Financial Accounting Assignment Solution, UGB105 Module

VerifiedAdded on 2023/01/09

|13

|3265

|61

Homework Assignment

AI Summary

This assignment solution provides a detailed analysis of financial accounting principles and practices. It begins with the preparation of Bob's trading account, profit and loss account, and statement of financial position, including calculations and interpretations. The solution then critically evaluates the main features of financial information for users, emphasizing relevance, reliability, timeliness, and understandability. It also demonstrates the importance of financial information for various stakeholders, including management, investors, employees, and shareholders. The assignment further includes the calculation and interpretation of key financial ratios, such as gross profit margin, return on capital employed, current ratio, trade payable period, and trade receivable period. Finally, it provides a balanced bank account for March. The assignment covers a wide range of topics, offering comprehensive insights into financial accounting.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1........................................................................................................................................1

1. Financial Statement of Bob’s Account....................................................................................1

2. Critically evaluate the main features of information for the users of financial information...3

Question 2........................................................................................................................................5

1. Calculate the following ratios and interpret the results...........................................................5

2. Balance the bank account........................................................................................................7

3. Prepare the provision for depreciation of machinery account by using different methods.....8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

MAIN BODY..................................................................................................................................1

Question 1........................................................................................................................................1

1. Financial Statement of Bob’s Account....................................................................................1

2. Critically evaluate the main features of information for the users of financial information...3

Question 2........................................................................................................................................5

1. Calculate the following ratios and interpret the results...........................................................5

2. Balance the bank account........................................................................................................7

3. Prepare the provision for depreciation of machinery account by using different methods.....8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial accounting is a complex framework with a multitude of activities to monitor,

assess and publish the results of such reports to users. The related operations are relevant to the

financial reports (Biddle, Ma and Song, 2020). It's being used to compile financial reports

including the income statement, statement of comprehensive income and cash flow statements in

order to show company credibility and results over a set period of time which is typically

periodic. The primary objective is to describe the shareholders with these findings as their money

is spent in the entity. Throughout this report, the key features of details that are useful to

consumers are weekend accounts. In addition to this, determine and explain various forms of

financial ratio to assess the financial position of the company and start preparing bank account in

every month. In addition, apply various methodologies of depreciation, and know various

notions of financial accounting.

MAIN BODY

Question 1

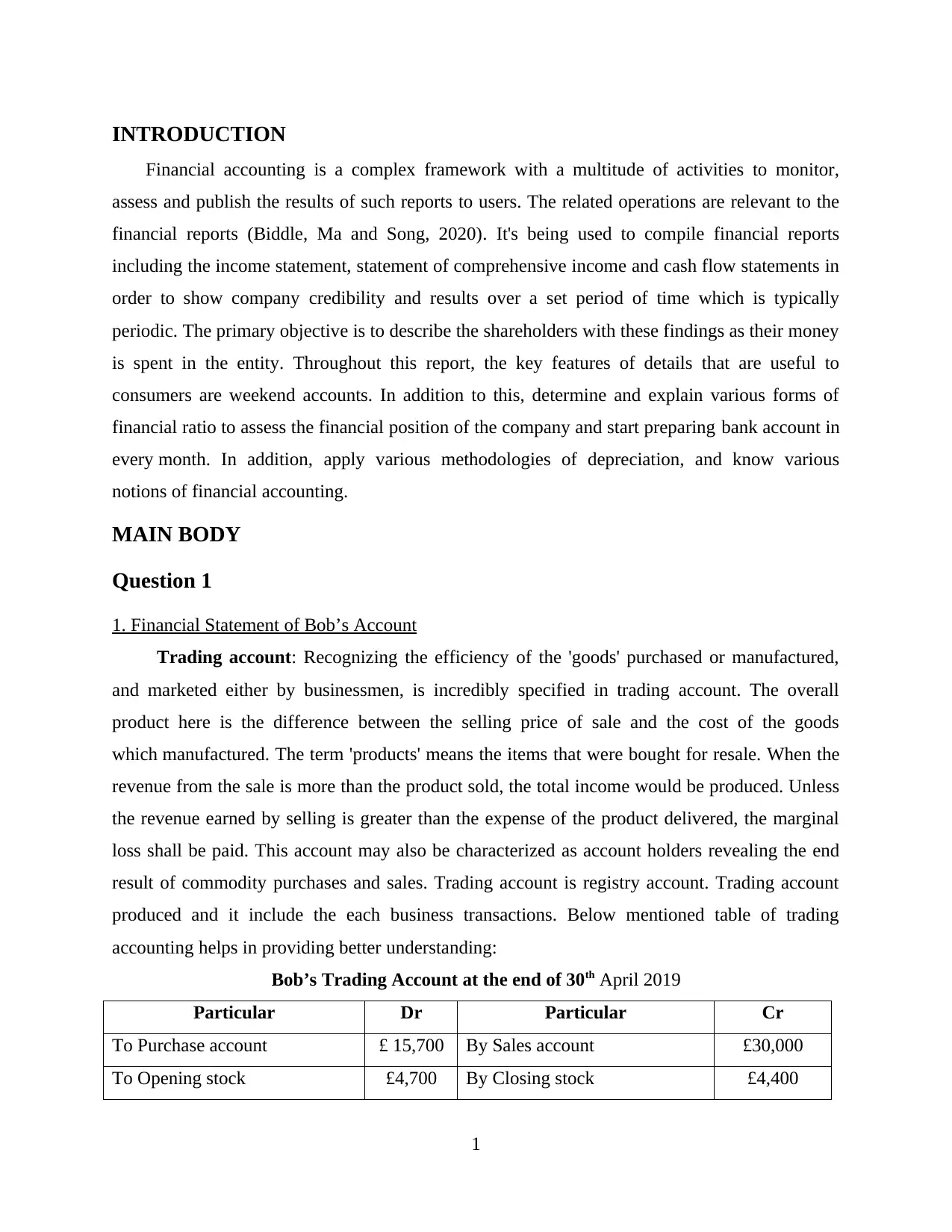

1. Financial Statement of Bob’s Account

Trading account: Recognizing the efficiency of the 'goods' purchased or manufactured,

and marketed either by businessmen, is incredibly specified in trading account. The overall

product here is the difference between the selling price of sale and the cost of the goods

which manufactured. The term 'products' means the items that were bought for resale. When the

revenue from the sale is more than the product sold, the total income would be produced. Unless

the revenue earned by selling is greater than the expense of the product delivered, the marginal

loss shall be paid. This account may also be characterized as account holders revealing the end

result of commodity purchases and sales. Trading account is registry account. Trading account

produced and it include the each business transactions. Below mentioned table of trading

accounting helps in providing better understanding:

Bob’s Trading Account at the end of 30th April 2019

Particular Dr Particular Cr

To Purchase account £ 15,700 By Sales account £30,000

To Opening stock £4,700 By Closing stock £4,400

1

Financial accounting is a complex framework with a multitude of activities to monitor,

assess and publish the results of such reports to users. The related operations are relevant to the

financial reports (Biddle, Ma and Song, 2020). It's being used to compile financial reports

including the income statement, statement of comprehensive income and cash flow statements in

order to show company credibility and results over a set period of time which is typically

periodic. The primary objective is to describe the shareholders with these findings as their money

is spent in the entity. Throughout this report, the key features of details that are useful to

consumers are weekend accounts. In addition to this, determine and explain various forms of

financial ratio to assess the financial position of the company and start preparing bank account in

every month. In addition, apply various methodologies of depreciation, and know various

notions of financial accounting.

