Corporate & Financial Accounting: Regulations, Standards & Analysis

VerifiedAdded on 2023/06/05

|15

|3069

|216

Report

AI Summary

This report provides a comprehensive overview of corporate and financial accounting, focusing on the regulatory environment and the role of accounting standard bodies like IASB and AASB. It discusses the importance of financial regulation in ensuring transparency and accuracy in financial reporting. Furthermore, the report includes a detailed debt and equity analysis of four publicly listed Australian companies: ANZ Bank, Bank of Queensland, Macquarie Group, and AMP Bank. The analysis examines components of owner's equity, including ordinary share capital, preference share capital, retained earnings, and reserves, to assess the financial health and performance of these companies. Desklib provides access to this assignment along with other solved papers.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Word Count:

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Word Count:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The report Financial and Corporate Accounting aims at evaluating the various steps involved

in the financial reporting and the various accounting standard policies set up by the

accounting standard bodies. The importance of having a financial regulator for maintain the

financial reports and data are covered under the assignment. The regulations of financial

accounting and reporting and the implications of the same is well covered. The projects also

gives a detailed brief about the participation of the Australian Accounting Standard Bodies in

the participation in global accounting standards. The role played by the IASB and the

compliance with the same are some of the relevant points covered. The third section of the

report goes into a detailed brief analysis of the four publically listed companies and the

analysis relating to debt and equity position in each of the firms were analysed.

Executive Summary

The report Financial and Corporate Accounting aims at evaluating the various steps involved

in the financial reporting and the various accounting standard policies set up by the

accounting standard bodies. The importance of having a financial regulator for maintain the

financial reports and data are covered under the assignment. The regulations of financial

accounting and reporting and the implications of the same is well covered. The projects also

gives a detailed brief about the participation of the Australian Accounting Standard Bodies in

the participation in global accounting standards. The role played by the IASB and the

compliance with the same are some of the relevant points covered. The third section of the

report goes into a detailed brief analysis of the four publically listed companies and the

analysis relating to debt and equity position in each of the firms were analysed.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Corporate Regulation.............................................................................................................3

Role of Accounting Standard Bodies.....................................................................................5

Owner’s Equity and Debt Analysis........................................................................................6

Analysis of the Equity............................................................................................................7

Comparative Analysis of Debt and Equity.............................................................................9

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Corporate Regulation.............................................................................................................3

Role of Accounting Standard Bodies.....................................................................................5

Owner’s Equity and Debt Analysis........................................................................................6

Analysis of the Equity............................................................................................................7

Comparative Analysis of Debt and Equity.............................................................................9

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction

The role of financial accounting and reporting is very important from the stakeholders

and from the investor’s perspective of a company. The key financial information and data

given by the management of the company serves as a common base by the stakeholders and

investors of the company as a source for performance evaluation (Nobes 2014). The need for

evaluation of financial data provided by the company is of much essence and need by the

financial standard setting bodies. The Accountability and the compliance for the financial

data and report presented should be well within the guidelines of the accounting standard

bodies. The role of IFRS in implementation of the global standard platform and as a common

tool for financial reporting is some of the key aspects and role played the IASB board. The

common principles and the accounting principles of both the AASB and IASB are similar and

the compliance from the same is somewhat similar. The debt and equity analysis of the four

publically listed companies helps us determine the key aspects of the company. The four

companies selected for the same were the ANZ Bank, Bank of Queensland, Macquarie Group

and AMP Bank (Kim, Shi and Zhou 2014).

