Management Accounting Report: Costing, Planning, and Integration

VerifiedAdded on 2020/10/22

|19

|5425

|405

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and techniques. It begins with an introduction to management accounting, its requirements, and various types such as inventory management and job costing. Task 1 explores the types and importance of management accounting reports, including cost, performance, and budget reports, along with the merits of job costing and inventory management systems. It also examines the integration of management accounting systems and reporting within an organization. Task 2 delves into costing methods, explaining absorption and marginal costing, preparing income statements using both methods, and analyzing break-even points. Task 3 focuses on planning tools, including budgetary control, and their application in analysis, forecasting, and problem-solving. The report compares different management accounting systems, evaluates techniques for financial problems, and identifies planning tools for financial solutions, culminating in a conclusion and references.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

B. Types of management accounting report with its importance................................................5

C. Merits of job costing and inventory management system along with its application............6

D. Integration of management accounting system and report in organisation............................7

TASK 2............................................................................................................................................8

A.1 Explaining absorption and marginal costing........................................................................8

A.2 Preparation of income statement by both methods............................................................10

B Applicability of formula of Break Even................................................................................11

C. Significance of task 2...........................................................................................................12

D. Interpretation of task 2.........................................................................................................13

TASK 3..........................................................................................................................................14

A. Merits and demerits of planning tools with context of budgetary control...........................14

B. Application of planning tool for analysing, forecasting and preparing................................15

C. Comparing methods of management accounting system in context of financial problem...15

D. Evaluating management accounting techniques for financial problems..............................16

E. Identifying planning tools which can be used for solving financial problems.....................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

B. Types of management accounting report with its importance................................................5

C. Merits of job costing and inventory management system along with its application............6

D. Integration of management accounting system and report in organisation............................7

TASK 2............................................................................................................................................8

A.1 Explaining absorption and marginal costing........................................................................8

A.2 Preparation of income statement by both methods............................................................10

B Applicability of formula of Break Even................................................................................11

C. Significance of task 2...........................................................................................................12

D. Interpretation of task 2.........................................................................................................13

TASK 3..........................................................................................................................................14

A. Merits and demerits of planning tools with context of budgetary control...........................14

B. Application of planning tool for analysing, forecasting and preparing................................15

C. Comparing methods of management accounting system in context of financial problem...15

D. Evaluating management accounting techniques for financial problems..............................16

E. Identifying planning tools which can be used for solving financial problems.....................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is considered as most important aspect for any organization or

industry whether it is small or big. Whole report is classified in three tasks which is signifying

importance of different management system and techniques. The present report is giving brief

understanding about different system of management accounting techniques which are adopted

by Ovation system who is one of SME. As it operating with 23 employees but in proper

condition. It will be discussing about various requirements along with its types. There is presence

of understanding on different reports such as performance report and many more than how they

are impacting organization with its significance. There is representation on importance of

integrated management accounting system in Ovation system. In next task it is reflecting

importance of various costing methods such as marginal and absorption costing method along

with income statement. There has been presentation of introducing new product which has been

analysed by Break even and margin of safety with its significance and importance. In the last

part it is replicating importance of different kinds of planning tool in context of budgetary

control along with its examples. It has also reflected its application, merits and demerits which

can be applied. It has also specified comparison on adopting different management accounting

system and problems with its solutions which lead to sustainable success of organization.

TASK 1

A. Defining management accounting with its requirement along with its types

Management accounting replicates information in context of accounting information for

formulating policies which has to be adopted through management and it must be able to assist

its daily routine activities. It is used by management for performing its various functions such as

controlling, planning, organising, staffing and directing. Management accounting is very

important to any organization as it increases the level of efficiency as its main advantages are in

given series below:

It helps in identifying objectives on the basis of specific information which is already

given.

It has huge contribution in preparing plan with appropriate analysis.

It helps in providing better services to customer by proper control device of control as ut

decreases price of product.

Management accounting is considered as most important aspect for any organization or

industry whether it is small or big. Whole report is classified in three tasks which is signifying

importance of different management system and techniques. The present report is giving brief

understanding about different system of management accounting techniques which are adopted

by Ovation system who is one of SME. As it operating with 23 employees but in proper

condition. It will be discussing about various requirements along with its types. There is presence

of understanding on different reports such as performance report and many more than how they

are impacting organization with its significance. There is representation on importance of

integrated management accounting system in Ovation system. In next task it is reflecting

importance of various costing methods such as marginal and absorption costing method along

with income statement. There has been presentation of introducing new product which has been

analysed by Break even and margin of safety with its significance and importance. In the last

part it is replicating importance of different kinds of planning tool in context of budgetary

control along with its examples. It has also reflected its application, merits and demerits which

can be applied. It has also specified comparison on adopting different management accounting

system and problems with its solutions which lead to sustainable success of organization.

