Management Accounting Report: Financial Analysis of Abeam Consulting

VerifiedAdded on 2021/02/20

|17

|5859

|35

Report

AI Summary

This report provides a detailed analysis of management accounting practices, specifically focusing on Abeam Consulting Ltd. It begins with an introduction to management accounting, its principles, and different types of accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. The report then explores various management accounting reports, such as accounts receivable aging reports, budget reports, cost managerial reports, and performance reports, and explains their integration within organizational processes. The core of the report delves into the calculation of net profit or loss under marginal costing and absorption costing methods, providing a comparative analysis of these techniques. Additionally, it discusses the advantages and disadvantages of planning tools used for budgetary control and examines how different management accounting systems assist in solving financial problems. The report references relevant literature to support its findings, offering a comprehensive overview of management accounting applications within a financial consulting firm.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

MAIN BODY.......................................................................................................................................3

LO 1 .....................................................................................................................................................3

P1 Meaning of Management Accounting and Different types of accounting systems....................3

P 2 Different methods of accounting reports prepared by Abeam consulting Ltd ..........................5

LO 2......................................................................................................................................................6

P 3 Calculation of net profit or loss under Marginal costing and Absorption costing ....................6

LO 3....................................................................................................................................................10

P 4 Advantages and Disadvantages of Planning Tools Used for Budgetary Control.....................10

P 5. Different management accounting system assisting in solving financial problem.................11

REFERENCES...................................................................................................................................15

INTRODUCTION................................................................................................................................3

MAIN BODY.......................................................................................................................................3

LO 1 .....................................................................................................................................................3

P1 Meaning of Management Accounting and Different types of accounting systems....................3

P 2 Different methods of accounting reports prepared by Abeam consulting Ltd ..........................5

LO 2......................................................................................................................................................6

P 3 Calculation of net profit or loss under Marginal costing and Absorption costing ....................6

LO 3....................................................................................................................................................10

P 4 Advantages and Disadvantages of Planning Tools Used for Budgetary Control.....................10

P 5. Different management accounting system assisting in solving financial problem.................11

REFERENCES...................................................................................................................................15

INTRODUCTION

Management Accounting is the system where all the transactions related to the financial

transactions are analysed, summarizes and recorded in the various to prepare the financial

statements for the organisation (Chenhall, 2015). Accounting helps in recording all the monetary

transactions of the company in order to know the financial position of the organisation. Abeam

Consulting is the medium sized financial consulting firm founded on 1st April, 1981. At present,

company is having 5915 employees all over the world. Company is having its headquarters in

Tokyo, Japan. The main business of the company is management consulting, business process

consulting, IT Consulting etc. Company is having 33 countries and 65 offices all over the world.

Total capital of the company is ¥6.2 Billion and net sales as per year 2019 is ¥85.8 billion. This

report consists of presenting the management accounting and the various methods of accounting

aspects of the company. It also covers the cost accounting systems and valuation methods of

inventory and financial problems and how resolve all the problems using various techniques.

MAIN BODY

LO 1

P1 Meaning of Management Accounting and Different types of accounting systems

Management Accounting is the process where the company analyses, summarizes and

records all the transactions related to the financial transactions for preparation of financial

statements of Abeam consulting Ltd. Management Accounting is prepared for internal and external

stakeholders of the company. Financial Statements of Abeam consulting helps in taking various

decisions for the company. They help in make trend analysis and forecasting for the company

through the various financial statements of the company.

Management Accounting systems are the systems which consists of measures and evaluating

the financial statements of Abeam consulting Ltd. Various elements of the accounts are compared

with each other in order to know where the extra cost has been allocated and how to eliminate the

extra cost from the company (Schmid, 2019). These are systems are important to integrate within

the organisation because the systems help the company in evaluating the financial statements of

Abeam consulting Ltd. Management Accounting covers the various other accounting such as

financial accounting, cost accounting and managerial accounting.

Origin of Management Accounting

Management Accounting was first emerged at the time of industrial revolution and rose after

Management Accounting is the system where all the transactions related to the financial

transactions are analysed, summarizes and recorded in the various to prepare the financial

statements for the organisation (Chenhall, 2015). Accounting helps in recording all the monetary

transactions of the company in order to know the financial position of the organisation. Abeam

Consulting is the medium sized financial consulting firm founded on 1st April, 1981. At present,

company is having 5915 employees all over the world. Company is having its headquarters in

Tokyo, Japan. The main business of the company is management consulting, business process

consulting, IT Consulting etc. Company is having 33 countries and 65 offices all over the world.

Total capital of the company is ¥6.2 Billion and net sales as per year 2019 is ¥85.8 billion. This

report consists of presenting the management accounting and the various methods of accounting

aspects of the company. It also covers the cost accounting systems and valuation methods of

inventory and financial problems and how resolve all the problems using various techniques.

MAIN BODY

LO 1

P1 Meaning of Management Accounting and Different types of accounting systems

Management Accounting is the process where the company analyses, summarizes and

records all the transactions related to the financial transactions for preparation of financial

statements of Abeam consulting Ltd. Management Accounting is prepared for internal and external

stakeholders of the company. Financial Statements of Abeam consulting helps in taking various

decisions for the company. They help in make trend analysis and forecasting for the company

through the various financial statements of the company.

Management Accounting systems are the systems which consists of measures and evaluating

the financial statements of Abeam consulting Ltd. Various elements of the accounts are compared

with each other in order to know where the extra cost has been allocated and how to eliminate the

extra cost from the company (Schmid, 2019). These are systems are important to integrate within

the organisation because the systems help the company in evaluating the financial statements of

Abeam consulting Ltd. Management Accounting covers the various other accounting such as

financial accounting, cost accounting and managerial accounting.

Origin of Management Accounting

Management Accounting was first emerged at the time of industrial revolution and rose after

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the financial accounting. The two leading industries played main role in bringing management

accounting i.e. Textile industry and railroads. These industries were having large cash receipts from

numerous customers because of which both financial and management accounting was raised in

order to measure the efficiency of moving passengers and freight.

Role of Management Accounting

The main role of management accounting is to measure and evaluate the financial statements

of Abeam Consulting Ltd. This helps in decision making for the company and also helps in

elimination of extra cost of the company. The another main role of management accounting is to

prepare the reports for the company which shows the financial position of Abeam consulting Ltd.

