Financial Decision Making Report: Financial Analysis of Acquisition

VerifiedAdded on 2023/01/17

|17

|4280

|87

Report

AI Summary

This report provides a comprehensive financial analysis of a potential acquisition, likely focusing on Starbucks. It begins with an executive summary and an industry review of the coffee sector, highlighting its growth and opportunities. The core of the report involves a detailed performance analysis, including income statements, balance sheets, and cash flow analysis of a target company (Roast Ltd). Key financial ratios like profitability, liquidity, and solvency ratios are evaluated to assess the financial health of the target. The report then delves into investment appraisal techniques, such as payback period, accounting rate of return, net present value, and discusses potential sources of funding for the acquisition. The analysis includes a working capital analysis and a discussion on dividend policy. The financial statements are used to assess the company's performance and make financial decisions. The report concludes with an assessment of the financial position of the company and its potential for acquisition, making recommendations based on the financial data provided. This report is a valuable resource for students studying finance and business, offering insights into real-world financial decision-making processes.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

PART-1- Industry review................................................................................................................3

PART-2: Performance analysis .......................................................................................................4

2.1 Statement of the income statement .......................................................................................4

2.2 Statement of balance sheet or financial position....................................................................5

2.3 cash flow analysis .................................................................................................................7

PART-3............................................................................................................................................9

3.1 Investment appraisal..............................................................................................................9

3.2 Sources through which funds could be raised .....................................................................12

REFERENCES................................................................................................................................1

EXECUTIVE SUMMARY.............................................................................................................3

PART-1- Industry review................................................................................................................3

PART-2: Performance analysis .......................................................................................................4

2.1 Statement of the income statement .......................................................................................4

2.2 Statement of balance sheet or financial position....................................................................5

2.3 cash flow analysis .................................................................................................................7

PART-3............................................................................................................................................9

3.1 Investment appraisal..............................................................................................................9

3.2 Sources through which funds could be raised .....................................................................12

REFERENCES................................................................................................................................1

EXECUTIVE SUMMARY

Financial decision making is defined as the deciding a single option form various

different alternative relating to the financial decisions of the company. The finance is the most

crucial part in the business because without finance no work can be done and it is very difficult

to work without money. Hence, it is very necessary for the company to select the cheapest source

of finance so that all the operations of the company can be carried on by the company in

successful manner. The present report is based on the analysis that whether Starbucks need to

acquire its target company or not. For analysing the attractiveness of the acquisition, the

company analyses the financial statements of the company in order to ascertain its financial

position and the financial performance of the target company. Further the report has discussed

the investment appraisal options for the acquisition with the help of the analysis of different

investment appraisal criteria. These criterion are like payback period, accounting rate of return,

net present value and many others. In the end the discussion held was on the different sources of

finance. This is very necessary because of the fact that finance need to be taken from outside so

it is very essential to have low cost of borrowing money form others.

PART-1- Industry review

The coffee industry has gained the success of 20 consecutive years and is still growing

and booming industry. The total estimated contribution of coffee industry in the Gross Value

Added to the GDP of UK was £3.7 billion in 2017. The growth rate of UK coffee industry was

around 7 % from 2012 to 2017. Also, this industry provides employment opportunities for the

country and the employees in the coffee industry was around 133,965 in the year 2017 (UK

coffee market analysis published, 2018). From the different survey it was outlined that the on an

average approximately 95 million of cups are consumed on daily basis in UK. This industry is

performing exceptionally well as the industry and the profits from it is growing to a great extent.

But then also there are many different opportunities and challenges with the industry.

The major opportunity for the coffee industry is the changes taking place in the

technology. This is a very crucial and important opportunity which needs to be undertaken by the

coffee industry. This is majorly due to the fact that the technology will assist the coffee industry

in simplifying the work of producing the coffee and to improve the quality of the product and

Financial decision making is defined as the deciding a single option form various

different alternative relating to the financial decisions of the company. The finance is the most

crucial part in the business because without finance no work can be done and it is very difficult

to work without money. Hence, it is very necessary for the company to select the cheapest source

of finance so that all the operations of the company can be carried on by the company in

successful manner. The present report is based on the analysis that whether Starbucks need to

acquire its target company or not. For analysing the attractiveness of the acquisition, the

company analyses the financial statements of the company in order to ascertain its financial

position and the financial performance of the target company. Further the report has discussed

the investment appraisal options for the acquisition with the help of the analysis of different

investment appraisal criteria. These criterion are like payback period, accounting rate of return,

net present value and many others. In the end the discussion held was on the different sources of

finance. This is very necessary because of the fact that finance need to be taken from outside so

it is very essential to have low cost of borrowing money form others.

PART-1- Industry review

The coffee industry has gained the success of 20 consecutive years and is still growing

and booming industry. The total estimated contribution of coffee industry in the Gross Value

Added to the GDP of UK was £3.7 billion in 2017. The growth rate of UK coffee industry was

around 7 % from 2012 to 2017. Also, this industry provides employment opportunities for the

country and the employees in the coffee industry was around 133,965 in the year 2017 (UK

coffee market analysis published, 2018). From the different survey it was outlined that the on an

average approximately 95 million of cups are consumed on daily basis in UK. This industry is

performing exceptionally well as the industry and the profits from it is growing to a great extent.

But then also there are many different opportunities and challenges with the industry.

The major opportunity for the coffee industry is the changes taking place in the

technology. This is a very crucial and important opportunity which needs to be undertaken by the

coffee industry. This is majorly due to the fact that the technology will assist the coffee industry

in simplifying the work of producing the coffee and to improve the quality of the product and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

services. Also, this is an opportunity because of the fact that the use of technology reduces the

human effort and this can be used in some other place.

The major challenge for the coffee industry is that the consumer taste and preferences and

the perception of the consumers relating to coffee and its consumption is fast changing. Thus, it

is very crucial for the coffee industry in UK to continuously monitor the needs and changing

expectation of the consumers in order to earn more of the profits and grow and develop the

industry.

