Detailed Report: Financial Accounting Practices of Spark New Zealand

VerifiedAdded on 2022/11/16

|14

|3508

|109

Report

AI Summary

This report provides a comprehensive analysis of the financial accounting practices of Spark New Zealand. It begins with an introduction to the importance of high-quality financial reporting and the role of the IASB and AASB in establishing accounting standards. The report then details several key accounting concepts used by Spark New Zealand, including the business entity concept, money measurement concept, going concern concept, accounting period concept, accounting cost concept, dual aspect concept, realization concept, and accrual concept. Furthermore, it delves into the measurement debate within accounting, examining different measurement bases such as historical cost and fair value, and their impact on financial reporting, with specific examples from Spark New Zealand's annual report. The report also discusses the importance of relevance and representational faithfulness in the conceptual accounting framework. The report concludes by summarizing the key findings and referencing the sources used.

Advance financial accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................3

Description of accounting concepts used by Spark New Zealand to prepare the annual report......3

Measurement Debate in Accounting in Reference to the Conceptual Framework and Examples

from the Selected Company.............................................................................................................7

Understanding of Relevance and Representational Faithfulness of Conceptual Accounting

Framework.....................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

Introduction......................................................................................................................................3

Description of accounting concepts used by Spark New Zealand to prepare the annual report......3

Measurement Debate in Accounting in Reference to the Conceptual Framework and Examples

from the Selected Company.............................................................................................................7

Understanding of Relevance and Representational Faithfulness of Conceptual Accounting

Framework.....................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

2

Introduction

The business entities are required to develop and provide high quality financial reports

for communicating its key financial results and figures to the end-users such as investors,

creditor, lenders and others. It is highly necessary that the business develop the financial reports

in compliance with the relevant accounting standards and policies to ensure that high quality

information is disclosed as it provides basis for the end-users to take various type of decisions.

The IASB (International Accounting Standards Board) has provided the conceptual accounting

frameworks in this context for ensuring that business entities worldwide develop high quality

financial reports by complying with the accounting concepts and principles provided by it. The

AASB (Australian Accounting Standards Board) also complies with the IASB standards and thus

have directed the business entities to follow the principles of conceptual accounting framework

in development of their financial reports.

This report has been prepared in the context of examining the annual report of a selected

ASX listed entity, that is, Spark New Zealand Foreign Exempt, a telecommunication company

involves in providing telephone and internet services across New Zealand. This report examines

the accounting concepts used by the company in addition with the measurement issues faced as

stated by the conceptual accounting framework. Also, it has discussed the importance of

relevance and representational faithfulness in the financial accounting framework as provided by

the conceptual accounting framework with the use of examples from the selected company.

Description of accounting concepts used by Spark New Zealand to prepare the annual

report

There are various accounting methods and valuation techniques available to perform

accounting of same financial items. So, it is very important to bring in uniformity and

consistency in recording the accounting transaction so that book of accounts maintain by

companies all over the world can have some sort of comparability. In order to maintain the

uniformity and consistency in books of accounts, international accounting bodies have developed

certain rules or principles and they are classified as accountings concepts and conventions. The

role of accounting concepts is to provide the basic accounting assumptions, rules and principles

to the accountants which act as the basis for recording accounting transactions and preparation of

3

The business entities are required to develop and provide high quality financial reports

for communicating its key financial results and figures to the end-users such as investors,

creditor, lenders and others. It is highly necessary that the business develop the financial reports

in compliance with the relevant accounting standards and policies to ensure that high quality

information is disclosed as it provides basis for the end-users to take various type of decisions.

The IASB (International Accounting Standards Board) has provided the conceptual accounting

frameworks in this context for ensuring that business entities worldwide develop high quality

financial reports by complying with the accounting concepts and principles provided by it. The

AASB (Australian Accounting Standards Board) also complies with the IASB standards and thus

have directed the business entities to follow the principles of conceptual accounting framework

in development of their financial reports.

This report has been prepared in the context of examining the annual report of a selected

ASX listed entity, that is, Spark New Zealand Foreign Exempt, a telecommunication company

involves in providing telephone and internet services across New Zealand. This report examines

the accounting concepts used by the company in addition with the measurement issues faced as

stated by the conceptual accounting framework. Also, it has discussed the importance of

relevance and representational faithfulness in the financial accounting framework as provided by

the conceptual accounting framework with the use of examples from the selected company.

Description of accounting concepts used by Spark New Zealand to prepare the annual

report

There are various accounting methods and valuation techniques available to perform

accounting of same financial items. So, it is very important to bring in uniformity and

consistency in recording the accounting transaction so that book of accounts maintain by

companies all over the world can have some sort of comparability. In order to maintain the

uniformity and consistency in books of accounts, international accounting bodies have developed

certain rules or principles and they are classified as accountings concepts and conventions. The

role of accounting concepts is to provide the basic accounting assumptions, rules and principles

to the accountants which act as the basis for recording accounting transactions and preparation of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statements (Mirza and Knorr, 2011). Below are some important accounting concepts

that are mandatory for the companies all over the world to apply while performing the process of

financial reporting:

Business Entity Concept: As per this accounting concept, it is assumed that business enterprise

and business owners are two separate bodies or entity and it is important to keep personal

transactions and business transactions separate. It can be understand from the example that,

Spark New Zealand has shown owner’s capital or share capital under heading equity and liability

not as the asset of the company.

