Financial Accounting: Exploring Statement Users and Analysis

VerifiedAdded on 2023/04/20

|17

|4382

|311

Report

AI Summary

This report provides an overview of financial accounting, emphasizing the different user groups of financial statements, including owners, investors, management, lenders, suppliers, government, employees, and customers, and their respective needs for financial information. It also analyzes the financial performance of Ryan Air and Delta Airlines using ratio analysis based on their income statements and balance sheets from 2013 to 2015, concluding that while Ryan Air initially showed negative ratios but improved over time, Delta Airlines started strong but faced financial challenges later. The study highlights the importance of financial accounting in assessing a company's financial health and making informed decisions.

Financial accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................3

1) Explain different user groups of financial statements.................................................................3

CONCLUSION....................................................................................................................................6

REFERENCES.....................................................................................................................................8

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF RYAN AIR.........................11

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF DELTA AIRLINES...........15

2

INTRODUCTION................................................................................................................................3

1) Explain different user groups of financial statements.................................................................3

CONCLUSION....................................................................................................................................6

REFERENCES.....................................................................................................................................8

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF RYAN AIR.........................11

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF DELTA AIRLINES...........15

2

INTRODUCTION

Financial accounting is one of the fields of accounting which is concerned with the

summary, analysis and reporting of financial transactions which takes place in a normal course of

business. It involves preparation of financial statements available for the public consumption

(Accounting- Need And Importance, 2016). The financial statements are used by stockholders,

suppliers, banks, employees and government agencies and the business owners. This kind of

financial accounting is governed by both local and international accounting standards. It also

follows generally accepted accounting principles which define different instructions and other

guidelines that assist in operating daily routine business. Financial report is the framework which

provides deeper insight to the business organization and its stakeholders about the monetary

aspects.

1) Explain different user groups of financial statements

A financial statement is a formal record of financial activities to determine the position of

the organization. The relevant financial information is presented in a structured and well defined

manner (Agoglia, Doupnik and Tsakumis, 2011). Following are the different user groups of

financial statements which can be further divided into two main categories such as internal as well

as external user groups:

Owners and investors- These are the basic user groups who use financial statements to find

out facts and information which can affect the financial condition of the company. It involves

shareholders of corporation who requires financial information in taking decisions regarding

finance (Bamber, Jiang and Wang, 2010). This act as a instrument which helps in taking better

decisions related to holding, selling and purchasing of new asset.Assessment of future growth and

profitability of a company is helpful for the potential investors. This instrument acts as a decision

tool to analyze the external forces implications on the current state of the business to take forward

step in life. Shareholders use financial statements to assess the risk and return on their investment in

a firm (Chen and et.al., 2010). Shareholders can use capital budgeting techniques to evaluate its

returns from the prospective returns from the potential investment. Investors may predict future

dividends based on the profits which is accurately disclosed in financial statements. Further, risk

associated with the investment may be gauged from the financial statements.

Management- The definition of management is different for every business such as owner

for small business. In large organisations, management is made up of hired professionals who are

entrusted with the responsibility of operating the activities or a part of the business. It require

financial statements to manage the affairs of the company by assessing financial performance

3

Financial accounting is one of the fields of accounting which is concerned with the

summary, analysis and reporting of financial transactions which takes place in a normal course of

business. It involves preparation of financial statements available for the public consumption

(Accounting- Need And Importance, 2016). The financial statements are used by stockholders,

suppliers, banks, employees and government agencies and the business owners. This kind of

financial accounting is governed by both local and international accounting standards. It also

follows generally accepted accounting principles which define different instructions and other

guidelines that assist in operating daily routine business. Financial report is the framework which

provides deeper insight to the business organization and its stakeholders about the monetary

aspects.

1) Explain different user groups of financial statements

A financial statement is a formal record of financial activities to determine the position of

the organization. The relevant financial information is presented in a structured and well defined

manner (Agoglia, Doupnik and Tsakumis, 2011). Following are the different user groups of

financial statements which can be further divided into two main categories such as internal as well

as external user groups:

Owners and investors- These are the basic user groups who use financial statements to find

out facts and information which can affect the financial condition of the company. It involves

shareholders of corporation who requires financial information in taking decisions regarding

finance (Bamber, Jiang and Wang, 2010). This act as a instrument which helps in taking better

decisions related to holding, selling and purchasing of new asset.Assessment of future growth and

profitability of a company is helpful for the potential investors. This instrument acts as a decision

tool to analyze the external forces implications on the current state of the business to take forward

step in life. Shareholders use financial statements to assess the risk and return on their investment in

a firm (Chen and et.al., 2010). Shareholders can use capital budgeting techniques to evaluate its

returns from the prospective returns from the potential investment. Investors may predict future

dividends based on the profits which is accurately disclosed in financial statements. Further, risk

associated with the investment may be gauged from the financial statements.

Management- The definition of management is different for every business such as owner

for small business. In large organisations, management is made up of hired professionals who are

entrusted with the responsibility of operating the activities or a part of the business. It require

financial statements to manage the affairs of the company by assessing financial performance

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Colson and et.al., 2010). Management plays a significant role in the whole organization in terms of

managing the targets to complete on time with high level of accuracy. The management needs to

comply with all rules and regulations imposed on the business. It is regarded as a head of the

organisation in achieving higher efficiency and effectiveness. The relevancy of different forms of

financial statements is different for the individuals. It includes income statement, balance sheet and

cash flow statements (Henderson and et. al., 2015). These financial statements will affect the

decision of business which may pose threats for the business.

Lenders- Lenders lend their money to business on basic terms and conditions and specified

amount of interest as a token of appreciation for helping business in tough and complex situations.

Lenders of funds include banks and other financial institutions who are interested in the company's

ability to pay its liabilities and obligations on its maturity (Lovell, 2014). These lenders will lend

amount to various business by judging its current efficiency to assure that they will get their amount

back. In today's competitive and complex environment, the scope of these financial institutions has

increased in providing different services to their regular as well as potential clients (Oler, Oler and

Skousen, 2010). They use financial statements as a tool to monitor the significant changes which

may takes place in daily routine business which may affect the profitability of the company.

Lenders use the financial facts and information to determine whether they should extend credit to

the business or restrict the amount of credit which has already been extended. The main focus of the

lender is to measure the overall changes which take place in the graph of credit taken by the

company.