MAIN BODY

Question 1

1. Financial Statement of Bob’s Account

Trading account: Recognizing the efficiency of the 'goods' purchased or manufactured,

and marketed either by businessmen, is incredibly specified in trading account. The overall

product here is the difference between the selling price of sale and the cost of the goods

which manufactured. The term 'products' means the items that were bought for resale. When the

revenue from the sale is more than the product sold, the total income would be produced. Unless

the revenue earned by selling is greater than the expense of the product delivered, the marginal

loss shall be paid. This account may also be characterized as account holders revealing the end

result of commodity purchases and sales. Trading account is registry account. Trading account

produced and it include the each business transactions. Below mentioned table of trading

accounting helps in providing better understanding:

Bob’s Trading Account at the end of 30th April 2019

Particular Dr Particular Cr

To Purchase account £ 15,700 By Sales account £30,000

To Opening stock £4,700 By Closing stock £4,400

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Shop wages £4,420

To Gross Profit £9,580

£34,400 £34,400

Profit and loss account: This statesmen is basically a form of financial reports as this

document allow the several users to evaluate how beneficial it is to make transactions in a certain

place based on the product (Brown, 2018). Profit and loss account shows the summary overall

incomes and expenses which done throughout the period. It helps in evaluating profitability

position of the company. To use this understanding an investor can make their decisions

regarding investment. Income and expense accounts are generally viewed in line with a balance

sheet which listing assets, contractor liability and equity, and cash flow statements reflecting any

adjustments to finances and sales. Below mention Bob’s profit and loss account provide better

understanding:

Bob’s profit & loss account for the year end of 30 April 2019

Particular Dr Particular Cr

To Shop fittings £13,000 By Gross Profit £9,580

To Light and heat £260 By Net Loss £8,300

To Rent £4,500

To Insurance £120

£17,880 £17,880

Financial position: Statement of financial position also called balance sheet which

consist two sides where first one is assets and another one is liabilities. The financial analysis

includes a description of what a company holds and owes, as well as the sums spent by the

creditors. The balance sheet reveals a corporation's wealth or reserves and it also reveals that

such money was invested either by investing underlying obligations or through generating profits

as seen in the shareholder's equity. This financial report contains an overview that how

effectively the managers of the organization use its capital, both for creditors and stakeholders.

2

To Gross Profit £9,580

£34,400 £34,400

Profit and loss account: This statesmen is basically a form of financial reports as this

document allow the several users to evaluate how beneficial it is to make transactions in a certain

place based on the product (Brown, 2018). Profit and loss account shows the summary overall

incomes and expenses which done throughout the period. It helps in evaluating profitability

position of the company. To use this understanding an investor can make their decisions

regarding investment. Income and expense accounts are generally viewed in line with a balance

sheet which listing assets, contractor liability and equity, and cash flow statements reflecting any

adjustments to finances and sales. Below mention Bob’s profit and loss account provide better

understanding:

Bob’s profit & loss account for the year end of 30 April 2019

Particular Dr Particular Cr

To Shop fittings £13,000 By Gross Profit £9,580

To Light and heat £260 By Net Loss £8,300

To Rent £4,500

To Insurance £120

£17,880 £17,880

Financial position: Statement of financial position also called balance sheet which

consist two sides where first one is assets and another one is liabilities. The financial analysis

includes a description of what a company holds and owes, as well as the sums spent by the

creditors. The balance sheet reveals a corporation's wealth or reserves and it also reveals that

such money was invested either by investing underlying obligations or through generating profits

as seen in the shareholder's equity. This financial report contains an overview that how

effectively the managers of the organization use its capital, both for creditors and stakeholders.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