Discussion

Corporate Regulation

The role of accounting standard bodies in defining and setting up the layout of the

financial report for the companies is important. The adjustments and the treatment of the

daily accounting transactions of an entity should be well within the prescribed guidelines of

the accounting standard bodies. The proper recording and classification of the accounting

transactions and adjustments should be in well guidelines and framework of the accounting

standards (Leuz and Wysocki 2016). The accounting standard body should regulate all the

financial reporting and accounting of a company. The accounting policy should be such that

Introduction

The role of financial accounting and reporting is very important from the stakeholders

and from the investor’s perspective of a company. The key financial information and data

given by the management of the company serves as a common base by the stakeholders and

investors of the company as a source for performance evaluation (Nobes 2014). The need for

evaluation of financial data provided by the company is of much essence and need by the

financial standard setting bodies. The Accountability and the compliance for the financial

data and report presented should be well within the guidelines of the accounting standard

bodies. The role of IFRS in implementation of the global standard platform and as a common

tool for financial reporting is some of the key aspects and role played the IASB board. The

common principles and the accounting principles of both the AASB and IASB are similar and

the compliance from the same is somewhat similar. The debt and equity analysis of the four

publically listed companies helps us determine the key aspects of the company. The four

companies selected for the same were the ANZ Bank, Bank of Queensland, Macquarie Group

and AMP Bank (Kim, Shi and Zhou 2014).

Discussion

Corporate Regulation

The role of accounting standard bodies in defining and setting up the layout of the

financial report for the companies is important. The adjustments and the treatment of the

daily accounting transactions of an entity should be well within the prescribed guidelines of

the accounting standard bodies. The proper recording and classification of the accounting

transactions and adjustments should be in well guidelines and framework of the accounting

standards (Leuz and Wysocki 2016). The accounting standard body should regulate all the

financial reporting and accounting of a company. The accounting policy should be such that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE AND FINANCIAL ACCOUNTING

the financial data provides a firm true and fair view of the financial position of the company.

The financial statements of the company presents an only source to the shareholders of the

company in the evaluation and forecasting of the financial position of the company (Lang and

Stice-Lawrence 2015). The financial information source like the cash flow statements,

income statement and the balance sheet of the company should be well regulated by the

accounting standard bodies and the market regulators by assessing the financial data

presented by the company to the retail and institutional clients (Tschopp and Nastanski 2014).

The objectivity of a correct and better financial report of a company could only be met when

the organisation maintains the form of financial presentation as per the guidelines of the

framework. The introduction and the following of the accounting standards will narrow down

the regulatory choices of recording of accountancy transactions (Claessens and Kodres 2014).

The introduction and the compliance with the regulatory framework will also provide the

option of flexibility to the management of the companies in the form of classification and

recording of income and expenses for a company. Every financial organisations and

companies should present their financial data and the report for a particular company that has

four qualities like transparency, consistency, timeliness and comprehensiveness of the

financial reporting (Tschopp and Huefner 2015). The classification of expenses and the

various types of companies in accordance with the nature of the same is better identified

when the same is regulated and governed by a standard setting bodies. The valuation of assets

and liabilities of the companies at the fair value or at the historical value and the recording for

the same is done can be better assessed with the help and the guided framework of the

accounting standard. The accounting and the true fair view of the financial position of the

company helps in better assessing the financial data and performance of the company.

the financial data provides a firm true and fair view of the financial position of the company.

The financial statements of the company presents an only source to the shareholders of the

company in the evaluation and forecasting of the financial position of the company (Lang and

Stice-Lawrence 2015). The financial information source like the cash flow statements,

income statement and the balance sheet of the company should be well regulated by the

accounting standard bodies and the market regulators by assessing the financial data

presented by the company to the retail and institutional clients (Tschopp and Nastanski 2014).

The objectivity of a correct and better financial report of a company could only be met when

the organisation maintains the form of financial presentation as per the guidelines of the

framework. The introduction and the following of the accounting standards will narrow down

the regulatory choices of recording of accountancy transactions (Claessens and Kodres 2014).

The introduction and the compliance with the regulatory framework will also provide the

option of flexibility to the management of the companies in the form of classification and

recording of income and expenses for a company. Every financial organisations and

companies should present their financial data and the report for a particular company that has

four qualities like transparency, consistency, timeliness and comprehensiveness of the

financial reporting (Tschopp and Huefner 2015). The classification of expenses and the

various types of companies in accordance with the nature of the same is better identified

when the same is regulated and governed by a standard setting bodies. The valuation of assets

and liabilities of the companies at the fair value or at the historical value and the recording for

the same is done can be better assessed with the help and the guided framework of the

accounting standard. The accounting and the true fair view of the financial position of the

company helps in better assessing the financial data and performance of the company.

