Management Accounting Report: Financial Analysis of AFC Energy PLC

VerifiedAdded on 2020/11/23

|20

|5553

|392

Report

AI Summary

This management accounting report analyzes the financial aspects of AFC Energy PLC, a developer of alkaline fuel cells. It begins by explaining different management accounting systems, including cost accounting, inventory management, and job costing, and their essential requirements. The report then details various management accounting reporting methods, such as performance reports, cost managerial accounting reports, budget reports, and accounts receivable aging reports. It also outlines the benefits of applying these systems within an organization. The core of the report includes a cost calculation using marginal costing. Furthermore, the report explores budgetary concepts, planning tools, and their advantages and disadvantages in budgetary control. Finally, it examines how management accounting systems can be adapted to solve financial problems, concluding with a comprehensive overview of the company's financial strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

P1. Explaining the essential requirement of different types of management accounting

systems. 3

P2. Different methods used for Management Accounting reporting. 5

LO2............................................................................................................................................7

P3 Calculation of cost using different method of cost calculation 7

Net present Value.....................................................................................................................12

Project Y...................................................................................................................................13

LO3..........................................................................................................................................13

P4 Advantages and Disadvantages of various planning tools for budgetary control 13

P5 Adaptation of management accounting system to solve financial problems 16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................20

INTRODUCTION......................................................................................................................3

MAIN BODY.............................................................................................................................3

P1. Explaining the essential requirement of different types of management accounting

systems. 3

P2. Different methods used for Management Accounting reporting. 5

LO2............................................................................................................................................7

P3 Calculation of cost using different method of cost calculation 7

Net present Value.....................................................................................................................12

Project Y...................................................................................................................................13

LO3..........................................................................................................................................13

P4 Advantages and Disadvantages of various planning tools for budgetary control 13

P5 Adaptation of management accounting system to solve financial problems 16

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................20

INTRODUCTION

Management accounting is defined as the mechanism of making analysis of the internal

management and financial accounting system which further assist in preparation of

managerial reports, records, and accounts. With the help of available information, statistics

and other financial as well as non-financial data, the managers and employees can make

sound investment decisions. Company should always focus on formulation of effective

business strategies and plans so as to achieve the business goals and objectives in a cost

effective manner. The present report is based on AFC Energy PLC which is a developer

of alkaline fuel cells & use hydrogen for production of electricity. The present report will

discuss different types of management accounting systems available and how organization

can seek benefits. Further the report will discuss about the concept of management

accounting reporting and its uses in decision making. Income statement under Marginal and

Absorption Costing of AFC Energy by using appropriate technique for analysing cost factor

will be disclosed. Furthermore, the report will disclose about the budgetary concepts and how

it aids in the decision making process. At last, the report will shed light on advantages and

disadvantages about different budgetary planning tools and how it assists in solving the

financial problems of the company.

MAIN BODY

LO 1

P1. Explaining the essential requirement of different types of management accounting

systems.

Management accounting system is a practice of analysing and preparing managerial

reports of the internal management systems. The management accounting system assists

company in identifying, analysing and recording all the statistical, financial and crucial

management information that can be used internally by managers for planning, decision-

making process. It helps company by providing accurate and timely information which helps

in maximizing the profit level as well as improving the performance of its business

operations.

Essential requirements of different types of Management Accounting System in AFC

Energy PLC are as follows:

Management accounting is defined as the mechanism of making analysis of the internal

management and financial accounting system which further assist in preparation of

managerial reports, records, and accounts. With the help of available information, statistics

and other financial as well as non-financial data, the managers and employees can make

sound investment decisions. Company should always focus on formulation of effective

business strategies and plans so as to achieve the business goals and objectives in a cost

effective manner. The present report is based on AFC Energy PLC which is a developer

of alkaline fuel cells & use hydrogen for production of electricity. The present report will

discuss different types of management accounting systems available and how organization

can seek benefits. Further the report will discuss about the concept of management

accounting reporting and its uses in decision making. Income statement under Marginal and

Absorption Costing of AFC Energy by using appropriate technique for analysing cost factor

will be disclosed. Furthermore, the report will disclose about the budgetary concepts and how

it aids in the decision making process. At last, the report will shed light on advantages and

disadvantages about different budgetary planning tools and how it assists in solving the

financial problems of the company.

MAIN BODY

LO 1

P1. Explaining the essential requirement of different types of management accounting

systems.

Management accounting system is a practice of analysing and preparing managerial

reports of the internal management systems. The management accounting system assists

company in identifying, analysing and recording all the statistical, financial and crucial

management information that can be used internally by managers for planning, decision-

making process. It helps company by providing accurate and timely information which helps

in maximizing the profit level as well as improving the performance of its business

operations.

Essential requirements of different types of Management Accounting System in AFC

Energy PLC are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Cost Accounting System – This method of management accounting system is

basically concerned with the cost aspect associated with the business operations and

processes. With the help of cost accounting system AFC Energy can evaluate and

analysis cost value which has been incurred for carrying on all the manufacturing and

production process of products and services (Jermias, 2017). This method aids in

assessing the profitability level with minimum cost of operations by improving the

quality of product and service rendered. Company should make effective business

plans and strategies so as to control the cost expenses associated with production and

manufacturing operations of the business. This method consists of following sub

parts:

Job Order Costing Method – This method of cost accounting system helps in

determining the cost value which has been incurred by the company for

producing or manufacturing a specific product or group of products.

Process Costing Method – The process costing method assist AFC Energy

with facility of collecting, gathering and making assignment of cost amount.

This cost amount is assigned to manufacturing processes or to the units

produced. This method is beneficial in companies where large production

process is carried out especially in case of identical units.