Money Measurement Concept: As per this accounting concept it is mandatory for all entities to

record only those transactions that can be measured in terms of money and should record them in

Country’s Currency. For example, company established in Australia will use Australian Dollar to

record all the transactions. It means company cannot record transactions that cannot be expressed

in books of accounts. In case of Spark New Zealand, all the transactions have been shown in

Australian Dollar and there are no transactions that have expressed as non monetary items. The

purpose of this accounting concept is to help the accountants to know what transactions have to

be recorded and what not to record (Needles, Powers and Crosson, 2013).

Going Concern Concept: This concept states that entity will continue forever for an indefinite

time period and it cannot be liquidated unless there is requirement to do so. This concept is most

important accounting concept as it provides the basis for calculating the value of assets and

liabilities. It can be understood from example that total value of purchases of plant and

machinery is being charged as depreciation up to the life of asset not as the expense in first year

itself. Spark New Zealand has followed this accounting concept as it deferred many expenses

and income in form of assets and liabilities in the balance which is a clear indication that

company based its accounting process through using going concern concept (Wahlen, Baginski

and Bradshaw, 2017).

4

that are mandatory for the companies all over the world to apply while performing the process of

financial reporting:

Business Entity Concept: As per this accounting concept, it is assumed that business enterprise

and business owners are two separate bodies or entity and it is important to keep personal

transactions and business transactions separate. It can be understand from the example that,

Spark New Zealand has shown owner’s capital or share capital under heading equity and liability

not as the asset of the company.

Money Measurement Concept: As per this accounting concept it is mandatory for all entities to

record only those transactions that can be measured in terms of money and should record them in

Country’s Currency. For example, company established in Australia will use Australian Dollar to

record all the transactions. It means company cannot record transactions that cannot be expressed

in books of accounts. In case of Spark New Zealand, all the transactions have been shown in

Australian Dollar and there are no transactions that have expressed as non monetary items. The

purpose of this accounting concept is to help the accountants to know what transactions have to

be recorded and what not to record (Needles, Powers and Crosson, 2013).

Going Concern Concept: This concept states that entity will continue forever for an indefinite

time period and it cannot be liquidated unless there is requirement to do so. This concept is most

important accounting concept as it provides the basis for calculating the value of assets and

liabilities. It can be understood from example that total value of purchases of plant and

machinery is being charged as depreciation up to the life of asset not as the expense in first year

itself. Spark New Zealand has followed this accounting concept as it deferred many expenses

and income in form of assets and liabilities in the balance which is a clear indication that

company based its accounting process through using going concern concept (Wahlen, Baginski

