University Accounting Report: Downer Ltd Financial Analysis

VerifiedAdded on 2021/05/31

|12

|2714

|48

Report

AI Summary

This report provides a detailed analysis of Downer Ltd's corporate accounting practices. It begins with an examination of the cash flow statement, highlighting significant items such as cash from operating, investing, and financing activities, and includes a comparative analysis across three years. The report then delves into the other comprehensive income statement, explaining the items reported and their understanding, followed by a discussion on the reporting of comprehensive income. Furthermore, the report covers accounting for income tax, including current tax expenses, the rate of tax charged, deferred tax assets and liabilities, and current tax assets and liabilities. It also addresses the difference in income tax expenses and income tax paid and reviews the tax policy of the business. The analysis is based on the financial statements of Downer Ltd, providing a comprehensive overview of its financial performance and accounting practices.

Running head: CORPORATE ACCOUNITNG

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Analysis of Cash Flow Statement....................................................................................................2

Significant Items included in Cash Flow Statement....................................................................2

Comparative Analysis of Three Classification of Cash Flow Statement....................................3

Other Comprehensive Income Statement........................................................................................5

Items reported as Other Comprehensive Income.........................................................................5

Understanding of Items shown under Comprehensive Income...................................................6

Reporting of Comprehensive Income..........................................................................................6

Accounting for Income Tax.............................................................................................................6

Current Tax Expenses..................................................................................................................6

Rate of tax charged by the business.............................................................................................7

Deferred Tax Assets and Liabilities............................................................................................7

Current Tax Assets and Liabilities..............................................................................................8

Difference in Income tax expenses and Income Tax paid...........................................................8

Review of the Tax policy of the business....................................................................................9

Reference.......................................................................................................................................10

CORPORATE ACCOUNTING

Table of Contents

Analysis of Cash Flow Statement....................................................................................................2

Significant Items included in Cash Flow Statement....................................................................2

Comparative Analysis of Three Classification of Cash Flow Statement....................................3

Other Comprehensive Income Statement........................................................................................5

Items reported as Other Comprehensive Income.........................................................................5

Understanding of Items shown under Comprehensive Income...................................................6

Reporting of Comprehensive Income..........................................................................................6

Accounting for Income Tax.............................................................................................................6

Current Tax Expenses..................................................................................................................6

Rate of tax charged by the business.............................................................................................7

Deferred Tax Assets and Liabilities............................................................................................7

Current Tax Assets and Liabilities..............................................................................................8

Difference in Income tax expenses and Income Tax paid...........................................................8

Review of the Tax policy of the business....................................................................................9

Reference.......................................................................................................................................10

2

CORPORATE ACCOUNTING

Analysis of Cash Flow Statement

Significant Items included in Cash Flow Statement

The cash flow statement is a part of the financial statements of the business which is to be

published with the profit and loss statement of the business and the balance sheet of the

company. The cash flow statement shows the cash inflows and outflow of the business and

ultimately shows the closing cash balance which is available to the company at the end of the

year (Call, Chen and Tong 2013). Cash flow statements are prepared by businesses to show the

liquidity of the business. The company which is selected for this assignment is Downer ltd for

which the analysis is to be conducted in the coming paragraphs.

The cash flow statement of Downer ltd shown and prepared as per the requirements of

relevant accounting standards and principles (Downer Corporate Site. 2018). The major items

which are shown in the cash from operating activities are the cash which the business collects

from the customers in case of credit sales. payments made to creditors and the income tax which

is applicable to the business during the year (Kaspina, Molotov and Kaspin 2015). The receipts

from the customers represents the main source of revenue for the business from operating

activities and the same is generated from sales and revenue generating activities of the business.

As per the financial statements for the year 2017, the cash which is collected from the customers

as shown in the cash flow statement for the year 2017 is $ 7957.7 million which has significantly

increased from the previous year which was shown to be $ 7615 million. The cash flow

statement of the business shows that the cash which is paid to the suppliers have also increased

from previous year and the same is shown as $ 7262 million and the sane was shown as 7123.4

million in 2016. The income tax of the business has also increased which is quite natural as the

CORPORATE ACCOUNTING

Analysis of Cash Flow Statement

Significant Items included in Cash Flow Statement

The cash flow statement is a part of the financial statements of the business which is to be

published with the profit and loss statement of the business and the balance sheet of the

company. The cash flow statement shows the cash inflows and outflow of the business and

ultimately shows the closing cash balance which is available to the company at the end of the

year (Call, Chen and Tong 2013). Cash flow statements are prepared by businesses to show the

liquidity of the business. The company which is selected for this assignment is Downer ltd for

which the analysis is to be conducted in the coming paragraphs.