5CORPORATE AND FINANCIAL ACCOUNTING

Role of Accounting Standard Bodies

The guiding principles and the accounting standards within the organisation and for the

International Financial Regulatory System (IFRS) is set up by the International Accounting

Standard Body (IASB). The Australian Accounting Standard Bodies have adopted and

followed the IFRS as there general accounting tools since January 2005 (Mittal et al. 2017).

The principles and the guidelines for the same were set in such a manner that the common

form of accounting is maintained and developed in a more better and efficient way. Both the

Australian Accounting Standard Bodies have significantly converged in the field of the

compliance and the general accounting concepts. Both the accounting standard bodies the

Australian Accounting Standard Bodies and the International Accounting Standard Bodies

are developing the common base and development of uniform base of accounting (Flower

2015). The IASB helps in providing the conceptual framework for the same in the way of

detailed comprehensive and transparent information that is provided to the stakeholders and

the investors of a company for the financial evaluation and analysis of the same. The main

motive and role of the IASB is that of catering and overviewing the financial data and the

statements that are presented by the company to the stakeholders of the company. Providing

Transparent and detailed analysis of the financial data included in the annual or financial

report by the company for the investment purpose. The important role played by the

Accounting Standard bodies is that for providing relevant and reliable information to the

financial data users. The report presented by the management of the company must offers

certain features like comparability, verifiability, timeliness and transparency. The data

provided and presented by the company should be well assessed as the same will be used by

the financial users of the company in forecasting the future financial needs of the company.

The International Accounting Standard Bodies has laid down and says that the financial

information and data that are used by the management of the companies must be in well

Role of Accounting Standard Bodies

The guiding principles and the accounting standards within the organisation and for the

International Financial Regulatory System (IFRS) is set up by the International Accounting

Standard Body (IASB). The Australian Accounting Standard Bodies have adopted and

followed the IFRS as there general accounting tools since January 2005 (Mittal et al. 2017).

The principles and the guidelines for the same were set in such a manner that the common

form of accounting is maintained and developed in a more better and efficient way. Both the

Australian Accounting Standard Bodies have significantly converged in the field of the

compliance and the general accounting concepts. Both the accounting standard bodies the

Australian Accounting Standard Bodies and the International Accounting Standard Bodies

are developing the common base and development of uniform base of accounting (Flower

2015). The IASB helps in providing the conceptual framework for the same in the way of

detailed comprehensive and transparent information that is provided to the stakeholders and

the investors of a company for the financial evaluation and analysis of the same. The main

motive and role of the IASB is that of catering and overviewing the financial data and the

statements that are presented by the company to the stakeholders of the company. Providing

Transparent and detailed analysis of the financial data included in the annual or financial

report by the company for the investment purpose. The important role played by the

Accounting Standard bodies is that for providing relevant and reliable information to the

financial data users. The report presented by the management of the company must offers

certain features like comparability, verifiability, timeliness and transparency. The data

provided and presented by the company should be well assessed as the same will be used by

the financial users of the company in forecasting the future financial needs of the company.

The International Accounting Standard Bodies has laid down and says that the financial

information and data that are used by the management of the companies must be in well

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

convergent and compliance if the stated principles of the company. The Australian

Accounting Bodies started discussions and the development of a uniform accounting policy

and standards in the year 1996 and 2002 was the year when both of the accounting standard

bodies have narrowed down and till then both of the accounting regulations have narrowed

down choices available to the management of the companies. The IFRS has a key role in

discussing and identifying key aspects of financial statements like recognition of expenditure

and income breakdown (Rey 2015).

Owner’s Equity and Debt Analysis.

