Financial Accounting Report: Stakeholders, Statements, and Entries

VerifiedAdded on 2021/02/20

|30

|4643

|34

Report

AI Summary

This financial accounting report provides a detailed analysis of the subject, starting with an introduction to the meaning and purpose of financial accounting (FA), along with a comparison between financial and management accounting. It identifies internal and external stakeholders and examines journal entries, trial balances, income statements, and balance sheets for different clients. The report also covers key accounting concepts like consistency and prudence, the purpose of depreciation, and differences between sole trader and limited company financial statements. Further topics include bank reconciliation statements, petty cash systems, sales and purchase ledgers, control accounts, suspense accounts, error rectification, and a final trial balance. The report concludes with a comprehensive overview of the subject matter, providing a thorough understanding of financial accounting principles and practices.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

a. Explaining the meaning and the purpose of financial accounting...........................................2

Difference in between financial accounting and management accounting ................................3

b. Two internal stakeholder and four external stakeholders important in the organisation. ......4

Client 1.............................................................................................................................................6

I. Recording and classification of the journal entries..................................................................6

........................................................................................................................................................11

........................................................................................................................................................12

ii. Preparation of the trial balance.............................................................................................15

Client 2...........................................................................................................................................16

a. Preparation of the income statement.....................................................................................16

b. Statement of balance sheet....................................................................................................17

c. Explaining the consistency and the prudence concept..........................................................18

d. Describing purpose of the depreciation and its methods .....................................................18

e. Evaluating the difference in between the financial statements of the sole trader and the

limited companies.....................................................................................................................19

Client 3...........................................................................................................................................19

a. Explaining the meaning and the purpose of the bank reconciliation statement ...................19

b. Listing down the areas where bank records can vary from the cash statement....................20

c. Explaining the imprest under the system of petty cash.........................................................20

d. Preparation of bank reconciliation statement........................................................................21

Client 4...........................................................................................................................................22

a. Preparing sales and the purchase ledger account..................................................................22

...................................................................................................................................................22

b. Explaining the meaning of the control account.....................................................................22

Client 5...........................................................................................................................................23

a. Explaining the meaning of suspense account and its features...............................................23

b. Drafting a trial balance .........................................................................................................23

INTRODUCTION...........................................................................................................................1

a. Explaining the meaning and the purpose of financial accounting...........................................2

Difference in between financial accounting and management accounting ................................3

b. Two internal stakeholder and four external stakeholders important in the organisation. ......4

Client 1.............................................................................................................................................6

I. Recording and classification of the journal entries..................................................................6

........................................................................................................................................................11

........................................................................................................................................................12

ii. Preparation of the trial balance.............................................................................................15

Client 2...........................................................................................................................................16

a. Preparation of the income statement.....................................................................................16

b. Statement of balance sheet....................................................................................................17

c. Explaining the consistency and the prudence concept..........................................................18

d. Describing purpose of the depreciation and its methods .....................................................18

e. Evaluating the difference in between the financial statements of the sole trader and the

limited companies.....................................................................................................................19

Client 3...........................................................................................................................................19

a. Explaining the meaning and the purpose of the bank reconciliation statement ...................19

b. Listing down the areas where bank records can vary from the cash statement....................20

c. Explaining the imprest under the system of petty cash.........................................................20

d. Preparation of bank reconciliation statement........................................................................21

Client 4...........................................................................................................................................22

a. Preparing sales and the purchase ledger account..................................................................22

...................................................................................................................................................22

b. Explaining the meaning of the control account.....................................................................22

Client 5...........................................................................................................................................23

a. Explaining the meaning of suspense account and its features...............................................23

b. Drafting a trial balance .........................................................................................................23

c. Rectification of errors ...........................................................................................................24

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

FA is a process which is used by company to keep a day to day record of company financial

activities. In this transaction are recorded, summarized and stipulated to examined the stability of

the company and also enhances the position to take risk in the business for some new projects

(Schaltegger and Burritt, 2017). The main purpose to prepared financial accounting is that to

helps company to take effective decision and also prepare the financial report which is to be

presented at the time when it is demanded by the stakeholders. Usually the financial statement

reflect the income and expenditure of an enterprise to maintain the b/s of the company in

summarized way. To prepared the financial accounting proper department is established to

analyse their financial transaction and also prepare their financial report and present them in

effective manner.

This report will incudes the meaning of FA and analysis of all the stakeholders within

the company. It includes the formulation of final accounts in respect of proprietors, partnership

and the limited liability organizations in context of its various principles, convention and

standards. It further includes the descriptive of bank reconciliation statement which ensure the

company and bank records. The report concludes with the matter to reconcile accounts which is

to be shifted in recorded transaction to establish the right accounts in the company.