The cash flow statement of Downer ltd shown and prepared as per the requirements of

relevant accounting standards and principles (Downer Corporate Site. 2018). The major items

which are shown in the cash from operating activities are the cash which the business collects

from the customers in case of credit sales. payments made to creditors and the income tax which

is applicable to the business during the year (Kaspina, Molotov and Kaspin 2015). The receipts

from the customers represents the main source of revenue for the business from operating

activities and the same is generated from sales and revenue generating activities of the business.

As per the financial statements for the year 2017, the cash which is collected from the customers

as shown in the cash flow statement for the year 2017 is $ 7957.7 million which has significantly

increased from the previous year which was shown to be $ 7615 million. The cash flow

statement of the business shows that the cash which is paid to the suppliers have also increased

from previous year and the same is shown as $ 7262 million and the sane was shown as 7123.4

million in 2016. The income tax of the business has also increased which is quite natural as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

sales revenue of the business has increased and the profit of the business has also increased

(Stevanović, Belopavlović and Lazarević-Moravčević 2017). The income tax which is to be paid

by the business for the year 2017 is shown as $49 million.

As per the cash flow statement of the business, the company has incurred significant

amount of expenses for the purpose of purchasing assets for the business. As per the cash flow

statement, the company has sold a part of property, plant and equipment which is shown to be $

23.2 million during the year 2017. The purchases of property, plant and equity which is made

during the year is shown to be $ 203.6 million which has significantly increased from previous

year’s expenditure. The company has also acquired intangible assets for which the amount which

is shown in the cash flow statement is $ 37.9 million and also acquired businesses which is

shown to be $ 143.2 million.

The main components which is shown in the cash flow statement for the year 2017 are

capital acquired, repayment of borrowings and dividend payed by the business. The company has

raised a capital of $989.9 million which is related to the takeover of the business which the

company has engaged in during the year. The company has also paid back a significant amount

of loan which is shown in the cash flow statement as $ 370 million. The company’s objective

behind such a significant amount of loan repayment may be to restructure the capital structure of

the business. The company has also declared a dividend for the year at $ 110.6 million which

signifies that the profitability of the business has increased and the business is performing well.

Comparative Analysis of Three Classification of Cash Flow Statement

Particular 2015 2016 2017

Net cash flows from operating activities

$

486.50

$

447.80

$

441.60

CORPORATE ACCOUNTING

sales revenue of the business has increased and the profit of the business has also increased

(Stevanović, Belopavlović and Lazarević-Moravčević 2017). The income tax which is to be paid

by the business for the year 2017 is shown as $49 million.

As per the cash flow statement of the business, the company has incurred significant

amount of expenses for the purpose of purchasing assets for the business. As per the cash flow

statement, the company has sold a part of property, plant and equipment which is shown to be $

23.2 million during the year 2017. The purchases of property, plant and equity which is made

during the year is shown to be $ 203.6 million which has significantly increased from previous

year’s expenditure. The company has also acquired intangible assets for which the amount which

is shown in the cash flow statement is $ 37.9 million and also acquired businesses which is

shown to be $ 143.2 million.

The main components which is shown in the cash flow statement for the year 2017 are

capital acquired, repayment of borrowings and dividend payed by the business. The company has

raised a capital of $989.9 million which is related to the takeover of the business which the

company has engaged in during the year. The company has also paid back a significant amount

of loan which is shown in the cash flow statement as $ 370 million. The company’s objective

behind such a significant amount of loan repayment may be to restructure the capital structure of

the business. The company has also declared a dividend for the year at $ 110.6 million which

signifies that the profitability of the business has increased and the business is performing well.