The owners’ equity comprises the breakdown of the statement of changes of equity in

the form of increasing and decreasing management effects. The debt and equity analysis of

the four publically listed companies helps us determine the key aspects of the company. The

four companies selected for the same were the ANZ Bank, Bank of Queensland, Macquarie

Group and AMP Bank. The financial analysis were performed on the above mentioned

companies in the form of changing statement of equities and the debt to equity analysis for

the companies (Wossen, Berger. and Di Falco 2015).

The components of the Statement of Equity or the breakdown of the Equity Components is

shown below:

Ordinary Share Capital: The Ordinary Share Capital gives us a detailed analysis of the

ownership capital paid by the equity share capital of the company. The Ordinary

Share Capital of the firm is the Pure Equity Share of a company where the risk and

reward of the shareholders are generally high. The equity shareholders or the ordinary

shareholders of the company is given the last preference after the preference share

capital of the company in the scope and distribution of the returns generated by the

company and the profit left with the operations of the company. The main important

convergent and compliance if the stated principles of the company. The Australian

Accounting Bodies started discussions and the development of a uniform accounting policy

and standards in the year 1996 and 2002 was the year when both of the accounting standard

bodies have narrowed down and till then both of the accounting regulations have narrowed

down choices available to the management of the companies. The IFRS has a key role in

discussing and identifying key aspects of financial statements like recognition of expenditure

and income breakdown (Rey 2015).

Owner’s Equity and Debt Analysis.

The owners’ equity comprises the breakdown of the statement of changes of equity in

the form of increasing and decreasing management effects. The debt and equity analysis of

the four publically listed companies helps us determine the key aspects of the company. The

four companies selected for the same were the ANZ Bank, Bank of Queensland, Macquarie

Group and AMP Bank. The financial analysis were performed on the above mentioned

companies in the form of changing statement of equities and the debt to equity analysis for

the companies (Wossen, Berger. and Di Falco 2015).

The components of the Statement of Equity or the breakdown of the Equity Components is

shown below:

Ordinary Share Capital: The Ordinary Share Capital gives us a detailed analysis of the

ownership capital paid by the equity share capital of the company. The Ordinary

Share Capital of the firm is the Pure Equity Share of a company where the risk and

reward of the shareholders are generally high. The equity shareholders or the ordinary

shareholders of the company is given the last preference after the preference share

capital of the company in the scope and distribution of the returns generated by the

company and the profit left with the operations of the company. The main important

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

and the distinguishing factor of the Equity or the Ordinary Common share capital of

the companies is that the use and exercise of the voting power in the corporate and

important managerial decisions and functions of the company( Piketty 2015).

Preference Shareholders: The preference shareholders of the company is an important

almost as same as the ordinary share capital of the company. The preference

shareholders of the company have first preference over the profits of the company in

the equity shareholders of a company. However they also lack the voting power and

the rights for the same (Wossen, Berger and Di Falco 2015).

Retained Earnings or Ploughed Back Profit: The ploughed back or the retained

earnings of the company shows the net amount of profits retained by the company in

the form of the internal reserves of a company (Penrose 2017). The ploughed back

profit or he retained earnings of the company acts as a best part of internal generation

of funds for the companies.

Reserves: The reserves of the company is a type of internally generated fund that is

created by the company in the due course of the operations and the business of an

organisations. The reserves of the company is settled and used internally by the

company (Abdelrehim and Toms 2017).

Analysis of the Equity

ANZ Bank: The ANZ Company had given an considerable increase and rise in the Share

capital of the company in the trend period and the four-year analysis period taken. The

company has tried to maintain the financing needs for the company through different equity

sources (Svitek 2015). The reserves for the company has been very volatile while the retained

earnings for the company has risen to a greater level with the passage and in each of the

period considered (Gitman, Juchau and Flanagan 2015).

and the distinguishing factor of the Equity or the Ordinary Common share capital of

the companies is that the use and exercise of the voting power in the corporate and

important managerial decisions and functions of the company( Piketty 2015).