2. Inventory Management System – This method of management accounting

emphasizes on cost controlling function which has been incurred on producing goods

and services for meeting the customer demands (King and Clarkson, 2015). It also

assists in managing inventory and stock level of the company. AFC Energy can

assess, monitor and track the quantity of goods, inventory and stock through the

supply chain or with the help of areas in which business operations takes place. This

method helps company in making inventory valuation, improving the accuracy of

inventory by maintaining continuous workflow and its reorder so as to facilitate

smooth functioning of business operations. Valuation of inventory can be done with

the help of following two methods:

LIFO – It stands for Last In First Out. In this method, goods which are bought or

purchased at last are available for sale at first place.

FIFO – This stands for First In First Out, it emphasizes on selling first of that

stock which is purchase or bought in at first place.

basically concerned with the cost aspect associated with the business operations and

processes. With the help of cost accounting system AFC Energy can evaluate and

analysis cost value which has been incurred for carrying on all the manufacturing and

production process of products and services (Jermias, 2017). This method aids in

assessing the profitability level with minimum cost of operations by improving the

quality of product and service rendered. Company should make effective business

plans and strategies so as to control the cost expenses associated with production and

manufacturing operations of the business. This method consists of following sub

parts:

Job Order Costing Method – This method of cost accounting system helps in

determining the cost value which has been incurred by the company for

producing or manufacturing a specific product or group of products.

Process Costing Method – The process costing method assist AFC Energy

with facility of collecting, gathering and making assignment of cost amount.

This cost amount is assigned to manufacturing processes or to the units

produced. This method is beneficial in companies where large production

process is carried out especially in case of identical units.

2. Inventory Management System – This method of management accounting

emphasizes on cost controlling function which has been incurred on producing goods

and services for meeting the customer demands (King and Clarkson, 2015). It also

assists in managing inventory and stock level of the company. AFC Energy can

assess, monitor and track the quantity of goods, inventory and stock through the

supply chain or with the help of areas in which business operations takes place. This

method helps company in making inventory valuation, improving the accuracy of

inventory by maintaining continuous workflow and its reorder so as to facilitate

smooth functioning of business operations. Valuation of inventory can be done with

the help of following two methods:

LIFO – It stands for Last In First Out. In this method, goods which are bought or

purchased at last are available for sale at first place.

FIFO – This stands for First In First Out, it emphasizes on selling first of that

stock which is purchase or bought in at first place.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Job Costing System – The job costing method of management accounting is that

business practice which aids AFC Energy in collecting and analysing all the important

and relevant information related to the cost incurred with the production function of

some specific job or product group. It acknowledges company in assessing the cost of

operations and helps in taking corrective measures by minimising the cost of that

activity which is incurring more cost expense. This method considers each part of

information which relates to direct materials, labour and overhead costs. Under this

system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made.

P2. Different methods used for Management Accounting reporting.

Management Accounting Reporting is concerned with the business process of

providing proper, correct & accurate internal information of both statistical and financial

aspect to the management of the company. It also provides deep insight about the business

operations and procedures which is required for making day to day as well as short term

decision making especially related to investment purpose.

Different methods which can be used by AFC Energy PLC for management accounting

reporting are as follows:

1. Performance Report – This report provides deeper insight about the monetary

performance of each department. The performance report helps company in

monitoring, assessing and reviewing the performance, position and situation of its

business operations and processes. It assists in evaluating the performance level of

each employee of the company and team as a whole involved in particular business

activity or task. By using these performance reports, the management of company can

make important strategic decisions and plans for the betterment of company, future

growth and success of business organization (Maas, Schaltegger and Crutzen, 2016).

Performance related report provides a deep insight about the working process,

procedures used by the company in carrying on business activities. By framing and

implementing strategies and plans, company can achieve its business goals and

continuous tracking of these strategies timely can improve business standards as well.

2. Cost Managerial Accounting Report – Such report contains information about

expenses incurred and cost associated with each unit. This accounting report helps in

assessing and determining the amount of cost incurred for undertaking the

business practice which aids AFC Energy in collecting and analysing all the important

and relevant information related to the cost incurred with the production function of

some specific job or product group. It acknowledges company in assessing the cost of

operations and helps in taking corrective measures by minimising the cost of that

activity which is incurring more cost expense. This method considers each part of

information which relates to direct materials, labour and overhead costs. Under this

system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made.

P2. Different methods used for Management Accounting reporting.

Management Accounting Reporting is concerned with the business process of

providing proper, correct & accurate internal information of both statistical and financial

aspect to the management of the company. It also provides deep insight about the business

operations and procedures which is required for making day to day as well as short term

decision making especially related to investment purpose.

Different methods which can be used by AFC Energy PLC for management accounting

reporting are as follows:

1. Performance Report – This report provides deeper insight about the monetary

performance of each department. The performance report helps company in

monitoring, assessing and reviewing the performance, position and situation of its

business operations and processes. It assists in evaluating the performance level of

each employee of the company and team as a whole involved in particular business

activity or task. By using these performance reports, the management of company can

make important strategic decisions and plans for the betterment of company, future

growth and success of business organization (Maas, Schaltegger and Crutzen, 2016).

Performance related report provides a deep insight about the working process,

procedures used by the company in carrying on business activities. By framing and

implementing strategies and plans, company can achieve its business goals and

continuous tracking of these strategies timely can improve business standards as well.

2. Cost Managerial Accounting Report – Such report contains information about

expenses incurred and cost associated with each unit. This accounting report helps in

assessing and determining the amount of cost incurred for undertaking the

manufacturing and production function of any product or services. This assessment

takes into consideration all the cost related to raw material, overhead, labour and

others factors. This helps managers in realizing the cost and selling prices of their

products and services which further helps in estimating the profit or revenue amount

for the company in the near future.

