Financial Accounting Process: Solution for ChiHerbal Ltd, ACCT6003

VerifiedAdded on 2023/01/19

|12

|1800

|98

Homework Assignment

AI Summary

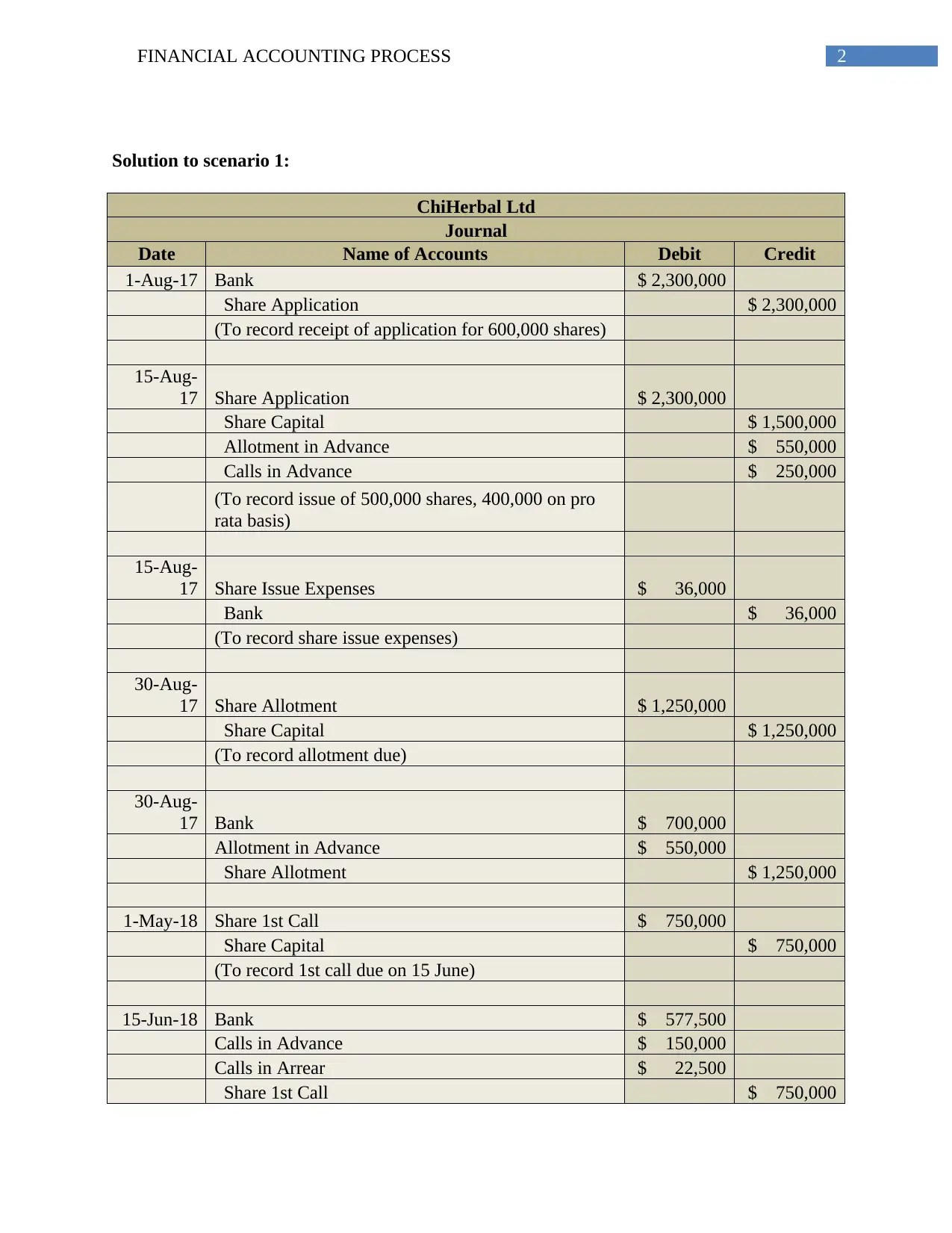

