ACC210 - Financial Accounting Task 2 Major Assignment, 2017

VerifiedAdded on 2020/03/16

|12

|2331

|82

Homework Assignment

AI Summary

This document presents a comprehensive solution for ACC210 Financial Accounting Task 2, focusing on key accounting concepts and standards. The assignment addresses four main questions: asset valuation under AASB 13 and AASB 116, including the determination of fair value, market, and valuation techniques for land and buildings; journal entries related to plant, property, and equipment (PPE), including depreciation, revaluation, and impairment losses; the accounting treatment of intangible assets, contrasting internally generated and acquired intangibles, with an analysis of the reasons for reluctance in accounting changes; and the accounting for employee benefits, specifically the calculation and reconciliation of a net defined benefit liability, including interest costs, income, and journal entries. The solution provides detailed calculations, accounting justifications, and relevant journal entries, demonstrating a strong understanding of financial accounting principles and standards.

ACC210 - Financial Accounting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. Ex 3.1..................................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Determine subject of measurement..........................................................................................3

2. Determine valuation premise/method......................................................................................3

3. Determine market.....................................................................................................................3

4. Determine Valuation technique.................................................................................................3

Question 2. Ex 5.18................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:.......................................................4

2. Calculations & General Journal Entries 1/8/18:.........................................................................4

3. Calculations & General Journal Entries 30/6/18:.......................................................................4

Question 3. Ex 6.11................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Explain accounting issues...........................................................................................................5

2. Differences Internally Generated vs Acquired...........................................................................5

3. Reasons for Reluctance..............................................................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 12

Question 1. Ex 3.1..................................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Determine subject of measurement..........................................................................................3

2. Determine valuation premise/method......................................................................................3

3. Determine market.....................................................................................................................3

4. Determine Valuation technique.................................................................................................3

Question 2. Ex 5.18................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:.......................................................4

2. Calculations & General Journal Entries 1/8/18:.........................................................................4

3. Calculations & General Journal Entries 30/6/18:.......................................................................4

Question 3. Ex 6.11................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Explain accounting issues...........................................................................................................5

2. Differences Internally Generated vs Acquired...........................................................................5

3. Reasons for Reluctance..............................................................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 12

Question 1. Ex 3.1

Accounting Justification:

AASB 13 deals with the provision relating to fair valuation of assets (AASB 13. Fair Value

Measurement. (2016). ASB 116 provides -specification relating to Plant , Property and

Equipment. Para 7-10 provides specification relating to recognition and provision relating to

initial cost and subsequent cost of Property, Plant and Equipment.

Relevant Issues:

In present case Maple own a factory and land on which the factory stands. Due to boom in

prices of residential property the price of land also increased as it is also part of residential

property. Thus in present scenario Para 7-10 of AASB 116 has been applied in order to

ascertain the value on which land and building should be recognized in books of accounts of

Maple Ltd.

1. Determine subject of measurement

In present case the measurement of land and office building situated on same is to be made

which was demolished and reconstructed. The valuation of building will be done after

assessing the fact that whether future economic cost of the asset can be reliably measured

or not. All the cost which is associated with the construction or incidental to renovation of

asset will be included in part of cost of asset. Further, any cost which is related to day to day

expenditure which does not enhance the quality or capability will not be included in cost of

asset.

2. Determine valuation premise/method

The asset of Maple Ltd in present scenario i.e. office building and land will be fairly valued

and recognized in books of accounts at revalue amount reduced by accumulated

depreciation and any impairment loss of asset. It is necessary for every entity to value their

asset at the end of reporting period to sure that carried value of asset is not higher in

comparison to its recoverable value (Basu and Andrews, 2014) .

3. Determine market

As per views of Zakaria and et.al. (2014) fair value of an asset is the value which is available

in the market between two parties having will to sell or buy the asset. In case if any asset is

acquired on lease than depreciation is required to be allocated on it on a fair basis. AASB

116 specifies the following disclosures to be necessarily provided relating to Plant, Property

and Equipment i.e. amount relating to contractual obligations which are due and required to

be paid in order to acquire the asset; value of expenses which are being provided in carrying

value of asset in its construction phase.

4. Determine Valuation technique

Valuation technique has been provided in AASB 116 and valuation of land and office on it will be

conducted in following manner:

Market Value of Land $1000000

Cost relating to demolishing building $1000000

Page 3 of 12

Accounting Justification:

AASB 13 deals with the provision relating to fair valuation of assets (AASB 13. Fair Value

Measurement. (2016). ASB 116 provides -specification relating to Plant , Property and

Equipment. Para 7-10 provides specification relating to recognition and provision relating to

initial cost and subsequent cost of Property, Plant and Equipment.

Relevant Issues:

In present case Maple own a factory and land on which the factory stands. Due to boom in

prices of residential property the price of land also increased as it is also part of residential

property. Thus in present scenario Para 7-10 of AASB 116 has been applied in order to

ascertain the value on which land and building should be recognized in books of accounts of

Maple Ltd.

1. Determine subject of measurement

In present case the measurement of land and office building situated on same is to be made

which was demolished and reconstructed. The valuation of building will be done after

assessing the fact that whether future economic cost of the asset can be reliably measured

or not. All the cost which is associated with the construction or incidental to renovation of

asset will be included in part of cost of asset. Further, any cost which is related to day to day

expenditure which does not enhance the quality or capability will not be included in cost of

asset.