Comparative Analysis of Three Classification of Cash Flow Statement

Particular 2015 2016 2017

Net cash flows from operating activities

$

486.50

$

447.80

$

441.60

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

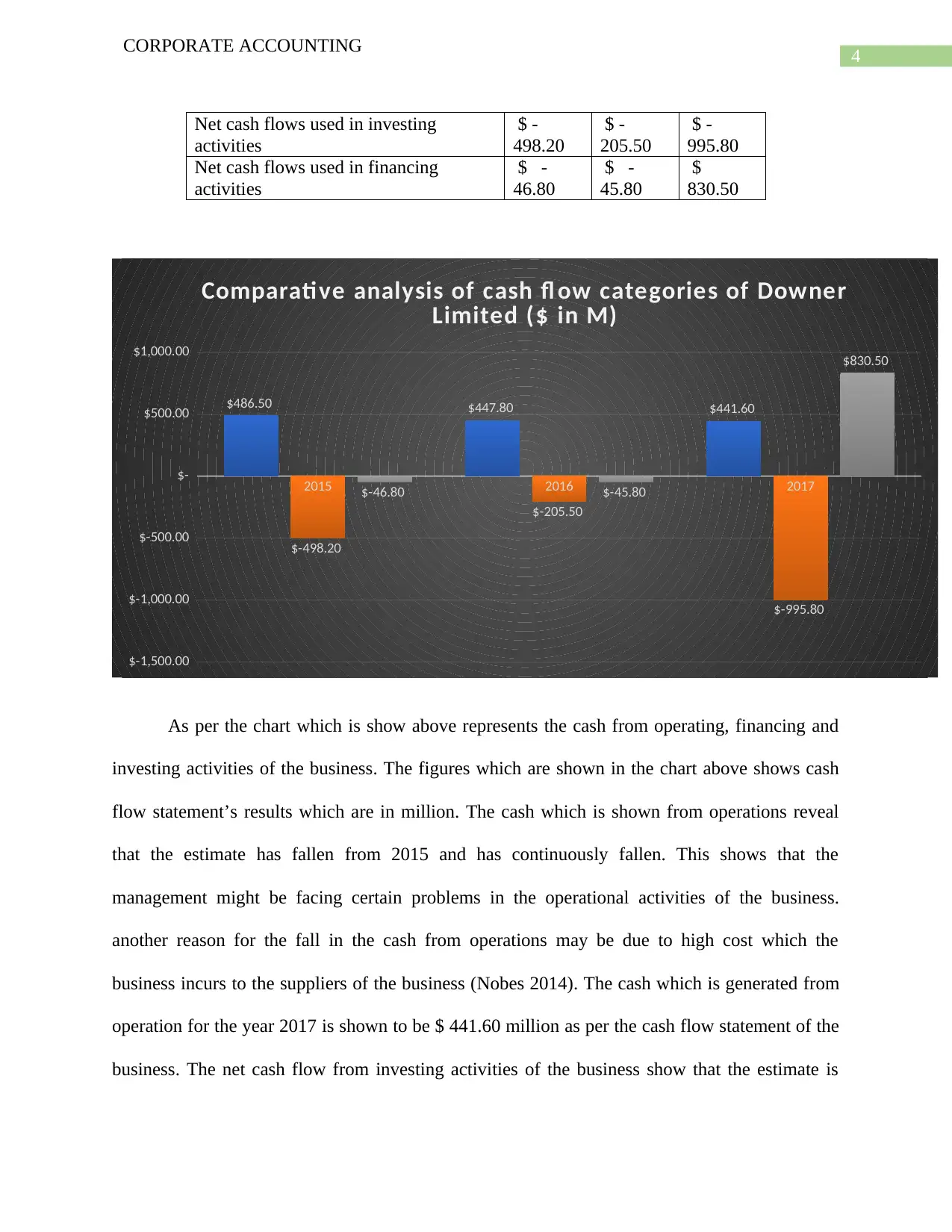

Net cash flows used in investing

activities

$ -

498.20

$ -

205.50

$ -

995.80

Net cash flows used in financing

activities

$ -

46.80

$ -

45.80

$

830.50

2015 2016 2017

$-1,500.00

$-1,000.00

$-500.00

$-

$500.00

$1,000.00

$486.50 $447.80 $441.60

$-498.20

$-205.50

$-995.80

$-46.80 $-45.80

$830.50

Comparative analysis of cash fl ow categories of Downer

Limited ($ in M)

