Financial Advisory Report: Retirement Plan for Sam and Kim Smith

VerifiedAdded on 2022/12/28

|21

|4869

|64

Report

AI Summary

This report provides a comprehensive financial advisory analysis for clients Sam and Kim Smith, focusing on their retirement plan and investment strategies. It begins with an introduction to advisory services and the importance of a compliant Statement of Advice (SOA). The report explores various investment options, including national senior term deposits and bank fixed deposits, analyzing their benefits and risks. It assesses the clients' financial goals, objectives, and risk profile, including liquidity and default risks associated with fixed deposits. The report also covers insurance needs analysis, reviewing existing insurance coverage and recommending strategies to secure their investment property. Furthermore, it highlights the advantages of using the property as rental income or as a fixed deposit, including tax benefits and guaranteed returns. The report concludes with a detailed analysis of the clients' financial situation and provides recommendations to help them achieve their retirement goals.

Financial Advisory Practice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

COMPLIANCE:........................................................................................................................................3

RECOMMENDATIONS........................................................................................................................18

REFERENCES........................................................................................................................................20

INTRODUCTION.....................................................................................................................................3

COMPLIANCE:........................................................................................................................................3

RECOMMENDATIONS........................................................................................................................18

REFERENCES........................................................................................................................................20

INTRODUCTION

Advisory service is the offering, typically for a fee, of competent, personalized investment

advice. Advisory management may be conducted by individuals, separate groups, or a team of

practitioners within a private fund, corporate finance company, or expert advisory company

(Dolata, Agotai, Schubiger and Schwabe, 2019). The report is based on scenario that is related to

offering suggestion to client regarded to their retirement plan. For better understanding or better

service to client, compliant Statement of Advice (SOA) is also offered. This can be known as a

form of document that lays out the recommendations that their certified financial advisor or

consultant provides to a customer. It may provide the grounds on which the guidance is offered,

the particulars of the delivering agency and any fees or benefits earned by the advisor or

licensee.

COMPLIANCE:

Advice to client: Though, above client has plan to use such property as rent but apart from this

they can use it different kinds of plans such as national senior term deposit and bank fixed

deposit. In both scheme above client will be able to generate higher amount of financial return.

Before going to this concept, this will be useful to know about both schemes:

National senior term deposit- In such scheme, investors can secure their future for long time

period. This is so because under this a fixed amount is deposited during the age of retirement and

after the retirement clients can gain higher amount of return on each month (Santacruz, 2018).

Term Deposits of National Seniors are a safe deposit account underneath the Monetary Claims

System of the Australia. Under such an arrangement, for each issuing bank at any registered

deposit-taking institution (ADI) established in Australia and authorized by the Bank of Australia

(RBA, such investments are covered up to a maximum of $250,000. (APRA). In the case of the

Monetary Claims System, APRA will seek to pay the bulk of clients within seven days from the

date for their covered deposits underneath the Scheme. Any transfer of part or more of the funds

until exhaustion will be subjected to a notification of 31 days. Conversely, they can contact them

2 business minutes before the release of the period if they wish to change the saving account.

Advisory service is the offering, typically for a fee, of competent, personalized investment

advice. Advisory management may be conducted by individuals, separate groups, or a team of

practitioners within a private fund, corporate finance company, or expert advisory company

(Dolata, Agotai, Schubiger and Schwabe, 2019). The report is based on scenario that is related to

offering suggestion to client regarded to their retirement plan. For better understanding or better

service to client, compliant Statement of Advice (SOA) is also offered. This can be known as a

form of document that lays out the recommendations that their certified financial advisor or

consultant provides to a customer. It may provide the grounds on which the guidance is offered,

the particulars of the delivering agency and any fees or benefits earned by the advisor or

licensee.

COMPLIANCE:

Advice to client: Though, above client has plan to use such property as rent but apart from this

they can use it different kinds of plans such as national senior term deposit and bank fixed

deposit. In both scheme above client will be able to generate higher amount of financial return.

Before going to this concept, this will be useful to know about both schemes:

National senior term deposit- In such scheme, investors can secure their future for long time

period. This is so because under this a fixed amount is deposited during the age of retirement and

after the retirement clients can gain higher amount of return on each month (Santacruz, 2018).

Term Deposits of National Seniors are a safe deposit account underneath the Monetary Claims

System of the Australia. Under such an arrangement, for each issuing bank at any registered

deposit-taking institution (ADI) established in Australia and authorized by the Bank of Australia

(RBA, such investments are covered up to a maximum of $250,000. (APRA). In the case of the

Monetary Claims System, APRA will seek to pay the bulk of clients within seven days from the

date for their covered deposits underneath the Scheme. Any transfer of part or more of the funds

until exhaustion will be subjected to a notification of 31 days. Conversely, they can contact them

2 business minutes before the release of the period if they wish to change the saving account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank fixed deposit- Term deposits, generally referred to as fixed deposits, are a savings method

where a lump-sum balance is invested for a specified period, varying from 1 month to 5 years, at

a negotiated inflation rate (Gurne and Grossi, 2019). Major banks, Non-Banking Finance Firms

(NBFC), community banks, bank branches and investment funds may benefit from savings

accounts. Though, in the case of above clients they are planning to use their property for long

time period and this will be beneficial for them to gain higher amount of return in upcoming time

period.