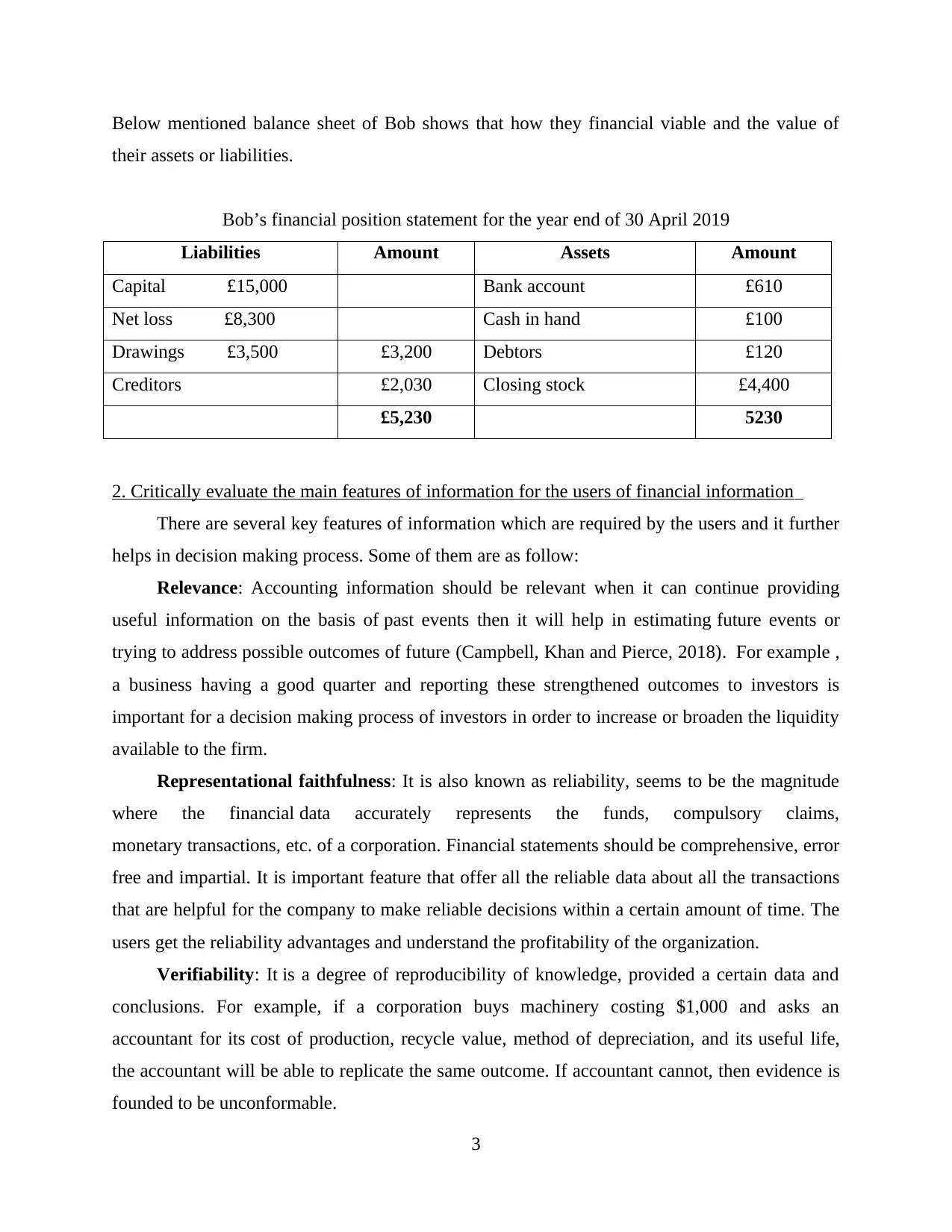

Below mentioned balance sheet of Bob shows that how they financial viable and the value of

their assets or liabilities.

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital £15,000 Bank account £610

Net loss £8,300 Cash in hand £100

Drawings £3,500 £3,200 Debtors £120

Creditors £2,030 Closing stock £4,400

£5,230 5230

2. Critically evaluate the main features of information for the users of financial information

There are several key features of information which are required by the users and it further

helps in decision making process. Some of them are as follow:

Relevance: Accounting information should be relevant when it can continue providing

useful information on the basis of past events then it will help in estimating future events or

trying to address possible outcomes of future (Campbell, Khan and Pierce, 2018). For example ,

a business having a good quarter and reporting these strengthened outcomes to investors is

important for a decision making process of investors in order to increase or broaden the liquidity

available to the firm.

Representational faithfulness: It is also known as reliability, seems to be the magnitude

where the financial data accurately represents the funds, compulsory claims,

monetary transactions, etc. of a corporation. Financial statements should be comprehensive, error

free and impartial. It is important feature that offer all the reliable data about all the transactions

that are helpful for the company to make reliable decisions within a certain amount of time. The

users get the reliability advantages and understand the profitability of the organization.

Verifiability: It is a degree of reproducibility of knowledge, provided a certain data and

conclusions. For example, if a corporation buys machinery costing $1,000 and asks an

accountant for its cost of production, recycle value, method of depreciation, and its useful life,

the accountant will be able to replicate the same outcome. If accountant cannot, then evidence is

founded to be unconformable.

3

their assets or liabilities.

Bob’s financial position statement for the year end of 30 April 2019

Liabilities Amount Assets Amount

Capital £15,000 Bank account £610

Net loss £8,300 Cash in hand £100

Drawings £3,500 £3,200 Debtors £120

Creditors £2,030 Closing stock £4,400

£5,230 5230

2. Critically evaluate the main features of information for the users of financial information

There are several key features of information which are required by the users and it further

helps in decision making process. Some of them are as follow:

Relevance: Accounting information should be relevant when it can continue providing

useful information on the basis of past events then it will help in estimating future events or

trying to address possible outcomes of future (Campbell, Khan and Pierce, 2018). For example ,

a business having a good quarter and reporting these strengthened outcomes to investors is

important for a decision making process of investors in order to increase or broaden the liquidity

available to the firm.

Representational faithfulness: It is also known as reliability, seems to be the magnitude

where the financial data accurately represents the funds, compulsory claims,

monetary transactions, etc. of a corporation. Financial statements should be comprehensive, error

free and impartial. It is important feature that offer all the reliable data about all the transactions

that are helpful for the company to make reliable decisions within a certain amount of time. The

users get the reliability advantages and understand the profitability of the organization.

Verifiability: It is a degree of reproducibility of knowledge, provided a certain data and

conclusions. For example, if a corporation buys machinery costing $1,000 and asks an

accountant for its cost of production, recycle value, method of depreciation, and its useful life,

the accountant will be able to replicate the same outcome. If accountant cannot, then evidence is

founded to be unconformable.