Trade creditors or suppliers- Suppliers need financial statements to determine the credit

worthiness of an enterprise to ascertain whether to supply goods on credit or not (Song, Thomas and

Yi, 2010). Suppliers are required know that the business is able to pay back its liability towards the

supplier or can get into liquidity trap or bankrupt. Terms of credit plays a significant role in

determining the financial health of its customers. Credit terms will form as legal evidence in case of

any default done by any party. Financial statements act as a weapon against the defaulters to the

contract. The company is required to make a separate provision for trade creditors to ensure its

correct and timely payment (Weil, Schipper and Francis, 2013).

Government- Government bodies of the state most importantly tax authorities will greatly

affect the smooth functioning of the business. Tax authorities are interested in an entity's financial

information for taxation and other regulatory purposes (Badertscher, Burks and Easton, 2011).

Government require financial statements to determine the correctness of tax declared in the tax

returns. They also keep track of economic progress by analyzing the financial statements of

businesses from different sectors of the economy. There are several government agencies that need

4

managing the targets to complete on time with high level of accuracy. The management needs to

comply with all rules and regulations imposed on the business. It is regarded as a head of the

organisation in achieving higher efficiency and effectiveness. The relevancy of different forms of

financial statements is different for the individuals. It includes income statement, balance sheet and

cash flow statements (Henderson and et. al., 2015). These financial statements will affect the

decision of business which may pose threats for the business.

Lenders- Lenders lend their money to business on basic terms and conditions and specified

amount of interest as a token of appreciation for helping business in tough and complex situations.

Lenders of funds include banks and other financial institutions who are interested in the company's

ability to pay its liabilities and obligations on its maturity (Lovell, 2014). These lenders will lend

amount to various business by judging its current efficiency to assure that they will get their amount

back. In today's competitive and complex environment, the scope of these financial institutions has

increased in providing different services to their regular as well as potential clients (Oler, Oler and

Skousen, 2010). They use financial statements as a tool to monitor the significant changes which

may takes place in daily routine business which may affect the profitability of the company.

Lenders use the financial facts and information to determine whether they should extend credit to

the business or restrict the amount of credit which has already been extended. The main focus of the

lender is to measure the overall changes which take place in the graph of credit taken by the

company.

Trade creditors or suppliers- Suppliers need financial statements to determine the credit

worthiness of an enterprise to ascertain whether to supply goods on credit or not (Song, Thomas and

Yi, 2010). Suppliers are required know that the business is able to pay back its liability towards the

supplier or can get into liquidity trap or bankrupt. Terms of credit plays a significant role in

determining the financial health of its customers. Credit terms will form as legal evidence in case of

any default done by any party. Financial statements act as a weapon against the defaulters to the

contract. The company is required to make a separate provision for trade creditors to ensure its

correct and timely payment (Weil, Schipper and Francis, 2013).

Government- Government bodies of the state most importantly tax authorities will greatly

affect the smooth functioning of the business. Tax authorities are interested in an entity's financial

information for taxation and other regulatory purposes (Badertscher, Burks and Easton, 2011).

Government require financial statements to determine the correctness of tax declared in the tax

returns. They also keep track of economic progress by analyzing the financial statements of

businesses from different sectors of the economy. There are several government agencies that need

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to know how the economy is performing to plan financial and industrial policies. The tax authorities

also consider different statements which shows financial data as a basis for assessing the amount of

tax payable by a business (Biondi and et.al., 2011).

Employee- Employees are interested in the company's financial statements to assess its

profitability and stability. These two factors play a significant role in ensuring permanent job

position of employees in the firm (Choi, 2013). Profitability is very effective for employees as it

will assure them that they will get deserving salaries and other employment benefits. These may

include incentives, perks, allowances and overtime compensation. They are also interested in

financial position and performance to assess company’s expansion possibilities. It is also beneficial

for an enterprise in providing ample of career opportunities and business development chances

which in return increases the job role of all employees (Edwards, 2013).

Customers- For every organisation, customer is regarded as a king of the market as it will

spoil or make a career of the business (Li, 2010). The implications of external users especially of

customer can be positive as well as negative which depends on the capability of a person. The long

term involvement of a person with the company is a good sign which states that company will

achieve its desired goals and the objectives in a reasonable time period. Customers are interested in

knowing minute details about the organization to continue its existence and maintain stability of

operations. This need is heightened in cases where the customers depend upon the entity (Macve,

2015).

LONDON STOCK MARKET

It is a stock exchange which is located in the city of London in United Kingdom. This

market had a market capitalisation of US$ 6.06 trillion. This stock market ranks among third largest

stock exchange in the whole nation (Rutherford, 2010). It was founded in 1801 and its current

premises are situated in Paternoster Square which is closest to St Paul's Cathedral in the same city.

The exchange is one of the subsidiaries of the London stock exchange group. It is one of the world's

oldest stock exchanges and can trace its history back more than 300 years. It is also known as Royal

exchange as it was founded by English financier Thomas Gresham on the model of the Antwerp

Bourse as a stock exchange (Uyar and Gungormus, 2016). Its performance has been affected with

several wars such as First World War and Second World War. It issues different types of securities

which are offered to general public as well as different companies. It deals in two kinds of markets

which include primary as well as secondary markets. There are several companies listed in this

stock exchange but here two companies are taken into considerations which are following:

