Moneykart Internship Journal: Financial Advisory Experience

VerifiedAdded on 2022/10/04

|29

|8301

|20

Report

AI Summary

This report details an internship experience at Moneykart, a financial advisory company in New Zealand. The report begins with an introduction to Moneykart, its services including mortgages and insurance, and its operational structure. The core of the report analyzes the intern's experience, including tasks like managing client portfolios, understanding loan review systems, and engaging in service and digital marketing. The analysis connects the internship activities to the student's MBA modules, such as Financial and Management Accounting, Quality Management, and Marketing. Specific activities like understanding lending principles, financial statement analysis, and the company's quality assurance processes are examined. The report includes discussions on the company's unique aspects, joint ventures, and human resources. It concludes with recommendations for the intern's improvement and suggestions for the organization, highlighting the benefits of the internship and areas for future development within Moneykart's financial advisory services.

Page 1

INTERNSHIP REPORT

TABLE OF CONTENT

1.0 INTRODUCTION.............................................................................................................. 3

1.1 Place of Attachment..........................................................................................................3

1.2 Company Overview...........................................................................................................3

1.2.1 Company slogan.................................................................................................................................4

1.2.2 Company Mission...............................................................................................................................4

1.2.3 Company Vision.................................................................................................................................4

1.2.4 Company Core Values........................................................................................................................4

1.3 Field of Specialization........................................................................................................4

1.3.1 Mortgages...........................................................................................................................................4

1.3.2 Insurance.............................................................................................................................................5

1.4 What makes the company unique?.....................................................................................5

1.5 Joint ventures.................................................................................................................... 5

1.6 Human Resource...............................................................................................................5

1.7 Company Organization chart.............................................................................................6

2.0 DISCUSSION AND ANALYSIS OF EXPERIENCE GAINED.......................7

2.1 Introduction……………………………………………………………………………………….7

2.2 Discussion and Analysis of selected activities done..............................................................8

2.2.1 Operating a financial company in New Zealand................................................................................8

2.2.2 Loan Review System..........................................................................................................................8

2.2.3 Ratio Analysis..................................................................................................................................10

2.2.4 Service Marketing and Digital Marketing........................................................................................17

2.2.5 Culture and lending..........................................................................................................................17

2.2.6 E-business and Digital Marketing....................................................................................................18

2.2.7 Quality Assurance............................................................................................................................21

2.2.8 Health insurance...............................................................................................................................22

2.2.9 Principles of lending.........................................................................................................................24

3.0 CONCLUSION AND RECOMMENDATION.......................................26

3.1 Conclusion...................................................................................................26

3.2 Recommendation..........................................................................................26

4.0 References......................................................................................28

INTERNSHIP REPORT

TABLE OF CONTENT

1.0 INTRODUCTION.............................................................................................................. 3

1.1 Place of Attachment..........................................................................................................3

1.2 Company Overview...........................................................................................................3

1.2.1 Company slogan.................................................................................................................................4

1.2.2 Company Mission...............................................................................................................................4

1.2.3 Company Vision.................................................................................................................................4

1.2.4 Company Core Values........................................................................................................................4

1.3 Field of Specialization........................................................................................................4

1.3.1 Mortgages...........................................................................................................................................4

1.3.2 Insurance.............................................................................................................................................5

1.4 What makes the company unique?.....................................................................................5

1.5 Joint ventures.................................................................................................................... 5

1.6 Human Resource...............................................................................................................5

1.7 Company Organization chart.............................................................................................6

2.0 DISCUSSION AND ANALYSIS OF EXPERIENCE GAINED.......................7

2.1 Introduction……………………………………………………………………………………….7

2.2 Discussion and Analysis of selected activities done..............................................................8

2.2.1 Operating a financial company in New Zealand................................................................................8

2.2.2 Loan Review System..........................................................................................................................8

2.2.3 Ratio Analysis..................................................................................................................................10

2.2.4 Service Marketing and Digital Marketing........................................................................................17

2.2.5 Culture and lending..........................................................................................................................17

2.2.6 E-business and Digital Marketing....................................................................................................18

2.2.7 Quality Assurance............................................................................................................................21

2.2.8 Health insurance...............................................................................................................................22

2.2.9 Principles of lending.........................................................................................................................24

3.0 CONCLUSION AND RECOMMENDATION.......................................26

3.1 Conclusion...................................................................................................26

3.2 Recommendation..........................................................................................26

4.0 References......................................................................................28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 2

INTERNSHIP REPORT

LIST OF FIGURES

Figure 1. 1 Company Organization Chart...............................................................................................6FIGURE 2. 1 LOAN REVIEW PROCESS.........................................................................10

Figure 2. 2 Moneykart Facebook page....................................................................................19

Figure 2. 3 Types of services offered for online booking.........................................................19

Figure 2. 4 Pop-out for selecting the date and time for an appointment.................................20

Figure 2. 5 Pop-out for giving contact details.........................................................................20

Figure 2. 6 Pop-out for successful appointment booking........................................................21

LIST OF TABLES

Table 2. 1 Ibrahim’s Laundry business financial statement....................................................10

Table 2. 2 Profitability Ratios..................................................................................................15

Table 2. 3 Turnover Ratios......................................................................................................15

Table 2. 4 Quality Assurance codes.........................................................................................21

Table 2. 5 Groups covered by NIB...........................................................................................22

INTERNSHIP REPORT

LIST OF FIGURES

Figure 1. 1 Company Organization Chart...............................................................................................6FIGURE 2. 1 LOAN REVIEW PROCESS.........................................................................10

Figure 2. 2 Moneykart Facebook page....................................................................................19

Figure 2. 3 Types of services offered for online booking.........................................................19

Figure 2. 4 Pop-out for selecting the date and time for an appointment.................................20

Figure 2. 5 Pop-out for giving contact details.........................................................................20

Figure 2. 6 Pop-out for successful appointment booking........................................................21

LIST OF TABLES

Table 2. 1 Ibrahim’s Laundry business financial statement....................................................10

Table 2. 2 Profitability Ratios..................................................................................................15

Table 2. 3 Turnover Ratios......................................................................................................15

Table 2. 4 Quality Assurance codes.........................................................................................21

Table 2. 5 Groups covered by NIB...........................................................................................22

Page 3

INTERNSHIP REPORT

1.0 INTRODUCTION

1.1 Place of Attachment

The internship commenced on 19th August and ended 10th October 2019 (32 days) at

Moneykart, New Lynn.