3

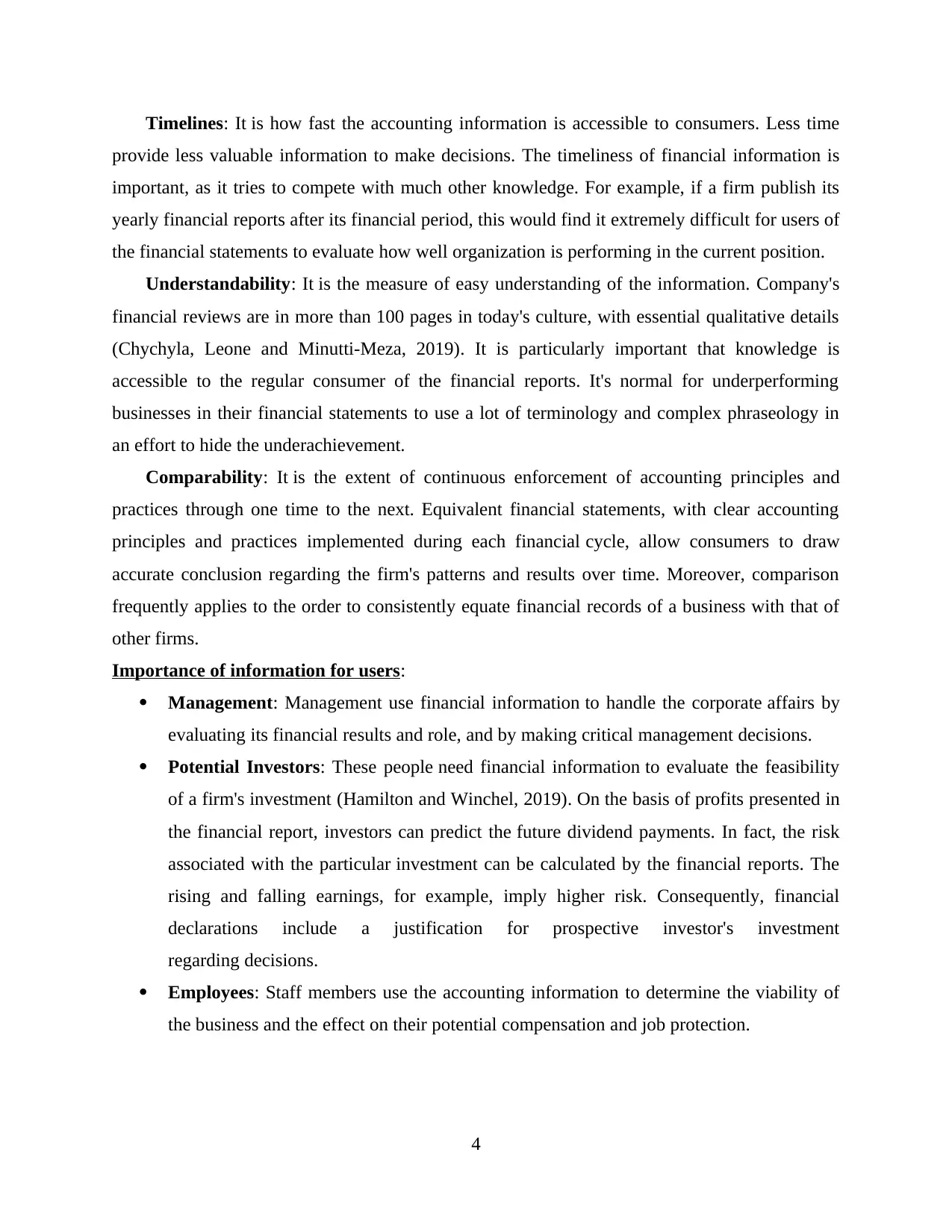

Timelines: It is how fast the accounting information is accessible to consumers. Less time

provide less valuable information to make decisions. The timeliness of financial information is

important, as it tries to compete with much other knowledge. For example, if a firm publish its

yearly financial reports after its financial period, this would find it extremely difficult for users of

the financial statements to evaluate how well organization is performing in the current position.

Understandability: It is the measure of easy understanding of the information. Company's

financial reviews are in more than 100 pages in today's culture, with essential qualitative details

(Chychyla, Leone and Minutti-Meza, 2019). It is particularly important that knowledge is

accessible to the regular consumer of the financial reports. It's normal for underperforming

businesses in their financial statements to use a lot of terminology and complex phraseology in

an effort to hide the underachievement.

Comparability: It is the extent of continuous enforcement of accounting principles and

practices through one time to the next. Equivalent financial statements, with clear accounting

principles and practices implemented during each financial cycle, allow consumers to draw

accurate conclusion regarding the firm's patterns and results over time. Moreover, comparison

frequently applies to the order to consistently equate financial records of a business with that of

other firms.

Importance of information for users:

Management: Management use financial information to handle the corporate affairs by

evaluating its financial results and role, and by making critical management decisions.

Potential Investors: These people need financial information to evaluate the feasibility

of a firm's investment (Hamilton and Winchel, 2019). On the basis of profits presented in

the financial report, investors can predict the future dividend payments. In fact, the risk

associated with the particular investment can be calculated by the financial reports. The

rising and falling earnings, for example, imply higher risk. Consequently, financial

declarations include a justification for prospective investor's investment

regarding decisions.

Employees: Staff members use the accounting information to determine the viability of

the business and the effect on their potential compensation and job protection.

4

provide less valuable information to make decisions. The timeliness of financial information is

important, as it tries to compete with much other knowledge. For example, if a firm publish its

yearly financial reports after its financial period, this would find it extremely difficult for users of

the financial statements to evaluate how well organization is performing in the current position.

Understandability: It is the measure of easy understanding of the information. Company's

financial reviews are in more than 100 pages in today's culture, with essential qualitative details

(Chychyla, Leone and Minutti-Meza, 2019). It is particularly important that knowledge is

accessible to the regular consumer of the financial reports. It's normal for underperforming

businesses in their financial statements to use a lot of terminology and complex phraseology in

an effort to hide the underachievement.

Comparability: It is the extent of continuous enforcement of accounting principles and

practices through one time to the next. Equivalent financial statements, with clear accounting

principles and practices implemented during each financial cycle, allow consumers to draw

accurate conclusion regarding the firm's patterns and results over time. Moreover, comparison

frequently applies to the order to consistently equate financial records of a business with that of

other firms.

Importance of information for users:

Management: Management use financial information to handle the corporate affairs by

evaluating its financial results and role, and by making critical management decisions.

Potential Investors: These people need financial information to evaluate the feasibility

of a firm's investment (Hamilton and Winchel, 2019). On the basis of profits presented in

the financial report, investors can predict the future dividend payments. In fact, the risk

associated with the particular investment can be calculated by the financial reports. The

rising and falling earnings, for example, imply higher risk. Consequently, financial

declarations include a justification for prospective investor's investment

regarding decisions.

Employees: Staff members use the accounting information to determine the viability of

the business and the effect on their potential compensation and job protection.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