Scope of advice- The scope of advice to support Sam and Kim SMITH for future so that they can

gain higher amount of return from their investment property. As the amount of investment

property is of $700,000 which has mortgage loan is of $200,000. The property has been acquired

in year 2010 and they want to use this property for future whether as rental purpose or by any

other option. The scope of advice to help couple in upcoming time period as they are going to

retire in 5 years so that they can gain higher amount of return from their property or investment.

Goal and objectives-

Clear goals: In accordance of above case study, both clients need an advice so that they can

survive in upcoming time period after retirement. Below some clear goals are mentioned in such

manner which are as follows:

One of the key goal of advice is to offer a guideline to both couples so that they can

generate higher return from their investment (Tharp, 2019).

Making their investment property more secure and effective which can sustain for long

time period.

They can generate higher amount of return from both options including bank fixed

deposit, and National senior term deposit.

Measurable goals: The measurable goal is the amount which will be received as a rental income

on their investment property if they will give such property for rent.

Time specific goals: The time specific goal is period of year on which their property will be

given on rent by above mentioned client. In this time period they might be able to recover total

cost of investment which is of $700,000 including amount of interest.

where a lump-sum balance is invested for a specified period, varying from 1 month to 5 years, at

a negotiated inflation rate (Gurne and Grossi, 2019). Major banks, Non-Banking Finance Firms

(NBFC), community banks, bank branches and investment funds may benefit from savings

accounts. Though, in the case of above clients they are planning to use their property for long

time period and this will be beneficial for them to gain higher amount of return in upcoming time

period.

Scope of advice- The scope of advice to support Sam and Kim SMITH for future so that they can

gain higher amount of return from their investment property. As the amount of investment

property is of $700,000 which has mortgage loan is of $200,000. The property has been acquired

in year 2010 and they want to use this property for future whether as rental purpose or by any

other option. The scope of advice to help couple in upcoming time period as they are going to

retire in 5 years so that they can gain higher amount of return from their property or investment.

Goal and objectives-

Clear goals: In accordance of above case study, both clients need an advice so that they can

survive in upcoming time period after retirement. Below some clear goals are mentioned in such

manner which are as follows:

One of the key goal of advice is to offer a guideline to both couples so that they can

generate higher return from their investment (Tharp, 2019).

Making their investment property more secure and effective which can sustain for long

time period.

They can generate higher amount of return from both options including bank fixed

deposit, and National senior term deposit.

Measurable goals: The measurable goal is the amount which will be received as a rental income

on their investment property if they will give such property for rent.

Time specific goals: The time specific goal is period of year on which their property will be

given on rent by above mentioned client. In this time period they might be able to recover total

cost of investment which is of $700,000 including amount of interest.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk Profile assessment: A risk profile is an estimation of the readiness and capacity to take

hazards of a person (Vulpoiu, 2018). The risks to which an entity is vulnerable may also be

alluded to. For determining an appropriate investment strategy for an investment, a risk profile is

essential. A risk profile is used by organizations as a means to minimize future hazards and

challenges. The appropriate level of risk a person is willing and ready to tolerate is defined by a

risk profile. The risk profile of an organization seeks to assess how an internal judgment process

can be influenced by a desire to take on threat (or an indifference to risk). In the context of above

case of Sam and Kim SMITH, this is essential for them to analyze overall risk which may be

faced by them in upcoming time period from the investment which they made of $700,000 and

there might be risk of not getting right lender for their property for rental purpose. As well as to

this, another risk is related to more time consumption in order to recover total investment value

of project which is of $700000. Basically if project consumes too much amount of time than this

may lead to higher risk for both people. Below some risks can occurred in such manner in the

context of above mentioned both plans:

Risks in fixed deposits-

Liquidity risk-It is possible to quickly liquidate bank current accounts (FDs). A tax may be

levied, nevertheless. Until expiration of the 5-year term, tax saver FDs should not be deleted.

Default risk- Bank defaults are uncommon but conceivable. Even so, the DICGC guarantees the

balance of the deposit, including interest of up to Dollar 5 lakh per individual per account, and

any amount above that is liable to risk premium (Maume, 2019).

No deposits additional. When you activate your term deposit, you will need to create a single

payment deposit, because there's no way to apply to your savings while you go (Cruciani,

Gardenal, and Rigoni, 2018). For daily savers, this may be a challenge, but one way to fight it is

by having additional deposit accounts with phased longer maturities.