1.2 Company Overview

Moneykart, Dainton, was founded and officially registered in May 2017 with registration

number 9429046103192 (Bizdb, 2019). The company, bearing company number 6275388,

was founded by Rajesh Krishnamurthy, the current director.

Rajesh Krishnamurthy is the principal adviser and a marketing communications specialist

with a vast experience in the financial industry of New Zealand (Rajesh, 2019). He has over

20 years of experience in international markets and good masterly in penetrating new markets

and ensuring business sustainability. He has worked in various companies like Westpac New

Zealand Limited, a senior banker at ANZ, a business consultant and New Business

Consultant. The company was registered under the K641930 Mortgage Broking Service

category.

The main office is located at Dainton Place at New Lynn, Auckland 00600.

Telephone: 09-8277887

Fax: 021 03 27466.

E-mail: rajesh@monekart.co.nz

Website: www.moneykart.biz

Moneykart is a financial advisory company that has been in the industry for about two years.

It mainly focuses on offering financial services and products ranging from loans, insurance

and KiwiSaver (Moneykart, 2019). With the two years in the financial industry, the firm has a

vast knowledge of the market trends and customer needs hence has fought tirelessly towards

rising and offering the best and competitive services to the clients. It has, therefore, reached

various clients over this period offering various services and meeting their financial needs

appropriately. The company has always aimed at offering New Zealanders with solutions to

their financial problems and assisting them in achieving their financial goals.

The company is registered with the Financial Markets Authority of New Zealand hence it is

in total compliance with the code of conduct and ethics as provided by the authority and the

profession itself. This has enhanced the trustworthy of the company to the clients it serves.

The firm further operates in for 24 hours to serve as many clients as possible. Experienced

INTERNSHIP REPORT

1.0 INTRODUCTION

1.1 Place of Attachment

The internship commenced on 19th August and ended 10th October 2019 (32 days) at

Moneykart, New Lynn.

1.2 Company Overview

Moneykart, Dainton, was founded and officially registered in May 2017 with registration

number 9429046103192 (Bizdb, 2019). The company, bearing company number 6275388,

was founded by Rajesh Krishnamurthy, the current director.

Rajesh Krishnamurthy is the principal adviser and a marketing communications specialist

with a vast experience in the financial industry of New Zealand (Rajesh, 2019). He has over

20 years of experience in international markets and good masterly in penetrating new markets

and ensuring business sustainability. He has worked in various companies like Westpac New

Zealand Limited, a senior banker at ANZ, a business consultant and New Business

Consultant. The company was registered under the K641930 Mortgage Broking Service

category.

The main office is located at Dainton Place at New Lynn, Auckland 00600.

Telephone: 09-8277887

Fax: 021 03 27466.

E-mail: rajesh@monekart.co.nz

Website: www.moneykart.biz

Moneykart is a financial advisory company that has been in the industry for about two years.

It mainly focuses on offering financial services and products ranging from loans, insurance

and KiwiSaver (Moneykart, 2019). With the two years in the financial industry, the firm has a

vast knowledge of the market trends and customer needs hence has fought tirelessly towards

rising and offering the best and competitive services to the clients. It has, therefore, reached

various clients over this period offering various services and meeting their financial needs

appropriately. The company has always aimed at offering New Zealanders with solutions to

their financial problems and assisting them in achieving their financial goals.

The company is registered with the Financial Markets Authority of New Zealand hence it is

in total compliance with the code of conduct and ethics as provided by the authority and the

profession itself. This has enhanced the trustworthy of the company to the clients it serves.

The firm further operates in for 24 hours to serve as many clients as possible. Experienced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 4

INTERNSHIP REPORT

and trained advisers of the company are equipped with necessary facilities like computers and

the internet to serve clients efficiently in an attempt to provide solutions to their financial

problems. Interestingly, the firm has deployed simple and customer friendly procedures when

dealing with customers.

1.2.1 Company slogan

Moneykart, simplifying finance.

1.2.2 Company Mission

Moneykart is on a mission to make the complicated world of finance simple and easy to

understand (Moneykart, 2019).

1.2.3 Company Vision

Moneykart’s vision is to be recognized as the premier financial services advisory firm

specializing in Mortgages, Risk Management and KiwiSaver in New Zealand (Moneykart,

2019).

1.2.4 Company Core Values

You before I

Trust,

Transparency,

Integrity

Ethics.

1.3 Field of Specialization

Moneykart offer a wide range of financial services in an attempt to meet the needs of the

customers. The following section presents the services offered by Moneykart.

1.3.1 Mortgages

According to Investopedia, a mortgage is a claim on a property. It is defined as a debt

instrument with collateral that is used in a particular real estate property where the borrower

agrees and signs a commitment to return the predetermined amount over the specified period.

Individuals and businesses can use mortgages to acquire property without the initial amount

of full payment. The one taking the mortgage is then required to agree on the payment terms

and the period of payment. The terms of payments, in this case, involve the interests (Kagan,

2019). Under this package, the firm also gives consultancy services on the home loans and

the most suitable payment plan for the customer.

INTERNSHIP REPORT

and trained advisers of the company are equipped with necessary facilities like computers and

the internet to serve clients efficiently in an attempt to provide solutions to their financial

problems. Interestingly, the firm has deployed simple and customer friendly procedures when

dealing with customers.

