Financial Analysis of Amazon: Performance, Ratios, and Recommendations

VerifiedAdded on 2021/05/27

|17

|4160

|472

Report

AI Summary

This report provides a detailed financial analysis of Amazon, focusing on the company's performance in the late 1990s and early 2000s. It begins with an introduction outlining the challenges Amazon faced in becoming profitable and creating shareholder value, particularly in the wake of the dot-com bubble. The report then analyzes Amazon's income statement, highlighting the growth in sales and the increasing costs, particularly fulfillment costs and interest expenses. A significant portion of the report is dedicated to ratio analysis, including net profit margin, debt-equity ratio, current ratio, quick ratio, inventory turnover, and asset turnover ratios. These ratios are used to assess Amazon's liquidity, solvency, and profitability. The analysis reveals declining net profit margins despite increasing sales, a concerning debt-equity ratio, and improvements in liquidity. The report concludes with an assessment of the company's future profitability and the impact of competition, ethical considerations, and external factors, including potential mergers and acquisitions, and provides recommendations for improvement.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2FINANCIAL MANAGEMENT

Table of Contents

Introduction:...............................................................................................................................2

Analysis of the income statement of the company:...................................................................3

Ratio Analysis:...........................................................................................................................4

Argument regarding the future profitability of the organisation:...............................................7

The impact of the competition on the functioning of the company:..........................................8

Different ethical considerations in case the organisation becomes insolvent:...........................8

The various external factors that are needed to be taken into consideration and the likely hood

of merger and acquisition:..........................................................................................................9

Conclusion and recommendation:............................................................................................10

Reference..................................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................2

Analysis of the income statement of the company:...................................................................3

Ratio Analysis:...........................................................................................................................4

Argument regarding the future profitability of the organisation:...............................................7

The impact of the competition on the functioning of the company:..........................................8

Different ethical considerations in case the organisation becomes insolvent:...........................8

The various external factors that are needed to be taken into consideration and the likely hood

of merger and acquisition:..........................................................................................................9

Conclusion and recommendation:............................................................................................10

Reference..................................................................................................................................12

3FINANCIAL MANAGEMENT

Introduction:

In the present report, an effort will be made in respect of presenting the economic

issues that were being faced by the online retail giant Amazon. It is quite understandable that

the company was facing issues of becoming profitable and create value for its shareholders.

The reason being that the company had arranged for huge amount of funds from the

shareholders and other financial institutions and the third parties. Due to the decrease in the

value of the stocks as a result OF the dot com phenomenon in the year 2000 the company had

lose a huge amount of its value. It is this required to identify the ways in which the company

can increase its value by increasing the profitability of its business (Titman et al., 2017). For

the analysis of the situation, a deeper study will be conducted of the various ratios and the

income statement of, the company along with the balance sheet of the company. Based on the

results of the analysis that is being carried out, several recommendations will be made in

respect of the viability of the future operations of the company and the propriety of the

investment made by the shareholders until date in the company.

Analysis of the income statement of the company:

As per the information that is being available from the income statement of the company,

the following observations can be made:

a) The growth of the sales of the company amounted to $2761983000 and $1639839000

in the year 2000 and 1999 respectively. During the same corresponding period, the

cost of sales OF, the company amounted to $21062016000 and $1349194000. This

means that the common show a growth of around 68% in respect of its sales (Renz &

Herman, 2016). However, deign the same period the cost of sales of the company

grew at a pace of around 49%. It is very understandable that due to the difference in

the growth rates of the sales of the company and the cost of sales it was possible for

Introduction:

In the present report, an effort will be made in respect of presenting the economic

issues that were being faced by the online retail giant Amazon. It is quite understandable that

the company was facing issues of becoming profitable and create value for its shareholders.

The reason being that the company had arranged for huge amount of funds from the

shareholders and other financial institutions and the third parties. Due to the decrease in the

value of the stocks as a result OF the dot com phenomenon in the year 2000 the company had

lose a huge amount of its value. It is this required to identify the ways in which the company

can increase its value by increasing the profitability of its business (Titman et al., 2017). For

the analysis of the situation, a deeper study will be conducted of the various ratios and the

income statement of, the company along with the balance sheet of the company. Based on the

results of the analysis that is being carried out, several recommendations will be made in

respect of the viability of the future operations of the company and the propriety of the

investment made by the shareholders until date in the company.

Analysis of the income statement of the company:

As per the information that is being available from the income statement of the company,

the following observations can be made:

a) The growth of the sales of the company amounted to $2761983000 and $1639839000

in the year 2000 and 1999 respectively. During the same corresponding period, the

cost of sales OF, the company amounted to $21062016000 and $1349194000. This

means that the common show a growth of around 68% in respect of its sales (Renz &

Herman, 2016). However, deign the same period the cost of sales of the company

grew at a pace of around 49%. It is very understandable that due to the difference in

the growth rates of the sales of the company and the cost of sales it was possible for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4FINANCIAL MANAGEMENT

the company to earn profits. However, the rate of increase in the cost of the company

cannot be justified by the overall increase in the gross profit of the company. The

reason being that there are several other costs that will soon catch up with the profits

of the company and diminish its overall return.

b) It can be observed that the expenditure incurred by the company in respect of the

fulfilment costs has increased significantly over the years. The fulfilment costs of the

company amounted to $15944, $65227, $237312 and $414509 respectively for the

year 1997, 1998, 1999 and 2000 respectively (Lau, 2016). It can be clearly seen that

the among incurred by the company in respect of the fulfilment costs increased

around 25 times. The effect of the same can be felt in the loss that the company is

presently earning. The expense has overshadowed the impact of the gross profit

earned by the company. The company needs to control the amount of fulfilment costs

immediately.

c) The interest expense of the company amounted to $326, $26639, $84566 and $130921

for the year 1997, 1998, 1999 and 2000 respectively. From this, it can be effectively

concluded that the interest expense of the company has risen substantially over the

period of four years. The reason being the ever-increasing borrowing amount of the

company (Waxman, 2018).

