Financial Accounting Assignment: Statement Analysis and Theory

VerifiedAdded on 2020/04/21

|12

|1606

|71

Homework Assignment

AI Summary

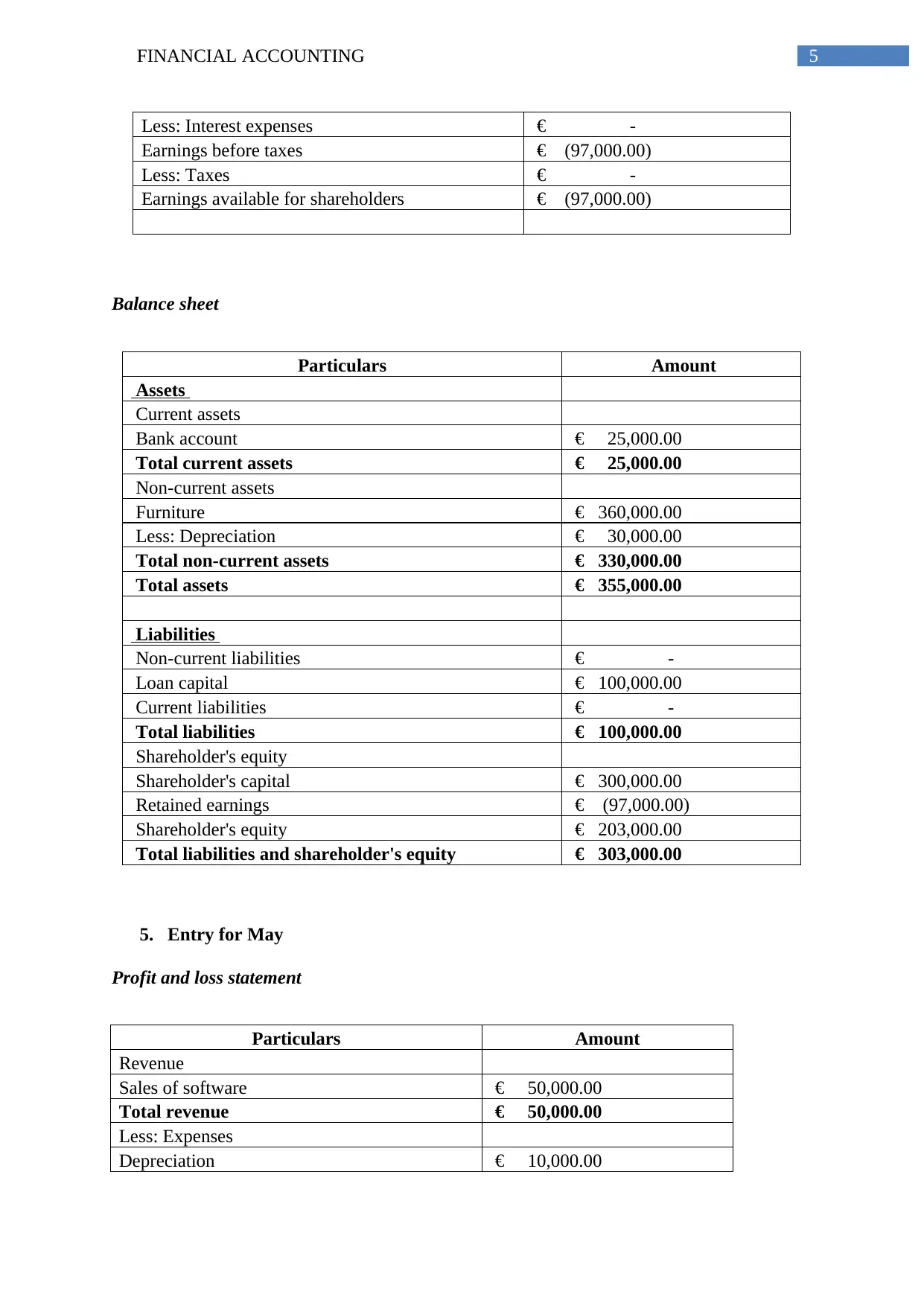

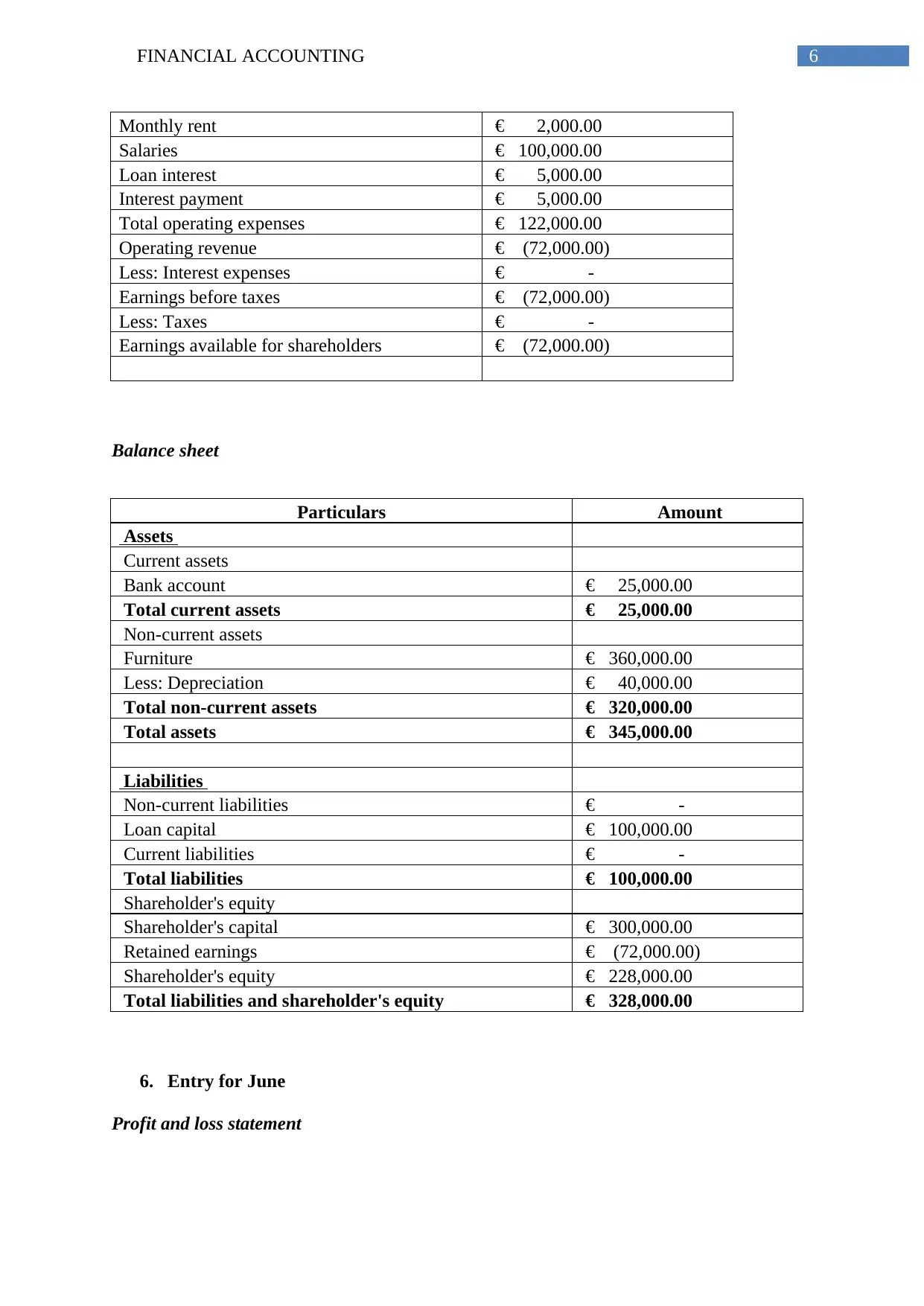

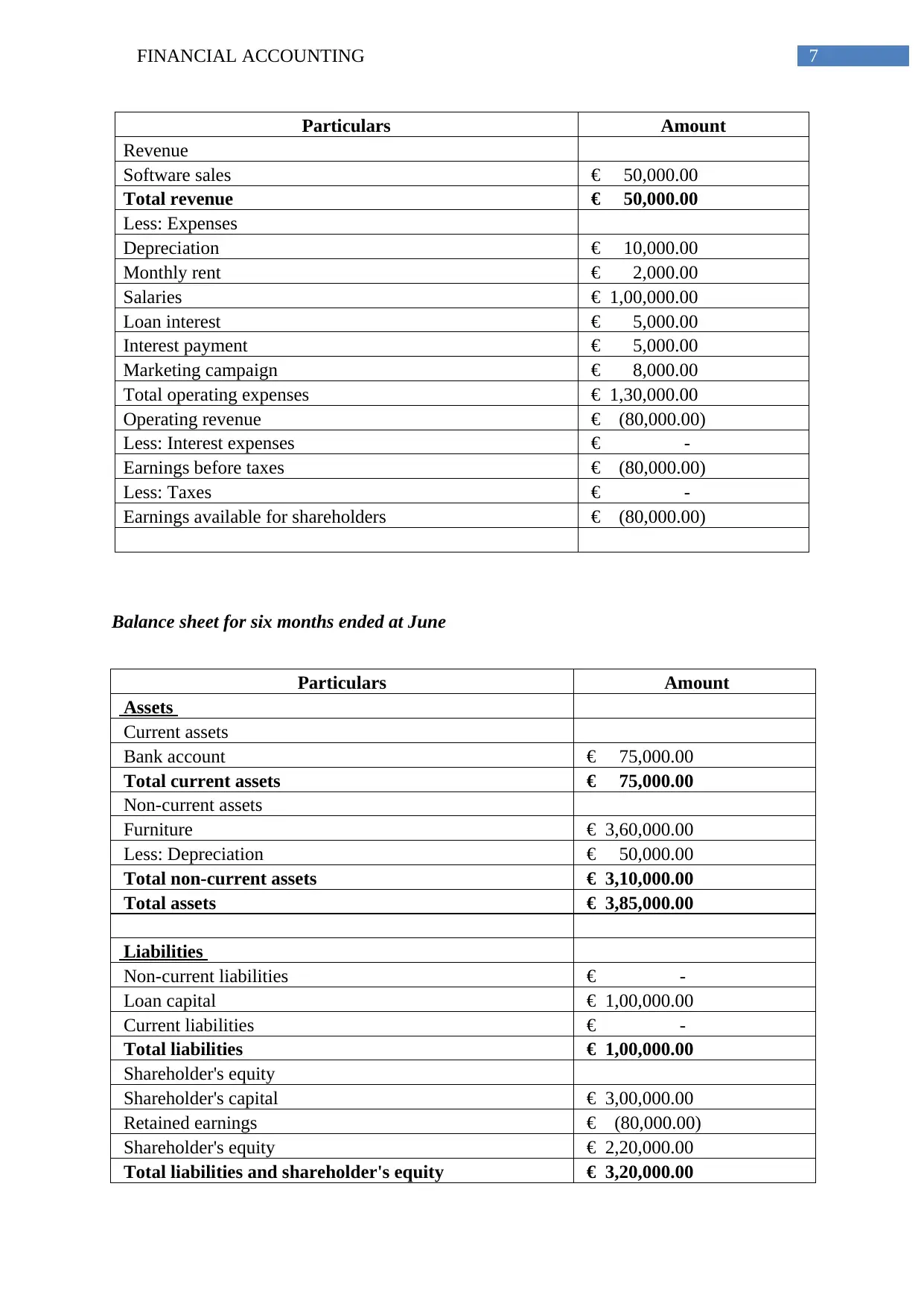

This financial accounting assignment provides a comprehensive analysis of financial statements and related accounting theory. The assignment includes detailed entries for a company's financial transactions from January to June, covering profit and loss statements and balance sheets for each month. The solution demonstrates the calculation of revenue, expenses, and profits, along with the presentation of assets, liabilities, and shareholder's equity. In addition to the practical exercises, the assignment also includes a theoretical section defining financial accounting, explaining the components of financial statements like balance sheets, income statements, and cash flow statements, and differentiating between profit, revenue, and cash. The assignment is a valuable resource for students studying financial accounting and is available on Desklib, a platform that provides AI-based study tools.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.