1.2.1 Company slogan

Moneykart, simplifying finance.

1.2.2 Company Mission

Moneykart is on a mission to make the complicated world of finance simple and easy to

understand (Moneykart, 2019).

1.2.3 Company Vision

Moneykart’s vision is to be recognized as the premier financial services advisory firm

specializing in Mortgages, Risk Management and KiwiSaver in New Zealand (Moneykart,

2019).

1.2.4 Company Core Values

You before I

Trust,

Transparency,

Integrity

Ethics.

1.3 Field of Specialization

Moneykart offer a wide range of financial services in an attempt to meet the needs of the

customers. The following section presents the services offered by Moneykart.

1.3.1 Mortgages

According to Investopedia, a mortgage is a claim on a property. It is defined as a debt

instrument with collateral that is used in a particular real estate property where the borrower

agrees and signs a commitment to return the predetermined amount over the specified period.

Individuals and businesses can use mortgages to acquire property without the initial amount

of full payment. The one taking the mortgage is then required to agree on the payment terms

and the period of payment. The terms of payments, in this case, involve the interests (Kagan,

2019). Under this package, the firm also gives consultancy services on the home loans and

the most suitable payment plan for the customer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 5

INTERNSHIP REPORT

1.3.2 Insurance

In a nutshell, insurance is to protect against a peril or a loss at a cost. The company covers

both life and non-life insurance. These include life, family, assets, trauma, total permanent

disability, income protection, mortgage protection, health insurance, and liabilities among

other things. Other forms of insurance offered in the company include travel insurance which

covers one for such events as repatriation, lost luggage, medical emergencies or even trip

canceled due to unavoidable circumstances.

1.4 What makes the company unique?

As an attempt for the company to reach a wide range of customers, the company staff have

the potential to communicate with the customers in their respective native languages. Some

of the languages include Hindi, Gujarat, Marathi, Punjabi, Malayalam, and Tamil

(Moneykart, 2019).

1.5 Joint ventures

The company has collaborated with renowned associate companies that offer insurance,

lending and loaning services to serve the clients efficiently.

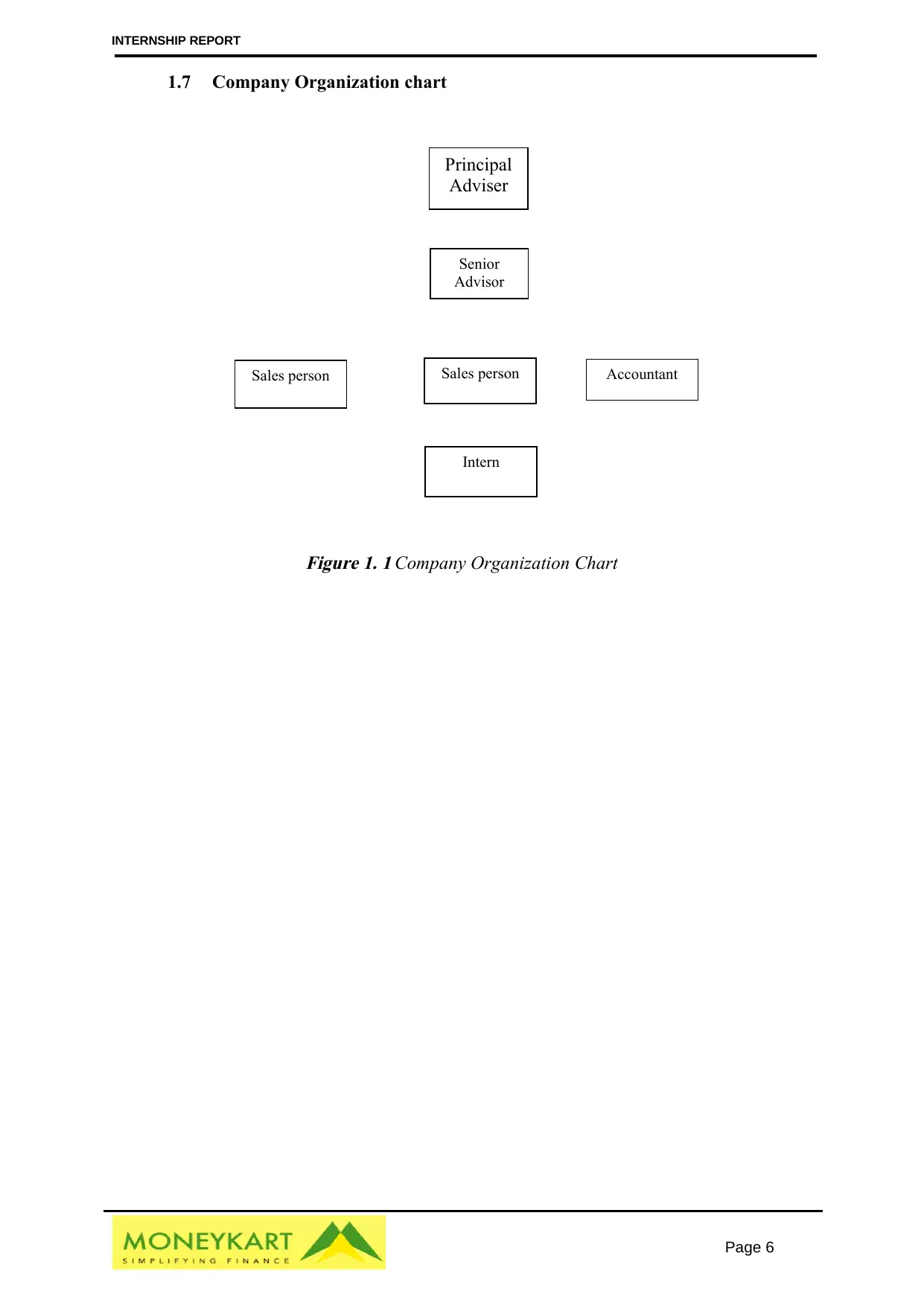

1.6 Human Resource

Moneykart is a single business managed by one person, Rajesh. Moneykart maintains various

categories of personnel comprising of permanent, temporary employees and consultants with

the total available workforce fluctuating around 5 persons to reflect the workload at hand.