2. Determine valuation premise/method

The asset of Maple Ltd in present scenario i.e. office building and land will be fairly valued

and recognized in books of accounts at revalue amount reduced by accumulated

depreciation and any impairment loss of asset. It is necessary for every entity to value their

asset at the end of reporting period to sure that carried value of asset is not higher in

comparison to its recoverable value (Basu and Andrews, 2014) .

3. Determine market

As per views of Zakaria and et.al. (2014) fair value of an asset is the value which is available

in the market between two parties having will to sell or buy the asset. In case if any asset is

acquired on lease than depreciation is required to be allocated on it on a fair basis. AASB

116 specifies the following disclosures to be necessarily provided relating to Plant, Property

and Equipment i.e. amount relating to contractual obligations which are due and required to

be paid in order to acquire the asset; value of expenses which are being provided in carrying

value of asset in its construction phase.

4. Determine Valuation technique

Valuation technique has been provided in AASB 116 and valuation of land and office on it will be

conducted in following manner:

Market Value of Land $1000000

Cost relating to demolishing building $1000000

Page 3 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of construction $780000

Total cost $2780000

Question 2. Ex 5.18

Accounting Justification:

AASB 116 specifies the provision relating to Plant, Property and Equipment. Para 31-42

provides provision relating to revaluation model to be applied in case of revaluation and

Para 43-49 specifies provision relating to depreciation to be applied to asset (AASB

116.Property Plant and Equipment, 2016).

Relevant Issues:

In present case revaluation of assets are being done at the end of each year and impairment

loss in accordance with specified provision has been applied in order to recognize asset at

appropriate value in books of accounts.

1. Calculations & General Journal Entries 1/7/16 to

30/6/17:

Calculations

Working Note 1

Depreciation

Machine A

Cost of Machine / No .of expected years

$100000/5

=$20000

Machine B

Cost of Machine / No .of expected years

$60000/3

=$20000

Working Note 2

Revaluation Surplus

Machine A

Fair Value – Book Value

$84000- $80000

$4000

Page 4 of 12

Total cost $2780000

Question 2. Ex 5.18

Accounting Justification:

AASB 116 specifies the provision relating to Plant, Property and Equipment. Para 31-42

provides provision relating to revaluation model to be applied in case of revaluation and

Para 43-49 specifies provision relating to depreciation to be applied to asset (AASB

116.Property Plant and Equipment, 2016).

Relevant Issues:

In present case revaluation of assets are being done at the end of each year and impairment

loss in accordance with specified provision has been applied in order to recognize asset at

appropriate value in books of accounts.

1. Calculations & General Journal Entries 1/7/16 to

30/6/17:

Calculations

Working Note 1

Depreciation

Machine A

Cost of Machine / No .of expected years

$100000/5

=$20000

Machine B

Cost of Machine / No .of expected years

$60000/3

=$20000

Working Note 2

Revaluation Surplus

Machine A

Fair Value – Book Value

$84000- $80000

$4000

Page 4 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

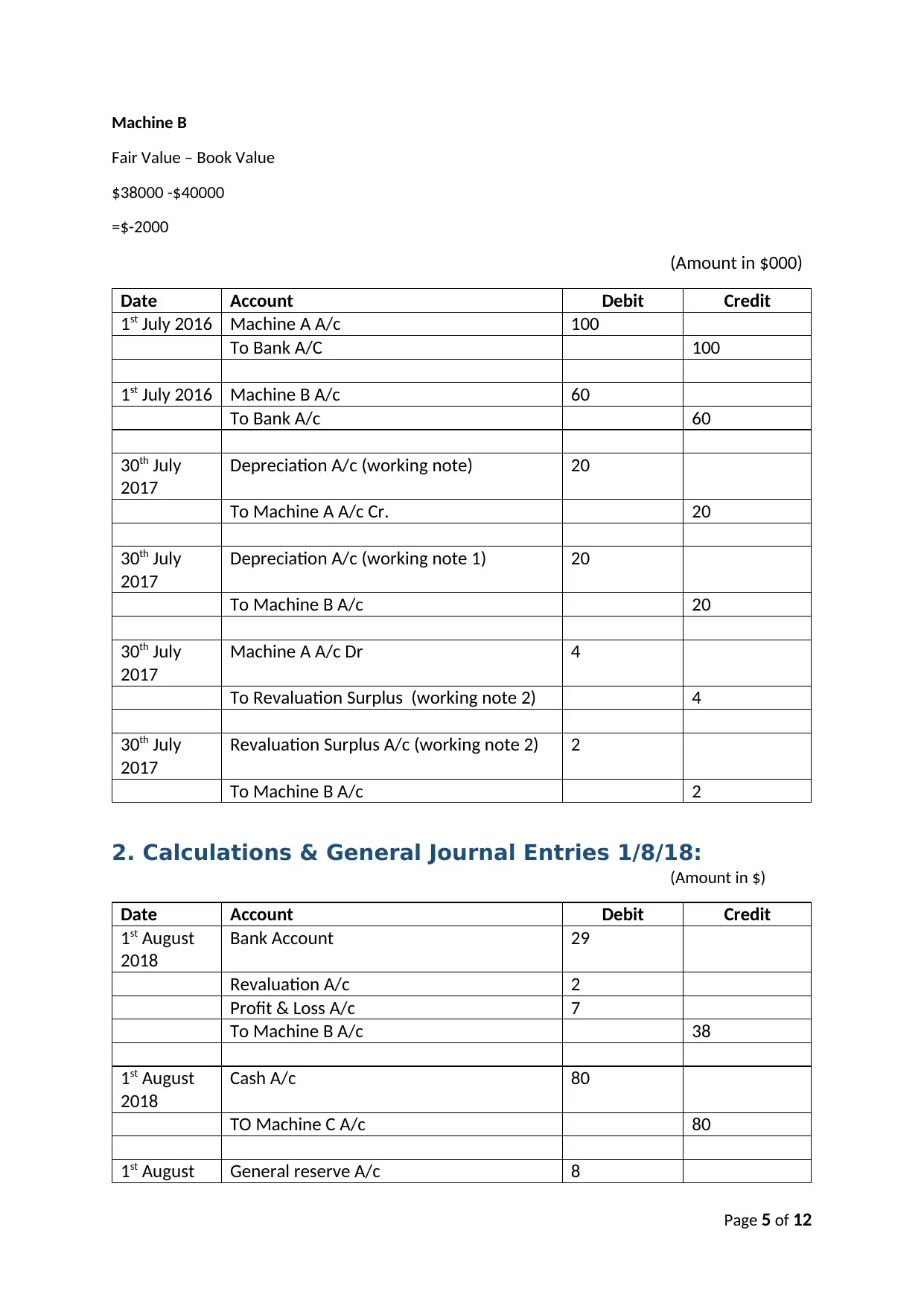

Machine B

Fair Value – Book Value

$38000 -$40000

=$-2000

(Amount in $000)

Date Account Debit Credit

1st July 2016 Machine A A/c 100

To Bank A/C 100

1st July 2016 Machine B A/c 60

To Bank A/c 60

30th July

2017

Depreciation A/c (working note) 20

To Machine A A/c Cr. 20

30th July

2017

Depreciation A/c (working note 1) 20

To Machine B A/c 20

30th July

2017

Machine A A/c Dr 4

To Revaluation Surplus (working note 2) 4

30th July

2017

Revaluation Surplus A/c (working note 2) 2

To Machine B A/c 2

2. Calculations & General Journal Entries 1/8/18:

(Amount in $)

Date Account Debit Credit

1st August

2018

Bank Account 29

Revaluation A/c 2

Profit & Loss A/c 7

To Machine B A/c 38

1st August

2018

Cash A/c 80

TO Machine C A/c 80

1st August General reserve A/c 8

Page 5 of 12

Fair Value – Book Value

$38000 -$40000

=$-2000

(Amount in $000)

Date Account Debit Credit

1st July 2016 Machine A A/c 100

To Bank A/C 100

1st July 2016 Machine B A/c 60

To Bank A/c 60

30th July

2017

Depreciation A/c (working note) 20

To Machine A A/c Cr. 20

30th July

2017

Depreciation A/c (working note 1) 20

To Machine B A/c 20

30th July

2017

Machine A A/c Dr 4

To Revaluation Surplus (working note 2) 4

30th July

2017

Revaluation Surplus A/c (working note 2) 2

To Machine B A/c 2

2. Calculations & General Journal Entries 1/8/18:

(Amount in $)

Date Account Debit Credit

1st August

2018

Bank Account 29

Revaluation A/c 2

Profit & Loss A/c 7

To Machine B A/c 38

1st August

2018

Cash A/c 80

TO Machine C A/c 80

1st August General reserve A/c 8

Page 5 of 12

2018

Revaluation Surplus A/c 2

TO Share Capital A/c 10

2. Calculations & General Journal Entries 30/6/18:

Calculations

Working Note 1

Depreciation

Machine A

Revalue amount / No of remaining years (Davies, 2014)

$84000/ 4

= $21000

Machine C

= $80000/4

= $ 20000 p.a.and the same will be divided by 2

= $10000 for six months

Working Note 2

Impairment loss

Machine A

Fair Value – Carried Value (Capalbo, 2013)

$61000 - $63000 ($84000-$21000)

$2000

Machine C

$68500-$70000 ($80000-$10000)

$ 1500

(Amount in $)

Date Account DR CR

30th June

2018

Depreciation A/c (working note 1) 21

To Machine A A/c 21

Page 6 of 12

Revaluation Surplus A/c 2

TO Share Capital A/c 10

2. Calculations & General Journal Entries 30/6/18:

Calculations

Working Note 1

Depreciation

Machine A

Revalue amount / No of remaining years (Davies, 2014)

$84000/ 4

= $21000

Machine C

= $80000/4

= $ 20000 p.a.and the same will be divided by 2

= $10000 for six months

Working Note 2

Impairment loss

Machine A

Fair Value – Carried Value (Capalbo, 2013)

$61000 - $63000 ($84000-$21000)

$2000

Machine C

$68500-$70000 ($80000-$10000)

$ 1500

(Amount in $)