3. Budget Report – The budget report lays emphasis on making future projections and

estimation related to the amount of money to be spent on business operations. By

making budgetary plans and strategies AFC Energy can conduct business operations

smoothly with the limited amount of budgeted amount and resources. With the help of

budget report, a company can make assessment of its performance as well as

profitability level. With proper estimates and budget, company can deal with future

contingencies and cost expenses.

4. Account Receivable Aging Report – It entails information about debtors and time

period for which sales made on credit. Such kind of report is helpful in case where

company conducts its business operations with the help of acquisition of raw material,

labour on credit basis. It is best suited for AFC Energy when it has to rely on large

credit amount for carrying on business activities (Craig and et.al., 2018). With the

help of this report, the manager of AFC can monitor and determine all the potential

defaulters in context of non-payment of money. It also helps in assessing the problem

or issues which the company is facing in its money collection process.

M1. Benefits of application of the management accounting system in an organisation.

AFC Energy can avail several benefits by adopting an effective management

accounting system in following ways:

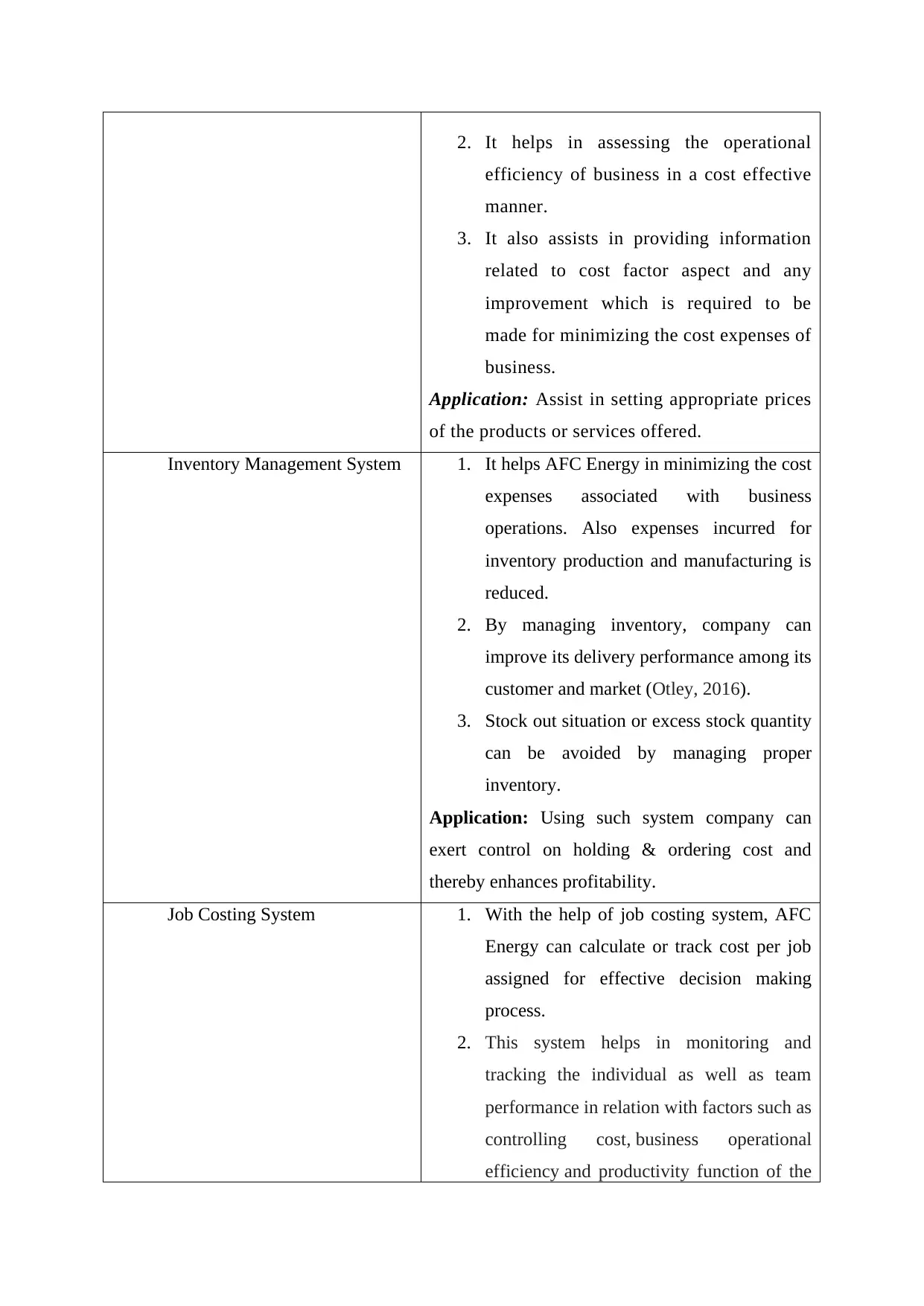

Management Accounting

System

Benefits to AFC Energy

Cost Accounting System 1. It helps company in making budget

compliance for every period i.e. actual

costs incurred can be compared with

budgeted cost for assessing most costly

part of business (Chenhall and Moers,

2015).

takes into consideration all the cost related to raw material, overhead, labour and

others factors. This helps managers in realizing the cost and selling prices of their

products and services which further helps in estimating the profit or revenue amount

for the company in the near future.

3. Budget Report – The budget report lays emphasis on making future projections and

estimation related to the amount of money to be spent on business operations. By

making budgetary plans and strategies AFC Energy can conduct business operations

smoothly with the limited amount of budgeted amount and resources. With the help of

budget report, a company can make assessment of its performance as well as

profitability level. With proper estimates and budget, company can deal with future

contingencies and cost expenses.

4. Account Receivable Aging Report – It entails information about debtors and time

period for which sales made on credit. Such kind of report is helpful in case where

company conducts its business operations with the help of acquisition of raw material,

labour on credit basis. It is best suited for AFC Energy when it has to rely on large

credit amount for carrying on business activities (Craig and et.al., 2018). With the

help of this report, the manager of AFC can monitor and determine all the potential

defaulters in context of non-payment of money. It also helps in assessing the problem

or issues which the company is facing in its money collection process.