Principle of Management Accounting

Principles of Management Accounting are disclosure of financial statements with

transparency and disclosing all the facts and figures related to the financial statements of Abeam

Consulting Ltd. The another principle of management accounting is to compile all the financial

statements of company as per the accounting standards (Pearce, 2016). The other two principles of

management accounting are causality and analogy. Causality Principle states the relation between

the quantitative output and quantitative input which has been consumed to achieve the output for

the company. Analogy principle is to use the past outcomes for forecasting the future targets for

Abeam consulting Ltd. It mainly focus how the user of information best uses the information of

financial statements.

Different types of Management accounting systems are

Various types of management accounting system are as follows

Cost- accounting systems

Cost Accounting systems is also called product costing system. It calculates the cost per unit

obtained in production of one unit of good for Abeam consulting Ltd. These systems also obtains

the information related to the total cost of the company and where the extra cost had been allocated

and how the cost can be eliminated within the different department where the extra cost is not

benefiting (Pearce, 2016). The system helps in preparation of cost reports related to raw materials,

work I progress and finished goods.

Inventory Management systems

Inventory Management system is the method where all the events related to the inventory

are recorded in order to know the sales and production budget for Abeam consulting Ltd. The

system helps the company in managing all the transaction related to the inventory in the system so

accounting i.e. Textile industry and railroads. These industries were having large cash receipts from

numerous customers because of which both financial and management accounting was raised in

order to measure the efficiency of moving passengers and freight.

Role of Management Accounting

The main role of management accounting is to measure and evaluate the financial statements

of Abeam Consulting Ltd. This helps in decision making for the company and also helps in

elimination of extra cost of the company. The another main role of management accounting is to

prepare the reports for the company which shows the financial position of Abeam consulting Ltd.

Principle of Management Accounting

Principles of Management Accounting are disclosure of financial statements with

transparency and disclosing all the facts and figures related to the financial statements of Abeam

Consulting Ltd. The another principle of management accounting is to compile all the financial

statements of company as per the accounting standards (Pearce, 2016). The other two principles of

management accounting are causality and analogy. Causality Principle states the relation between

the quantitative output and quantitative input which has been consumed to achieve the output for

the company. Analogy principle is to use the past outcomes for forecasting the future targets for

Abeam consulting Ltd. It mainly focus how the user of information best uses the information of

financial statements.

Different types of Management accounting systems are

Various types of management accounting system are as follows

Cost- accounting systems

Cost Accounting systems is also called product costing system. It calculates the cost per unit

obtained in production of one unit of good for Abeam consulting Ltd. These systems also obtains

the information related to the total cost of the company and where the extra cost had been allocated

and how the cost can be eliminated within the different department where the extra cost is not

benefiting (Pearce, 2016). The system helps in preparation of cost reports related to raw materials,

work I progress and finished goods.

Inventory Management systems

Inventory Management system is the method where all the events related to the inventory

are recorded in order to know the sales and production budget for Abeam consulting Ltd. The

system helps the company in managing all the transaction related to the inventory in the system so

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that the company can know the time period of converting inventory into sales. The main benefit of

inventory management system is to prepare the sales and production budgets on the basis of

previous year sales occurred in Abeam consulting Ltd.

Job Costing systems

Job costing system helps in knowing the total cost applied in every department and what is

extra cost allocated in Abeam consulting Ltd. The system shows the cost allocated in production of

various units in the company and how to eliminate the various cost in the job. It includes the various

costs such as direct material costs, direct labour cost and overheads cost. Cost sheets are prepared in

Abeam Consulting in order to know the over absorption and under absorption of costs through

evaluating cost sheets.

Price- optimization systems

Price optimization system shows that how the customers will respond to the price of goods

given by Abeam consulting Ltd in market for sale. It also helps the company in maximizing its

operating profits of the company and decreasing the extra costs of the company. The main benefit of

Price Optimization system is to know the potential buyers of the products and helps in determining

the price models for the different products of Abeam consulting Ltd.

P 2 Different methods of accounting reports prepared by Abeam consulting Ltd

Management Accounting Reports are prepared in order to evaluate the financial statements

of Abeam Ltd. It helps in taking various decisions for the company and what are the main problems

of the company where extra cost has been eliminated. The various types of reports are-

Account Receivables Aging Reports

Account Receivables Aging reports helps in knowing the company that in how much time

company converts its debtors of the company in cash. This report help Abeam consulting Ltd in

making the account receivable related policies for the company. The main benefits of reports is to

know that where the company is lacking in no collecting the cash from debtors on time.

Budget Reports

Budgets Reports are prepared in order to set the budgets for the company and to compare the

actual performance of Abeam consulting with budgeted performance of the company. It also helps

the company in setting up target for achieving those targets in future in order to achieve the budgets

profits for the company.

Cost Managerial Reports

inventory management system is to prepare the sales and production budgets on the basis of

previous year sales occurred in Abeam consulting Ltd.

Job Costing systems

Job costing system helps in knowing the total cost applied in every department and what is

extra cost allocated in Abeam consulting Ltd. The system shows the cost allocated in production of

various units in the company and how to eliminate the various cost in the job. It includes the various

costs such as direct material costs, direct labour cost and overheads cost. Cost sheets are prepared in

Abeam Consulting in order to know the over absorption and under absorption of costs through

evaluating cost sheets.

Price- optimization systems

Price optimization system shows that how the customers will respond to the price of goods

given by Abeam consulting Ltd in market for sale. It also helps the company in maximizing its

operating profits of the company and decreasing the extra costs of the company. The main benefit of

Price Optimization system is to know the potential buyers of the products and helps in determining

the price models for the different products of Abeam consulting Ltd.

P 2 Different methods of accounting reports prepared by Abeam consulting Ltd

Management Accounting Reports are prepared in order to evaluate the financial statements

of Abeam Ltd. It helps in taking various decisions for the company and what are the main problems

of the company where extra cost has been eliminated. The various types of reports are-

Account Receivables Aging Reports

Account Receivables Aging reports helps in knowing the company that in how much time

company converts its debtors of the company in cash. This report help Abeam consulting Ltd in

making the account receivable related policies for the company. The main benefits of reports is to

know that where the company is lacking in no collecting the cash from debtors on time.