Preference Shareholders: The preference shareholders of the company is an important

almost as same as the ordinary share capital of the company. The preference

shareholders of the company have first preference over the profits of the company in

the equity shareholders of a company. However they also lack the voting power and

the rights for the same (Wossen, Berger and Di Falco 2015).

Retained Earnings or Ploughed Back Profit: The ploughed back or the retained

earnings of the company shows the net amount of profits retained by the company in

the form of the internal reserves of a company (Penrose 2017). The ploughed back

profit or he retained earnings of the company acts as a best part of internal generation

of funds for the companies.

Reserves: The reserves of the company is a type of internally generated fund that is

created by the company in the due course of the operations and the business of an

organisations. The reserves of the company is settled and used internally by the

company (Abdelrehim and Toms 2017).

Analysis of the Equity

ANZ Bank: The ANZ Company had given an considerable increase and rise in the Share

capital of the company in the trend period and the four-year analysis period taken. The

company has tried to maintain the financing needs for the company through different equity

sources (Svitek 2015). The reserves for the company has been very volatile while the retained

earnings for the company has risen to a greater level with the passage and in each of the

period considered (Gitman, Juchau and Flanagan 2015).

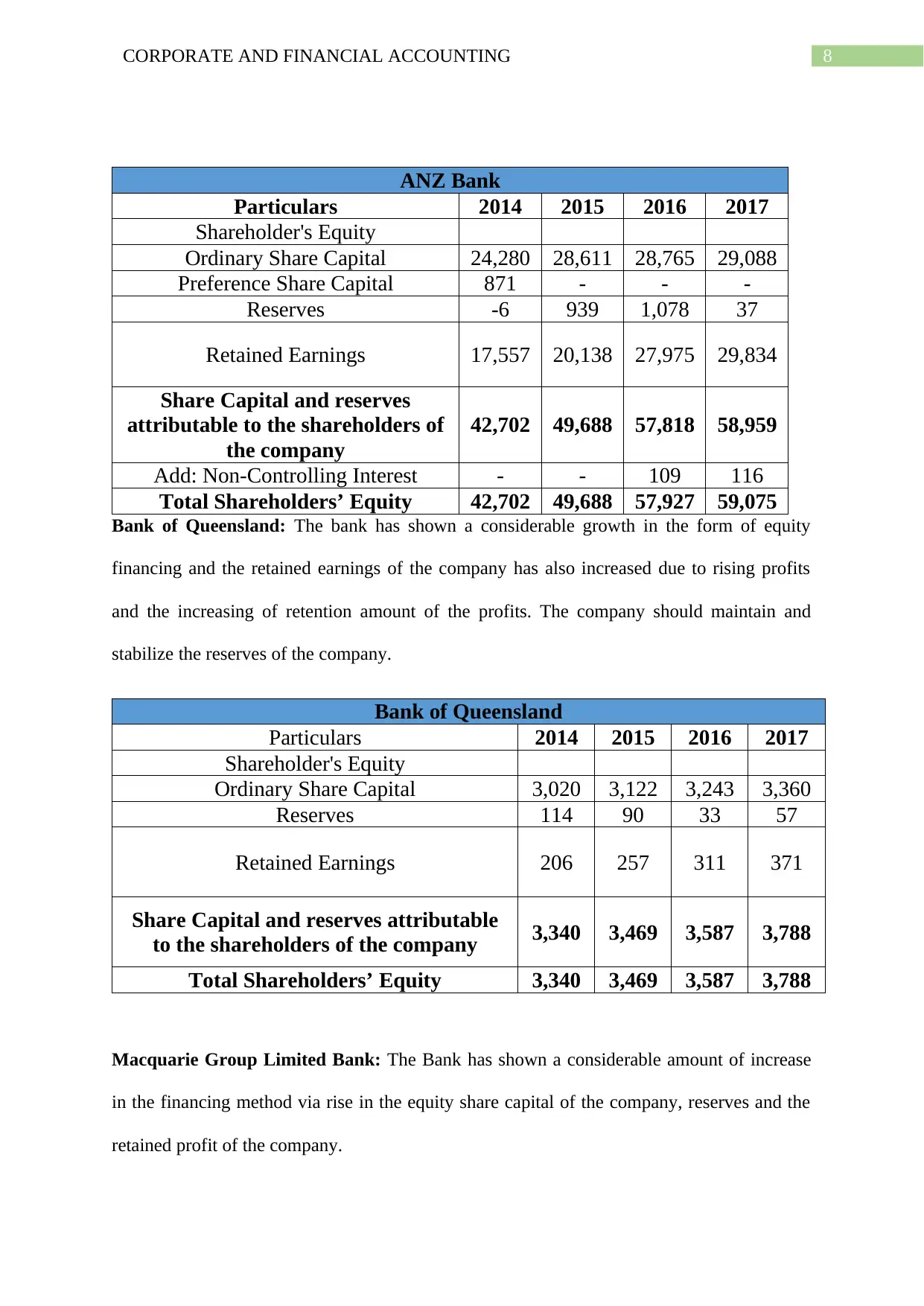

8CORPORATE AND FINANCIAL ACCOUNTING

ANZ Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 24,280 28,611 28,765 29,088

Preference Share Capital 871 - - -

Reserves -6 939 1,078 37

Retained Earnings 17,557 20,138 27,975 29,834

Share Capital and reserves

attributable to the shareholders of

the company

42,702 49,688 57,818 58,959

Add: Non-Controlling Interest - - 109 116

Total Shareholders’ Equity 42,702 49,688 57,927 59,075

Bank of Queensland: The bank has shown a considerable growth in the form of equity

financing and the retained earnings of the company has also increased due to rising profits

and the increasing of retention amount of the profits. The company should maintain and

stabilize the reserves of the company.

