BSBFIM601 Manage Finance Assignment: Financial Reporting and Taxation

VerifiedAdded on 2022/11/29

|18

|3292

|241

Homework Assignment

AI Summary

This assignment addresses key aspects of financial management, including financial probity, fraudulent behavior, and the requirements for audited accounts. It explores cash and accrual accounting principles, outlining their advantages and disadvantages. The assignment also covers taxation and superannuation obligations for businesses, detailing the Australian Business Number (ABN), Goods and Services Tax (GST), Pay As You Go (PAYG), and Fringe Benefits Tax (FBT). Additionally, it examines the requirements for financial reporting and auditing under the Corporations Act 2001, including those for registered foreign companies. The document further includes a profit and loss statement, a cash flow statement, and a budget statement analysis, providing practical application of financial concepts. Finally, the document discusses GST reporting processes and withholding obligations for employees and contractors.

Running head - MANAGE FINANCE

Manage Finance

Name of the student

Name of the university

Author’s note

Manage Finance

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGE FINANCE

Assessment Task 1

1. Identify and describe financial probity requirements for businesses.

Answer - A public authority must be able to demonstrate to suppliers and the community that

it conducts its procurement activities with high standards of probity and accountability

Probity requires that a public authority conduct its procurement activities ethically,

honestly and fairly. Elements of a procurement culture that promotes and demonstrates high

standards of probity include the following:

Expected behaviours are articulated and enforced.

Officers involved are skilled, knowledgeable and experienced.

Appropriate checks and balances are in place at various stages in the procurement

process.

Accountability requires that a public authority be able to publicly account for its

decisions and take responsibility for the achievement of procurement outcomes. Elements of

a procurement culture that promotes and demonstrates a high level of accountability include

the following:

Responsibility for decisions is readily identifiable.

Adequate records are maintained to enable external scrutiny of decisions.

2. Identify four examples of what would be consider fraudulent behaviour in regard to

company finances.

Answer –

Assessment Task 1

1. Identify and describe financial probity requirements for businesses.

Answer - A public authority must be able to demonstrate to suppliers and the community that

it conducts its procurement activities with high standards of probity and accountability

Probity requires that a public authority conduct its procurement activities ethically,

honestly and fairly. Elements of a procurement culture that promotes and demonstrates high

standards of probity include the following:

Expected behaviours are articulated and enforced.

Officers involved are skilled, knowledgeable and experienced.

Appropriate checks and balances are in place at various stages in the procurement

process.

Accountability requires that a public authority be able to publicly account for its

decisions and take responsibility for the achievement of procurement outcomes. Elements of

a procurement culture that promotes and demonstrates a high level of accountability include

the following:

Responsibility for decisions is readily identifiable.

Adequate records are maintained to enable external scrutiny of decisions.

2. Identify four examples of what would be consider fraudulent behaviour in regard to

company finances.

Answer –

2MANAGE FINANCE

Check Forgery

An employee forges a signature on a check made out to himself/herself or to someone

else.

Check Kiting

An employee writes checks on an account that doesn’t have sufficient funds with the

expectation that the funds will be in the account before the check clears.

Check Tampering

An employee alters the payee, amount or other details on a check or creates an

unauthorized check.

Inventory Theft

An employee steals product from a company, either by physically taking it or

diverting it in some other way.

3. Identify the requirements for audited accounts and the purpose of an audit report.

Answer –

Audit exemption statement

It must include the following statement on the balance sheet of your accounts if they are

using an audit exemption. For the year ending the company was entitled to exemption from

audit under section 477 of the Companies Act 2006 relating to small companies. The

members have not required the company to obtain an audit of its accounts for the year in

question in accordance with section 476. The directors acknowledge their responsibilities for

complying with the requirements of the Act with respect to accounting records and the

Check Forgery

An employee forges a signature on a check made out to himself/herself or to someone

else.

Check Kiting

An employee writes checks on an account that doesn’t have sufficient funds with the

expectation that the funds will be in the account before the check clears.

Check Tampering

An employee alters the payee, amount or other details on a check or creates an

unauthorized check.