These comprise:

Principal advisor.

Senior advisor

Sales people

Intern

INTERNSHIP REPORT

1.3.2 Insurance

In a nutshell, insurance is to protect against a peril or a loss at a cost. The company covers

both life and non-life insurance. These include life, family, assets, trauma, total permanent

disability, income protection, mortgage protection, health insurance, and liabilities among

other things. Other forms of insurance offered in the company include travel insurance which

covers one for such events as repatriation, lost luggage, medical emergencies or even trip

canceled due to unavoidable circumstances.

1.4 What makes the company unique?

As an attempt for the company to reach a wide range of customers, the company staff have

the potential to communicate with the customers in their respective native languages. Some

of the languages include Hindi, Gujarat, Marathi, Punjabi, Malayalam, and Tamil

(Moneykart, 2019).

1.5 Joint ventures

The company has collaborated with renowned associate companies that offer insurance,

lending and loaning services to serve the clients efficiently.

1.6 Human Resource

Moneykart is a single business managed by one person, Rajesh. Moneykart maintains various

categories of personnel comprising of permanent, temporary employees and consultants with

the total available workforce fluctuating around 5 persons to reflect the workload at hand.

These comprise:

Principal advisor.

Senior advisor

Sales people

Intern

Page 6

INTERNSHIP REPORT

1.7 Company Organization chart

Figure 1. 1 Company Organization Chart

Principal

Adviser

Senior

Advisor

Sales person Sales person Accountant

Intern

INTERNSHIP REPORT

1.7 Company Organization chart

Figure 1. 1 Company Organization Chart

Principal

Adviser

Senior

Advisor

Sales person Sales person Accountant

Intern

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 7

INTERNSHIP REPORT

2.0 DISCUSSION AND ANALYSIS OF EXPERIENCE

GAINED

2.1 Introduction

Having discussed the company of internship in the preceding chapter, it is evident that the

firm is actively engaging in the construction industry and hence provides a good opportunity

to acquire some fundamental experiences. In this chapter, the activities that were done during

the internship period have been discussed in detail using typical case studies that were

encountered. My input as an intern has also been discussed regarding the modules learned in

class.

The following described the tasks and responsibilities that my job entailed.

Manage and grow client portfolio across a range of industries.

Track and project financial performance and factors affecting expenses/profitability

on a functional or another basis.

Learning how to actively manage a portfolio through proactive service, and retained

portfolios.

Focus on maintaining client and portfolio profitability.

Maintain professional knowledge and skills on legislative and compliance on products

and technical issues.

However, the following specific issues were carried out during the internship period:

Understanding the basic operations of lending, mortgage, and insurance.

Studying and understanding financial party rights, monetary policies and relevant

regulations like the Service Level Agreement, SLA.

Understanding the role of key players in the industry like lenders, banks, participants

such as aggregators, franchisors, mortgage managers and other providers of broking

services. This also included understanding the key competitors and drivers of the

industry like NIB and AIA who have advanced in their area of specialty in the

financing industry. NIB is one of the largest health insurance providers in New

Zealand.

Relationship between price and quality.

Emerging issues in lending as practiced by typical lending companies like Peer to

Peer which is practiced by Zagga Company. Other current market trends were also

studied.

INTERNSHIP REPORT

2.0 DISCUSSION AND ANALYSIS OF EXPERIENCE

GAINED

2.1 Introduction

Having discussed the company of internship in the preceding chapter, it is evident that the

firm is actively engaging in the construction industry and hence provides a good opportunity

to acquire some fundamental experiences. In this chapter, the activities that were done during

the internship period have been discussed in detail using typical case studies that were

encountered. My input as an intern has also been discussed regarding the modules learned in

class.

The following described the tasks and responsibilities that my job entailed.

Manage and grow client portfolio across a range of industries.

Track and project financial performance and factors affecting expenses/profitability

on a functional or another basis.

Learning how to actively manage a portfolio through proactive service, and retained

portfolios.

Focus on maintaining client and portfolio profitability.

Maintain professional knowledge and skills on legislative and compliance on products

and technical issues.

However, the following specific issues were carried out during the internship period:

Understanding the basic operations of lending, mortgage, and insurance.

Studying and understanding financial party rights, monetary policies and relevant

regulations like the Service Level Agreement, SLA.

Understanding the role of key players in the industry like lenders, banks, participants

such as aggregators, franchisors, mortgage managers and other providers of broking

services. This also included understanding the key competitors and drivers of the

industry like NIB and AIA who have advanced in their area of specialty in the

financing industry. NIB is one of the largest health insurance providers in New

Zealand.

Relationship between price and quality.

Emerging issues in lending as practiced by typical lending companies like Peer to

Peer which is practiced by Zagga Company. Other current market trends were also

studied.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 8

INTERNSHIP REPORT

Calculations and considerations involving interest in different types of mortgages like

home loans, equity release and reverse annuity mortgages. The calculations also

involved determination of loan value ratios, liquidity and current ratio, and how they

are interpreted and applied in making decisions in lending problems.

Recording and keeping the fundamental workbook of the company.

Lending principles.

Lending securities and collaterals.

Using businesses’ financial statements to check for cash flow and determine the loan

status.

Statement of movements in equity as provided by the New Zealand Mortgage Broking

Association.

Strategic market services and digital marketing.

Mortgage risks and their management.

Quality assurance and a zero-defect target.