Ratio Analysis:

1) Net profit margin:

Net Profit Margin

2000 1999 1998 1997

Net Profit -1411273 -719968 -

124546

-31020

Sales 2761983 163983

9

609819 14778

7

Net Profit Margin -0.51 -0.44 -0.20 -0.21

the company to earn profits. However, the rate of increase in the cost of the company

cannot be justified by the overall increase in the gross profit of the company. The

reason being that there are several other costs that will soon catch up with the profits

of the company and diminish its overall return.

b) It can be observed that the expenditure incurred by the company in respect of the

fulfilment costs has increased significantly over the years. The fulfilment costs of the

company amounted to $15944, $65227, $237312 and $414509 respectively for the

year 1997, 1998, 1999 and 2000 respectively (Lau, 2016). It can be clearly seen that

the among incurred by the company in respect of the fulfilment costs increased

around 25 times. The effect of the same can be felt in the loss that the company is

presently earning. The expense has overshadowed the impact of the gross profit

earned by the company. The company needs to control the amount of fulfilment costs

immediately.

c) The interest expense of the company amounted to $326, $26639, $84566 and $130921

for the year 1997, 1998, 1999 and 2000 respectively. From this, it can be effectively

concluded that the interest expense of the company has risen substantially over the

period of four years. The reason being the ever-increasing borrowing amount of the

company (Waxman, 2018).

Ratio Analysis:

1) Net profit margin:

Net Profit Margin

2000 1999 1998 1997

Net Profit -1411273 -719968 -

124546

-31020

Sales 2761983 163983

9

609819 14778

7

Net Profit Margin -0.51 -0.44 -0.20 -0.21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5FINANCIAL MANAGEMENT

It can be seen that the net profit margin of the company has been steadily decaling over

the years. This is happening despite the fact that the sales of the company has been increasing

steadily over the period of last four years. It can be seen that the sales OF the company

amounted to 147787, 609819, 1639839 and 2761983 respectively for the year 1997, 1998,

1999 and 2000. This clearly depicts that the company has been able to steadily increase its

customer’s base over the years (Finkler et al., 2016). The increase in the customer base of the

company has however not been able to generate enough cash flows so as to cover up the

expenses of the company and to generate profit for the company. The reason being that

certain expenses of the company re so high that the company is not being able to cope up

with them. For instance, the fulfilment costs OF the company amounted to 15944, 65227,

237312 and 414509 respectively for the year 1997, 1998, 1999 and 2000. This clearly shows

the trend of the expenses that have been incurred by the company in respect OF the fulfilment

costs. This clearly shows that the expenses of the company in this respect have increased over

25 times over the last four years. Another example OF such exuberant expenditure incurred

by company includes expenditure related to the restructuring of the company (Zietlow et al.,

2018). The restructuring expenses OF the company amounted to $3535, $8072 and $200311

respectively for the year 1998. 1999 and 2000. The expenditure incurred by the company in

respect of restructuring of the company increased about 24 times within a period of just one

year. Hence thought the sales of the company are increasing over the years the company is

not able to increase its net profit at the Sam pace.

It can be seen that the net profit margin of the company has been steadily decaling over

the years. This is happening despite the fact that the sales of the company has been increasing

steadily over the period of last four years. It can be seen that the sales OF the company

amounted to 147787, 609819, 1639839 and 2761983 respectively for the year 1997, 1998,

1999 and 2000. This clearly depicts that the company has been able to steadily increase its

customer’s base over the years (Finkler et al., 2016). The increase in the customer base of the

company has however not been able to generate enough cash flows so as to cover up the

expenses of the company and to generate profit for the company. The reason being that

certain expenses of the company re so high that the company is not being able to cope up

with them. For instance, the fulfilment costs OF the company amounted to 15944, 65227,

237312 and 414509 respectively for the year 1997, 1998, 1999 and 2000. This clearly shows

the trend of the expenses that have been incurred by the company in respect OF the fulfilment

costs. This clearly shows that the expenses of the company in this respect have increased over

25 times over the last four years. Another example OF such exuberant expenditure incurred

by company includes expenditure related to the restructuring of the company (Zietlow et al.,

2018). The restructuring expenses OF the company amounted to $3535, $8072 and $200311

respectively for the year 1998. 1999 and 2000. The expenditure incurred by the company in

respect of restructuring of the company increased about 24 times within a period of just one

year. Hence thought the sales of the company are increasing over the years the company is

not able to increase its net profit at the Sam pace.