PART-2: Performance analysis

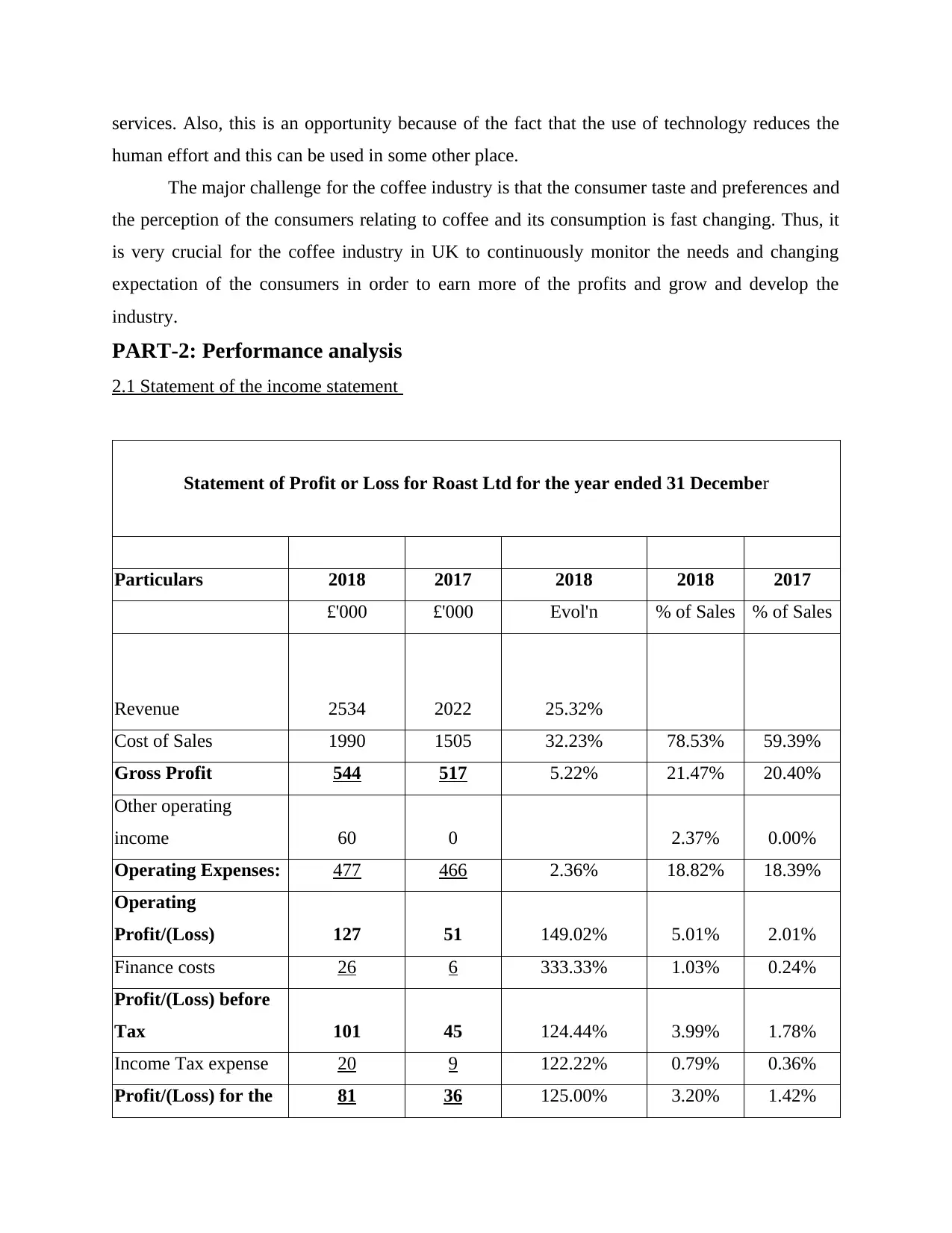

2.1 Statement of the income statement

Statement of Profit or Loss for Roast Ltd for the year ended 31 December

Particulars 2018 2017 2018 2018 2017

£'000 £'000 Evol'n % of Sales % of Sales

Revenue 2534 2022 25.32%

Cost of Sales 1990 1505 32.23% 78.53% 59.39%

Gross Profit 544 517 5.22% 21.47% 20.40%

Other operating

income 60 0 2.37% 0.00%

Operating Expenses: 477 466 2.36% 18.82% 18.39%

Operating

Profit/(Loss) 127 51 149.02% 5.01% 2.01%

Finance costs 26 6 333.33% 1.03% 0.24%

Profit/(Loss) before

Tax 101 45 124.44% 3.99% 1.78%

Income Tax expense 20 9 122.22% 0.79% 0.36%

Profit/(Loss) for the 81 36 125.00% 3.20% 1.42%

human effort and this can be used in some other place.

The major challenge for the coffee industry is that the consumer taste and preferences and

the perception of the consumers relating to coffee and its consumption is fast changing. Thus, it

is very crucial for the coffee industry in UK to continuously monitor the needs and changing

expectation of the consumers in order to earn more of the profits and grow and develop the

industry.

PART-2: Performance analysis

2.1 Statement of the income statement

Statement of Profit or Loss for Roast Ltd for the year ended 31 December

Particulars 2018 2017 2018 2018 2017

£'000 £'000 Evol'n % of Sales % of Sales

Revenue 2534 2022 25.32%

Cost of Sales 1990 1505 32.23% 78.53% 59.39%

Gross Profit 544 517 5.22% 21.47% 20.40%

Other operating

income 60 0 2.37% 0.00%

Operating Expenses: 477 466 2.36% 18.82% 18.39%

Operating

Profit/(Loss) 127 51 149.02% 5.01% 2.01%

Finance costs 26 6 333.33% 1.03% 0.24%

Profit/(Loss) before

Tax 101 45 124.44% 3.99% 1.78%

Income Tax expense 20 9 122.22% 0.79% 0.36%

Profit/(Loss) for the 81 36 125.00% 3.20% 1.42%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

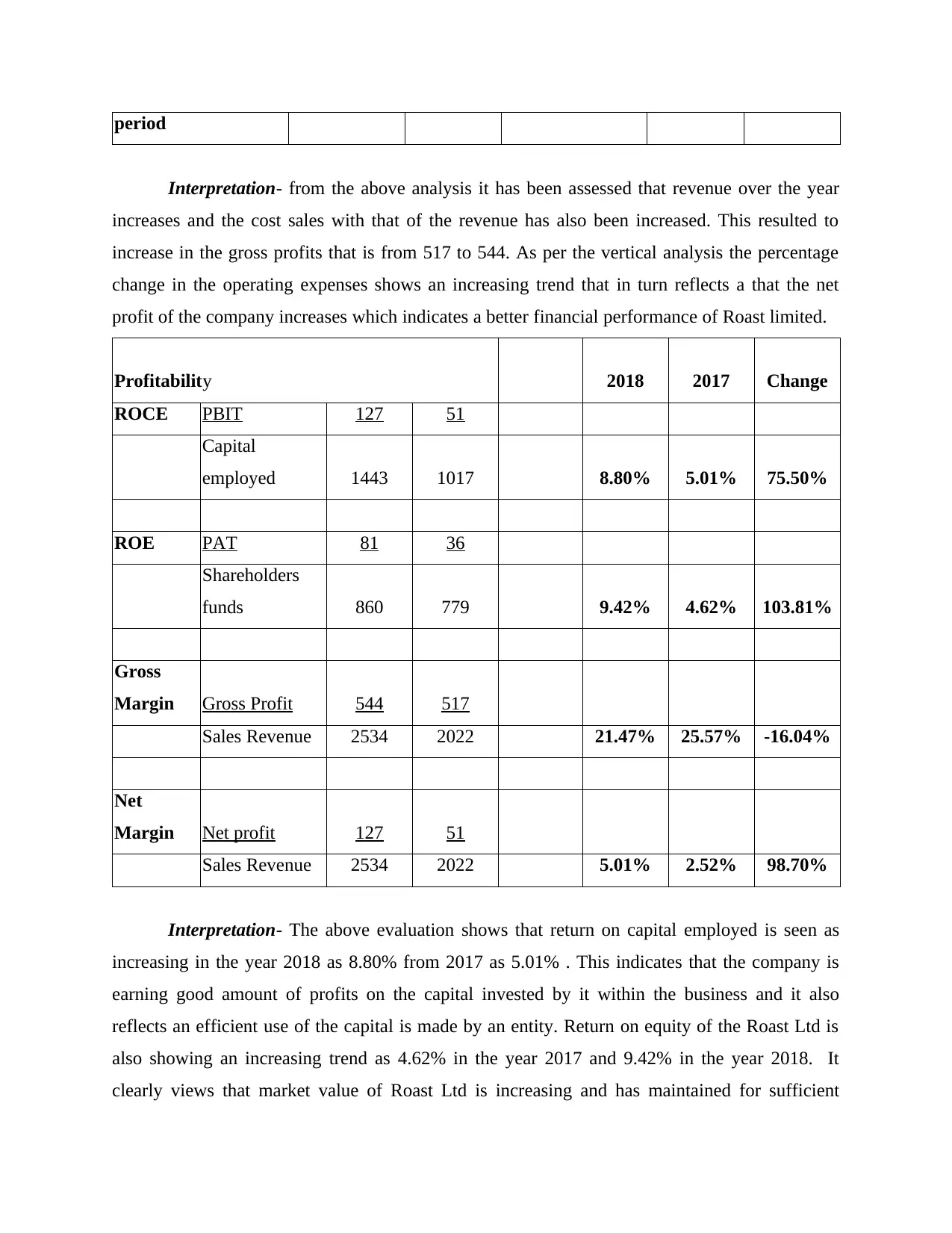

period

Interpretation- from the above analysis it has been assessed that revenue over the year

increases and the cost sales with that of the revenue has also been increased. This resulted to

increase in the gross profits that is from 517 to 544. As per the vertical analysis the percentage

change in the operating expenses shows an increasing trend that in turn reflects a that the net

profit of the company increases which indicates a better financial performance of Roast limited.