Budget Reports

Budgets Reports are prepared in order to set the budgets for the company and to compare the

actual performance of Abeam consulting with budgeted performance of the company. It also helps

the company in setting up target for achieving those targets in future in order to achieve the budgets

profits for the company.

Cost Managerial Reports

Cost Managerial Reports helps in knowing the total cost of the company in production of

goods Abeam Consulting Ltd. The report helps the company in knowing the various cost allocated

in various department and how to eliminate the cost for the company (Schmid, 2019). It also helps

in calculating the best price for the goods which can be sold to customers by the company.

Performance Reports

Performance Reports helps in knowing the performance of various department in Abeam

Consulting Ltd in order to know that which department can give more benefits to the company. It

also helps in knowing the that which department is efficiently and effectively working in the

organisation (Leung, 2015). Performance Reports also help in knowing the under- performers and

over- performers of Abeam consulting Ltd.

Management accounting systems and management accounting reporting are integrated in

organisational process because both are inter-related and interconnected to each other. They both

help in preparation of financial statements and evaluates and measured the various elements in the

financials statements.

Benefits of management accounting system

Management accounting system assists company in making improvement in its internal

business operations as well as system. Also, it helps Abeam Ltd in its decision making process in

following manner:

Inventory management system

It helps Abeam in ensuring proper flow of inventory in the business thereby reducing overall

cost of maintaining inventory and leads to increase in profit levels as well.

Also, it ensures that overall efficiency and performance of business operations improves

thereby increasing productivity level.

Cost accounting system

It helps in determining unproductive business areas which are contributing to increase in

business expenses and lowering of profit margins thereby eliminating such business

operations for the betterment of company as a whole.

Assists in making proper estimation as well as allocation of cost amount for conducting of

smooth business operations.

Integration of management accounting system and reporting

Management accounting system and reporting are considered as most integrated part for

every business organisation as both aspects of business are highly depended on each other. On the

goods Abeam Consulting Ltd. The report helps the company in knowing the various cost allocated

in various department and how to eliminate the cost for the company (Schmid, 2019). It also helps

in calculating the best price for the goods which can be sold to customers by the company.

Performance Reports

Performance Reports helps in knowing the performance of various department in Abeam

Consulting Ltd in order to know that which department can give more benefits to the company. It

also helps in knowing the that which department is efficiently and effectively working in the

organisation (Leung, 2015). Performance Reports also help in knowing the under- performers and

over- performers of Abeam consulting Ltd.

Management accounting systems and management accounting reporting are integrated in

organisational process because both are inter-related and interconnected to each other. They both

help in preparation of financial statements and evaluates and measured the various elements in the

financials statements.

Benefits of management accounting system

Management accounting system assists company in making improvement in its internal

business operations as well as system. Also, it helps Abeam Ltd in its decision making process in

following manner:

Inventory management system

It helps Abeam in ensuring proper flow of inventory in the business thereby reducing overall

cost of maintaining inventory and leads to increase in profit levels as well.

Also, it ensures that overall efficiency and performance of business operations improves

thereby increasing productivity level.

Cost accounting system

It helps in determining unproductive business areas which are contributing to increase in

business expenses and lowering of profit margins thereby eliminating such business

operations for the betterment of company as a whole.

Assists in making proper estimation as well as allocation of cost amount for conducting of

smooth business operations.

Integration of management accounting system and reporting

Management accounting system and reporting are considered as most integrated part for

every business organisation as both aspects of business are highly depended on each other. On the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

basis of management accounting system such cost and inventory system, it assists Abeam Ltd in

preparation of cost accounting report depicting about cost structure of the business. Also, with the

help of such reports, the management of the company can make effective decision for making

improvement in overall business as well as employees performance and profitability level. The cost

accounting report prepared on the basis of cost accounting system helps the company in making

decision regarding to elimination and minimizing of unnecessary cost expenditure in order to

increase the profitability. Furthermore, with the help of job costing system. Abeam Ltd can prepare

job costing report so as to identify profitability of business regarding to specific job.

LO 2

P 3 Calculation of net profit or loss under Marginal costing and Absorption costing

Cost is the element which can be defined as the total cost absorbed in the production of

goods by Abeam consulting Ltd. It consists of various cost such as raw material, labour, overhead

costs (Gavva, and et.al., 2016). Cost analysis is the relationship between cos and output of the

company. It shows the various cost applied in production of goods and the number of units are

output for the company.

Flexible budgeting is prepared on the basis of level of activity of the company. The budget

can be easily calculated and can be changed with the change in the level of activity of Abeam

Consulting Ltd. The various cost are fixed costs and variable cost (Nobre, 2016). Fixed cost does

not change with the change in the output whereas variable costs changes with the change in the

output of Abeam consulting Ltd. Normal costing is the actual costing incurred in the company on

the basis of actual performance of the company. Standard Costing is the set budgets by the company

which are to be achieved by the managers of the company in order to achieve the costs of the

company.

Marginal costing and Absorption Costing

Marginal costing uses only marginal costing at the time of valuation of closing inventory of

the company. Under this method, Marginal Costing deducts all the variable expenses to calculate

the contribution of Abeam consulting Ltd. All fixed expenses are deducted from contribution in

order to calculate the net profit or loss for the company (Ray, 2015).

Absorption costing helps in calculating cost amount as associated with the business

operations such as manufacturing or production of a specific product or services. It is defines that

all the cost amount incurred on manufacturing operations have been assigned to all the units

produced. It calculates absorption cost per unit in order to value the closing inventory of Abeam

preparation of cost accounting report depicting about cost structure of the business. Also, with the

help of such reports, the management of the company can make effective decision for making

improvement in overall business as well as employees performance and profitability level. The cost

accounting report prepared on the basis of cost accounting system helps the company in making

decision regarding to elimination and minimizing of unnecessary cost expenditure in order to

increase the profitability. Furthermore, with the help of job costing system. Abeam Ltd can prepare

job costing report so as to identify profitability of business regarding to specific job.

LO 2

P 3 Calculation of net profit or loss under Marginal costing and Absorption costing

Cost is the element which can be defined as the total cost absorbed in the production of

goods by Abeam consulting Ltd. It consists of various cost such as raw material, labour, overhead

costs (Gavva, and et.al., 2016). Cost analysis is the relationship between cos and output of the

company. It shows the various cost applied in production of goods and the number of units are

output for the company.