6FINANCIAL MANAGEMENT

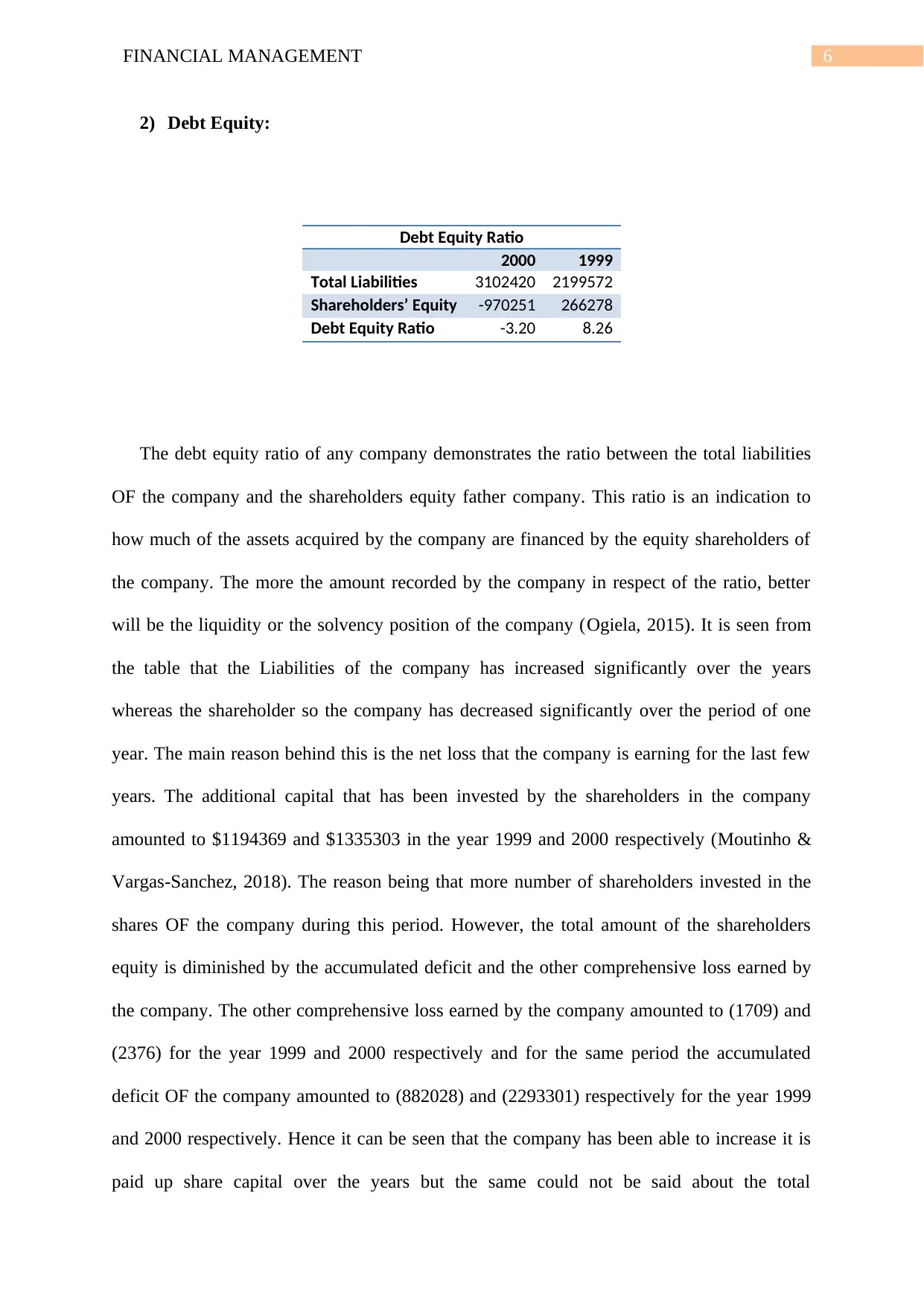

2) Debt Equity:

The debt equity ratio of any company demonstrates the ratio between the total liabilities

OF the company and the shareholders equity father company. This ratio is an indication to

how much of the assets acquired by the company are financed by the equity shareholders of

the company. The more the amount recorded by the company in respect of the ratio, better

will be the liquidity or the solvency position of the company (Ogiela, 2015). It is seen from

the table that the Liabilities of the company has increased significantly over the years

whereas the shareholder so the company has decreased significantly over the period of one

year. The main reason behind this is the net loss that the company is earning for the last few

years. The additional capital that has been invested by the shareholders in the company

amounted to $1194369 and $1335303 in the year 1999 and 2000 respectively (Moutinho &

Vargas-Sanchez, 2018). The reason being that more number of shareholders invested in the

shares OF the company during this period. However, the total amount of the shareholders

equity is diminished by the accumulated deficit and the other comprehensive loss earned by

the company. The other comprehensive loss earned by the company amounted to (1709) and

(2376) for the year 1999 and 2000 respectively and for the same period the accumulated

deficit OF the company amounted to (882028) and (2293301) respectively for the year 1999

and 2000 respectively. Hence it can be seen that the company has been able to increase it is

paid up share capital over the years but the same could not be said about the total

Debt Equity Ratio

2000 1999

Total Liabilities 3102420 2199572

Shareholders’ Equity -970251 266278

Debt Equity Ratio -3.20 8.26

2) Debt Equity:

The debt equity ratio of any company demonstrates the ratio between the total liabilities