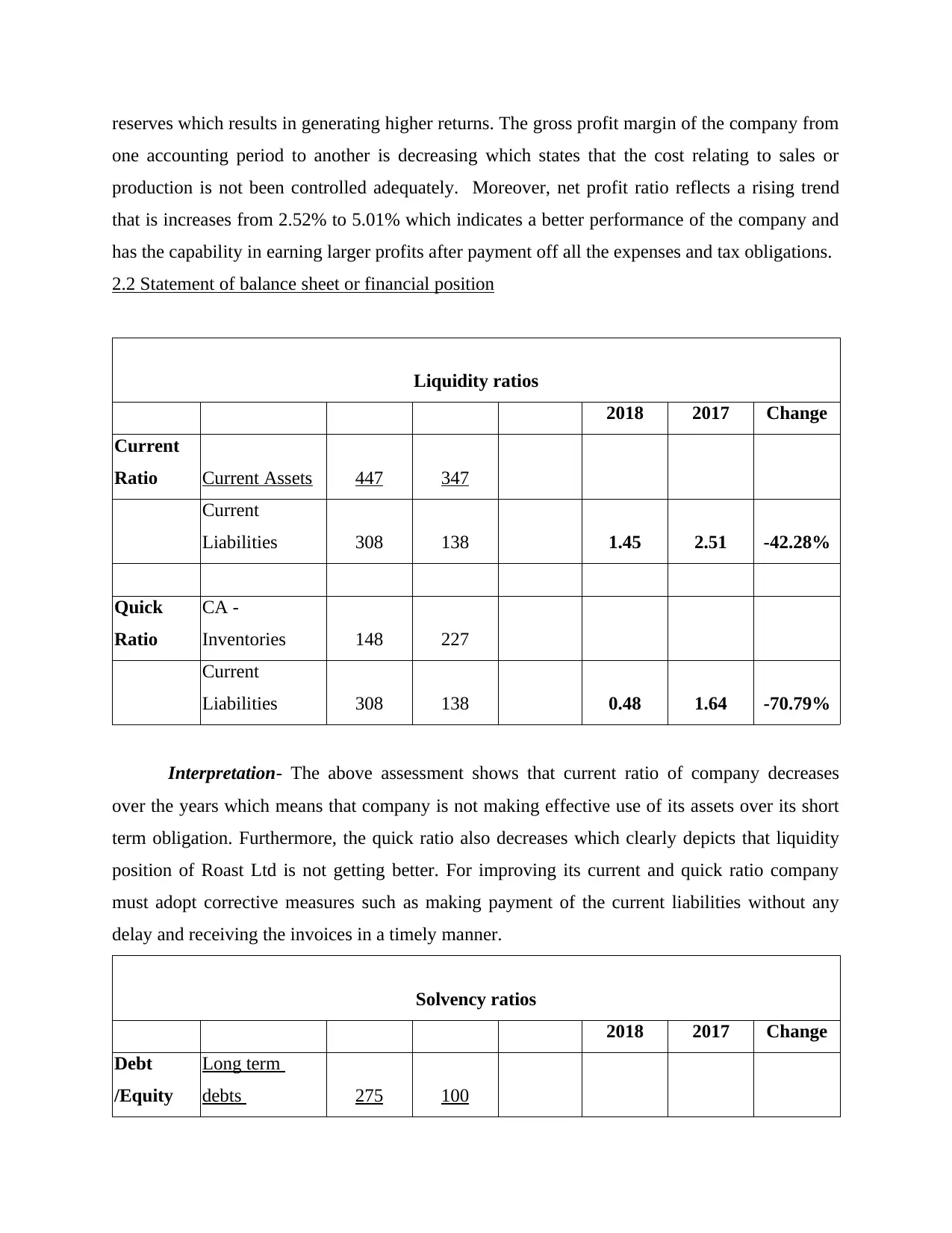

Profitability 2018 2017 Change

ROCE PBIT 127 51

Capital

employed 1443 1017 8.80% 5.01% 75.50%

ROE PAT 81 36

Shareholders

funds 860 779 9.42% 4.62% 103.81%

Gross

Margin Gross Profit 544 517

Sales Revenue 2534 2022 21.47% 25.57% -16.04%

Net

Margin Net profit 127 51

Sales Revenue 2534 2022 5.01% 2.52% 98.70%

Interpretation- The above evaluation shows that return on capital employed is seen as

increasing in the year 2018 as 8.80% from 2017 as 5.01% . This indicates that the company is

earning good amount of profits on the capital invested by it within the business and it also

reflects an efficient use of the capital is made by an entity. Return on equity of the Roast Ltd is

also showing an increasing trend as 4.62% in the year 2017 and 9.42% in the year 2018. It

clearly views that market value of Roast Ltd is increasing and has maintained for sufficient

Interpretation- from the above analysis it has been assessed that revenue over the year

increases and the cost sales with that of the revenue has also been increased. This resulted to

increase in the gross profits that is from 517 to 544. As per the vertical analysis the percentage

change in the operating expenses shows an increasing trend that in turn reflects a that the net

profit of the company increases which indicates a better financial performance of Roast limited.

Profitability 2018 2017 Change

ROCE PBIT 127 51

Capital

employed 1443 1017 8.80% 5.01% 75.50%

ROE PAT 81 36

Shareholders

funds 860 779 9.42% 4.62% 103.81%

Gross

Margin Gross Profit 544 517

Sales Revenue 2534 2022 21.47% 25.57% -16.04%

Net

Margin Net profit 127 51

Sales Revenue 2534 2022 5.01% 2.52% 98.70%

Interpretation- The above evaluation shows that return on capital employed is seen as

increasing in the year 2018 as 8.80% from 2017 as 5.01% . This indicates that the company is

earning good amount of profits on the capital invested by it within the business and it also

reflects an efficient use of the capital is made by an entity. Return on equity of the Roast Ltd is

also showing an increasing trend as 4.62% in the year 2017 and 9.42% in the year 2018. It

clearly views that market value of Roast Ltd is increasing and has maintained for sufficient