TASK 1

A. Defining management accounting with its requirement along with its types

Management accounting replicates information in context of accounting information for

formulating policies which has to be adopted through management and it must be able to assist

its daily routine activities. It is used by management for performing its various functions such as

controlling, planning, organising, staffing and directing. Management accounting is very

important to any organization as it increases the level of efficiency as its main advantages are in

given series below:

It helps in identifying objectives on the basis of specific information which is already

given.

It has huge contribution in preparing plan with appropriate analysis.

It helps in providing better services to customer by proper control device of control as ut

decreases price of product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It provides ease in providing judgement for identifying policy.

There is presence of different budgetary techniques which enables measurement of

performance.

Efficiency of business has been increased by management accounting.

Effective management control has been given by management accounting.

There are various types of management accounting system which are elaborated as

below:

Inventory management: It is used for keeping record of various application, orders and

its component of its production of goods. It usually manages inventory and stock of Ovation

system. There is presence of various element of supply chain management and inventory

management consists of controlling and observing the orders of inventory along with its storage

and amount has been controlled with amount of sale of product. In the present scenario, Ovation

system is an electronic manufacturer organization so in this it manages inventory of its raw

materials such as cables, barcode printers and different video surveillance equipment (Zhao, Liu,

Zhang and Huang, 2017).

Job costing system: It is replicated as system which is used for assigning different cost

of manufacturing to a specific individual product or different batches of product. It has its main

application during products are manufactured and they vary from each other.

B. Types of management accounting report with its importance

Ovation system is a SME but for reviewing performance for each employee and

organization it uses different reports such as:

Cost report: In management accounting, manufacturing of any single item has been

calculated which includes labour, raw production overheads and any other cost which is

used and its sum is distributed into production of goods. The formation of each product of

Ovation system is briefed in this specific report. All items cost price has been compared

to its selling price which has been given by manager. The profit margin has been

estimated and monitored in this cost managerial accounting report. There is presence of

optimum utilisation of resources of each department as this report clearly depicts its

original picture.

Performance report: The main objective of this report is to monitor performance of

ovation system. Huge turnover has been generated by big organizations so in these

There is presence of different budgetary techniques which enables measurement of

performance.

Efficiency of business has been increased by management accounting.

Effective management control has been given by management accounting.

There are various types of management accounting system which are elaborated as

below:

Inventory management: It is used for keeping record of various application, orders and

its component of its production of goods. It usually manages inventory and stock of Ovation

system. There is presence of various element of supply chain management and inventory

management consists of controlling and observing the orders of inventory along with its storage

and amount has been controlled with amount of sale of product. In the present scenario, Ovation

system is an electronic manufacturer organization so in this it manages inventory of its raw

materials such as cables, barcode printers and different video surveillance equipment (Zhao, Liu,

Zhang and Huang, 2017).

Job costing system: It is replicated as system which is used for assigning different cost

of manufacturing to a specific individual product or different batches of product. It has its main

application during products are manufactured and they vary from each other.

B. Types of management accounting report with its importance

Ovation system is a SME but for reviewing performance for each employee and

organization it uses different reports such as:

Cost report: In management accounting, manufacturing of any single item has been

calculated which includes labour, raw production overheads and any other cost which is

used and its sum is distributed into production of goods. The formation of each product of

Ovation system is briefed in this specific report. All items cost price has been compared

to its selling price which has been given by manager. The profit margin has been

estimated and monitored in this cost managerial accounting report. There is presence of

optimum utilisation of resources of each department as this report clearly depicts its

original picture.

Performance report: The main objective of this report is to monitor performance of

ovation system. Huge turnover has been generated by big organizations so in these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

departments, it is framed as department wise. The performance has been observed by

accountants in context of expected outcome or any other differences which should be

rectified. At every year end, there is preparation of performance report and it has

originally quantified financial information for performance report. It plays essential

contribution in perspective of strategic decision making. It provides deep insights in

context of operation of organization's performance.

Budget report: It is considered as most fundamental report in context of management

accounting. Usually every organization prepares this report as it gives proper

understanding of schemes which are useful (Hu, Martinez and Yang, 2017). The budget

has been set by considering previous year as base as it alters different forecast for

circumstances which might arise in the future. The budget of Ovation system provides

gives all sources of revenue and expenses. The accomplishment of objective in specific

budgeted amount, all efforts are practice by Ovation system. It keeps record of alteration

in expenses and sales and it also helps in setting incentives of employees, negotiation of

raw material and reducing cost.