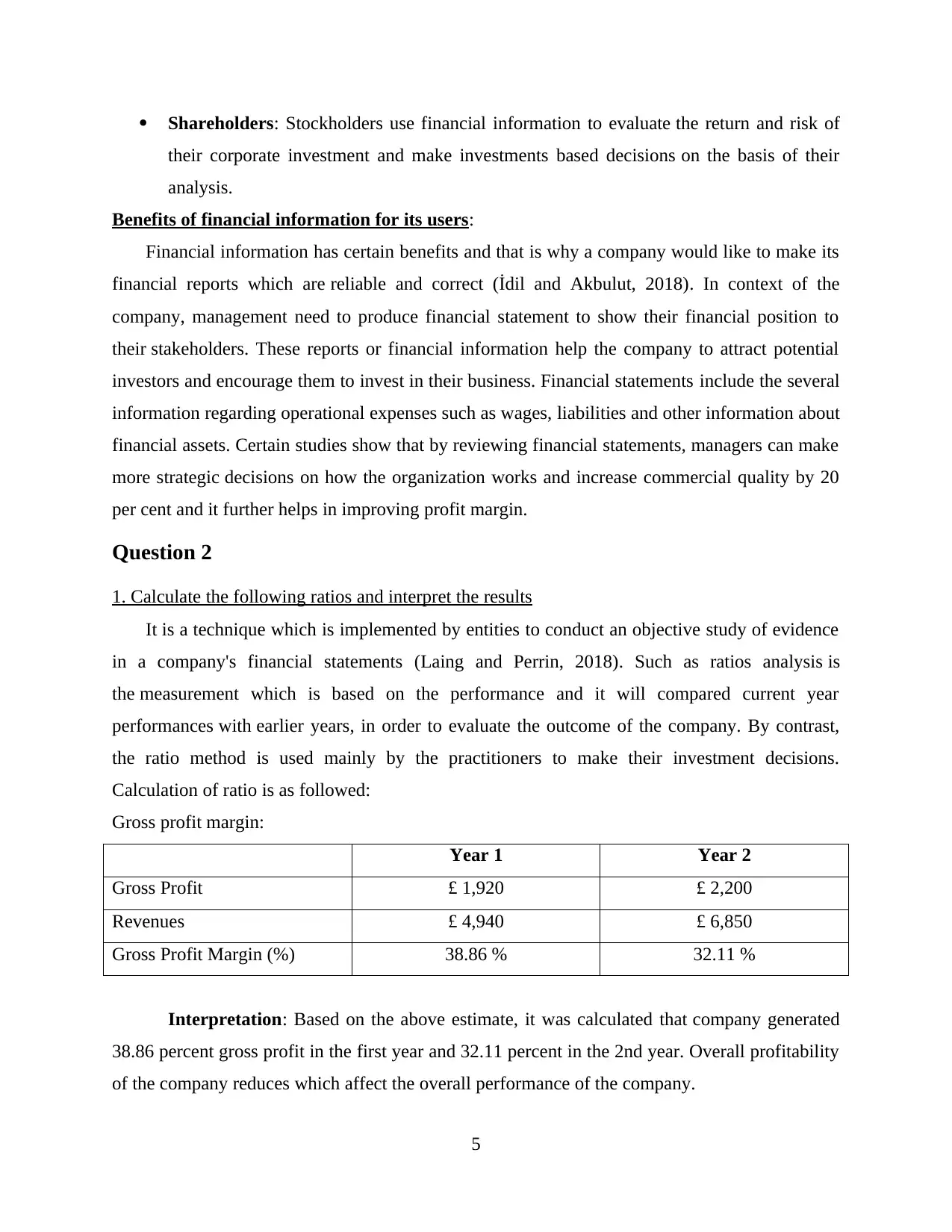

Shareholders: Stockholders use financial information to evaluate the return and risk of

their corporate investment and make investments based decisions on the basis of their

analysis.

Benefits of financial information for its users:

Financial information has certain benefits and that is why a company would like to make its

financial reports which are reliable and correct (İdil and Akbulut, 2018). In context of the

company, management need to produce financial statement to show their financial position to

their stakeholders. These reports or financial information help the company to attract potential

investors and encourage them to invest in their business. Financial statements include the several

information regarding operational expenses such as wages, liabilities and other information about

financial assets. Certain studies show that by reviewing financial statements, managers can make

more strategic decisions on how the organization works and increase commercial quality by 20

per cent and it further helps in improving profit margin.

Question 2

1. Calculate the following ratios and interpret the results

It is a technique which is implemented by entities to conduct an objective study of evidence

in a company's financial statements (Laing and Perrin, 2018). Such as ratios analysis is

the measurement which is based on the performance and it will compared current year

performances with earlier years, in order to evaluate the outcome of the company. By contrast,

the ratio method is used mainly by the practitioners to make their investment decisions.

Calculation of ratio is as followed:

Gross profit margin:

Year 1 Year 2

Gross Profit £ 1,920 £ 2,200

Revenues £ 4,940 £ 6,850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: Based on the above estimate, it was calculated that company generated

38.86 percent gross profit in the first year and 32.11 percent in the 2nd year. Overall profitability

of the company reduces which affect the overall performance of the company.

5

their corporate investment and make investments based decisions on the basis of their

analysis.

Benefits of financial information for its users:

Financial information has certain benefits and that is why a company would like to make its

financial reports which are reliable and correct (İdil and Akbulut, 2018). In context of the

company, management need to produce financial statement to show their financial position to

their stakeholders. These reports or financial information help the company to attract potential

investors and encourage them to invest in their business. Financial statements include the several

information regarding operational expenses such as wages, liabilities and other information about

financial assets. Certain studies show that by reviewing financial statements, managers can make

more strategic decisions on how the organization works and increase commercial quality by 20

per cent and it further helps in improving profit margin.

Question 2

1. Calculate the following ratios and interpret the results

It is a technique which is implemented by entities to conduct an objective study of evidence

in a company's financial statements (Laing and Perrin, 2018). Such as ratios analysis is

the measurement which is based on the performance and it will compared current year

performances with earlier years, in order to evaluate the outcome of the company. By contrast,

the ratio method is used mainly by the practitioners to make their investment decisions.

Calculation of ratio is as followed:

Gross profit margin:

Year 1 Year 2

Gross Profit £ 1,920 £ 2,200

Revenues £ 4,940 £ 6,850

Gross Profit Margin (%) 38.86 % 32.11 %

Interpretation: Based on the above estimate, it was calculated that company generated

38.86 percent gross profit in the first year and 32.11 percent in the 2nd year. Overall profitability

of the company reduces which affect the overall performance of the company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

