Management Accounting: Financial Decision Analysis Report

VerifiedAdded on 2020/05/28

|10

|1943

|33

Report

AI Summary

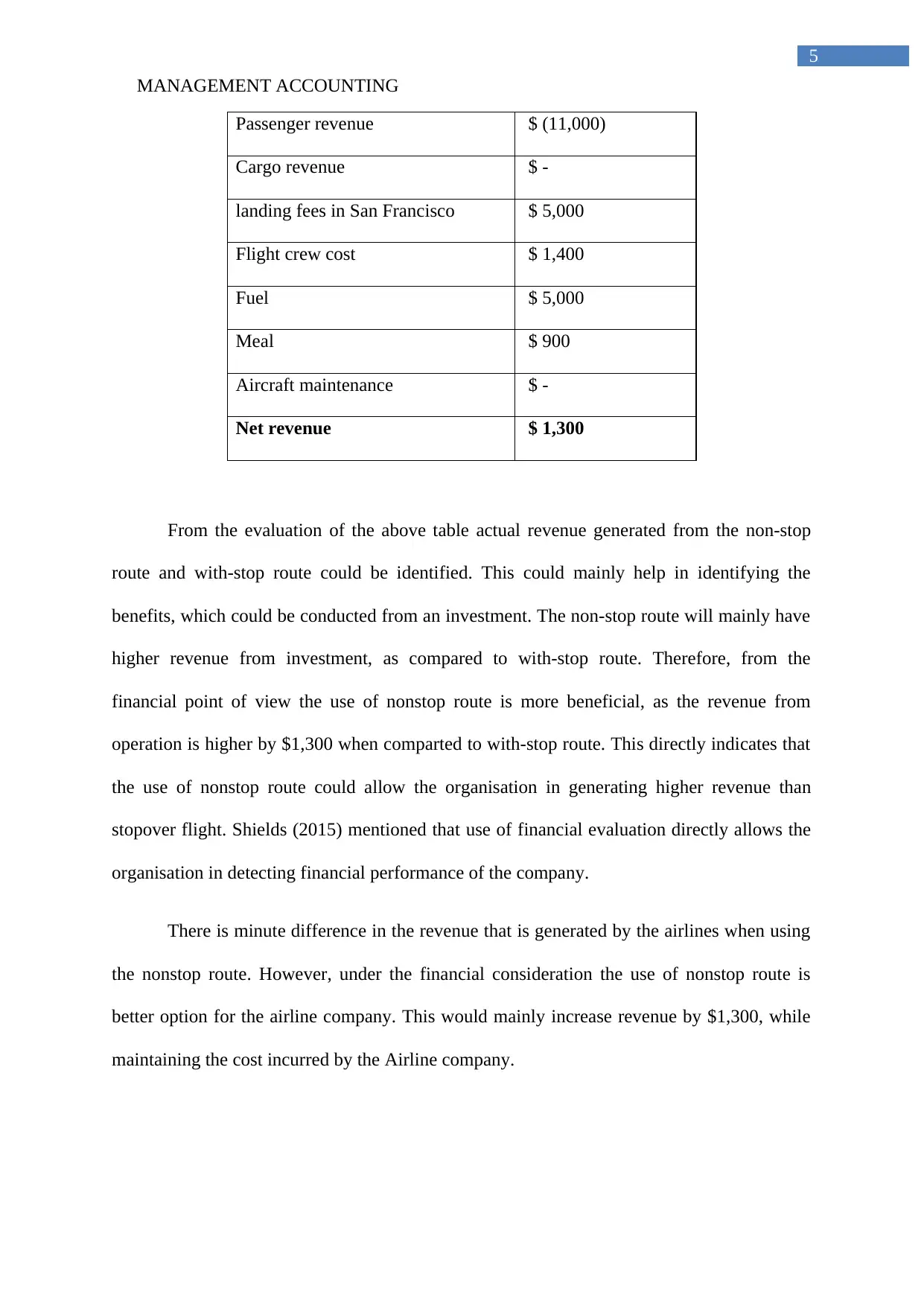

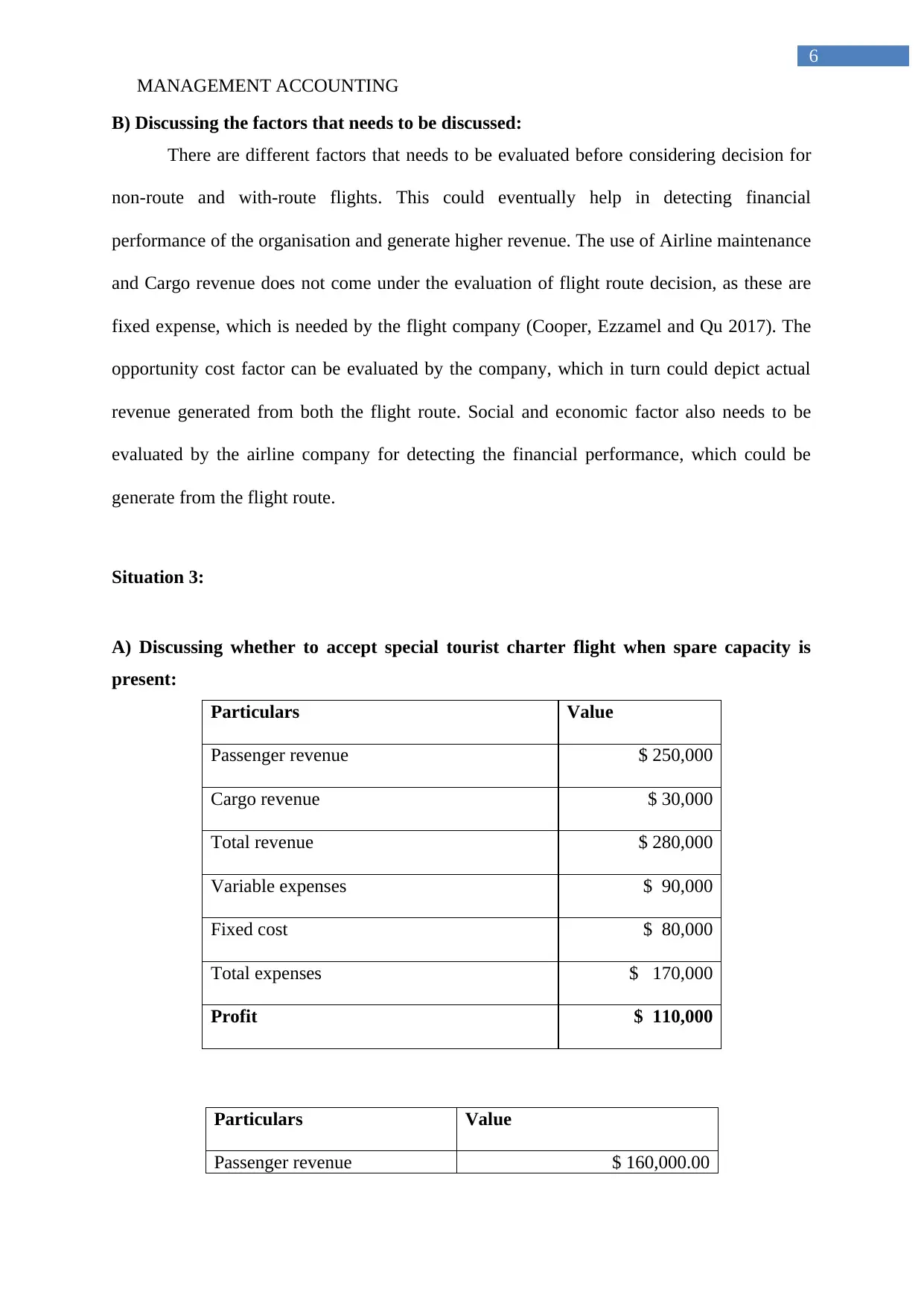

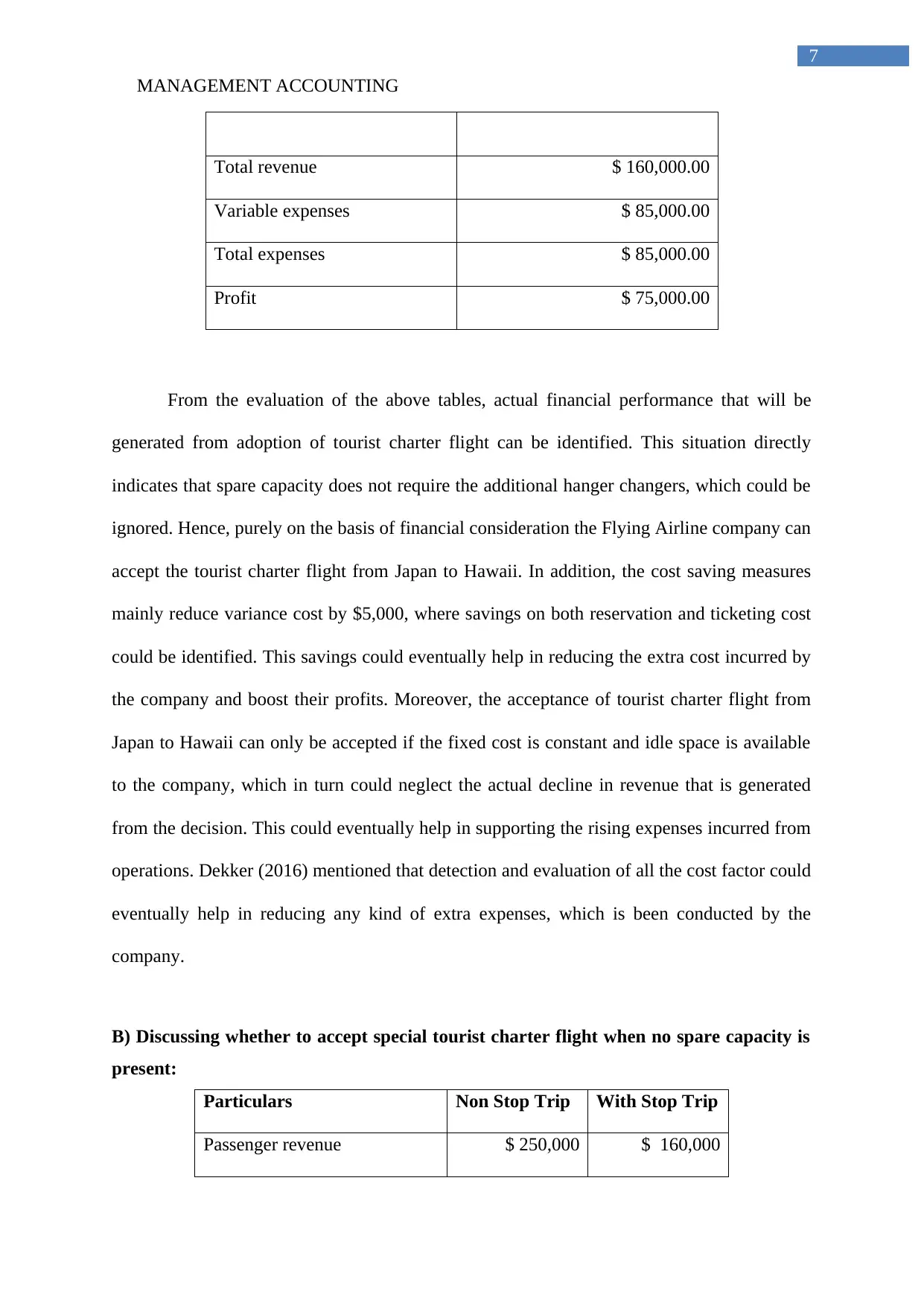

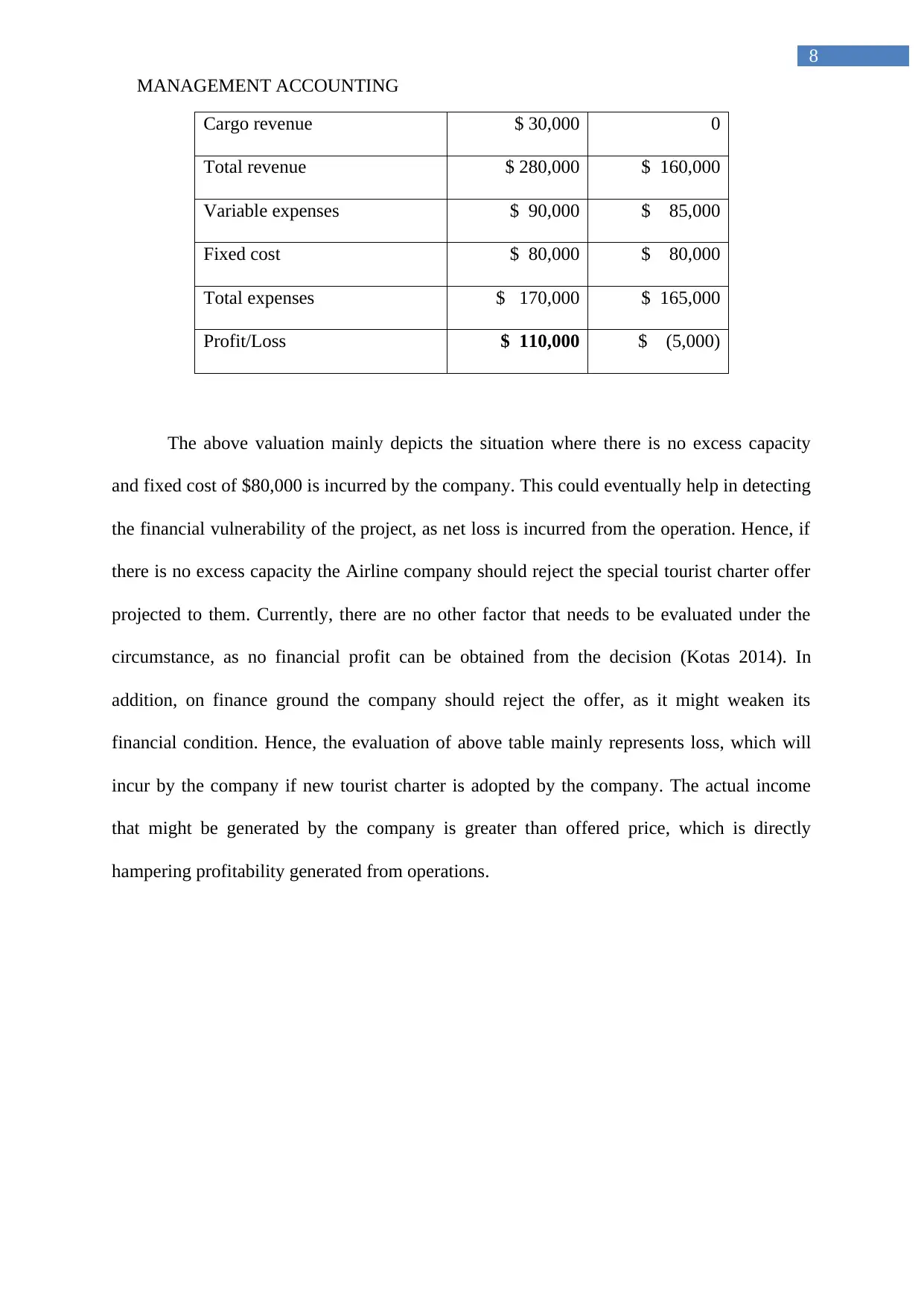

This management accounting report presents a detailed financial analysis of various scenarios within the airline industry. The report begins by evaluating the decision of whether to replace an old truck loader with a new one, calculating differential costs to determine the most cost-effective option. It then analyzes two flight route scenarios: a non-stop route versus a route with a stopover, assessing passenger and cargo revenue, landing fees, and operational costs to identify the most financially beneficial choice. Finally, the report examines the acceptance of special tourist charter flights, considering situations with and without spare capacity, to determine the impact on profit and loss. The analysis includes calculations of revenue, variable expenses, fixed costs, and profit, providing a comprehensive understanding of financial decision-making in the context of airline management. The report references several academic sources to support its findings.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.