and Bradshaw, 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

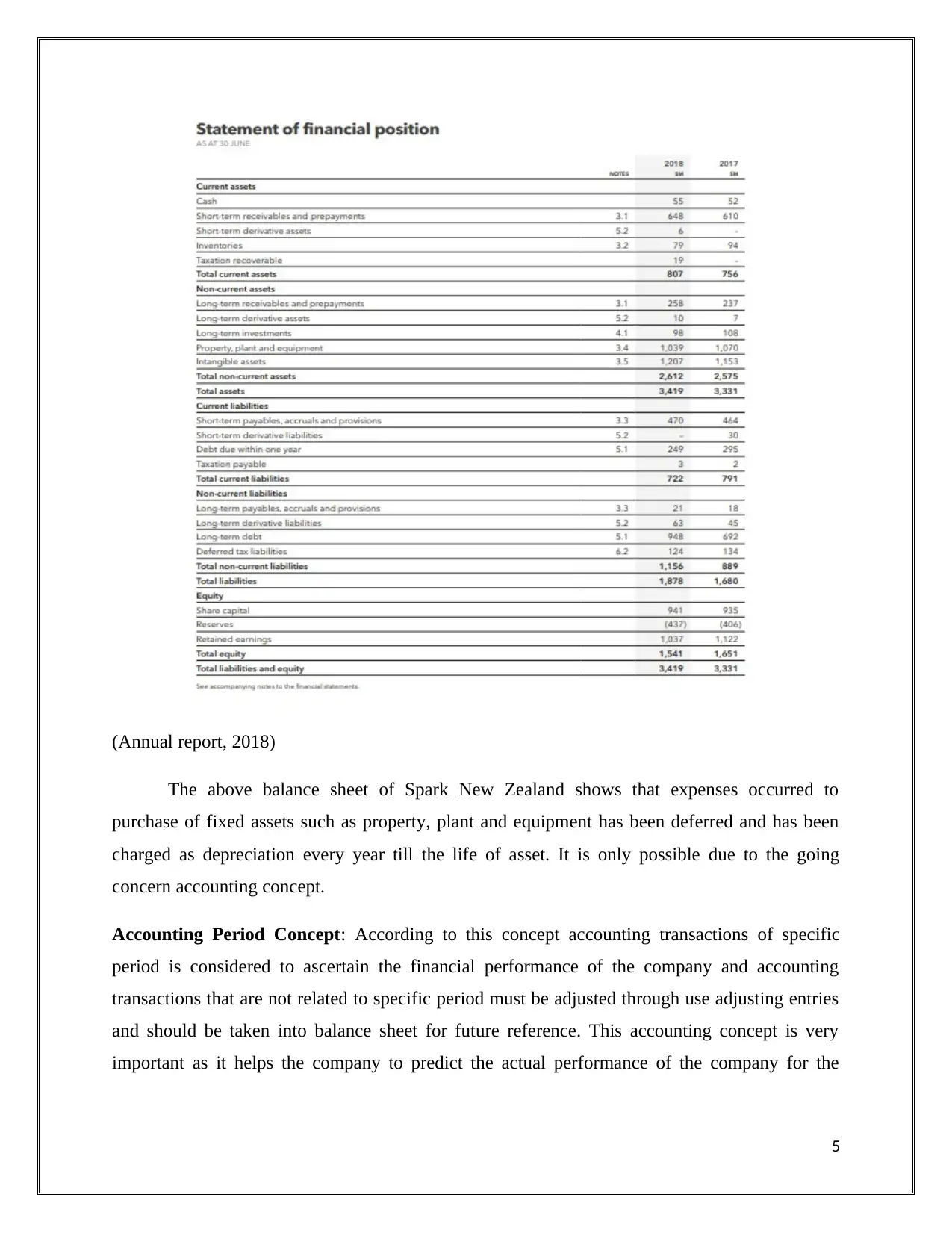

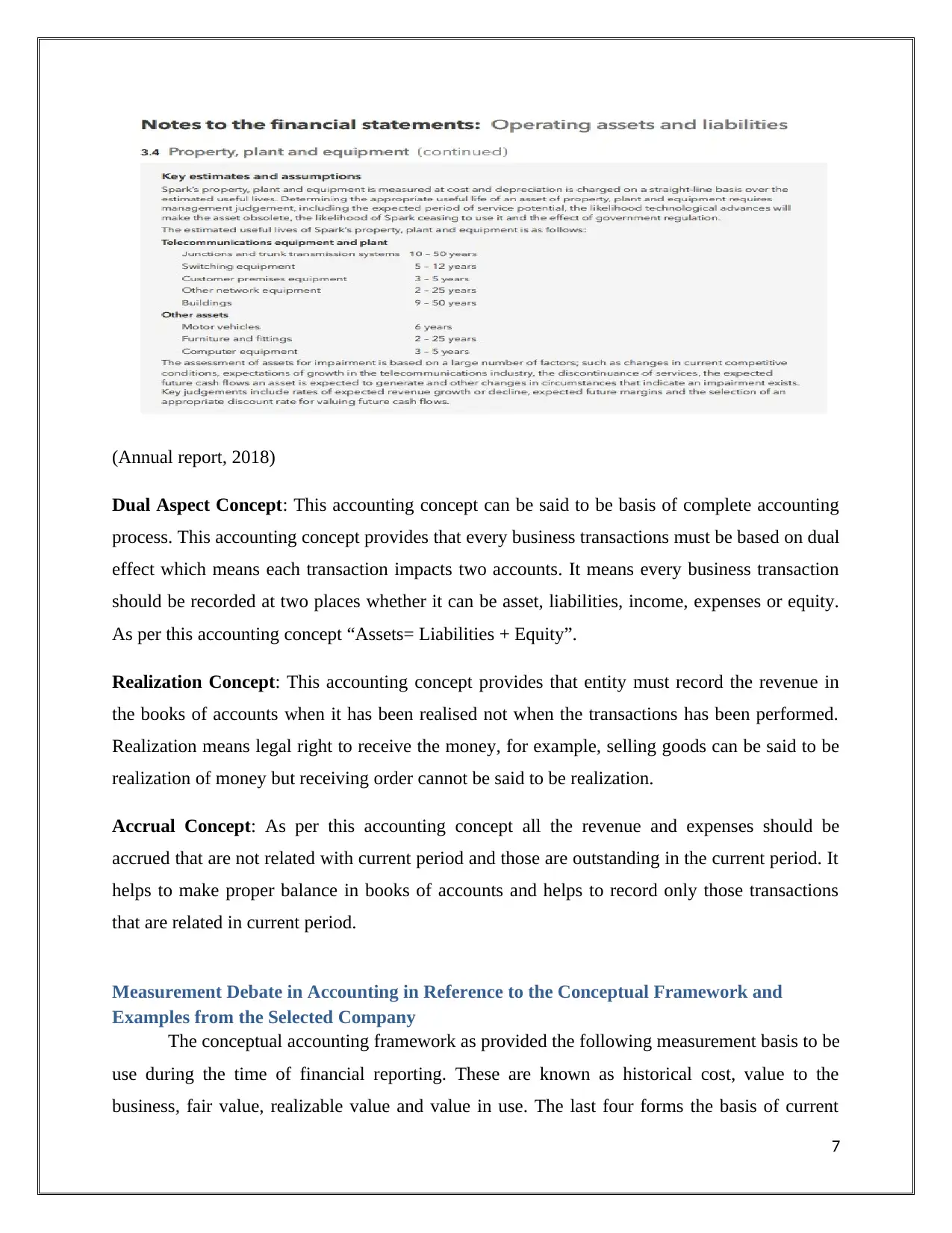

(Annual report, 2018)

The above balance sheet of Spark New Zealand shows that expenses occurred to

purchase of fixed assets such as property, plant and equipment has been deferred and has been

charged as depreciation every year till the life of asset. It is only possible due to the going

concern accounting concept.

