Management Accounting Report: Prime Furniture Ltd Financial Strategies

VerifiedAdded on 2021/02/19

|19

|5063

|18

Report

AI Summary

This report delves into the realm of management accounting, focusing on Prime Furniture Ltd. It explores the core concepts of management accounting, encompassing financial, cost, and tax accounting, with practical examples. The report details various methods used in management accounting reporting, including budget reports, job cost reports, and inventory management systems. It also examines the benefits of different accounting systems and the integration of management accounting reporting. The report further analyzes financial statements prepared using both absorption and marginal costing methods, providing interpretations of case studies related to financial planning tools. The report concludes by comparing how organizations adapt management accounting systems to address financial problems, offering a comprehensive overview of the subject matter.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting .....................................................................................1

P2 Explain different methods used for management accounting reporting................................2

M1 Benefits of Management Accounting ..................................................................................7

D1 Integration of management accounting reporting and system..............................................7

P3 Preparation of income statement by using absorption and marginal costing.........................7

D 2 Interpretation of case 1 & 2..................................................................................................9

P 4 Advantage and disadvantage of different planning tools....................................................10

M3 Analysing use of different planning tools...........................................................................12

P5: Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

M4 use of management accounting in resolving financial problems........................................14

D3 Critically analyses of planning tools to resolve financial problems....................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting .....................................................................................1

P2 Explain different methods used for management accounting reporting................................2

M1 Benefits of Management Accounting ..................................................................................7

D1 Integration of management accounting reporting and system..............................................7

P3 Preparation of income statement by using absorption and marginal costing.........................7

D 2 Interpretation of case 1 & 2..................................................................................................9

P 4 Advantage and disadvantage of different planning tools....................................................10

M3 Analysing use of different planning tools...........................................................................12

P5: Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

M4 use of management accounting in resolving financial problems........................................14

D3 Critically analyses of planning tools to resolve financial problems....................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management Accounting is about preparing all the financial reports such as P/L, B/S and

various other reports for disclosures. This report is about Prime Furniture Ltd. which is medium

sized enterprise in the manufacturing sector. It shows the concept of management accounting, its

various methods such as cost accounting, financial accounting, tax accounting with examples.

Furthermore, this study includes various cases and their interpretation which includes marginal

costing and absorption costing, various types of budgets, cash flow forecasting and their

interpretation.

TASK 1

P1 Concept of management accounting

Management Accounting is the process of analysing business costs and operations to

prepare internal financial reports, records, and budget reports, Account Receivable Aging

reports, Cost managerial accounting reports which would help managers to take best decision in

order to achieve business goals of Prime Furniture Ltd (Appelbaum, Kogan and et.al., 2017).

Functions of Management Accounting System -

It provides necessary information and data which helps managers in making short term

and long term goals for the organisation.

It helps the management in organising human and non-human resources for the

organisation.

It helps in controlling the various cost for the organisation through standard cost, budget

costing, Return on Investment etc.

It helps in making analysis on various data available and make interpretation so that

managers could take decision for the organisation.

Types of Management Accounting System are-

1.Financial Accounting

Financial Accounting means to classify, analyse, summarize and record the financial

transactions of the Prime Furniture Ltd. A company is required to record financial transactions as

per accounting rules and procedures which are defined under Accounting Standards and

Principles such as Going Concern, Book Keeping, Dual Accounting System etc. Accounting

Information System is used by company to collect, store, manage, records all the data so it could

1

Management Accounting is about preparing all the financial reports such as P/L, B/S and

various other reports for disclosures. This report is about Prime Furniture Ltd. which is medium

sized enterprise in the manufacturing sector. It shows the concept of management accounting, its

various methods such as cost accounting, financial accounting, tax accounting with examples.

Furthermore, this study includes various cases and their interpretation which includes marginal

costing and absorption costing, various types of budgets, cash flow forecasting and their

interpretation.

TASK 1

P1 Concept of management accounting

Management Accounting is the process of analysing business costs and operations to

prepare internal financial reports, records, and budget reports, Account Receivable Aging

reports, Cost managerial accounting reports which would help managers to take best decision in

order to achieve business goals of Prime Furniture Ltd (Appelbaum, Kogan and et.al., 2017).

Functions of Management Accounting System -

It provides necessary information and data which helps managers in making short term

and long term goals for the organisation.

It helps the management in organising human and non-human resources for the

organisation.

It helps in controlling the various cost for the organisation through standard cost, budget

costing, Return on Investment etc.

It helps in making analysis on various data available and make interpretation so that

managers could take decision for the organisation.

Types of Management Accounting System are-

1.Financial Accounting

Financial Accounting means to classify, analyse, summarize and record the financial

transactions of the Prime Furniture Ltd. A company is required to record financial transactions as

per accounting rules and procedures which are defined under Accounting Standards and

Principles such as Going Concern, Book Keeping, Dual Accounting System etc. Accounting

Information System is used by company to collect, store, manage, records all the data so it could

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

help accountants, investors, auditors, regulators to take the decision from the available data.

Internal Control as defined under auditing means to check the performance on regular basis.

Example – Cash Purchases by Prime Furniture Ltd. of $ 1,00,000

Purchases A/c Dr. $1,00,000

To Cash A/c $1,00,000

2.Cost Accounting

Cost Accounting means classifying, analysing, summarizing and recording all the cost

related to organisation to make the decision so as to control the cost (Weygandt and et.al., 2018).