Inventory Theft

An employee steals product from a company, either by physically taking it or

diverting it in some other way.

3. Identify the requirements for audited accounts and the purpose of an audit report.

Answer –

Audit exemption statement

It must include the following statement on the balance sheet of your accounts if they are

using an audit exemption. For the year ending the company was entitled to exemption from

audit under section 477 of the Companies Act 2006 relating to small companies. The

members have not required the company to obtain an audit of its accounts for the year in

question in accordance with section 476. The directors acknowledge their responsibilities for

complying with the requirements of the Act with respect to accounting records and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGE FINANCE

preparation of accounts. These accounts have been prepared in accordance with the

provisions applicable to companies subject to the small companies’ regime.

An annual turnover of no more than £10.2 million

Assets worth no more than £5.1 million

50 or fewer employees on average

In articulating the purpose of an audit it is critical to clarify and understand the purpose of

financial statements. Though this was not one of the group’s objectives, members of the

group felt that it would be difficult to consider the purpose of the audit without looking at the

purpose of financial statements.

4. Describe the principle of cash accounting one advantage and one disadvantage of

cash accounting.

Answer –

Understanding Cash Accounting

Cash accounting is one of two forms of accounting. The other is accrual accounting,

where revenue and expenses are recorded when they are incurred. Small businesses often use

cash accounting because it is simpler and more straightforward and it provides a clear picture

of how much money the business actually has on hand.

One Advantage

Simple: As a business, you have to choose one of the accounting methods. If you choose this

accounting, it’s the simplest because you will only record transactions that are related to cash.

Other transactions won’t be taken into consideration.

preparation of accounts. These accounts have been prepared in accordance with the

provisions applicable to companies subject to the small companies’ regime.

An annual turnover of no more than £10.2 million

Assets worth no more than £5.1 million

50 or fewer employees on average

In articulating the purpose of an audit it is critical to clarify and understand the purpose of

financial statements. Though this was not one of the group’s objectives, members of the

group felt that it would be difficult to consider the purpose of the audit without looking at the

purpose of financial statements.

4. Describe the principle of cash accounting one advantage and one disadvantage of

cash accounting.

Answer –

Understanding Cash Accounting

Cash accounting is one of two forms of accounting. The other is accrual accounting,

where revenue and expenses are recorded when they are incurred. Small businesses often use

cash accounting because it is simpler and more straightforward and it provides a clear picture

of how much money the business actually has on hand.

One Advantage

Simple: As a business, you have to choose one of the accounting methods. If you choose this

accounting, it’s the simplest because you will only record transactions that are related to cash.

Other transactions won’t be taken into consideration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGE FINANCE

One Disadvantage

Not very accurate: Since it is only recorded cash transactions, It doesn’t include all the

transactions. As a result, we can’t say that cash accounting is very accurate. Plus under this

accounting revenue or expenses is recorded when the company receives or pays cash, even in

the different accounting period.

5. Describe the principle of accrual accounting and one advantage and one disadvantage

of accrual accounting.

Answer –

Accrual Accounting

Accrual accounting is considered to be the standard accounting practice for most

companies, with the exception of very small businesses. This method provides a more

accurate picture of the company's current condition, but its relative complexity makes it more

expensive to implement.

One Advantage

The matching of expenses and revenue using this method allows you to conduct more

useful business analysis. For instance, when you purchase expensive machinery to be used

over the next decade, its cost will be spread over such a period. Just as this time frame will

see some benefits of the equipment, each year in the period will also get some of the expenses

through the revenue gained from selling products the machine has produced.

One disadvantages

Difficulty is one huge drawback of accrual basis accounting, where rules in the

recognition of revenue and expenses can be very complicated. Now, if you want to fully and

One Disadvantage

Not very accurate: Since it is only recorded cash transactions, It doesn’t include all the

transactions. As a result, we can’t say that cash accounting is very accurate. Plus under this

accounting revenue or expenses is recorded when the company receives or pays cash, even in

the different accounting period.

5. Describe the principle of accrual accounting and one advantage and one disadvantage

of accrual accounting.