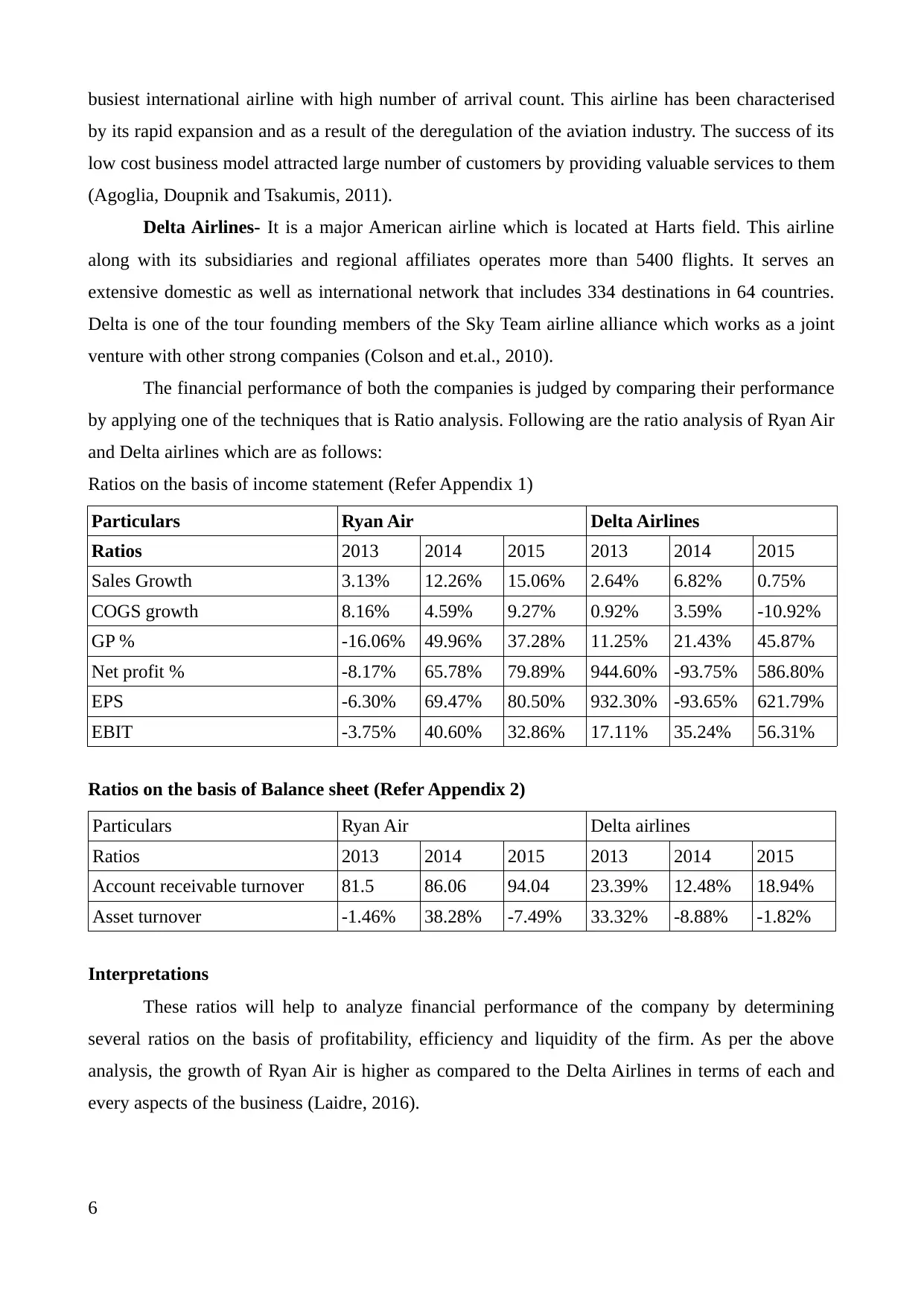

Ryan Air- It is an Irish low cost airline which is headquartered in Swords in Dublin Ireland.

Ryan Air was the largest European airlines which are regarded as common passenger airline and

5

also consider different statements which shows financial data as a basis for assessing the amount of

tax payable by a business (Biondi and et.al., 2011).

Employee- Employees are interested in the company's financial statements to assess its

profitability and stability. These two factors play a significant role in ensuring permanent job

position of employees in the firm (Choi, 2013). Profitability is very effective for employees as it

will assure them that they will get deserving salaries and other employment benefits. These may

include incentives, perks, allowances and overtime compensation. They are also interested in

financial position and performance to assess company’s expansion possibilities. It is also beneficial

for an enterprise in providing ample of career opportunities and business development chances

which in return increases the job role of all employees (Edwards, 2013).

Customers- For every organisation, customer is regarded as a king of the market as it will

spoil or make a career of the business (Li, 2010). The implications of external users especially of

customer can be positive as well as negative which depends on the capability of a person. The long

term involvement of a person with the company is a good sign which states that company will

achieve its desired goals and the objectives in a reasonable time period. Customers are interested in

knowing minute details about the organization to continue its existence and maintain stability of

operations. This need is heightened in cases where the customers depend upon the entity (Macve,

2015).

LONDON STOCK MARKET

It is a stock exchange which is located in the city of London in United Kingdom. This

market had a market capitalisation of US$ 6.06 trillion. This stock market ranks among third largest

stock exchange in the whole nation (Rutherford, 2010). It was founded in 1801 and its current

premises are situated in Paternoster Square which is closest to St Paul's Cathedral in the same city.

The exchange is one of the subsidiaries of the London stock exchange group. It is one of the world's

oldest stock exchanges and can trace its history back more than 300 years. It is also known as Royal

exchange as it was founded by English financier Thomas Gresham on the model of the Antwerp

Bourse as a stock exchange (Uyar and Gungormus, 2016). Its performance has been affected with

several wars such as First World War and Second World War. It issues different types of securities

which are offered to general public as well as different companies. It deals in two kinds of markets

which include primary as well as secondary markets. There are several companies listed in this

stock exchange but here two companies are taken into considerations which are following:

Ryan Air- It is an Irish low cost airline which is headquartered in Swords in Dublin Ireland.

Ryan Air was the largest European airlines which are regarded as common passenger airline and

5

busiest international airline with high number of arrival count. This airline has been characterised

by its rapid expansion and as a result of the deregulation of the aviation industry. The success of its

low cost business model attracted large number of customers by providing valuable services to them

(Agoglia, Doupnik and Tsakumis, 2011).

Delta Airlines- It is a major American airline which is located at Harts field. This airline

along with its subsidiaries and regional affiliates operates more than 5400 flights. It serves an

extensive domestic as well as international network that includes 334 destinations in 64 countries.

Delta is one of the tour founding members of the Sky Team airline alliance which works as a joint

venture with other strong companies (Colson and et.al., 2010).

