ACC514 Financial Accounting: Superstore & Rippa Ltd Detailed Analysis

VerifiedAdded on 2023/06/07

|15

|2527

|144

Homework Assignment

AI Summary

This assignment provides comprehensive solutions to several financial accounting problems. It addresses changes in accounting estimates for Superstore Ltd, including revisions to equipment depreciation and corrections of errors related to unpaid invoices and misclassified expenses. It also covers the accounting treatment for declines in share prices. Furthermore, the assignment includes journal entries and analysis for Rippa Ltd's share issuance, forfeiture, and re-issuance. It presents a detailed worksheet for current and deferred tax liabilities/refundable amounts. Additionally, the assignment provides journal entries for asset revaluation and sale, as well as impairment loss calculations and allocation for Foodie Ltd, demonstrating a thorough understanding of various accounting principles and standards. Desklib offers a range of solved assignments and past papers to support students in their studies.

Running head: ADVANCE FINANCIAL ACCOUNTING

Advance Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Advance Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Assignment 3...................................................................................................................................2

Question 1....................................................................................................................................2

Part 1........................................................................................................................................2

Part 2........................................................................................................................................2

Part 3........................................................................................................................................3

Part 4........................................................................................................................................3

Question 2....................................................................................................................................4

Requirement i:.........................................................................................................................4

Requirement ii.........................................................................................................................6

Question 3:...................................................................................................................................7

Requirement 1:.........................................................................................................................7

Requirement ii:........................................................................................................................9

Question 4:...................................................................................................................................9

Question 5:.................................................................................................................................11

Reference.......................................................................................................................................13

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Assignment 3...................................................................................................................................2

Question 1....................................................................................................................................2

Part 1........................................................................................................................................2

Part 2........................................................................................................................................2

Part 3........................................................................................................................................3

Part 4........................................................................................................................................3

Question 2....................................................................................................................................4

Requirement i:.........................................................................................................................4

Requirement ii.........................................................................................................................6

Question 3:...................................................................................................................................7

Requirement 1:.........................................................................................................................7

Requirement ii:........................................................................................................................9

Question 4:...................................................................................................................................9

Question 5:.................................................................................................................................11

Reference.......................................................................................................................................13

2

ADVANCE FINANCIAL ACCOUNTING

Assignment 3

Question 1

Part 1

As per the case which is provided in the question, on the basis of accounting information

available to the directors of Superstore ltd, the decision of the management is to revise the useful

life of a manufacturing equipment. The equipment is to be depreciated on a straight-line basis as

per the policy of the management. Due to the change in the useful life of the equipment the same

will be treated as a change in accounting estimate of the business. As per International

Accounting Standard 8, para 36 states that any change in accounting estimate is to be considered

prospectively which means that the transaction will affect the current period and also future

period if the change relates to the same (Capkun, Collins & Jeanjean, 2016). Therefore, the

director needs to calculate the revised depreciation amount on the basis of the new useful life of

the assets and apply the change prospectively (Barbu et al., 2014). The director does not need to

make changes in the financial statements of 2016 or 2017. In the current year the directors need

to change the depreciation amount and also makes changes to balance sheet of the business as

per the revision.

Part 2

As per the case which is provided, the accountable payable officer identified that

Superstore ltd has not paid an invoice of $ 20,000 which is related to repair expenses on

equipment. The management of the company needs to make changes in the financial statements

for the year 2018. Due to the inclusion of repair expenses, the business will be getting a refund of

taxes for the year (Das, 2013). In this situation, the management of the company needs to pass

adjustment entries in order to make appropriate changes in the financial statements of the

ADVANCE FINANCIAL ACCOUNTING

Assignment 3

Question 1

Part 1

As per the case which is provided in the question, on the basis of accounting information

available to the directors of Superstore ltd, the decision of the management is to revise the useful

life of a manufacturing equipment. The equipment is to be depreciated on a straight-line basis as

per the policy of the management. Due to the change in the useful life of the equipment the same

will be treated as a change in accounting estimate of the business. As per International

Accounting Standard 8, para 36 states that any change in accounting estimate is to be considered

prospectively which means that the transaction will affect the current period and also future

period if the change relates to the same (Capkun, Collins & Jeanjean, 2016). Therefore, the

director needs to calculate the revised depreciation amount on the basis of the new useful life of

the assets and apply the change prospectively (Barbu et al., 2014). The director does not need to

make changes in the financial statements of 2016 or 2017. In the current year the directors need

to change the depreciation amount and also makes changes to balance sheet of the business as

per the revision.

Part 2

As per the case which is provided, the accountable payable officer identified that

Superstore ltd has not paid an invoice of $ 20,000 which is related to repair expenses on

equipment. The management of the company needs to make changes in the financial statements

for the year 2018. Due to the inclusion of repair expenses, the business will be getting a refund of

taxes for the year (Das, 2013). In this situation, the management of the company needs to pass

adjustment entries in order to make appropriate changes in the financial statements of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCE FINANCIAL ACCOUNTING

business. The journal entry which is required by the management to make necessary adjustment

are shown below:

Retained Earnings A/c……………………………Dr 14,000

Deferred Tax Assets A/c…………………………Dr 6,000

To Account Payable A/c 20,000

(Being Adjustment entry passed)

Part 3

As per the case which is provided in the question, the share prices of ABC ltd which was

held by Superstore ltd declined sharply in 2018. The share price of ABC ltd was recognized to be