1

FA is a process which is used by company to keep a day to day record of company financial

activities. In this transaction are recorded, summarized and stipulated to examined the stability of

the company and also enhances the position to take risk in the business for some new projects

(Schaltegger and Burritt, 2017). The main purpose to prepared financial accounting is that to

helps company to take effective decision and also prepare the financial report which is to be

presented at the time when it is demanded by the stakeholders. Usually the financial statement

reflect the income and expenditure of an enterprise to maintain the b/s of the company in

summarized way. To prepared the financial accounting proper department is established to

analyse their financial transaction and also prepare their financial report and present them in

effective manner.

This report will incudes the meaning of FA and analysis of all the stakeholders within

the company. It includes the formulation of final accounts in respect of proprietors, partnership

and the limited liability organizations in context of its various principles, convention and

standards. It further includes the descriptive of bank reconciliation statement which ensure the

company and bank records. The report concludes with the matter to reconcile accounts which is

to be shifted in recorded transaction to establish the right accounts in the company.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting

It is the main branch categorised as of accounting in which, financial accounting assists

traces the financial transactions of a company. There are standard guidelines which are used in

recording, presenting and summarizing in a financial report which includes balance sheet or

income statements (Männasoo, Maripuu and Hazak, 2018). This accounting serves for interest of

stakeholders, owners, creditors, etc. Companies generally issue financial statements on a daily

basis for providing regular data and other related information to the interested people.

The standard format of financial accounting relates to double entry book keeping in

which the transaction are recorded under credit and debit side. Along with it, the accrual basis of

account concept is followed under financial accounting. This concept represents that the revenue

are recorded only when it has earned even amount is not received. The financial accounting

reports is prepared under the guidelines of GAAP. The financial reports comprise income

statements, cash flow & retained earning statements. These statements are framed under GAAP

and IFRS guidelines.

a. Explaining the meaning and the purpose of financial accounting

Purpose of financial accounting

Provide information to interested individuals - The main purpose for which financial

accounting is prepared under business is to gather financial report and offer important and

relevant information about the action taken by the firm to parties like creditors, taxation

authority, investors, etc. Also, these reports of financial accounting is helpful to ascertain cash

flows within a business (Persson, Radcliffe, and Stein, 2018.). The reports are prepared for the

purpose of providing guidelines for future investment for reaching to decision making and

increase the profitability of a business organisation.

Determining cash flows for future investments - It is the main purpose of financial

accounting for assisting the detail of cash flows under which cash inflows and cash outflows are

determined. Every statements of financial accounting is different from each other and contain

different information as well in relation to business operations. The purpose satisfies by

developing financial reports for the use of critical business decisions by owners or stock holders

of a company.

Act as an evidence in case of dispute - It is also prepared for the purpose for the use of

an evidence in which these records are taken as legal evidence in case of any dispute arises in the

It is the main branch categorised as of accounting in which, financial accounting assists

traces the financial transactions of a company. There are standard guidelines which are used in

recording, presenting and summarizing in a financial report which includes balance sheet or

income statements (Männasoo, Maripuu and Hazak, 2018). This accounting serves for interest of

stakeholders, owners, creditors, etc. Companies generally issue financial statements on a daily

basis for providing regular data and other related information to the interested people.

The standard format of financial accounting relates to double entry book keeping in

which the transaction are recorded under credit and debit side. Along with it, the accrual basis of

account concept is followed under financial accounting. This concept represents that the revenue

are recorded only when it has earned even amount is not received. The financial accounting

reports is prepared under the guidelines of GAAP. The financial reports comprise income

statements, cash flow & retained earning statements. These statements are framed under GAAP

and IFRS guidelines.

a. Explaining the meaning and the purpose of financial accounting

Purpose of financial accounting

Provide information to interested individuals - The main purpose for which financial

accounting is prepared under business is to gather financial report and offer important and

relevant information about the action taken by the firm to parties like creditors, taxation

authority, investors, etc. Also, these reports of financial accounting is helpful to ascertain cash

flows within a business (Persson, Radcliffe, and Stein, 2018.). The reports are prepared for the

purpose of providing guidelines for future investment for reaching to decision making and

increase the profitability of a business organisation.

Determining cash flows for future investments - It is the main purpose of financial

accounting for assisting the detail of cash flows under which cash inflows and cash outflows are

determined. Every statements of financial accounting is different from each other and contain

different information as well in relation to business operations. The purpose satisfies by

developing financial reports for the use of critical business decisions by owners or stock holders

of a company.

Act as an evidence in case of dispute - It is also prepared for the purpose for the use of

an evidence in which these records are taken as legal evidence in case of any dispute arises in the

company (Coyne, Coyne and Walker, 2018). Along with it, this also lay an appropriate financial

information which can facilitate company to avail facility of credit from lenders as good

financial records create goodwill of the company among creditors.

Profit comparison for determining actual position - At last, the financial statements are

developed for the purpose of comparison of profit which are well analysed by the maintained

records of current year with the previous year. This company is able to measure their

performance from the past year statements with that of current year statements. Theses figures

enables the company in ascertaining their positions.

