Management Accounting Report: Agmet Chemical Manufacturing

VerifiedAdded on 2020/10/22

|19

|5607

|212

Report

AI Summary

This report examines management accounting principles and their application within Agmet, a chemical product-manufacturing unit. It begins with an introduction to management accounting, its different types, and the various reports used by Agmet. The report then delves into the benefits of management accounting systems, including cost accounting, job costing, inventory management, and price optimization. Task 1 analyzes management accounting and its types, the reports used by Agmet, and the benefits of each system. Task 2 explores marginal and absorption costing methods, preparing income statements based on both methods, and calculations based on the break-even formula. Task 3 discusses planning tools for budgetary control, their advantages and disadvantages, and the adaptation of management accounting systems to address financial problems, along with relevant techniques to achieve sustainable success. The report concludes by summarizing the key findings and recommendations for Agmet, emphasizing the importance of management accounting in decision-making and financial performance.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and its different types.....................................................................1

B. Different management accounting report use by Agmet and its importance to Management

.....................................................................................................................................................2

C. evaluation of benefits of management accounting system and its application in Agmet.......3

D. Evaluation of integration of management accounting system and management accounting

reporting......................................................................................................................................5

TASK 2............................................................................................................................................5

A. Marginal costing and absorption costing methods and preparation of income statements on

basis of both methods..................................................................................................................5

B. Calculations based on break even formula.............................................................................7

C. Financial reporting documents...............................................................................................8

D. Interpretation of the data by financial reports .......................................................................8

TASK 3 ...........................................................................................................................................9

A. Advantages and disadvantages of different planning tools for budgetary control ................9

B. Application of planning tools for preparing, forecasting and analysing budgets.................11

C. Adaption of management accounting system to respond to financial problems..................11

D. Management accounting techniques to respond to financial problems and lead to

sustainable success....................................................................................................................12

E. Use of planning tools to solve financial problems and lead to sustainable success.............13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and its different types.....................................................................1

B. Different management accounting report use by Agmet and its importance to Management

.....................................................................................................................................................2

C. evaluation of benefits of management accounting system and its application in Agmet.......3

D. Evaluation of integration of management accounting system and management accounting

reporting......................................................................................................................................5

TASK 2............................................................................................................................................5

A. Marginal costing and absorption costing methods and preparation of income statements on

basis of both methods..................................................................................................................5

B. Calculations based on break even formula.............................................................................7

C. Financial reporting documents...............................................................................................8

D. Interpretation of the data by financial reports .......................................................................8

TASK 3 ...........................................................................................................................................9

A. Advantages and disadvantages of different planning tools for budgetary control ................9

B. Application of planning tools for preparing, forecasting and analysing budgets.................11

C. Adaption of management accounting system to respond to financial problems..................11

D. Management accounting techniques to respond to financial problems and lead to

sustainable success....................................................................................................................12

E. Use of planning tools to solve financial problems and lead to sustainable success.............13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is an area related with activities of decision-making, devising

planning, performance management system, providing financial reporting expertise and planning

formulation implementation of organisational strategy and its controlling. It is a planning and

decision support system of an organisation. Management accounting system takes all financial

and operational information and present reports which assists in decision-making process.

The present report is about business Agmet, which is a chemical product-manufacturing

unit. The report presents Agmet with different management accounting systems and report and

states all their benefits. An Application of various planning tools their advantages and

disadvantages to the firm. Are also explained.

TASK 1

A. Management accounting and its different types

Management Accounting

Management Accounting is a combination of financial and statistical information and

preparation of management reports on the basis of available information. These reports guide

management of a business in decision-making process (Maas, Schaltegger and Crutzen, 2016.

Management accounting takes into consideration the entire activities of an organisation, which

are accounting, financial, operational and statistical activities take data and relevant information

from these activities and make day-to-day business decisions.

The reports that are presented under management accounting system provides details and

information related to cash and cash equivalents available with the firm, revenues generated from

sales, status of accounts payables and receivables, raw material, inventories and debtors and

creditors of the firm.

Different types of management accounting systems are:

Cost Accounting System: this system of management accounting deals with

determination of cost related to production of units of goods in a firm. The cost and sales

revenue are evaluated to determine profits. This system classifies information in manner required

1

Management accounting is an area related with activities of decision-making, devising

planning, performance management system, providing financial reporting expertise and planning

formulation implementation of organisational strategy and its controlling. It is a planning and

decision support system of an organisation. Management accounting system takes all financial

and operational information and present reports which assists in decision-making process.

The present report is about business Agmet, which is a chemical product-manufacturing

unit. The report presents Agmet with different management accounting systems and report and

states all their benefits. An Application of various planning tools their advantages and

disadvantages to the firm. Are also explained.

TASK 1

A. Management accounting and its different types

Management Accounting

Management Accounting is a combination of financial and statistical information and

preparation of management reports on the basis of available information. These reports guide

management of a business in decision-making process (Maas, Schaltegger and Crutzen, 2016.