Accounting Period Concept: According to this concept accounting transactions of specific

period is considered to ascertain the financial performance of the company and accounting

transactions that are not related to specific period must be adjusted through use adjusting entries

and should be taken into balance sheet for future reference. This accounting concept is very

important as it helps the company to predict the actual performance of the company for the

5

The above balance sheet of Spark New Zealand shows that expenses occurred to

purchase of fixed assets such as property, plant and equipment has been deferred and has been

charged as depreciation every year till the life of asset. It is only possible due to the going

concern accounting concept.

Accounting Period Concept: According to this concept accounting transactions of specific

period is considered to ascertain the financial performance of the company and accounting

transactions that are not related to specific period must be adjusted through use adjusting entries

and should be taken into balance sheet for future reference. This accounting concept is very

important as it helps the company to predict the actual performance of the company for the

5

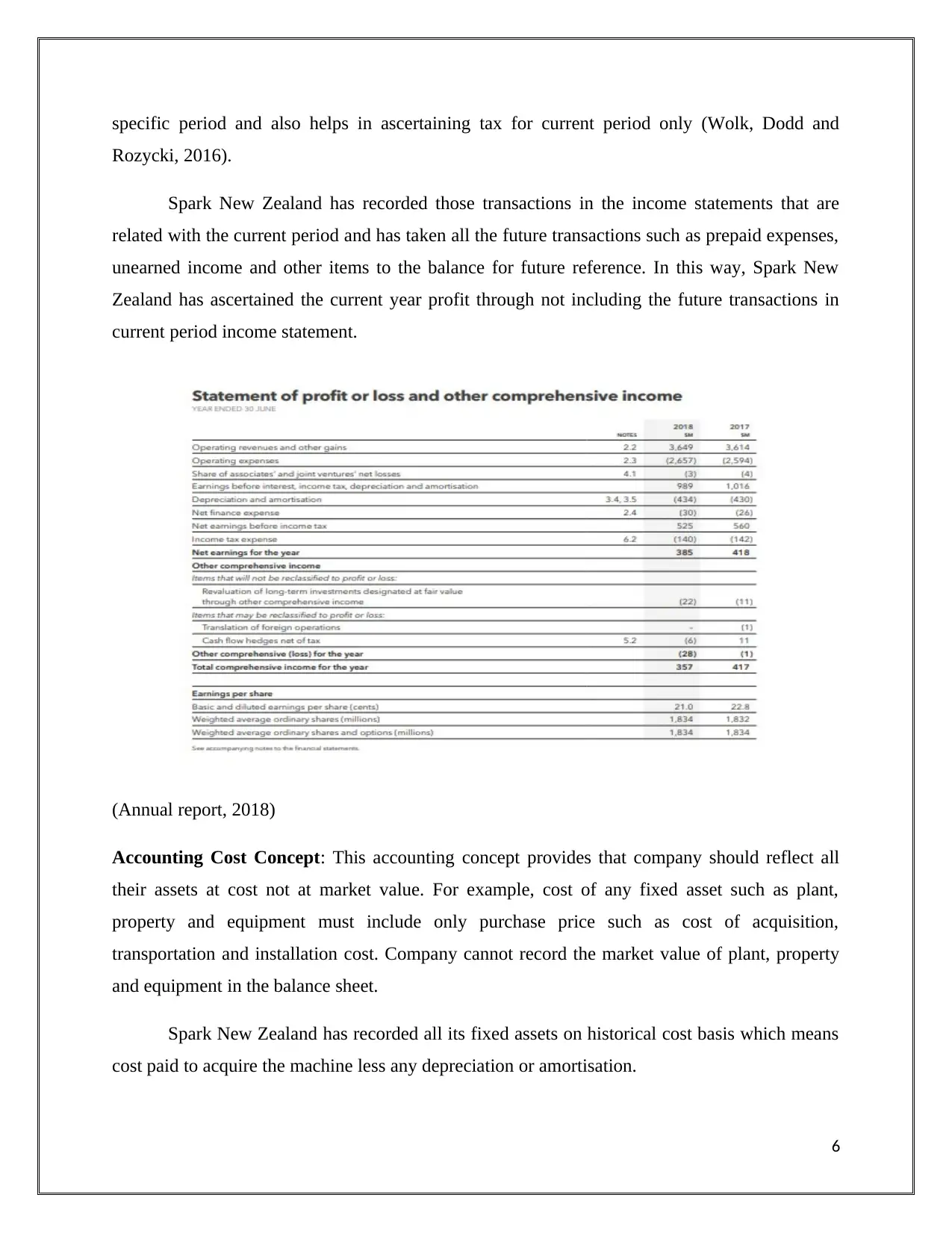

specific period and also helps in ascertaining tax for current period only (Wolk, Dodd and

Rozycki, 2016).