Flexible budgeting is prepared on the basis of level of activity of the company. The budget

can be easily calculated and can be changed with the change in the level of activity of Abeam

Consulting Ltd. The various cost are fixed costs and variable cost (Nobre, 2016). Fixed cost does

not change with the change in the output whereas variable costs changes with the change in the

output of Abeam consulting Ltd. Normal costing is the actual costing incurred in the company on

the basis of actual performance of the company. Standard Costing is the set budgets by the company

which are to be achieved by the managers of the company in order to achieve the costs of the

company.

Marginal costing and Absorption Costing

Marginal costing uses only marginal costing at the time of valuation of closing inventory of

the company. Under this method, Marginal Costing deducts all the variable expenses to calculate

the contribution of Abeam consulting Ltd. All fixed expenses are deducted from contribution in

order to calculate the net profit or loss for the company (Ray, 2015).

Absorption costing helps in calculating cost amount as associated with the business

operations such as manufacturing or production of a specific product or services. It is defines that

all the cost amount incurred on manufacturing operations have been assigned to all the units

produced. It calculates absorption cost per unit in order to value the closing inventory of Abeam

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consulting Ltd. All the fixed costs and variable costs of the company are taken into for calculation

of absorption cost per unit (Schmidt, 2015). All the fixed and variable production costs to calculate

gross profit for the company. Fixed and variable selling costs are deducted in order to calculate net

profit or loss for the company. Absorption costs considers all the cost which are absorb at the time

of production of goods.

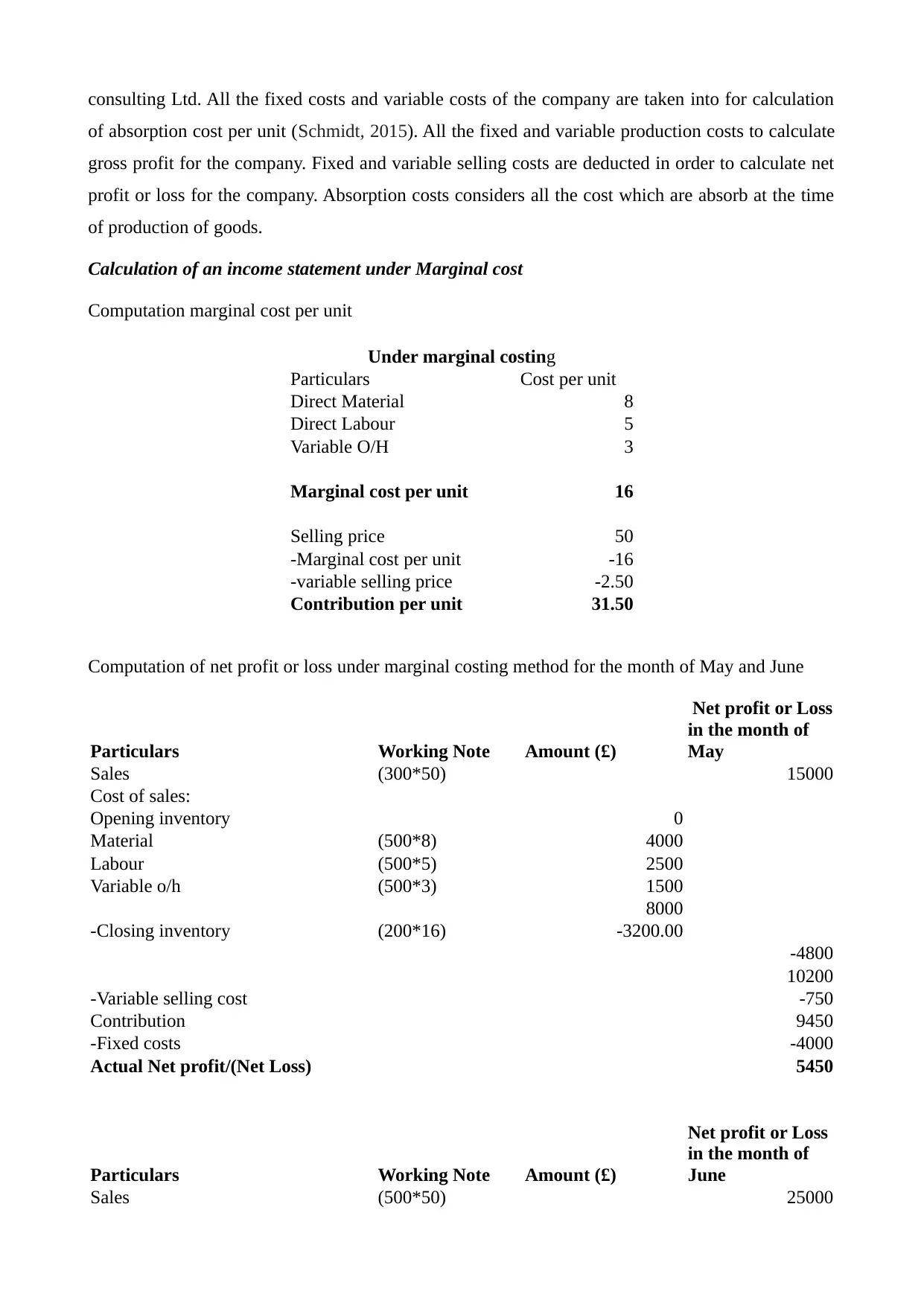

Calculation of an income statement under Marginal cost

Computation marginal cost per unit

Under marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

Computation of net profit or loss under marginal costing method for the month of May and June

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

June

Sales (500*50) 25000

of absorption cost per unit (Schmidt, 2015). All the fixed and variable production costs to calculate

gross profit for the company. Fixed and variable selling costs are deducted in order to calculate net

profit or loss for the company. Absorption costs considers all the cost which are absorb at the time

of production of goods.