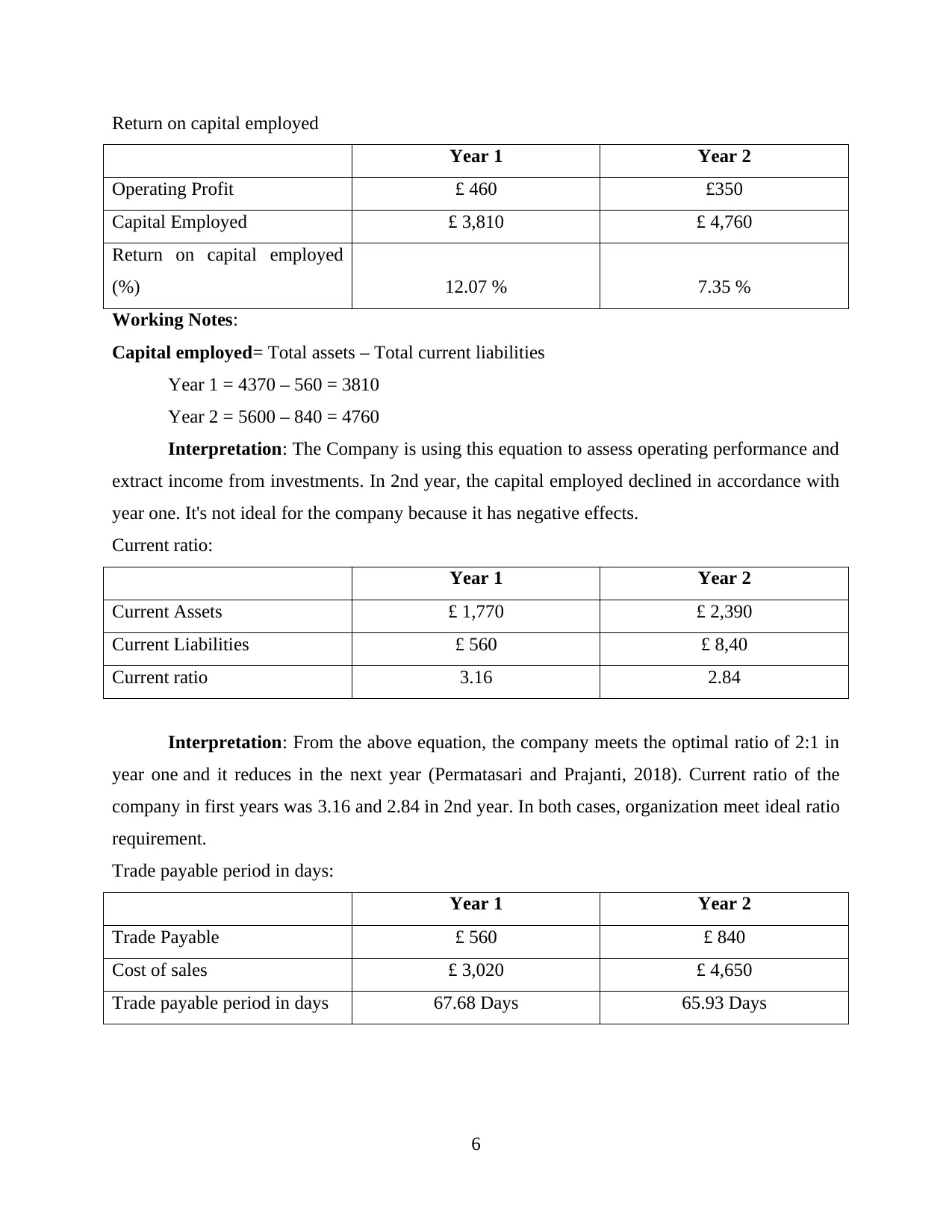

Return on capital employed

Year 1 Year 2

Operating Profit £ 460 £350

Capital Employed £ 3,810 £ 4,760

Return on capital employed

(%) 12.07 % 7.35 %

Working Notes:

Capital employed= Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Interpretation: The Company is using this equation to assess operating performance and

extract income from investments. In 2nd year, the capital employed declined in accordance with

year one. It's not ideal for the company because it has negative effects.

Current ratio:

Year 1 Year 2

Current Assets £ 1,770 £ 2,390

Current Liabilities £ 560 £ 8,40

Current ratio 3.16 2.84

Interpretation: From the above equation, the company meets the optimal ratio of 2:1 in

year one and it reduces in the next year (Permatasari and Prajanti, 2018). Current ratio of the

company in first years was 3.16 and 2.84 in 2nd year. In both cases, organization meet ideal ratio

requirement.

Trade payable period in days:

Year 1 Year 2

Trade Payable £ 560 £ 840

Cost of sales £ 3,020 £ 4,650

Trade payable period in days 67.68 Days 65.93 Days

6

Year 1 Year 2

Operating Profit £ 460 £350

Capital Employed £ 3,810 £ 4,760

Return on capital employed

(%) 12.07 % 7.35 %

Working Notes:

Capital employed= Total assets – Total current liabilities

Year 1 = 4370 – 560 = 3810

Year 2 = 5600 – 840 = 4760

Interpretation: The Company is using this equation to assess operating performance and

extract income from investments. In 2nd year, the capital employed declined in accordance with

year one. It's not ideal for the company because it has negative effects.

Current ratio:

Year 1 Year 2

Current Assets £ 1,770 £ 2,390

Current Liabilities £ 560 £ 8,40

Current ratio 3.16 2.84

Interpretation: From the above equation, the company meets the optimal ratio of 2:1 in

year one and it reduces in the next year (Permatasari and Prajanti, 2018). Current ratio of the

company in first years was 3.16 and 2.84 in 2nd year. In both cases, organization meet ideal ratio

requirement.

Trade payable period in days:

Year 1 Year 2

Trade Payable £ 560 £ 840

Cost of sales £ 3,020 £ 4,650

Trade payable period in days 67.68 Days 65.93 Days

6

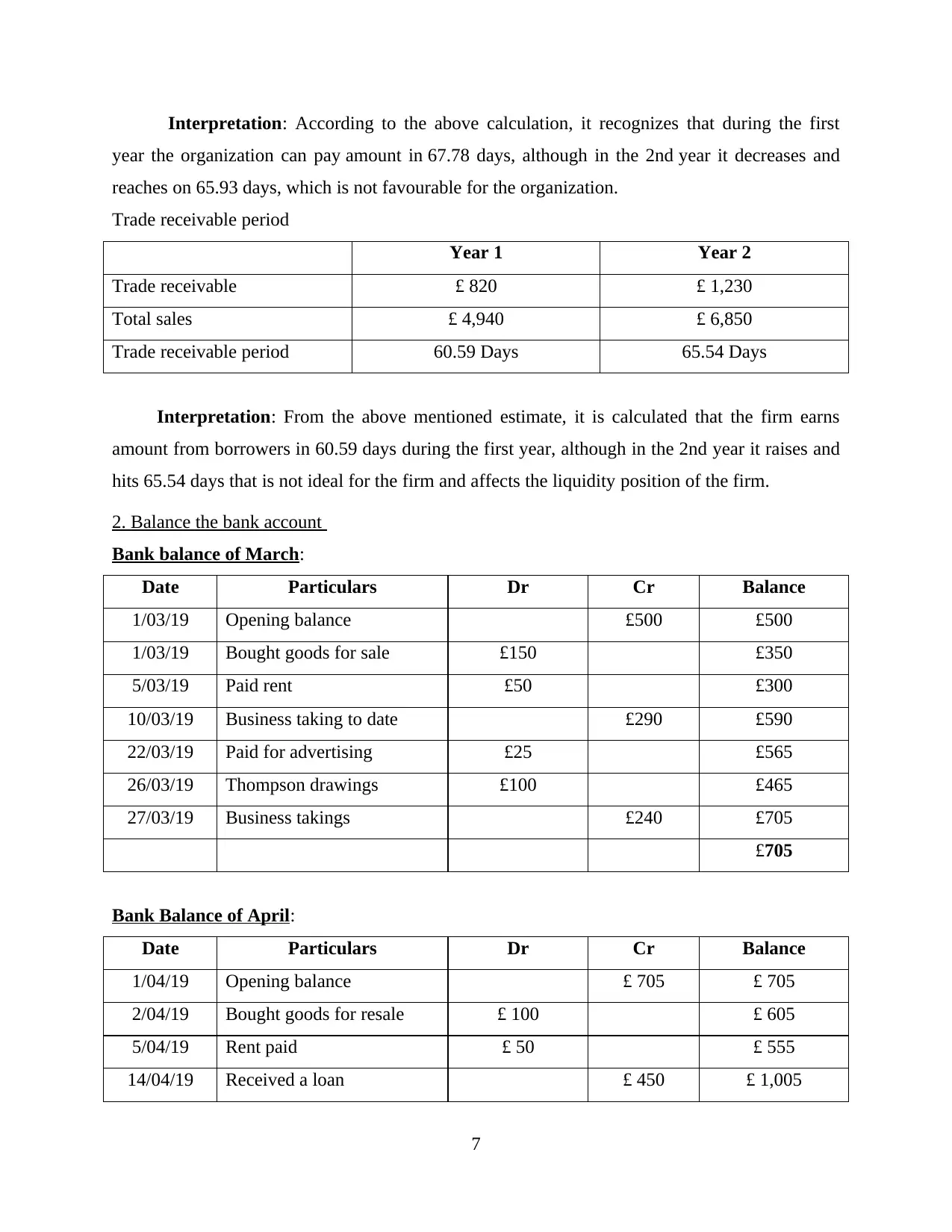

Interpretation: According to the above calculation, it recognizes that during the first

year the organization can pay amount in 67.78 days, although in the 2nd year it decreases and

reaches on 65.93 days, which is not favourable for the organization.

Trade receivable period

Year 1 Year 2

Trade receivable £ 820 £ 1,230

Total sales £ 4,940 £ 6,850

Trade receivable period 60.59 Days 65.54 Days

Interpretation: From the above mentioned estimate, it is calculated that the firm earns

amount from borrowers in 60.59 days during the first year, although in the 2nd year it raises and

hits 65.54 days that is not ideal for the firm and affects the liquidity position of the firm.

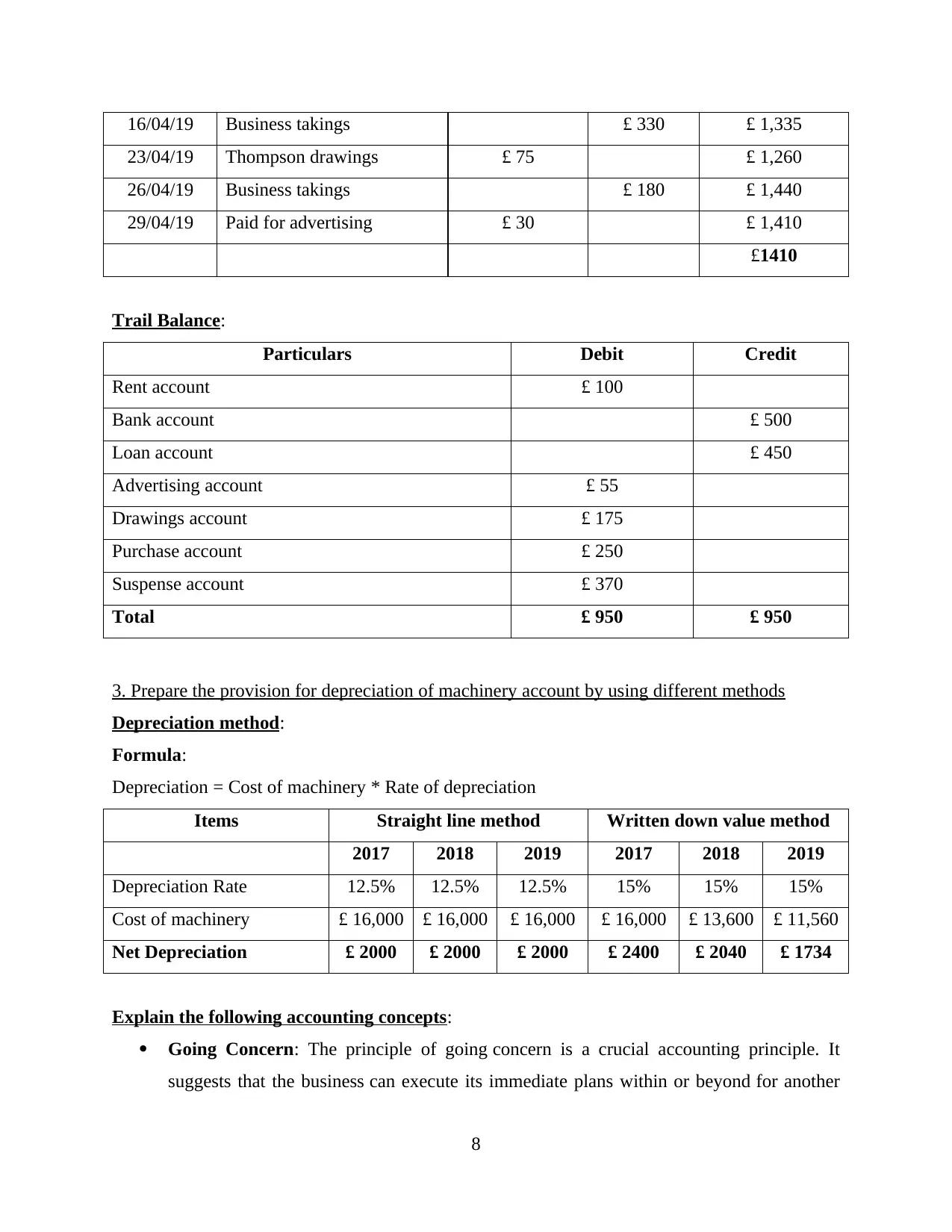

2. Balance the bank account

Bank balance of March:

Date Particulars Dr Cr Balance

1/03/19 Opening balance £500 £500

1/03/19 Bought goods for sale £150 £350

5/03/19 Paid rent £50 £300

10/03/19 Business taking to date £290 £590

22/03/19 Paid for advertising £25 £565

26/03/19 Thompson drawings £100 £465

27/03/19 Business takings £240 £705

£705

Bank Balance of April:

Date Particulars Dr Cr Balance

1/04/19 Opening balance £ 705 £ 705

2/04/19 Bought goods for resale £ 100 £ 605

5/04/19 Rent paid £ 50 £ 555

14/04/19 Received a loan £ 450 £ 1,005

7

year the organization can pay amount in 67.78 days, although in the 2nd year it decreases and

reaches on 65.93 days, which is not favourable for the organization.

Trade receivable period

Year 1 Year 2

Trade receivable £ 820 £ 1,230

Total sales £ 4,940 £ 6,850

Trade receivable period 60.59 Days 65.54 Days

Interpretation: From the above mentioned estimate, it is calculated that the firm earns

amount from borrowers in 60.59 days during the first year, although in the 2nd year it raises and

hits 65.54 days that is not ideal for the firm and affects the liquidity position of the firm.