$ 6,00,000 in 30th June and the same declined tremendously to $ 2,50,000 in 10th July 2018. The

management needs to make necessary changes in the financial statements in order to make the

presentation accurate. The management will be passing the following journal entry

Unrealized Holding Loss A/c……………………………Dr 3,50,000

To Shares in ABC ltd 3,50,000

(Being loss recorded)

Part 4

As per the case which is provided in question, the accountant of Superstore ltd has

wrongly recorded expenses which the accountant has used for personal purposes has been

recorded as advertisement expenses. The management of the company needs to investigate the

fraudulent activity which is undertaken by the management. The management also needs to make

ADVANCE FINANCIAL ACCOUNTING

business. The journal entry which is required by the management to make necessary adjustment

are shown below:

Retained Earnings A/c……………………………Dr 14,000

Deferred Tax Assets A/c…………………………Dr 6,000

To Account Payable A/c 20,000

(Being Adjustment entry passed)

Part 3

As per the case which is provided in the question, the share prices of ABC ltd which was

held by Superstore ltd declined sharply in 2018. The share price of ABC ltd was recognized to be

$ 6,00,000 in 30th June and the same declined tremendously to $ 2,50,000 in 10th July 2018. The

management needs to make necessary changes in the financial statements in order to make the

presentation accurate. The management will be passing the following journal entry

Unrealized Holding Loss A/c……………………………Dr 3,50,000

To Shares in ABC ltd 3,50,000

(Being loss recorded)

Part 4

As per the case which is provided in question, the accountant of Superstore ltd has

wrongly recorded expenses which the accountant has used for personal purposes has been

recorded as advertisement expenses. The management of the company needs to investigate the

fraudulent activity which is undertaken by the management. The management also needs to make

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCE FINANCIAL ACCOUNTING

changes to the journal entry which is recorded in the annual report of the business. The journal

entry which is needed to be passed is shown below

Cash A/c …………………………………………………Dr $ 32,000

To Advertisement A/c $ 32,000

(Being wrong entry reversed)

Advertisement A/c ………………………………..……….Dr $ 32,000

To Max A/c $

32,000

(Adjustment Entry Passed)

ADVANCE FINANCIAL ACCOUNTING

changes to the journal entry which is recorded in the annual report of the business. The journal

entry which is needed to be passed is shown below

Cash A/c …………………………………………………Dr $ 32,000

To Advertisement A/c $ 32,000

(Being wrong entry reversed)

Advertisement A/c ………………………………..……….Dr $ 32,000

To Max A/c $

32,000

(Adjustment Entry Passed)