Spark New Zealand has recorded those transactions in the income statements that are

related with the current period and has taken all the future transactions such as prepaid expenses,

unearned income and other items to the balance for future reference. In this way, Spark New

Zealand has ascertained the current year profit through not including the future transactions in

current period income statement.

(Annual report, 2018)

Accounting Cost Concept: This accounting concept provides that company should reflect all

their assets at cost not at market value. For example, cost of any fixed asset such as plant,

property and equipment must include only purchase price such as cost of acquisition,

transportation and installation cost. Company cannot record the market value of plant, property

and equipment in the balance sheet.

Spark New Zealand has recorded all its fixed assets on historical cost basis which means

cost paid to acquire the machine less any depreciation or amortisation.

6

Rozycki, 2016).

Spark New Zealand has recorded those transactions in the income statements that are

related with the current period and has taken all the future transactions such as prepaid expenses,

unearned income and other items to the balance for future reference. In this way, Spark New

Zealand has ascertained the current year profit through not including the future transactions in

current period income statement.

(Annual report, 2018)

Accounting Cost Concept: This accounting concept provides that company should reflect all

their assets at cost not at market value. For example, cost of any fixed asset such as plant,

property and equipment must include only purchase price such as cost of acquisition,

transportation and installation cost. Company cannot record the market value of plant, property

and equipment in the balance sheet.

Spark New Zealand has recorded all its fixed assets on historical cost basis which means

cost paid to acquire the machine less any depreciation or amortisation.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