Date Account DR CR

30th June

2018

Depreciation A/c (working note 1) 21

To Machine A A/c 21

Page 6 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

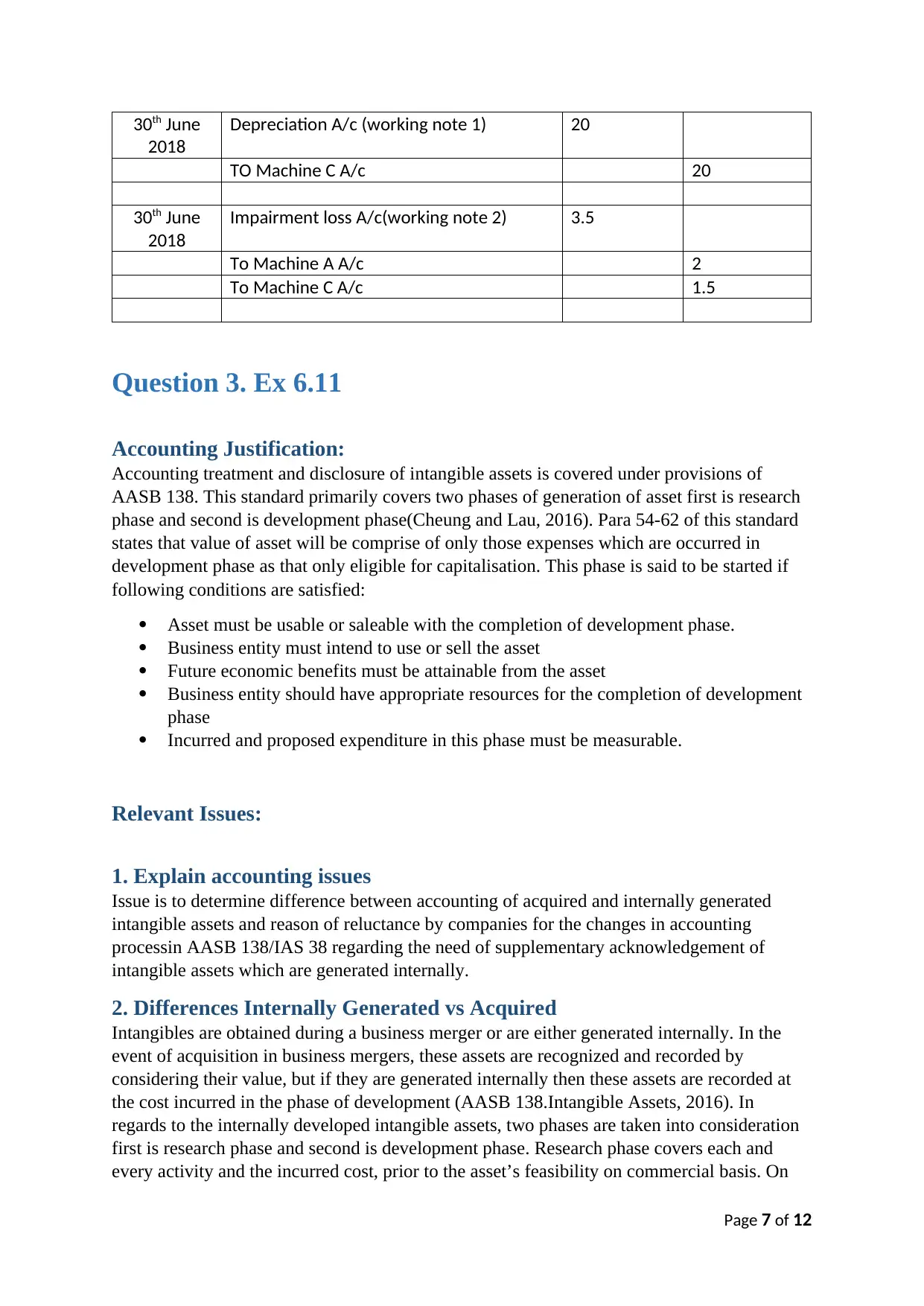

30th June

2018

Depreciation A/c (working note 1) 20

TO Machine C A/c 20

30th June

2018

Impairment loss A/c(working note 2) 3.5

To Machine A A/c 2

To Machine C A/c 1.5

Question 3. Ex 6.11

Accounting Justification:

Accounting treatment and disclosure of intangible assets is covered under provisions of

AASB 138. This standard primarily covers two phases of generation of asset first is research

phase and second is development phase(Cheung and Lau, 2016). Para 54-62 of this standard

states that value of asset will be comprise of only those expenses which are occurred in

development phase as that only eligible for capitalisation. This phase is said to be started if

following conditions are satisfied:

Asset must be usable or saleable with the completion of development phase.

Business entity must intend to use or sell the asset

Future economic benefits must be attainable from the asset

Business entity should have appropriate resources for the completion of development

phase

Incurred and proposed expenditure in this phase must be measurable.

Relevant Issues:

1. Explain accounting issues

Issue is to determine difference between accounting of acquired and internally generated

intangible assets and reason of reluctance by companies for the changes in accounting

processin AASB 138/IAS 38 regarding the need of supplementary acknowledgement of

intangible assets which are generated internally.

2. Differences Internally Generated vs Acquired

Intangibles are obtained during a business merger or are either generated internally. In the

event of acquisition in business mergers, these assets are recognized and recorded by

considering their value, but if they are generated internally then these assets are recorded at

the cost incurred in the phase of development (AASB 138.Intangible Assets, 2016). In

regards to the internally developed intangible assets, two phases are taken into consideration

first is research phase and second is development phase. Research phase covers each and

every activity and the incurred cost, prior to the asset’s feasibility on commercial basis. On

Page 7 of 12

2018

Depreciation A/c (working note 1) 20

TO Machine C A/c 20

30th June

2018

Impairment loss A/c(working note 2) 3.5

To Machine A A/c 2

To Machine C A/c 1.5

Question 3. Ex 6.11

Accounting Justification:

Accounting treatment and disclosure of intangible assets is covered under provisions of

AASB 138. This standard primarily covers two phases of generation of asset first is research

phase and second is development phase(Cheung and Lau, 2016). Para 54-62 of this standard

states that value of asset will be comprise of only those expenses which are occurred in

development phase as that only eligible for capitalisation. This phase is said to be started if

following conditions are satisfied:

Asset must be usable or saleable with the completion of development phase.