Cost Accounting includes Product costing and Activity based costing. Product Costing is related

to the prime cost such as direct raw materials are allocated per unit, direct labour is allocated as

per hour, fixed and variable overheads etc. Activity Based Costing is related to the indirect costs

of the company such as setting up machine for production purpose etc. It is basically used in

manufacturing organisation.

Example –

Revenue 100000

-Cost of Goods Sold -25000

=Gross Profit 75000

-Fixed Expenses -25000

-Variable Expenses -15000

=Net Profit 35000

3.Tax Accounting

Tax Accounting is a structure of accounting methods where accounts are made related to

tax rather than for public financial statements. Example of Tax Accounting are for individual

Income Tax is levied, Tax levied on partnerships and corporates is Corporate Tax and on Sales-

Sales Tax or GST is levied.

Example- Prime Furniture Ltd. sold the goods worth $1,000 on which there is 10% tax

Cash / Account Receivable A/C Dr. $1,100

To Sales Revenue A/C $1,000

2

Internal Control as defined under auditing means to check the performance on regular basis.

Example – Cash Purchases by Prime Furniture Ltd. of $ 1,00,000

Purchases A/c Dr. $1,00,000

To Cash A/c $1,00,000

2.Cost Accounting

Cost Accounting means classifying, analysing, summarizing and recording all the cost

related to organisation to make the decision so as to control the cost (Weygandt and et.al., 2018).

Cost Accounting includes Product costing and Activity based costing. Product Costing is related

to the prime cost such as direct raw materials are allocated per unit, direct labour is allocated as

per hour, fixed and variable overheads etc. Activity Based Costing is related to the indirect costs

of the company such as setting up machine for production purpose etc. It is basically used in

manufacturing organisation.

Example –

Revenue 100000

-Cost of Goods Sold -25000

=Gross Profit 75000

-Fixed Expenses -25000

-Variable Expenses -15000

=Net Profit 35000

3.Tax Accounting

Tax Accounting is a structure of accounting methods where accounts are made related to

tax rather than for public financial statements. Example of Tax Accounting are for individual

Income Tax is levied, Tax levied on partnerships and corporates is Corporate Tax and on Sales-

Sales Tax or GST is levied.

Example- Prime Furniture Ltd. sold the goods worth $1,000 on which there is 10% tax

Cash / Account Receivable A/C Dr. $1,100

To Sales Revenue A/C $1,000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Sales Tax Payable A/C $ 100

4.Management Accounting

Management Accounting is the process where managers uses relevant information or data

to take the better decisions for the organisation before going under certain matter. One of the

example of Management Accounting is Profit management by preparing Trading and P&L A/C.

P2 Explain different methods used for management accounting reporting.

Managerial Accounting Reporting are basically used for planning, regulating, decision

making, measuring performance for an organisation. Various kinds of Managerial Accounting

Reports are: 'Budget reports', 'Accounts Receivable Aging', 'Job Cost Reports', 'Inventory and

manufacturing' etc. (Butler and et.al., 2015).

There are various types Managerial Accounting Reports such as Trading &P&L account

determines profit/ loss made by the company in a financial year, Cost of Goods Sold shows

direct cost incurred by a business in its production and selling, Income Statement shows

expenses and proceeds from different activities in an organisation and determine its profitability,

Balance sheet shows a company's financial position through accounting its assets and liabilities,

Cash Flow Statement shows the cash balance of the company through its various activities.

