Financial Accounting: Share Capital, Tax, and Asset Revaluation

VerifiedAdded on 2023/06/04

|13

|893

|106

Homework Assignment

AI Summary

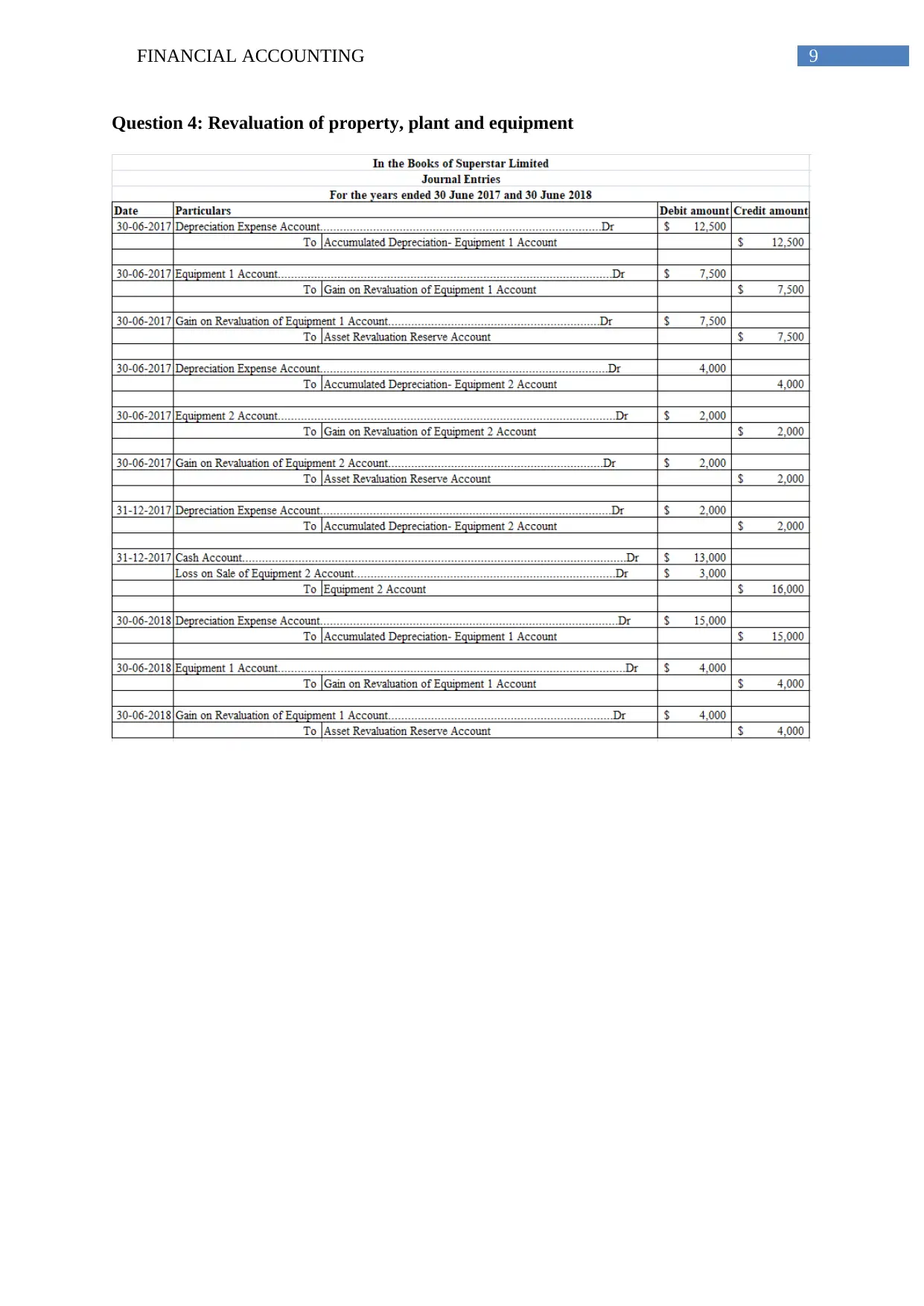

This assignment solution delves into various aspects of financial accounting, addressing key concepts and their practical applications. It covers financial statement disclosures as per AASB standards, including changes in accounting estimates and non-adjusting events. The solution also provides a detailed analysis of accounting for share capital, including forfeiture and reissuance. Furthermore, it examines the accounting treatment for income tax, deferred tax assets, and liabilities. The revaluation of property, plant, and equipment is discussed, along with the impairment of assets and relevant accounting entries. This document, contributed by a student and available on Desklib, serves as a valuable resource for students seeking to understand and apply these complex accounting principles, with Desklib providing additional AI-powered study tools and resources.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.