The financial performance of both the companies is judged by comparing their performance

by applying one of the techniques that is Ratio analysis. Following are the ratio analysis of Ryan Air

and Delta airlines which are as follows:

Ratios on the basis of income statement (Refer Appendix 1)

Particulars Ryan Air Delta Airlines

Ratios 2013 2014 2015 2013 2014 2015

Sales Growth 3.13% 12.26% 15.06% 2.64% 6.82% 0.75%

COGS growth 8.16% 4.59% 9.27% 0.92% 3.59% -10.92%

GP % -16.06% 49.96% 37.28% 11.25% 21.43% 45.87%

Net profit % -8.17% 65.78% 79.89% 944.60% -93.75% 586.80%

EPS -6.30% 69.47% 80.50% 932.30% -93.65% 621.79%

EBIT -3.75% 40.60% 32.86% 17.11% 35.24% 56.31%

Ratios on the basis of Balance sheet (Refer Appendix 2)

Particulars Ryan Air Delta airlines

Ratios 2013 2014 2015 2013 2014 2015

Account receivable turnover 81.5 86.06 94.04 23.39% 12.48% 18.94%

Asset turnover -1.46% 38.28% -7.49% 33.32% -8.88% -1.82%

Interpretations

These ratios will help to analyze financial performance of the company by determining

several ratios on the basis of profitability, efficiency and liquidity of the firm. As per the above

analysis, the growth of Ryan Air is higher as compared to the Delta Airlines in terms of each and

every aspects of the business (Laidre, 2016).

6

by its rapid expansion and as a result of the deregulation of the aviation industry. The success of its

low cost business model attracted large number of customers by providing valuable services to them

(Agoglia, Doupnik and Tsakumis, 2011).

Delta Airlines- It is a major American airline which is located at Harts field. This airline

along with its subsidiaries and regional affiliates operates more than 5400 flights. It serves an

extensive domestic as well as international network that includes 334 destinations in 64 countries.

Delta is one of the tour founding members of the Sky Team airline alliance which works as a joint

venture with other strong companies (Colson and et.al., 2010).

The financial performance of both the companies is judged by comparing their performance

by applying one of the techniques that is Ratio analysis. Following are the ratio analysis of Ryan Air

and Delta airlines which are as follows:

Ratios on the basis of income statement (Refer Appendix 1)

Particulars Ryan Air Delta Airlines

Ratios 2013 2014 2015 2013 2014 2015

Sales Growth 3.13% 12.26% 15.06% 2.64% 6.82% 0.75%

COGS growth 8.16% 4.59% 9.27% 0.92% 3.59% -10.92%

GP % -16.06% 49.96% 37.28% 11.25% 21.43% 45.87%

Net profit % -8.17% 65.78% 79.89% 944.60% -93.75% 586.80%

EPS -6.30% 69.47% 80.50% 932.30% -93.65% 621.79%

EBIT -3.75% 40.60% 32.86% 17.11% 35.24% 56.31%

Ratios on the basis of Balance sheet (Refer Appendix 2)

Particulars Ryan Air Delta airlines

Ratios 2013 2014 2015 2013 2014 2015

Account receivable turnover 81.5 86.06 94.04 23.39% 12.48% 18.94%

Asset turnover -1.46% 38.28% -7.49% 33.32% -8.88% -1.82%

Interpretations

These ratios will help to analyze financial performance of the company by determining

several ratios on the basis of profitability, efficiency and liquidity of the firm. As per the above

analysis, the growth of Ryan Air is higher as compared to the Delta Airlines in terms of each and

every aspects of the business (Laidre, 2016).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above study it can be concluded that financial accounting have a major role in

determining the financial performance of the company. The different users of the financial

statements use different forms of financial statements to achieve their desired goals and the

objectives. The performance of the two companies Ryan Air and Delta Airlines will clearly reflect

the actual conditions of a firm. It states that Ryan Air starts with negative ratios but slowly moved

on the path of success. On the contrary, delta Airlines will be on stable position in beginning and

slowly goes into debt trap by showing negative ratios.

7

From the above study it can be concluded that financial accounting have a major role in

determining the financial performance of the company. The different users of the financial

statements use different forms of financial statements to achieve their desired goals and the

objectives. The performance of the two companies Ryan Air and Delta Airlines will clearly reflect

the actual conditions of a firm. It states that Ryan Air starts with negative ratios but slowly moved

on the path of success. On the contrary, delta Airlines will be on stable position in beginning and

slowly goes into debt trap by showing negative ratios.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Agoglia, C.P., Doupnik, T.S. and Tsakumis, G.T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength on

financial reporting decisions. The Accounting Review. 86(3). pp. 747-767.

Badertscher, B.A., Burks, J.J. and Easton, P.D., 2011. A convenient scapegoat: Fair value

accounting by commercial banks during the financial crisis. The Accounting Review. 87(1).

pp. 59-90.

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What's my style? The influence of top managers on

voluntary corporate financial disclosure. The accounting review. 85(4). pp. 1131-1162.

Biondi, Y. and et.al., 2011. A Perspective on the Joint IASB/FASB Exposure Draft on Accounting

for Leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC).Accounting Horizons. 25(4). pp. 861-871.

Chen, H. and et.al., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial

Management & Accounting. 21(3). pp. 220-278.

Choi, S., 2013. The Linkage Strategies Between Productivity Metrics and Financial Accounting

Metrics in TPM and PAC Activities. Journal of the Korea Safety Management and Science.

15(3). pp. 151-161.

Colson, R.H. and et.al., 2010. Response to the Financial Accounting Standards Board's and the

International Accounting Standards Board's Joint Discussion Paper Entitled Preliminary

Views on Revenue Recognition in Contracts with Customers. Accounting horizons. 24(4).

pp. 689-702.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gassen, J., 2014. Causal inference in empirical archival financial accounting research. Accounting,

Organizations and Society. 39(7). pp. 535-544.

Henderson, S. and et. al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2010. Financial accounting: tools for business

decision making. John Wiley & Sons.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the

European Union reduce the cost of equity capital?. The accounting review. 85(2). pp. 607-

636.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting. Economy

and Society. 43(2). pp. 260-284.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision, Tool,

Or Threat?. Routledge.

8

Books and Journals

Agoglia, C.P., Doupnik, T.S. and Tsakumis, G.T., 2011. Principles-based versus rules-based

accounting standards: The influence of standard precision and audit committee strength on

financial reporting decisions. The Accounting Review. 86(3). pp. 747-767.

Badertscher, B.A., Burks, J.J. and Easton, P.D., 2011. A convenient scapegoat: Fair value

accounting by commercial banks during the financial crisis. The Accounting Review. 87(1).

pp. 59-90.

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What's my style? The influence of top managers on

voluntary corporate financial disclosure. The accounting review. 85(4). pp. 1131-1162.

Biondi, Y. and et.al., 2011. A Perspective on the Joint IASB/FASB Exposure Draft on Accounting

for Leases: American Accounting Association's Financial Accounting Standards Committee

(AAA FASC).Accounting Horizons. 25(4). pp. 861-871.