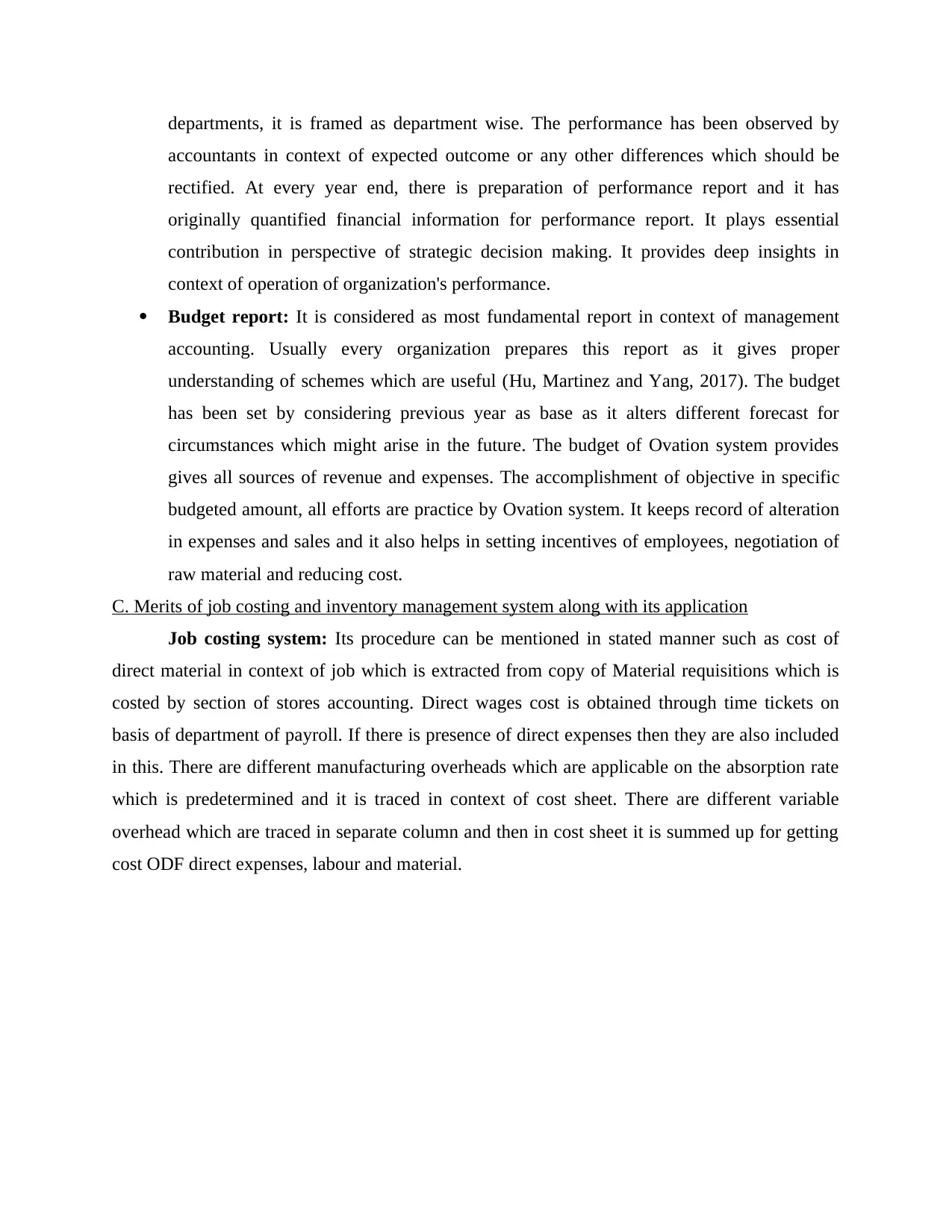

C. Merits of job costing and inventory management system along with its application

Job costing system: Its procedure can be mentioned in stated manner such as cost of

direct material in context of job which is extracted from copy of Material requisitions which is

costed by section of stores accounting. Direct wages cost is obtained through time tickets on

basis of department of payroll. If there is presence of direct expenses then they are also included

in this. There are different manufacturing overheads which are applicable on the absorption rate

which is predetermined and it is traced in context of cost sheet. There are different variable

overhead which are traced in separate column and then in cost sheet it is summed up for getting

cost ODF direct expenses, labour and material.

accountants in context of expected outcome or any other differences which should be

rectified. At every year end, there is preparation of performance report and it has

originally quantified financial information for performance report. It plays essential

contribution in perspective of strategic decision making. It provides deep insights in

context of operation of organization's performance.