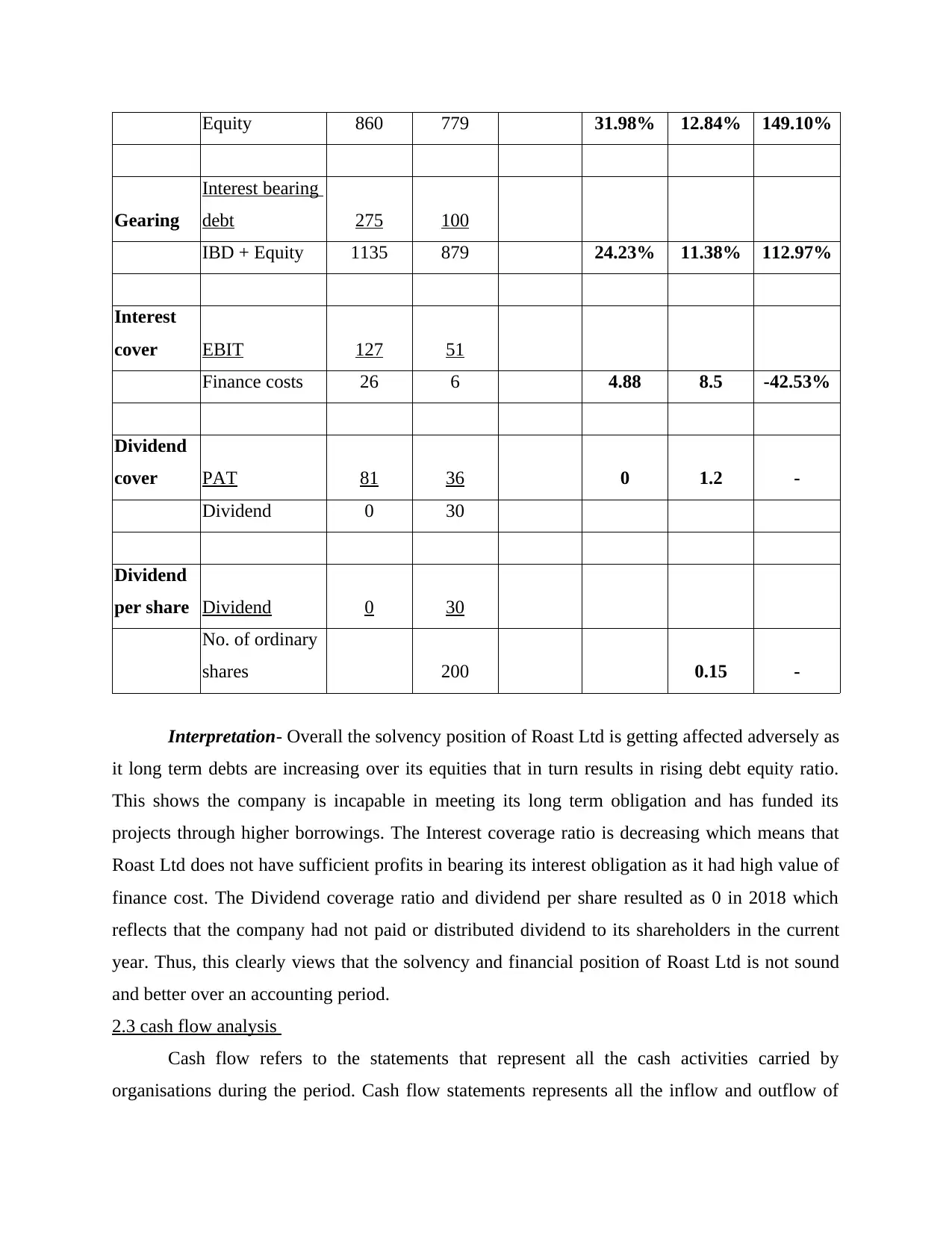

reserves which results in generating higher returns. The gross profit margin of the company from

one accounting period to another is decreasing which states that the cost relating to sales or

production is not been controlled adequately. Moreover, net profit ratio reflects a rising trend

that is increases from 2.52% to 5.01% which indicates a better performance of the company and

has the capability in earning larger profits after payment off all the expenses and tax obligations.

2.2 Statement of balance sheet or financial position

Liquidity ratios

2018 2017 Change

Current

Ratio Current Assets 447 347

Current

Liabilities 308 138 1.45 2.51 -42.28%

Quick

Ratio

CA -

Inventories 148 227

Current

Liabilities 308 138 0.48 1.64 -70.79%

Interpretation- The above assessment shows that current ratio of company decreases

over the years which means that company is not making effective use of its assets over its short

term obligation. Furthermore, the quick ratio also decreases which clearly depicts that liquidity

position of Roast Ltd is not getting better. For improving its current and quick ratio company

must adopt corrective measures such as making payment of the current liabilities without any

delay and receiving the invoices in a timely manner.

Solvency ratios

2018 2017 Change

Debt

/Equity

Long term

debts 275 100

one accounting period to another is decreasing which states that the cost relating to sales or

production is not been controlled adequately. Moreover, net profit ratio reflects a rising trend

that is increases from 2.52% to 5.01% which indicates a better performance of the company and

has the capability in earning larger profits after payment off all the expenses and tax obligations.

2.2 Statement of balance sheet or financial position

Liquidity ratios

2018 2017 Change

Current

Ratio Current Assets 447 347

Current

Liabilities 308 138 1.45 2.51 -42.28%

Quick

Ratio

CA -

Inventories 148 227

Current

Liabilities 308 138 0.48 1.64 -70.79%

Interpretation- The above assessment shows that current ratio of company decreases

over the years which means that company is not making effective use of its assets over its short

term obligation. Furthermore, the quick ratio also decreases which clearly depicts that liquidity

position of Roast Ltd is not getting better. For improving its current and quick ratio company

must adopt corrective measures such as making payment of the current liabilities without any

delay and receiving the invoices in a timely manner.

