Financial Accounting: Detailed Analysis of Client Transactions Records

VerifiedAdded on 2020/07/23

|20

|5085

|52

Homework Assignment

AI Summary

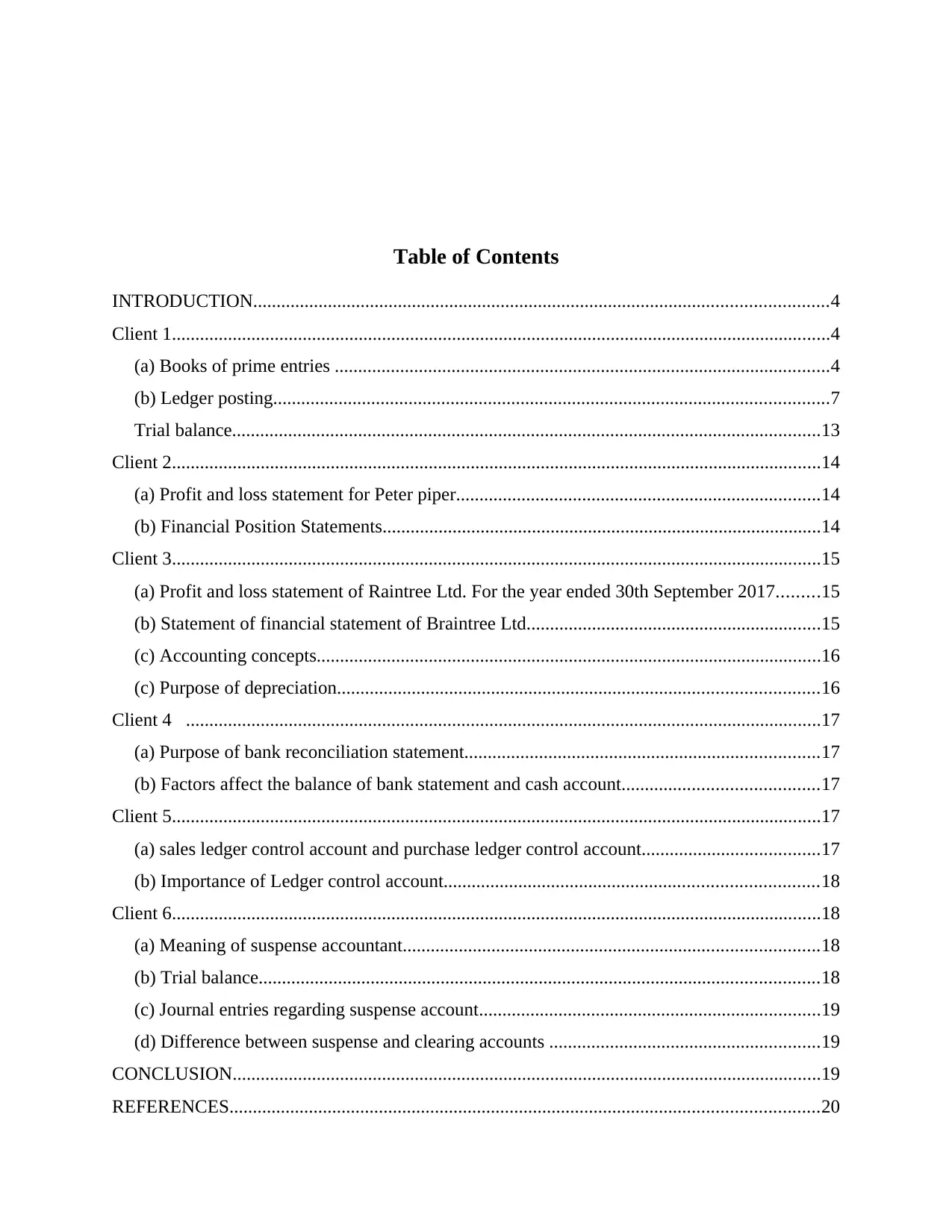