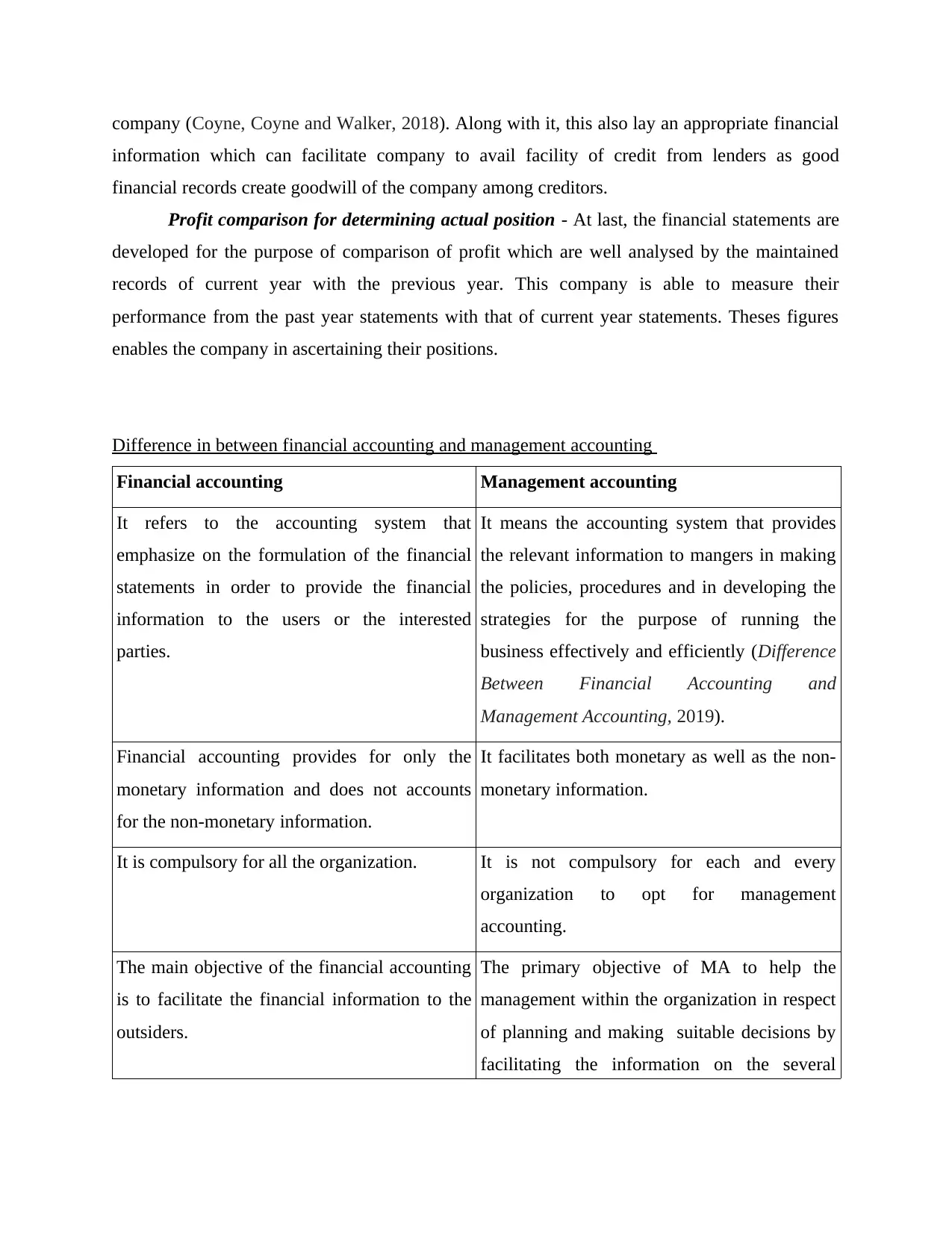

Difference in between financial accounting and management accounting

Financial accounting Management accounting

It refers to the accounting system that

emphasize on the formulation of the financial

statements in order to provide the financial

information to the users or the interested

parties.

It means the accounting system that provides

the relevant information to mangers in making

the policies, procedures and in developing the

strategies for the purpose of running the

business effectively and efficiently (Difference

Between Financial Accounting and

Management Accounting, 2019).

Financial accounting provides for only the

monetary information and does not accounts

for the non-monetary information.

It facilitates both monetary as well as the non-

monetary information.

It is compulsory for all the organization. It is not compulsory for each and every

organization to opt for management

accounting.

The main objective of the financial accounting

is to facilitate the financial information to the

outsiders.

The primary objective of MA to help the

management within the organization in respect

of planning and making suitable decisions by

facilitating the information on the several

information which can facilitate company to avail facility of credit from lenders as good

financial records create goodwill of the company among creditors.

Profit comparison for determining actual position - At last, the financial statements are

developed for the purpose of comparison of profit which are well analysed by the maintained

records of current year with the previous year. This company is able to measure their

performance from the past year statements with that of current year statements. Theses figures

enables the company in ascertaining their positions.