Calculation of an income statement under Marginal cost

Computation marginal cost per unit

Under marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

Computation of net profit or loss under marginal costing method for the month of May and June

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

June

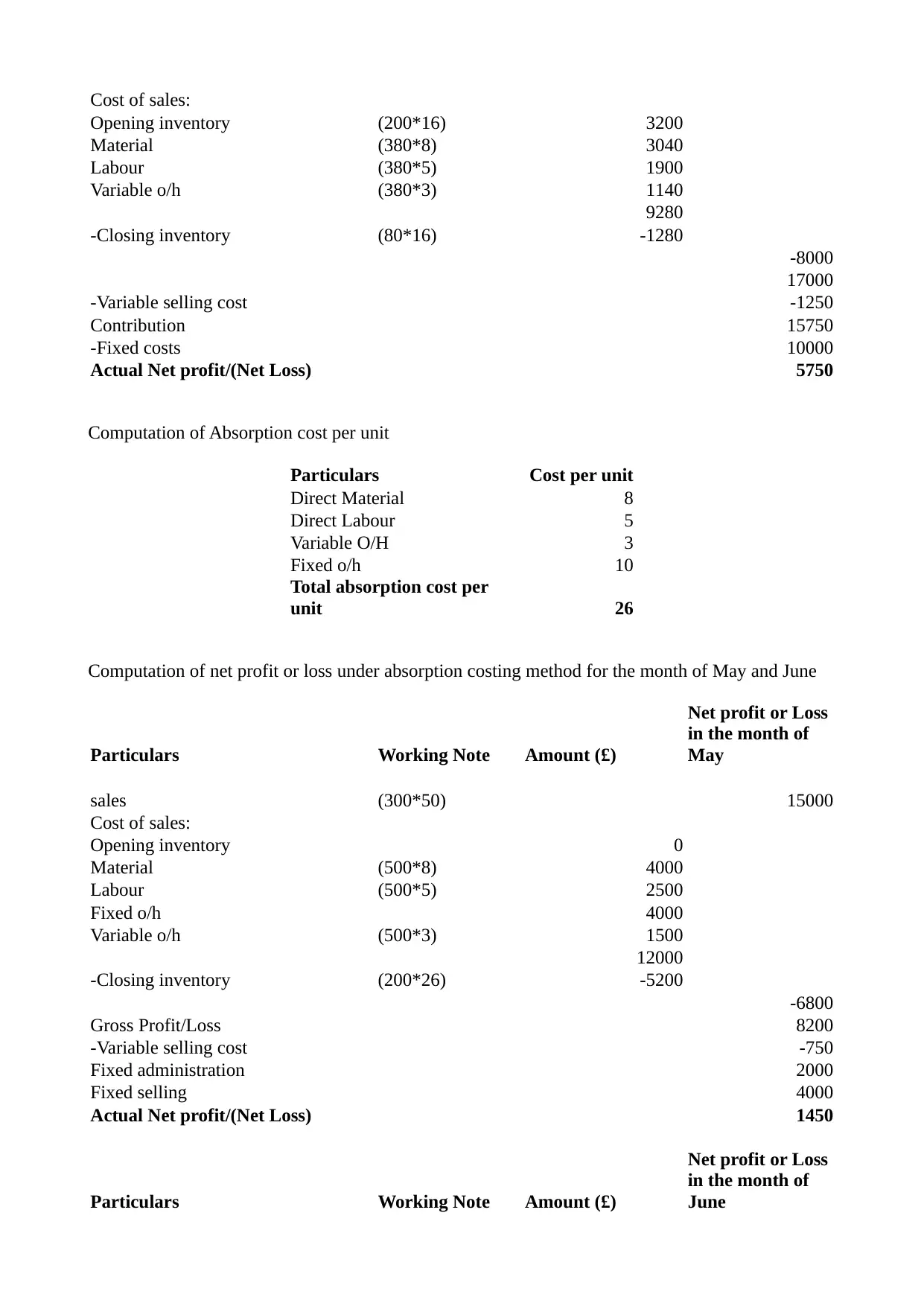

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs 10000

Actual Net profit/(Net Loss) 5750

Computation of Absorption cost per unit

Particulars Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per

unit 26

Computation of net profit or loss under absorption costing method for the month of May and June

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*26) -5200

-6800

Gross Profit/Loss 8200

-Variable selling cost -750

Fixed administration 2000

Fixed selling 4000

Actual Net profit/(Net Loss) 1450

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

June

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs 10000

Actual Net profit/(Net Loss) 5750

Computation of Absorption cost per unit

Particulars Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per

unit 26

Computation of net profit or loss under absorption costing method for the month of May and June

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*26) -5200

-6800

Gross Profit/Loss 8200

-Variable selling cost -750

Fixed administration 2000

Fixed selling 4000

Actual Net profit/(Net Loss) 1450

Particulars Working Note Amount (£)