Solvency ratios

2018 2017 Change

Debt

/Equity

Long term

debts 275 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

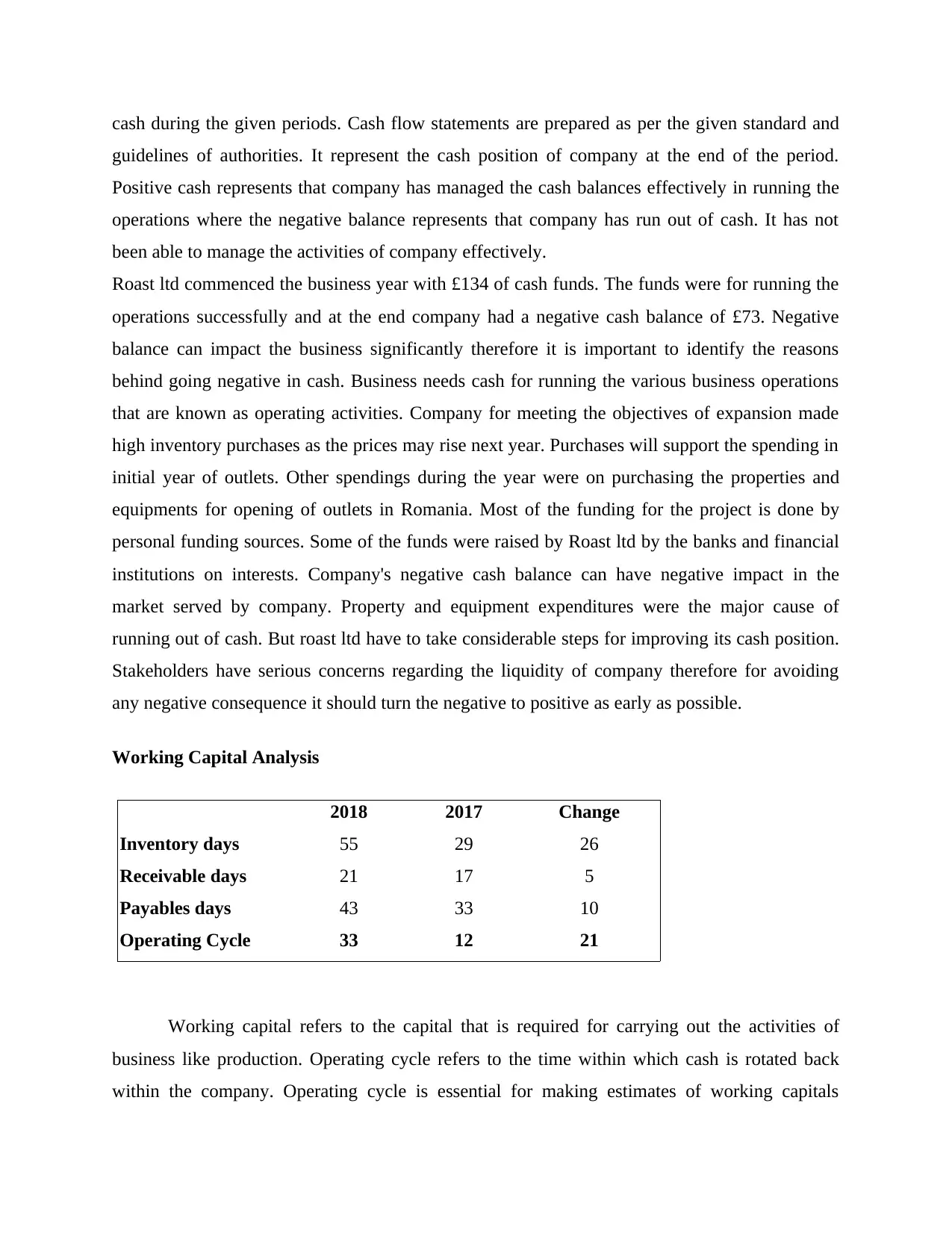

Equity 860 779 31.98% 12.84% 149.10%

Gearing

Interest bearing

debt 275 100

IBD + Equity 1135 879 24.23% 11.38% 112.97%

Interest

cover EBIT 127 51

Finance costs 26 6 4.88 8.5 -42.53%

Dividend

cover PAT 81 36 0 1.2 -

Dividend 0 30

Dividend

per share Dividend 0 30

No. of ordinary

shares 200 0.15 -

Interpretation- Overall the solvency position of Roast Ltd is getting affected adversely as

it long term debts are increasing over its equities that in turn results in rising debt equity ratio.

This shows the company is incapable in meeting its long term obligation and has funded its

projects through higher borrowings. The Interest coverage ratio is decreasing which means that

Roast Ltd does not have sufficient profits in bearing its interest obligation as it had high value of

finance cost. The Dividend coverage ratio and dividend per share resulted as 0 in 2018 which

reflects that the company had not paid or distributed dividend to its shareholders in the current

year. Thus, this clearly views that the solvency and financial position of Roast Ltd is not sound

and better over an accounting period.

2.3 cash flow analysis

Cash flow refers to the statements that represent all the cash activities carried by

organisations during the period. Cash flow statements represents all the inflow and outflow of

Gearing

Interest bearing

debt 275 100

IBD + Equity 1135 879 24.23% 11.38% 112.97%

Interest

cover EBIT 127 51

Finance costs 26 6 4.88 8.5 -42.53%

Dividend

cover PAT 81 36 0 1.2 -

Dividend 0 30

Dividend

per share Dividend 0 30

No. of ordinary

shares 200 0.15 -

Interpretation- Overall the solvency position of Roast Ltd is getting affected adversely as

it long term debts are increasing over its equities that in turn results in rising debt equity ratio.

This shows the company is incapable in meeting its long term obligation and has funded its

projects through higher borrowings. The Interest coverage ratio is decreasing which means that

Roast Ltd does not have sufficient profits in bearing its interest obligation as it had high value of

finance cost. The Dividend coverage ratio and dividend per share resulted as 0 in 2018 which

reflects that the company had not paid or distributed dividend to its shareholders in the current

year. Thus, this clearly views that the solvency and financial position of Roast Ltd is not sound

and better over an accounting period.

2.3 cash flow analysis

Cash flow refers to the statements that represent all the cash activities carried by

organisations during the period. Cash flow statements represents all the inflow and outflow of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash during the given periods. Cash flow statements are prepared as per the given standard and

guidelines of authorities. It represent the cash position of company at the end of the period.

Positive cash represents that company has managed the cash balances effectively in running the

operations where the negative balance represents that company has run out of cash. It has not

been able to manage the activities of company effectively.

Roast ltd commenced the business year with £134 of cash funds. The funds were for running the

operations successfully and at the end company had a negative cash balance of £73. Negative

balance can impact the business significantly therefore it is important to identify the reasons

behind going negative in cash. Business needs cash for running the various business operations

that are known as operating activities. Company for meeting the objectives of expansion made

high inventory purchases as the prices may rise next year. Purchases will support the spending in

initial year of outlets. Other spendings during the year were on purchasing the properties and

equipments for opening of outlets in Romania. Most of the funding for the project is done by

personal funding sources. Some of the funds were raised by Roast ltd by the banks and financial

institutions on interests. Company's negative cash balance can have negative impact in the

market served by company. Property and equipment expenditures were the major cause of

running out of cash. But roast ltd have to take considerable steps for improving its cash position.

Stakeholders have serious concerns regarding the liquidity of company therefore for avoiding

any negative consequence it should turn the negative to positive as early as possible.