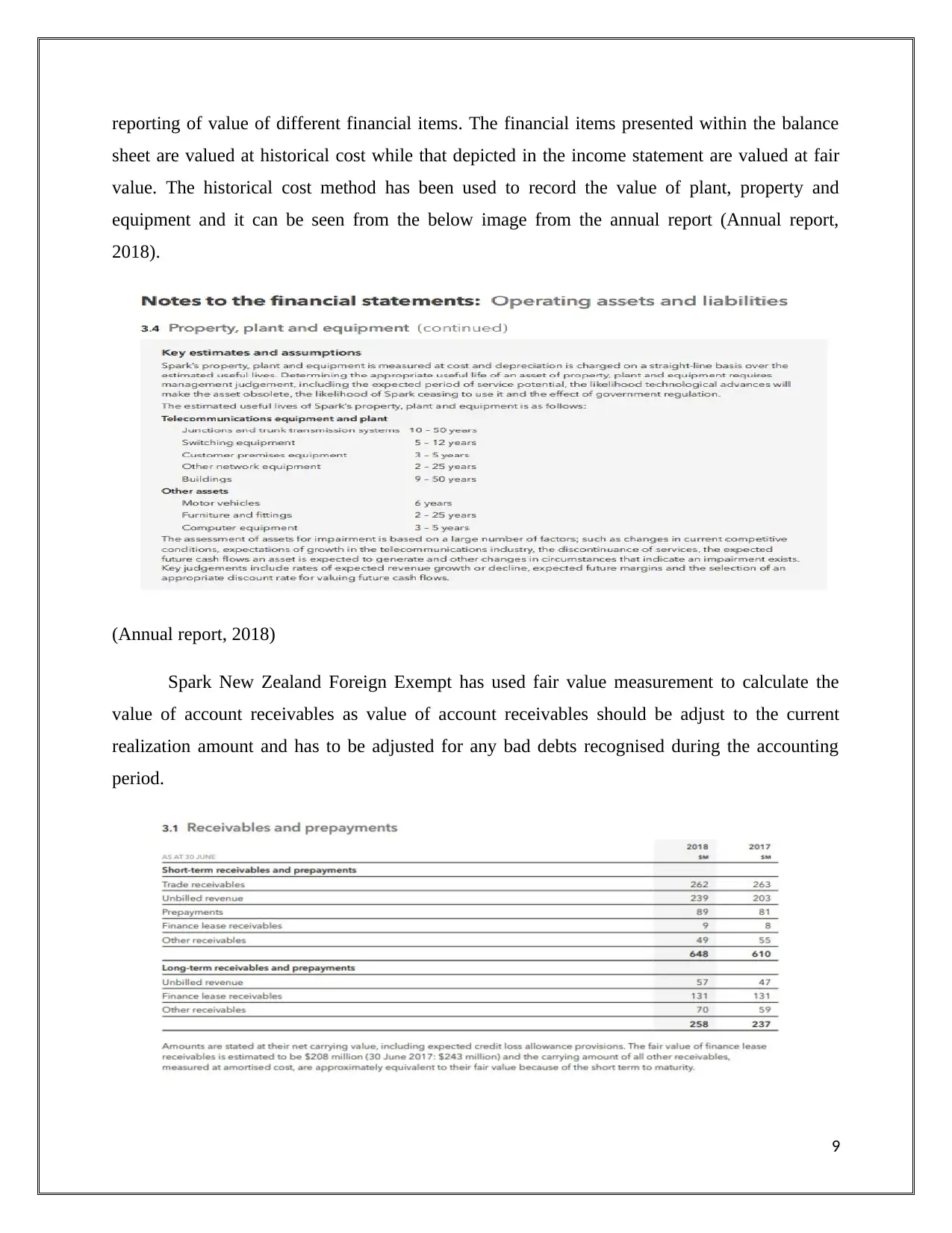

(Annual report, 2018)

Dual Aspect Concept: This accounting concept can be said to be basis of complete accounting

process. This accounting concept provides that every business transactions must be based on dual

effect which means each transaction impacts two accounts. It means every business transaction

should be recorded at two places whether it can be asset, liabilities, income, expenses or equity.

As per this accounting concept “Assets= Liabilities + Equity”.

Realization Concept: This accounting concept provides that entity must record the revenue in

the books of accounts when it has been realised not when the transactions has been performed.

Realization means legal right to receive the money, for example, selling goods can be said to be

realization of money but receiving order cannot be said to be realization.

Accrual Concept: As per this accounting concept all the revenue and expenses should be

accrued that are not related with current period and those are outstanding in the current period. It

helps to make proper balance in books of accounts and helps to record only those transactions

that are related in current period.

Measurement Debate in Accounting in Reference to the Conceptual Framework and

Examples from the Selected Company

The conceptual accounting framework as provided the following measurement basis to be

use during the time of financial reporting. These are known as historical cost, value to the

business, fair value, realizable value and value in use. The last four forms the basis of current

7

Dual Aspect Concept: This accounting concept can be said to be basis of complete accounting

process. This accounting concept provides that every business transactions must be based on dual

effect which means each transaction impacts two accounts. It means every business transaction

should be recorded at two places whether it can be asset, liabilities, income, expenses or equity.

As per this accounting concept “Assets= Liabilities + Equity”.

Realization Concept: This accounting concept provides that entity must record the revenue in

the books of accounts when it has been realised not when the transactions has been performed.

Realization means legal right to receive the money, for example, selling goods can be said to be

realization of money but receiving order cannot be said to be realization.

Accrual Concept: As per this accounting concept all the revenue and expenses should be

accrued that are not related with current period and those are outstanding in the current period. It

helps to make proper balance in books of accounts and helps to record only those transactions

that are related in current period.

Measurement Debate in Accounting in Reference to the Conceptual Framework and

Examples from the Selected Company

The conceptual accounting framework as provided the following measurement basis to be

use during the time of financial reporting. These are known as historical cost, value to the

business, fair value, realizable value and value in use. The last four forms the basis of current

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

value measurement and it along with historical cost method is used generally by the business for

measuring and reporting the value of assets and liabilities (ICAEW, 2016). However, the

measurement issue that is generally faced during financial reporting is use of an adequate

measurement approach that is able to meet the qualitative characteristics of conceptual

framework of relevance and reliability. The different measurement basis provided by the

conceptual framework has varying uses, costs and extent of relevance and reliability for

reporting of assets and liabilities (IFRS, 2017). It is required on the part of business managers to

select adequate measurement approach as per the nature of assets and liabilities (Conceptual

framework — Measurements and elements of financial statements, 2013). However, the major

issue that is present in the selection of an adequate measurement approach that is able to provide

both relevant and reliable financial information for meeting the conceptual accounting

framework principles. The IFRS has provided the use of different basis for measuring different

items within accounts. This results in generating inconsistency between different items of

financial reporting and thus there requires a need for eliminating the inconsistency in the

financial reporting that exists with the use of different method of measurement. The financial

items of balance sheet such as assets and liabilities are measured with the use of different

measurement method while the financial items of income statements are measured with the use

another measurement approach (Filipova, 2016).

The issue of measurement basis is present as there are particular strengths and

weaknesses associated with each measurement approach of accounting that are provided by the

conceptual framework of accounting. For example, fair value method of cost measurement may

seems to be ineffective in the absence of active markets while method of historical costing does

not have significance in valuing certain items such as financial instruments that does not have

any historical cost (Sadowska, 2016). Therefore, the use of a measurement approach can results

in producing significant value for one financial item while may fail to depict the actual value of

others. As such, the business entities tend to use different method of measuring for valuing of

different assets and liabilities and this often results in generating inconsistency in the financial

reporting (International Accounting Standards Board, 2016).