Net profit or Loss

in the month of

June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

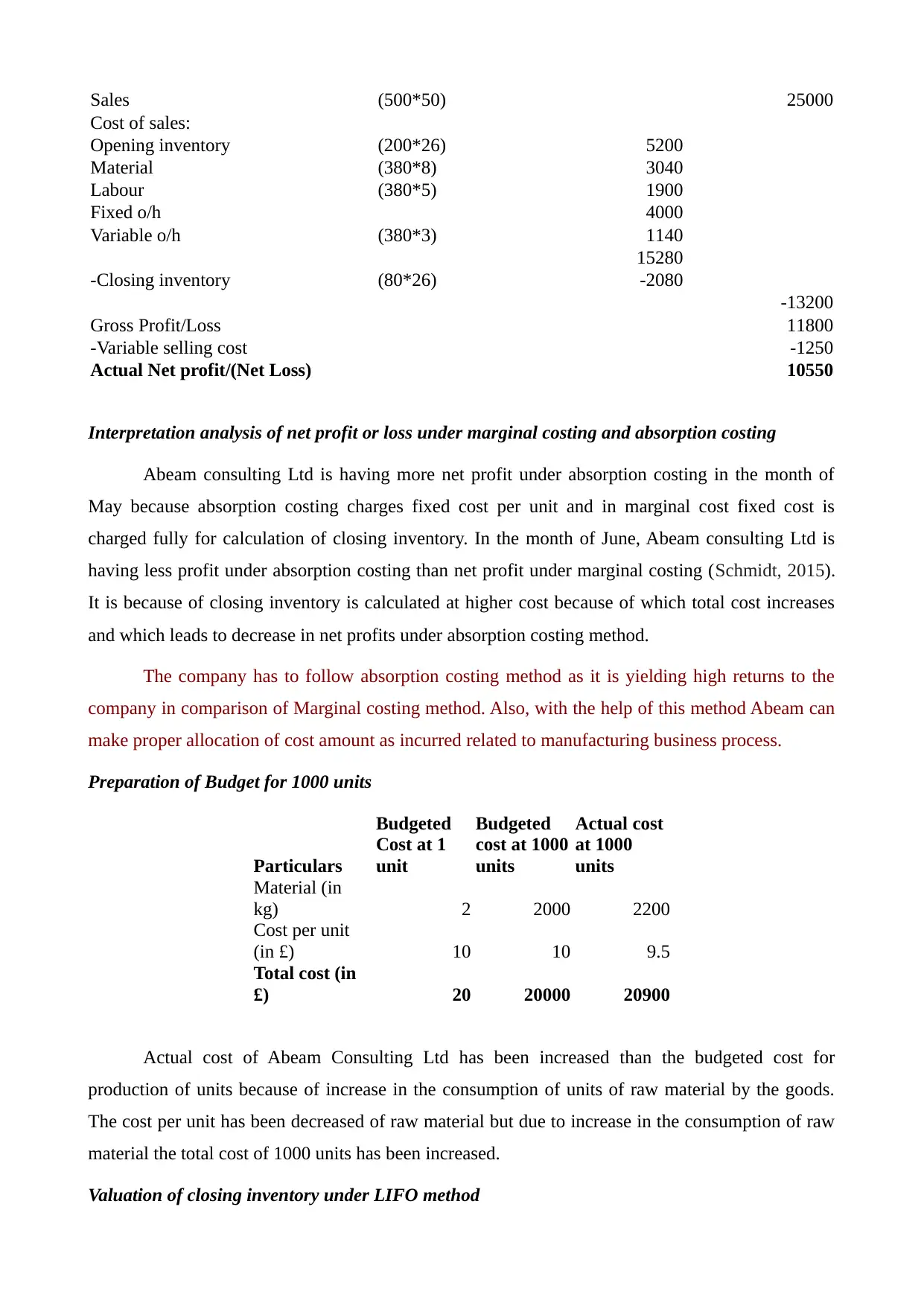

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 4000

Variable o/h (380*3) 1140

15280

-Closing inventory (80*26) -2080

-13200

Gross Profit/Loss 11800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 10550

Interpretation analysis of net profit or loss under marginal costing and absorption costing

Abeam consulting Ltd is having more net profit under absorption costing in the month of

May because absorption costing charges fixed cost per unit and in marginal cost fixed cost is

charged fully for calculation of closing inventory. In the month of June, Abeam consulting Ltd is

having less profit under absorption costing than net profit under marginal costing (Schmidt, 2015).

It is because of closing inventory is calculated at higher cost because of which total cost increases

and which leads to decrease in net profits under absorption costing method.

The company has to follow absorption costing method as it is yielding high returns to the

company in comparison of Marginal costing method. Also, with the help of this method Abeam can

make proper allocation of cost amount as incurred related to manufacturing business process.

Preparation of Budget for 1000 units

Particulars

Budgeted

Cost at 1

unit

Budgeted

cost at 1000

units

Actual cost

at 1000

units

Material (in

kg) 2 2000 2200

Cost per unit

(in £) 10 10 9.5

Total cost (in

£) 20 20000 20900

Actual cost of Abeam Consulting Ltd has been increased than the budgeted cost for

production of units because of increase in the consumption of units of raw material by the goods.

The cost per unit has been decreased of raw material but due to increase in the consumption of raw

material the total cost of 1000 units has been increased.

Valuation of closing inventory under LIFO method

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 4000

Variable o/h (380*3) 1140

15280

-Closing inventory (80*26) -2080

-13200

Gross Profit/Loss 11800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 10550

Interpretation analysis of net profit or loss under marginal costing and absorption costing

Abeam consulting Ltd is having more net profit under absorption costing in the month of

May because absorption costing charges fixed cost per unit and in marginal cost fixed cost is

charged fully for calculation of closing inventory. In the month of June, Abeam consulting Ltd is

having less profit under absorption costing than net profit under marginal costing (Schmidt, 2015).

It is because of closing inventory is calculated at higher cost because of which total cost increases

and which leads to decrease in net profits under absorption costing method.

The company has to follow absorption costing method as it is yielding high returns to the

company in comparison of Marginal costing method. Also, with the help of this method Abeam can

make proper allocation of cost amount as incurred related to manufacturing business process.

Preparation of Budget for 1000 units

Particulars

Budgeted

Cost at 1

unit

Budgeted

cost at 1000

units

Actual cost

at 1000

units

Material (in

kg) 2 2000 2200

Cost per unit

(in £) 10 10 9.5

Total cost (in

£) 20 20000 20900

Actual cost of Abeam Consulting Ltd has been increased than the budgeted cost for

production of units because of increase in the consumption of units of raw material by the goods.

The cost per unit has been decreased of raw material but due to increase in the consumption of raw

material the total cost of 1000 units has been increased.