As per the chart which is show above represents the cash from operating, financing and

investing activities of the business. The figures which are shown in the chart above shows cash

flow statement’s results which are in million. The cash which is shown from operations reveal

that the estimate has fallen from 2015 and has continuously fallen. This shows that the

management might be facing certain problems in the operational activities of the business.

another reason for the fall in the cash from operations may be due to high cost which the

business incurs to the suppliers of the business (Nobes 2014). The cash which is generated from

operation for the year 2017 is shown to be $ 441.60 million as per the cash flow statement of the

business. The net cash flow from investing activities of the business show that the estimate is

CORPORATE ACCOUNTING

Net cash flows used in investing

activities

$ -

498.20

$ -

205.50

$ -

995.80

Net cash flows used in financing

activities

$ -

46.80

$ -

45.80

$

830.50

2015 2016 2017

$-1,500.00

$-1,000.00

$-500.00

$-

$500.00

$1,000.00

$486.50 $447.80 $441.60

$-498.20

$-205.50

$-995.80

$-46.80 $-45.80

$830.50

Comparative analysis of cash fl ow categories of Downer

Limited ($ in M)

As per the chart which is show above represents the cash from operating, financing and

investing activities of the business. The figures which are shown in the chart above shows cash

flow statement’s results which are in million. The cash which is shown from operations reveal

that the estimate has fallen from 2015 and has continuously fallen. This shows that the

management might be facing certain problems in the operational activities of the business.

another reason for the fall in the cash from operations may be due to high cost which the

business incurs to the suppliers of the business (Nobes 2014). The cash which is generated from

operation for the year 2017 is shown to be $ 441.60 million as per the cash flow statement of the

business. The net cash flow from investing activities of the business show that the estimate is

5

CORPORATE ACCOUNTING

highest for the year 2017 where the cash expenses is the most. This can be attributed to the

significant purchases of assets which was made by the company during the year 2017. The

company purchased plant, property, equipment, acquired businesses and acquired intangible

assets for the business. The cash which is generated from the financing activities of the business

has improved significantly in the year 2017 due the capital which is raised by the business which

is of a significant amount of $ 989.9 million as per the cash flow statement of the business

(Mousavi et al. 2013). The company has also paid a significant amount for repayment of debts of

the business and has also declared a dividend of $ 110.6 million for the year 2017 as per the cash

flow statement of Downer ltd.

Other Comprehensive Income Statement

The comprehensive income statement which is shown in the financial statement just

below the profit and loss account, deals with certain items of revenue and expenses which are not

revealed in the profit and loss account and the same is shown as Comprehensive income which is

shown separately from the profit and loss account of the business (Eaton, Easterday and Rhodes

2013). The financial statement of Downer ltd shows that the business has prepared

comprehensive income amount for the various items which are

Items reported as Other Comprehensive Income

As per the profit and loss account of the business which is shown for the year 2017 show

that the various items which are included in the comprehensive income statement are exchange

difference transaction from foreign operations, certain losses which the business incurred,

income tax component of other comprehensive income of the business (Schaberl and Victoravich

2015).

CORPORATE ACCOUNTING

highest for the year 2017 where the cash expenses is the most. This can be attributed to the

significant purchases of assets which was made by the company during the year 2017. The

company purchased plant, property, equipment, acquired businesses and acquired intangible

assets for the business. The cash which is generated from the financing activities of the business

has improved significantly in the year 2017 due the capital which is raised by the business which

is of a significant amount of $ 989.9 million as per the cash flow statement of the business

(Mousavi et al. 2013). The company has also paid a significant amount for repayment of debts of

the business and has also declared a dividend of $ 110.6 million for the year 2017 as per the cash

flow statement of Downer ltd.