The same has been examined from the analysis of the financial report of Spark New

Zealand Foreign Exempt that has also adopted the use of different measurement basis for

8

measuring and reporting the value of assets and liabilities (ICAEW, 2016). However, the

measurement issue that is generally faced during financial reporting is use of an adequate

measurement approach that is able to meet the qualitative characteristics of conceptual

framework of relevance and reliability. The different measurement basis provided by the

conceptual framework has varying uses, costs and extent of relevance and reliability for

reporting of assets and liabilities (IFRS, 2017). It is required on the part of business managers to

select adequate measurement approach as per the nature of assets and liabilities (Conceptual

framework — Measurements and elements of financial statements, 2013). However, the major

issue that is present in the selection of an adequate measurement approach that is able to provide

both relevant and reliable financial information for meeting the conceptual accounting

framework principles. The IFRS has provided the use of different basis for measuring different

items within accounts. This results in generating inconsistency between different items of

financial reporting and thus there requires a need for eliminating the inconsistency in the

financial reporting that exists with the use of different method of measurement. The financial

items of balance sheet such as assets and liabilities are measured with the use of different

measurement method while the financial items of income statements are measured with the use

another measurement approach (Filipova, 2016).

The issue of measurement basis is present as there are particular strengths and

weaknesses associated with each measurement approach of accounting that are provided by the

conceptual framework of accounting. For example, fair value method of cost measurement may

seems to be ineffective in the absence of active markets while method of historical costing does

not have significance in valuing certain items such as financial instruments that does not have

any historical cost (Sadowska, 2016). Therefore, the use of a measurement approach can results

in producing significant value for one financial item while may fail to depict the actual value of

others. As such, the business entities tend to use different method of measuring for valuing of

different assets and liabilities and this often results in generating inconsistency in the financial

reporting (International Accounting Standards Board, 2016).

The same has been examined from the analysis of the financial report of Spark New

Zealand Foreign Exempt that has also adopted the use of different measurement basis for

8

reporting of value of different financial items. The financial items presented within the balance

sheet are valued at historical cost while that depicted in the income statement are valued at fair

value. The historical cost method has been used to record the value of plant, property and

equipment and it can be seen from the below image from the annual report (Annual report,

2018).

(Annual report, 2018)

Spark New Zealand Foreign Exempt has used fair value measurement to calculate the

value of account receivables as value of account receivables should be adjust to the current

realization amount and has to be adjusted for any bad debts recognised during the accounting

period.

9

sheet are valued at historical cost while that depicted in the income statement are valued at fair

value. The historical cost method has been used to record the value of plant, property and

equipment and it can be seen from the below image from the annual report (Annual report,

2018).

(Annual report, 2018)

Spark New Zealand Foreign Exempt has used fair value measurement to calculate the

value of account receivables as value of account receivables should be adjust to the current

realization amount and has to be adjusted for any bad debts recognised during the accounting

period.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Annual report, 2018)

Understanding of Relevance and Representational Faithfulness of Conceptual Accounting

Framework

The conceptual framework of accounting has stated the two major qualitative

characteristics that must be used by business entities during the development of their financial

reports. These two characteristics are relevancy and faithful representation of information. The

relevance characteristics have required that the financial information need to be capable of

making a difference in the decision-making of the users such as investors, creditors and others.

This requires them to make predictions about the past, present and future outcome events of an

entity (Grüber, 2014). As such, it needs to be predictive that is able to predict the future cash

generation capability of a business entity also a feedback value which regards providing value

about the past and present activities of an entity to provide confirmatory value for taking

decisions. On the other hand, the faithful representation of information depicts that the

information must be materialistically correct, free from any error and must also be verifiable by

independent observers such as auditors (Hopwood, 2013). These two qualitative characteristics

need to be adopted by the business entities at the time of financial reporting for developing high

quality financial reports (Ashford, 2011).

However, there exists a tradeoff between relevance and reliability as giving importance

on one aspect during financial reporting may result in negatively influencing its other aspect.

This is because both are important to be applied for generating high quality financial outcomes

and therefore it requires developing a trade-off between them so that emphasis placed on one

does not negatively impact the other (Dye and Sridhar, 2010). For example, under the use of

accrual method the sales that are done on credit are recognized as revenue and thus making the

financial reports more relevant while it will impact the financial reports less reliable as it fails to

depict the actual value of an entity to the end-users (Gassen and Schwedler, 2010).

Similarly, under the method of reserve recognition accounting, the business entities

recognizes the present value of proven reserves in the net income and thus the information can be

regarded as more relevant. On the other hand, the fluctuations in the future value of proven new

reserve due to volatility in the market may impact their current value and thus making the

10

Understanding of Relevance and Representational Faithfulness of Conceptual Accounting

Framework

The conceptual framework of accounting has stated the two major qualitative

characteristics that must be used by business entities during the development of their financial

reports. These two characteristics are relevancy and faithful representation of information. The

relevance characteristics have required that the financial information need to be capable of

making a difference in the decision-making of the users such as investors, creditors and others.

This requires them to make predictions about the past, present and future outcome events of an

entity (Grüber, 2014). As such, it needs to be predictive that is able to predict the future cash

generation capability of a business entity also a feedback value which regards providing value

about the past and present activities of an entity to provide confirmatory value for taking

decisions. On the other hand, the faithful representation of information depicts that the

information must be materialistically correct, free from any error and must also be verifiable by

independent observers such as auditors (Hopwood, 2013). These two qualitative characteristics

need to be adopted by the business entities at the time of financial reporting for developing high

quality financial reports (Ashford, 2011).