M1. Benefits of application of the management accounting system in an organisation.

AFC Energy can avail several benefits by adopting an effective management

accounting system in following ways:

Management Accounting

System

Benefits to AFC Energy

Cost Accounting System 1. It helps company in making budget

compliance for every period i.e. actual

costs incurred can be compared with

budgeted cost for assessing most costly

part of business (Chenhall and Moers,

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. It helps in assessing the operational

efficiency of business in a cost effective

manner.

3. It also assists in providing information

related to cost factor aspect and any

improvement which is required to be

made for minimizing the cost expenses of

business.

Application: Assist in setting appropriate prices

of the products or services offered.

Inventory Management System 1. It helps AFC Energy in minimizing the cost

expenses associated with business

operations. Also expenses incurred for

inventory production and manufacturing is

reduced.

2. By managing inventory, company can

improve its delivery performance among its

customer and market (Otley, 2016).

3. Stock out situation or excess stock quantity

can be avoided by managing proper

inventory.

Application: Using such system company can

exert control on holding & ordering cost and

thereby enhances profitability.

Job Costing System 1. With the help of job costing system, AFC

Energy can calculate or track cost per job

assigned for effective decision making

process.

2. This system helps in monitoring and

tracking the individual as well as team

performance in relation with factors such as

controlling cost, business operational

efficiency and productivity function of the

efficiency of business in a cost effective

manner.

3. It also assists in providing information

related to cost factor aspect and any

improvement which is required to be

made for minimizing the cost expenses of

business.

Application: Assist in setting appropriate prices

of the products or services offered.

Inventory Management System 1. It helps AFC Energy in minimizing the cost

expenses associated with business

operations. Also expenses incurred for

inventory production and manufacturing is

reduced.

2. By managing inventory, company can

improve its delivery performance among its

customer and market (Otley, 2016).

3. Stock out situation or excess stock quantity

can be avoided by managing proper

inventory.

Application: Using such system company can

exert control on holding & ordering cost and

thereby enhances profitability.

Job Costing System 1. With the help of job costing system, AFC

Energy can calculate or track cost per job

assigned for effective decision making

process.

2. This system helps in monitoring and

tracking the individual as well as team

performance in relation with factors such as

controlling cost, business operational

efficiency and productivity function of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business.

LO2

P3 Calculation of cost using different method of cost calculation

Annexure A

Question 1

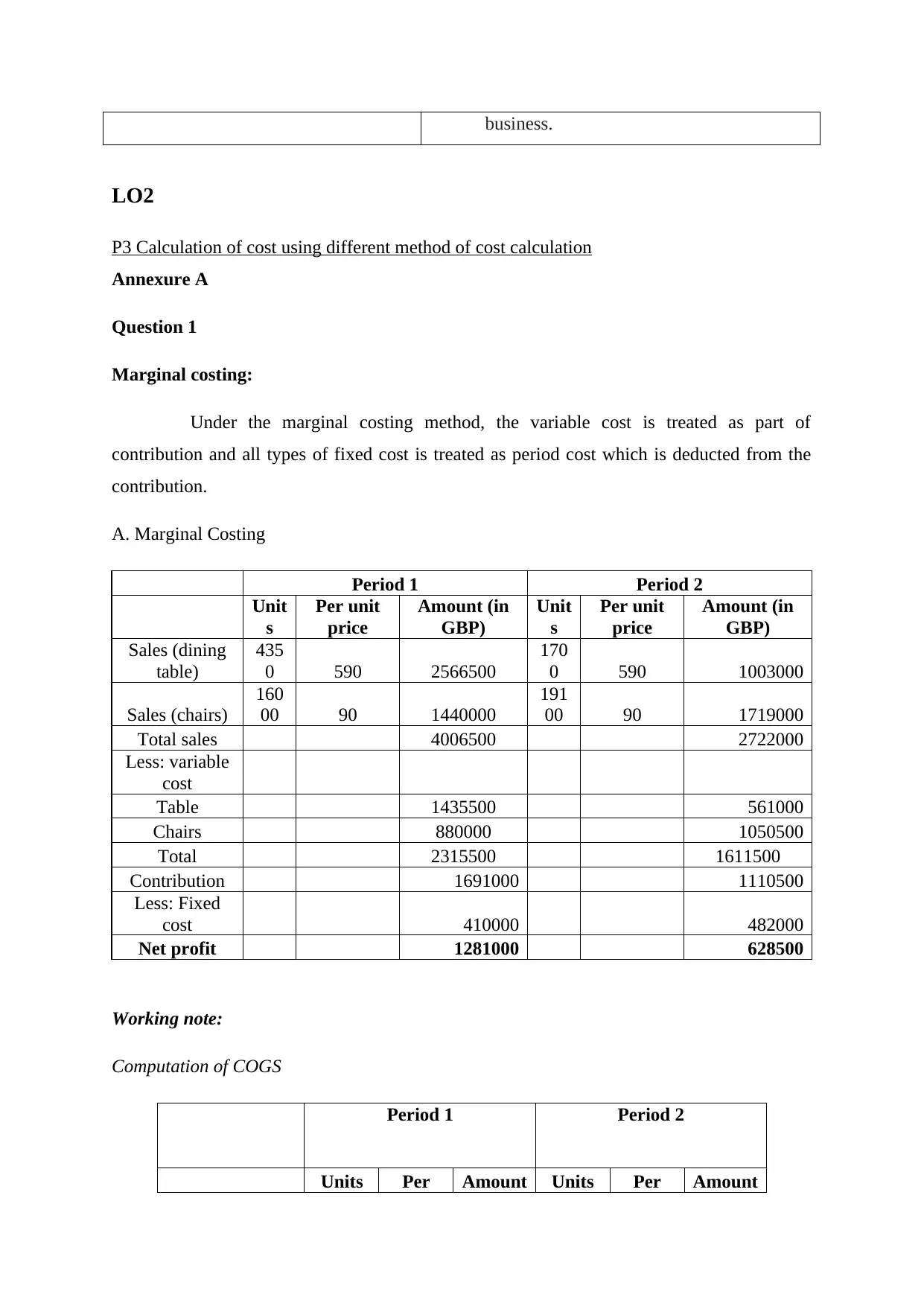

Marginal costing:

Under the marginal costing method, the variable cost is treated as part of

contribution and all types of fixed cost is treated as period cost which is deducted from the

contribution.