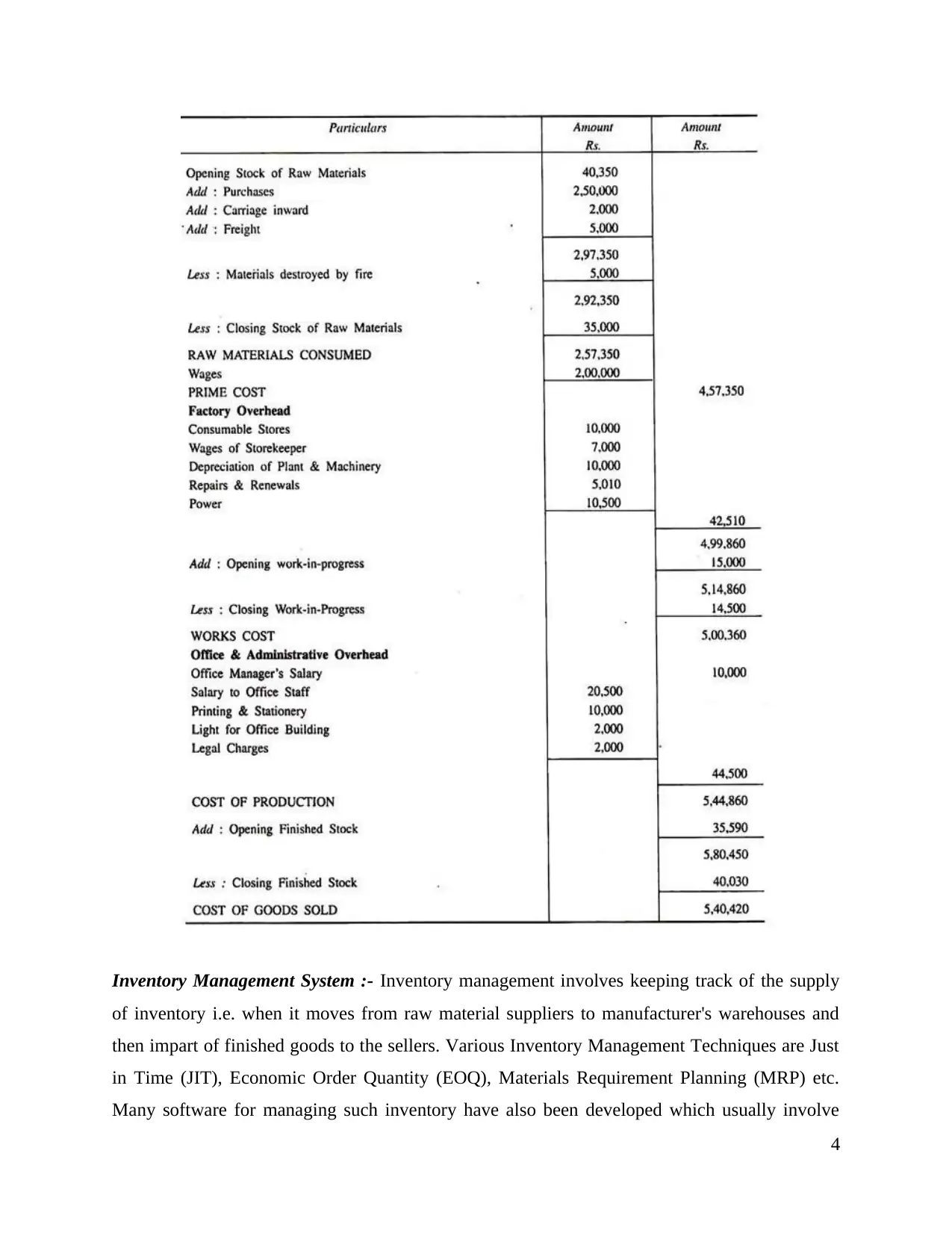

Cost Accounting System :- This method is used by accountants to keep accurate and upto date

track record of all the costs incurred during the entire production process from the moment raw

material are ordered till the finished good is delivered. It includes inventory valuation, cost

control and profitability analysis. Two main types of cost accounting system are Job Order

costing and process costing. It also involves Traditional costing system which is applied in each

to each job and Activity based costing which calculates activity rate (Kim, Schmidgall and et.al.,

2017).

Example

3

4.Management Accounting

Management Accounting is the process where managers uses relevant information or data

to take the better decisions for the organisation before going under certain matter. One of the

example of Management Accounting is Profit management by preparing Trading and P&L A/C.

P2 Explain different methods used for management accounting reporting.

Managerial Accounting Reporting are basically used for planning, regulating, decision

making, measuring performance for an organisation. Various kinds of Managerial Accounting

Reports are: 'Budget reports', 'Accounts Receivable Aging', 'Job Cost Reports', 'Inventory and

manufacturing' etc. (Butler and et.al., 2015).

There are various types Managerial Accounting Reports such as Trading &P&L account

determines profit/ loss made by the company in a financial year, Cost of Goods Sold shows

direct cost incurred by a business in its production and selling, Income Statement shows

expenses and proceeds from different activities in an organisation and determine its profitability,

Balance sheet shows a company's financial position through accounting its assets and liabilities,

Cash Flow Statement shows the cash balance of the company through its various activities.

Cost Accounting System :- This method is used by accountants to keep accurate and upto date

track record of all the costs incurred during the entire production process from the moment raw

material are ordered till the finished good is delivered. It includes inventory valuation, cost

control and profitability analysis. Two main types of cost accounting system are Job Order

costing and process costing. It also involves Traditional costing system which is applied in each

to each job and Activity based costing which calculates activity rate (Kim, Schmidgall and et.al.,

2017).