Less mobility. Low risk is a term deposit - however the downside is that this is not a very

versatile choice for investments. In terms of versatile features and choices, most plans with

similar costs, such as fixed interest bank deposits, offer a lot more.

hazards of a person (Vulpoiu, 2018). The risks to which an entity is vulnerable may also be

alluded to. For determining an appropriate investment strategy for an investment, a risk profile is

essential. A risk profile is used by organizations as a means to minimize future hazards and

challenges. The appropriate level of risk a person is willing and ready to tolerate is defined by a

risk profile. The risk profile of an organization seeks to assess how an internal judgment process

can be influenced by a desire to take on threat (or an indifference to risk). In the context of above

case of Sam and Kim SMITH, this is essential for them to analyze overall risk which may be

faced by them in upcoming time period from the investment which they made of $700,000 and

there might be risk of not getting right lender for their property for rental purpose. As well as to

this, another risk is related to more time consumption in order to recover total investment value

of project which is of $700000. Basically if project consumes too much amount of time than this

may lead to higher risk for both people. Below some risks can occurred in such manner in the

context of above mentioned both plans:

Risks in fixed deposits-

Liquidity risk-It is possible to quickly liquidate bank current accounts (FDs). A tax may be

levied, nevertheless. Until expiration of the 5-year term, tax saver FDs should not be deleted.

Default risk- Bank defaults are uncommon but conceivable. Even so, the DICGC guarantees the

balance of the deposit, including interest of up to Dollar 5 lakh per individual per account, and

any amount above that is liable to risk premium (Maume, 2019).

No deposits additional. When you activate your term deposit, you will need to create a single

payment deposit, because there's no way to apply to your savings while you go (Cruciani,

Gardenal, and Rigoni, 2018). For daily savers, this may be a challenge, but one way to fight it is

by having additional deposit accounts with phased longer maturities.

Less mobility. Low risk is a term deposit - however the downside is that this is not a very

versatile choice for investments. In terms of versatile features and choices, most plans with

similar costs, such as fixed interest bank deposits, offer a lot more.

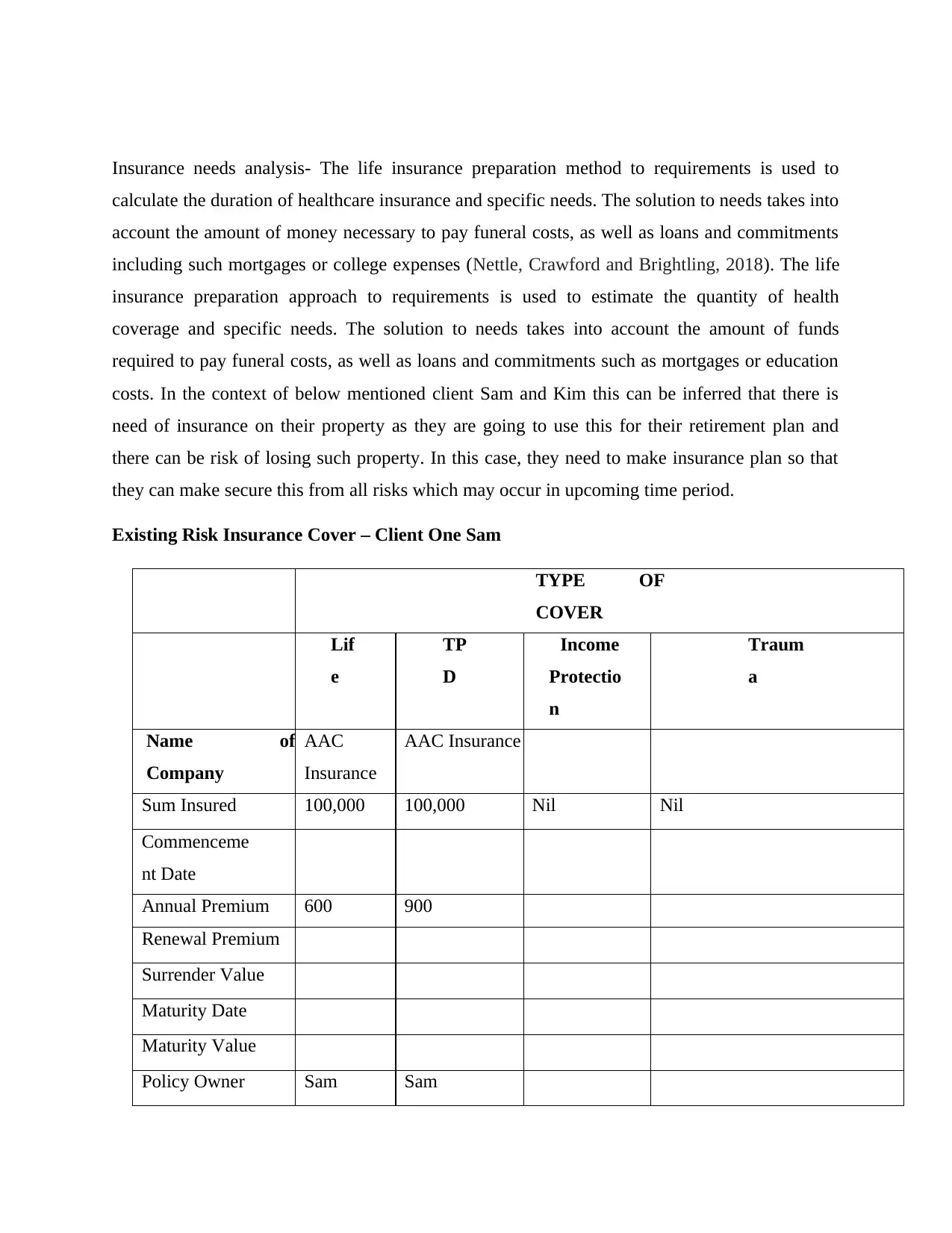

Insurance needs analysis- The life insurance preparation method to requirements is used to