2.0 Discussion and Analysis of selected activities done

2.0.1 Operating a financial company in New Zealand

To operate a business offering financial services and advises in New Zealand, one must

register with the Financial Markets Authority (FMA) which is the regulatory body (New

Zealand Now, 2019). This requirement applies to banks, non-bank deposit takers, fund

managers, insurers and derivatives issuers (Tim & Chapman, 2016). They must also be

registered in the Financial Service Providers Register maintained by the agency.

I also learned that for insurers like Moneykart, they must be registered with the Reserve

Bank. The license requires that the companies should:

Have an appointed actuary.

Comply with the set policies.

Maintaining solvency and disclosing solvency and credit rating information through

regularly published statements (Tim & Chapman, 2016).

2.0.2 Loan Review System

The Federal Deposit Insurance Corporation (FIDIC) RMS Manual of Examination Policies

and, for accounting and finance defines a loan review system (also known as the credit risk

review system) as a system that involves credit underwriting, loan administration, loan

workout and assembling all the information necessary to establish the appropriateness of

INTERNSHIP REPORT

Calculations and considerations involving interest in different types of mortgages like

home loans, equity release and reverse annuity mortgages. The calculations also

involved determination of loan value ratios, liquidity and current ratio, and how they

are interpreted and applied in making decisions in lending problems.

Recording and keeping the fundamental workbook of the company.

Lending principles.

Lending securities and collaterals.

Using businesses’ financial statements to check for cash flow and determine the loan

status.

Statement of movements in equity as provided by the New Zealand Mortgage Broking

Association.

Strategic market services and digital marketing.

Mortgage risks and their management.

Quality assurance and a zero-defect target.

2.0 Discussion and Analysis of selected activities done

2.0.1 Operating a financial company in New Zealand

To operate a business offering financial services and advises in New Zealand, one must

register with the Financial Markets Authority (FMA) which is the regulatory body (New

Zealand Now, 2019). This requirement applies to banks, non-bank deposit takers, fund

managers, insurers and derivatives issuers (Tim & Chapman, 2016). They must also be

registered in the Financial Service Providers Register maintained by the agency.

I also learned that for insurers like Moneykart, they must be registered with the Reserve

Bank. The license requires that the companies should:

Have an appointed actuary.

Comply with the set policies.

Maintaining solvency and disclosing solvency and credit rating information through

regularly published statements (Tim & Chapman, 2016).

2.0.2 Loan Review System

The Federal Deposit Insurance Corporation (FIDIC) RMS Manual of Examination Policies

and, for accounting and finance defines a loan review system (also known as the credit risk

review system) as a system that involves credit underwriting, loan administration, loan

workout and assembling all the information necessary to establish the appropriateness of

Page 9

INTERNSHIP REPORT

these aspects. The complexity and rigorous nature of the system depend on the size of the

company and the nature of cases dealt with (FIDIC, 1999).

Objectives of a loan review system (FIDIC, 1999)

To identify credit weakness in time and minimize resulting credit loss as much as

possible.

To establish all the necessary information to guide the next course of action.

To evaluate all the responsibilities of the lending personnel.

To avail relevant information to the management to facilitate the assessment of the

client's portfolio.

To establish the relevant trends which may affect the client’s loan portfolio.

I was assigned to keep the customers, portfolio and compile all their lending history and

information. I also kept their current cash flows and business engagements. This information

is kept in a database and it is the one used for analysis before lending.

With the company's experience, I realized that one of the major problems is a credit risk.

What this means is that a loan review system is a very key process before the issuance loans.

Wrong calculations and interpretations may lead to wrong decisions which may result in the

issuance of loans to a customer who is not able to pay the loan. As at the time of entry in the

company, the firm had kept a list of loan defaulters but the trend seemed to reduce

significantly due to efficient credit approval and appraisal system. I, therefore, was tasked to

assist in evaluating the customers' ability to repay the loans with the accumulated interests. In

Moneykart, the credit review system is a rigorous process that takes at least 6 hours to be

approved by the principal advisor, Mr. Rajesh.

The following procedure was adopted by the company.

INTERNSHIP REPORT

these aspects. The complexity and rigorous nature of the system depend on the size of the

company and the nature of cases dealt with (FIDIC, 1999).

Objectives of a loan review system (FIDIC, 1999)

To identify credit weakness in time and minimize resulting credit loss as much as

possible.

To establish all the necessary information to guide the next course of action.

To evaluate all the responsibilities of the lending personnel.

To avail relevant information to the management to facilitate the assessment of the

client's portfolio.

To establish the relevant trends which may affect the client’s loan portfolio.

I was assigned to keep the customers, portfolio and compile all their lending history and

information. I also kept their current cash flows and business engagements. This information

is kept in a database and it is the one used for analysis before lending.

With the company's experience, I realized that one of the major problems is a credit risk.

What this means is that a loan review system is a very key process before the issuance loans.

Wrong calculations and interpretations may lead to wrong decisions which may result in the

issuance of loans to a customer who is not able to pay the loan. As at the time of entry in the

company, the firm had kept a list of loan defaulters but the trend seemed to reduce

significantly due to efficient credit approval and appraisal system. I, therefore, was tasked to

assist in evaluating the customers' ability to repay the loans with the accumulated interests. In

Moneykart, the credit review system is a rigorous process that takes at least 6 hours to be

approved by the principal advisor, Mr. Rajesh.