Example

3

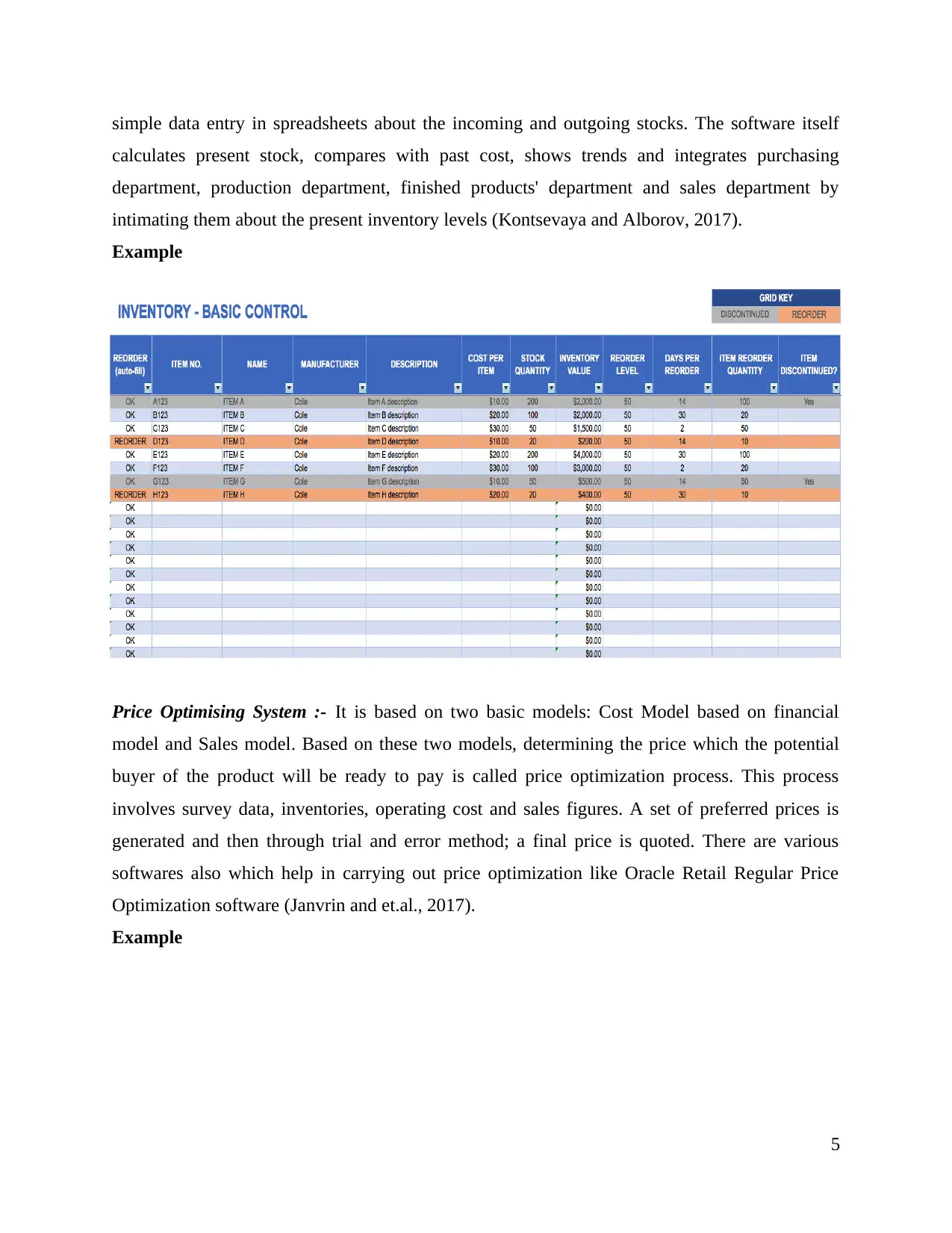

Inventory Management System :- Inventory management involves keeping track of the supply

of inventory i.e. when it moves from raw material suppliers to manufacturer's warehouses and

then impart of finished goods to the sellers. Various Inventory Management Techniques are Just

in Time (JIT), Economic Order Quantity (EOQ), Materials Requirement Planning (MRP) etc.

Many software for managing such inventory have also been developed which usually involve

4

of inventory i.e. when it moves from raw material suppliers to manufacturer's warehouses and

then impart of finished goods to the sellers. Various Inventory Management Techniques are Just

in Time (JIT), Economic Order Quantity (EOQ), Materials Requirement Planning (MRP) etc.

Many software for managing such inventory have also been developed which usually involve

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

simple data entry in spreadsheets about the incoming and outgoing stocks. The software itself

calculates present stock, compares with past cost, shows trends and integrates purchasing

department, production department, finished products' department and sales department by

intimating them about the present inventory levels (Kontsevaya and Alborov, 2017).

Example

Price Optimising System :- It is based on two basic models: Cost Model based on financial

model and Sales model. Based on these two models, determining the price which the potential

buyer of the product will be ready to pay is called price optimization process. This process

involves survey data, inventories, operating cost and sales figures. A set of preferred prices is

generated and then through trial and error method; a final price is quoted. There are various

softwares also which help in carrying out price optimization like Oracle Retail Regular Price

Optimization software (Janvrin and et.al., 2017).

Example

5

calculates present stock, compares with past cost, shows trends and integrates purchasing

department, production department, finished products' department and sales department by

intimating them about the present inventory levels (Kontsevaya and Alborov, 2017).

Example

Price Optimising System :- It is based on two basic models: Cost Model based on financial

model and Sales model. Based on these two models, determining the price which the potential

buyer of the product will be ready to pay is called price optimization process. This process

involves survey data, inventories, operating cost and sales figures. A set of preferred prices is

generated and then through trial and error method; a final price is quoted. There are various

softwares also which help in carrying out price optimization like Oracle Retail Regular Price

Optimization software (Janvrin and et.al., 2017).