Business entity must intend to use or sell the asset

Future economic benefits must be attainable from the asset

Business entity should have appropriate resources for the completion of development

phase

Incurred and proposed expenditure in this phase must be measurable.

Relevant Issues:

1. Explain accounting issues

Issue is to determine difference between accounting of acquired and internally generated

intangible assets and reason of reluctance by companies for the changes in accounting

processin AASB 138/IAS 38 regarding the need of supplementary acknowledgement of

intangible assets which are generated internally.

2. Differences Internally Generated vs Acquired

Intangibles are obtained during a business merger or are either generated internally. In the

event of acquisition in business mergers, these assets are recognized and recorded by

considering their value, but if they are generated internally then these assets are recorded at

the cost incurred in the phase of development (AASB 138.Intangible Assets, 2016). In

regards to the internally developed intangible assets, two phases are taken into consideration

first is research phase and second is development phase. Research phase covers each and

every activity and the incurred cost, prior to the asset’s feasibility on commercial basis. On

Page 7 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

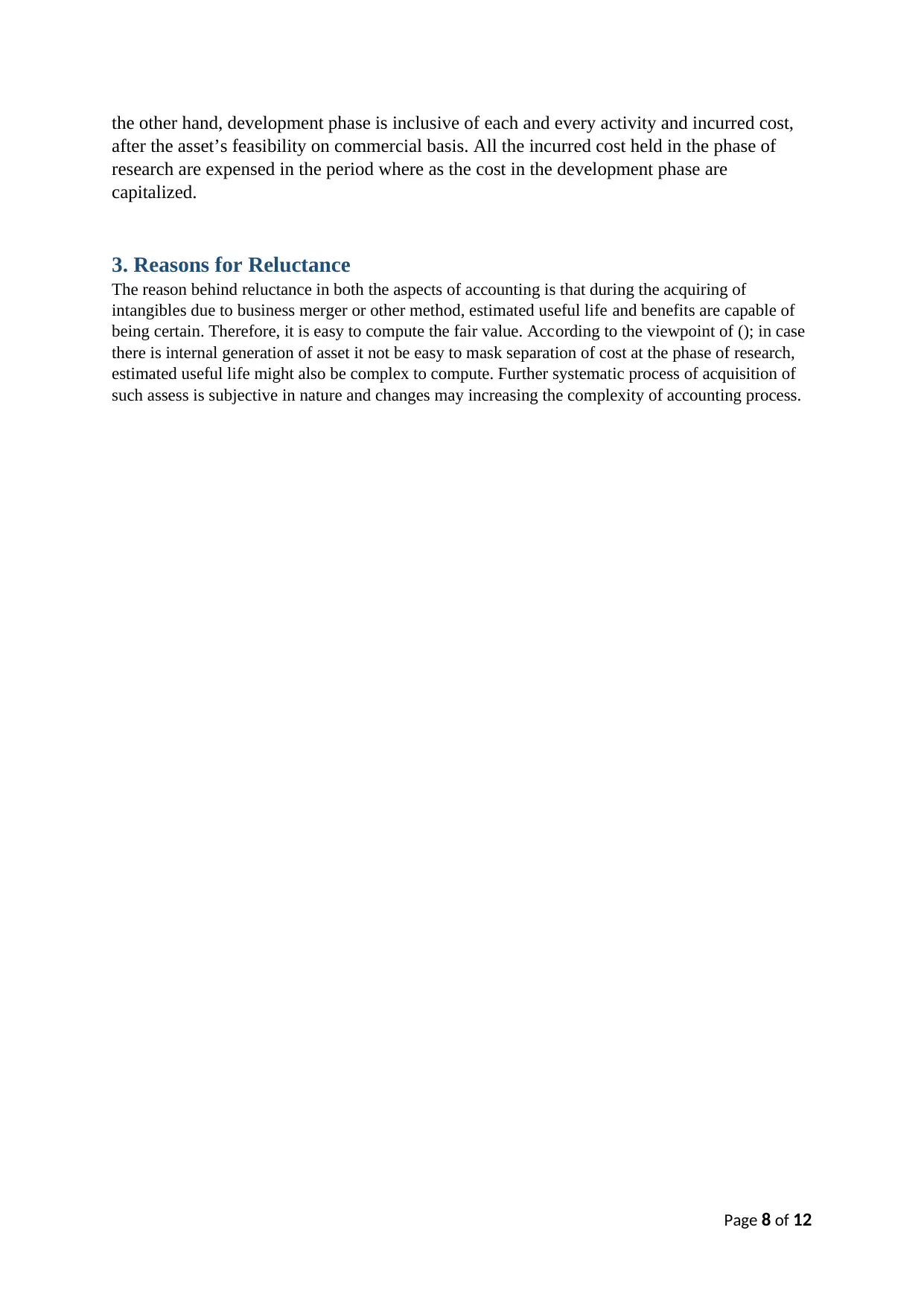

the other hand, development phase is inclusive of each and every activity and incurred cost,

after the asset’s feasibility on commercial basis. All the incurred cost held in the phase of

research are expensed in the period where as the cost in the development phase are

capitalized.

3. Reasons for Reluctance

The reason behind reluctance in both the aspects of accounting is that during the acquiring of

intangibles due to business merger or other method, estimated useful life and benefits are capable of

being certain. Therefore, it is easy to compute the fair value. According to the viewpoint of (); in case

there is internal generation of asset it not be easy to mask separation of cost at the phase of research,

estimated useful life might also be complex to compute. Further systematic process of acquisition of

such assess is subjective in nature and changes may increasing the complexity of accounting process.