5

ADVANCE FINANCIAL ACCOUNTING

Question 2

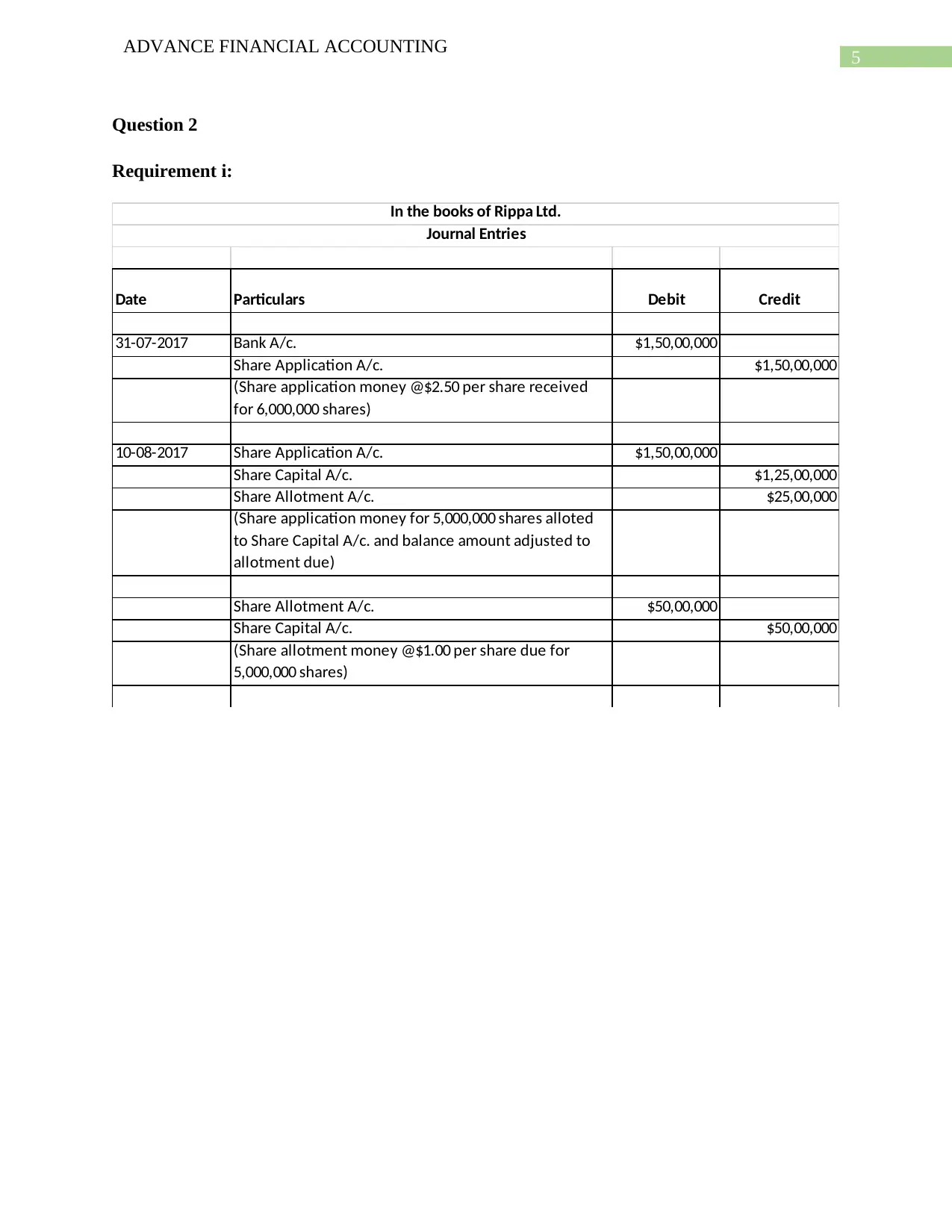

Requirement i:

Date Particulars Debit Credit

31-07-2017 Bank A/c. $1,50,00,000

Share Application A/c. $1,50,00,000

(Share application money @$2.50 per share received

for 6,000,000 shares)

10-08-2017 Share Application A/c. $1,50,00,000

Share Capital A/c. $1,25,00,000

Share Allotment A/c. $25,00,000

(Share application money for 5,000,000 shares alloted

to Share Capital A/c. and balance amount adjusted to

allotment due)

Share Allotment A/c. $50,00,000

Share Capital A/c. $50,00,000

(Share allotment money @$1.00 per share due for

5,000,000 shares)

In the books of Rippa Ltd.

Journal Entries

ADVANCE FINANCIAL ACCOUNTING

Question 2

Requirement i:

Date Particulars Debit Credit

31-07-2017 Bank A/c. $1,50,00,000

Share Application A/c. $1,50,00,000

(Share application money @$2.50 per share received

for 6,000,000 shares)

10-08-2017 Share Application A/c. $1,50,00,000

Share Capital A/c. $1,25,00,000

Share Allotment A/c. $25,00,000

(Share application money for 5,000,000 shares alloted

to Share Capital A/c. and balance amount adjusted to

allotment due)

Share Allotment A/c. $50,00,000

Share Capital A/c. $50,00,000

(Share allotment money @$1.00 per share due for

5,000,000 shares)

In the books of Rippa Ltd.