calculate the duration of healthcare insurance and specific needs. The solution to needs takes into

account the amount of money necessary to pay funeral costs, as well as loans and commitments

including such mortgages or college expenses (Nettle, Crawford and Brightling, 2018). The life

insurance preparation approach to requirements is used to estimate the quantity of health

coverage and specific needs. The solution to needs takes into account the amount of funds

required to pay funeral costs, as well as loans and commitments such as mortgages or education

costs. In the context of below mentioned client Sam and Kim this can be inferred that there is

need of insurance on their property as they are going to use this for their retirement plan and

there can be risk of losing such property. In this case, they need to make insurance plan so that

they can make secure this from all risks which may occur in upcoming time period.

Existing Risk Insurance Cover – Client One Sam

TYPE OF

COVER

Lif

e

TP

D

Income

Protectio

n

Traum

a

Name of

Company

AAC

Insurance

AAC Insurance

Sum Insured 100,000 100,000 Nil Nil

Commenceme

nt Date

Annual Premium 600 900

Renewal Premium

Surrender Value

Maturity Date

Maturity Value

Policy Owner Sam Sam

calculate the duration of healthcare insurance and specific needs. The solution to needs takes into

account the amount of money necessary to pay funeral costs, as well as loans and commitments

including such mortgages or college expenses (Nettle, Crawford and Brightling, 2018). The life

insurance preparation approach to requirements is used to estimate the quantity of health

coverage and specific needs. The solution to needs takes into account the amount of funds

required to pay funeral costs, as well as loans and commitments such as mortgages or education

costs. In the context of below mentioned client Sam and Kim this can be inferred that there is

need of insurance on their property as they are going to use this for their retirement plan and

there can be risk of losing such property. In this case, they need to make insurance plan so that

they can make secure this from all risks which may occur in upcoming time period.

Existing Risk Insurance Cover – Client One Sam

TYPE OF

COVER

Lif

e

TP

D

Income

Protectio

n

Traum

a

Name of

Company

AAC

Insurance

AAC Insurance

Sum Insured 100,000 100,000 Nil Nil

Commenceme

nt Date

Annual Premium 600 900

Renewal Premium

Surrender Value

Maturity Date

Maturity Value

Policy Owner Sam Sam

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Life Insured

Substandar

d Loadings

Last Review Date

Adviser Name

As in the aspect of above client Sam, this can be inferred that they have an insurance policy

which has annual premium of 600 of life and 900 of TPD. In such case, it can be inferred that

their life has been secured from all kinds of risk and this may be helpful for them in upcoming

time period.