Example

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

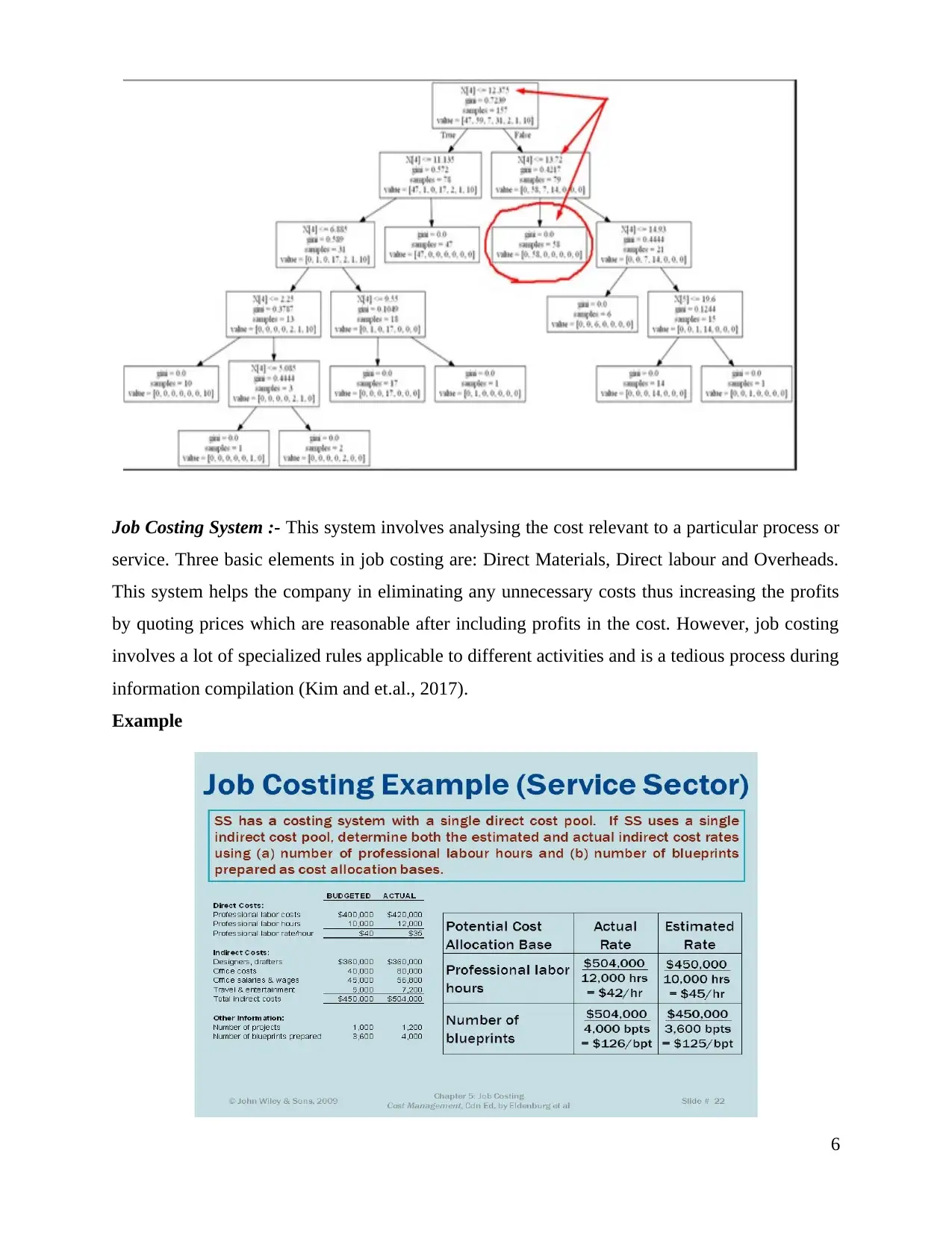

Job Costing System :- This system involves analysing the cost relevant to a particular process or

service. Three basic elements in job costing are: Direct Materials, Direct labour and Overheads.

This system helps the company in eliminating any unnecessary costs thus increasing the profits

by quoting prices which are reasonable after including profits in the cost. However, job costing

involves a lot of specialized rules applicable to different activities and is a tedious process during

information compilation (Kim and et.al., 2017).

Example

6

service. Three basic elements in job costing are: Direct Materials, Direct labour and Overheads.

This system helps the company in eliminating any unnecessary costs thus increasing the profits

by quoting prices which are reasonable after including profits in the cost. However, job costing

involves a lot of specialized rules applicable to different activities and is a tedious process during

information compilation (Kim and et.al., 2017).

Example

6

M1 Benefits of Management Accounting

Benefits of Cost Accounting System are -

It can help the management in controlling the extra cost incurred in organisation.

It can help the organisation through comparisons, cost cutting, cost elimination and

bringing all the data at one place and then analyse, summarize, and record in the

accounts.

Benefits of Inventory Management System are -

Achieve efficiency and productivity in operations by keeping minimum stock and safety

stock.

Minimises costs and Maximises sales & profits.

Benefits of Job-Costing System are-

Cost can be ascertained at any stage of the job which helps to control the cost in that

particular area.

Profit earned from each area is separately known.

Benefits of Price-Optimising System are-

It helps in setting up separate price for each area separately.

It helps in determining the profitability for the job and helps the customers or companies

to take up job or not.

D1 Integration of management accounting reporting and system

Management Accounting System helps the Prime Furniture Ltd. to classify, summarize,

analyse, record and record all the data in their respective accounts such as all expenses and

incomes will be recorded in P&L, all assets and liabilities in B/S, cash inflows and cash outflows

in Cash Flow Statement. These reports help in interpretation for the organisation about the costs

and incomes and make comparisons from budgets (Ghose, 2017).

P3 Preparation of income statement by using absorption and marginal costing

Marginal costing

Marginal Costing is one of the technique of cost analysis to prepare an income statement

means change in the total cost due to the change in the quantity of goods produced by the

company i.e. one more additional unit of good produced. In marginal costing, fixed costs are

accounted at last after all the other expenses are taken into account.

7

Benefits of Cost Accounting System are -

It can help the management in controlling the extra cost incurred in organisation.

It can help the organisation through comparisons, cost cutting, cost elimination and

bringing all the data at one place and then analyse, summarize, and record in the

accounts.

Benefits of Inventory Management System are -

Achieve efficiency and productivity in operations by keeping minimum stock and safety

stock.

Minimises costs and Maximises sales & profits.