Other Comprehensive Income Statement

The comprehensive income statement which is shown in the financial statement just

below the profit and loss account, deals with certain items of revenue and expenses which are not

revealed in the profit and loss account and the same is shown as Comprehensive income which is

shown separately from the profit and loss account of the business (Eaton, Easterday and Rhodes

2013). The financial statement of Downer ltd shows that the business has prepared

comprehensive income amount for the various items which are

Items reported as Other Comprehensive Income

As per the profit and loss account of the business which is shown for the year 2017 show

that the various items which are included in the comprehensive income statement are exchange

difference transaction from foreign operations, certain losses which the business incurred,

income tax component of other comprehensive income of the business (Schaberl and Victoravich

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

Understanding of Items shown under Comprehensive Income

The exchange difference which is shown in the profit and loss account under

comprehensive income is shown because of the change in the value of foreign currency of the

business. This also suggest that the company has engaged in foreign transaction during the year.

There are times when the translation value fluctuates of foreign currency and therefore

businesses tend to get income from such fluctuation which is shown in the comprehensive

income statement (Towbin and Weber 2013). The business of Downer ltd has incurred certain

losses during the year which relates to foreign currency forward contracts and cross currency

transaction which the business had engaged in during the year. Then there is the tax expenses

which is related to the comprehensive income which is applicable to tax. The last two items

which are shown is related to the small amount of change has occurred which is included in the

comprehensive statement.

Reporting of Comprehensive Income

The items of comprehensive income are recorded separately as they are different from

items which are shown in the profit and loss statement of the business. The main purpose of

disclosing the comprehensive items of the business from which the business earns revenue or

incurs expenses so that the users of the financial statements are informed on all matters.

Accounting for Income Tax

Current Tax Expenses

The current income tax expenses which is incurred by the business for the year 2017 is

shown to be $ 69.5 million which has increased from the previous year which is shown to be

CORPORATE ACCOUNTING

Understanding of Items shown under Comprehensive Income

The exchange difference which is shown in the profit and loss account under

comprehensive income is shown because of the change in the value of foreign currency of the

business. This also suggest that the company has engaged in foreign transaction during the year.

There are times when the translation value fluctuates of foreign currency and therefore

businesses tend to get income from such fluctuation which is shown in the comprehensive

income statement (Towbin and Weber 2013). The business of Downer ltd has incurred certain

losses during the year which relates to foreign currency forward contracts and cross currency

transaction which the business had engaged in during the year. Then there is the tax expenses

which is related to the comprehensive income which is applicable to tax. The last two items

which are shown is related to the small amount of change has occurred which is included in the

comprehensive statement.

Reporting of Comprehensive Income

The items of comprehensive income are recorded separately as they are different from

items which are shown in the profit and loss statement of the business. The main purpose of

disclosing the comprehensive items of the business from which the business earns revenue or

incurs expenses so that the users of the financial statements are informed on all matters.

Accounting for Income Tax

Current Tax Expenses

The current income tax expenses which is incurred by the business for the year 2017 is

shown to be $ 69.5 million which has increased from the previous year which is shown to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

63.3 million in the year 2016. The increase in the income tax which the business has to pay is

due to the increase in the level of profits of the business.

Rate of tax charged by the business

The net profit which is generated by Downer ltd for the year 2017 and 2016 is shown as $

181.5 million and $ 180.6 million. These figures reflect the after tax figures of the business and

after the adjustment of the comprehensive income is made the profit which is remaining is for the

owners of the company. The tax expenses which is charged for the year of 2017 is shown to be

69.5 million and the same is shown to be $ 63.3 million as shown in the financial statement of

the business. The tax which is shown in the financial statement is lower than what the actual

expenses should be considering the tax rate is 30%. The difference in the actual tax expenses and

the one which is calculated might be caused due to the presence of deferred tax asset and

liabilities which are set off during the year with the current tax expenses of the business.

Deferred Tax Assets and Liabilities

The deferred tax assets arises when an individual or a company pays tax which is more

than what is due from him and therefore such excessive tax paid becomes the deferred tax assets

of the business, On the other hand, the deferred tax liabilities of the business arises when an

individual or a company has paid less than what is due to the tax authorities of Australia (Laux

2013). The financial statement of Downer ltd reveals that the company has deferred tax asset

which is shown to be $ 59.4 million in 2017. The deferred tax assets have just been recognized as

it is not shown in 2016 which suggest that the company has paid tax in excess which is the

reason for the deferred tax assets as shown in the balance sheet of the company. It is a known

CORPORATE ACCOUNTING

63.3 million in the year 2016. The increase in the income tax which the business has to pay is

due to the increase in the level of profits of the business.

