless of this principle, in which the sum of expected inflows over a period is in

question, the business will report the minimum compensation method and the most cost

necessary.

They're so much about the business being able to afford wages and also offering workplace

opportunities. They may also be interested in financial position and effects to assess market

development prospects and career progression.

Clients: Once a lengthy-term engagement or partnership has been reached between both the

business and its customers, buyers become interested in the capability of the firm to immediately

follow its existence and sustain operating consistency. Its use is even enhanced in situations

where the organization is also dependent on the customers (Rezaee and Tuo, 2017).

Investors: Future investors need financial reporting to determine the company's efficiency and

future for productivity. Likewise, smaller businesses require personal and financial information

to make sure that the project is worthwhile or even if it must proceed, be enhanced or go down.

The information provided in the financial reporting mentioned above are restricted, there are

much more still who needed the data to make their judgments. They can be both internally and

externally financial statements consumers. Likewise, Brooks’ city organization provides detailed

statements for its customers' use.

Question 4

There are many basic principles that are very crucial for investment companies to

implement in order to preserve their account balances and display information as per the

concepts. These are as follows:

Monetary transactions: Accounting intends to measure all the true economic entity values. It is

not possible because as barter system cannot be given for this. Therefore, applying definitions to

entities and items is a question, since it is subjective. Nevertheless, reporting has suggested

standards for working with exactly the very same (Demerjian and Owens, 2016).

Going concern: This term indicates the business will proceed to do its usual life during the next

going to make money is given up and the reverse is not stated. Because of the principle of viable

business, businesses will operate on loans, pay for additional payments and deferred revenue that

they intend to receive or repay over their lifespan, and experience impairment if the process has

been used for centuries to come.

Conservatism principle: specialists are generally seen to be very radical. They want to keep

optimistic, and start preparing for something worse. The regulations they produced for their

professional life show this. Constancy concept is also another core element of financial

reporting. Regardless of this principle, in which the sum of expected inflows over a period is in

question, the business will report the minimum compensation method and the most cost

necessary.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.