Page 8 of 12

after the asset’s feasibility on commercial basis. All the incurred cost held in the phase of

research are expensed in the period where as the cost in the development phase are

capitalized.

3. Reasons for Reluctance

The reason behind reluctance in both the aspects of accounting is that during the acquiring of

intangibles due to business merger or other method, estimated useful life and benefits are capable of

being certain. Therefore, it is easy to compute the fair value. According to the viewpoint of (); in case

there is internal generation of asset it not be easy to mask separation of cost at the phase of research,

estimated useful life might also be complex to compute. Further systematic process of acquisition of

such assess is subjective in nature and changes may increasing the complexity of accounting process.

Page 8 of 12

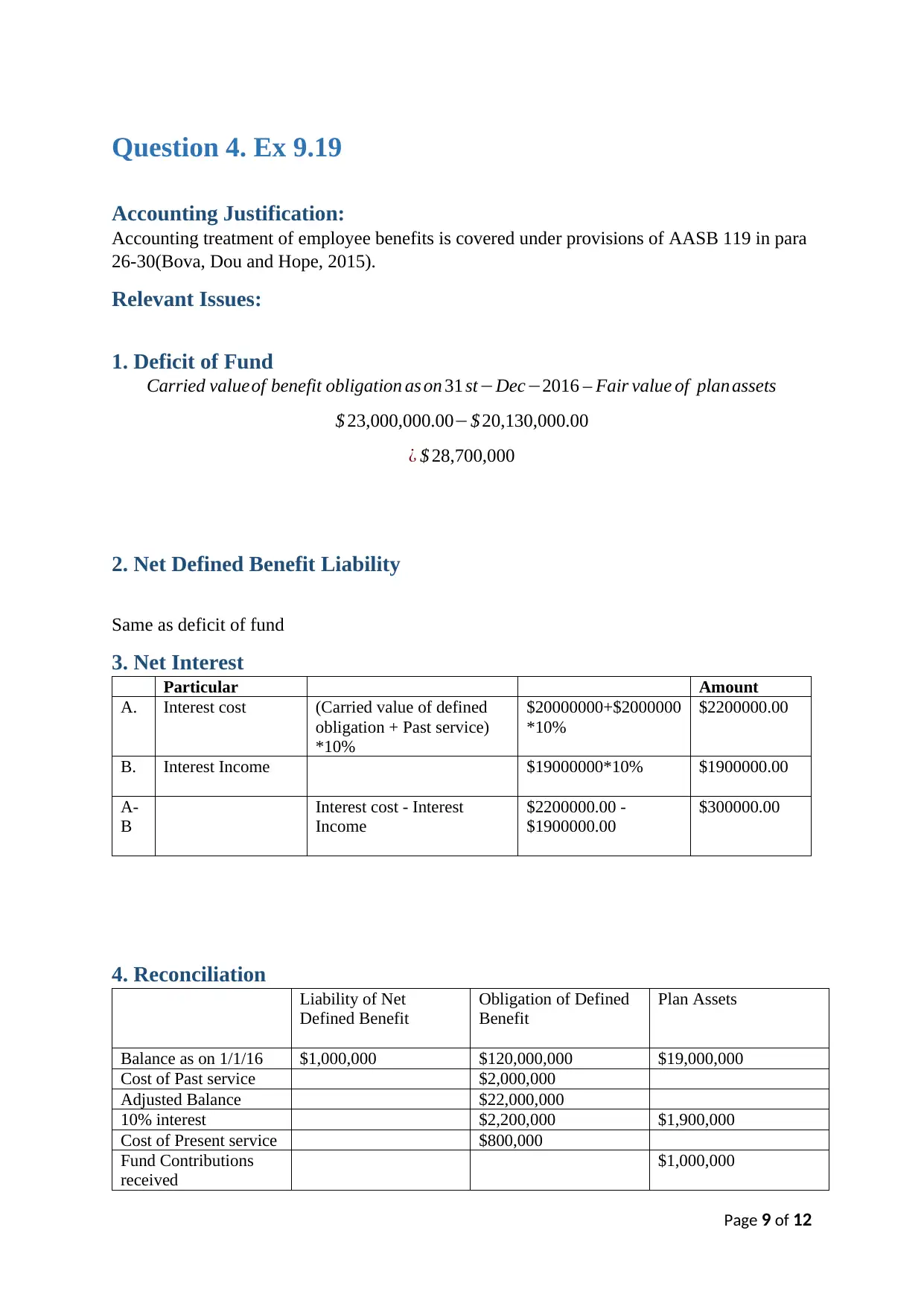

Question 4. Ex 9.19

Accounting Justification:

Accounting treatment of employee benefits is covered under provisions of AASB 119 in para

26-30(Bova, Dou and Hope, 2015).