2. Balance the bank account

Bank balance of March:

Date Particulars Dr Cr Balance

1/03/19 Opening balance £500 £500

1/03/19 Bought goods for sale £150 £350

5/03/19 Paid rent £50 £300

10/03/19 Business taking to date £290 £590

22/03/19 Paid for advertising £25 £565

26/03/19 Thompson drawings £100 £465

27/03/19 Business takings £240 £705

£705

Bank Balance of April:

Date Particulars Dr Cr Balance

1/04/19 Opening balance £ 705 £ 705

2/04/19 Bought goods for resale £ 100 £ 605

5/04/19 Rent paid £ 50 £ 555

14/04/19 Received a loan £ 450 £ 1,005

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

16/04/19 Business takings £ 330 £ 1,335

23/04/19 Thompson drawings £ 75 £ 1,260

26/04/19 Business takings £ 180 £ 1,440

29/04/19 Paid for advertising £ 30 £ 1,410

£1410

Trail Balance:

Particulars Debit Credit

Rent account £ 100

Bank account £ 500

Loan account £ 450

Advertising account £ 55

Drawings account £ 175

Purchase account £ 250

Suspense account £ 370

Total £ 950 £ 950

3. Prepare the provision for depreciation of machinery account by using different methods

Depreciation method:

Formula:

Depreciation = Cost of machinery * Rate of depreciation

Items Straight line method Written down value method

2017 2018 2019 2017 2018 2019

Depreciation Rate 12.5% 12.5% 12.5% 15% 15% 15%

Cost of machinery £ 16,000 £ 16,000 £ 16,000 £ 16,000 £ 13,600 £ 11,560

Net Depreciation £ 2000 £ 2000 £ 2000 £ 2400 £ 2040 £ 1734

Explain the following accounting concepts:

Going Concern: The principle of going concern is a crucial accounting principle. It

suggests that the business can execute its immediate plans within or beyond for another

8

23/04/19 Thompson drawings £ 75 £ 1,260

26/04/19 Business takings £ 180 £ 1,440

29/04/19 Paid for advertising £ 30 £ 1,410

£1410

Trail Balance:

Particulars Debit Credit

Rent account £ 100

Bank account £ 500

Loan account £ 450

Advertising account £ 55

Drawings account £ 175

Purchase account £ 250

Suspense account £ 370

Total £ 950 £ 950

3. Prepare the provision for depreciation of machinery account by using different methods

Depreciation method:

Formula:

Depreciation = Cost of machinery * Rate of depreciation

Items Straight line method Written down value method

2017 2018 2019 2017 2018 2019

Depreciation Rate 12.5% 12.5% 12.5% 15% 15% 15%

Cost of machinery £ 16,000 £ 16,000 £ 16,000 £ 16,000 £ 13,600 £ 11,560

Net Depreciation £ 2000 £ 2000 £ 2000 £ 2400 £ 2040 £ 1734

Explain the following accounting concepts:

Going Concern: The principle of going concern is a crucial accounting principle. It

suggests that the business can execute its immediate plans within or beyond for another

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fiscal period, incorporate its existing resources and proceed to accomplish its financial

responsibilities (Schroeder, Clark and Cathey, 2019). Clearly put, it's an expectation that

the firm will stay in operation and also that the valuation of the properties will continue.

The fundamental theory is known as idea of ongoing care. When an accountant has cause

to question a company's ability to operate as a corporation to uphold its commitments to

protect its properties, it is their responsibility to disclose that in its audit or

inspection report.

Materiality: Consequently, materiality represents the value of the sales, accounts and

errors found in the financial reports. Materiality determines the limit or restricted point at

which financial data is important to the users and it helps in making decision as per the

need. Therefore, the facts found in the financial documents must be accurate in all

relevant ways, so that they may provide a real and reasonable view of the firm's affairs

(Weygandt, Kimmel and Kieso, 2019). This is a subject of judgment that knowledge is

true. The materiality concept works like a filtration system via which organisations sifts

knowledge. Its aim is to protect that financial data which might affect the decision of

shareholders is included with the financial reports.

Business entity concept: It states that the activities related to a business must be kept

separated from its owners or their competitors. It includes the use for entity of different

accounting reports which fully exempt any other individual or owner's assets and debts.

Because of the following reasons these accounting concepts are of significant importance.

Auditing a company's documents is complicated and futile as they are interacted with that

of multiple entities or individuals. The definition guarantees independent taxes on each

and almost every corporate entity.

CONCLUSION

On the basis of above discussion it was observed that the every organization use accounting

information to assess the overall financial position of the company. Within organization, various

types of reports prepared to reflect actual financial results and allow company management to

make the best decision. Trading account, income statements, balance sheet, cash flow statements

are made to analyze the financial results. For this specific reason even it helps in measuring the

overall performance by using ratio analysis. This ratio analysis help the inventors to made their

decisions regarding future investment.

9

responsibilities (Schroeder, Clark and Cathey, 2019). Clearly put, it's an expectation that

the firm will stay in operation and also that the valuation of the properties will continue.

The fundamental theory is known as idea of ongoing care. When an accountant has cause

to question a company's ability to operate as a corporation to uphold its commitments to

protect its properties, it is their responsibility to disclose that in its audit or

inspection report.

Materiality: Consequently, materiality represents the value of the sales, accounts and

errors found in the financial reports. Materiality determines the limit or restricted point at

which financial data is important to the users and it helps in making decision as per the

need. Therefore, the facts found in the financial documents must be accurate in all

relevant ways, so that they may provide a real and reasonable view of the firm's affairs

(Weygandt, Kimmel and Kieso, 2019). This is a subject of judgment that knowledge is

true. The materiality concept works like a filtration system via which organisations sifts

knowledge. Its aim is to protect that financial data which might affect the decision of

shareholders is included with the financial reports.

Business entity concept: It states that the activities related to a business must be kept

separated from its owners or their competitors. It includes the use for entity of different

accounting reports which fully exempt any other individual or owner's assets and debts.

Because of the following reasons these accounting concepts are of significant importance.

Auditing a company's documents is complicated and futile as they are interacted with that

of multiple entities or individuals. The definition guarantees independent taxes on each

and almost every corporate entity.

CONCLUSION

On the basis of above discussion it was observed that the every organization use accounting

information to assess the overall financial position of the company. Within organization, various

types of reports prepared to reflect actual financial results and allow company management to

make the best decision. Trading account, income statements, balance sheet, cash flow statements

are made to analyze the financial results. For this specific reason even it helps in measuring the

overall performance by using ratio analysis. This ratio analysis help the inventors to made their

decisions regarding future investment.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.