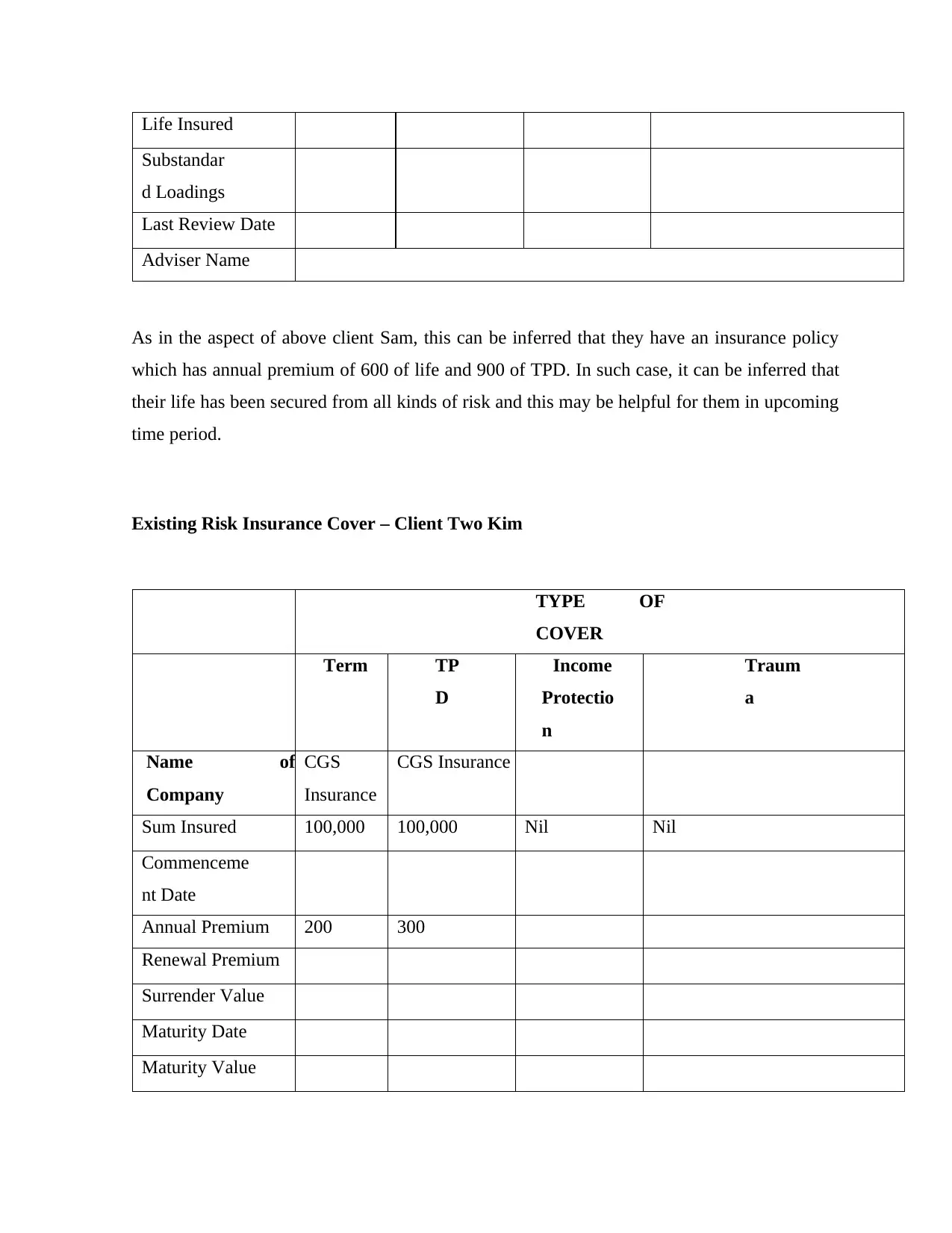

Existing Risk Insurance Cover – Client Two Kim

TYPE OF

COVER

Term TP

D

Income

Protectio

n

Traum

a

Name of

Company

CGS

Insurance

CGS Insurance

Sum Insured 100,000 100,000 Nil Nil

Commenceme

nt Date

Annual Premium 200 300

Renewal Premium

Surrender Value

Maturity Date

Maturity Value

Substandar

d Loadings

Last Review Date

Adviser Name

As in the aspect of above client Sam, this can be inferred that they have an insurance policy

which has annual premium of 600 of life and 900 of TPD. In such case, it can be inferred that

their life has been secured from all kinds of risk and this may be helpful for them in upcoming

time period.

Existing Risk Insurance Cover – Client Two Kim

TYPE OF

COVER

Term TP

D

Income

Protectio

n

Traum

a

Name of

Company

CGS

Insurance

CGS Insurance

Sum Insured 100,000 100,000 Nil Nil

Commenceme

nt Date

Annual Premium 200 300

Renewal Premium

Surrender Value

Maturity Date

Maturity Value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Policy Owner Kim Kim

Life Insured

Loadings

Last Review Date

Adviser Name

As in the aspect of above client Kim, this can be inferred that they have an insurance policy

which has annual premium of 200 of life and 300 of TPD. In such case, it can be inferred that

their life has been secured from all kinds of risk and this may be helpful for them in upcoming

time period.

Benefits of advice:

Advantages of using property of $700000 as rental: -

By far, rental revenue is one of the main advantages of buying investment estate. If the rental

expenditure raises the holding costs of the house (such as property taxes, depreciation,

renovations, and maintenance) as well as the cost of borrowing, the owner collects a payment per

quarter for as much as the land is leased and the occupant pays on time, providing a stable stream

of income. As the above clients can get higher amount of income in each year which may reduce

burden of expenses (Dolata, Kilic and Schwabe, 2019).

Although not necessarily the case, real estate understands, or rises in value, over time in most

cases. Based on where the new property is purchased, in relation to the extra revenue it creates

from being leased, there is a risk that the owner will benefit from the possible value of the

property (Seshanna and Seshanna, 2018). If the capital gains increase the costs and borrowing

cost of the house, the interest is charged from the resident's rental charge, reducing the principal

balance every month it is leased. Which ensures that the landlord creates equity in the property

without paying a mortgage or interest on his own.

The tax advantages are another major bonus of buying a rental home. A number of tax

deductions are possible for financial securities, including:

Life Insured

Loadings

Last Review Date

Adviser Name

As in the aspect of above client Kim, this can be inferred that they have an insurance policy

which has annual premium of 200 of life and 300 of TPD. In such case, it can be inferred that

their life has been secured from all kinds of risk and this may be helpful for them in upcoming

time period.

Benefits of advice:

Advantages of using property of $700000 as rental: -

By far, rental revenue is one of the main advantages of buying investment estate. If the rental

expenditure raises the holding costs of the house (such as property taxes, depreciation,

renovations, and maintenance) as well as the cost of borrowing, the owner collects a payment per

quarter for as much as the land is leased and the occupant pays on time, providing a stable stream

of income. As the above clients can get higher amount of income in each year which may reduce

burden of expenses (Dolata, Kilic and Schwabe, 2019).

Although not necessarily the case, real estate understands, or rises in value, over time in most

cases. Based on where the new property is purchased, in relation to the extra revenue it creates

from being leased, there is a risk that the owner will benefit from the possible value of the

property (Seshanna and Seshanna, 2018). If the capital gains increase the costs and borrowing

cost of the house, the interest is charged from the resident's rental charge, reducing the principal

balance every month it is leased. Which ensures that the landlord creates equity in the property

without paying a mortgage or interest on his own.