Relevant Issues:

1. Deficit of Fund

Carried valueof benefit obligation as on 31 st−Dec−2016 – Fair value of plan assets

$ 23,000,000.00−$ 20,130,000.00

¿ $ 28,700,000

2. Net Defined Benefit Liability

Same as deficit of fund

3. Net Interest

Particular Amount

A. Interest cost (Carried value of defined

obligation + Past service)

*10%

$20000000+$2000000

*10%

$2200000.00

B. Interest Income $19000000*10% $1900000.00

A-

B

Interest cost - Interest

Income

$2200000.00 -

$1900000.00

$300000.00

4. Reconciliation

Liability of Net

Defined Benefit

Obligation of Defined

Benefit

Plan Assets

Balance as on 1/1/16 $1,000,000 $120,000,000 $19,000,000

Cost of Past service $2,000,000

Adjusted Balance $22,000,000

10% interest $2,200,000 $1,900,000

Cost of Present service $800,000

Fund Contributions

received

$1,000,000

Page 9 of 12

Accounting Justification:

Accounting treatment of employee benefits is covered under provisions of AASB 119 in para

26-30(Bova, Dou and Hope, 2015).

Relevant Issues:

1. Deficit of Fund

Carried valueof benefit obligation as on 31 st−Dec−2016 – Fair value of plan assets

$ 23,000,000.00−$ 20,130,000.00

¿ $ 28,700,000

2. Net Defined Benefit Liability

Same as deficit of fund

3. Net Interest

Particular Amount

A. Interest cost (Carried value of defined

obligation + Past service)

*10%

$20000000+$2000000

*10%

$2200000.00

B. Interest Income $19000000*10% $1900000.00

A-

B

Interest cost - Interest

Income

$2200000.00 -

$1900000.00

$300000.00

4. Reconciliation

Liability of Net

Defined Benefit

Obligation of Defined

Benefit

Plan Assets

Balance as on 1/1/16 $1,000,000 $120,000,000 $19,000,000

Cost of Past service $2,000,000

Adjusted Balance $22,000,000

10% interest $2,200,000 $1,900,000

Cost of Present service $800,000

Fund Contributions

received

$1,000,000

Page 9 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Funds’ paid Benefits ($2,100,000) ($2,100,000)

Return on Plan Assets

excluding Interest

$330,000

Remeasured Actual

loss of Defined Benefit

Obligation

$100,000

Balance as 31st

December 2016

$2,870,000 $23,000,000 $20,130,000

Return on plan asset excluding interest

Value as on 31.12.06 $20,130,000

Less Opening balance -$19,000,000

Less Contribution -$1,000,000

Less Paid benefits -$1,900,000

Add Interest income $2,100,000 $19,800,000

Return on plan asset excluding interest $330,000

5. Summary Journal

Profit or Loss Other

comprehens

ive Income

Bank Net DBL(A)

Opening

balance

$1,000,000

Past service

cost

$2,000,000

Net interest $300,000

Service cost $800,000

Contributio

ns paid to

the fund

$1,000,000

Gain on

plan assets

(ex. interest)

$330,000

Actuarial

loss on

DBO

-$100,000

Journal

entry

$3,100,000 $230,000 $1,000,000 $1,870,000

Debit Credit Credit Credit

Closing $2,870,000

Page 10 of 12

Return on Plan Assets

excluding Interest

$330,000

Remeasured Actual

loss of Defined Benefit

Obligation

$100,000

Balance as 31st

December 2016

$2,870,000 $23,000,000 $20,130,000

Return on plan asset excluding interest

Value as on 31.12.06 $20,130,000

Less Opening balance -$19,000,000

Less Contribution -$1,000,000

Less Paid benefits -$1,900,000

Add Interest income $2,100,000 $19,800,000

Return on plan asset excluding interest $330,000

5. Summary Journal

Profit or Loss Other

comprehens

ive Income

Bank Net DBL(A)

Opening

balance

$1,000,000

Past service

cost

$2,000,000

Net interest $300,000

Service cost $800,000

Contributio

ns paid to

the fund

$1,000,000

Gain on

plan assets

(ex. interest)