Budget report: It is considered as most fundamental report in context of management

accounting. Usually every organization prepares this report as it gives proper

understanding of schemes which are useful (Hu, Martinez and Yang, 2017). The budget

has been set by considering previous year as base as it alters different forecast for

circumstances which might arise in the future. The budget of Ovation system provides

gives all sources of revenue and expenses. The accomplishment of objective in specific

budgeted amount, all efforts are practice by Ovation system. It keeps record of alteration

in expenses and sales and it also helps in setting incentives of employees, negotiation of

raw material and reducing cost.

C. Merits of job costing and inventory management system along with its application

Job costing system: Its procedure can be mentioned in stated manner such as cost of

direct material in context of job which is extracted from copy of Material requisitions which is

costed by section of stores accounting. Direct wages cost is obtained through time tickets on

basis of department of payroll. If there is presence of direct expenses then they are also included

in this. There are different manufacturing overheads which are applicable on the absorption rate

which is predetermined and it is traced in context of cost sheet. There are different variable

overhead which are traced in separate column and then in cost sheet it is summed up for getting

cost ODF direct expenses, labour and material.

Illustration 1: Specimen of job cost sheet

Advantages

It determines profitability of every job.

It gives an appropriate basis for identifying cost of jobs which are similar and to be

undertaken in the future.

Detailed analysis has been provided by cost of labour, material and overheads of every

job whenever it is required.

The efficiency of plant cab be maintained and controlled by giving specific attention to

cost in context of individual job.

It is considered as most essential for contract of cost plus where price of contract is

identified directly on specific cost basis.

Advantages

It determines profitability of every job.

It gives an appropriate basis for identifying cost of jobs which are similar and to be

undertaken in the future.

Detailed analysis has been provided by cost of labour, material and overheads of every

job whenever it is required.

The efficiency of plant cab be maintained and controlled by giving specific attention to

cost in context of individual job.

It is considered as most essential for contract of cost plus where price of contract is

identified directly on specific cost basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management: It is considered as most necessary aspect of business as it

includes both retail and manufacturing facilities. In ovation system it maintains proper inventory

level as it is determined as most crucial factor because it could be very expensive. The flow of

merchandise which is incoming and outgoing has been balanced and controlled by inventory

management system. The strong management inventory system gives advantages to many

organisations due to:

Presence of adequate supply and demand of specific product for fulfilling customer

requirements. As it increases both sales and customer service.

Inventory of supply must be maintained by manufacturing facilities as it is very vital for

production of their specific products.

It is considered as very important management system as it identifies the time for

maintaining order at certain times and especially for items which vary lead times.

One of the most significant benefit is that it decreases liabilities and loss which has been

created by overstock (Hu, Martinez and Yang, 2017).

D. Integration of management accounting system and report in organisation

The integration of management accounting system reporting and system in process of

organization is termed as integrated management accounting system. It benefits organization in

various aspects such as:

If only one set of account has been maintained in this system then it will state only one

profit figure as its necessity of preparing statement of reconciliation will not arise for

Ovation system.

If only one account will be maintained then it will reduce chances of duplication of

efforts and time and cost which is also saved.

Information will be not delayed by records of accounting for purpose of costing and

finance.

If its operation will be in computerized format and accounting which is mechanized then

it will be a huge advantage to organization (Cooper, Ezzamel and Qu, 2017).

If cost and financial accounts are integrated then accounting and information both will be

centralized if there are possibilities as it saves expense and time as well.

The procedure of accounting is simplified as it helps in controlling operations in effective

manner.

includes both retail and manufacturing facilities. In ovation system it maintains proper inventory

level as it is determined as most crucial factor because it could be very expensive. The flow of

merchandise which is incoming and outgoing has been balanced and controlled by inventory

management system. The strong management inventory system gives advantages to many

organisations due to:

Presence of adequate supply and demand of specific product for fulfilling customer

requirements. As it increases both sales and customer service.

Inventory of supply must be maintained by manufacturing facilities as it is very vital for

production of their specific products.

It is considered as very important management system as it identifies the time for

maintaining order at certain times and especially for items which vary lead times.

One of the most significant benefit is that it decreases liabilities and loss which has been

created by overstock (Hu, Martinez and Yang, 2017).

D. Integration of management accounting system and report in organisation

The integration of management accounting system reporting and system in process of

organization is termed as integrated management accounting system. It benefits organization in

various aspects such as:

If only one set of account has been maintained in this system then it will state only one

profit figure as its necessity of preparing statement of reconciliation will not arise for

Ovation system.

If only one account will be maintained then it will reduce chances of duplication of

efforts and time and cost which is also saved.

Information will be not delayed by records of accounting for purpose of costing and

finance.

If its operation will be in computerized format and accounting which is mechanized then

it will be a huge advantage to organization (Cooper, Ezzamel and Qu, 2017).

If cost and financial accounts are integrated then accounting and information both will be

centralized if there are possibilities as it saves expense and time as well.