Bank of Queensland

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 3,020 3,122 3,243 3,360

Reserves 114 90 33 57

Retained Earnings 206 257 311 371

Share Capital and reserves attributable

to the shareholders of the company 3,340 3,469 3,587 3,788

Total Shareholders’ Equity 3,340 3,469 3,587 3,788

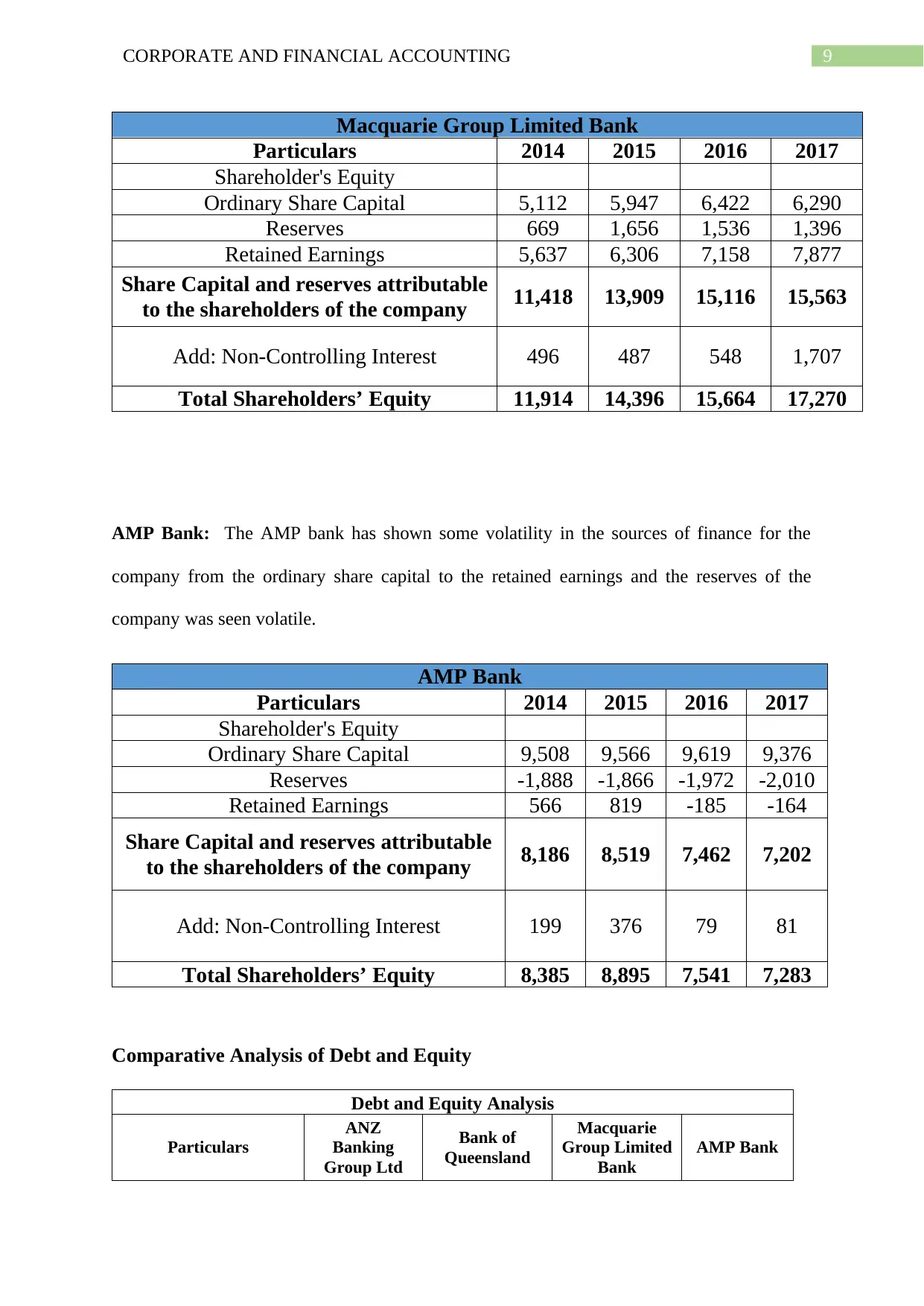

Macquarie Group Limited Bank: The Bank has shown a considerable amount of increase

in the financing method via rise in the equity share capital of the company, reserves and the

retained profit of the company.

ANZ Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 24,280 28,611 28,765 29,088

Preference Share Capital 871 - - -

Reserves -6 939 1,078 37

Retained Earnings 17,557 20,138 27,975 29,834

Share Capital and reserves

attributable to the shareholders of

the company

42,702 49,688 57,818 58,959

Add: Non-Controlling Interest - - 109 116

Total Shareholders’ Equity 42,702 49,688 57,927 59,075

Bank of Queensland: The bank has shown a considerable growth in the form of equity

financing and the retained earnings of the company has also increased due to rising profits

and the increasing of retention amount of the profits. The company should maintain and

stabilize the reserves of the company.

Bank of Queensland

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 3,020 3,122 3,243 3,360

Reserves 114 90 33 57

Retained Earnings 206 257 311 371

Share Capital and reserves attributable

to the shareholders of the company 3,340 3,469 3,587 3,788

Total Shareholders’ Equity 3,340 3,469 3,587 3,788

Macquarie Group Limited Bank: The Bank has shown a considerable amount of increase

in the financing method via rise in the equity share capital of the company, reserves and the

retained profit of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE AND FINANCIAL ACCOUNTING

Macquarie Group Limited Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 5,112 5,947 6,422 6,290

Reserves 669 1,656 1,536 1,396

Retained Earnings 5,637 6,306 7,158 7,877

Share Capital and reserves attributable

to the shareholders of the company 11,418 13,909 15,116 15,563

Add: Non-Controlling Interest 496 487 548 1,707

Total Shareholders’ Equity 11,914 14,396 15,664 17,270

AMP Bank: The AMP bank has shown some volatility in the sources of finance for the

company from the ordinary share capital to the retained earnings and the reserves of the

company was seen volatile.