Benefits of Job-Costing System are-

Cost can be ascertained at any stage of the job which helps to control the cost in that

particular area.

Profit earned from each area is separately known.

Benefits of Price-Optimising System are-

It helps in setting up separate price for each area separately.

It helps in determining the profitability for the job and helps the customers or companies

to take up job or not.

D1 Integration of management accounting reporting and system

Management Accounting System helps the Prime Furniture Ltd. to classify, summarize,

analyse, record and record all the data in their respective accounts such as all expenses and

incomes will be recorded in P&L, all assets and liabilities in B/S, cash inflows and cash outflows

in Cash Flow Statement. These reports help in interpretation for the organisation about the costs

and incomes and make comparisons from budgets (Ghose, 2017).

P3 Preparation of income statement by using absorption and marginal costing

Marginal costing

Marginal Costing is one of the technique of cost analysis to prepare an income statement

means change in the total cost due to the change in the quantity of goods produced by the

company i.e. one more additional unit of good produced. In marginal costing, fixed costs are

accounted at last after all the other expenses are taken into account.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

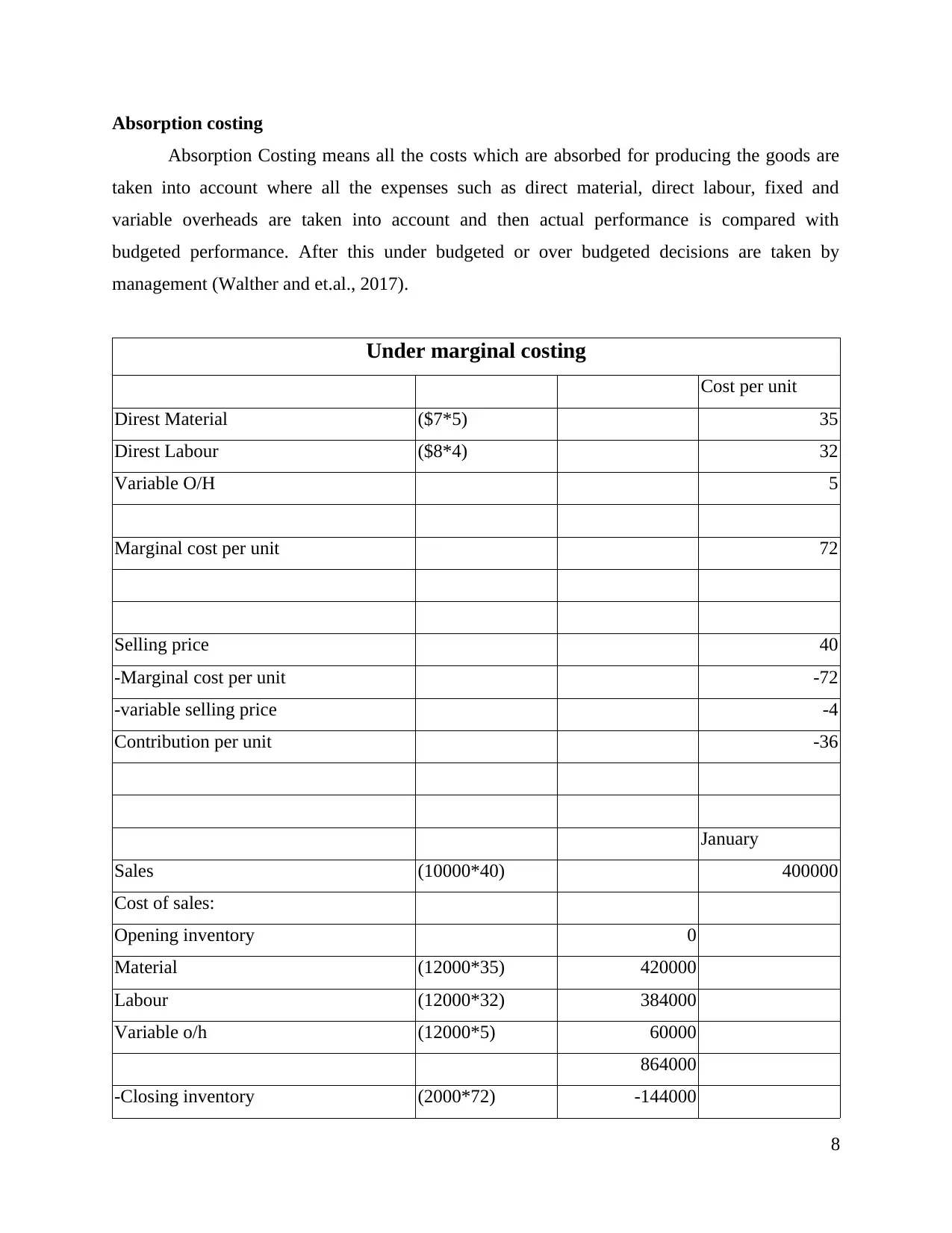

Absorption costing

Absorption Costing means all the costs which are absorbed for producing the goods are

taken into account where all the expenses such as direct material, direct labour, fixed and

variable overheads are taken into account and then actual performance is compared with

budgeted performance. After this under budgeted or over budgeted decisions are taken by

management (Walther and et.al., 2017).