The procedure of accounting is simplified as it helps in controlling operations in effective

manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The information related to costing can be generated from original entry of books as it

avoids delay in getting information.

Whole information is furnished in context of cost of every item, operation or job and it

also highlights differences for purpose of effective control.

All information about profit and loss will be provided of full organization and it will be

indicating financial position will be helping management for better control on its specific

operations.

It will directly ensures pertainment of marginal cost, abnormal loss and gains and along

with its variations.

TASK 2

A.1 Explaining absorption and marginal costing

Absorption costing: It is a costing system which has its applicability in valuing

inventory. It absorbs all expense related to manufacturing of any specific product which consist

of both fixed and variable cost. All the expense which are direct such as material cost and in this

series indirect cost such as overhead expense are considered as inventory's price. It provides very

accurate and comprehensive view on amount which is actually produced inventory and then

method for variable costing (Absorption Costing. 2018). It is also replicated as full costing.

There is brief explanation about elements of absorption costing such as:

Direct material

direct labour

Fixed manufacturing overhead

Variable manufacturing overhead

The cost which is considered under this method as it does not include in specific cost of product

such as:

Variable selling and administrative

Fixed administrative and selling

avoids delay in getting information.

Whole information is furnished in context of cost of every item, operation or job and it

also highlights differences for purpose of effective control.

All information about profit and loss will be provided of full organization and it will be

indicating financial position will be helping management for better control on its specific

operations.

It will directly ensures pertainment of marginal cost, abnormal loss and gains and along

with its variations.

TASK 2

A.1 Explaining absorption and marginal costing

Absorption costing: It is a costing system which has its applicability in valuing

inventory. It absorbs all expense related to manufacturing of any specific product which consist

of both fixed and variable cost. All the expense which are direct such as material cost and in this

series indirect cost such as overhead expense are considered as inventory's price. It provides very

accurate and comprehensive view on amount which is actually produced inventory and then

method for variable costing (Absorption Costing. 2018). It is also replicated as full costing.

There is brief explanation about elements of absorption costing such as:

Direct material

direct labour

Fixed manufacturing overhead

Variable manufacturing overhead

The cost which is considered under this method as it does not include in specific cost of product

such as:

Variable selling and administrative

Fixed administrative and selling

Illustration 2: Overview of cost

(Source: Absorption Costing, 2018)

Marginal costing: Under this method all variable expense are included in costs unit and

fixed cost which is directly attributed to specific period which is written off in full as not in

favour of specific contribution of that mentioned period. It pertains marginal expense and its

impact on alterations of profit in context of volume or outcome by creating variation in fixed and

variable expense. Usually cost are classified in both variable and fixed costs.

Illustration 3: Approaches of marginal costing

(Source: Marginal costing, 2018)

(Source: Absorption Costing, 2018)

Marginal costing: Under this method all variable expense are included in costs unit and

fixed cost which is directly attributed to specific period which is written off in full as not in

favour of specific contribution of that mentioned period. It pertains marginal expense and its

impact on alterations of profit in context of volume or outcome by creating variation in fixed and

variable expense. Usually cost are classified in both variable and fixed costs.

Illustration 3: Approaches of marginal costing

(Source: Marginal costing, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is directly on basis of cost behaviour which varies from volume according to volume of

result. It is also replicated as variable costs which is directly accumulated along with per unit of

cost while pertaining with variable cost. The marginal and direct costing is specified as

interchangeable terms mostly (Marginal costing. 2018). The key difference between them is that

expenses which are determined as variable nature is covered in marginal cost and cost which is

fixed in nature is justified as objective of cost.