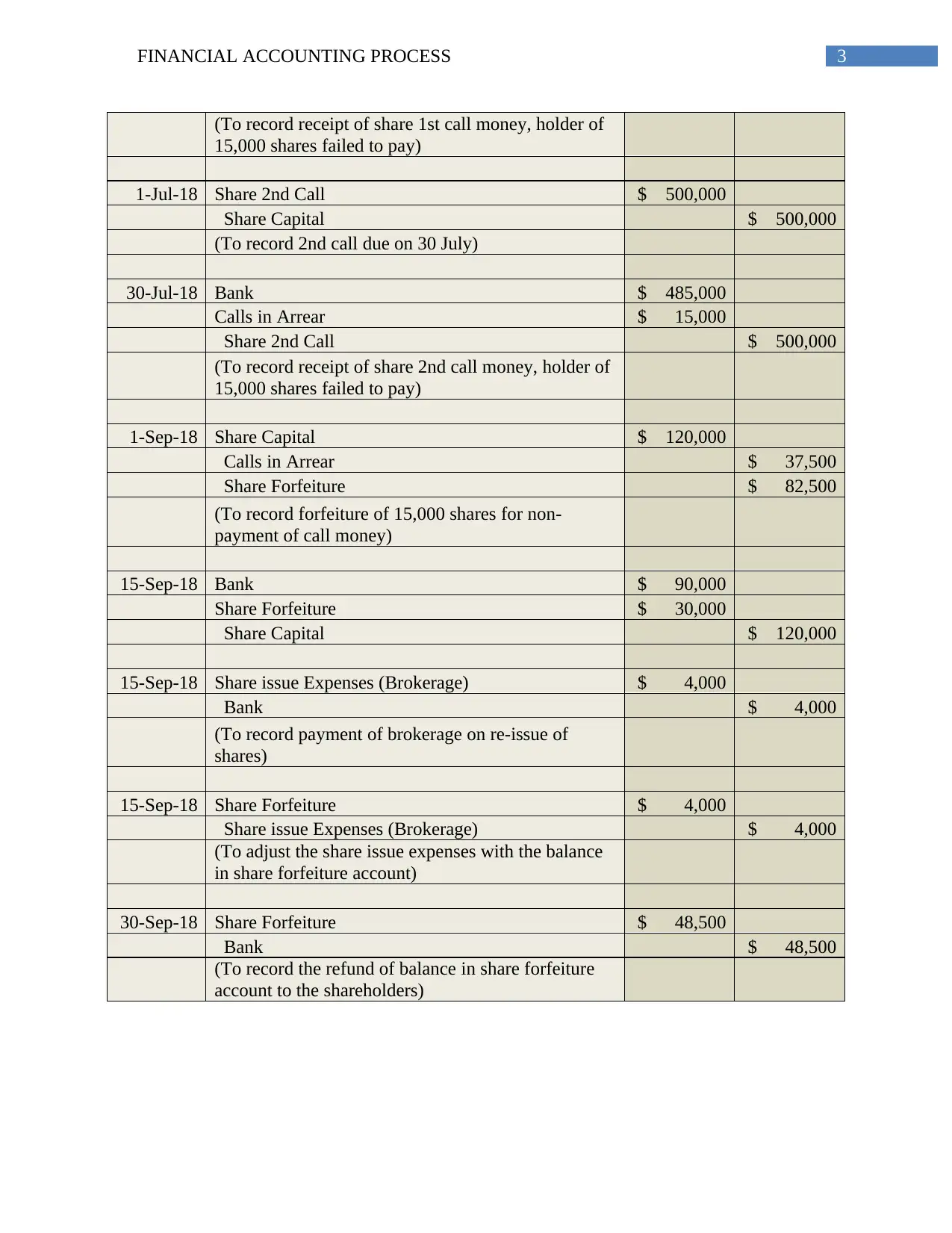

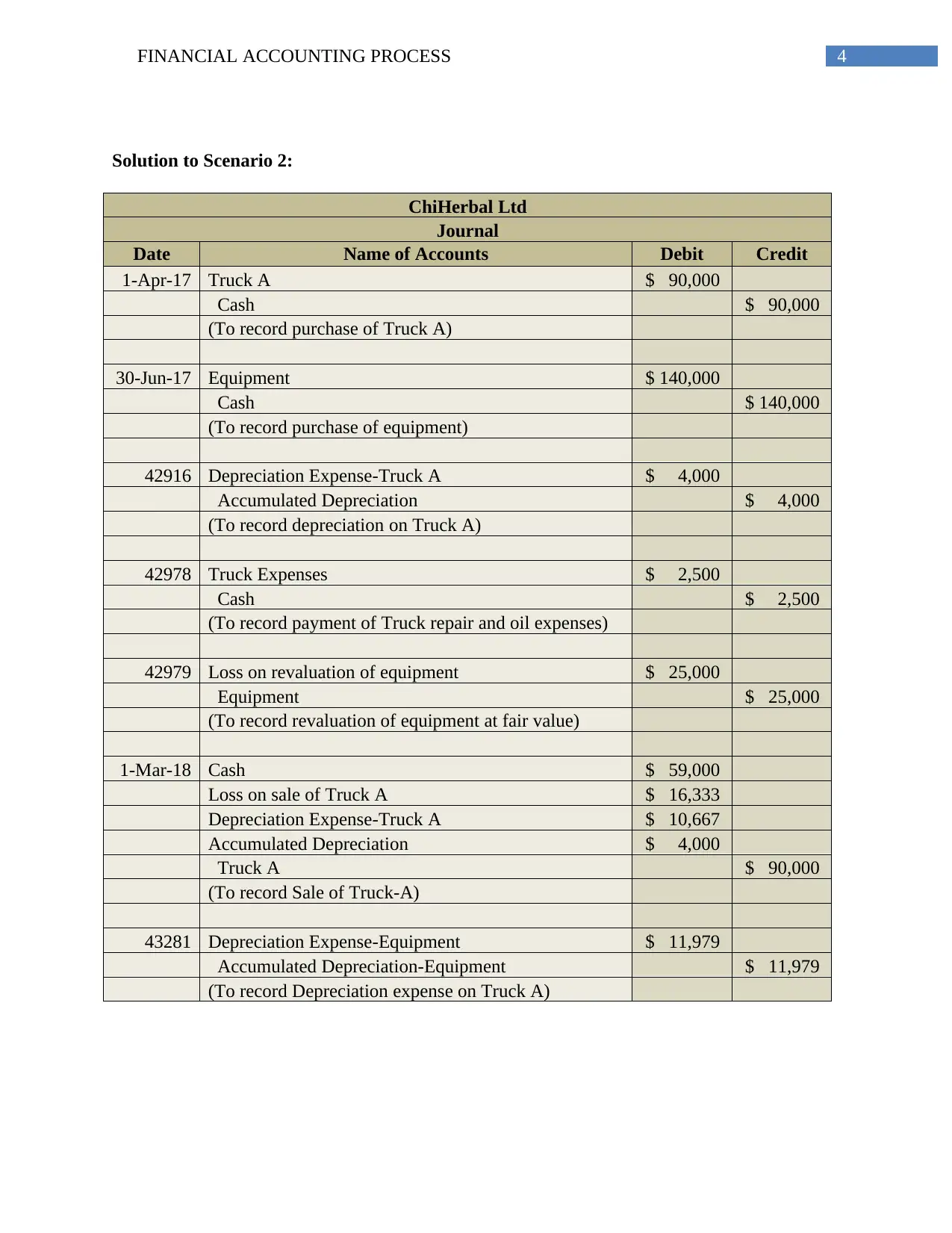

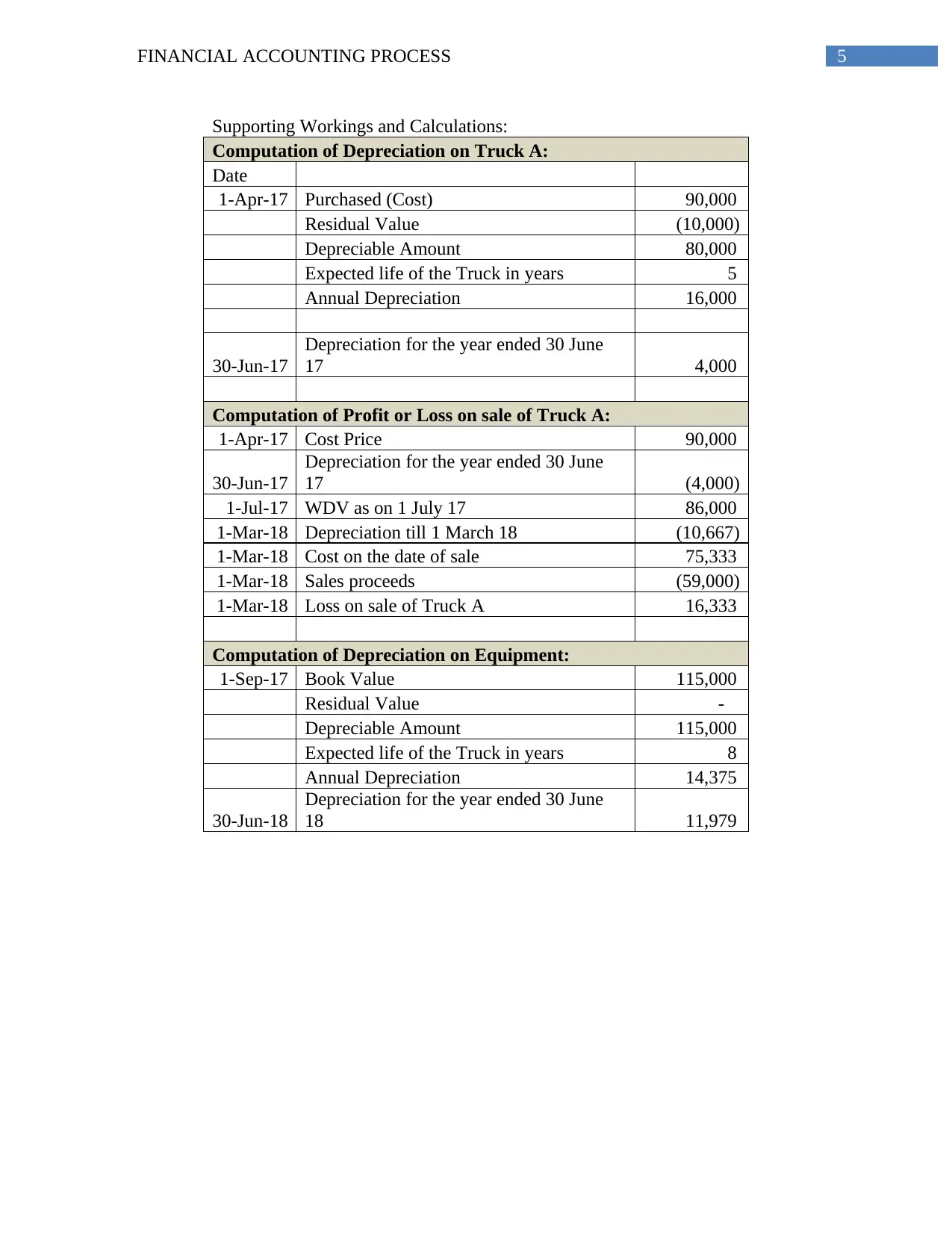

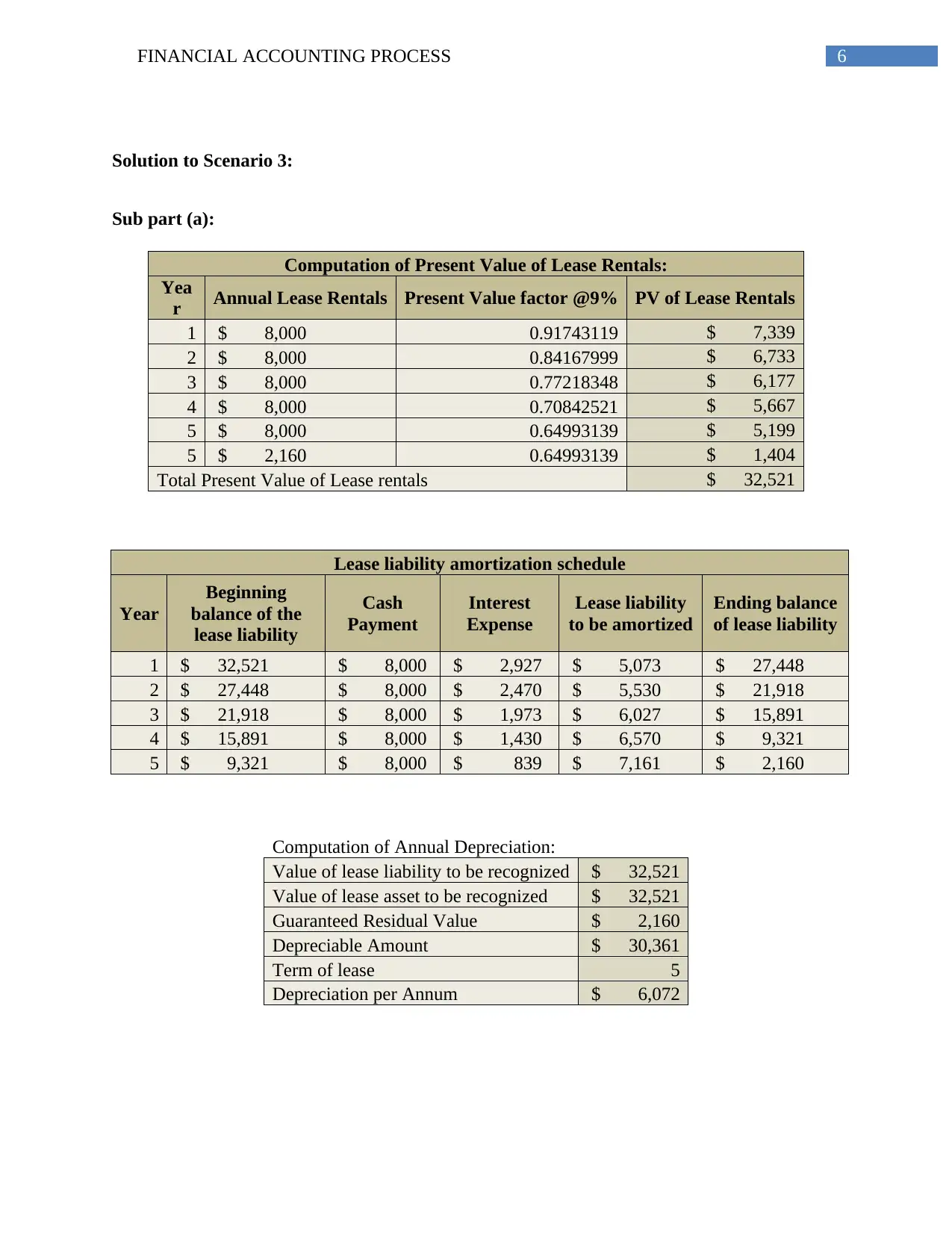