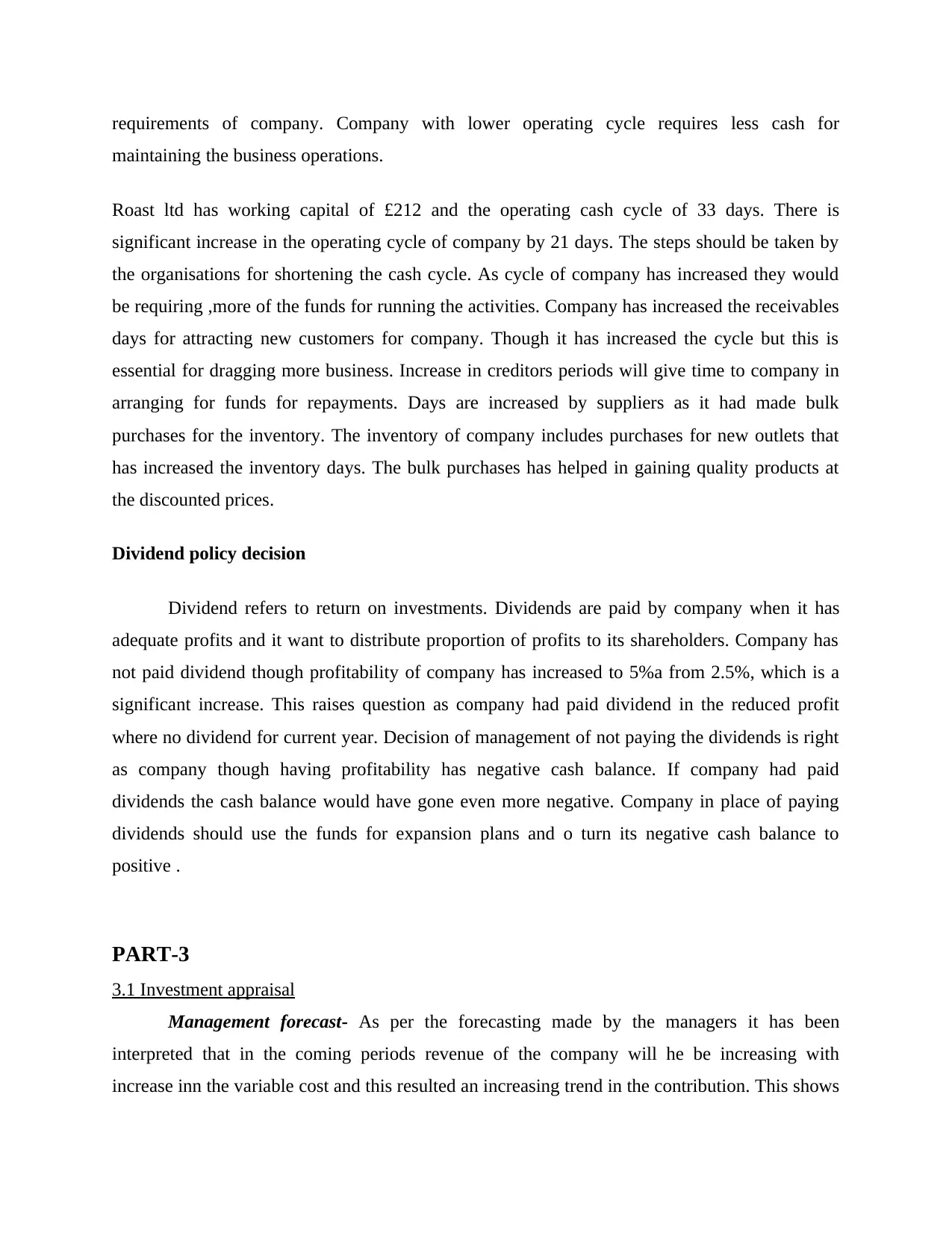

Working Capital Analysis

2018 2017 Change

Inventory days 55 29 26

Receivable days 21 17 5

Payables days 43 33 10

Operating Cycle 33 12 21

Working capital refers to the capital that is required for carrying out the activities of

business like production. Operating cycle refers to the time within which cash is rotated back

within the company. Operating cycle is essential for making estimates of working capitals

guidelines of authorities. It represent the cash position of company at the end of the period.

Positive cash represents that company has managed the cash balances effectively in running the

operations where the negative balance represents that company has run out of cash. It has not

been able to manage the activities of company effectively.

Roast ltd commenced the business year with £134 of cash funds. The funds were for running the

operations successfully and at the end company had a negative cash balance of £73. Negative

balance can impact the business significantly therefore it is important to identify the reasons

behind going negative in cash. Business needs cash for running the various business operations

that are known as operating activities. Company for meeting the objectives of expansion made

high inventory purchases as the prices may rise next year. Purchases will support the spending in

initial year of outlets. Other spendings during the year were on purchasing the properties and

equipments for opening of outlets in Romania. Most of the funding for the project is done by

personal funding sources. Some of the funds were raised by Roast ltd by the banks and financial

institutions on interests. Company's negative cash balance can have negative impact in the

market served by company. Property and equipment expenditures were the major cause of

running out of cash. But roast ltd have to take considerable steps for improving its cash position.

Stakeholders have serious concerns regarding the liquidity of company therefore for avoiding

any negative consequence it should turn the negative to positive as early as possible.

Working Capital Analysis

2018 2017 Change

Inventory days 55 29 26

Receivable days 21 17 5

Payables days 43 33 10

Operating Cycle 33 12 21

Working capital refers to the capital that is required for carrying out the activities of

business like production. Operating cycle refers to the time within which cash is rotated back

within the company. Operating cycle is essential for making estimates of working capitals

requirements of company. Company with lower operating cycle requires less cash for

maintaining the business operations.

Roast ltd has working capital of £212 and the operating cash cycle of 33 days. There is

significant increase in the operating cycle of company by 21 days. The steps should be taken by

the organisations for shortening the cash cycle. As cycle of company has increased they would

be requiring ,more of the funds for running the activities. Company has increased the receivables

days for attracting new customers for company. Though it has increased the cycle but this is

essential for dragging more business. Increase in creditors periods will give time to company in

arranging for funds for repayments. Days are increased by suppliers as it had made bulk

purchases for the inventory. The inventory of company includes purchases for new outlets that

has increased the inventory days. The bulk purchases has helped in gaining quality products at

the discounted prices.

Dividend policy decision

Dividend refers to return on investments. Dividends are paid by company when it has

adequate profits and it want to distribute proportion of profits to its shareholders. Company has

not paid dividend though profitability of company has increased to 5%a from 2.5%, which is a

significant increase. This raises question as company had paid dividend in the reduced profit

where no dividend for current year. Decision of management of not paying the dividends is right

as company though having profitability has negative cash balance. If company had paid

dividends the cash balance would have gone even more negative. Company in place of paying

dividends should use the funds for expansion plans and o turn its negative cash balance to

positive .

PART-3

3.1 Investment appraisal

Management forecast- As per the forecasting made by the managers it has been

interpreted that in the coming periods revenue of the company will he be increasing with

increase inn the variable cost and this resulted an increasing trend in the contribution. This shows

maintaining the business operations.

Roast ltd has working capital of £212 and the operating cash cycle of 33 days. There is

significant increase in the operating cycle of company by 21 days. The steps should be taken by

the organisations for shortening the cash cycle. As cycle of company has increased they would

be requiring ,more of the funds for running the activities. Company has increased the receivables

days for attracting new customers for company. Though it has increased the cycle but this is

essential for dragging more business. Increase in creditors periods will give time to company in

arranging for funds for repayments. Days are increased by suppliers as it had made bulk

purchases for the inventory. The inventory of company includes purchases for new outlets that

has increased the inventory days. The bulk purchases has helped in gaining quality products at

the discounted prices.

Dividend policy decision

Dividend refers to return on investments. Dividends are paid by company when it has

adequate profits and it want to distribute proportion of profits to its shareholders. Company has

not paid dividend though profitability of company has increased to 5%a from 2.5%, which is a

significant increase. This raises question as company had paid dividend in the reduced profit

where no dividend for current year. Decision of management of not paying the dividends is right

as company though having profitability has negative cash balance. If company had paid

dividends the cash balance would have gone even more negative. Company in place of paying

dividends should use the funds for expansion plans and o turn its negative cash balance to

positive .

PART-3

3.1 Investment appraisal

Management forecast- As per the forecasting made by the managers it has been

interpreted that in the coming periods revenue of the company will he be increasing with

increase inn the variable cost and this resulted an increasing trend in the contribution. This shows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that the profits of the company will also be increasing in the coming 5 years that in turn reflects

growing success in execution of the projects could be gained by Firm.