However, there exists a tradeoff between relevance and reliability as giving importance

on one aspect during financial reporting may result in negatively influencing its other aspect.

This is because both are important to be applied for generating high quality financial outcomes

and therefore it requires developing a trade-off between them so that emphasis placed on one

does not negatively impact the other (Dye and Sridhar, 2010). For example, under the use of

accrual method the sales that are done on credit are recognized as revenue and thus making the

financial reports more relevant while it will impact the financial reports less reliable as it fails to

depict the actual value of an entity to the end-users (Gassen and Schwedler, 2010).

Similarly, under the method of reserve recognition accounting, the business entities

recognizes the present value of proven reserves in the net income and thus the information can be

regarded as more relevant. On the other hand, the fluctuations in the future value of proven new

reserve due to volatility in the market may impact their current value and thus making the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information less reliable (Conceptual Framework for Financial Reporting, 2018). The business

entities also tend to adopt the use of different measurement basis in recognition of their assets

and liabilities to achieve a trade-off between relevance and reliability. The historical method of

costing used in measurement of assets and liabilities may result in making the financial

information more reliable while fair value that helps in assessing the future financial position of

an entity helps in making the financial statements more relevant (Albrech, Stice and Stice, 2010).

The investors emphasizes on relevance in forecasting the future financial position of an

entity while auditors during reviewing the materialistic correctness of the financial information

emphasis on reliability. Thus, investors prefer that financial statements are developed with the

use of fair value while auditors place more emphasis on historical costs to be used for

development of the financial statements (Burlaud, 2013). The business entities are placing large

emphasis on improving the relevancy of the financial reporting to meet the needs and

expectations of the investors. As such, businesses are developing their financial statements more

on the basis of fair value but it does not mean ignoring the reliability, Therefore, they tend to

adopt a trade-off between the two qualitative principles of the conceptual accounting framework

and use measurement approach at fair value for financial items that requires more relevance and

other at historical cost that requires more reliability (Bellandi, 2017).

The same can be depicted form analyzing the annual report of Spark New Zealand Foreign

Exempt which has adopted the use of both historical and fair value methods to develop its

financial reports. The use of historical basis is done for reporting the value of fixed assets that

requires more reliability while operating expenses and revenue and financial instruments are

valued at fair value that are requires to depict more relevant information. The items of income

statements need to depict the future performance of an entity and therefore required to be

developed with the use of fair value as analyzed from Spark New Zealand Foreign Exempt. On

the other hand, the balance sheets are developed with the use of historical method of financial

reporting as they tend depict the reliable value to used by prepares for assessing the materiality

correctness of the financial information (Annual report, 2018)

11

entities also tend to adopt the use of different measurement basis in recognition of their assets

and liabilities to achieve a trade-off between relevance and reliability. The historical method of

costing used in measurement of assets and liabilities may result in making the financial

information more reliable while fair value that helps in assessing the future financial position of

an entity helps in making the financial statements more relevant (Albrech, Stice and Stice, 2010).

The investors emphasizes on relevance in forecasting the future financial position of an

entity while auditors during reviewing the materialistic correctness of the financial information

emphasis on reliability. Thus, investors prefer that financial statements are developed with the

use of fair value while auditors place more emphasis on historical costs to be used for

development of the financial statements (Burlaud, 2013). The business entities are placing large

emphasis on improving the relevancy of the financial reporting to meet the needs and

expectations of the investors. As such, businesses are developing their financial statements more

on the basis of fair value but it does not mean ignoring the reliability, Therefore, they tend to

adopt a trade-off between the two qualitative principles of the conceptual accounting framework

and use measurement approach at fair value for financial items that requires more relevance and

other at historical cost that requires more reliability (Bellandi, 2017).

The same can be depicted form analyzing the annual report of Spark New Zealand Foreign

Exempt which has adopted the use of both historical and fair value methods to develop its

financial reports. The use of historical basis is done for reporting the value of fixed assets that

requires more reliability while operating expenses and revenue and financial instruments are

valued at fair value that are requires to depict more relevant information. The items of income

statements need to depict the future performance of an entity and therefore required to be

developed with the use of fair value as analyzed from Spark New Zealand Foreign Exempt. On

the other hand, the balance sheets are developed with the use of historical method of financial

reporting as they tend depict the reliable value to used by prepares for assessing the materiality

correctness of the financial information (Annual report, 2018)

11

Conclusion

The above report has inferred that the conceptual accounting framework of reporting is

very important to be used by the business entities for development of their financial reports. The

accounting framework provides relevance and representational faithfulness as the major principle

of financial reporting. However, it requires a trade-off to be developed between the two for

meeting the objective of financial reports development.

12

The above report has inferred that the conceptual accounting framework of reporting is

very important to be used by the business entities for development of their financial reports. The

accounting framework provides relevance and representational faithfulness as the major principle

of financial reporting. However, it requires a trade-off to be developed between the two for

meeting the objective of financial reports development.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.