Difference in between financial accounting and management accounting

Financial accounting Management accounting

It refers to the accounting system that

emphasize on the formulation of the financial

statements in order to provide the financial

information to the users or the interested

parties.

It means the accounting system that provides

the relevant information to mangers in making

the policies, procedures and in developing the

strategies for the purpose of running the

business effectively and efficiently (Difference

Between Financial Accounting and

Management Accounting, 2019).

Financial accounting provides for only the

monetary information and does not accounts

for the non-monetary information.

It facilitates both monetary as well as the non-

monetary information.

It is compulsory for all the organization. It is not compulsory for each and every

organization to opt for management

accounting.

The main objective of the financial accounting

is to facilitate the financial information to the

outsiders.

The primary objective of MA to help the

management within the organization in respect

of planning and making suitable decisions by

facilitating the information on the several

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

matters.

Format of the financial accounting is been

specified by the appropriate authorities that is

IFRS and GAAP.

There is no any specified format under the

management accounting.

Under financial accounting, the financial

reports are been framed at year end of an

accounting period that is one year.

Under the MA, reports relating to the

management are been prepared according to

the requirements of an enterprise.

Main users of the FA are the internal and an

external users such as investors, creditors,

mangers, employees, government etc.

Internal management is considered as the main

user under the management accounting.

Financial accounting summarizes the reports

by stating the financial position of an entity.

However, management accounting provides for

the complete and the detailed report in relation

to the various information.

The final reports under the financial

accounting needed to be published and requires

the auditing by the statutory auditors.

The management reports formulated under the

management accounting neither required to be

published nor needed to be audited by the

statutory auditors.

b. Two internal stakeholder and four external stakeholders important in the organisation.

Internal stakeholders refers to such person who manages the company internal affairs are

also responsible to carry various activities (Pijper, 2016). External stakeholders are important ass

due to their inspection in company it reflects the stability of the company and also they manage

the company affairs effectively.

Internal stakeholders Employees - They Handel the internal working

of the company and also enhanced the stability

in the market at large scale (Duff, 2018). They

are important as due to their dedication and

work experiences they increase the sale in the

company.

Format of the financial accounting is been

specified by the appropriate authorities that is

IFRS and GAAP.

There is no any specified format under the

management accounting.

Under financial accounting, the financial

reports are been framed at year end of an

accounting period that is one year.

Under the MA, reports relating to the

management are been prepared according to

the requirements of an enterprise.

Main users of the FA are the internal and an

external users such as investors, creditors,

mangers, employees, government etc.

Internal management is considered as the main

user under the management accounting.

Financial accounting summarizes the reports

by stating the financial position of an entity.

However, management accounting provides for

the complete and the detailed report in relation

to the various information.

The final reports under the financial

accounting needed to be published and requires

the auditing by the statutory auditors.

The management reports formulated under the

management accounting neither required to be

published nor needed to be audited by the

statutory auditors.

b. Two internal stakeholder and four external stakeholders important in the organisation.

Internal stakeholders refers to such person who manages the company internal affairs are

also responsible to carry various activities (Pijper, 2016). External stakeholders are important ass

due to their inspection in company it reflects the stability of the company and also they manage

the company affairs effectively.

Internal stakeholders Employees - They Handel the internal working

of the company and also enhanced the stability

in the market at large scale (Duff, 2018). They

are important as due to their dedication and

work experiences they increase the sale in the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