Valuation of closing inventory under LIFO method

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

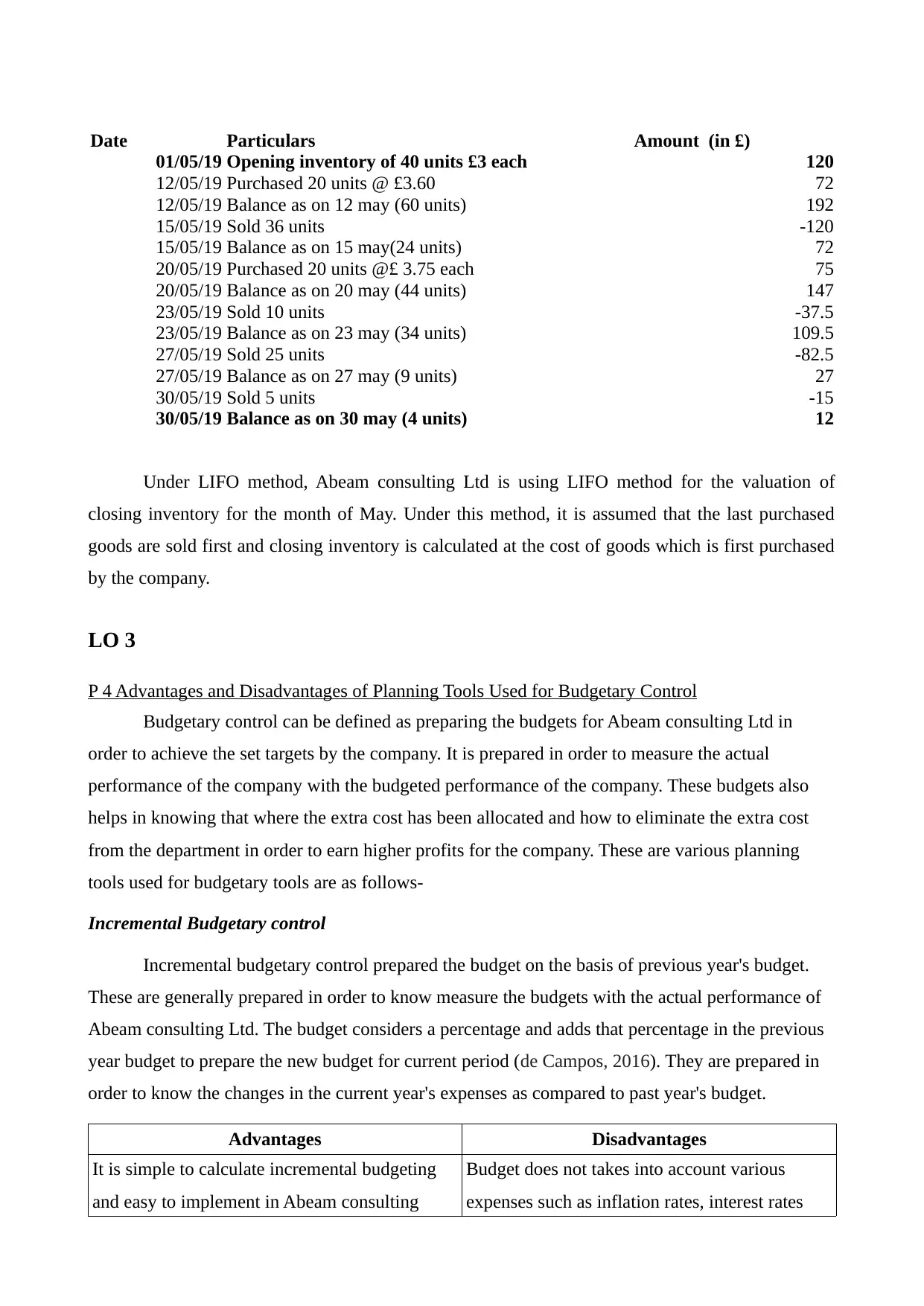

Date Particulars Amount (in £)

01/05/19 Opening inventory of 40 units £3 each 120

12/05/19 Purchased 20 units @ £3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @£ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

Under LIFO method, Abeam consulting Ltd is using LIFO method for the valuation of

closing inventory for the month of May. Under this method, it is assumed that the last purchased

goods are sold first and closing inventory is calculated at the cost of goods which is first purchased

by the company.

LO 3

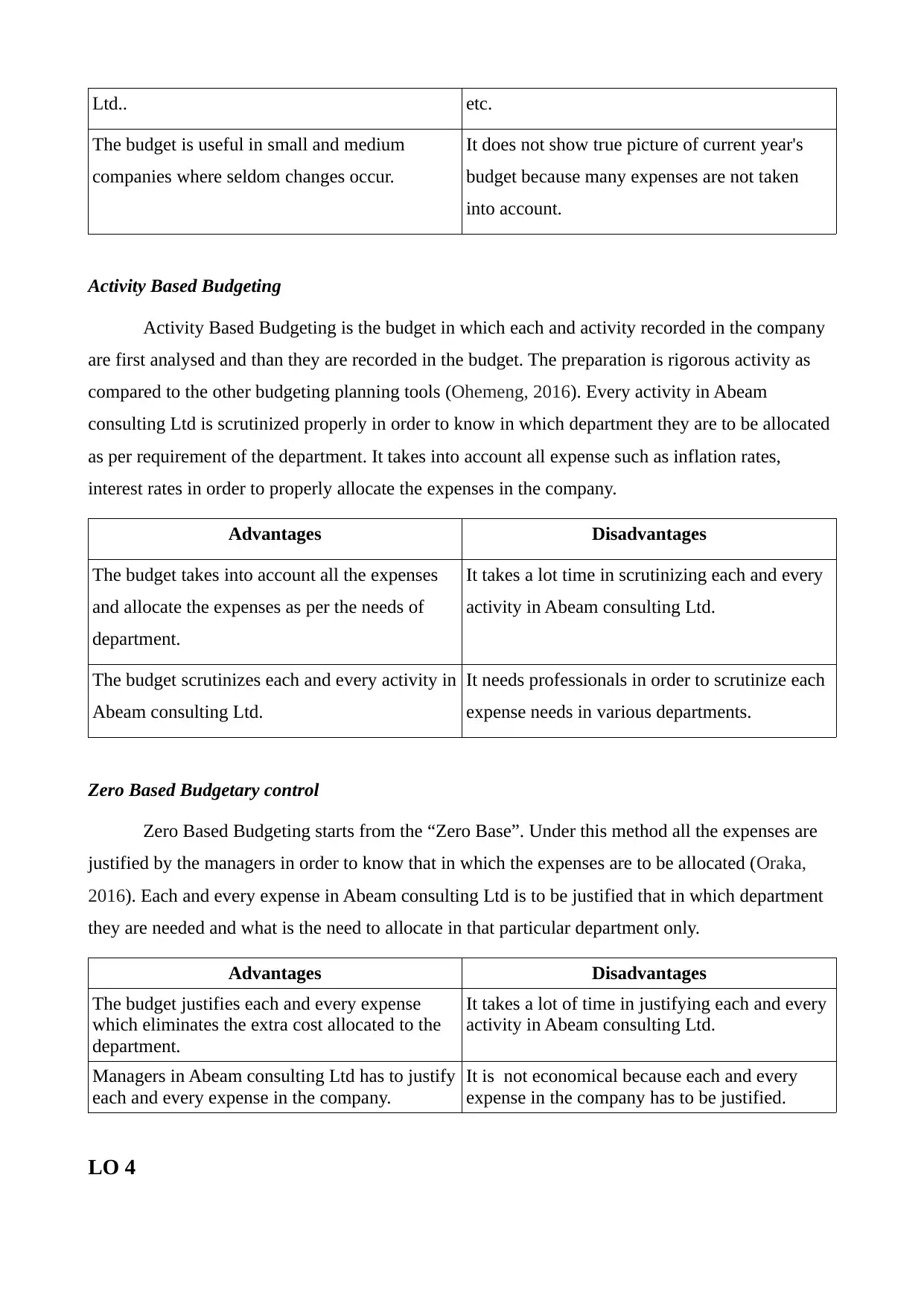

P 4 Advantages and Disadvantages of Planning Tools Used for Budgetary Control

Budgetary control can be defined as preparing the budgets for Abeam consulting Ltd in

