Financial Accounting Assignment - Course FINC101 - Solutions

VerifiedAdded on 2022/09/11

|18

|1797

|27

Homework Assignment

AI Summary

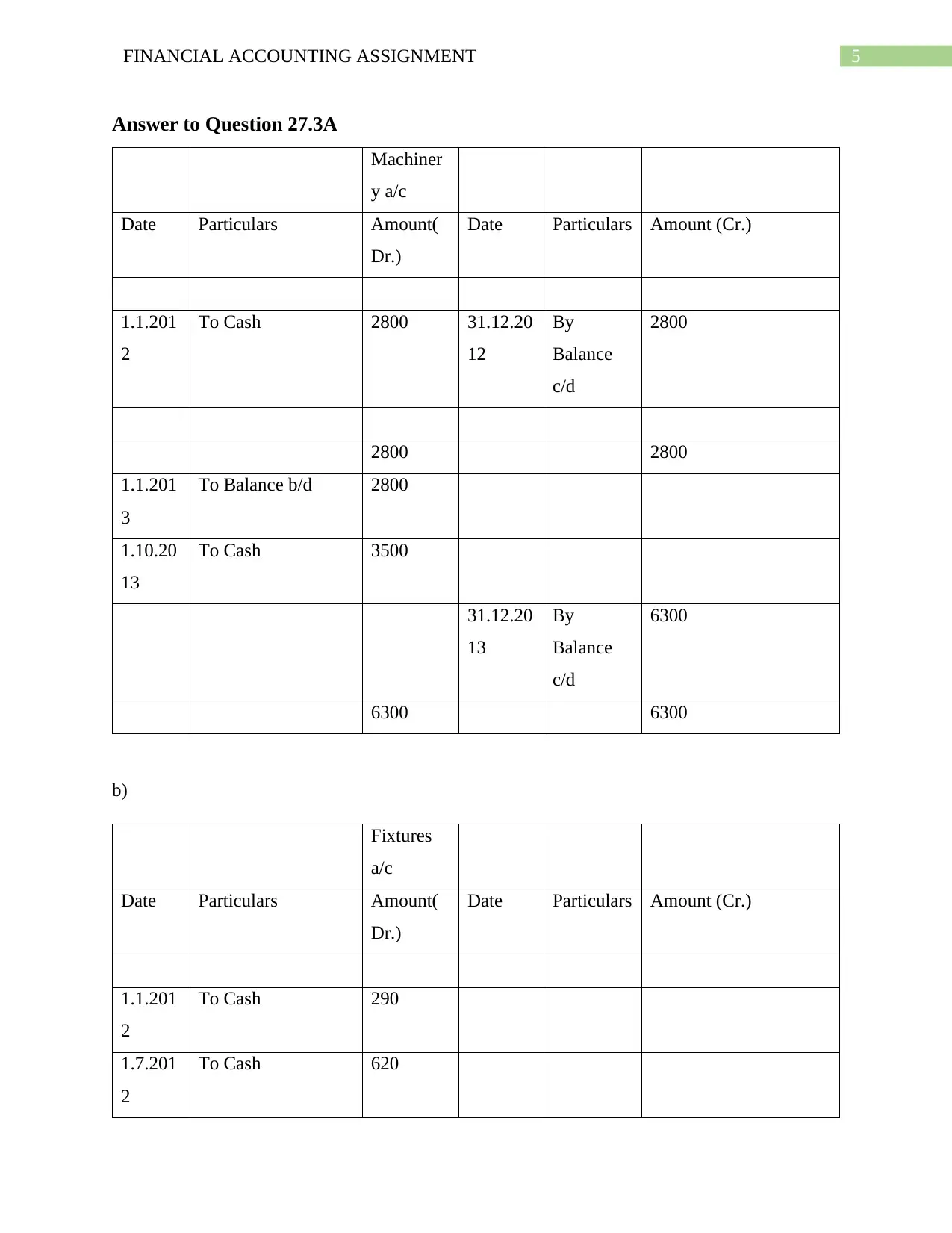