The following procedure was adopted by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 10

INTERNSHIP REPORT

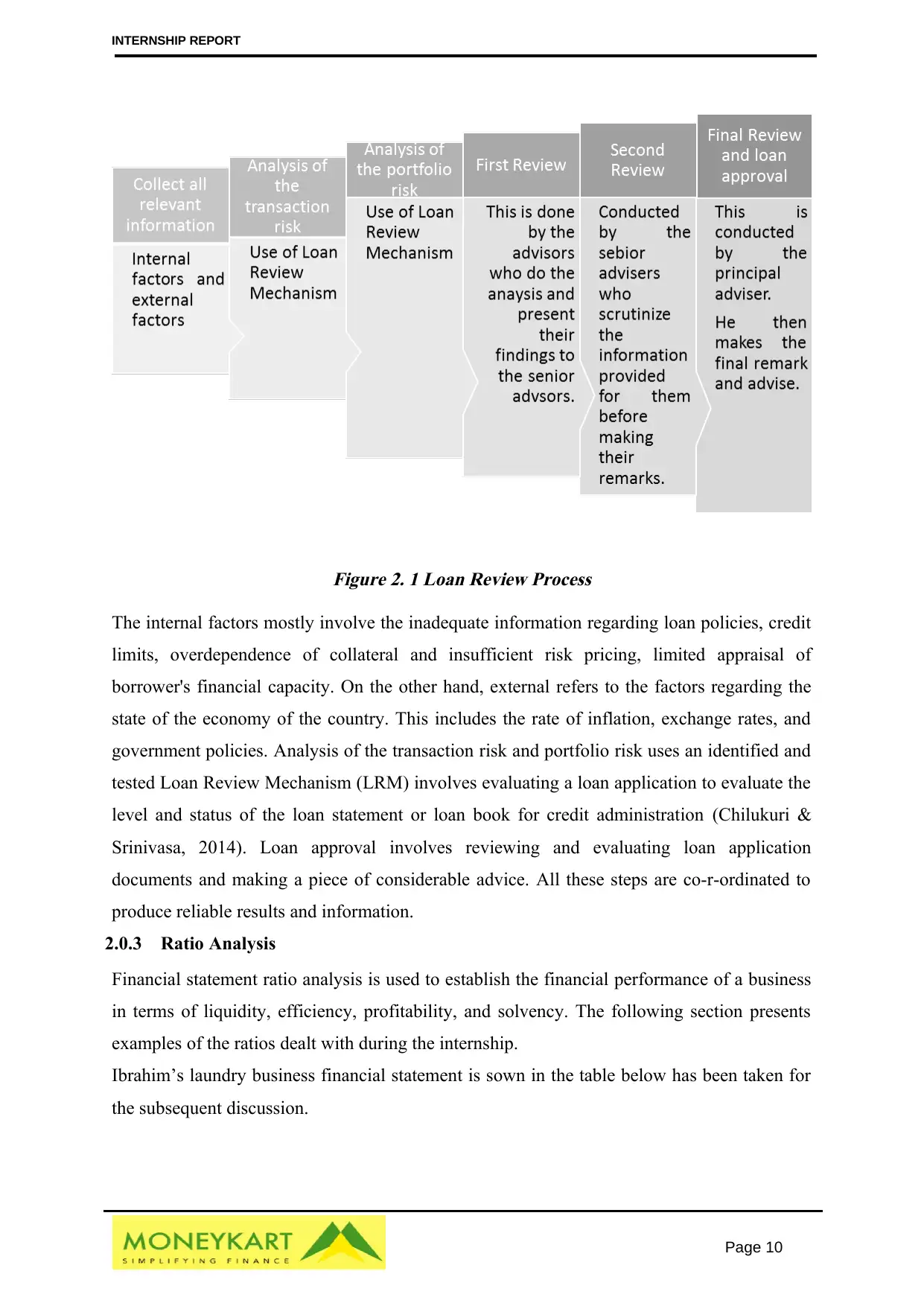

Figure 2. 1 Loan Review Process

The internal factors mostly involve the inadequate information regarding loan policies, credit

limits, overdependence of collateral and insufficient risk pricing, limited appraisal of

borrower's financial capacity. On the other hand, external refers to the factors regarding the

state of the economy of the country. This includes the rate of inflation, exchange rates, and

government policies. Analysis of the transaction risk and portfolio risk uses an identified and

tested Loan Review Mechanism (LRM) involves evaluating a loan application to evaluate the

level and status of the loan statement or loan book for credit administration (Chilukuri &

Srinivasa, 2014). Loan approval involves reviewing and evaluating loan application

documents and making a piece of considerable advice. All these steps are co-r-ordinated to

produce reliable results and information.