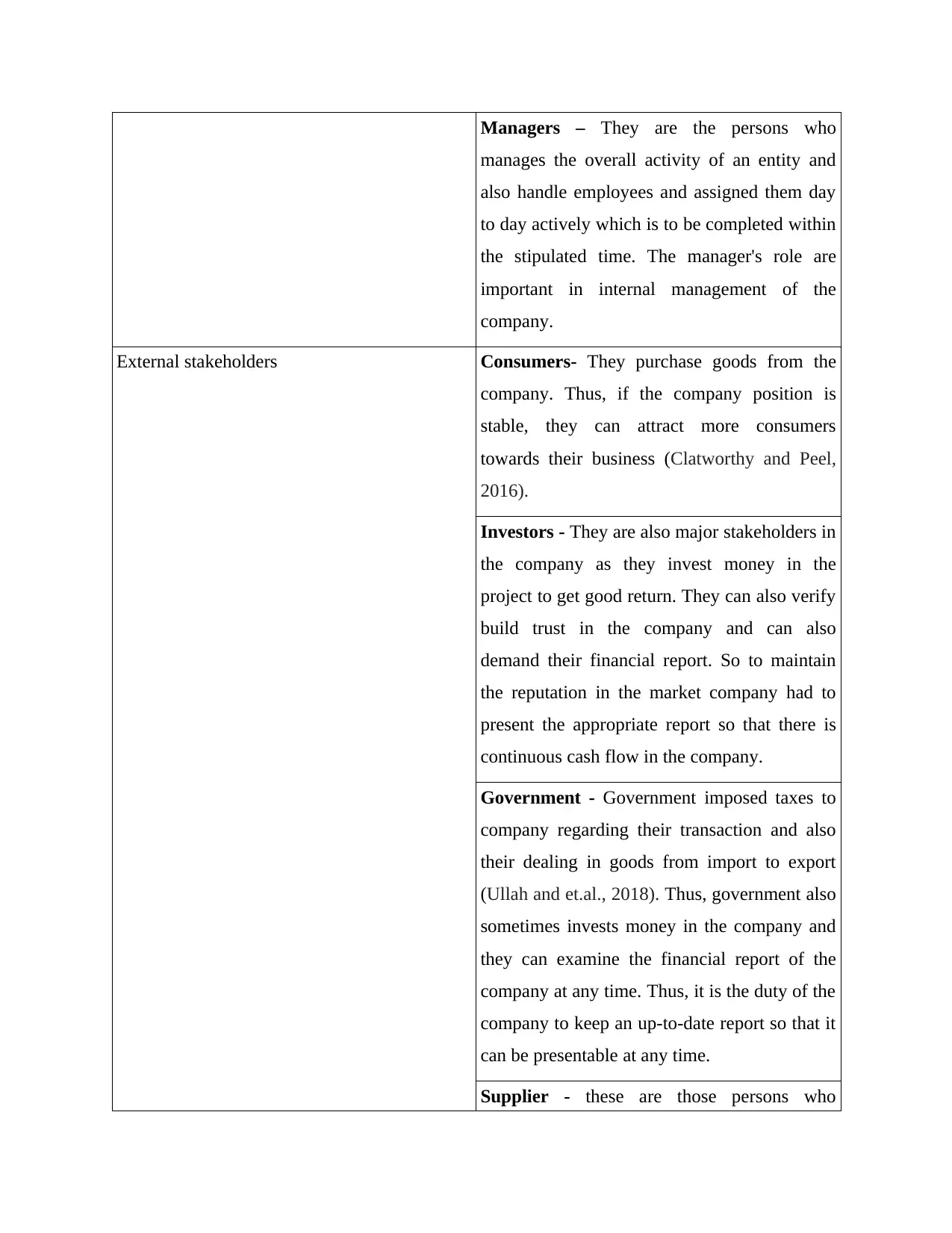

Managers – They are the persons who

manages the overall activity of an entity and

also handle employees and assigned them day

to day actively which is to be completed within

the stipulated time. The manager's role are

important in internal management of the

company.

External stakeholders Consumers- They purchase goods from the

company. Thus, if the company position is

stable, they can attract more consumers

towards their business (Clatworthy and Peel,

2016).

Investors - They are also major stakeholders in

the company as they invest money in the

project to get good return. They can also verify

build trust in the company and can also

demand their financial report. So to maintain

the reputation in the market company had to

present the appropriate report so that there is

continuous cash flow in the company.

Government - Government imposed taxes to

company regarding their transaction and also

their dealing in goods from import to export

(Ullah and et.al., 2018). Thus, government also

sometimes invests money in the company and

they can examine the financial report of the

company at any time. Thus, it is the duty of the

company to keep an up-to-date report so that it

can be presentable at any time.

Supplier - these are those persons who

manages the overall activity of an entity and

also handle employees and assigned them day

to day actively which is to be completed within

the stipulated time. The manager's role are

important in internal management of the

company.

External stakeholders Consumers- They purchase goods from the

company. Thus, if the company position is

stable, they can attract more consumers

towards their business (Clatworthy and Peel,

2016).

Investors - They are also major stakeholders in

the company as they invest money in the

project to get good return. They can also verify

build trust in the company and can also

demand their financial report. So to maintain

the reputation in the market company had to

present the appropriate report so that there is

continuous cash flow in the company.

Government - Government imposed taxes to

company regarding their transaction and also

their dealing in goods from import to export

(Ullah and et.al., 2018). Thus, government also

sometimes invests money in the company and

they can examine the financial report of the

company at any time. Thus, it is the duty of the

company to keep an up-to-date report so that it

can be presentable at any time.

Supplier - these are those persons who

supplies goods to the company and also they

are important. As company manage their

transaction by viewing the supply of raw

material and resources in the company. Thus,

supplier provides finished goods to company at

bargain rates if company had good terms with

them (Weetman, 2019).