The tax advantages are another major bonus of buying a rental home. A number of tax

deductions are possible for financial securities, including:

Deductions for Industry (if the property is owned by a company or LLC).

Land charges, including property premiums, property taxes, and any expenditures or

renovations for maintenance.

Benefits of using property as Fixed deposit-

The guaranteed return on investment is the main reason why individuals favor saving their assets

in a fixed deposit. They will be confident of obtaining the claimed rate of return if the invest the

funds in a fixed deposit (Dimmock, Gerken and Graham, 2018). Stocks post the fixed interest

borrowing costs on their website and in bank stores, making it easier for a borrower to decide

how often returns he will get. Banks also offer a fixed lending rate calculation on their website

that for a certain amount of time a customer will measure the return he can gain on spending a

certain amount of money. Such as in the aspect of above clients this will be beneficial for them

to gain higher return in upcoming time period.

For just a fixed deposit, the term is variable and relies on the owners of the deposit. Through

banking has its own mandatory tenure guidelines, but the investment holder may take the

ultimate decision. It is therefore possible to determine if the fixed deposit can be redeemed or

renewed for the same duration.

Benefits of using property as National senior term deposit: -This is also an important and key

approach which can be used by above clients because under it there can be more opportunity to

gain higher return in upcoming time period (Jung, Erdfelder and Glaser, 2018). As well as they

can generate more revenue in upcoming time period.

Risks associated with advice: -

Fixed deposit- One of the best savings around is manage risks. Unlike other portfolios, such as

bonds or cash, there is practically no chance that the money the deposit will be wasted. There are

no costs added to term deposits for creation or continuing operation (unless they remove the

assets soon), meaning they don't have to think about hidden penalties and expenses chewing

away at the investment account (Mutiga, Mushongi and Kangéthe, 2019). This accounts help

Land charges, including property premiums, property taxes, and any expenditures or

renovations for maintenance.

Benefits of using property as Fixed deposit-

The guaranteed return on investment is the main reason why individuals favor saving their assets

in a fixed deposit. They will be confident of obtaining the claimed rate of return if the invest the

funds in a fixed deposit (Dimmock, Gerken and Graham, 2018). Stocks post the fixed interest

borrowing costs on their website and in bank stores, making it easier for a borrower to decide

how often returns he will get. Banks also offer a fixed lending rate calculation on their website

that for a certain amount of time a customer will measure the return he can gain on spending a

certain amount of money. Such as in the aspect of above clients this will be beneficial for them

to gain higher return in upcoming time period.

For just a fixed deposit, the term is variable and relies on the owners of the deposit. Through

banking has its own mandatory tenure guidelines, but the investment holder may take the

ultimate decision. It is therefore possible to determine if the fixed deposit can be redeemed or

renewed for the same duration.

Benefits of using property as National senior term deposit: -This is also an important and key

approach which can be used by above clients because under it there can be more opportunity to

gain higher return in upcoming time period (Jung, Erdfelder and Glaser, 2018). As well as they

can generate more revenue in upcoming time period.

Risks associated with advice: -

Fixed deposit- One of the best savings around is manage risks. Unlike other portfolios, such as

bonds or cash, there is practically no chance that the money the deposit will be wasted. There are

no costs added to term deposits for creation or continuing operation (unless they remove the

assets soon), meaning they don't have to think about hidden penalties and expenses chewing

away at the investment account (Mutiga, Mushongi and Kangéthe, 2019). This accounts help

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they to receive a reasonable interest rate on your account balance, and they don't have to think

about dropping interest rates undermining your saving power because the interest rate is set. It

also ensures that you can determine precisely how much return on the deposit account they can

receive, helping it to prepare long in advance for future spending and savings.

In short, savings accounts provide a perfect way to safely place the cash anywhere and let it

expand. There is no necessary ongoing account maintenance and practically no risk involved

with the portfolio. In the aspect of above case, client has to bear risk of depositing amount in

fixed deposit.

Using investment as rental property: -

The sources of resources allow a fixed deposit convenient. Not all investment costs can,

nevertheless, be readily divested. An income FD, for instance, whose period is 5 years, cannot be

forced to liquidate before its duration. It will have to visit the bank to fill out the papers if they

already have an FD at a company that does not accept online bankruptcy, so it might be a couple

of days until they get the cash. In the context of above clients, this can become cause of riskier

task for them as there can be fluctuation in economy or any factor may lead to less amount of

return in upcoming time period.

Using investment as national senior term deposit: - Under this approach there is no any risk but

future is uncertain and there can be possibility of lower amount of return (Norman and

Bagranoff, 2019). It is so because in upcoming time period government of Australia might

change their policies and regulations related to future pension schemes and this may become

cause of lesser return on amount which have been invested in any form of plan for old age.

Similarly,above clients can also face such risk in future time period.