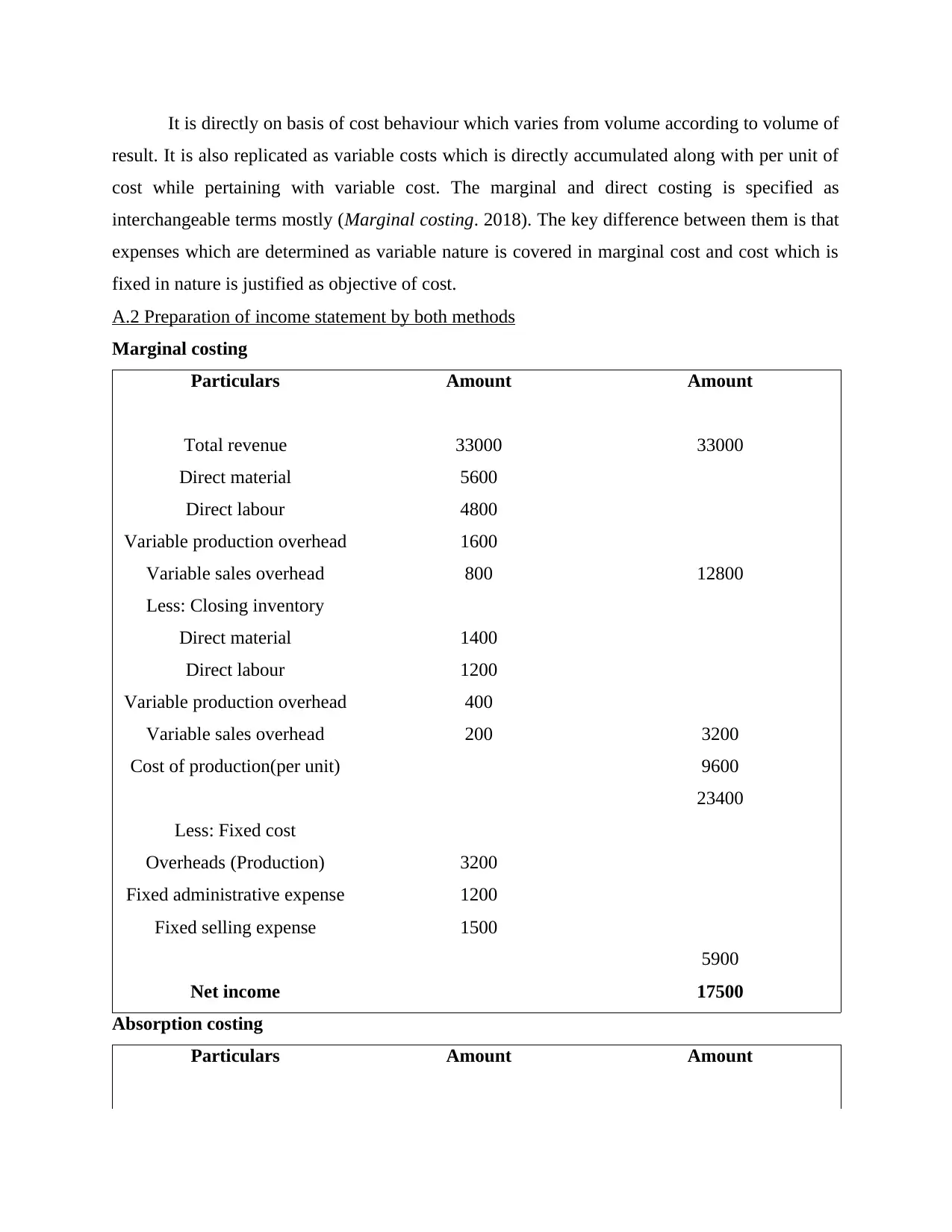

A.2 Preparation of income statement by both methods

Marginal costing

Particulars Amount Amount

Total revenue 33000 33000

Direct material 5600

Direct labour 4800

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable production overhead 400