Journal Entries

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

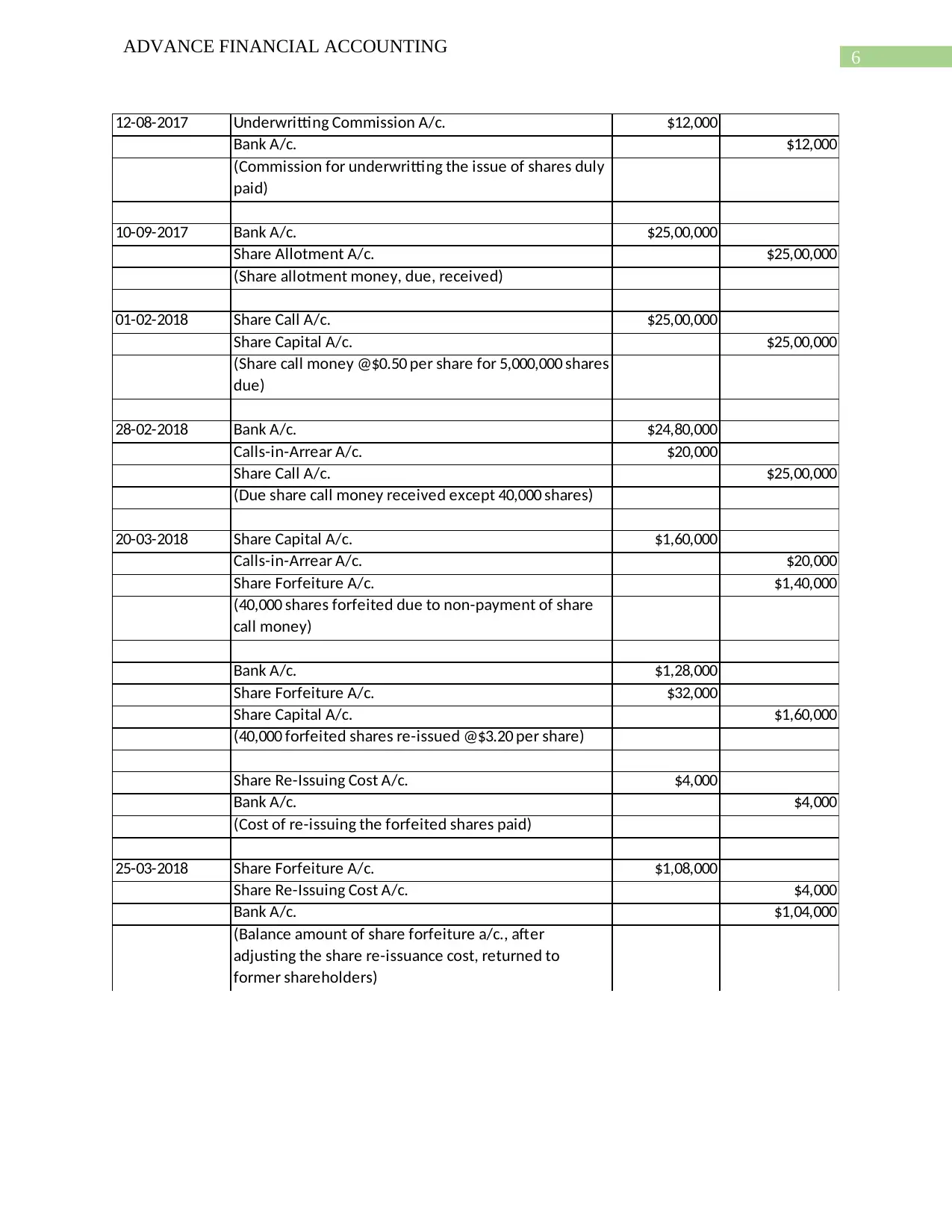

ADVANCE FINANCIAL ACCOUNTING

12-08-2017 Underwritting Commission A/c. $12,000

Bank A/c. $12,000

(Commission for underwritting the issue of shares duly

paid)

10-09-2017 Bank A/c. $25,00,000

Share Allotment A/c. $25,00,000

(Share allotment money, due, received)

01-02-2018 Share Call A/c. $25,00,000

Share Capital A/c. $25,00,000

(Share call money @$0.50 per share for 5,000,000 shares

due)

28-02-2018 Bank A/c. $24,80,000

Calls-in-Arrear A/c. $20,000

Share Call A/c. $25,00,000

(Due share call money received except 40,000 shares)

20-03-2018 Share Capital A/c. $1,60,000

Calls-in-Arrear A/c. $20,000

Share Forfeiture A/c. $1,40,000

(40,000 shares forfeited due to non-payment of share

call money)

Bank A/c. $1,28,000

Share Forfeiture A/c. $32,000

Share Capital A/c. $1,60,000

(40,000 forfeited shares re-issued @$3.20 per share)

Share Re-Issuing Cost A/c. $4,000

Bank A/c. $4,000

(Cost of re-issuing the forfeited shares paid)

25-03-2018 Share Forfeiture A/c. $1,08,000

Share Re-Issuing Cost A/c. $4,000

Bank A/c. $1,04,000

(Balance amount of share forfeiture a/c., after

adjusting the share re-issuance cost, returned to

former shareholders)

ADVANCE FINANCIAL ACCOUNTING

12-08-2017 Underwritting Commission A/c. $12,000

Bank A/c. $12,000

(Commission for underwritting the issue of shares duly

paid)

10-09-2017 Bank A/c. $25,00,000

Share Allotment A/c. $25,00,000

(Share allotment money, due, received)

01-02-2018 Share Call A/c. $25,00,000

Share Capital A/c. $25,00,000

(Share call money @$0.50 per share for 5,000,000 shares

due)

28-02-2018 Bank A/c. $24,80,000

Calls-in-Arrear A/c. $20,000

Share Call A/c. $25,00,000

(Due share call money received except 40,000 shares)

20-03-2018 Share Capital A/c. $1,60,000

Calls-in-Arrear A/c. $20,000

Share Forfeiture A/c. $1,40,000

(40,000 shares forfeited due to non-payment of share

call money)

Bank A/c. $1,28,000

Share Forfeiture A/c. $32,000

Share Capital A/c. $1,60,000

(40,000 forfeited shares re-issued @$3.20 per share)

Share Re-Issuing Cost A/c. $4,000

Bank A/c. $4,000

(Cost of re-issuing the forfeited shares paid)

25-03-2018 Share Forfeiture A/c. $1,08,000

Share Re-Issuing Cost A/c. $4,000

Bank A/c. $1,04,000

(Balance amount of share forfeiture a/c., after

adjusting the share re-issuance cost, returned to

former shareholders)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCE FINANCIAL ACCOUNTING

Requirement ii

As per the case, one of the shareholders of Rippa Ltd whose shares was forfeited due to

non-payment of call money has received lesser amount for the shares held instead of $ 3.50

which is made up of application and allotment money. The management has incurred expenses

which is related to issue of forfeited shares and cost of forfeiture which is undertaken by the

management. The company has to incur such expenses due to the fault of the shareholder and

therefore such cost is also transferred to the shareholder as it is reduced from the share money

which is to be refunded to the shareholder. The management had to sell the forfeited shares at $

3.20 per share for the share which originally was valued at $ 4 per share. In addition to this, the

management also incurs $ 4,000 on reissue of shares which is the main reason the money

refunded to the shareholders are lower than what the shareholder originally paid for the share.

ADVANCE FINANCIAL ACCOUNTING

Requirement ii

As per the case, one of the shareholders of Rippa Ltd whose shares was forfeited due to

non-payment of call money has received lesser amount for the shares held instead of $ 3.50

which is made up of application and allotment money. The management has incurred expenses

which is related to issue of forfeited shares and cost of forfeiture which is undertaken by the

management. The company has to incur such expenses due to the fault of the shareholder and

therefore such cost is also transferred to the shareholder as it is reduced from the share money

which is to be refunded to the shareholder. The management had to sell the forfeited shares at $

3.20 per share for the share which originally was valued at $ 4 per share. In addition to this, the

management also incurs $ 4,000 on reissue of shares which is the main reason the money

refunded to the shareholders are lower than what the shareholder originally paid for the share.