order to achieve the set targets by the company. It is prepared in order to measure the actual

performance of the company with the budgeted performance of the company. These budgets also

helps in knowing that where the extra cost has been allocated and how to eliminate the extra cost

from the department in order to earn higher profits for the company. These are various planning

tools used for budgetary tools are as follows-

Incremental Budgetary control

Incremental budgetary control prepared the budget on the basis of previous year's budget.

These are generally prepared in order to know measure the budgets with the actual performance of

Abeam consulting Ltd. The budget considers a percentage and adds that percentage in the previous

year budget to prepare the new budget for current period (de Campos, 2016). They are prepared in

order to know the changes in the current year's expenses as compared to past year's budget.

Advantages Disadvantages

It is simple to calculate incremental budgeting

and easy to implement in Abeam consulting

Budget does not takes into account various

expenses such as inflation rates, interest rates

01/05/19 Opening inventory of 40 units £3 each 120

12/05/19 Purchased 20 units @ £3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @£ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

30/05/19 Balance as on 30 may (4 units) 12

Under LIFO method, Abeam consulting Ltd is using LIFO method for the valuation of

closing inventory for the month of May. Under this method, it is assumed that the last purchased

goods are sold first and closing inventory is calculated at the cost of goods which is first purchased

by the company.

LO 3

P 4 Advantages and Disadvantages of Planning Tools Used for Budgetary Control

Budgetary control can be defined as preparing the budgets for Abeam consulting Ltd in

order to achieve the set targets by the company. It is prepared in order to measure the actual

performance of the company with the budgeted performance of the company. These budgets also

helps in knowing that where the extra cost has been allocated and how to eliminate the extra cost

from the department in order to earn higher profits for the company. These are various planning

tools used for budgetary tools are as follows-

Incremental Budgetary control

Incremental budgetary control prepared the budget on the basis of previous year's budget.

These are generally prepared in order to know measure the budgets with the actual performance of

Abeam consulting Ltd. The budget considers a percentage and adds that percentage in the previous

year budget to prepare the new budget for current period (de Campos, 2016). They are prepared in

order to know the changes in the current year's expenses as compared to past year's budget.

Advantages Disadvantages

It is simple to calculate incremental budgeting

and easy to implement in Abeam consulting

Budget does not takes into account various

expenses such as inflation rates, interest rates

Ltd.. etc.

The budget is useful in small and medium

companies where seldom changes occur.

It does not show true picture of current year's

budget because many expenses are not taken

into account.

Activity Based Budgeting

Activity Based Budgeting is the budget in which each and activity recorded in the company

are first analysed and than they are recorded in the budget. The preparation is rigorous activity as

compared to the other budgeting planning tools (Ohemeng, 2016). Every activity in Abeam

consulting Ltd is scrutinized properly in order to know in which department they are to be allocated

as per requirement of the department. It takes into account all expense such as inflation rates,

interest rates in order to properly allocate the expenses in the company.

Advantages Disadvantages

The budget takes into account all the expenses

and allocate the expenses as per the needs of

department.

It takes a lot time in scrutinizing each and every

activity in Abeam consulting Ltd.

The budget scrutinizes each and every activity in

Abeam consulting Ltd.

It needs professionals in order to scrutinize each

expense needs in various departments.

Zero Based Budgetary control

Zero Based Budgeting starts from the “Zero Base”. Under this method all the expenses are

justified by the managers in order to know that in which the expenses are to be allocated (Oraka,

2016). Each and every expense in Abeam consulting Ltd is to be justified that in which department

they are needed and what is the need to allocate in that particular department only.

Advantages Disadvantages

The budget justifies each and every expense

which eliminates the extra cost allocated to the

department.

It takes a lot of time in justifying each and every

activity in Abeam consulting Ltd.

Managers in Abeam consulting Ltd has to justify

each and every expense in the company.

It is not economical because each and every

expense in the company has to be justified.

LO 4

The budget is useful in small and medium

companies where seldom changes occur.

It does not show true picture of current year's

budget because many expenses are not taken

into account.

Activity Based Budgeting

Activity Based Budgeting is the budget in which each and activity recorded in the company

are first analysed and than they are recorded in the budget. The preparation is rigorous activity as

compared to the other budgeting planning tools (Ohemeng, 2016). Every activity in Abeam

consulting Ltd is scrutinized properly in order to know in which department they are to be allocated

as per requirement of the department. It takes into account all expense such as inflation rates,

interest rates in order to properly allocate the expenses in the company.

Advantages Disadvantages

The budget takes into account all the expenses

and allocate the expenses as per the needs of

department.

It takes a lot time in scrutinizing each and every

activity in Abeam consulting Ltd.

The budget scrutinizes each and every activity in

Abeam consulting Ltd.

It needs professionals in order to scrutinize each

expense needs in various departments.

Zero Based Budgetary control

Zero Based Budgeting starts from the “Zero Base”. Under this method all the expenses are

justified by the managers in order to know that in which the expenses are to be allocated (Oraka,

2016). Each and every expense in Abeam consulting Ltd is to be justified that in which department

they are needed and what is the need to allocate in that particular department only.

Advantages Disadvantages

The budget justifies each and every expense

which eliminates the extra cost allocated to the

department.

It takes a lot of time in justifying each and every

activity in Abeam consulting Ltd.

Managers in Abeam consulting Ltd has to justify

each and every expense in the company.

It is not economical because each and every

expense in the company has to be justified.

LO 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.