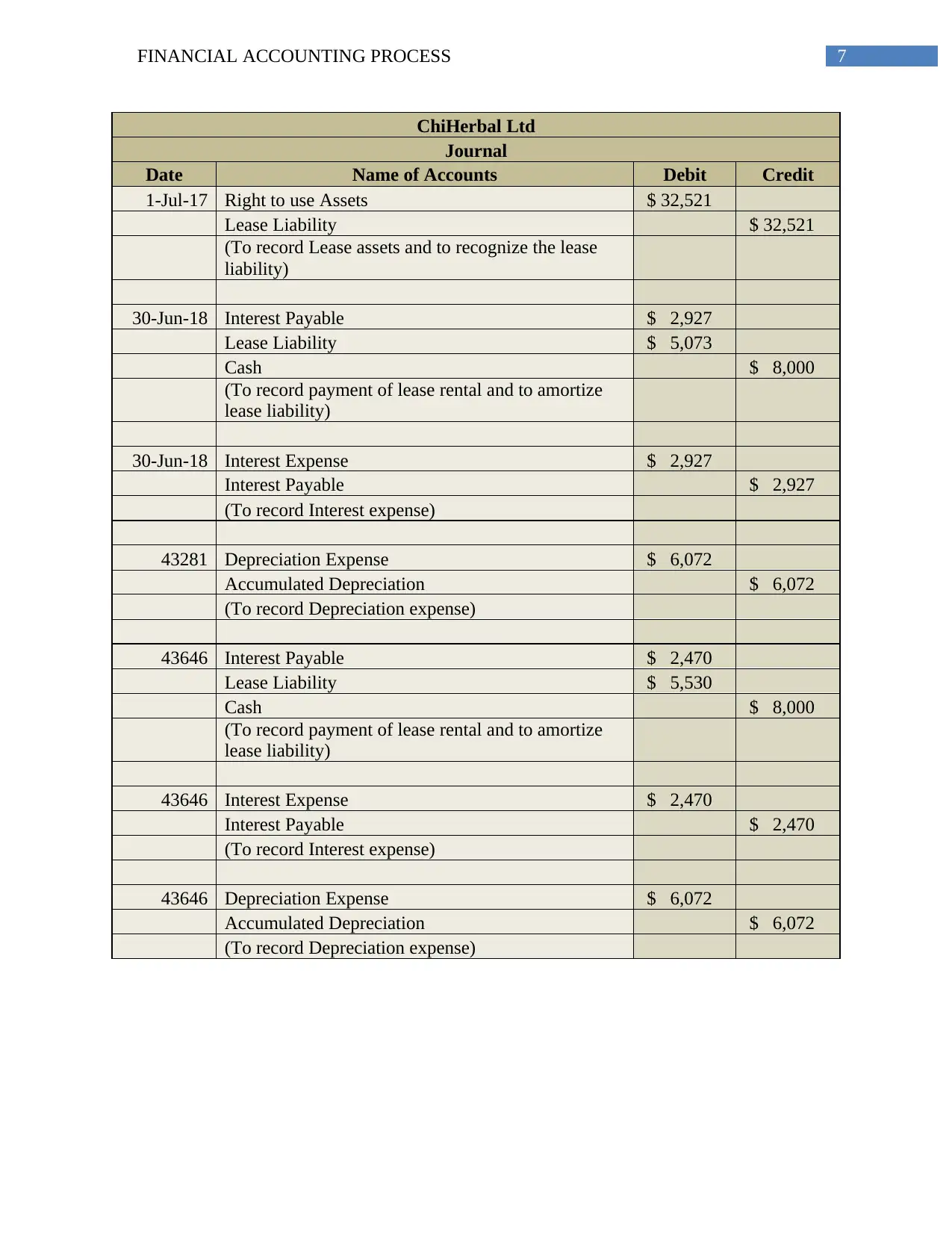

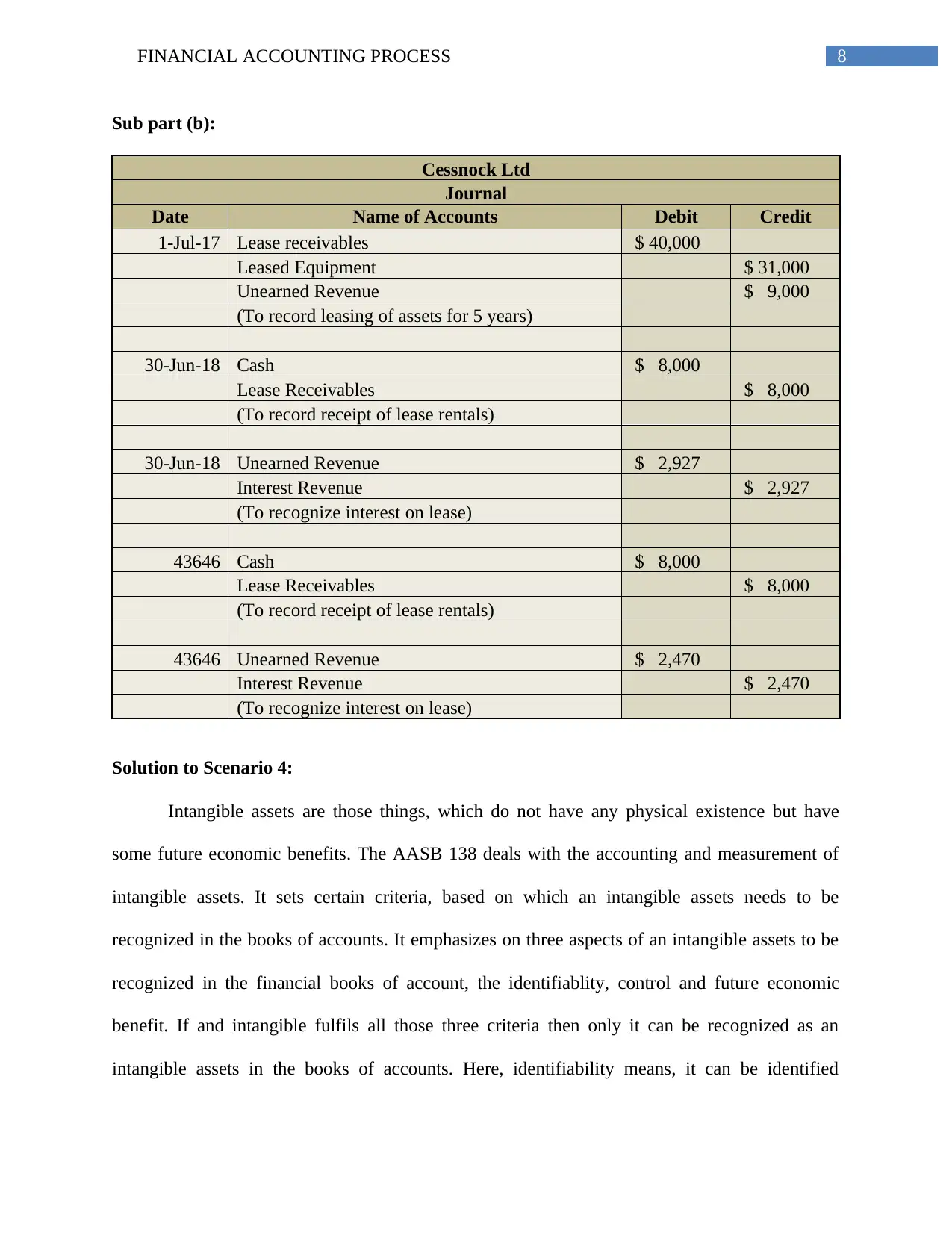

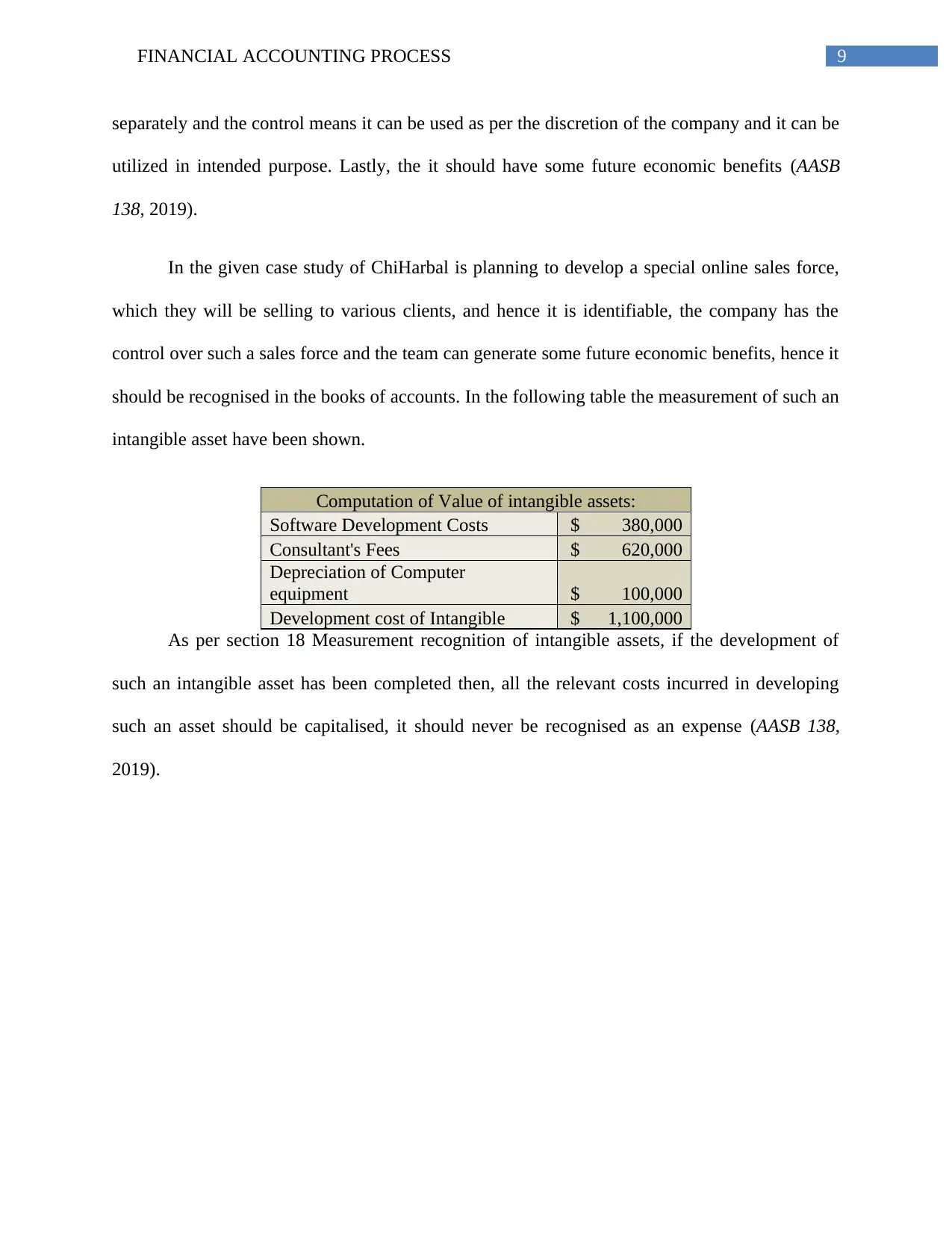

This document presents a comprehensive solution to a financial accounting assignment centered around ChiHerbal Ltd, a company transitioning from a private to a public structure. The solution meticulously details journal entries for share issues, including application receipts, share allotments, and call money transactions, addressing scenarios like share issue expenses and share forfeitures. Furthermore, it provides detailed accounting for non-current assets such as trucks and equipment, including depreciation calculations and the accounting treatment for asset revaluations and disposals. The assignment also delves into lease accounting, covering the present value of lease rentals, amortization schedules, and journal entries for both the lessee and lessor. Finally, it addresses the accounting for intangible assets, specifically focusing on the recognition and measurement of development costs for an online sales force, referencing AASB 138 guidelines.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.