Chen, H. and et.al., 2010. The role of international financial reporting standards in accounting

quality: Evidence from the European Union. Journal of International Financial

Management & Accounting. 21(3). pp. 220-278.

Choi, S., 2013. The Linkage Strategies Between Productivity Metrics and Financial Accounting

Metrics in TPM and PAC Activities. Journal of the Korea Safety Management and Science.

15(3). pp. 151-161.

Colson, R.H. and et.al., 2010. Response to the Financial Accounting Standards Board's and the

International Accounting Standards Board's Joint Discussion Paper Entitled Preliminary

Views on Revenue Recognition in Contracts with Customers. Accounting horizons. 24(4).

pp. 689-702.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting)(Vol. 29). Routledge.

Gassen, J., 2014. Causal inference in empirical archival financial accounting research. Accounting,

Organizations and Society. 39(7). pp. 535-544.

Henderson, S. and et. al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2010. Financial accounting: tools for business

decision making. John Wiley & Sons.

Li, S., 2010. Does mandatory adoption of International Financial Reporting Standards in the

European Union reduce the cost of equity capital?. The accounting review. 85(2). pp. 607-

636.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting. Economy

and Society. 43(2). pp. 260-284.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision, Tool,

Or Threat?. Routledge.

8

Oler, D.K., Oler, M.J. and Skousen, C.J., 2010. Characterizing accounting research. Accounting

Horizons. 24(4). pp. 635-670.

Rutherford, B.A., 2010. The social scientific turn in UK financial accounting research: a

philosophical and sociological analysis. Accounting and Business Research. 40(2). pp. 149-

171.

Song, C.J., Thomas, W.B. and Yi, H., 2010. Value relevance of FAS No. 157 fair value hierarchy

information and the impact of corporate governance mechanisms. The Accounting Review.

85(4). pp. 1375-1410.

Uyar, A. and Gungormus, A.H., 2016. Factors associated with student performance in financial

accounting course. European Journal of Economic and Political Studies. 4(2). pp. 141-156.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

Online

Accounting- Need And Importance. 2016. [Online]. Available through:

<http://fareedsiddiqui.expertscolumn.com/article/accounting-need-and-importance>.

[Accessed on 6th August, 2016].

Laidre, A., 2016. The Importance of Financial Ratios. [Online]. Available through:

<http://www.iplanner.net/business-financial/online/how-to-articles.aspx?

article_id=financial-ratios >. [Accessed on 6th August, 2016].