Rate of tax charged by the business

The net profit which is generated by Downer ltd for the year 2017 and 2016 is shown as $

181.5 million and $ 180.6 million. These figures reflect the after tax figures of the business and

after the adjustment of the comprehensive income is made the profit which is remaining is for the

owners of the company. The tax expenses which is charged for the year of 2017 is shown to be

69.5 million and the same is shown to be $ 63.3 million as shown in the financial statement of

the business. The tax which is shown in the financial statement is lower than what the actual

expenses should be considering the tax rate is 30%. The difference in the actual tax expenses and

the one which is calculated might be caused due to the presence of deferred tax asset and

liabilities which are set off during the year with the current tax expenses of the business.

Deferred Tax Assets and Liabilities

The deferred tax assets arises when an individual or a company pays tax which is more

than what is due from him and therefore such excessive tax paid becomes the deferred tax assets

of the business, On the other hand, the deferred tax liabilities of the business arises when an

individual or a company has paid less than what is due to the tax authorities of Australia (Laux

2013). The financial statement of Downer ltd reveals that the company has deferred tax asset

which is shown to be $ 59.4 million in 2017. The deferred tax assets have just been recognized as

it is not shown in 2016 which suggest that the company has paid tax in excess which is the

reason for the deferred tax assets as shown in the balance sheet of the company. It is a known

8

CORPORATE ACCOUNTING

fact that deferred tax assets and liabilities arise due to temporary difference between items which

are on different balance sheet date (Dhaliwal et al 2013).

The deferred tax assets and liabilities are carried forward by the business from year to

year so that the business can set them off in the future years. In the case of deferred tax asset

which is shown in the financial statement of Downer ltd is the one which is newly created.

Current Tax Assets and Liabilities

The balance sheet which is prepared by the management of Downer ltd shows that

Downer ltd has current tax liabilities shown in the current liabilities section and current tax assets

which is shown in current asset section. The system of accounting records transaction on accrual

basis and thus the income tax which is payable is shown as current liabilities of the business. The

current tax liability of the business which is shown to be $ 7.2 million which has increased from

the previous year. The current tax assets of the business is shown to be $ 45.5 million for the

current year.

Difference in Income tax expenses and Income Tax paid.

The income tax expenses which is shown in the income statement of the business is

different from the actual income tax paid which is shown in the cash flow statement of the

business. The actual expenses which is paid in the cash flow statement is $ 49 million and the

same is measured in the profit and loss account as $ 69.5 million. The difference can be due to

full tax is not paid to the tax authority or tax which is pending and being carried forward is added

to the teax figure for the current year.

CORPORATE ACCOUNTING

fact that deferred tax assets and liabilities arise due to temporary difference between items which

are on different balance sheet date (Dhaliwal et al 2013).

The deferred tax assets and liabilities are carried forward by the business from year to

year so that the business can set them off in the future years. In the case of deferred tax asset

which is shown in the financial statement of Downer ltd is the one which is newly created.

Current Tax Assets and Liabilities

The balance sheet which is prepared by the management of Downer ltd shows that

Downer ltd has current tax liabilities shown in the current liabilities section and current tax assets

which is shown in current asset section. The system of accounting records transaction on accrual

basis and thus the income tax which is payable is shown as current liabilities of the business. The

current tax liability of the business which is shown to be $ 7.2 million which has increased from

the previous year. The current tax assets of the business is shown to be $ 45.5 million for the

current year.

Difference in Income tax expenses and Income Tax paid.

The income tax expenses which is shown in the income statement of the business is

different from the actual income tax paid which is shown in the cash flow statement of the

business. The actual expenses which is paid in the cash flow statement is $ 49 million and the

same is measured in the profit and loss account as $ 69.5 million. The difference can be due to

full tax is not paid to the tax authority or tax which is pending and being carried forward is added

to the teax figure for the current year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Review of the Tax policy of the business.