8

ADVANCE FINANCIAL ACCOUNTING

Question 3:

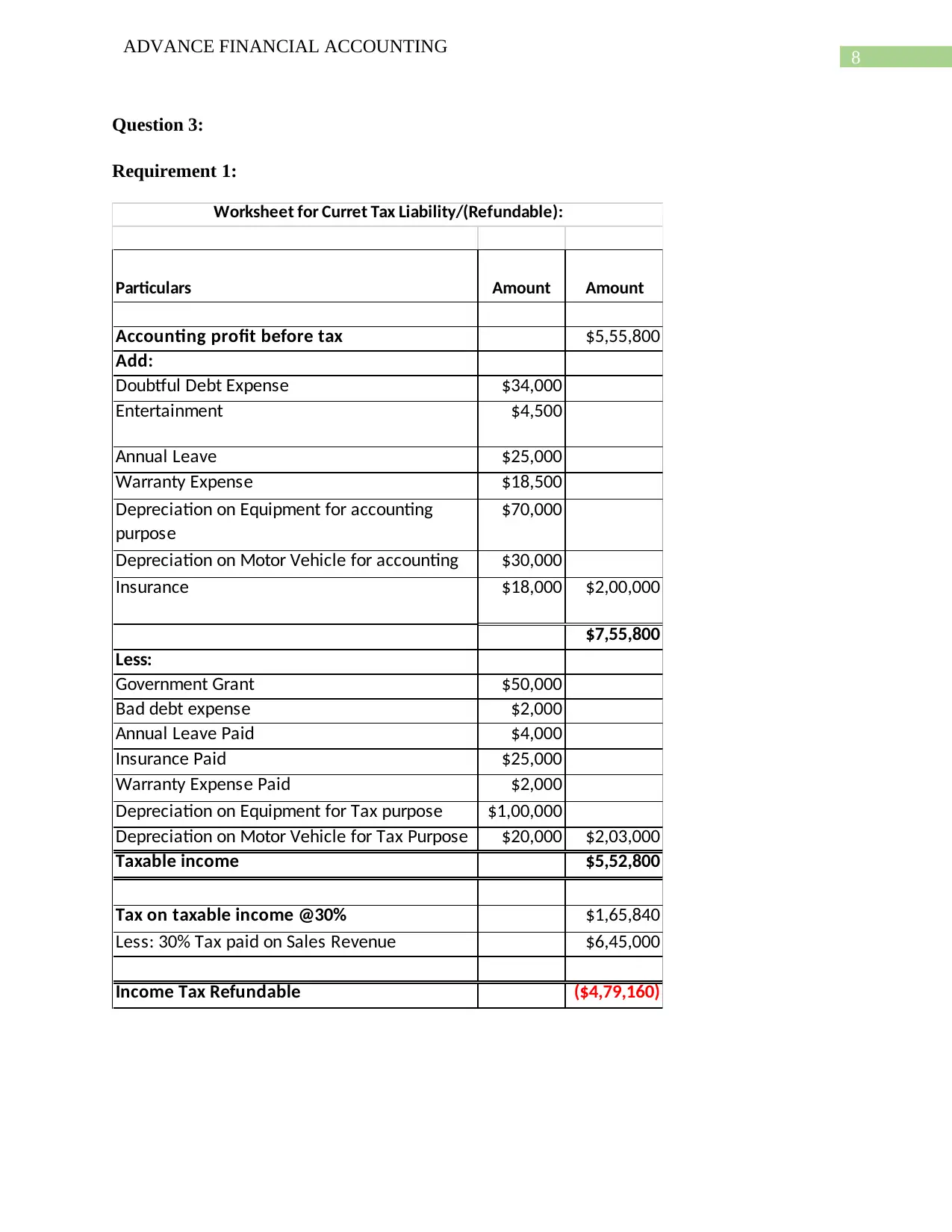

Requirement 1:

Particulars Amount Amount

Accounting profit before tax $5,55,800

Add:

Doubtful Debt Expense $34,000

Entertainment $4,500

Annual Leave $25,000

Warranty Expense $18,500

Depreciation on Equipment for accounting

purpose

$70,000

Depreciation on Motor Vehicle for accounting

purpose

$30,000

Insurance $18,000 $2,00,000

$7,55,800

Less:

Government Grant $50,000

Bad debt expense $2,000

Annual Leave Paid $4,000

Insurance Paid $25,000

Warranty Expense Paid $2,000

Depreciation on Equipment for Tax purpose $1,00,000

Depreciation on Motor Vehicle for Tax Purpose $20,000 $2,03,000

Taxable income $5,52,800

Tax on taxable income @30% $1,65,840

Less: 30% Tax paid on Sales Revenue $6,45,000

Income Tax Refundable ($4,79,160)

Worksheet for Curret Tax Liability/(Refundable):

ADVANCE FINANCIAL ACCOUNTING

Question 3:

Requirement 1:

Particulars Amount Amount

Accounting profit before tax $5,55,800

Add:

Doubtful Debt Expense $34,000

Entertainment $4,500

Annual Leave $25,000

Warranty Expense $18,500

Depreciation on Equipment for accounting

purpose

$70,000

Depreciation on Motor Vehicle for accounting

purpose

$30,000

Insurance $18,000 $2,00,000

$7,55,800

Less:

Government Grant $50,000

Bad debt expense $2,000

Annual Leave Paid $4,000

Insurance Paid $25,000

Warranty Expense Paid $2,000

Depreciation on Equipment for Tax purpose $1,00,000

Depreciation on Motor Vehicle for Tax Purpose $20,000 $2,03,000

Taxable income $5,52,800

Tax on taxable income @30% $1,65,840

Less: 30% Tax paid on Sales Revenue $6,45,000

Income Tax Refundable ($4,79,160)

Worksheet for Curret Tax Liability/(Refundable):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

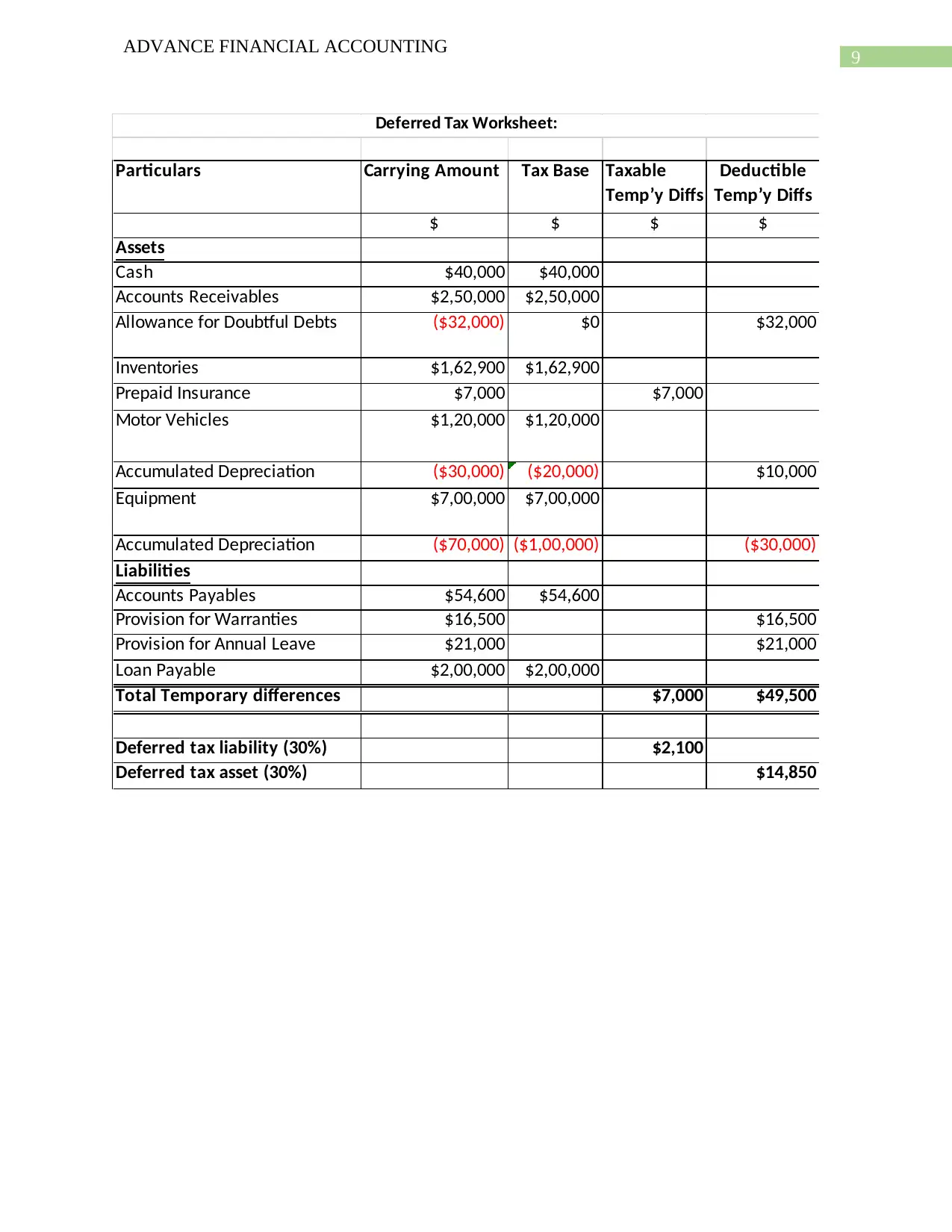

ADVANCE FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $40,000 $40,000

Accounts Receivables $2,50,000 $2,50,000

Allowance for Doubtful Debts ($32,000) $0 $32,000

Inventories $1,62,900 $1,62,900

Prepaid Insurance $7,000 $7,000

Motor Vehicles $1,20,000 $1,20,000

Accumulated Depreciation ($30,000) ($20,000) $10,000

Equipment $7,00,000 $7,00,000

Accumulated Depreciation ($70,000) ($1,00,000) ($30,000)

Liabilities

Accounts Payables $54,600 $54,600

Provision for Warranties $16,500 $16,500

Provision for Annual Leave $21,000 $21,000

Loan Payable $2,00,000 $2,00,000

Total Temporary differences $7,000 $49,500

Deferred tax liability (30%) $2,100

Deferred tax asset (30%) $14,850

Deferred Tax Worksheet:

ADVANCE FINANCIAL ACCOUNTING

Particulars Carrying Amount Tax Base Taxable

Temp’y Diffs

Deductible

Temp’y Diffs

$ $ $ $

Assets

Cash $40,000 $40,000

Accounts Receivables $2,50,000 $2,50,000

Allowance for Doubtful Debts ($32,000) $0 $32,000

Inventories $1,62,900 $1,62,900

Prepaid Insurance $7,000 $7,000

Motor Vehicles $1,20,000 $1,20,000

Accumulated Depreciation ($30,000) ($20,000) $10,000

Equipment $7,00,000 $7,00,000

Accumulated Depreciation ($70,000) ($1,00,000) ($30,000)

Liabilities

Accounts Payables $54,600 $54,600

Provision for Warranties $16,500 $16,500

Provision for Annual Leave $21,000 $21,000

Loan Payable $2,00,000 $2,00,000

Total Temporary differences $7,000 $49,500

Deferred tax liability (30%) $2,100

Deferred tax asset (30%) $14,850

Deferred Tax Worksheet:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCE FINANCIAL ACCOUNTING

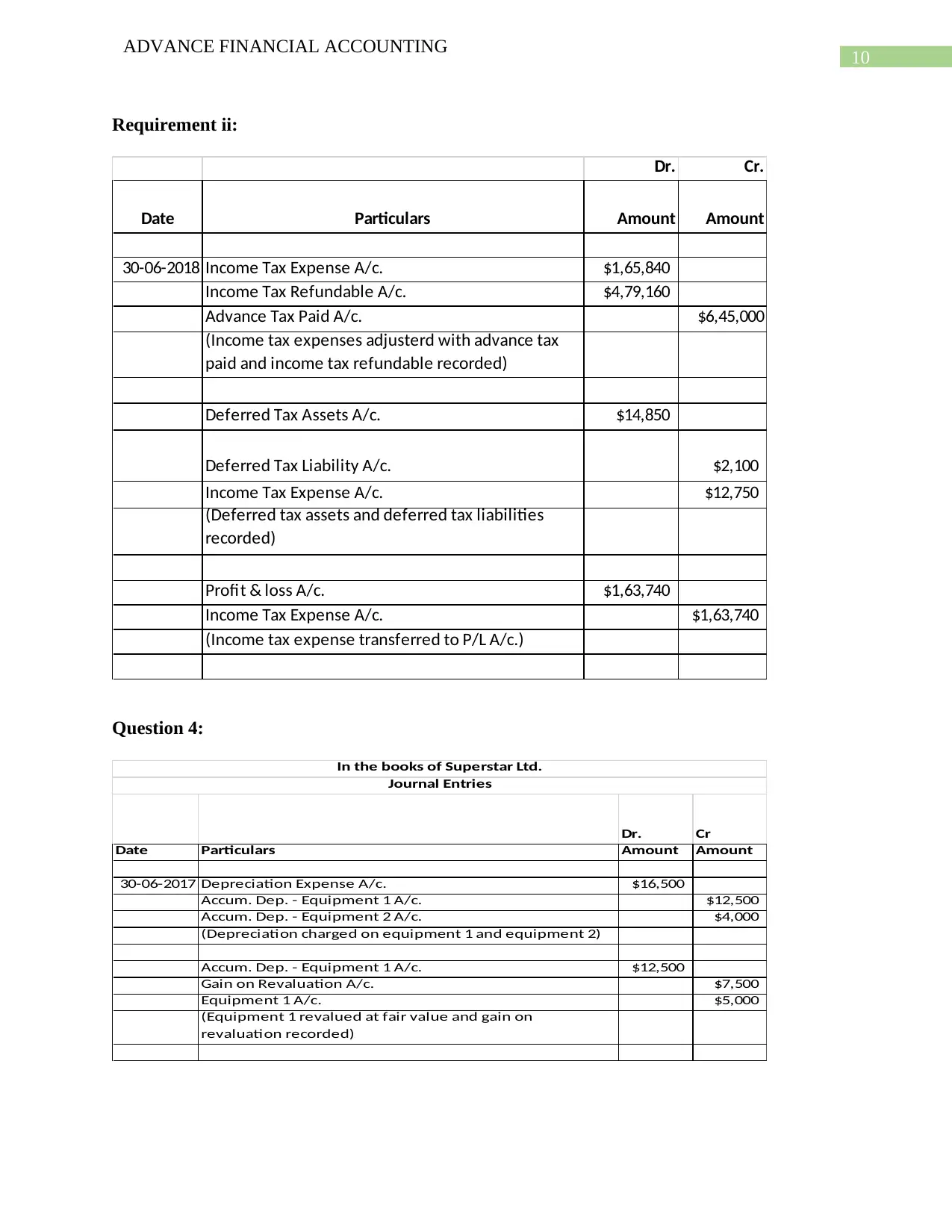

Requirement ii:

Dr. Cr.

Date Particulars Amount Amount

30-06-2018 Income Tax Expense A/c. $1,65,840

Income Tax Refundable A/c. $4,79,160

Advance Tax Paid A/c. $6,45,000

(Income tax expenses adjusterd with advance tax

paid and income tax refundable recorded)

Deferred Tax Assets A/c. $14,850

Deferred Tax Liability A/c. $2,100

Income Tax Expense A/c. $12,750

(Deferred tax assets and deferred tax liabilities

recorded)

Profit & loss A/c. $1,63,740

Income Tax Expense A/c. $1,63,740

(Income tax expense transferred to P/L A/c.)