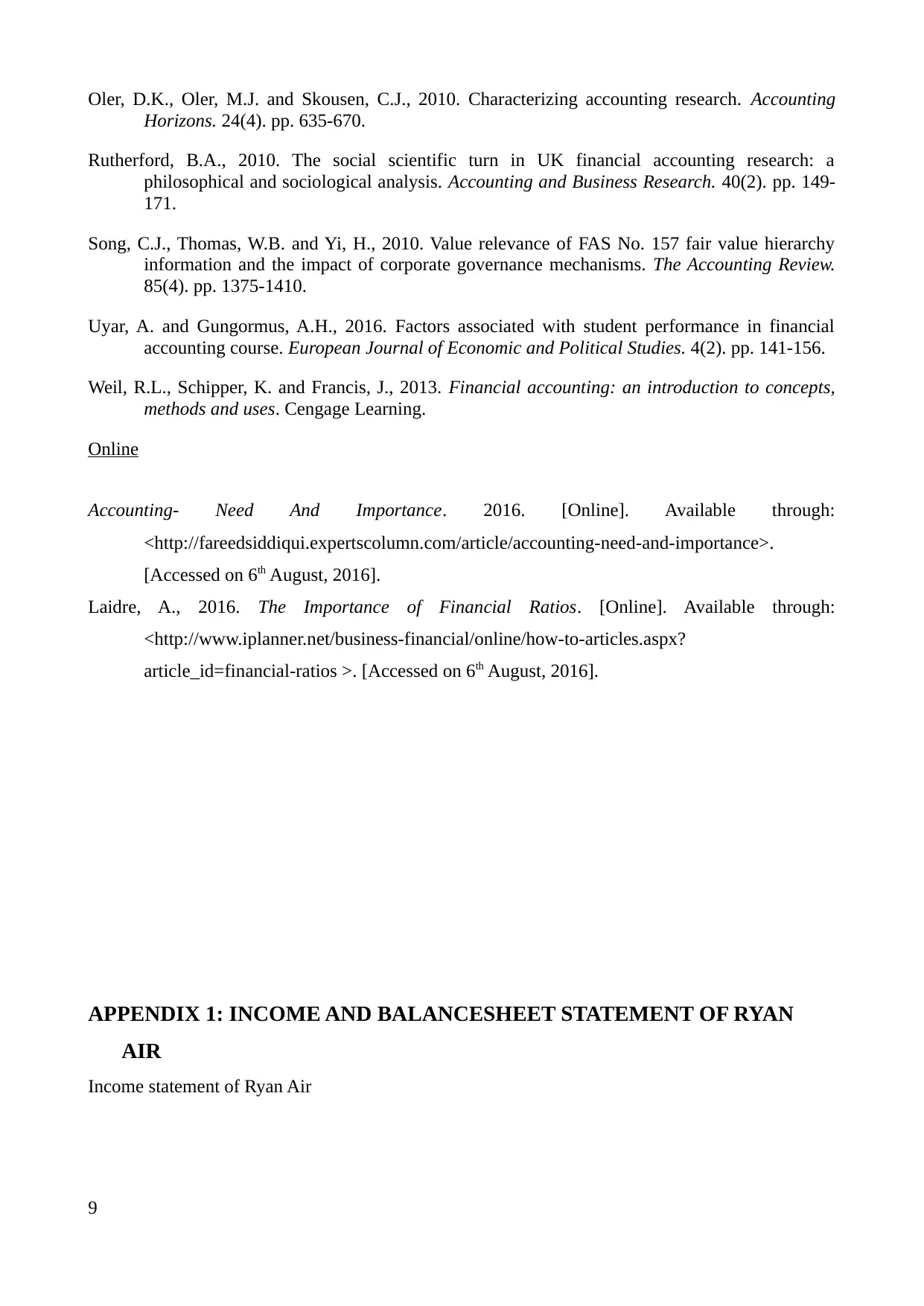

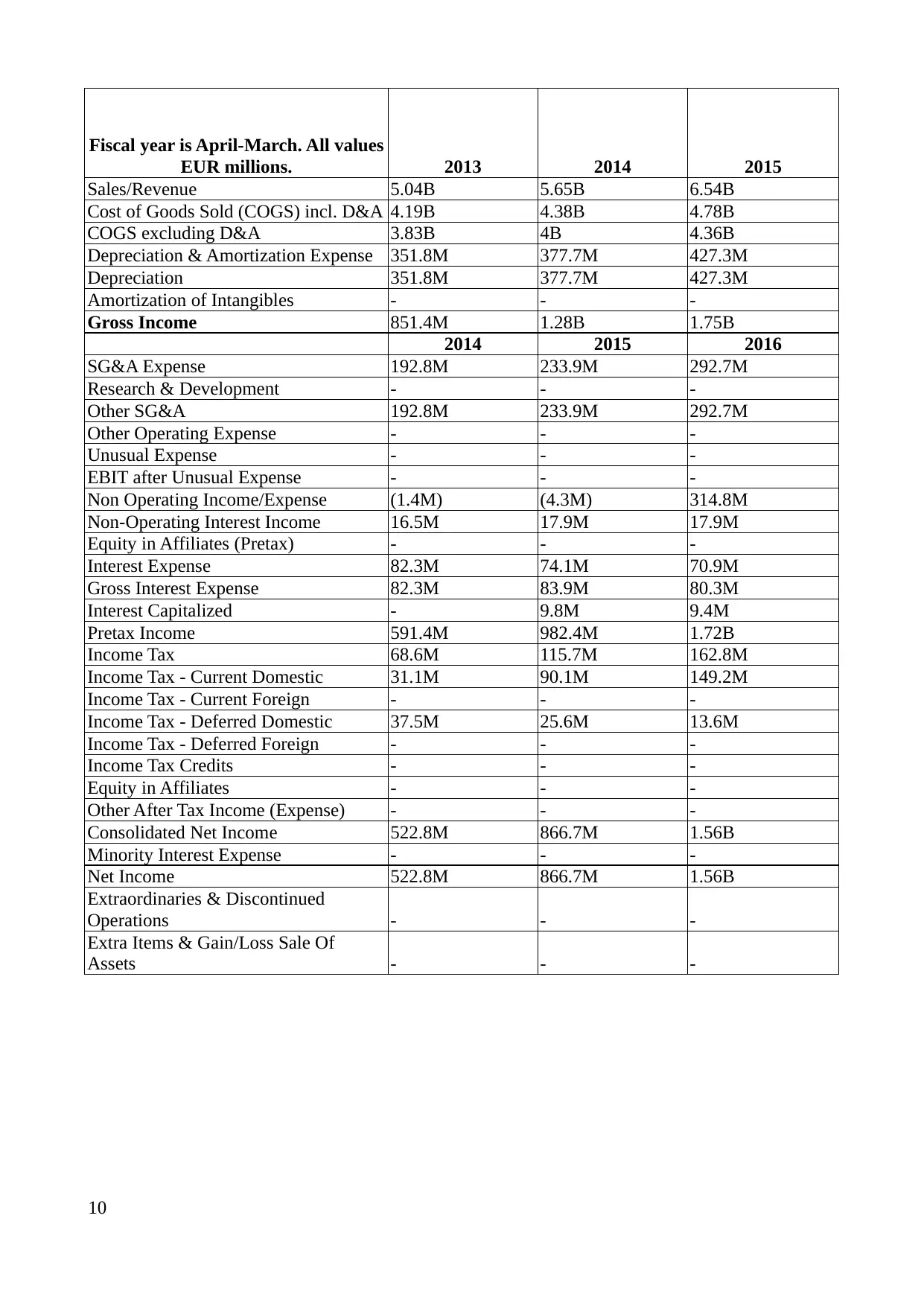

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF RYAN

AIR

Income statement of Ryan Air

9

Horizons. 24(4). pp. 635-670.

Rutherford, B.A., 2010. The social scientific turn in UK financial accounting research: a

philosophical and sociological analysis. Accounting and Business Research. 40(2). pp. 149-

171.

Song, C.J., Thomas, W.B. and Yi, H., 2010. Value relevance of FAS No. 157 fair value hierarchy

information and the impact of corporate governance mechanisms. The Accounting Review.

85(4). pp. 1375-1410.

Uyar, A. and Gungormus, A.H., 2016. Factors associated with student performance in financial

accounting course. European Journal of Economic and Political Studies. 4(2). pp. 141-156.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to concepts,

methods and uses. Cengage Learning.

Online

Accounting- Need And Importance. 2016. [Online]. Available through:

<http://fareedsiddiqui.expertscolumn.com/article/accounting-need-and-importance>.

[Accessed on 6th August, 2016].

Laidre, A., 2016. The Importance of Financial Ratios. [Online]. Available through:

<http://www.iplanner.net/business-financial/online/how-to-articles.aspx?

article_id=financial-ratios >. [Accessed on 6th August, 2016].

APPENDIX 1: INCOME AND BALANCESHEET STATEMENT OF RYAN

AIR

Income statement of Ryan Air

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fiscal year is April-March. All values