Answer –

Accrual Accounting

Accrual accounting is considered to be the standard accounting practice for most

companies, with the exception of very small businesses. This method provides a more

accurate picture of the company's current condition, but its relative complexity makes it more

expensive to implement.

One Advantage

The matching of expenses and revenue using this method allows you to conduct more

useful business analysis. For instance, when you purchase expensive machinery to be used

over the next decade, its cost will be spread over such a period. Just as this time frame will

see some benefits of the equipment, each year in the period will also get some of the expenses

through the revenue gained from selling products the machine has produced.

One disadvantages

Difficulty is one huge drawback of accrual basis accounting, where rules in the

recognition of revenue and expenses can be very complicated. Now, if you want to fully and

5MANAGE FINANCE

record transactions in your small business in accordance with GAAP, you should seek the

help of an accountant.

6. Explain the four main taxation and superannuation obligations for a business.

Briefly discuss each obligation.

Answer –

Australian business number (ABN)

Consider getting an ABN for your business. An ABN helps to manage your tax and

business obligations, and is used as a reference by the Australian Taxation Office (ATO) for

your business. You will also use your ABN when dealing with other businesses and

government departments.

Goods and services tax (GST)

GST is a broad-based tax of 10% imposed on most goods, services and other items

sold in Australia. Depending on your turnover or service, you may need to register for GST.

Pay as you go (PAYG)

PAYG is a system that allows you to pay an expected tax liability in instalments. The

ATO will notify you of your PAYG obligations

Fringe benefits tax (FBT)

If you (or a person on your behalf) provide certain benefits to your employees or to

people associated with your employees, you may be liable for FBT. If so, you must register

for FBT with the ATO, and lodge a return each year.

record transactions in your small business in accordance with GAAP, you should seek the

help of an accountant.

6. Explain the four main taxation and superannuation obligations for a business.

Briefly discuss each obligation.

Answer –

Australian business number (ABN)

Consider getting an ABN for your business. An ABN helps to manage your tax and

business obligations, and is used as a reference by the Australian Taxation Office (ATO) for

your business. You will also use your ABN when dealing with other businesses and

government departments.

Goods and services tax (GST)

GST is a broad-based tax of 10% imposed on most goods, services and other items

sold in Australia. Depending on your turnover or service, you may need to register for GST.

Pay as you go (PAYG)

PAYG is a system that allows you to pay an expected tax liability in instalments. The

ATO will notify you of your PAYG obligations

Fringe benefits tax (FBT)

If you (or a person on your behalf) provide certain benefits to your employees or to

people associated with your employees, you may be liable for FBT. If so, you must register

for FBT with the ATO, and lodge a return each year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGE FINANCE

7. Identify the Act that details requirements for financial reporting and auditing and,

explain the requirements for companies for preparing and lodging financial reports

under this Act.

Answer –

This section contains information about the financial reporting and auditing

requirements under the Corporations Act 2001 (Corporations Act).

ASIC regulates compliance with the financial reporting and auditing requirements for

entities subject to the Corporations Act and provides relief from those requirements in certain

circumstances. Our active monitoring of entities’ compliance with these requirements

contributes directly to market integrity and investor confidence. It seeks to ensure that the

financial reports and audit opinions issued are relevant and reliable, and help users make

better informed decisions in the marketplace.

8. Explain the requirements for registered foreign companies regarding preparing and

lodging financial reports.

Answer –

7. Identify the Act that details requirements for financial reporting and auditing and,

explain the requirements for companies for preparing and lodging financial reports

under this Act.

Answer –

This section contains information about the financial reporting and auditing

requirements under the Corporations Act 2001 (Corporations Act).

ASIC regulates compliance with the financial reporting and auditing requirements for

entities subject to the Corporations Act and provides relief from those requirements in certain

circumstances. Our active monitoring of entities’ compliance with these requirements

contributes directly to market integrity and investor confidence. It seeks to ensure that the

financial reports and audit opinions issued are relevant and reliable, and help users make

better informed decisions in the marketplace.

