Financial Accounting Assignment: Stakeholders and Ratio Analysis

VerifiedAdded on 2022/10/11

|10

|1732

|11

Homework Assignment

AI Summary

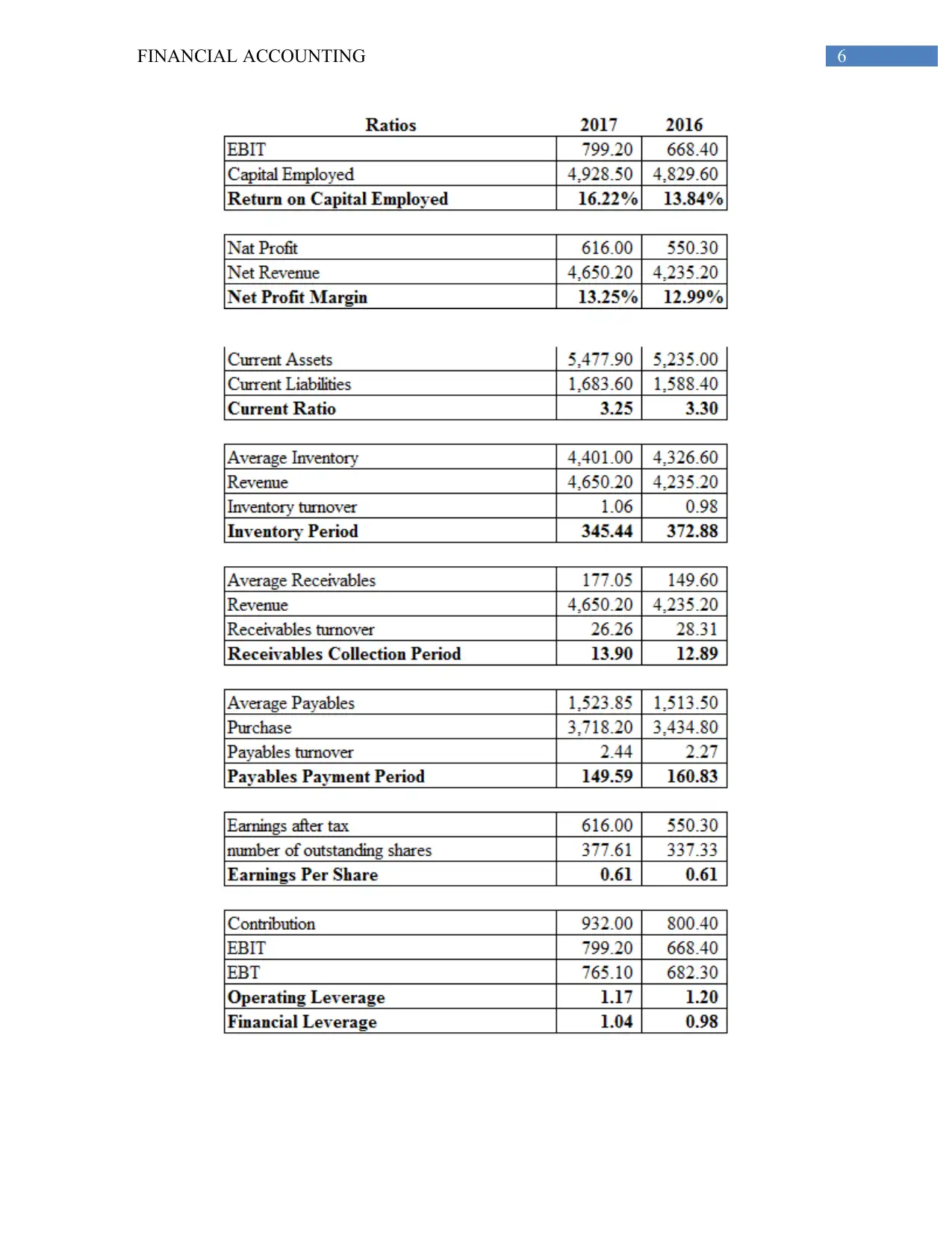

This financial accounting assignment analyzes financial statements and the information needs of various stakeholders. The assignment begins by identifying the key stakeholders, including managers, investors, lenders, employees, suppliers, customers, governments, and the public, and explains their specific requirements from financial statements. It then examines the sources of financial information, focusing on the income statement and the balance sheet, and highlights the importance of sustainability reports. The second part of the assignment performs a comparative financial statement analysis using Barratt Developments, calculating and interpreting profitability, efficiency, and capital structure ratios for 2016 and 2017. The analysis identifies strengths and weaknesses in the company's financial performance based on the calculated ratios, such as gross profit margin, net profit margin, current ratio, inventory period, receivable collection period, and payable payment period, providing insights into the company's financial health and management efficiency. The document concludes with a list of references and bibliography of resources used for the assignment.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.