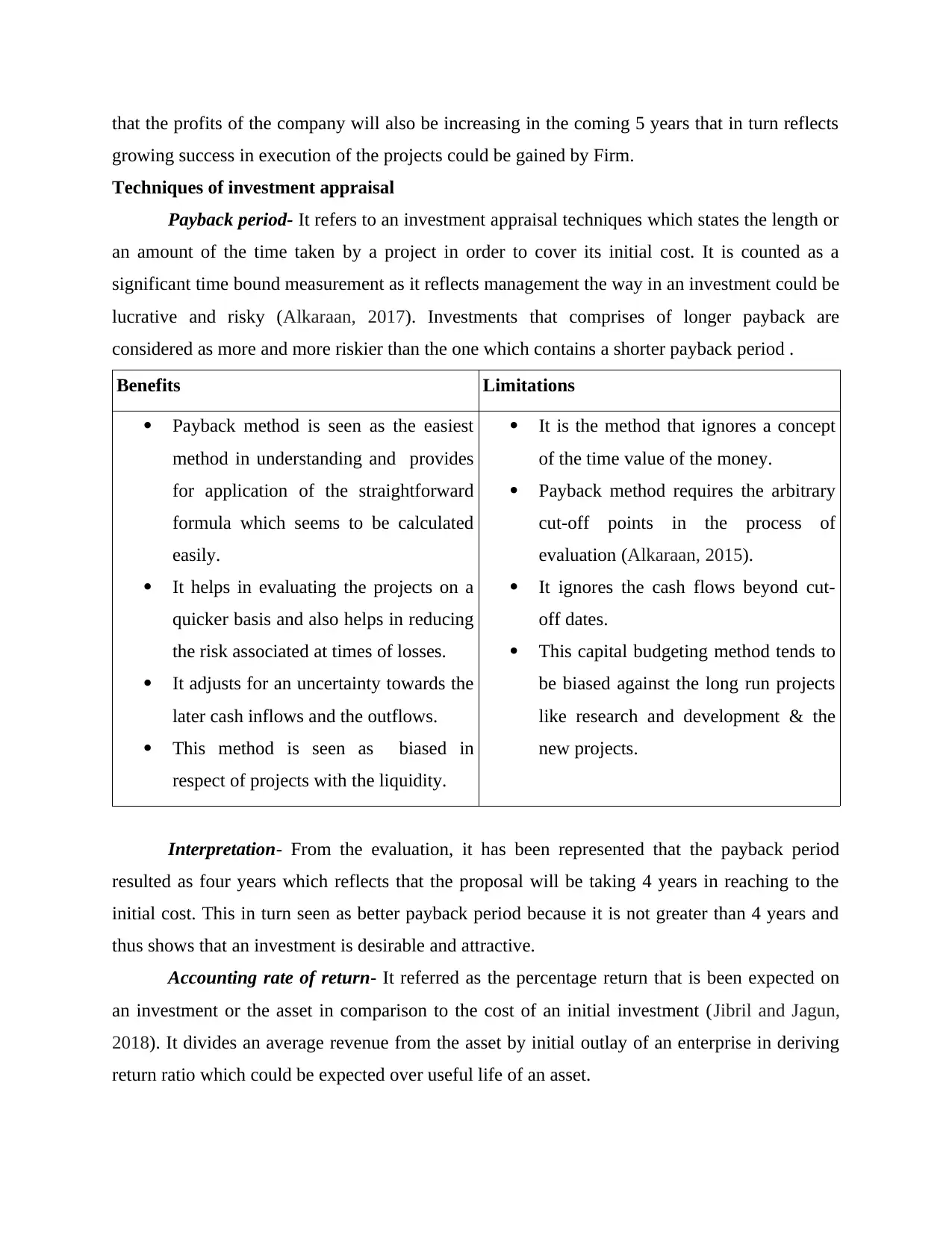

Techniques of investment appraisal

Payback period- It refers to an investment appraisal techniques which states the length or

an amount of the time taken by a project in order to cover its initial cost. It is counted as a

significant time bound measurement as it reflects management the way in an investment could be

lucrative and risky (Alkaraan, 2017). Investments that comprises of longer payback are

considered as more and more riskier than the one which contains a shorter payback period .

Benefits Limitations

Payback method is seen as the easiest

method in understanding and provides

for application of the straightforward

formula which seems to be calculated

easily.

It helps in evaluating the projects on a

quicker basis and also helps in reducing

the risk associated at times of losses.

It adjusts for an uncertainty towards the

later cash inflows and the outflows.

This method is seen as biased in

respect of projects with the liquidity.

It is the method that ignores a concept

of the time value of the money.

Payback method requires the arbitrary

cut-off points in the process of

evaluation (Alkaraan, 2015).

It ignores the cash flows beyond cut-

off dates.

This capital budgeting method tends to

be biased against the long run projects

like research and development & the

new projects.

Interpretation- From the evaluation, it has been represented that the payback period

resulted as four years which reflects that the proposal will be taking 4 years in reaching to the

initial cost. This in turn seen as better payback period because it is not greater than 4 years and

thus shows that an investment is desirable and attractive.

Accounting rate of return- It referred as the percentage return that is been expected on

an investment or the asset in comparison to the cost of an initial investment (Jibril and Jagun,

2018). It divides an average revenue from the asset by initial outlay of an enterprise in deriving

return ratio which could be expected over useful life of an asset.

growing success in execution of the projects could be gained by Firm.

Techniques of investment appraisal

Payback period- It refers to an investment appraisal techniques which states the length or

an amount of the time taken by a project in order to cover its initial cost. It is counted as a

significant time bound measurement as it reflects management the way in an investment could be

lucrative and risky (Alkaraan, 2017). Investments that comprises of longer payback are

considered as more and more riskier than the one which contains a shorter payback period .

Benefits Limitations

Payback method is seen as the easiest

method in understanding and provides

for application of the straightforward

formula which seems to be calculated

easily.

It helps in evaluating the projects on a

quicker basis and also helps in reducing

the risk associated at times of losses.

It adjusts for an uncertainty towards the

later cash inflows and the outflows.

This method is seen as biased in

respect of projects with the liquidity.

It is the method that ignores a concept

of the time value of the money.

Payback method requires the arbitrary

cut-off points in the process of

evaluation (Alkaraan, 2015).

It ignores the cash flows beyond cut-

off dates.

This capital budgeting method tends to

be biased against the long run projects

like research and development & the

new projects.

Interpretation- From the evaluation, it has been represented that the payback period

resulted as four years which reflects that the proposal will be taking 4 years in reaching to the

initial cost. This in turn seen as better payback period because it is not greater than 4 years and

thus shows that an investment is desirable and attractive.

Accounting rate of return- It referred as the percentage return that is been expected on

an investment or the asset in comparison to the cost of an initial investment (Jibril and Jagun,

2018). It divides an average revenue from the asset by initial outlay of an enterprise in deriving

return ratio which could be expected over useful life of an asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