The analysis of the financial statement of Downer ltd shows that the business has

prepared the financial statements as per the rules and regulations which are applicable in

Australia. The financial statements of the business reveal that the company has deferred tax

assets as well as current tax assets and current tax liabilities which are shown in the balance sheet

of the business. The treatment of tax and all the disclosures relating to the same is appropriately

shown in the financial statement of the business.

CORPORATE ACCOUNTING

Review of the Tax policy of the business.

The analysis of the financial statement of Downer ltd shows that the business has

prepared the financial statements as per the rules and regulations which are applicable in

Australia. The financial statements of the business reveal that the company has deferred tax

assets as well as current tax assets and current tax liabilities which are shown in the balance sheet

of the business. The treatment of tax and all the disclosures relating to the same is appropriately

shown in the financial statement of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Reference

Call, A.C., Chen, S. and Tong, Y.H., 2013. Are analysts' cash flow forecasts naïve extensions of

their own earnings forecasts?. Contemporary Accounting Research, 30(2), pp.438-465.

Dhaliwal, D.S., Kaplan, S.E., Laux, R.C. and Weisbrod, E., 2013. The information content of tax

expense for firms reporting losses. Journal of Accounting Research, 51(1), pp.135-164.

Downer Corporate Site. (2018). Downer Group. [online] Available at:

https://www.downergroup.com [Accessed 22 May 2018].

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Kaspina, R.G., Molotov, L.A. and Kaspin, L.E., 2015. Cash flow forecasting as an element of

integrated reporting: an empirical study. Asian social science, 11(11), p.89.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Mousavi, S.M., Hajipour, V., Niaki, S.T.A. and Alikar, N., 2013. Optimizing multi-item multi-

period inventory control system with discounted cash flow and inflation: two calibrated meta-

heuristic algorithms. Applied Mathematical Modelling, 37(4), pp.2241-2256.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Schaberl, P.D. and Victoravich, L.M., 2015. Reporting location and the value relevance of

accounting information: The case of other comprehensive income. Advances in

Accounting, 31(2), pp.239-246.

CORPORATE ACCOUNTING

Reference

Call, A.C., Chen, S. and Tong, Y.H., 2013. Are analysts' cash flow forecasts naïve extensions of

their own earnings forecasts?. Contemporary Accounting Research, 30(2), pp.438-465.

Dhaliwal, D.S., Kaplan, S.E., Laux, R.C. and Weisbrod, E., 2013. The information content of tax

expense for firms reporting losses. Journal of Accounting Research, 51(1), pp.135-164.

Downer Corporate Site. (2018). Downer Group. [online] Available at:

https://www.downergroup.com [Accessed 22 May 2018].

Eaton, T.V., Easterday, K.E. and Rhodes, M.R., 2013. The presentation of other comprehensive

income. The CPA Journal, 83(3), p.32.

Kaspina, R.G., Molotov, L.A. and Kaspin, L.E., 2015. Cash flow forecasting as an element of

integrated reporting: an empirical study. Asian social science, 11(11), p.89.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Mousavi, S.M., Hajipour, V., Niaki, S.T.A. and Alikar, N., 2013. Optimizing multi-item multi-

period inventory control system with discounted cash flow and inflation: two calibrated meta-

heuristic algorithms. Applied Mathematical Modelling, 37(4), pp.2241-2256.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Schaberl, P.D. and Victoravich, L.M., 2015. Reporting location and the value relevance of

accounting information: The case of other comprehensive income. Advances in

Accounting, 31(2), pp.239-246.

11

CORPORATE ACCOUNTING

Stevanović, S., Belopavlović, G. and Lazarević-Moravčević, M., 2017. Creative Cash Flow

Reporting–the Motivation and Opportunities. Economic analysis, 46(1-2), pp.28-39.

Towbin, P. and Weber, S., 2013. Limits of floating exchange rates: The role of foreign currency

debt and import structure. Journal of Development Economics, 101, pp.179-194.

CORPORATE ACCOUNTING

Stevanović, S., Belopavlović, G. and Lazarević-Moravčević, M., 2017. Creative Cash Flow

Reporting–the Motivation and Opportunities. Economic analysis, 46(1-2), pp.28-39.

Towbin, P. and Weber, S., 2013. Limits of floating exchange rates: The role of foreign currency

debt and import structure. Journal of Development Economics, 101, pp.179-194.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.