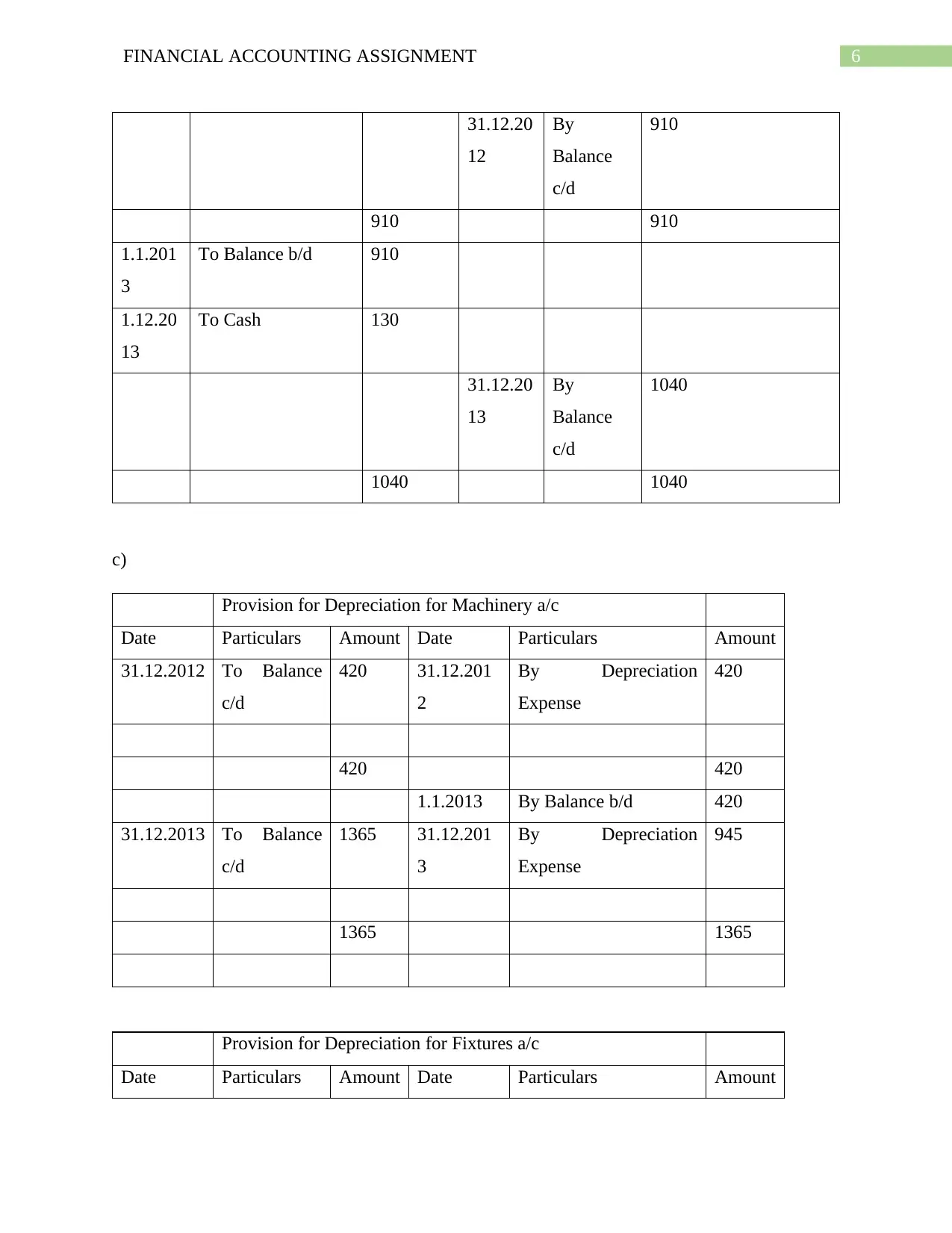

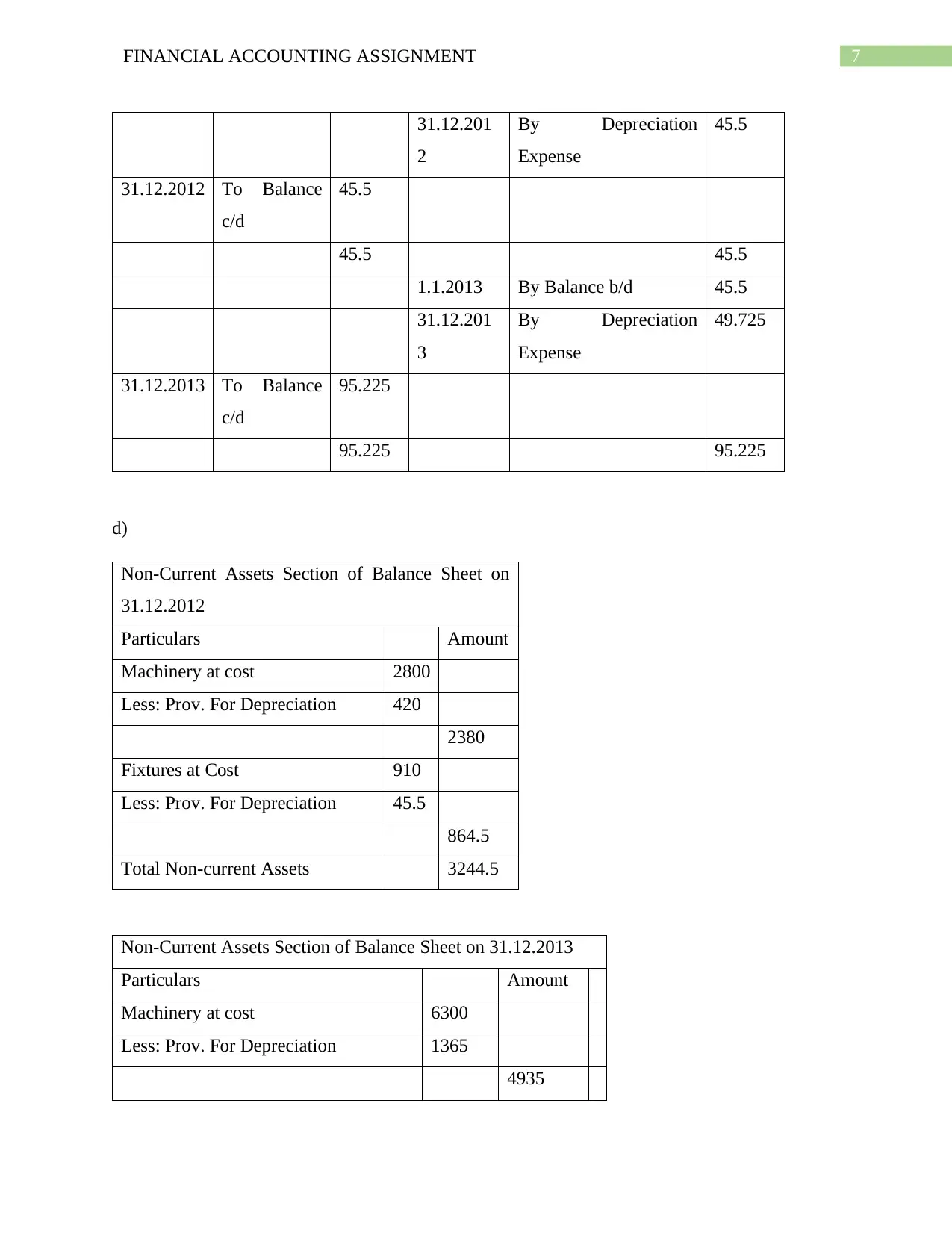

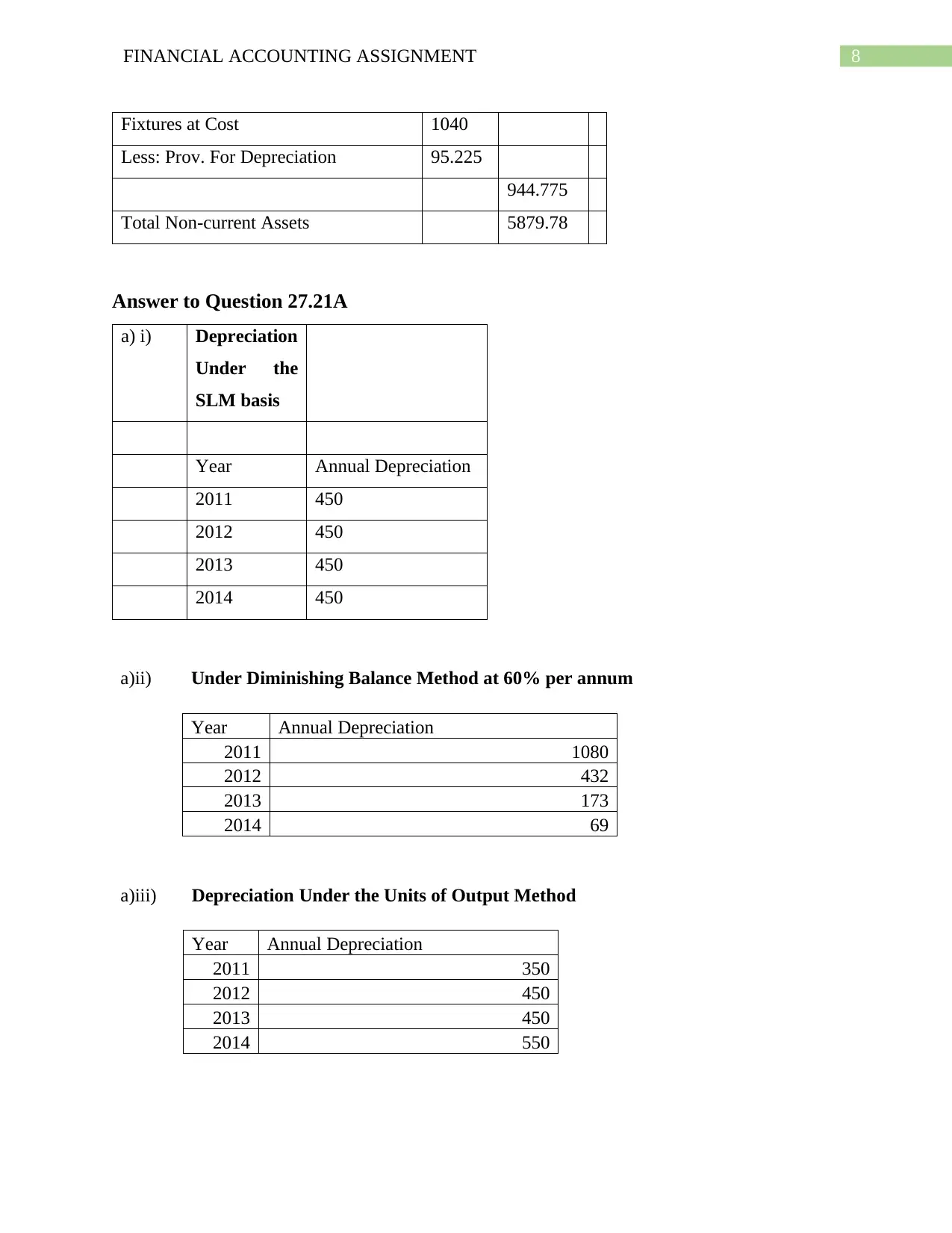

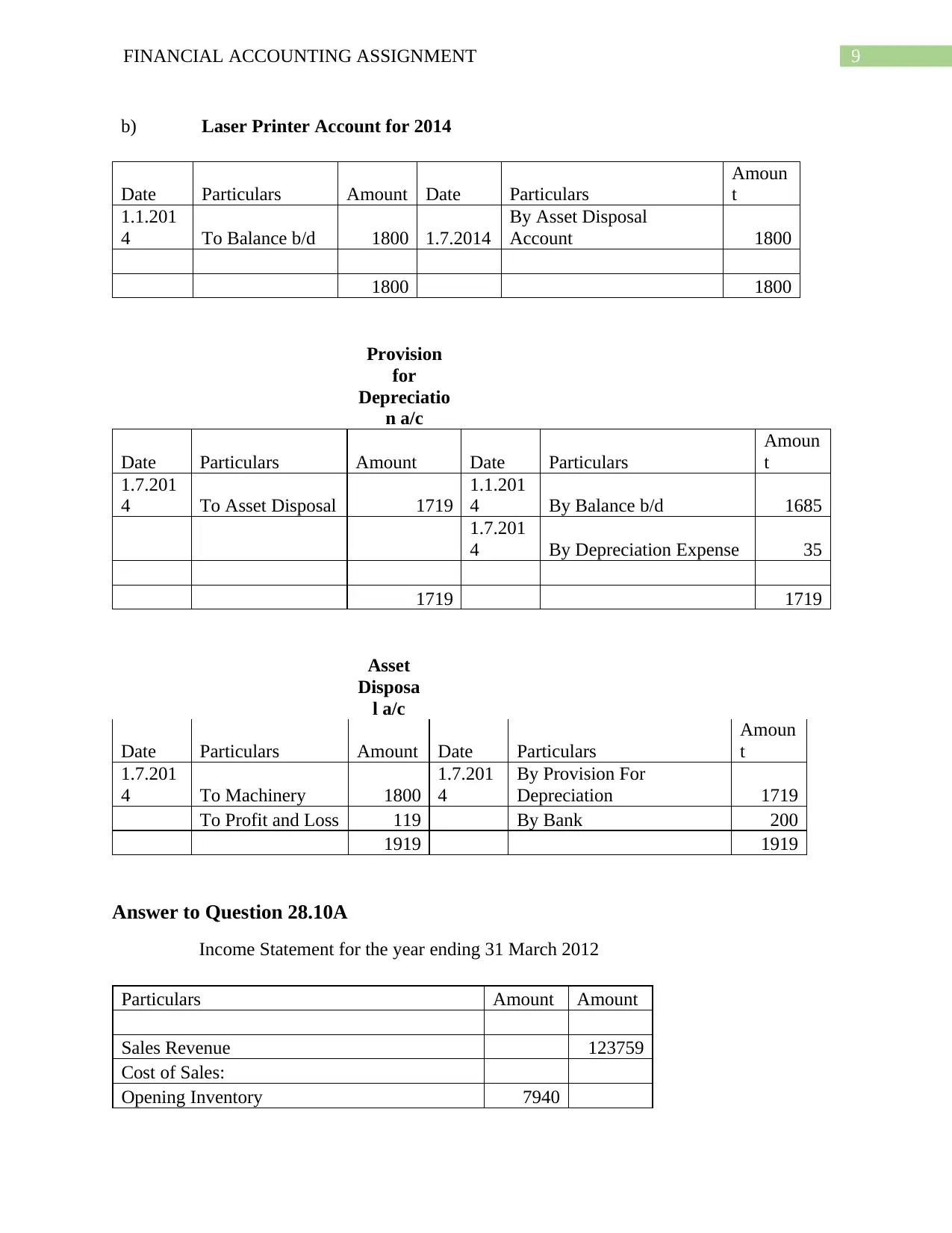