A. Marginal Costing

Period 1 Period 2

Unit

s

Per unit

price

Amount (in

GBP)

Unit

s

Per unit

price

Amount (in

GBP)

Sales (dining

table)

435

0 590 2566500

170

0 590 1003000

Sales (chairs)

160

00 90 1440000

191

00 90 1719000

Total sales 4006500 2722000

Less: variable

cost

Table 1435500 561000

Chairs 880000 1050500

Total 2315500 1611500

Contribution 1691000 1110500

Less: Fixed

cost 410000 482000

Net profit 1281000 628500

Working note:

Computation of COGS

Period 1 Period 2

Units Per Amount Units Per Amount

LO2

P3 Calculation of cost using different method of cost calculation

Annexure A

Question 1

Marginal costing:

Under the marginal costing method, the variable cost is treated as part of

contribution and all types of fixed cost is treated as period cost which is deducted from the

contribution.

A. Marginal Costing

Period 1 Period 2

Unit

s

Per unit

price

Amount (in

GBP)

Unit

s

Per unit

price

Amount (in

GBP)

Sales (dining

table)

435

0 590 2566500

170

0 590 1003000

Sales (chairs)

160

00 90 1440000

191

00 90 1719000

Total sales 4006500 2722000

Less: variable

cost

Table 1435500 561000

Chairs 880000 1050500

Total 2315500 1611500

Contribution 1691000 1110500

Less: Fixed

cost 410000 482000

Net profit 1281000 628500

Working note:

Computation of COGS

Period 1 Period 2

Units Per Amount Units Per Amount

unit

price

(in

GBP)

unit

price

(in

GBP)