Question 4:

Dr. Cr

Date Particulars Amount Amount

30-06-2017 Depreciation Expense A/c. $16,500

Accum. Dep. - Equipment 1 A/c. $12,500

Accum. Dep. - Equipment 2 A/c. $4,000

(Depreciation charged on equipment 1 and equipment 2)

Accum. Dep. - Equipment 1 A/c. $12,500

Gain on Revaluation A/c. $7,500

Equipment 1 A/c. $5,000

(Equipment 1 revalued at fair value and gain on

revaluation recorded)

Journal Entries

In the books of Superstar Ltd.

ADVANCE FINANCIAL ACCOUNTING

Requirement ii:

Dr. Cr.

Date Particulars Amount Amount

30-06-2018 Income Tax Expense A/c. $1,65,840

Income Tax Refundable A/c. $4,79,160

Advance Tax Paid A/c. $6,45,000

(Income tax expenses adjusterd with advance tax

paid and income tax refundable recorded)

Deferred Tax Assets A/c. $14,850

Deferred Tax Liability A/c. $2,100

Income Tax Expense A/c. $12,750

(Deferred tax assets and deferred tax liabilities

recorded)

Profit & loss A/c. $1,63,740

Income Tax Expense A/c. $1,63,740

(Income tax expense transferred to P/L A/c.)

Question 4:

Dr. Cr

Date Particulars Amount Amount

30-06-2017 Depreciation Expense A/c. $16,500

Accum. Dep. - Equipment 1 A/c. $12,500

Accum. Dep. - Equipment 2 A/c. $4,000

(Depreciation charged on equipment 1 and equipment 2)

Accum. Dep. - Equipment 1 A/c. $12,500

Gain on Revaluation A/c. $7,500

Equipment 1 A/c. $5,000

(Equipment 1 revalued at fair value and gain on

revaluation recorded)

Journal Entries

In the books of Superstar Ltd.

11

ADVANCE FINANCIAL ACCOUNTING

Accum. Dep. - Equipment 2 A/c. $4,000

Gain on Revaluation A/c. $2,000

Equipment 2 A/c. $2,000

(Equipment 2 revalued at fair value and gain on

revaluation recorded)

Gain on Revaluation A/c. $9,500

Asset Revaluation Reserve A/c. $9,500

(Gain on revaluation transferred to asset revaluation

reserve)

Deferred Tax Assets A/c. $3,450

Income Tax Expense A/c. $3,450

(Deferred tax recorded for the asset revaluation)

31-12-2017 Depreciation Expense A/c. $2,000

Accum. Dep. - Equipment 2 A/c. $2,000

(Depreciation charged on Equipment 2)

Bank A/c. $13,000

Accum. Dep. - Equipment 2 A/c. $2,000

Loss on Sale of Assets A/c. $3,000

Equipment 2 A/c. $18,000

(Equipment 2 sold at loss)

30-06-2018 Depreciation Expense A/c. $15,000

Accum. Dep. - Equipment 1 A/c. $15,000

(Depreciation charged on equipment 1)

Accum. Dep. - Equipment 1 A/c. $15,000

Gain on Revaluation A/c. $4,000

Equipment 1 A/c. $11,000

(Equipment 1 revalued at fair value and gain on

revaluation recorded)

Deferred Tax Assets A/c. $1,200

Income Tax Expense A/c. $1,200

(Deferred tax recorded for the asset revaluation)

Gain on Revaluation A/c. $4,000

Asset Revaluation Reserve A/c. $4,000

(Gain on revaluation transferred to asset revaluation

reserve)

ADVANCE FINANCIAL ACCOUNTING

Accum. Dep. - Equipment 2 A/c. $4,000

Gain on Revaluation A/c. $2,000

Equipment 2 A/c. $2,000

(Equipment 2 revalued at fair value and gain on

revaluation recorded)

Gain on Revaluation A/c. $9,500

Asset Revaluation Reserve A/c. $9,500

(Gain on revaluation transferred to asset revaluation

reserve)

Deferred Tax Assets A/c. $3,450

Income Tax Expense A/c. $3,450

(Deferred tax recorded for the asset revaluation)

31-12-2017 Depreciation Expense A/c. $2,000

Accum. Dep. - Equipment 2 A/c. $2,000

(Depreciation charged on Equipment 2)

Bank A/c. $13,000

Accum. Dep. - Equipment 2 A/c. $2,000

Loss on Sale of Assets A/c. $3,000

Equipment 2 A/c. $18,000

(Equipment 2 sold at loss)

30-06-2018 Depreciation Expense A/c. $15,000

Accum. Dep. - Equipment 1 A/c. $15,000

(Depreciation charged on equipment 1)

Accum. Dep. - Equipment 1 A/c. $15,000

Gain on Revaluation A/c. $4,000

Equipment 1 A/c. $11,000

(Equipment 1 revalued at fair value and gain on

revaluation recorded)

Deferred Tax Assets A/c. $1,200

Income Tax Expense A/c. $1,200

(Deferred tax recorded for the asset revaluation)

Gain on Revaluation A/c. $4,000

Asset Revaluation Reserve A/c. $4,000

(Gain on revaluation transferred to asset revaluation

reserve)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.