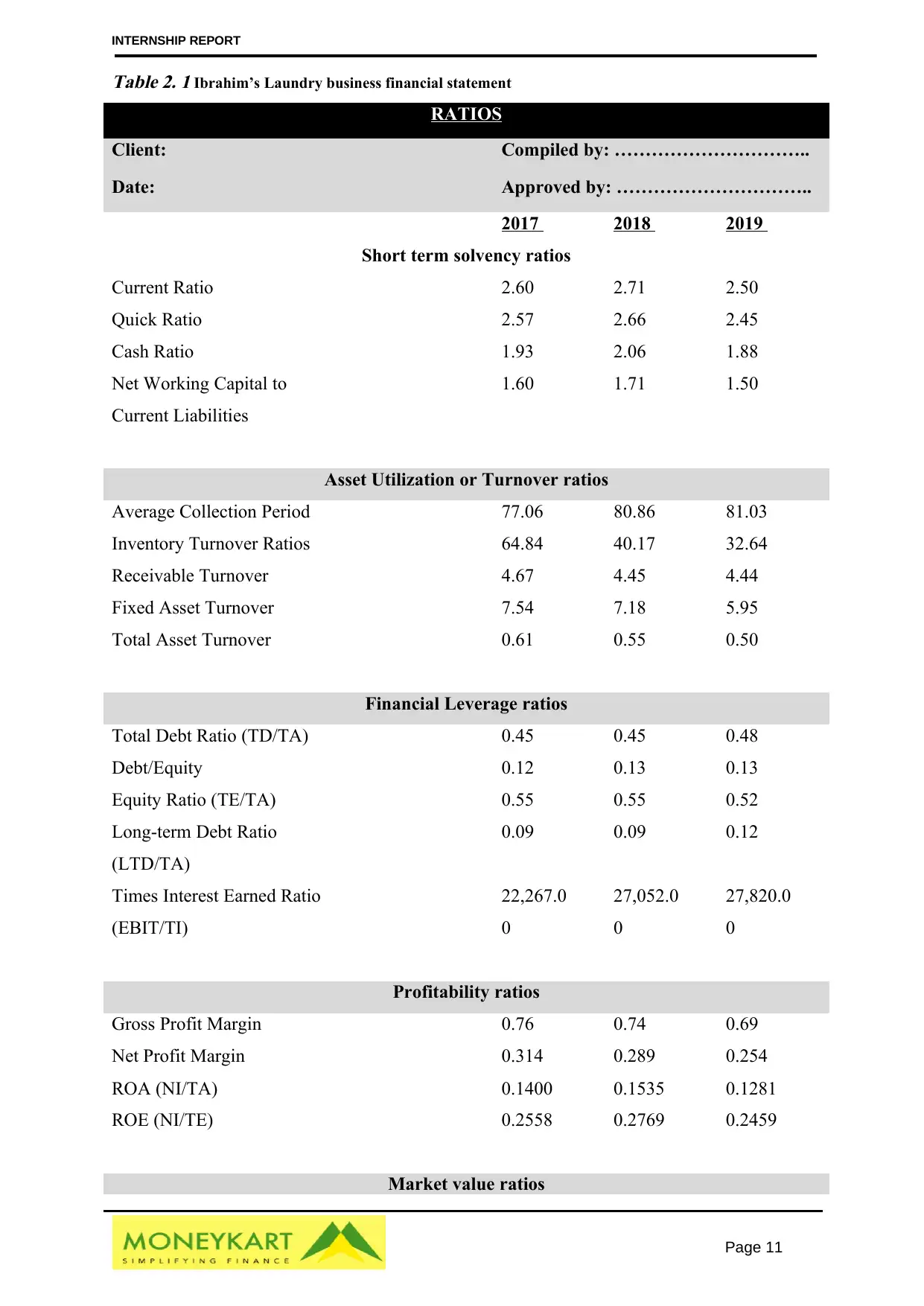

2.0.3 Ratio Analysis

Financial statement ratio analysis is used to establish the financial performance of a business

in terms of liquidity, efficiency, profitability, and solvency. The following section presents

examples of the ratios dealt with during the internship.

Ibrahim’s laundry business financial statement is sown in the table below has been taken for

the subsequent discussion.

INTERNSHIP REPORT

Figure 2. 1 Loan Review Process

The internal factors mostly involve the inadequate information regarding loan policies, credit

limits, overdependence of collateral and insufficient risk pricing, limited appraisal of

borrower's financial capacity. On the other hand, external refers to the factors regarding the

state of the economy of the country. This includes the rate of inflation, exchange rates, and

government policies. Analysis of the transaction risk and portfolio risk uses an identified and

tested Loan Review Mechanism (LRM) involves evaluating a loan application to evaluate the

level and status of the loan statement or loan book for credit administration (Chilukuri &

Srinivasa, 2014). Loan approval involves reviewing and evaluating loan application

documents and making a piece of considerable advice. All these steps are co-r-ordinated to

produce reliable results and information.

2.0.3 Ratio Analysis

Financial statement ratio analysis is used to establish the financial performance of a business

in terms of liquidity, efficiency, profitability, and solvency. The following section presents

examples of the ratios dealt with during the internship.

Ibrahim’s laundry business financial statement is sown in the table below has been taken for

the subsequent discussion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 11

INTERNSHIP REPORT

Table 2. 1 Ibrahim’s Laundry business financial statement

RATIOS

Client: Compiled by: …………………………..

Date: Approved by: …………………………..

2017 2018 2019

Short term solvency ratios

Current Ratio 2.60 2.71 2.50

Quick Ratio 2.57 2.66 2.45

Cash Ratio 1.93 2.06 1.88

Net Working Capital to

Current Liabilities

1.60 1.71 1.50

Asset Utilization or Turnover ratios

Average Collection Period 77.06 80.86 81.03

Inventory Turnover Ratios 64.84 40.17 32.64

Receivable Turnover 4.67 4.45 4.44

Fixed Asset Turnover 7.54 7.18 5.95

Total Asset Turnover 0.61 0.55 0.50

Financial Leverage ratios

Total Debt Ratio (TD/TA) 0.45 0.45 0.48

Debt/Equity 0.12 0.13 0.13

Equity Ratio (TE/TA) 0.55 0.55 0.52

Long-term Debt Ratio

(LTD/TA)

0.09 0.09 0.12

Times Interest Earned Ratio

(EBIT/TI)

22,267.0

0

27,052.0

0

27,820.0

0

Profitability ratios

Gross Profit Margin 0.76 0.74 0.69

Net Profit Margin 0.314 0.289 0.254

ROA (NI/TA) 0.1400 0.1535 0.1281

ROE (NI/TE) 0.2558 0.2769 0.2459

Market value ratios

INTERNSHIP REPORT

Table 2. 1 Ibrahim’s Laundry business financial statement

RATIOS

Client: Compiled by: …………………………..

Date: Approved by: …………………………..