8. Explain the requirements for registered foreign companies regarding preparing and

lodging financial reports.

Answer –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE FINANCE

If an entity satisfies the definition of ‘foreign company’ in section 9 of the

Corporations Act 2001 (Corporations Act) – that is, generally, a company registered outside

Australia – it must be registered with ASIC to carry on business in Australia.

If you’re unsure if your entity satisfies the definition of a foreign company carrying

on business in Australia, we recommend getting your own advice. Corporations sole, exempt

public authorities and unincorporated bodies that were formed outside Australia and cannot

hold property, or sue or be sued in accordance wi th the law of their place of formation, are

not foreign companies.

9. Identify the current company tax rate for both smaller and larger businesses.

Answer - Income tax is levied on the total income of the company computed as per the

Income Tax Act. Total income of a company is closely related to the profit of the company.

Total income is not related to the turnover or sales revenue of a company.

10. Explain the process by which a business reports GST to the Australian Tax Office.

Answer –

GST reporting and payment cycle will be one of the following:

Monthly – if your GST turnover is $20 million or more.

Quarterly – if your GST turnover is less than $20 million – and we have not told you that you

must report monthly.

Annually – if you are voluntarily registered for GST. That is, you are registered for GST; and

your GST turnover is under $75,000

If an entity satisfies the definition of ‘foreign company’ in section 9 of the

Corporations Act 2001 (Corporations Act) – that is, generally, a company registered outside

Australia – it must be registered with ASIC to carry on business in Australia.

If you’re unsure if your entity satisfies the definition of a foreign company carrying

on business in Australia, we recommend getting your own advice. Corporations sole, exempt

public authorities and unincorporated bodies that were formed outside Australia and cannot

hold property, or sue or be sued in accordance wi th the law of their place of formation, are

not foreign companies.

9. Identify the current company tax rate for both smaller and larger businesses.

Answer - Income tax is levied on the total income of the company computed as per the

Income Tax Act. Total income of a company is closely related to the profit of the company.

Total income is not related to the turnover or sales revenue of a company.

10. Explain the process by which a business reports GST to the Australian Tax Office.

Answer –

GST reporting and payment cycle will be one of the following:

Monthly – if your GST turnover is $20 million or more.

Quarterly – if your GST turnover is less than $20 million – and we have not told you that you

must report monthly.

Annually – if you are voluntarily registered for GST. That is, you are registered for GST; and

your GST turnover is under $75,000

8MANAGE FINANCE

11. Identify the penalty rate to be applied if a supplier does not provide an ABN?

Answer –

If the supplier does not provide an ABN and the total payment for goods and services

is more than $75 (excluding GST) you generally withhold the top rate of tax from the

payment and pay it to us.

If a supplier has applied for an ABN you can offer to hold payment until they have

obtained and quoted their ABN. This is a matter for you and your supplier to work out.

However you must not make full payment to the supplier on the understanding that an ABN

will be quoted later.

12. A non-profit organisation needs to register for GST after it has a turnover of more

than how much?

Answer –

You must register for GST if:

Your business has a GST turnover of $75,000 or more

Your non-profit organisation has a turnover of $150,000 per year or more

You provide taxi travel for passengers in exchange for a fare as part of your business,

regardless of your GST turnover. This rule applies to both taxi owner drivers and people who

just rent a taxi.

11. Identify the penalty rate to be applied if a supplier does not provide an ABN?

Answer –

If the supplier does not provide an ABN and the total payment for goods and services

is more than $75 (excluding GST) you generally withhold the top rate of tax from the

payment and pay it to us.

If a supplier has applied for an ABN you can offer to hold payment until they have

obtained and quoted their ABN. This is a matter for you and your supplier to work out.

However you must not make full payment to the supplier on the understanding that an ABN

will be quoted later.

12. A non-profit organisation needs to register for GST after it has a turnover of more

than how much?

Answer –

You must register for GST if:

Your business has a GST turnover of $75,000 or more

Your non-profit organisation has a turnover of $150,000 per year or more

You provide taxi travel for passengers in exchange for a fare as part of your business,

regardless of your GST turnover. This rule applies to both taxi owner drivers and people who

just rent a taxi.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGE FINANCE

13. Explain the difference in Pay As You Go withholding obligations for employees and

contractors.