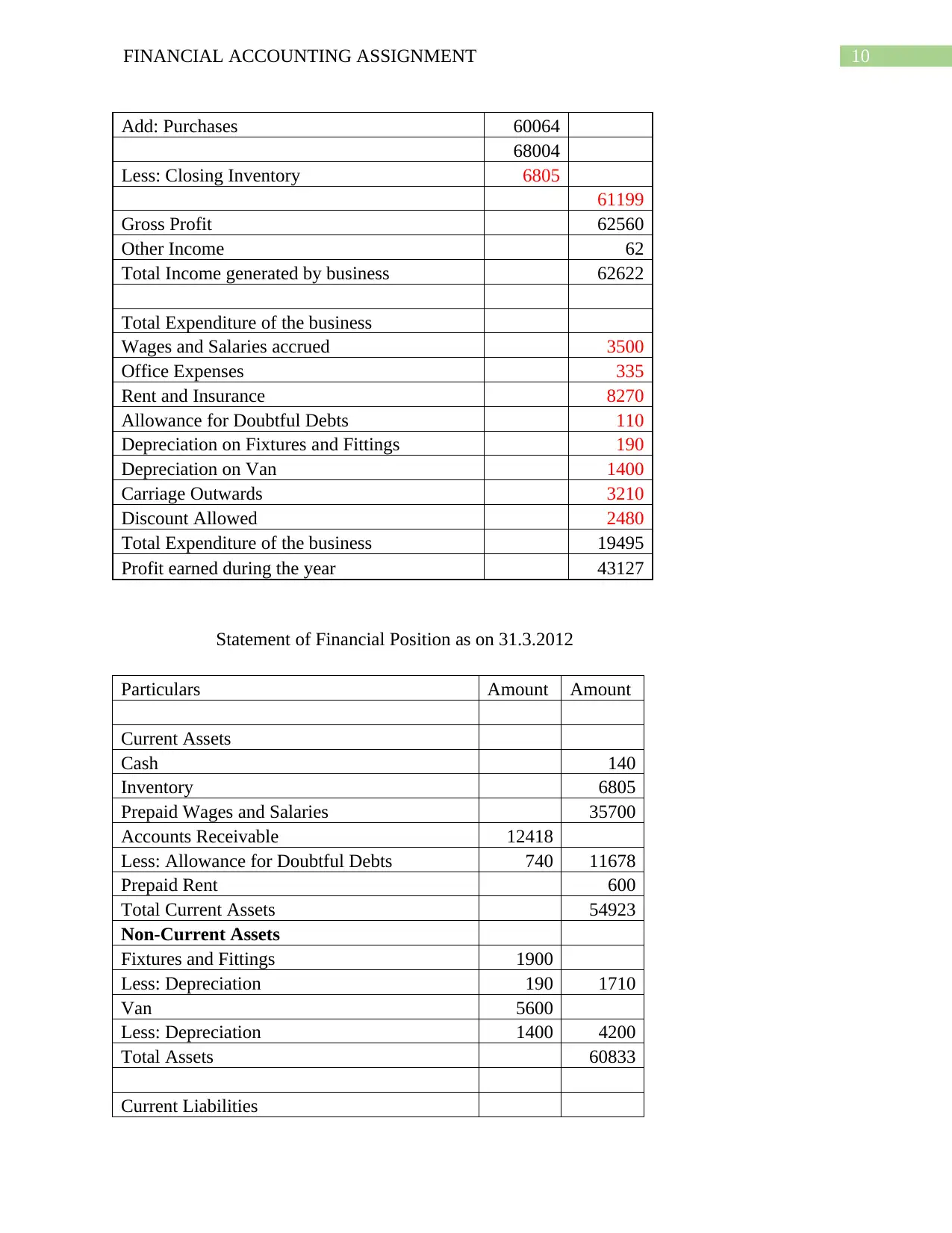

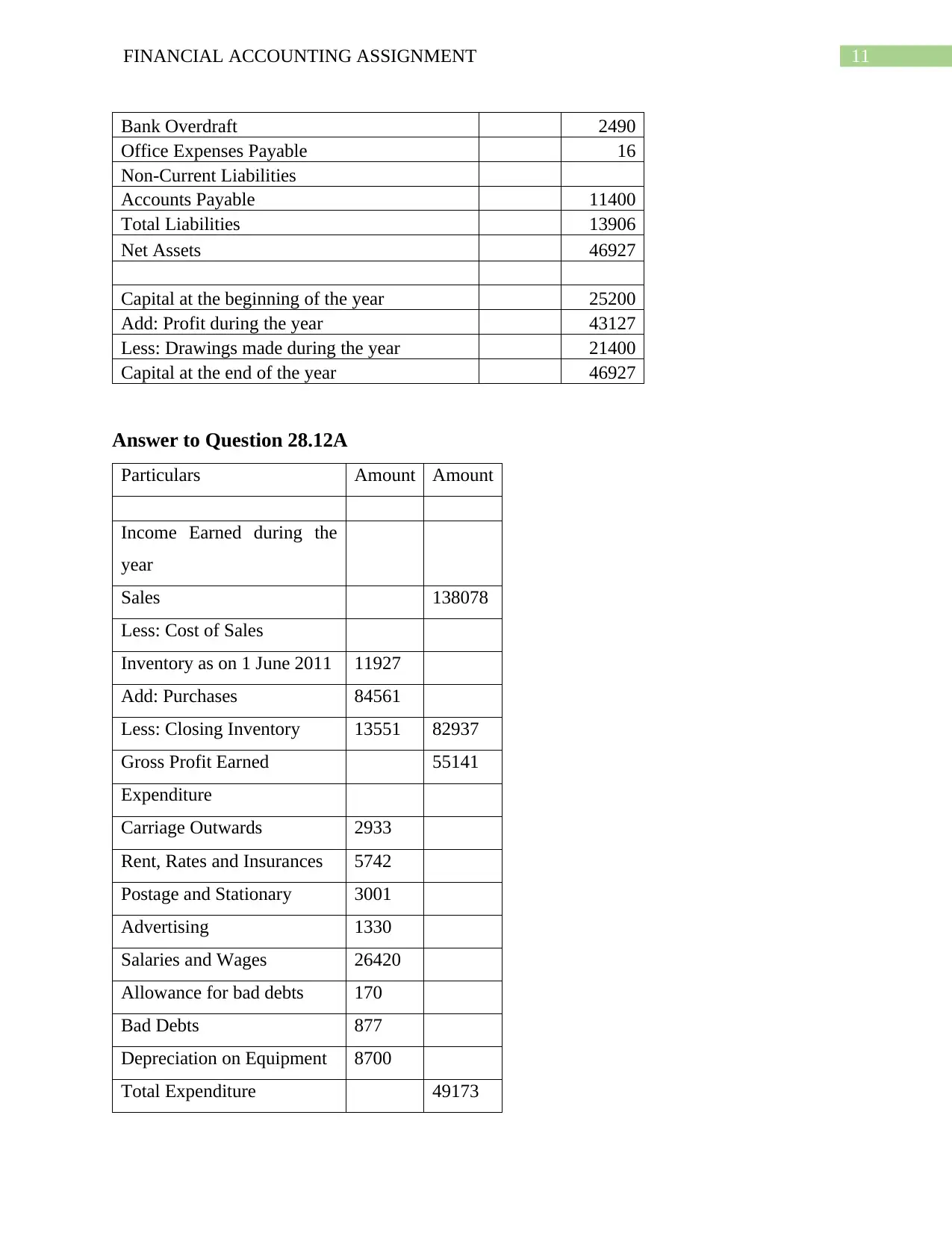

This document presents a comprehensive solution to a financial accounting assignment, addressing multiple questions and concepts. The assignment covers a wide array of topics, including bad debts, depreciation methods (straight-line, reducing balance, and units of output), asset accounting, income statements, balance sheets, inventory valuation (FIFO, LIFO, and AVCO), and cash flow statements. It also explores ratio analysis, providing insights into profitability, liquidity, and efficiency. Detailed calculations, journal entries, and financial statements are included to demonstrate the application of accounting principles. The solutions provide a thorough understanding of financial accounting concepts and their practical application.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.