EUR millions. 2013 2014 2015

Sales/Revenue 5.04B 5.65B 6.54B

Cost of Goods Sold (COGS) incl. D&A 4.19B 4.38B 4.78B

COGS excluding D&A 3.83B 4B 4.36B

Depreciation & Amortization Expense 351.8M 377.7M 427.3M

Depreciation 351.8M 377.7M 427.3M

Amortization of Intangibles - - -

Gross Income 851.4M 1.28B 1.75B

2014 2015 2016

SG&A Expense 192.8M 233.9M 292.7M

Research & Development - - -

Other SG&A 192.8M 233.9M 292.7M

Other Operating Expense - - -

Unusual Expense - - -

EBIT after Unusual Expense - - -

Non Operating Income/Expense (1.4M) (4.3M) 314.8M

Non-Operating Interest Income 16.5M 17.9M 17.9M

Equity in Affiliates (Pretax) - - -

Interest Expense 82.3M 74.1M 70.9M

Gross Interest Expense 82.3M 83.9M 80.3M

Interest Capitalized - 9.8M 9.4M

Pretax Income 591.4M 982.4M 1.72B

Income Tax 68.6M 115.7M 162.8M

Income Tax - Current Domestic 31.1M 90.1M 149.2M

Income Tax - Current Foreign - - -

Income Tax - Deferred Domestic 37.5M 25.6M 13.6M

Income Tax - Deferred Foreign - - -

Income Tax Credits - - -

Equity in Affiliates - - -

Other After Tax Income (Expense) - - -

Consolidated Net Income 522.8M 866.7M 1.56B

Minority Interest Expense - - -

Net Income 522.8M 866.7M 1.56B

Extraordinaries & Discontinued

Operations - - -

Extra Items & Gain/Loss Sale Of

Assets - - -

10

EUR millions. 2013 2014 2015

Sales/Revenue 5.04B 5.65B 6.54B

Cost of Goods Sold (COGS) incl. D&A 4.19B 4.38B 4.78B

COGS excluding D&A 3.83B 4B 4.36B

Depreciation & Amortization Expense 351.8M 377.7M 427.3M

Depreciation 351.8M 377.7M 427.3M

Amortization of Intangibles - - -

Gross Income 851.4M 1.28B 1.75B

2014 2015 2016

SG&A Expense 192.8M 233.9M 292.7M

Research & Development - - -

Other SG&A 192.8M 233.9M 292.7M

Other Operating Expense - - -

Unusual Expense - - -

EBIT after Unusual Expense - - -

Non Operating Income/Expense (1.4M) (4.3M) 314.8M

Non-Operating Interest Income 16.5M 17.9M 17.9M

Equity in Affiliates (Pretax) - - -

Interest Expense 82.3M 74.1M 70.9M

Gross Interest Expense 82.3M 83.9M 80.3M

Interest Capitalized - 9.8M 9.4M

Pretax Income 591.4M 982.4M 1.72B

Income Tax 68.6M 115.7M 162.8M

Income Tax - Current Domestic 31.1M 90.1M 149.2M

Income Tax - Current Foreign - - -

Income Tax - Deferred Domestic 37.5M 25.6M 13.6M

Income Tax - Deferred Foreign - - -

Income Tax Credits - - -

Equity in Affiliates - - -

Other After Tax Income (Expense) - - -

Consolidated Net Income 522.8M 866.7M 1.56B

Minority Interest Expense - - -

Net Income 522.8M 866.7M 1.56B

Extraordinaries & Discontinued

Operations - - -

Extra Items & Gain/Loss Sale Of

Assets - - -

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cumulative Effect - Accounting Chg - - -