Answer –

Pay As You Go (PAYG) withholding is a legal requirement to withhold amounts for

income tax purposes.

If you have employees, you're required to withhold tax from payments you make to

them. You may have to withhold tax from payments to other workers, such as contract

workers. As a new employer, you must register with the Australian Taxation Office (ATO)

before you withhold from payments to your employees.

13. Explain the difference in Pay As You Go withholding obligations for employees and

contractors.

Answer –

Pay As You Go (PAYG) withholding is a legal requirement to withhold amounts for

income tax purposes.

If you have employees, you're required to withhold tax from payments you make to

them. You may have to withhold tax from payments to other workers, such as contract

workers. As a new employer, you must register with the Australian Taxation Office (ATO)

before you withhold from payments to your employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGE FINANCE

Assessment Task 2

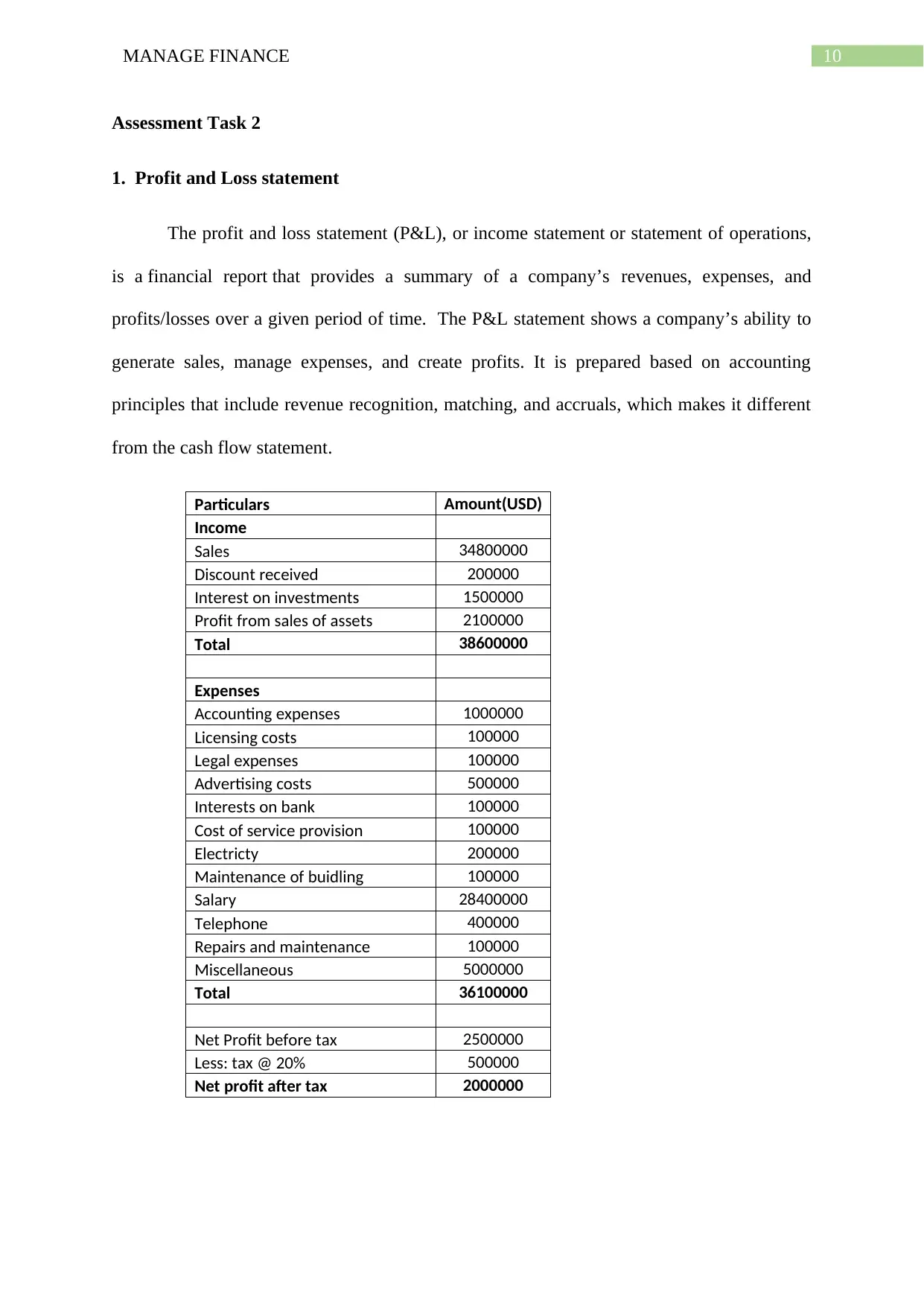

1. Profit and Loss statement

The profit and loss statement (P&L), or income statement or statement of operations,

is a financial report that provides a summary of a company’s revenues, expenses, and

profits/losses over a given period of time. The P&L statement shows a company’s ability to

generate sales, manage expenses, and create profits. It is prepared based on accounting

principles that include revenue recognition, matching, and accruals, which makes it different

from the cash flow statement.

Particulars Amount(USD)

Income

Sales 34800000

Discount received 200000

Interest on investments 1500000

Profit from sales of assets 2100000

Total 38600000

Expenses

Accounting expenses 1000000

Licensing costs 100000

Legal expenses 100000

Advertising costs 500000

Interests on bank 100000

Cost of service provision 100000

Electricty 200000

Maintenance of buidling 100000

Salary 28400000

Telephone 400000

Repairs and maintenance 100000

Miscellaneous 5000000

Total 36100000

Net Profit before tax 2500000

Less: tax @ 20% 500000

Net profit after tax 2000000

Assessment Task 2

1. Profit and Loss statement

The profit and loss statement (P&L), or income statement or statement of operations,

is a financial report that provides a summary of a company’s revenues, expenses, and

profits/losses over a given period of time. The P&L statement shows a company’s ability to

generate sales, manage expenses, and create profits. It is prepared based on accounting

principles that include revenue recognition, matching, and accruals, which makes it different

from the cash flow statement.

Particulars Amount(USD)