OF the company and the shareholders equity father company. This ratio is an indication to

how much of the assets acquired by the company are financed by the equity shareholders of

the company. The more the amount recorded by the company in respect of the ratio, better

will be the liquidity or the solvency position of the company (Ogiela, 2015). It is seen from

the table that the Liabilities of the company has increased significantly over the years

whereas the shareholder so the company has decreased significantly over the period of one

year. The main reason behind this is the net loss that the company is earning for the last few

years. The additional capital that has been invested by the shareholders in the company

amounted to $1194369 and $1335303 in the year 1999 and 2000 respectively (Moutinho &

Vargas-Sanchez, 2018). The reason being that more number of shareholders invested in the

shares OF the company during this period. However, the total amount of the shareholders

equity is diminished by the accumulated deficit and the other comprehensive loss earned by

the company. The other comprehensive loss earned by the company amounted to (1709) and

(2376) for the year 1999 and 2000 respectively and for the same period the accumulated

deficit OF the company amounted to (882028) and (2293301) respectively for the year 1999

and 2000 respectively. Hence it can be seen that the company has been able to increase it is

paid up share capital over the years but the same could not be said about the total

Debt Equity Ratio

2000 1999

Total Liabilities 3102420 2199572

Shareholders’ Equity -970251 266278

Debt Equity Ratio -3.20 8.26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7FINANCIAL MANAGEMENT

shareholders equity. As the total shareholders, equity is subjected to the profits and the losses

earned by the company in the respective period (Andreou et al., 2014). As the company has

not been able to generate sufficient or positive returns, the debt equity ratio of the company

has dwindled over the years. This possess a serious threat to the solvency of the company as

the assets that are acquired by the company seems to be acquired by use of the borrowings

from the third parties or from institutions in the form of loan The company must immediately

strive to improve its profitability (Schaeck & Cihák, 2014).

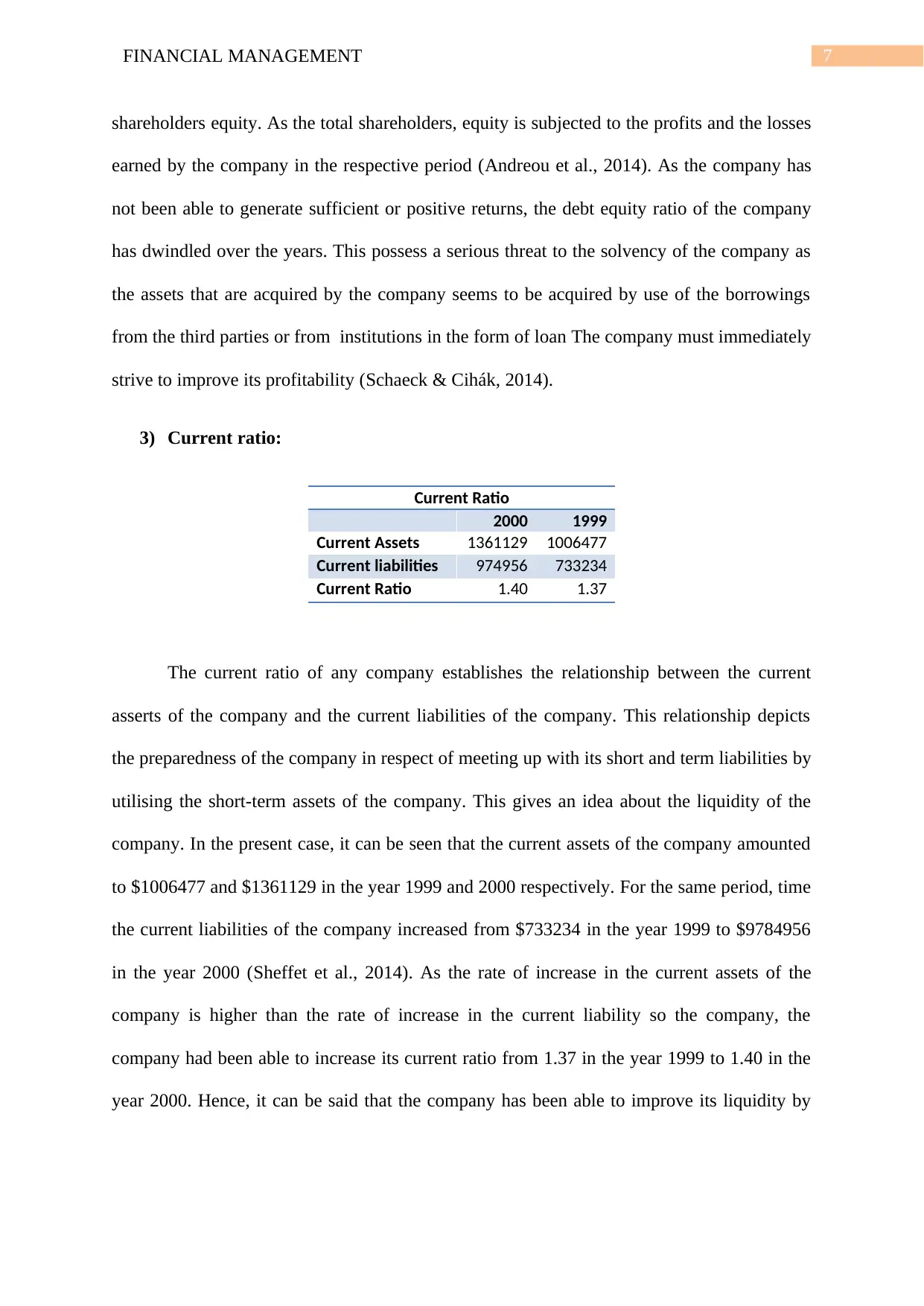

3) Current ratio:

Current Ratio

2000 1999

Current Assets 1361129 1006477

Current liabilities 974956 733234

Current Ratio 1.40 1.37

The current ratio of any company establishes the relationship between the current

asserts of the company and the current liabilities of the company. This relationship depicts

the preparedness of the company in respect of meeting up with its short and term liabilities by

utilising the short-term assets of the company. This gives an idea about the liquidity of the

company. In the present case, it can be seen that the current assets of the company amounted

to $1006477 and $1361129 in the year 1999 and 2000 respectively. For the same period, time

the current liabilities of the company increased from $733234 in the year 1999 to $9784956

in the year 2000 (Sheffet et al., 2014). As the rate of increase in the current assets of the

company is higher than the rate of increase in the current liability so the company, the

company had been able to increase its current ratio from 1.37 in the year 1999 to 1.40 in the

year 2000. Hence, it can be said that the company has been able to improve its liquidity by

shareholders equity. As the total shareholders, equity is subjected to the profits and the losses

earned by the company in the respective period (Andreou et al., 2014). As the company has

not been able to generate sufficient or positive returns, the debt equity ratio of the company

has dwindled over the years. This possess a serious threat to the solvency of the company as

the assets that are acquired by the company seems to be acquired by use of the borrowings

from the third parties or from institutions in the form of loan The company must immediately

strive to improve its profitability (Schaeck & Cihák, 2014).

3) Current ratio:

Current Ratio

2000 1999

Current Assets 1361129 1006477

Current liabilities 974956 733234

Current Ratio 1.40 1.37

The current ratio of any company establishes the relationship between the current

asserts of the company and the current liabilities of the company. This relationship depicts

the preparedness of the company in respect of meeting up with its short and term liabilities by

utilising the short-term assets of the company. This gives an idea about the liquidity of the

company. In the present case, it can be seen that the current assets of the company amounted

to $1006477 and $1361129 in the year 1999 and 2000 respectively. For the same period, time

the current liabilities of the company increased from $733234 in the year 1999 to $9784956

in the year 2000 (Sheffet et al., 2014). As the rate of increase in the current assets of the

company is higher than the rate of increase in the current liability so the company, the

company had been able to increase its current ratio from 1.37 in the year 1999 to 1.40 in the

year 2000. Hence, it can be said that the company has been able to improve its liquidity by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8FINANCIAL MANAGEMENT

improving its ability to meet up its current liabilities that crop up during the regular

operations of the company (Petty et al., 2015).