Under marginal costing

Cost per unit

Direst Material ($7*5) 35

Direst Labour ($8*4) 32

Variable O/H 5

Marginal cost per unit 72

Selling price 40

-Marginal cost per unit -72

-variable selling price -4

Contribution per unit -36

January

Sales (10000*40) 400000

Cost of sales:

Opening inventory 0

Material (12000*35) 420000

Labour (12000*32) 384000

Variable o/h (12000*5) 60000

864000

-Closing inventory (2000*72) -144000

8

Absorption Costing means all the costs which are absorbed for producing the goods are

taken into account where all the expenses such as direct material, direct labour, fixed and

variable overheads are taken into account and then actual performance is compared with

budgeted performance. After this under budgeted or over budgeted decisions are taken by

management (Walther and et.al., 2017).

Under marginal costing

Cost per unit

Direst Material ($7*5) 35

Direst Labour ($8*4) 32

Variable O/H 5

Marginal cost per unit 72

Selling price 40

-Marginal cost per unit -72

-variable selling price -4

Contribution per unit -36

January

Sales (10000*40) 400000

Cost of sales:

Opening inventory 0

Material (12000*35) 420000

Labour (12000*32) 384000

Variable o/h (12000*5) 60000

864000

-Closing inventory (2000*72) -144000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

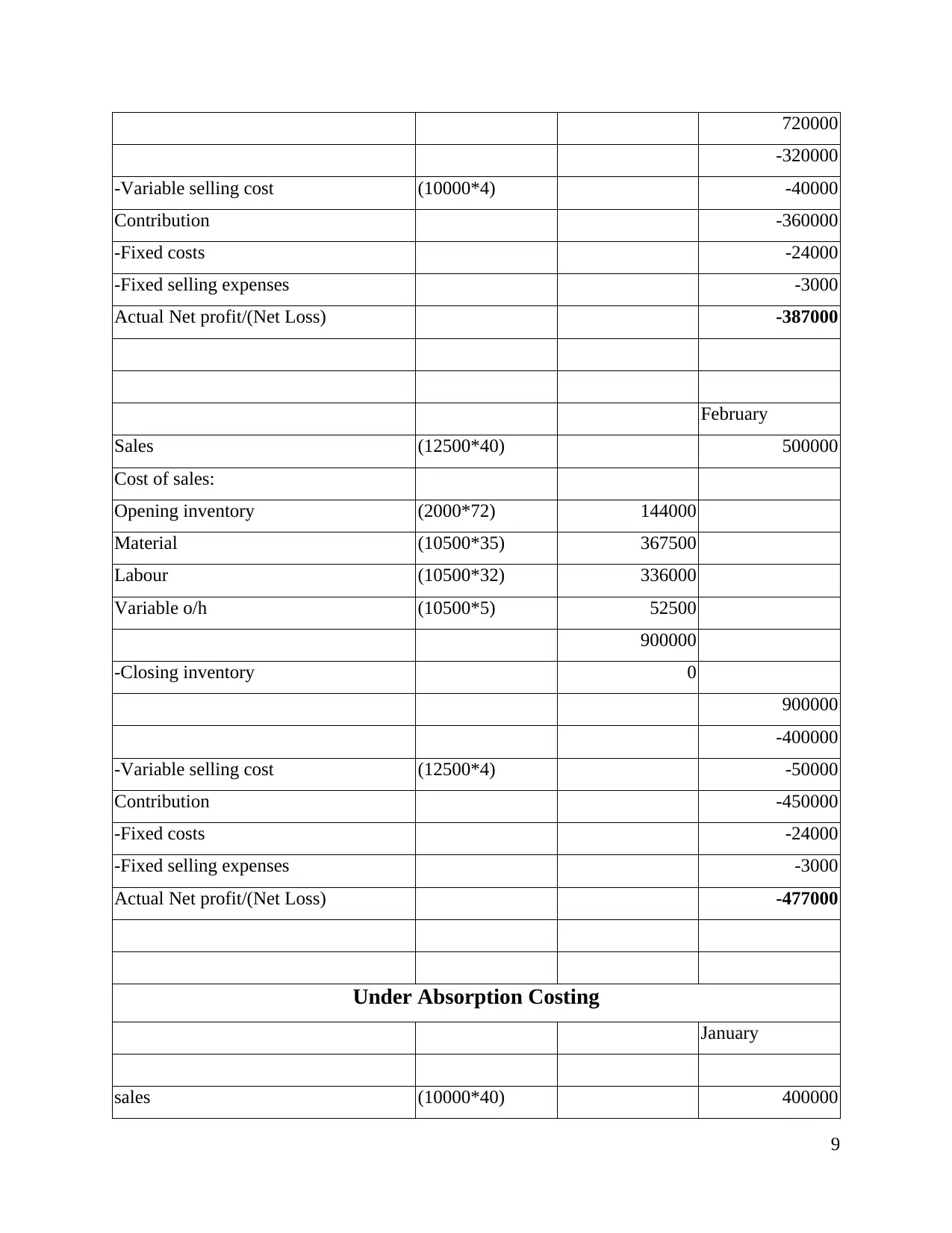

720000

-320000

-Variable selling cost (10000*4) -40000

Contribution -360000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -387000

February

Sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Variable o/h (10500*5) 52500

900000

-Closing inventory 0

900000

-400000

-Variable selling cost (12500*4) -50000

Contribution -450000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -477000

Under Absorption Costing

January

sales (10000*40) 400000

9

-320000

-Variable selling cost (10000*4) -40000

Contribution -360000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -387000

February

Sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Variable o/h (10500*5) 52500