AMP Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 9,508 9,566 9,619 9,376

Reserves -1,888 -1,866 -1,972 -2,010

Retained Earnings 566 819 -185 -164

Share Capital and reserves attributable

to the shareholders of the company 8,186 8,519 7,462 7,202

Add: Non-Controlling Interest 199 376 79 81

Total Shareholders’ Equity 8,385 8,895 7,541 7,283

Comparative Analysis of Debt and Equity

Debt and Equity Analysis

Particulars

ANZ

Banking

Group Ltd

Bank of

Queensland

Macquarie

Group Limited

Bank

AMP Bank

Macquarie Group Limited Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 5,112 5,947 6,422 6,290

Reserves 669 1,656 1,536 1,396

Retained Earnings 5,637 6,306 7,158 7,877

Share Capital and reserves attributable

to the shareholders of the company 11,418 13,909 15,116 15,563

Add: Non-Controlling Interest 496 487 548 1,707

Total Shareholders’ Equity 11,914 14,396 15,664 17,270

AMP Bank: The AMP bank has shown some volatility in the sources of finance for the

company from the ordinary share capital to the retained earnings and the reserves of the

company was seen volatile.

AMP Bank

Particulars 2014 2015 2016 2017

Shareholder's Equity

Ordinary Share Capital 9,508 9,566 9,619 9,376

Reserves -1,888 -1,866 -1,972 -2,010

Retained Earnings 566 819 -185 -164

Share Capital and reserves attributable

to the shareholders of the company 8,186 8,519 7,462 7,202

Add: Non-Controlling Interest 199 376 79 81

Total Shareholders’ Equity 8,385 8,895 7,541 7,283

Comparative Analysis of Debt and Equity

Debt and Equity Analysis

Particulars

ANZ

Banking

Group Ltd

Bank of

Queensland

Macquarie

Group Limited

Bank

AMP Bank

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE AND FINANCIAL ACCOUNTING

Total Long Term Debt 1,07,973 262 50,828 21,009

Shareholders' Equity 59,075 3,788 15,563 7,283

Debt/Equity Ratio 1.83 0.07 3.27 2.88

ANZ Banking

Group Ltd Bank of

Queensland Macquarie

Group Limited

Bank

AMP Bank

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Debt/Equity Ratio

2014 2015 2016 2017

-10,000

0

10,000

20,000

30,000

40,000

ANZ Bank

Ordinary Share Capital Preference Share Capital

Reserves Retained Earnings

2014 2015 2016 2017

0

2,000

4,000

6,000

8,000

10,000

Bank of Queensland

Ordinary Share Capital Reserves Retained Earnings

Total Long Term Debt 1,07,973 262 50,828 21,009

Shareholders' Equity 59,075 3,788 15,563 7,283

Debt/Equity Ratio 1.83 0.07 3.27 2.88

ANZ Banking

Group Ltd Bank of

Queensland Macquarie

Group Limited

Bank

AMP Bank

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Debt/Equity Ratio

2014 2015 2016 2017

-10,000

0

10,000

20,000

30,000

40,000

ANZ Bank

Ordinary Share Capital Preference Share Capital

Reserves Retained Earnings

2014 2015 2016 2017

0

2,000

4,000

6,000

8,000

10,000

Bank of Queensland

Ordinary Share Capital Reserves Retained Earnings

11CORPORATE AND FINANCIAL ACCOUNTING

2014 2015 2016 2017

-4,000

0

4,000

8,000

12,000

AMP Bank

Ordinary Share Capital Reserves Retained Earnings

2014 2015 2016 2017

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Macquarie Group Limited Bank

Ordinary Share Capital Reserves Retained Earnings

2014 2015 2016 2017

-4,000

0

4,000

8,000

12,000

AMP Bank

Ordinary Share Capital Reserves Retained Earnings

2014 2015 2016 2017

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Macquarie Group Limited Bank

Ordinary Share Capital Reserves Retained Earnings

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.