$330,000

Actuarial

loss on

DBO

-$100,000

Journal

entry

$3,100,000 $230,000 $1,000,000 $1,870,000

Debit Credit Credit Credit

Closing $2,870,000

Page 10 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

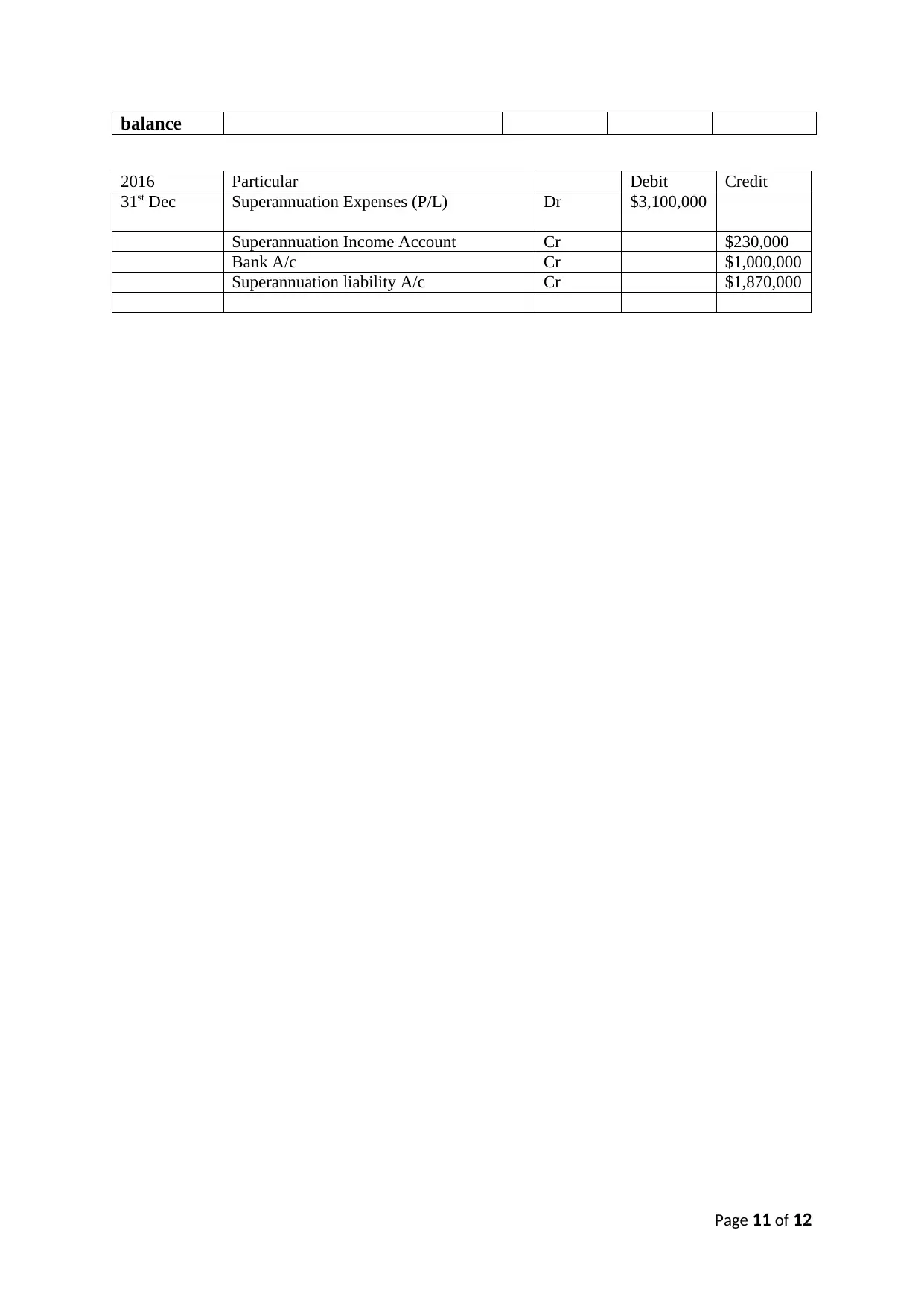

balance

2016 Particular Debit Credit

31st Dec Superannuation Expenses (P/L) Dr $3,100,000

Superannuation Income Account Cr $230,000

Bank A/c Cr $1,000,000

Superannuation liability A/c Cr $1,870,000

Page 11 of 12

2016 Particular Debit Credit

31st Dec Superannuation Expenses (P/L) Dr $3,100,000

Superannuation Income Account Cr $230,000

Bank A/c Cr $1,000,000

Superannuation liability A/c Cr $1,870,000

Page 11 of 12

References

Books and Journal

AASB 138.Intangible Assets. 2016. [PDF]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-

14.pdf> [Accessed on9th October 2017]

Basu, A. and Andrews, S., 2014. Asset allocation policy, returns and expenses of

superannuation funds: recent evidence based on default options. Australian Economic

Review, 47(1), pp.63-77.

Bova, F., Dou, Y. and Hope, O.K., 2015. Employee ownership and firm

disclosure. Contemporary Accounting Research, 32(2), pp.639-673.

Capalbo, F., 2013. Impairment of Assets

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Davies, B., 2014. Defined Benefit vs Defined Contribution or is There a Third Way? Defined

Ambition Schemes: An Alternative Approach to Risk Sharing.

Zakaria, A., Edwards, D.J., Holt, G.D. and Ramachandran, V., 2014. A Review of Property,

Plant and Equipment Asset Revaluation Decision Making in Indonesia: Development of a

Conceptual Model. Mindanao Journal of Science and Technology, 12(1), pp.1-1.

Online

AASB 116.Property Plant and Equipment. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-04_COMPjun09_07-

09.pdf>. [Accessed on 30th September 2017.]

AASB 13. Fair Value Measurement. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_09-11.pdf>. [Accessed on 30th

September 2017.]

AASB 138.Intangible Assets. 2016. [PDF]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-

14.pdf> [Accessed on9th October 2017]

Page 12 of 12

Books and Journal

AASB 138.Intangible Assets. 2016. [PDF]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-

14.pdf> [Accessed on9th October 2017]

Basu, A. and Andrews, S., 2014. Asset allocation policy, returns and expenses of

superannuation funds: recent evidence based on default options. Australian Economic

Review, 47(1), pp.63-77.

Bova, F., Dou, Y. and Hope, O.K., 2015. Employee ownership and firm

disclosure. Contemporary Accounting Research, 32(2), pp.639-673.

Capalbo, F., 2013. Impairment of Assets

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Davies, B., 2014. Defined Benefit vs Defined Contribution or is There a Third Way? Defined

Ambition Schemes: An Alternative Approach to Risk Sharing.

Zakaria, A., Edwards, D.J., Holt, G.D. and Ramachandran, V., 2014. A Review of Property,

Plant and Equipment Asset Revaluation Decision Making in Indonesia: Development of a

Conceptual Model. Mindanao Journal of Science and Technology, 12(1), pp.1-1.

Online

AASB 116.Property Plant and Equipment. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-04_COMPjun09_07-

09.pdf>. [Accessed on 30th September 2017.]

AASB 13. Fair Value Measurement. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_09-11.pdf>. [Accessed on 30th

September 2017.]

AASB 138.Intangible Assets. 2016. [PDF]. Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-

14.pdf> [Accessed on9th October 2017]

Page 12 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.