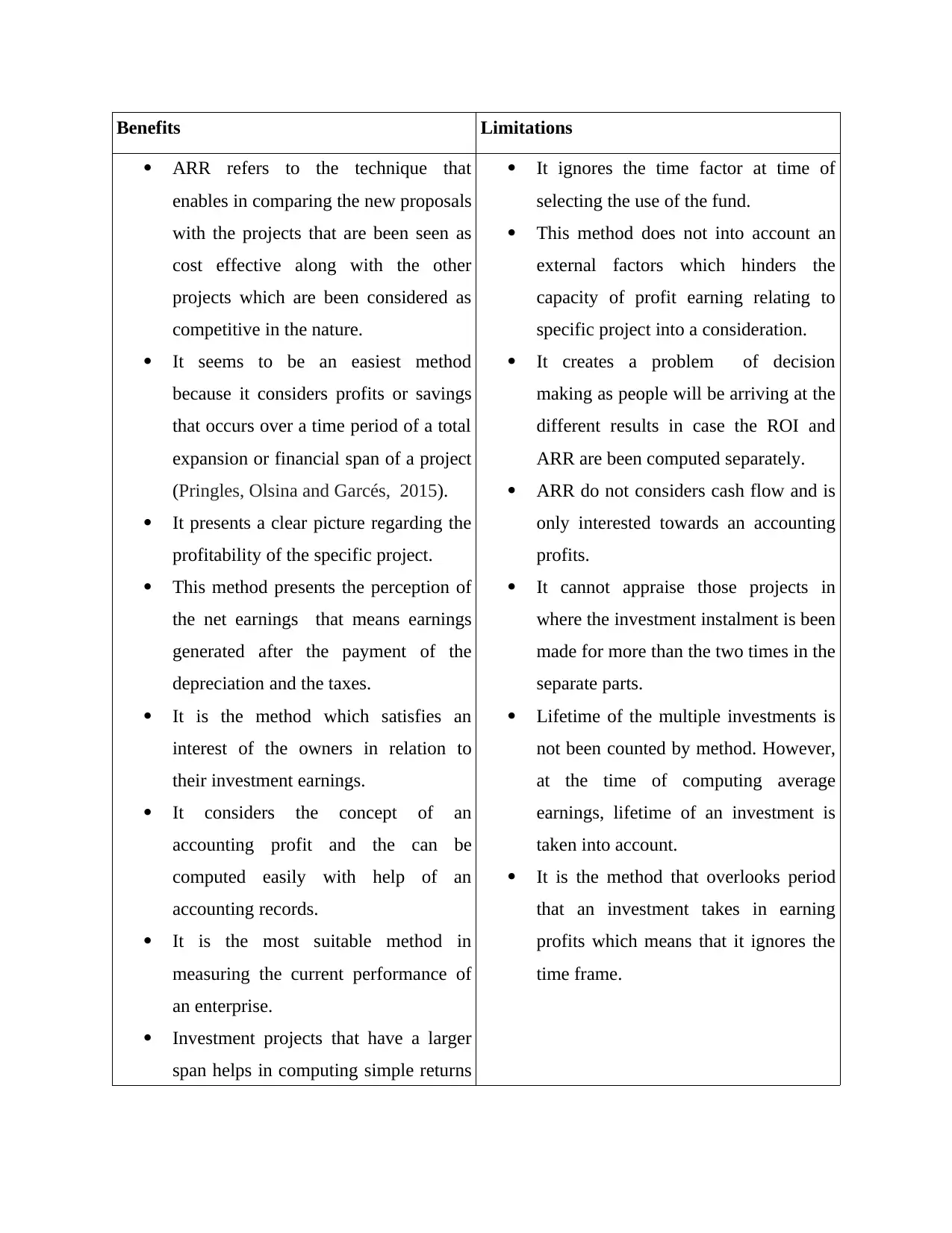

Benefits Limitations

ARR refers to the technique that

enables in comparing the new proposals

with the projects that are been seen as

cost effective along with the other

projects which are been considered as

competitive in the nature.

It seems to be an easiest method

because it considers profits or savings

that occurs over a time period of a total

expansion or financial span of a project

(Pringles, Olsina and Garcés, 2015).

It presents a clear picture regarding the

profitability of the specific project.

This method presents the perception of

the net earnings that means earnings

generated after the payment of the

depreciation and the taxes.

It is the method which satisfies an

interest of the owners in relation to

their investment earnings.

It considers the concept of an

accounting profit and the can be

computed easily with help of an

accounting records.

It is the most suitable method in

measuring the current performance of

an enterprise.

Investment projects that have a larger

span helps in computing simple returns

It ignores the time factor at time of

selecting the use of the fund.

This method does not into account an

external factors which hinders the

capacity of profit earning relating to

specific project into a consideration.

It creates a problem of decision

making as people will be arriving at the

different results in case the ROI and

ARR are been computed separately.

ARR do not considers cash flow and is

only interested towards an accounting

profits.

It cannot appraise those projects in

where the investment instalment is been

made for more than the two times in the

separate parts.

Lifetime of the multiple investments is

not been counted by method. However,

at the time of computing average

earnings, lifetime of an investment is

taken into account.

It is the method that overlooks period

that an investment takes in earning

profits which means that it ignores the

time frame.

ARR refers to the technique that

enables in comparing the new proposals

with the projects that are been seen as

cost effective along with the other

projects which are been considered as

competitive in the nature.

It seems to be an easiest method

because it considers profits or savings

that occurs over a time period of a total

expansion or financial span of a project

(Pringles, Olsina and Garcés, 2015).

It presents a clear picture regarding the

profitability of the specific project.

This method presents the perception of

the net earnings that means earnings

generated after the payment of the

depreciation and the taxes.

It is the method which satisfies an

interest of the owners in relation to

their investment earnings.

It considers the concept of an

accounting profit and the can be

computed easily with help of an

accounting records.

It is the most suitable method in

measuring the current performance of

an enterprise.

Investment projects that have a larger

span helps in computing simple returns

It ignores the time factor at time of

selecting the use of the fund.

This method does not into account an

external factors which hinders the

capacity of profit earning relating to

specific project into a consideration.

It creates a problem of decision

making as people will be arriving at the

different results in case the ROI and

ARR are been computed separately.

ARR do not considers cash flow and is

only interested towards an accounting

profits.

It cannot appraise those projects in

where the investment instalment is been

made for more than the two times in the

separate parts.

Lifetime of the multiple investments is

not been counted by method. However,

at the time of computing average

earnings, lifetime of an investment is

taken into account.

It is the method that overlooks period

that an investment takes in earning

profits which means that it ignores the

time frame.

with that of a true rate of return.

Interpretation- As stated greater the value of ARR higher earnings the project will

generate so the project with highest rate of return must be accepted (Babatunde, 2016). In this

project as per the management forecast, it has been seen that ARR resulted as 18% which

reflects that an investment tend to be highly profitable and larger returns will be gained in the

future periods.

Net present value- It means the method which is used for identifying current or present

value of all the cash flows in future that is generated by project with inclusion of an initial

investment in the capital (Navimipour and Charband, 2016). This method is widely used in the

investment appraisal for establishing which project likely turns into the greatest profits.

Benefits Limitations

The main advantage of this method is

that it is based on the time value of

money concept.

It considers an earnings or the savings

over the useful life of a project. Such

savings or the earnings are been

converted into an current value of the

money.

It helps in making the comparative

analysis of the different proposals or

the project.

This method is applied to the uneven

and the even patterns of the cash

inflows.

NPV helps in maximising the profits of

an entity and is recommended as the

best method selecting the most suitable

or profitable project (Elmassri, Harris,

It does not reflect return rate that is

expected for earning the profits in the

future periods.

This technique might fail in giving the

satisfactory results at the time when

proposals needs various level of an

investment amount with the different

life of projects.

Usage and an application of this

method needs a knowledge relating to

the cost of capital rate. In case if the

capital cost is not known then this

method could not be used.

This method leads to the contradictory

and the confusing answers in context of

ranking the complicated projects.

Under this method it is found as

difficult to identify an adequate value

Interpretation- As stated greater the value of ARR higher earnings the project will

generate so the project with highest rate of return must be accepted (Babatunde, 2016). In this

project as per the management forecast, it has been seen that ARR resulted as 18% which

reflects that an investment tend to be highly profitable and larger returns will be gained in the

future periods.

Net present value- It means the method which is used for identifying current or present

value of all the cash flows in future that is generated by project with inclusion of an initial

investment in the capital (Navimipour and Charband, 2016). This method is widely used in the

investment appraisal for establishing which project likely turns into the greatest profits.

Benefits Limitations

The main advantage of this method is

that it is based on the time value of

money concept.

It considers an earnings or the savings

over the useful life of a project. Such

savings or the earnings are been

converted into an current value of the

money.

It helps in making the comparative

analysis of the different proposals or

the project.

This method is applied to the uneven

and the even patterns of the cash

inflows.

NPV helps in maximising the profits of

an entity and is recommended as the

best method selecting the most suitable

or profitable project (Elmassri, Harris,

It does not reflect return rate that is

expected for earning the profits in the

future periods.

This technique might fail in giving the

satisfactory results at the time when

proposals needs various level of an

investment amount with the different

life of projects.

Usage and an application of this

method needs a knowledge relating to

the cost of capital rate. In case if the

capital cost is not known then this

method could not be used.

This method leads to the contradictory

and the confusing answers in context of

ranking the complicated projects.

Under this method it is found as

difficult to identify an adequate value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.