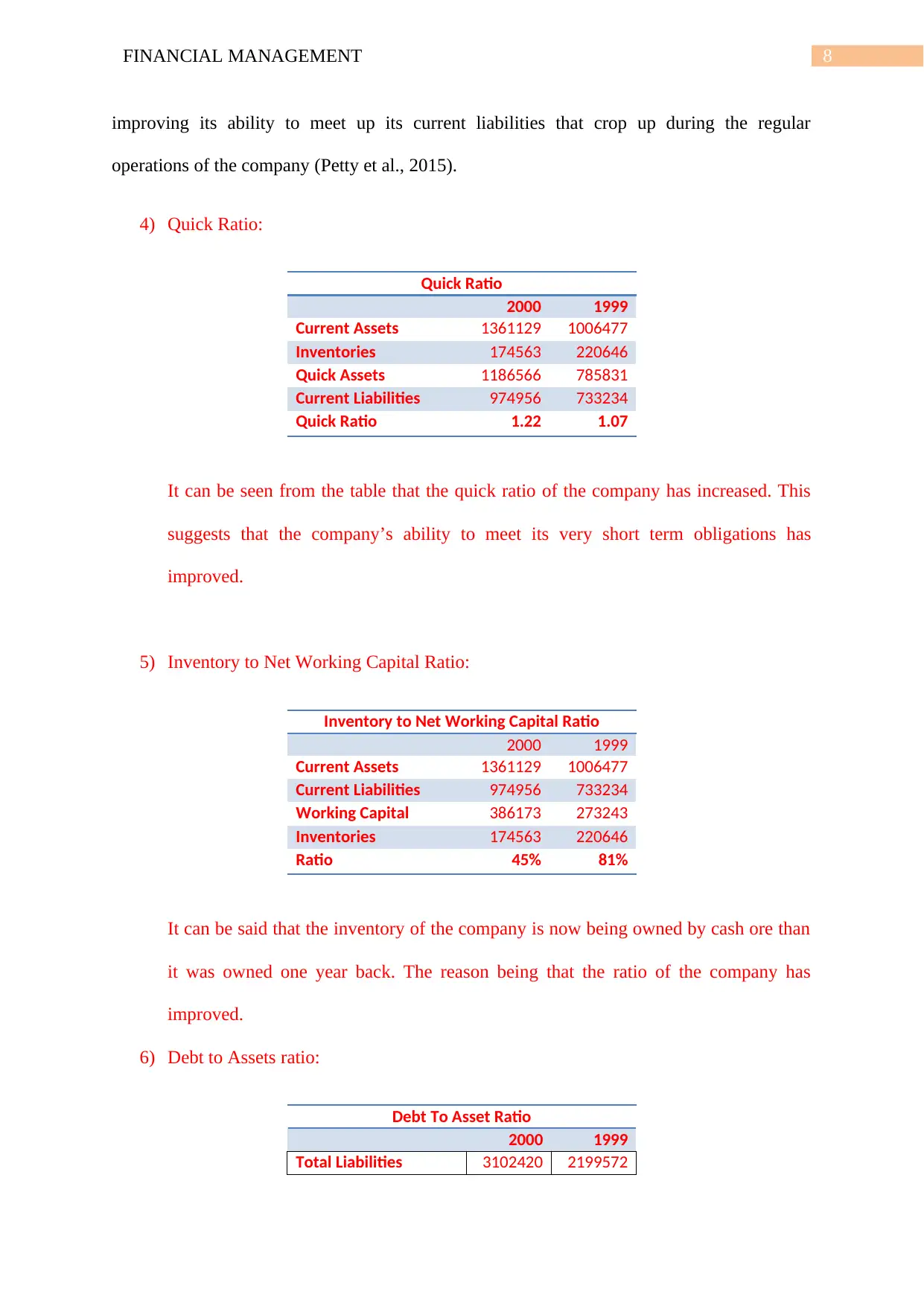

4) Quick Ratio:

Quick Ratio

2000 1999

Current Assets 1361129 1006477

Inventories 174563 220646

Quick Assets 1186566 785831

Current Liabilities 974956 733234

Quick Ratio 1.22 1.07

It can be seen from the table that the quick ratio of the company has increased. This

suggests that the company’s ability to meet its very short term obligations has

improved.

5) Inventory to Net Working Capital Ratio:

Inventory to Net Working Capital Ratio

2000 1999

Current Assets 1361129 1006477

Current Liabilities 974956 733234

Working Capital 386173 273243

Inventories 174563 220646

Ratio 45% 81%

It can be said that the inventory of the company is now being owned by cash ore than

it was owned one year back. The reason being that the ratio of the company has

improved.

6) Debt to Assets ratio:

Debt To Asset Ratio

2000 1999

Total Liabilities 3102420 2199572

improving its ability to meet up its current liabilities that crop up during the regular

operations of the company (Petty et al., 2015).

4) Quick Ratio:

Quick Ratio

2000 1999

Current Assets 1361129 1006477

Inventories 174563 220646

Quick Assets 1186566 785831

Current Liabilities 974956 733234

Quick Ratio 1.22 1.07

It can be seen from the table that the quick ratio of the company has increased. This

suggests that the company’s ability to meet its very short term obligations has

improved.

5) Inventory to Net Working Capital Ratio:

Inventory to Net Working Capital Ratio

2000 1999

Current Assets 1361129 1006477

Current Liabilities 974956 733234

Working Capital 386173 273243

Inventories 174563 220646

Ratio 45% 81%

It can be said that the inventory of the company is now being owned by cash ore than

it was owned one year back. The reason being that the ratio of the company has

improved.

6) Debt to Assets ratio:

Debt To Asset Ratio

2000 1999

Total Liabilities 3102420 2199572

9FINANCIAL MANAGEMENT

Total Assets 2135169 2465850

Debt To Asset Ratio 1.45 0.89

It can be seen that the total assets of the company has decreased over the period of

one year and for the same period the liabilities of the company has increased. Hence,

the ratio of the company has increased significantly.

7) Inventory Turnover Ratio:

Inventory Turnover Ratio

2000 1999

COGS 210620

6

134919

4

Inventory 174563 220646

Inventory Turnover Ratio 12.07 6.11

It can be noticed that the cost of goof sold of the company has increased over the

period of one year and during the same time; the inventory of the company has

decreased. Hence, the ratio has increased significantly over the period of one year.

8) Fixed Assets Turnover ratio:

Fixed Assets Turnover Ratio

2000 1999

Sales 276198

3

163983

9

Fixed Assets 366416 317613

Fixed Asset Turnover

Ratio

7.54 5.16

It can be seen that the fixed asset turnover ratio of the company has improved

significantly over the period of one year.

9) Total Assets Turnover ratio:

Total Assets Turnover Ratio

2000 1999

Sales 276198

3

163983

9

Total Assets 213516

9

246585

0

Total Assets 2135169 2465850

Debt To Asset Ratio 1.45 0.89

It can be seen that the total assets of the company has decreased over the period of

one year and for the same period the liabilities of the company has increased. Hence,

the ratio of the company has increased significantly.

7) Inventory Turnover Ratio:

Inventory Turnover Ratio

2000 1999

COGS 210620

6

134919

4

Inventory 174563 220646

Inventory Turnover Ratio 12.07 6.11

It can be noticed that the cost of goof sold of the company has increased over the

period of one year and during the same time; the inventory of the company has

decreased. Hence, the ratio has increased significantly over the period of one year.

8) Fixed Assets Turnover ratio:

Fixed Assets Turnover Ratio

2000 1999

Sales 276198

3

163983

9

Fixed Assets 366416 317613

Fixed Asset Turnover

Ratio

7.54 5.16

It can be seen that the fixed asset turnover ratio of the company has improved

significantly over the period of one year.