Income

Sales 34800000

Discount received 200000

Interest on investments 1500000

Profit from sales of assets 2100000

Total 38600000

Expenses

Accounting expenses 1000000

Licensing costs 100000

Legal expenses 100000

Advertising costs 500000

Interests on bank 100000

Cost of service provision 100000

Electricty 200000

Maintenance of buidling 100000

Salary 28400000

Telephone 400000

Repairs and maintenance 100000

Miscellaneous 5000000

Total 36100000

Net Profit before tax 2500000

Less: tax @ 20% 500000

Net profit after tax 2000000

11MANAGE FINANCE

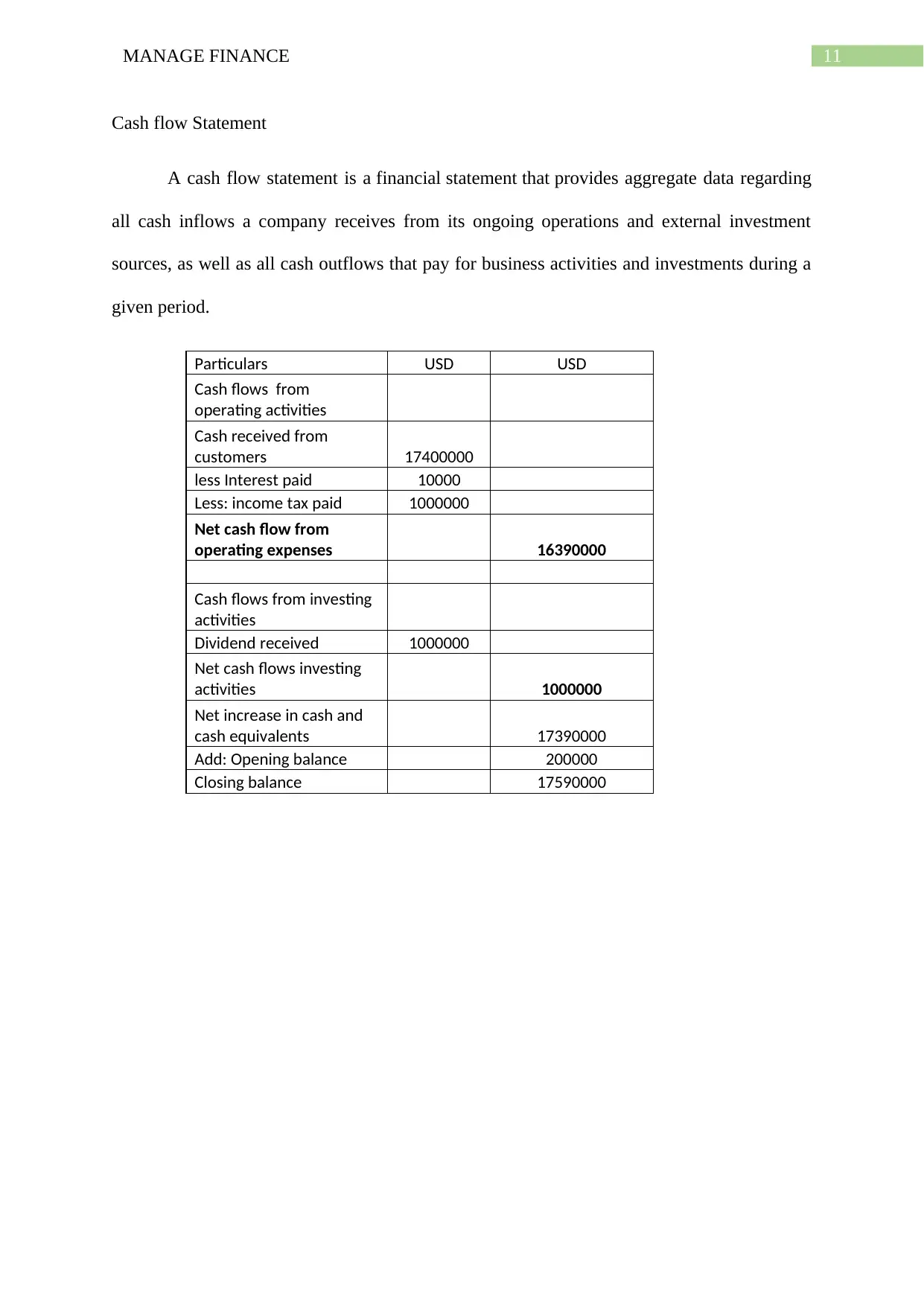

Cash flow Statement

A cash flow statement is a financial statement that provides aggregate data regarding

all cash inflows a company receives from its ongoing operations and external investment

sources, as well as all cash outflows that pay for business activities and investments during a

given period.

Particulars USD USD

Cash flows from

operating activities

Cash received from

customers 17400000

less Interest paid 10000

Less: income tax paid 1000000

Net cash flow from

operating expenses 16390000

Cash flows from investing

activities

Dividend received 1000000

Net cash flows investing

activities 1000000

Net increase in cash and

cash equivalents 17390000

Add: Opening balance 200000

Closing balance 17590000

Cash flow Statement

A cash flow statement is a financial statement that provides aggregate data regarding

all cash inflows a company receives from its ongoing operations and external investment

sources, as well as all cash outflows that pay for business activities and investments during a

given period.

Particulars USD USD

Cash flows from

operating activities

Cash received from

customers 17400000

less Interest paid 10000

Less: income tax paid 1000000

Net cash flow from

operating expenses 16390000

Cash flows from investing

activities

Dividend received 1000000

Net cash flows investing

activities 1000000

Net increase in cash and

cash equivalents 17390000

Add: Opening balance 200000

Closing balance 17590000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

![BSBFIM601 Manage Finances: Assessment Report, [Semester], [College]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fxm%2F162b9d69229e4e1db10d1eff3736f19c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.