Variable sales overhead 200 3200

Cost of production(per unit) 9600

23400

Less: Fixed cost

Overheads (Production) 3200

Fixed administrative expense 1200

Fixed selling expense 1500

5900

Net income 17500

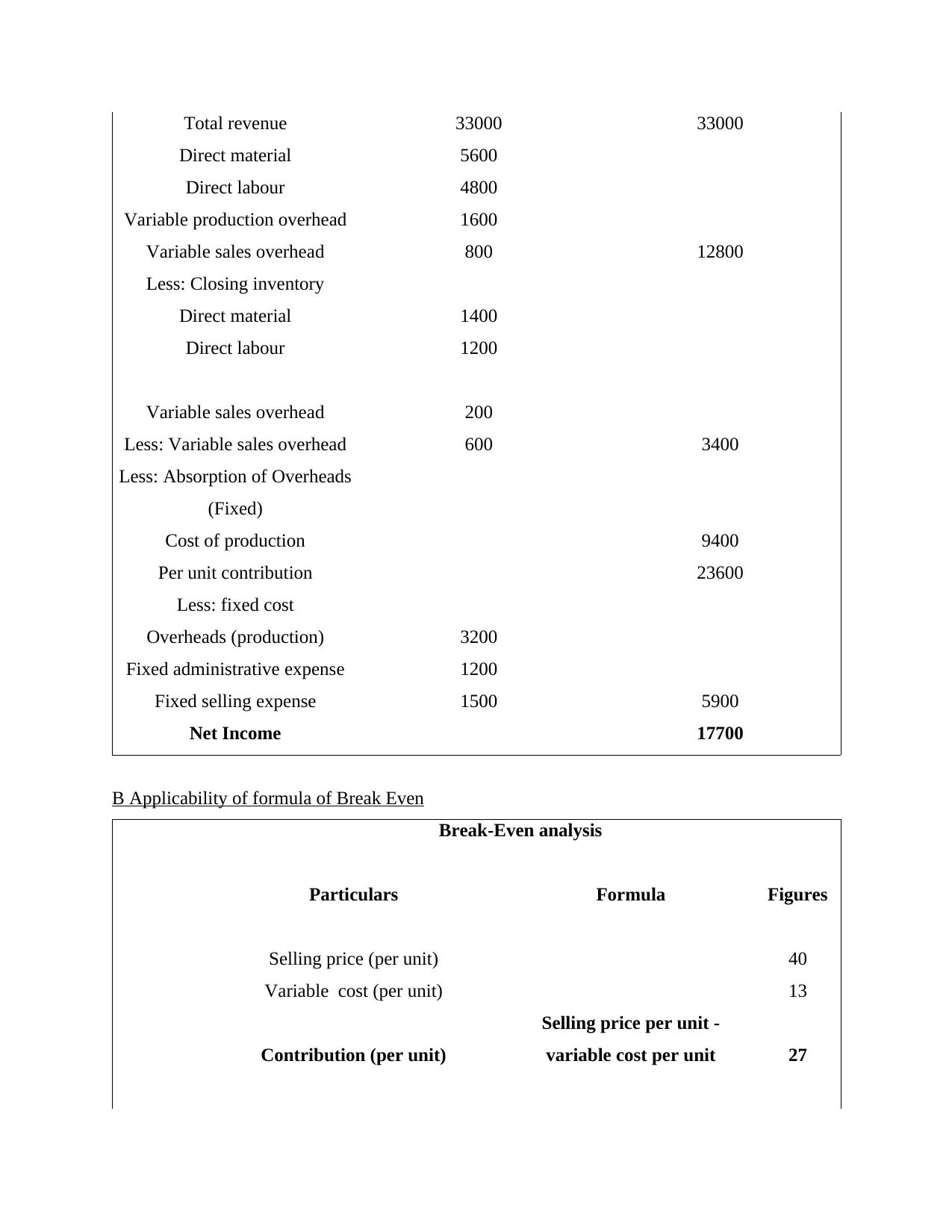

Absorption costing

Particulars Amount Amount

result. It is also replicated as variable costs which is directly accumulated along with per unit of

cost while pertaining with variable cost. The marginal and direct costing is specified as

interchangeable terms mostly (Marginal costing. 2018). The key difference between them is that

expenses which are determined as variable nature is covered in marginal cost and cost which is

fixed in nature is justified as objective of cost.

A.2 Preparation of income statement by both methods

Marginal costing

Particulars Amount Amount

Total revenue 33000 33000

Direct material 5600

Direct labour 4800

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable production overhead 400

Variable sales overhead 200 3200

Cost of production(per unit) 9600

23400

Less: Fixed cost

Overheads (Production) 3200

Fixed administrative expense 1200

Fixed selling expense 1500

5900

Net income 17500

Absorption costing

Particulars Amount Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total revenue 33000 33000

Direct material 5600

Direct labour 4800

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable sales overhead 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative expense 1200

Fixed selling expense 1500 5900

Net Income 17700

B Applicability of formula of Break Even

Break-Even analysis

Particulars Formula Figures

Selling price (per unit) 40

Variable cost (per unit) 13

Contribution (per unit)

Selling price per unit -

variable cost per unit 27

Direct material 5600

Direct labour 4800

Variable production overhead 1600

Variable sales overhead 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable sales overhead 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative expense 1200

Fixed selling expense 1500 5900

Net Income 17700

B Applicability of formula of Break Even

Break-Even analysis

Particulars Formula Figures

Selling price (per unit) 40

Variable cost (per unit) 13

Contribution (per unit)