Opening stock

Add: purchase

Table 5000 330 1650000 5200 330 1716000

Chairs 20000 55 1100000 22000 55 1210000

Less: closing

stock

Table 650 330 214500 3500 330 1155000

Chairs 4000 55 220000 2900 55 159500

COGS

Table 1435500 561000

Chairs 880000 1050500

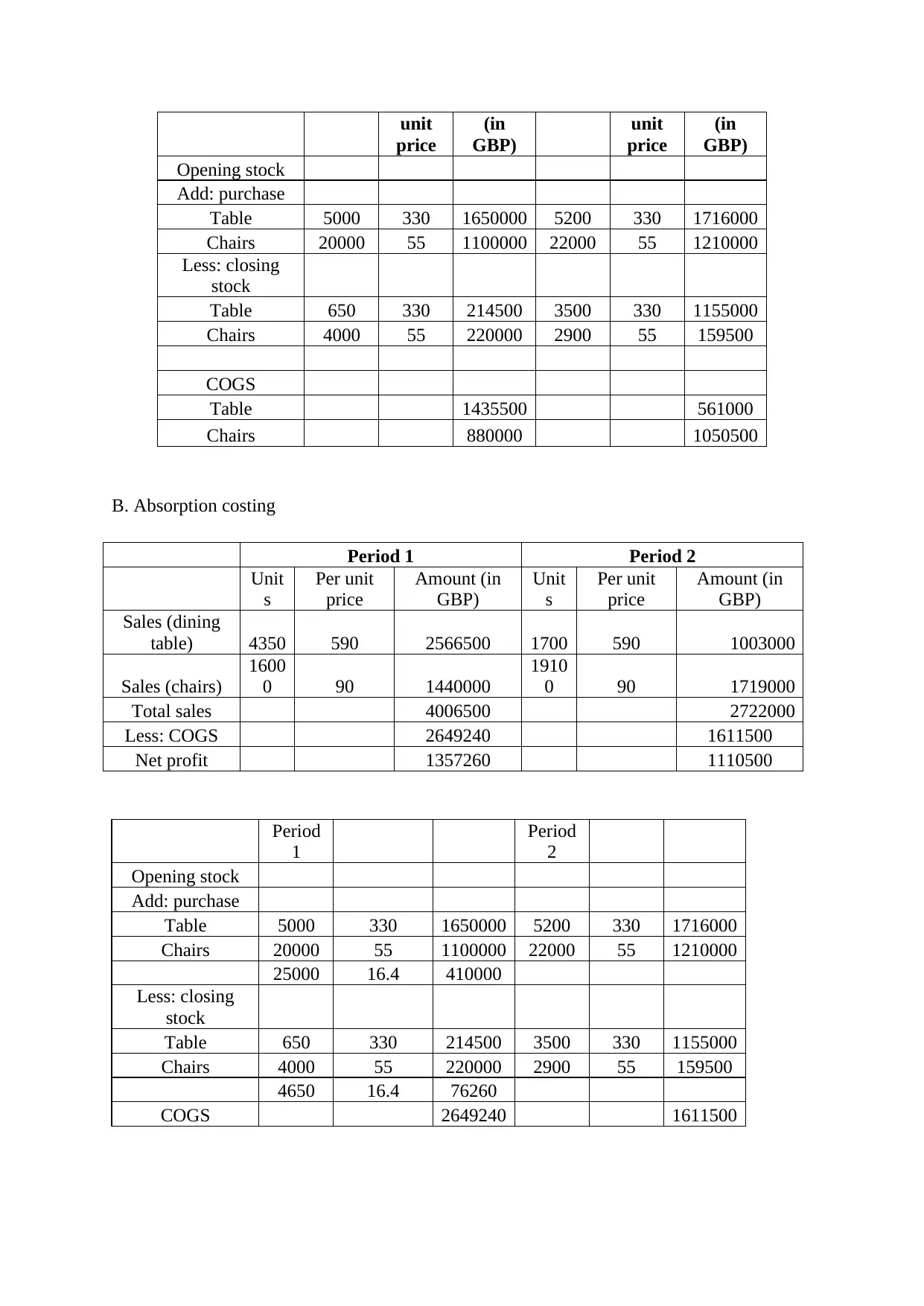

B. Absorption costing

Period 1 Period 2

Unit

s

Per unit

price

Amount (in

GBP)

Unit

s

Per unit

price

Amount (in

GBP)

Sales (dining

table) 4350 590 2566500 1700 590 1003000

Sales (chairs)

1600

0 90 1440000

1910

0 90 1719000

Total sales 4006500 2722000

Less: COGS 2649240 1611500

Net profit 1357260 1110500

Period

1

Period

2

Opening stock

Add: purchase

Table 5000 330 1650000 5200 330 1716000

Chairs 20000 55 1100000 22000 55 1210000

25000 16.4 410000

Less: closing

stock

Table 650 330 214500 3500 330 1155000

Chairs 4000 55 220000 2900 55 159500

4650 16.4 76260

COGS 2649240 1611500

price

(in

GBP)

unit

price

(in

GBP)

Opening stock

Add: purchase

Table 5000 330 1650000 5200 330 1716000

Chairs 20000 55 1100000 22000 55 1210000

Less: closing

stock

Table 650 330 214500 3500 330 1155000

Chairs 4000 55 220000 2900 55 159500

COGS

Table 1435500 561000

Chairs 880000 1050500

B. Absorption costing

Period 1 Period 2

Unit

s

Per unit

price

Amount (in

GBP)

Unit

s

Per unit

price

Amount (in

GBP)

Sales (dining

table) 4350 590 2566500 1700 590 1003000

Sales (chairs)