9) Total Assets Turnover ratio:

Total Assets Turnover Ratio

2000 1999

Sales 276198

3

163983

9

Total Assets 213516

9

246585

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10FINANCIAL MANAGEMENT

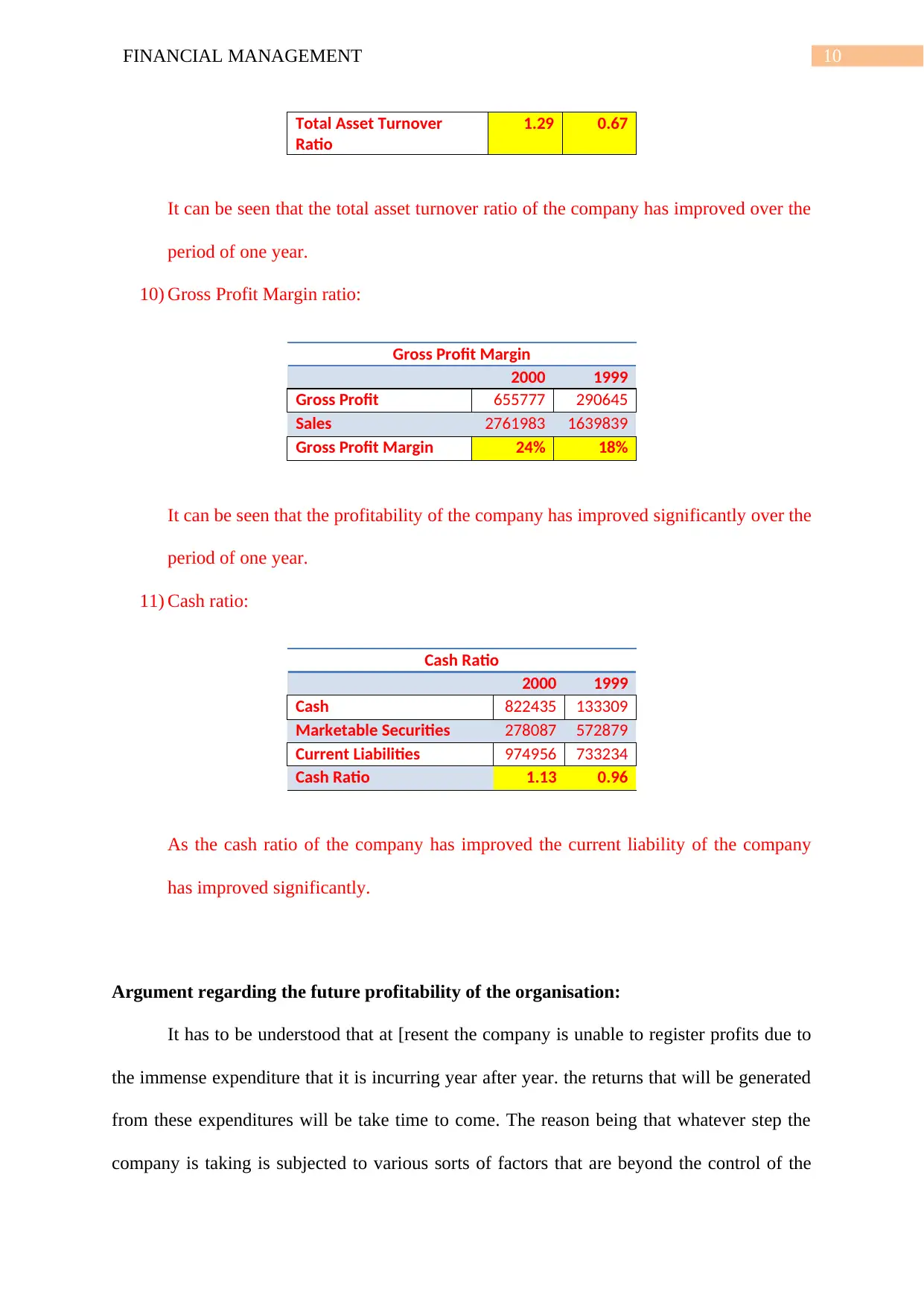

Total Asset Turnover

Ratio

1.29 0.67

It can be seen that the total asset turnover ratio of the company has improved over the

period of one year.

10) Gross Profit Margin ratio:

Gross Profit Margin

2000 1999

Gross Profit 655777 290645

Sales 2761983 1639839

Gross Profit Margin 24% 18%

It can be seen that the profitability of the company has improved significantly over the

period of one year.

11) Cash ratio:

Cash Ratio

2000 1999

Cash 822435 133309

Marketable Securities 278087 572879

Current Liabilities 974956 733234

Cash Ratio 1.13 0.96

As the cash ratio of the company has improved the current liability of the company

has improved significantly.

Argument regarding the future profitability of the organisation:

It has to be understood that at [resent the company is unable to register profits due to

the immense expenditure that it is incurring year after year. the returns that will be generated

from these expenditures will be take time to come. The reason being that whatever step the

company is taking is subjected to various sorts of factors that are beyond the control of the

Total Asset Turnover

Ratio

1.29 0.67

It can be seen that the total asset turnover ratio of the company has improved over the

period of one year.

10) Gross Profit Margin ratio:

Gross Profit Margin

2000 1999

Gross Profit 655777 290645

Sales 2761983 1639839

Gross Profit Margin 24% 18%

It can be seen that the profitability of the company has improved significantly over the

period of one year.

11) Cash ratio:

Cash Ratio

2000 1999

Cash 822435 133309

Marketable Securities 278087 572879

Current Liabilities 974956 733234

Cash Ratio 1.13 0.96

As the cash ratio of the company has improved the current liability of the company

has improved significantly.