Selling price per unit -

variable cost per unit 27

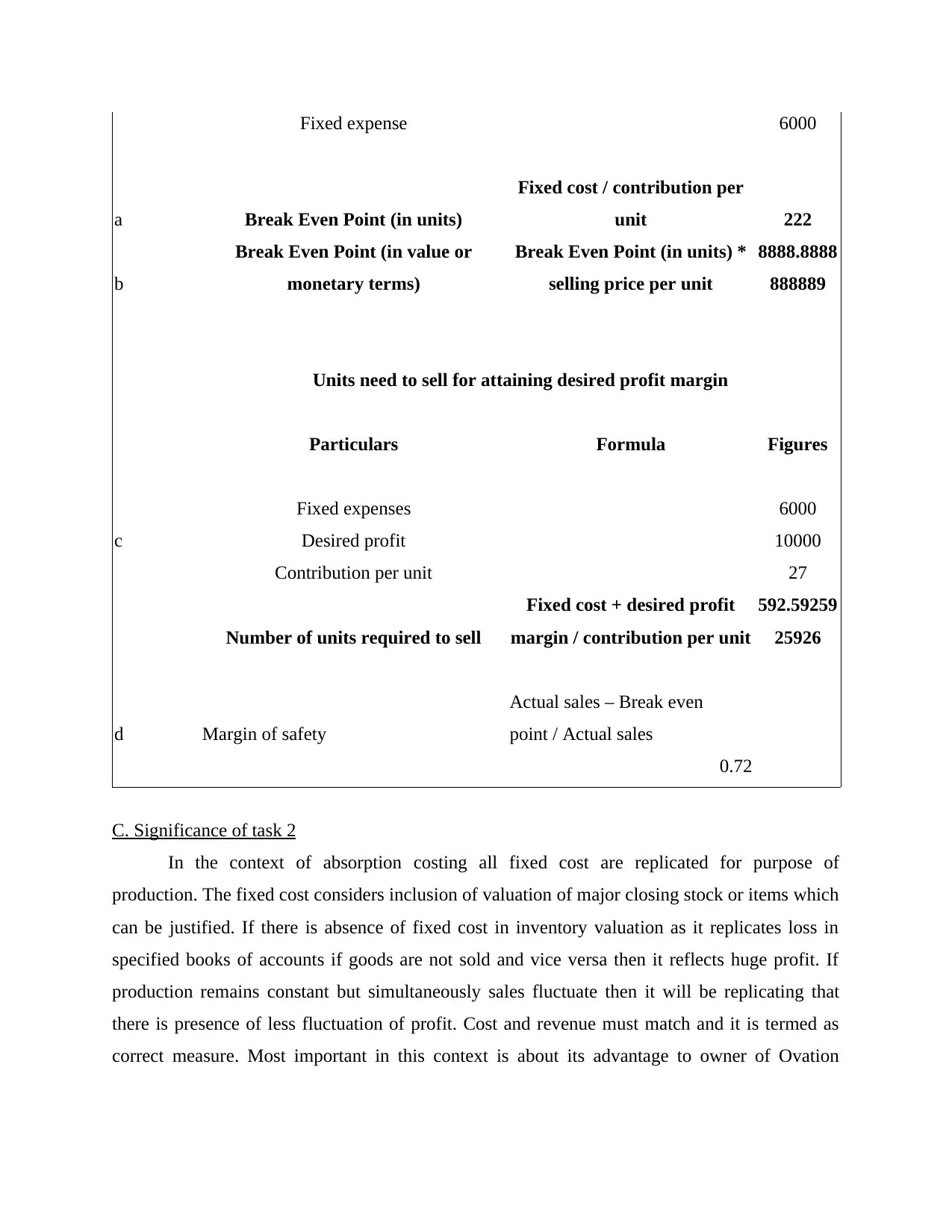

Fixed expense 6000

a Break Even Point (in units)

Fixed cost / contribution per

unit 222

b

Break Even Point (in value or

monetary terms)

Break Even Point (in units) *

selling price per unit

8888.8888

888889

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

c Desired profit 10000

Contribution per unit 27

Number of units required to sell

Fixed cost + desired profit

margin / contribution per unit

592.59259

25926

d Margin of safety

Actual sales – Break even

point / Actual sales

0.72

C. Significance of task 2

In the context of absorption costing all fixed cost are replicated for purpose of

production. The fixed cost considers inclusion of valuation of major closing stock or items which

can be justified. If there is absence of fixed cost in inventory valuation as it replicates loss in

specified books of accounts if goods are not sold and vice versa then it reflects huge profit. If

production remains constant but simultaneously sales fluctuate then it will be replicating that

there is presence of less fluctuation of profit. Cost and revenue must match and it is termed as

correct measure. Most important in this context is about its advantage to owner of Ovation

a Break Even Point (in units)

Fixed cost / contribution per

unit 222

b

Break Even Point (in value or

monetary terms)

Break Even Point (in units) *

selling price per unit

8888.8888

888889

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

c Desired profit 10000

Contribution per unit 27

Number of units required to sell

Fixed cost + desired profit

margin / contribution per unit

592.59259

25926

d Margin of safety

Actual sales – Break even

point / Actual sales

0.72

C. Significance of task 2

In the context of absorption costing all fixed cost are replicated for purpose of

production. The fixed cost considers inclusion of valuation of major closing stock or items which

can be justified. If there is absence of fixed cost in inventory valuation as it replicates loss in

specified books of accounts if goods are not sold and vice versa then it reflects huge profit. If

production remains constant but simultaneously sales fluctuate then it will be replicating that

there is presence of less fluctuation of profit. Cost and revenue must match and it is termed as

correct measure. Most important in this context is about its advantage to owner of Ovation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.