2017 2018 2019

Short term solvency ratios

Current Ratio 2.60 2.71 2.50

Quick Ratio 2.57 2.66 2.45

Cash Ratio 1.93 2.06 1.88

Net Working Capital to

Current Liabilities

1.60 1.71 1.50

Asset Utilization or Turnover ratios

Average Collection Period 77.06 80.86 81.03

Inventory Turnover Ratios 64.84 40.17 32.64

Receivable Turnover 4.67 4.45 4.44

Fixed Asset Turnover 7.54 7.18 5.95

Total Asset Turnover 0.61 0.55 0.50

Financial Leverage ratios

Total Debt Ratio (TD/TA) 0.45 0.45 0.48

Debt/Equity 0.12 0.13 0.13

Equity Ratio (TE/TA) 0.55 0.55 0.52

Long-term Debt Ratio

(LTD/TA)

0.09 0.09 0.12

Times Interest Earned Ratio

(EBIT/TI)

22,267.0

0

27,052.0

0

27,820.0

0

Profitability ratios

Gross Profit Margin 0.76 0.74 0.69

Net Profit Margin 0.314 0.289 0.254

ROA (NI/TA) 0.1400 0.1535 0.1281

ROE (NI/TE) 0.2558 0.2769 0.2459

Market value ratios

Page 12

INTERNSHIP REPORT

Price/Earnings Ratio 10.4000 11.20 14.00

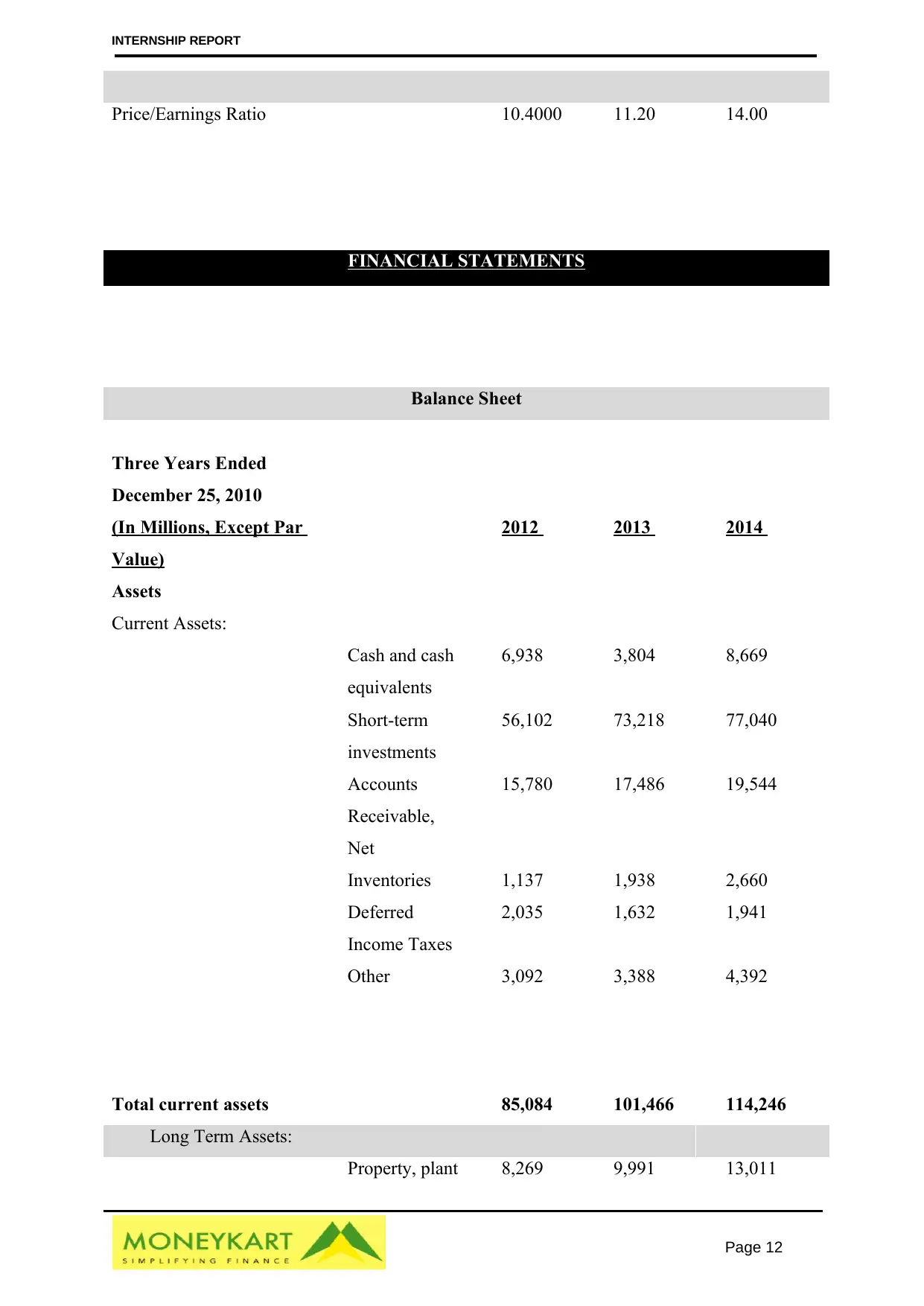

FINANCIAL STATEMENTS

Balance Sheet

Three Years Ended

December 25, 2010

(In Millions, Except Par

Value)

2012 2013 2014

Assets

Current Assets:

Cash and cash

equivalents

6,938 3,804 8,669

Short-term

investments

56,102 73,218 77,040

Accounts

Receivable,

Net

15,780 17,486 19,544

Inventories 1,137 1,938 2,660

Deferred

Income Taxes

2,035 1,632 1,941

Other 3,092 3,388 4,392

Total current assets 85,084 101,466 114,246

Long Term Assets:

Property, plant 8,269 9,991 13,011

INTERNSHIP REPORT

Price/Earnings Ratio 10.4000 11.20 14.00

FINANCIAL STATEMENTS

Balance Sheet

Three Years Ended

December 25, 2010

(In Millions, Except Par

Value)

2012 2013 2014

Assets

Current Assets:

Cash and cash

equivalents

6,938 3,804 8,669

Short-term

investments

56,102 73,218 77,040

Accounts

Receivable,

Net

15,780 17,486 19,544

Inventories 1,137 1,938 2,660

Deferred

Income Taxes

2,035 1,632 1,941

Other 3,092 3,388 4,392

Total current assets 85,084 101,466 114,246

Long Term Assets:

Property, plant 8,269 9,991 13,011

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.