Investment Appraisal Techniques for ABC plc: A Financial Report

VerifiedAdded on 2023/01/13

|8

|1436

|93

Report

AI Summary

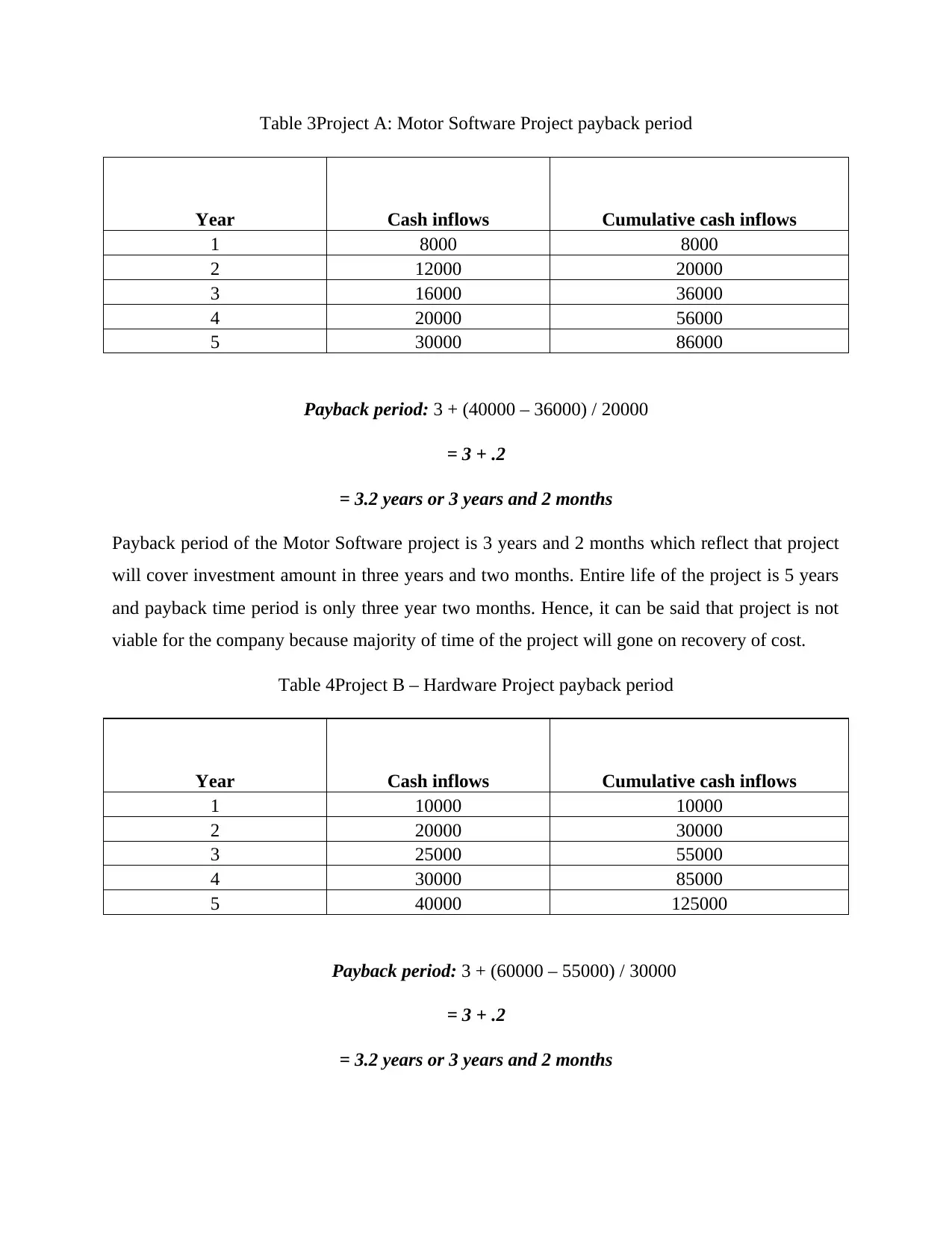

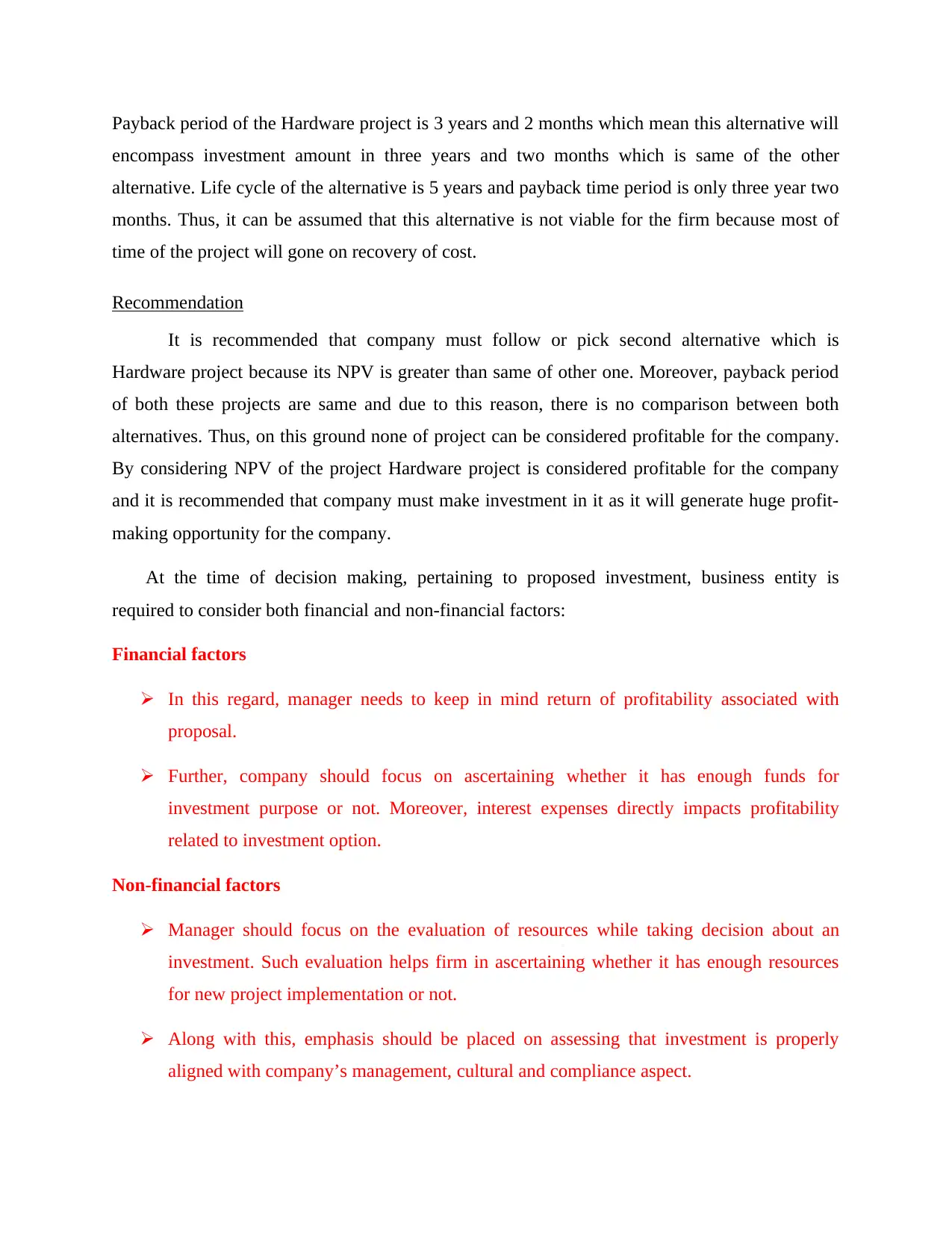

This report provides a financial analysis of two potential projects for ABC plc, focusing on investment appraisal techniques. It begins with an introduction to capital budgeting and the importance of decision-making in business organizations. The core of the report assesses the viability of each project (Motor Software and Hardware) using Net Present Value (NPV) and payback period methods. The NPV calculations show positive values for both projects, with the Hardware project having a higher NPV. The payback period analysis indicates that both projects recover their initial investment in 3.2 years. The report recommends the Hardware project due to its higher NPV, emphasizing the importance of considering both financial and non-financial factors in investment decisions. The report concludes by highlighting the significance of project evaluation methods for businesses, stressing the need for a comprehensive approach to ensure sound investment choices and maximize profitability. References to relevant academic sources are also included.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.