1600

0 90 1440000

1910

0 90 1719000

Total sales 4006500 2722000

Less: COGS 2649240 1611500

Net profit 1357260 1110500

Period

1

Period

2

Opening stock

Add: purchase

Table 5000 330 1650000 5200 330 1716000

Chairs 20000 55 1100000 22000 55 1210000

25000 16.4 410000

Less: closing

stock

Table 650 330 214500 3500 330 1155000

Chairs 4000 55 220000 2900 55 159500

4650 16.4 76260

COGS 2649240 1611500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

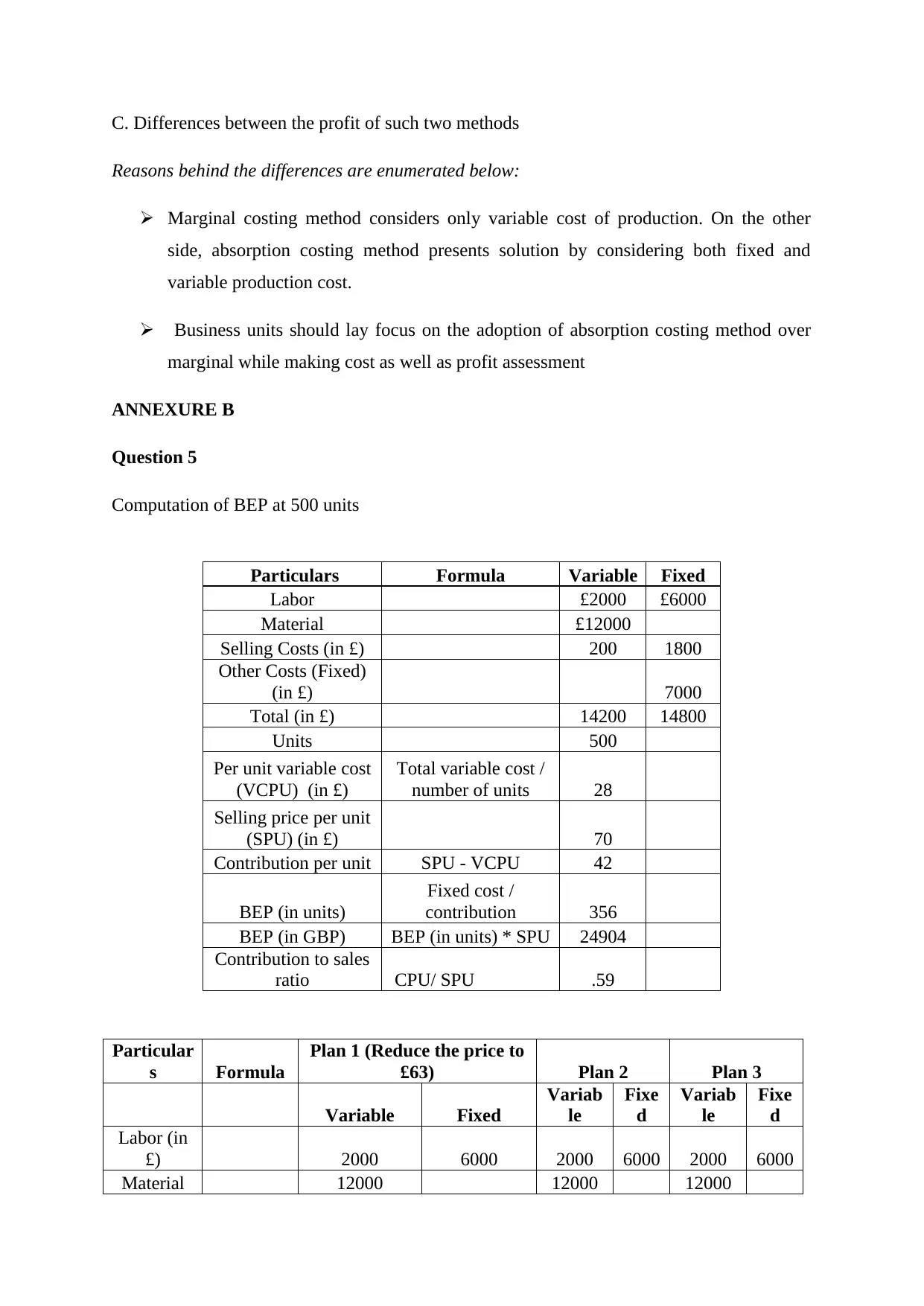

C. Differences between the profit of such two methods

Reasons behind the differences are enumerated below:

Marginal costing method considers only variable cost of production. On the other

side, absorption costing method presents solution by considering both fixed and

variable production cost.

Business units should lay focus on the adoption of absorption costing method over

marginal while making cost as well as profit assessment

ANNEXURE B

Question 5

Computation of BEP at 500 units

Particulars Formula Variable Fixed

Labor £2000 £6000

Material £12000

Selling Costs (in £) 200 1800

Other Costs (Fixed)

(in £) 7000

Total (in £) 14200 14800

Units 500

Per unit variable cost

(VCPU) (in £)

Total variable cost /

number of units 28

Selling price per unit

(SPU) (in £) 70

Contribution per unit SPU - VCPU 42

BEP (in units)

Fixed cost /

contribution 356

BEP (in GBP) BEP (in units) * SPU 24904

Contribution to sales

ratio CPU/ SPU .59

Particular

s Formula

Plan 1 (Reduce the price to

£63) Plan 2 Plan 3

Variable Fixed

Variab

le

Fixe

d

Variab

le

Fixe

d

Labor (in

£) 2000 6000 2000 6000 2000 6000

Material 12000 12000 12000

Reasons behind the differences are enumerated below:

Marginal costing method considers only variable cost of production. On the other

side, absorption costing method presents solution by considering both fixed and

variable production cost.

Business units should lay focus on the adoption of absorption costing method over

marginal while making cost as well as profit assessment

ANNEXURE B

Question 5

Computation of BEP at 500 units

Particulars Formula Variable Fixed

Labor £2000 £6000

Material £12000

Selling Costs (in £) 200 1800

Other Costs (Fixed)

(in £) 7000

Total (in £) 14200 14800

Units 500

Per unit variable cost

(VCPU) (in £)

Total variable cost /

number of units 28

Selling price per unit

(SPU) (in £) 70

Contribution per unit SPU - VCPU 42

BEP (in units)

Fixed cost /

contribution 356

BEP (in GBP) BEP (in units) * SPU 24904

Contribution to sales

ratio CPU/ SPU .59

Particular

s Formula

Plan 1 (Reduce the price to

£63) Plan 2 Plan 3

Variable Fixed

Variab

le

Fixe

d

Variab

le

Fixe

d

Labor (in

£) 2000 6000 2000 6000 2000 6000

Material 12000 12000 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(in £)

Selling

Costs (in

£) 200 1800 200 1800 200 1800

Other

Costs

(Fixed in

£)) 7000 7000 7000

Total (in

£) 14200 14800 14200

1480

0 14200

1480

0

Units 650 400 650

Per unit

variable

cost

(VCPU)

(in £)

Total

variable

cost /

number of

units 22 36 22

Selling

price per

unit (SPU)

(in £) 63 80 70

Contributi

on per unit

SPU -

VCPU 41 45 48

BEP (in

units)

Fixed cost

/

contributi

on 360 333 307

BEP (in

GBP)

BEP (in

units) *

SPU 22656 26607 21514

Contributi

on to sales

ratio

CPU/

SPU 0.65 0.56 0.69

LO3

P4 Advantages and Disadvantages of various planning tools for budgetary control

The company uses various planning tools to control their budget to exceed the

revenue and to deal with various uncertainties that the business can face in its lifetime. The

budget of company is prepared by keeping various factors in mind so that the operations of

the company can work smoothly and efficiently. There are various planning tools used by the

company in control their budget which are –

Selling

Costs (in

£) 200 1800 200 1800 200 1800

Other

Costs

(Fixed in

£)) 7000 7000 7000

Total (in

£) 14200 14800 14200

1480

0 14200

1480

0

Units 650 400 650

Per unit

variable

cost

(VCPU)

(in £)

Total

variable

cost /

number of

units 22 36 22

Selling

price per

unit (SPU)

(in £) 63 80 70

Contributi

on per unit

SPU -

VCPU 41 45 48

BEP (in

units)

Fixed cost

/

contributi

on 360 333 307

BEP (in

GBP)