Argument regarding the future profitability of the organisation:

It has to be understood that at [resent the company is unable to register profits due to

the immense expenditure that it is incurring year after year. the returns that will be generated

from these expenditures will be take time to come. The reason being that whatever step the

company is taking is subjected to various sorts of factors that are beyond the control of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11FINANCIAL MANAGEMENT

company and the company has to gain step back and mould its actions according to the

scenario that has cropped up recently (Attig et al., 2016). This is the reason why the company

is not making headway in terms of tangible profits to be shown to the shareholders of the

company. However, the potential of the company in respect OF its profit earning capacity

cannot be denied. The reason being that the consumer has completely accepted the model

presented before them by the company regarding online retailing. The change in the

preference of the consumers can be seen from the increased sales recorded by the company in

year in year on basis.

The impact of the competition on the functioning of the company:

There are severe implication so the competition that the company is facing from the

offline retailers in the present time. The purpose of countering them, the company had to

close the online portal of its website selling toys under the brand name of another company.

In place of selling it on amazon, the company is pairing up with the toy company so as to

create a website for the company, manage the inventory the company, and provide world

calls delivery services and customer services (Bundy et al., 2015). THz Toy Company in turn

is expected to own the inventory of Amazon Company. This model has significantly helped

the company to overcome the obstacle of the presence of competitors in the market. The

reason being that by optimally utilising its present asset the company is able to generate

profits without having to make the sale itself.

Different ethical considerations in case the organisation becomes insolvent:

Every organisation must remember the Iron Law of Responsibility. This law suggest that

the company is only a trustee of the resources OF the society. It must make sure that it

utilises the resources in the most appropriate manner possible and generate value for its

shareholders in return of the right granted to it by the society to use its resources. In case the

company and the company has to gain step back and mould its actions according to the

scenario that has cropped up recently (Attig et al., 2016). This is the reason why the company

is not making headway in terms of tangible profits to be shown to the shareholders of the

company. However, the potential of the company in respect OF its profit earning capacity

cannot be denied. The reason being that the consumer has completely accepted the model

presented before them by the company regarding online retailing. The change in the

preference of the consumers can be seen from the increased sales recorded by the company in

year in year on basis.

The impact of the competition on the functioning of the company:

There are severe implication so the competition that the company is facing from the

offline retailers in the present time. The purpose of countering them, the company had to

close the online portal of its website selling toys under the brand name of another company.

In place of selling it on amazon, the company is pairing up with the toy company so as to

create a website for the company, manage the inventory the company, and provide world

calls delivery services and customer services (Bundy et al., 2015). THz Toy Company in turn

is expected to own the inventory of Amazon Company. This model has significantly helped

the company to overcome the obstacle of the presence of competitors in the market. The

reason being that by optimally utilising its present asset the company is able to generate

profits without having to make the sale itself.

Different ethical considerations in case the organisation becomes insolvent:

Every organisation must remember the Iron Law of Responsibility. This law suggest that

the company is only a trustee of the resources OF the society. It must make sure that it

utilises the resources in the most appropriate manner possible and generate value for its

shareholders in return of the right granted to it by the society to use its resources. In case the

12FINANCIAL MANAGEMENT

company fails to meet the expectation of the society, it can take it back too (Pauw et al.,

2015). Hence, if the organisation becomes insolvent it must make sure to abide by several

ethical principles. They can be summarised as follows:

a) Makes sure that the information OF the insolvency is given out to the stakeholders in

the right time.

b) There should be no effort anthem part of the company to hide the severity of the

situation

c) The company must ensure that it cooperates with the liquidator in settling the

liabilities of the stakeholders who have a preferential right over the assets of the

company before the non-preferential stakeholders of the company (Cashin et al.,

2017).

d) The shareholders must make sure that the company abides by all the rules and

regulations in respect of liquidation of the companies.

The various external factors that are needed to be taken into consideration and the

likely hood of merger and acquisition:

The are several external factors that are going to affect the business of the entity. They as

follows:

a) The presence of the competitors-

There are several competitors that are going to crop up before the company from time

to time. In order to deal within the same the company needs to continuously monitor

the various ways in which it can gain an added advantage over its competitors.

b) the change in the tastes and the preferences of the customer from time to time-

company fails to meet the expectation of the society, it can take it back too (Pauw et al.,

2015). Hence, if the organisation becomes insolvent it must make sure to abide by several

ethical principles. They can be summarised as follows:

a) Makes sure that the information OF the insolvency is given out to the stakeholders in

the right time.

b) There should be no effort anthem part of the company to hide the severity of the

situation

c) The company must ensure that it cooperates with the liquidator in settling the

liabilities of the stakeholders who have a preferential right over the assets of the

company before the non-preferential stakeholders of the company (Cashin et al.,

2017).

d) The shareholders must make sure that the company abides by all the rules and

regulations in respect of liquidation of the companies.

The various external factors that are needed to be taken into consideration and the

likely hood of merger and acquisition:

The are several external factors that are going to affect the business of the entity. They as

follows:

a) The presence of the competitors-

There are several competitors that are going to crop up before the company from time

to time. In order to deal within the same the company needs to continuously monitor

the various ways in which it can gain an added advantage over its competitors.

b) the change in the tastes and the preferences of the customer from time to time-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.