Discontinued Operations - - -

Net Income After Extraordinaries 522.8M 866.7M 1.56B

Preferred Dividends - - -

Net Income Available to Common 522.8M 866.7M 1.56B

EPS (Basic) 0.38 0.64 1.16

Basic Shares Outstanding 1.38B 1.35B 1.34B

EPS (Diluted) 0.38 0.64 1.16

Diluted Shares Outstanding 1.38B 1.35B 1.35B

EBITDA 1.01B 1.42B 1.89B

Balance sheet of Ryan Air

Assets

Fiscal year is April-March. All values

EUR millions. 2013 2014 2015

Cash & Short Term Investments 3.64B 3.26B 5.54B

Cash Only 1.27B 1.74B 1.19B

Short-Term Investments 2.37B 1.52B 4.35B

Total Accounts Receivable 58.9M 61.8M 65.7M

Accounts Receivables, Net 56.1M 58.1M 60.1M

Accounts Receivables, Gross 56.2M 58.2M 60.2M

Bad Debt/Doubtful Accounts -10000 -100000 -100000

Other Receivables 2.8M 3.7M 5.6M

Inventories 2.7M 2.5M 2.1M

Finished Goods - - -

Work in Progress - - -

Raw Materials - 2.5M 2.1M

Progress Payments & Other - - -

Other Current Assets 64.9M 121.6M 133.9M

Miscellaneous Current Assets - - -

Total Current Assets 3.76B 3.44B 5.74B

2013 2014 2015

Net Property, Plant & Equipment 4.91B 5.06B 5.47B

Property, Plant & Equipment - Gross 6.53B 6.95B 7.68B

Buildings 58.8M 67.3M 67.4M

Land & Improvements - - -

11

Discontinued Operations - - -

Net Income After Extraordinaries 522.8M 866.7M 1.56B

Preferred Dividends - - -

Net Income Available to Common 522.8M 866.7M 1.56B

EPS (Basic) 0.38 0.64 1.16

Basic Shares Outstanding 1.38B 1.35B 1.34B

EPS (Diluted) 0.38 0.64 1.16

Diluted Shares Outstanding 1.38B 1.35B 1.35B

EBITDA 1.01B 1.42B 1.89B

Balance sheet of Ryan Air

Assets

Fiscal year is April-March. All values

EUR millions. 2013 2014 2015

Cash & Short Term Investments 3.64B 3.26B 5.54B

Cash Only 1.27B 1.74B 1.19B

Short-Term Investments 2.37B 1.52B 4.35B

Total Accounts Receivable 58.9M 61.8M 65.7M

Accounts Receivables, Net 56.1M 58.1M 60.1M

Accounts Receivables, Gross 56.2M 58.2M 60.2M

Bad Debt/Doubtful Accounts -10000 -100000 -100000

Other Receivables 2.8M 3.7M 5.6M

Inventories 2.7M 2.5M 2.1M

Finished Goods - - -

Work in Progress - - -

Raw Materials - 2.5M 2.1M

Progress Payments & Other - - -

Other Current Assets 64.9M 121.6M 133.9M

Miscellaneous Current Assets - - -

Total Current Assets 3.76B 3.44B 5.74B

2013 2014 2015

Net Property, Plant & Equipment 4.91B 5.06B 5.47B

Property, Plant & Equipment - Gross 6.53B 6.95B 7.68B

Buildings 58.8M 67.3M 67.4M

Land & Improvements - - -

11

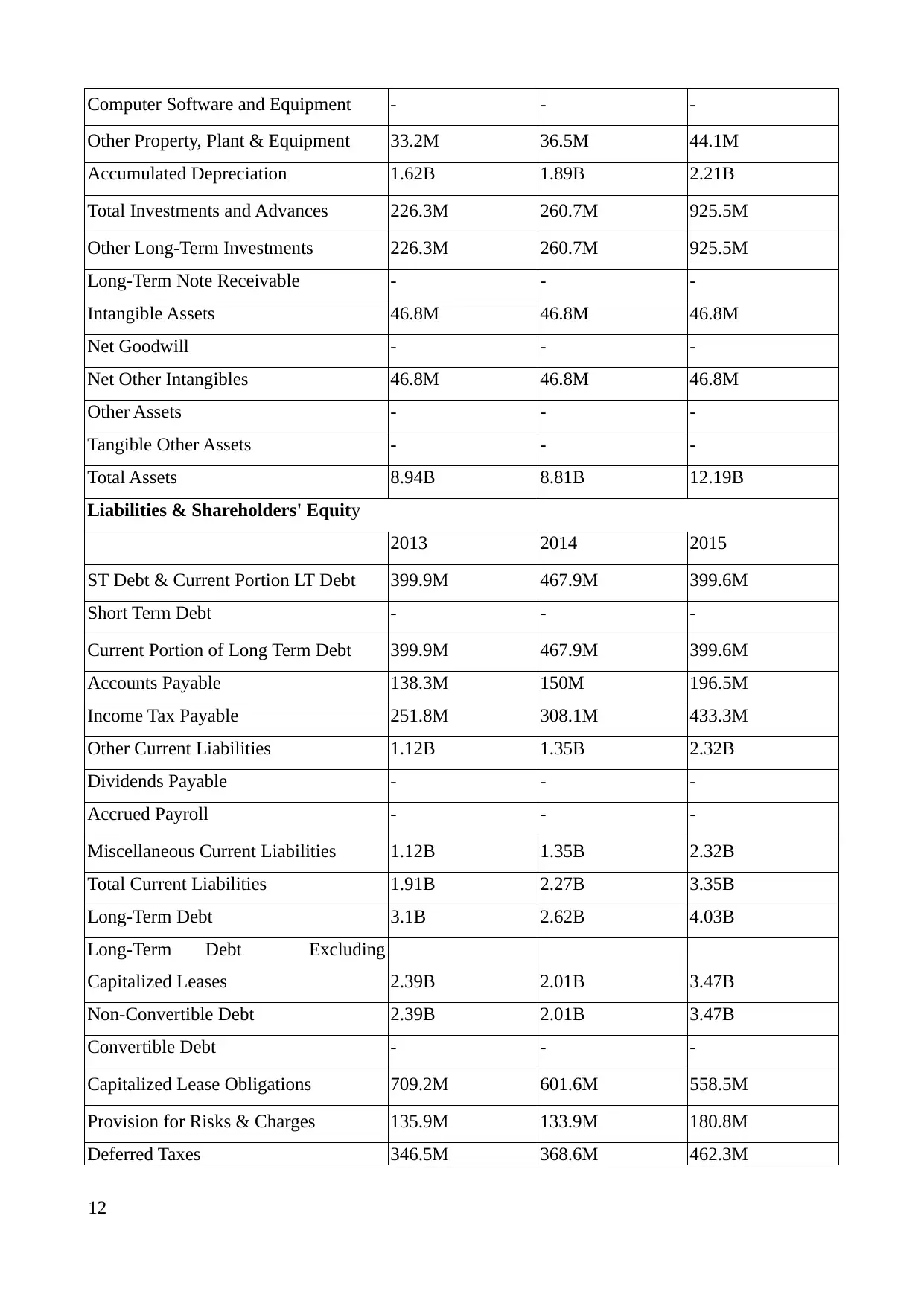

Computer Software and Equipment - - -

Other Property, Plant & Equipment 33.2M 36.5M 44.1M

Accumulated Depreciation 1.62B 1.89B 2.21B

Total Investments and Advances 226.3M 260.7M 925.5M

Other Long-Term Investments 226.3M 260.7M 925.5M

Long-Term Note Receivable - - -

Intangible Assets 46.8M 46.8M 46.8M

Net Goodwill - - -

Net Other Intangibles 46.8M 46.8M 46.8M

Other Assets - - -

Tangible Other Assets - - -

Total Assets 8.94B 8.81B 12.19B

Liabilities & Shareholders' Equity

2013 2014 2015

ST Debt & Current Portion LT Debt 399.9M 467.9M 399.6M

Short Term Debt - - -

Current Portion of Long Term Debt 399.9M 467.9M 399.6M

Accounts Payable 138.3M 150M 196.5M

Income Tax Payable 251.8M 308.1M 433.3M

Other Current Liabilities 1.12B 1.35B 2.32B

Dividends Payable - - -

Accrued Payroll - - -

Miscellaneous Current Liabilities 1.12B 1.35B 2.32B

Total Current Liabilities 1.91B 2.27B 3.35B

Long-Term Debt 3.1B 2.62B 4.03B

Long-Term Debt Excluding

Capitalized Leases 2.39B 2.01B 3.47B

Non-Convertible Debt 2.39B 2.01B 3.47B

Convertible Debt - - -

Capitalized Lease Obligations 709.2M 601.6M 558.5M

Provision for Risks & Charges 135.9M 133.9M 180.8M

Deferred Taxes 346.5M 368.6M 462.3M

12

Other Property, Plant & Equipment 33.2M 36.5M 44.1M

Accumulated Depreciation 1.62B 1.89B 2.21B

Total Investments and Advances 226.3M 260.7M 925.5M

Other Long-Term Investments 226.3M 260.7M 925.5M

Long-Term Note Receivable - - -

Intangible Assets 46.8M 46.8M 46.8M

Net Goodwill - - -

Net Other Intangibles 46.8M 46.8M 46.8M

Other Assets - - -

Tangible Other Assets - - -

Total Assets 8.94B 8.81B 12.19B

Liabilities & Shareholders' Equity

2013 2014 2015

ST Debt & Current Portion LT Debt 399.9M 467.9M 399.6M

Short Term Debt - - -

Current Portion of Long Term Debt 399.9M 467.9M 399.6M

Accounts Payable 138.3M 150M 196.5M

Income Tax Payable 251.8M 308.1M 433.3M

Other Current Liabilities 1.12B 1.35B 2.32B

Dividends Payable - - -

Accrued Payroll - - -

Miscellaneous Current Liabilities 1.12B 1.35B 2.32B

Total Current Liabilities 1.91B 2.27B 3.35B

Long-Term Debt 3.1B 2.62B 4.03B

Long-Term Debt Excluding

Capitalized Leases 2.39B 2.01B 3.47B

Non-Convertible Debt 2.39B 2.01B 3.47B

Convertible Debt - - -

Capitalized Lease Obligations 709.2M 601.6M 558.5M

Provision for Risks & Charges 135.9M 133.9M 180.8M

Deferred Taxes 346.5M 368.6M 462.3M

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.