BEP (in

units) *

SPU 22656 26607 21514

Contributi

on to sales

ratio

CPU/

SPU 0.65 0.56 0.69

LO3

P4 Advantages and Disadvantages of various planning tools for budgetary control

The company uses various planning tools to control their budget to exceed the

revenue and to deal with various uncertainties that the business can face in its lifetime. The

budget of company is prepared by keeping various factors in mind so that the operations of

the company can work smoothly and efficiently. There are various planning tools used by the

company in control their budget which are –

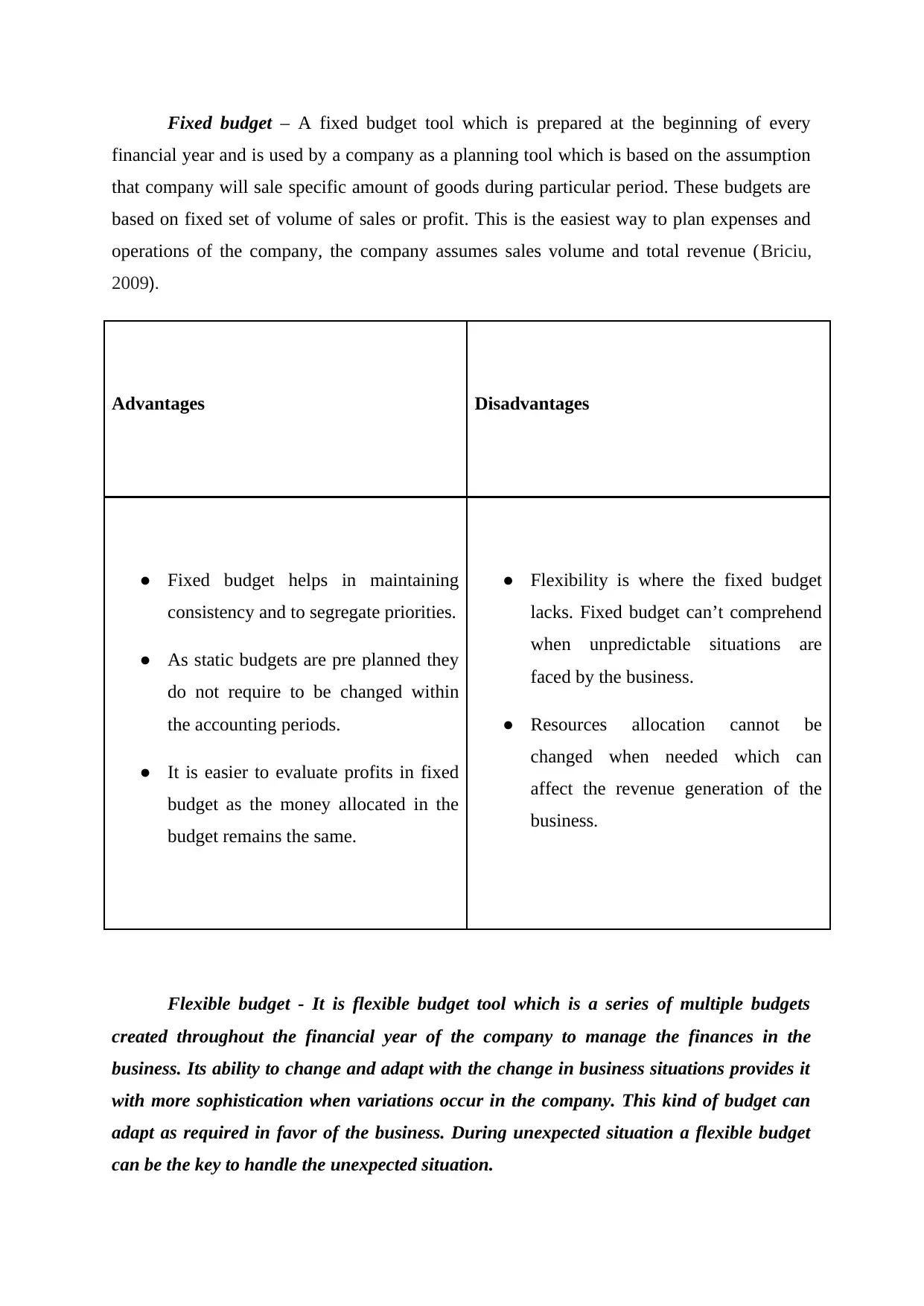

Fixed budget – A fixed budget tool which is prepared at the beginning of every

financial year and is used by a company as a planning tool which is based on the assumption

that company will sale specific amount of goods during particular period. These budgets are

based on fixed set of volume of sales or profit. This is the easiest way to plan expenses and

operations of the company, the company assumes sales volume and total revenue (Briciu,

2009).

Advantages Disadvantages

● Fixed budget helps in maintaining

consistency and to segregate priorities.

● As static budgets are pre planned they

do not require to be changed within

the accounting periods.

● It is easier to evaluate profits in fixed

budget as the money allocated in the

budget remains the same.

● Flexibility is where the fixed budget

lacks. Fixed budget can’t comprehend

when unpredictable situations are

faced by the business.

● Resources allocation cannot be

changed when needed which can

affect the revenue generation of the

business.

Flexible budget - It is flexible budget tool which is a series of multiple budgets

created throughout the financial year of the company to manage the finances in the

business. Its ability to change and adapt with the change in business situations provides it

with more sophistication when variations occur in the company. This kind of budget can

adapt as required in favor of the business. During unexpected situation a flexible budget

can be the key to handle the unexpected situation.

financial year and is used by a company as a planning tool which is based on the assumption

that company will sale specific amount of goods during particular period. These budgets are

based on fixed set of volume of sales or profit. This is the easiest way to plan expenses and

operations of the company, the company assumes sales volume and total revenue (Briciu,

2009).

Advantages Disadvantages

● Fixed budget helps in maintaining

consistency and to segregate priorities.

● As static budgets are pre planned they

do not require to be changed within

the accounting periods.

● It is easier to evaluate profits in fixed

budget as the money allocated in the

budget remains the same.

● Flexibility is where the fixed budget

lacks. Fixed budget can’t comprehend

when unpredictable situations are

faced by the business.

● Resources allocation cannot be

changed when needed which can

affect the revenue generation of the

business.

Flexible budget - It is flexible budget tool which is a series of multiple budgets

created throughout the financial year of the company to manage the finances in the

business. Its ability to change and adapt with the change in business situations provides it

with more sophistication when variations occur in the company. This kind of budget can

adapt as required in favor of the business. During unexpected situation a flexible budget

can be the key to handle the unexpected situation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.