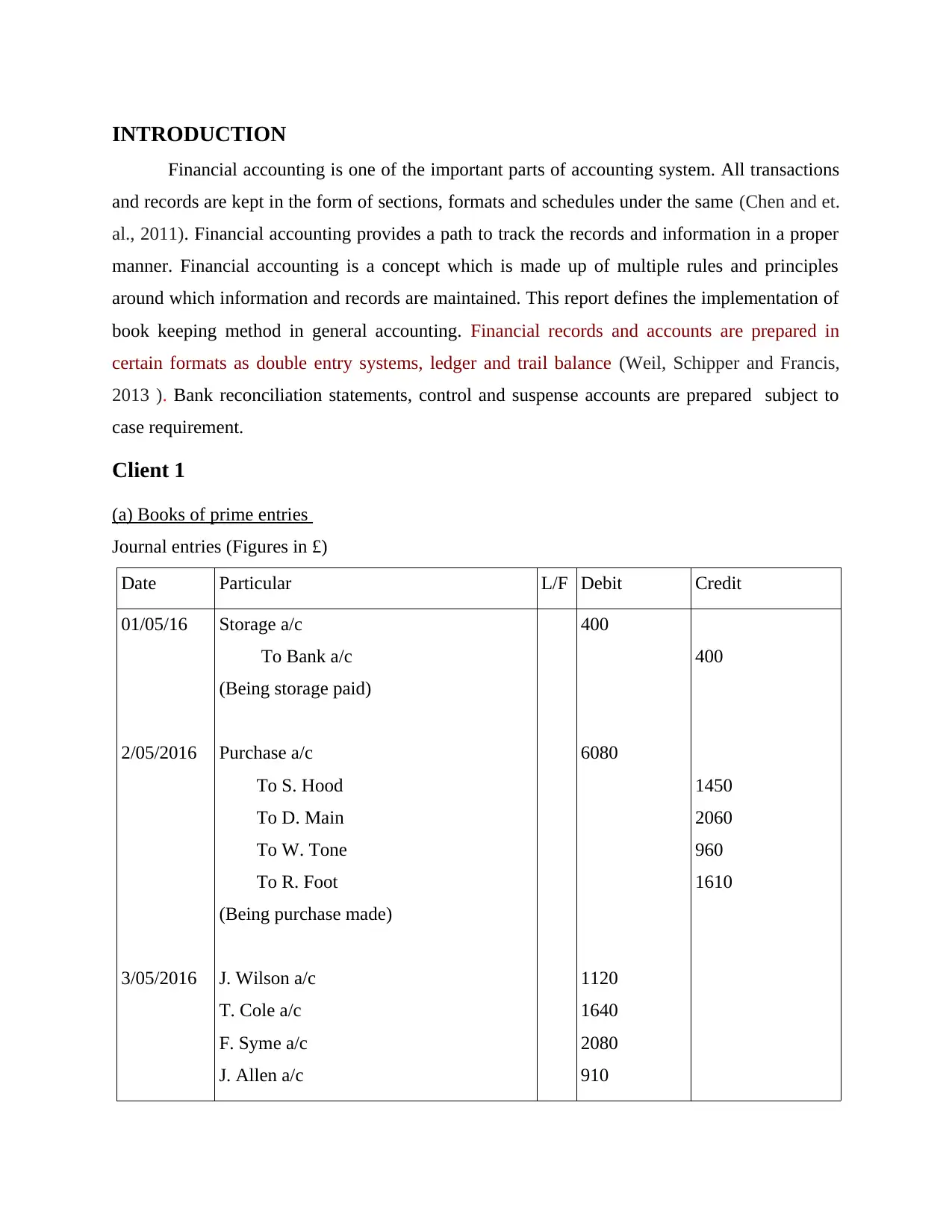

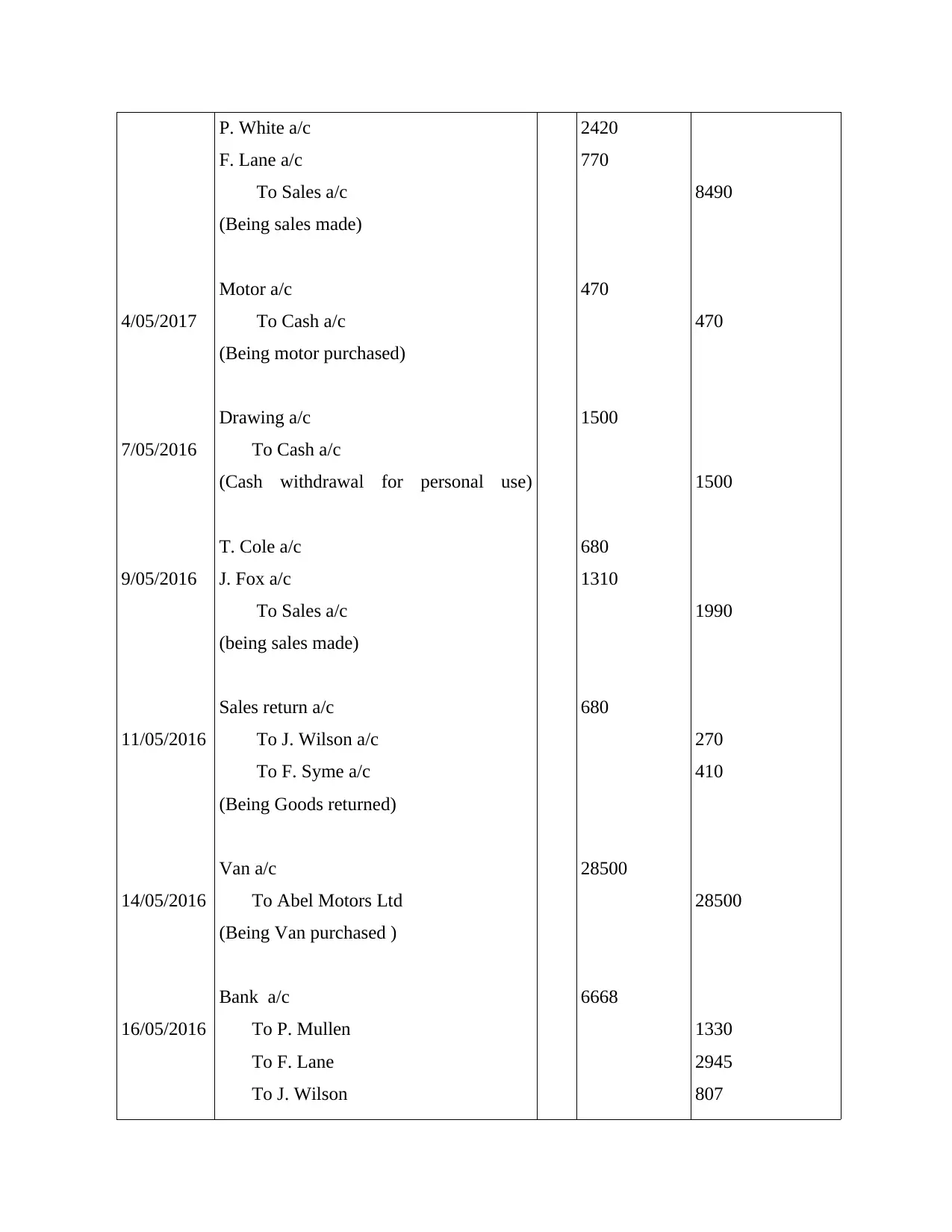

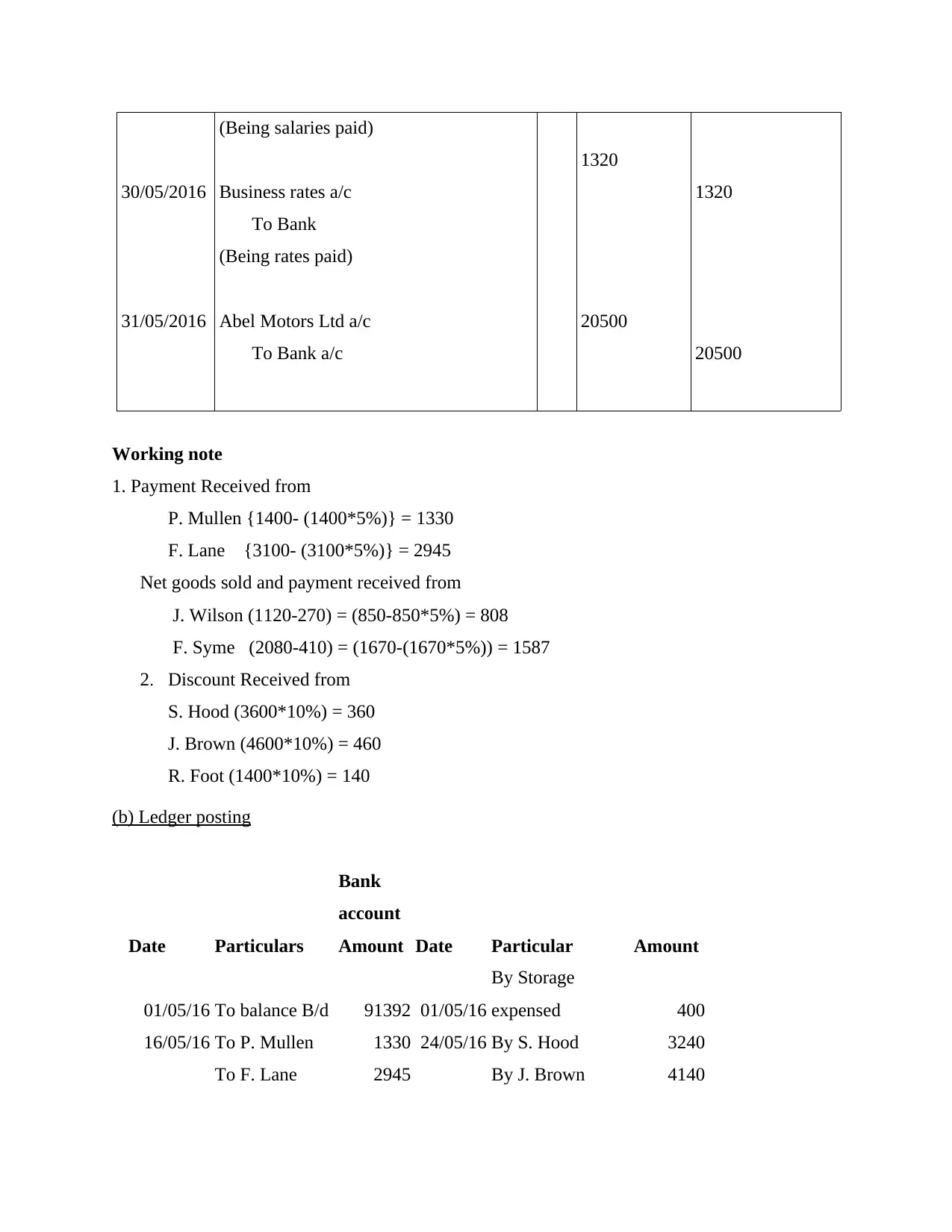

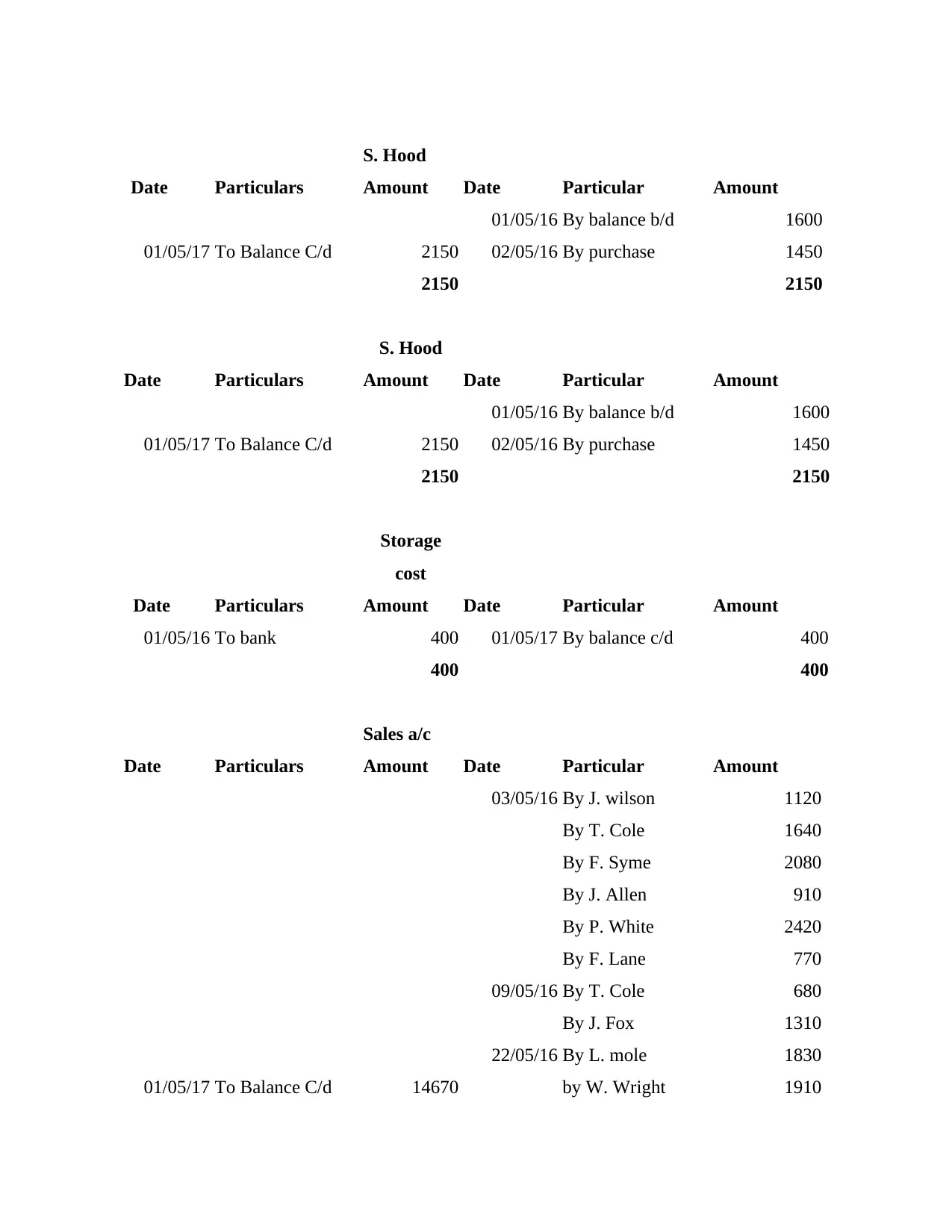

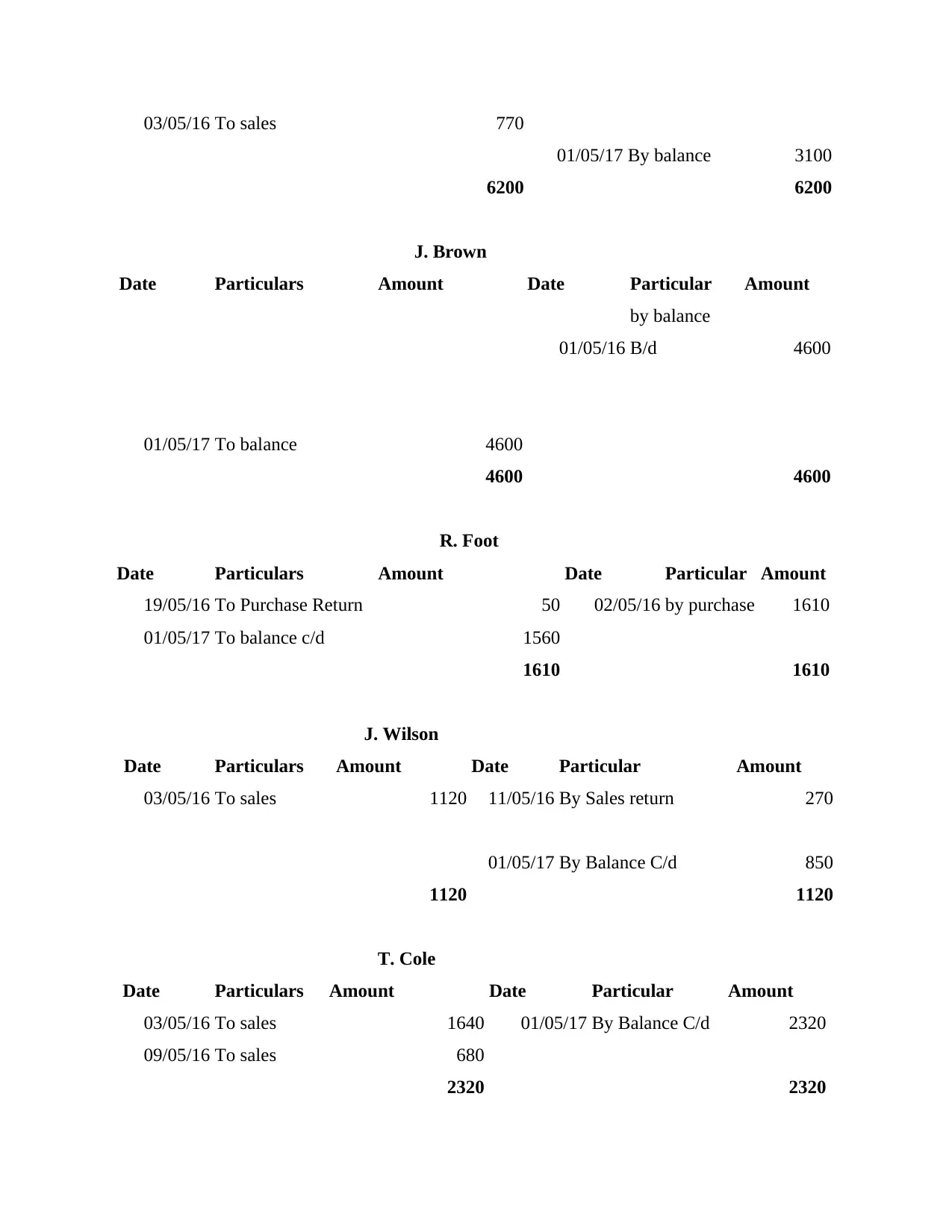

This financial accounting assignment delves into the practical application of accounting principles through the analysis of various client transactions. The report meticulously details journal entries, ledger postings, and the construction of trial balances for multiple clients. It covers the preparation of profit and loss statements and financial position statements, alongside an exploration of accounting concepts and the purpose of depreciation. Furthermore, the assignment addresses bank reconciliation statements, control accounts, suspense accounts, and their significance. The document provides a comprehensive overview of financial accounting procedures, offering a valuable resource for students studying accounting.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.