900000

-Closing inventory 0

900000

-400000

-Variable selling cost (12500*4) -50000

Contribution -450000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -477000

Under Absorption Costing

January

sales (10000*40) 400000

9

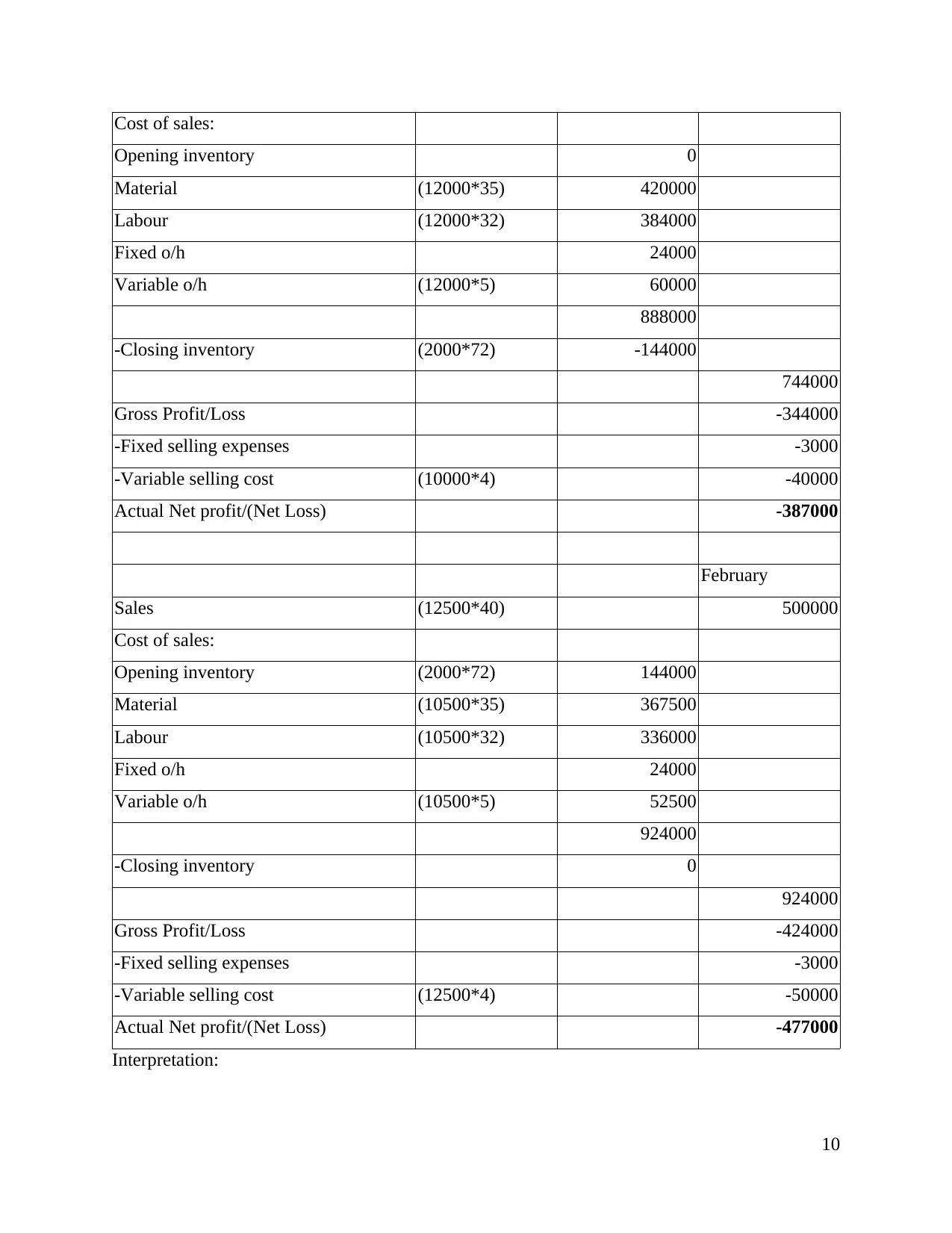

Cost of sales:

Opening inventory 0

Material (12000*35) 420000

Labour (12000*32) 384000

Fixed o/h 24000

Variable o/h (12000*5) 60000

888000

-Closing inventory (2000*72) -144000

744000

Gross Profit/Loss -344000

-Fixed selling expenses -3000

-Variable selling cost (10000*4) -40000

Actual Net profit/(Net Loss) -387000

February

Sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Fixed o/h 24000

Variable o/h (10500*5) 52500

924000

-Closing inventory 0

924000

Gross Profit/Loss -424000

-Fixed selling expenses -3000

-Variable selling cost (12500*4) -50000

Actual Net profit/(Net Loss) -477000

Interpretation:

10

Opening inventory 0

Material (12000*35) 420000

Labour (12000*32) 384000

Fixed o/h 24000

Variable o/h (12000*5) 60000

888000

-Closing inventory (2000*72) -144000

744000

Gross Profit/Loss -344000

-Fixed selling expenses -3000

-Variable selling cost (10000*4) -40000

Actual Net profit/(Net Loss) -387000

February

Sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Fixed o/h 24000

Variable o/h (10500*5) 52500

924000

-Closing inventory 0

924000

Gross Profit/Loss -424000

-Fixed selling expenses -3000

-Variable selling cost (12500*4) -50000

Actual Net profit/(Net Loss) -477000

Interpretation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.