SOA (Statement of Advice): -

Executive summary: This report summarizes about detailed analysis of statement of advice to

the given clients Sam and Kim. The purpose of the report to give advice about their financial

property which is of $700000.

about dropping interest rates undermining your saving power because the interest rate is set. It

also ensures that you can determine precisely how much return on the deposit account they can

receive, helping it to prepare long in advance for future spending and savings.

In short, savings accounts provide a perfect way to safely place the cash anywhere and let it

expand. There is no necessary ongoing account maintenance and practically no risk involved

with the portfolio. In the aspect of above case, client has to bear risk of depositing amount in

fixed deposit.

Using investment as rental property: -

The sources of resources allow a fixed deposit convenient. Not all investment costs can,

nevertheless, be readily divested. An income FD, for instance, whose period is 5 years, cannot be

forced to liquidate before its duration. It will have to visit the bank to fill out the papers if they

already have an FD at a company that does not accept online bankruptcy, so it might be a couple

of days until they get the cash. In the context of above clients, this can become cause of riskier

task for them as there can be fluctuation in economy or any factor may lead to less amount of

return in upcoming time period.

Using investment as national senior term deposit: - Under this approach there is no any risk but

future is uncertain and there can be possibility of lower amount of return (Norman and

Bagranoff, 2019). It is so because in upcoming time period government of Australia might

change their policies and regulations related to future pension schemes and this may become

cause of lesser return on amount which have been invested in any form of plan for old age.

Similarly,above clients can also face such risk in future time period.

SOA (Statement of Advice): -

Executive summary: This report summarizes about detailed analysis of statement of advice to

the given clients Sam and Kim. The purpose of the report to give advice about their financial

property which is of $700000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

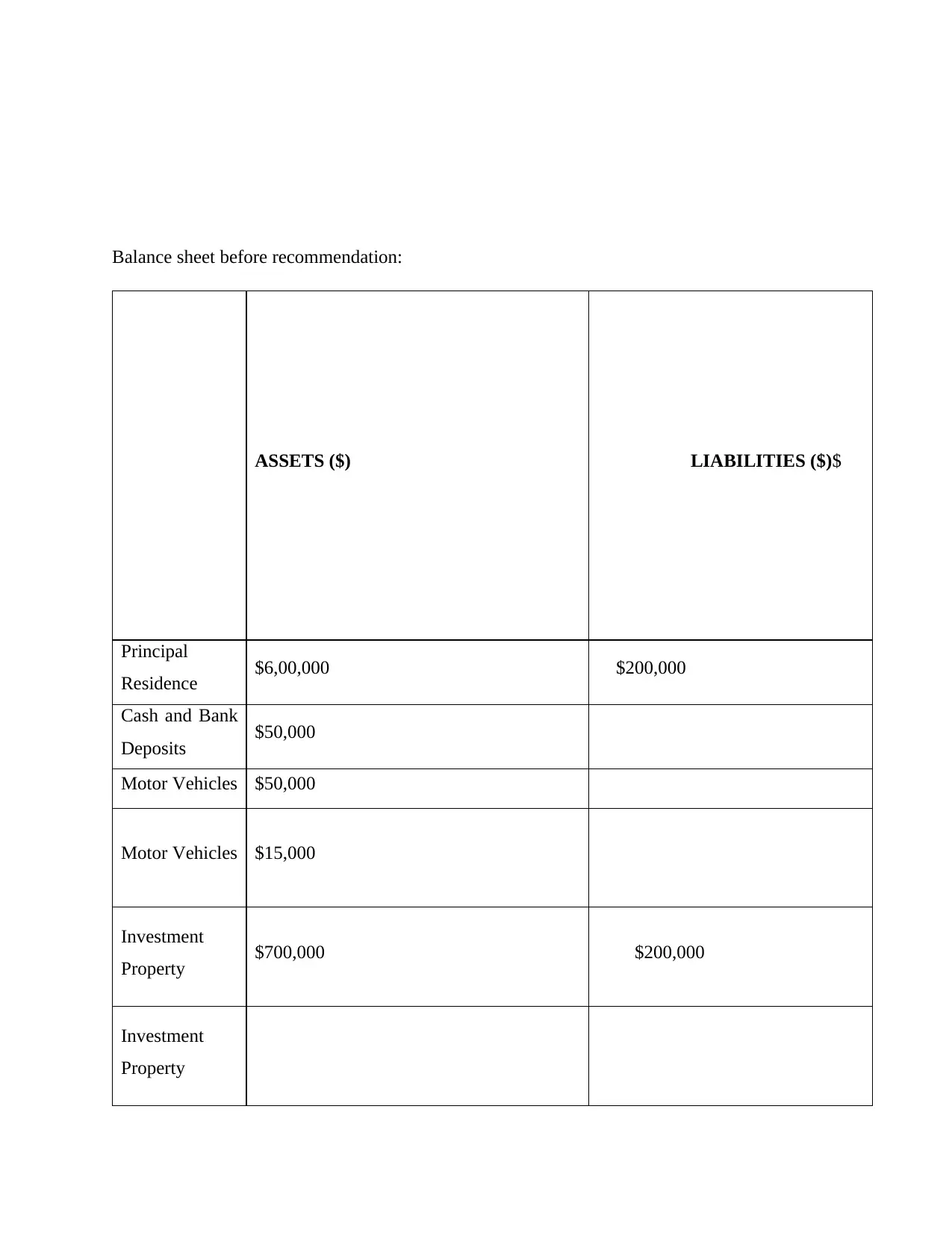

Balance sheet before recommendation:

ASSETS ($) LIABILITIES ($)$

Principal

Residence $6,00,000 $200,000

Cash and Bank

Deposits $50,000

Motor Vehicles $50,000

Motor Vehicles $15,000

Investment

Property $700,000 $200,000

Investment

Property

ASSETS ($) LIABILITIES ($)$

Principal

Residence $6,00,000 $200,000

Cash and Bank

Deposits $50,000

Motor Vehicles $50,000

Motor Vehicles $15,000

Investment

Property $700,000 $200,000

Investment

Property

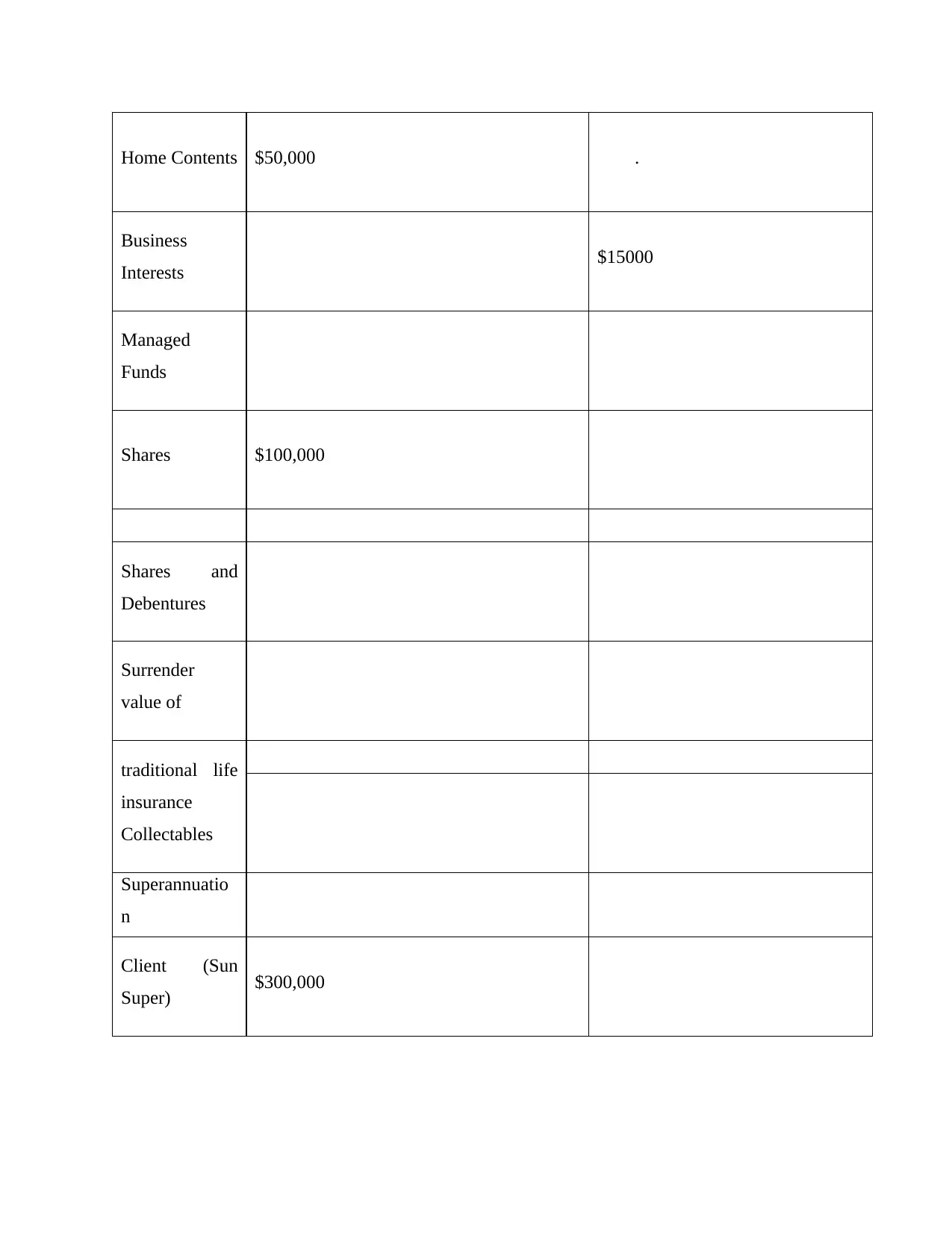

Home Contents $50,000 .

Business

Interests $15000

Managed

Funds

Shares $100,000

Shares and

Debentures

Surrender

value of

traditional life

insurance

Collectables

Superannuatio

n

Client (Sun

Super) $300,000

Business

Interests $15000

Managed

Funds

Shares $100,000

Shares and

Debentures

Surrender

value of

traditional life

insurance

Collectables

Superannuatio

n

Client (Sun

Super) $300,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.