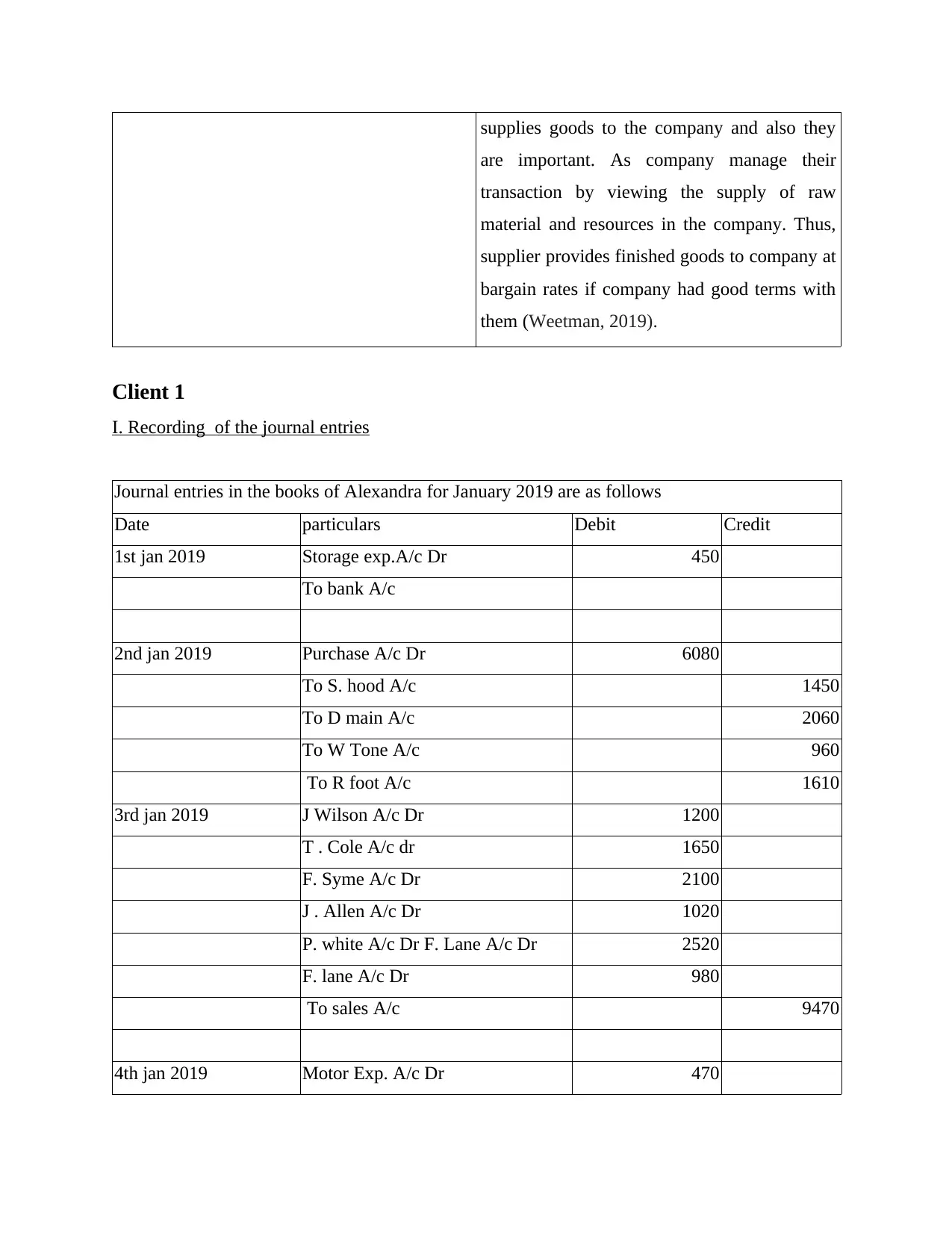

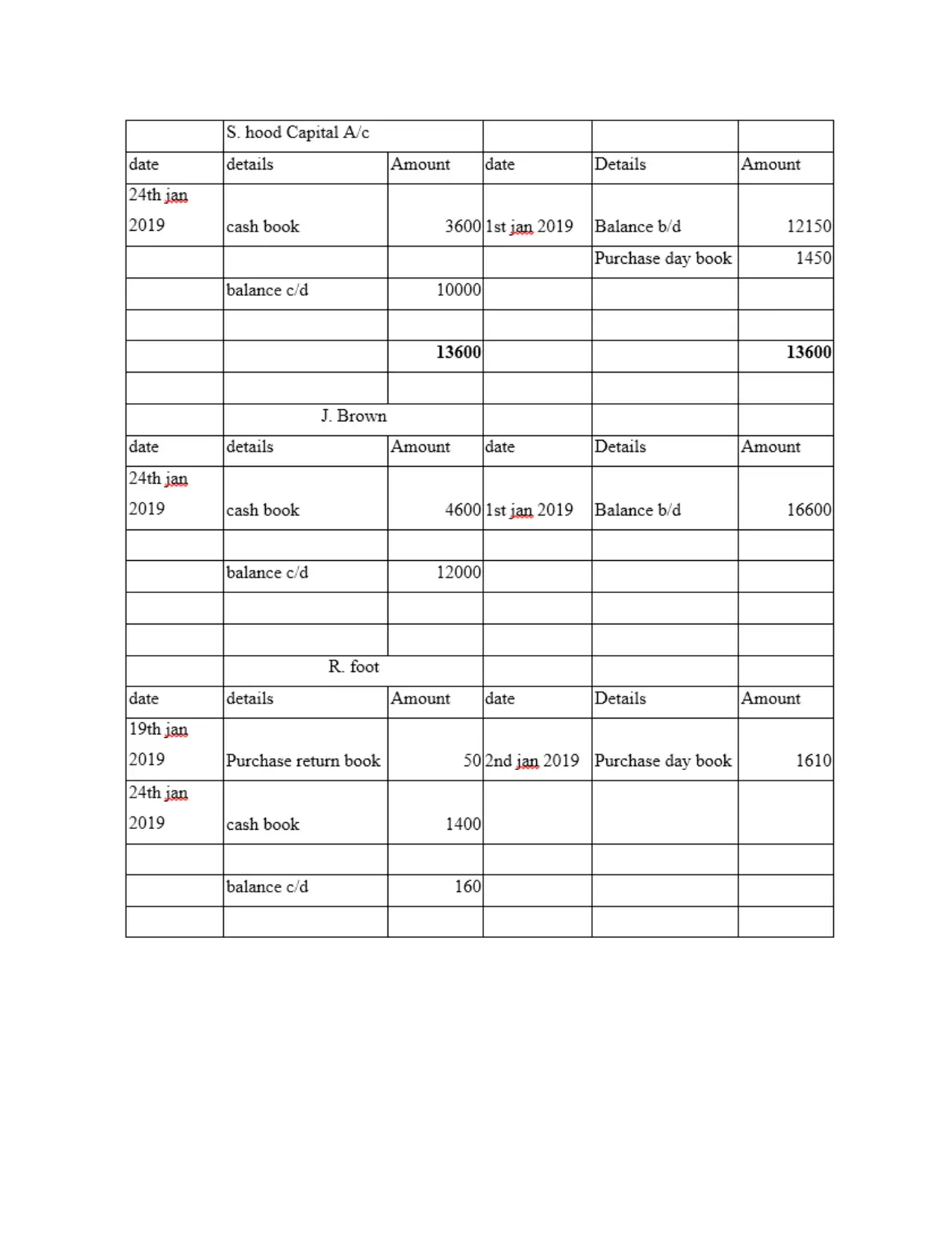

Client 1

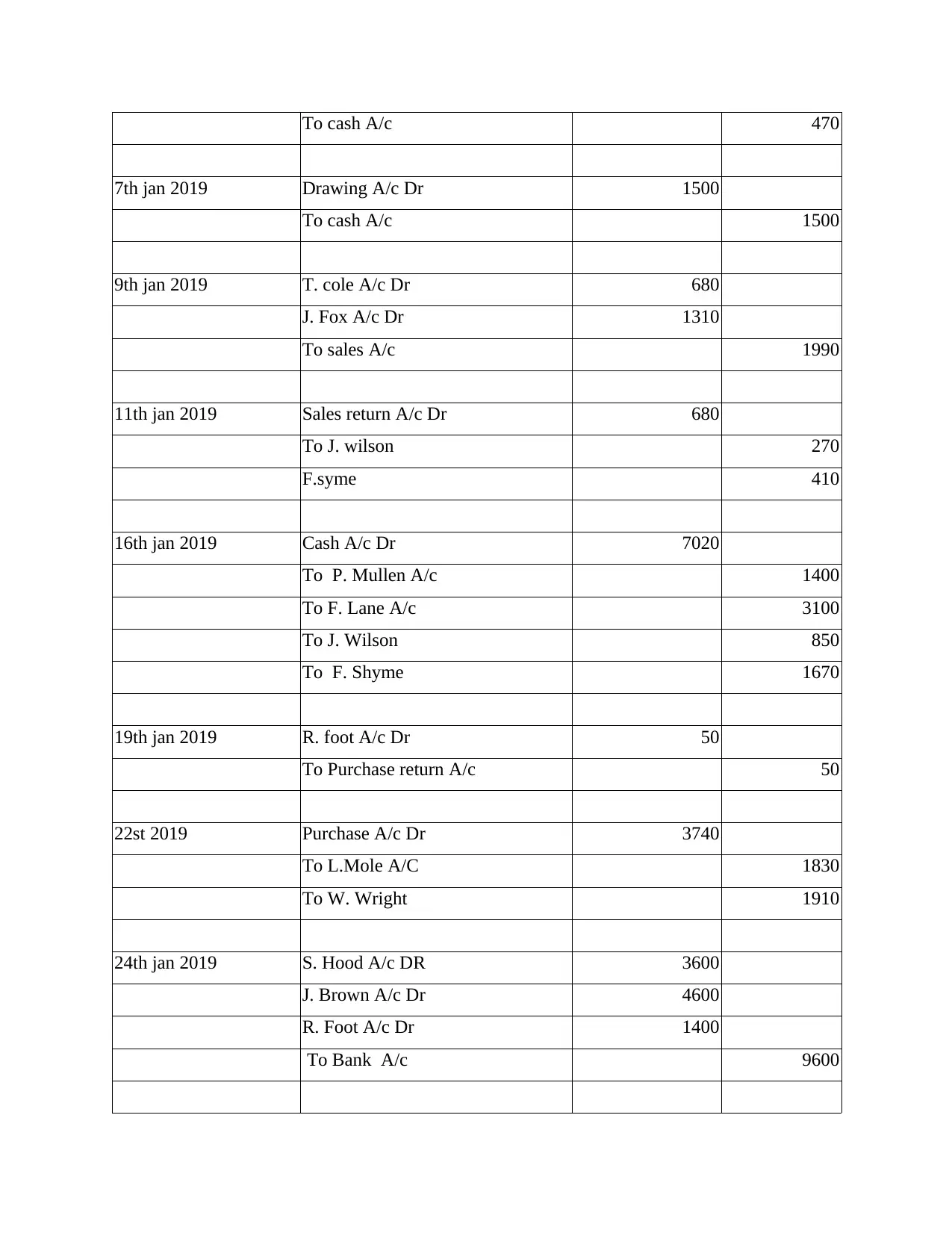

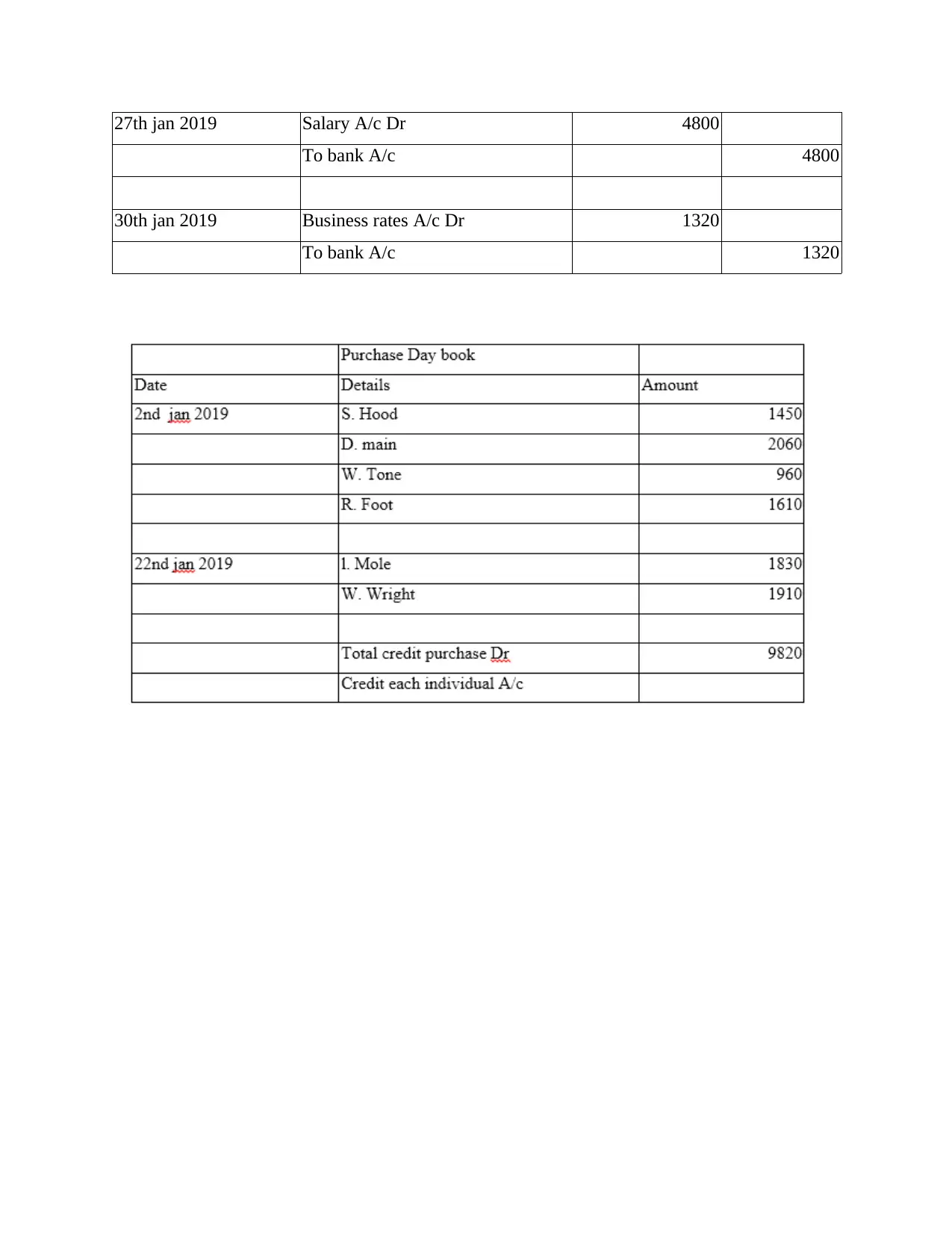

I. Recording of the journal entries

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

are important. As company manage their

transaction by viewing the supply of raw

material and resources in the company. Thus,

supplier provides finished goods to company at

bargain rates if company had good terms with

them (Weetman, 2019).

Client 1

I. Recording of the journal entries

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.