Management accounting takes into consideration the entire activities of an organisation, which

are accounting, financial, operational and statistical activities take data and relevant information

from these activities and make day-to-day business decisions.

The reports that are presented under management accounting system provides details and

information related to cash and cash equivalents available with the firm, revenues generated from

sales, status of accounts payables and receivables, raw material, inventories and debtors and

creditors of the firm.

Different types of management accounting systems are:

Cost Accounting System: this system of management accounting deals with

determination of cost related to production of units of goods in a firm. The cost and sales

revenue are evaluated to determine profits. This system classifies information in manner required

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by management of the firm. Being a small manufacturer, Agmet have to consider all cost

relevant information to maximize its profits and lower operational and production cost.

Job costing system: this is a system where records related to cost of each job performed

in a firm that are determined separately. This helps management in determination of cost and

expense incurred on each particular job and quotes the selling price in accordingly. The

information can be used to assign inventory cost to manufacturing cost. This system assists

mangers of Agmet to clearly identify cost related to each job and take decision accordingly.

Inventory management system: this is a system of monitoring and maintaining stock of

goods produced in a firm. This system maintains a record of units produced, from the stage of its

manufacturing up to stage of selling. A proper channel of line is followed to keep proper

records of stock. Agmet is a small manufacturing business and it shall keep a close eye on stock

of chemical produced.

Price optimization system: this system is concerned with adoption of the best price for

product produced in the firm. Price optimization means the reaction consumers will give on price

quoted by firm. Agmet takes into consideration all expenses, cost of product and sets selling

price of product, and try to keep it minimal.

B. Different management accounting report use by Agmet and its importance to Management

Management accounting reports are prepared for planning of business operation and to

assist management in decision-making. This report is prepared by taking internal data

information by managers, which are:

Budgets: for making a report on different operations of the firm the managers uses the

techniques of budget preparation (Taleb, Gibson and Hovey, 2015). The budgets are prepared for

various activities such as sales, production, manufacturing, selling and distribution and

administrative expenses. The budgets are prepared in comprehensive manner, which assists

managers in formulation of plans and polices to be applied in the firm. The budgets give a

performance evaluation of the activity in relation to which it was prepared.

Performance report: for a firm, the employees are an integral and important part of the

business. To evaluate their performance and presenting a report on it has a vital role for the

operations of a firm. These report is necessary to prepare to know the quality of performance of

2

relevant information to maximize its profits and lower operational and production cost.

Job costing system: this is a system where records related to cost of each job performed

in a firm that are determined separately. This helps management in determination of cost and

expense incurred on each particular job and quotes the selling price in accordingly. The

information can be used to assign inventory cost to manufacturing cost. This system assists

mangers of Agmet to clearly identify cost related to each job and take decision accordingly.

Inventory management system: this is a system of monitoring and maintaining stock of

goods produced in a firm. This system maintains a record of units produced, from the stage of its

manufacturing up to stage of selling. A proper channel of line is followed to keep proper

records of stock. Agmet is a small manufacturing business and it shall keep a close eye on stock

of chemical produced.

Price optimization system: this system is concerned with adoption of the best price for

product produced in the firm. Price optimization means the reaction consumers will give on price

quoted by firm. Agmet takes into consideration all expenses, cost of product and sets selling

price of product, and try to keep it minimal.

B. Different management accounting report use by Agmet and its importance to Management

Management accounting reports are prepared for planning of business operation and to

assist management in decision-making. This report is prepared by taking internal data

information by managers, which are:

Budgets: for making a report on different operations of the firm the managers uses the

techniques of budget preparation (Taleb, Gibson and Hovey, 2015). The budgets are prepared for

various activities such as sales, production, manufacturing, selling and distribution and

administrative expenses. The budgets are prepared in comprehensive manner, which assists

managers in formulation of plans and polices to be applied in the firm. The budgets give a

performance evaluation of the activity in relation to which it was prepared.

Performance report: for a firm, the employees are an integral and important part of the

business. To evaluate their performance and presenting a report on it has a vital role for the

operations of a firm. These report is necessary to prepare to know the quality of performance of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employees and if any deviation to find out reason for such deviation. To eliminate deviation, the

managers take corrective measures for better performance of employees.

Cost report: in a business activity the most important thing is cost, to carry on any

activity, business have to spend first then only it can get returns. To manage the cost is critical

and of key importance. The cost incurred can be calculated by using different costing methods

such as job costing, marginal and absorption costing, standard costing.

Project report: these reports are prepared to evaluate the status of ongoing or finished

projects. In these reports, the performance is evaluated in relation to the use of funds allocated to

them and the level of progress and success of such projects (Fullerton, Kennedy and Widener,

2014). These reports present-detailed information on projects. The report also states further

requisition of resources or material for completion of ongoing projects and measures to be taken

for making a project successful.

Activity report: The report is prepared in relation to activities performed in day-to-day

operation of business. This gives a close eye on actual performance of each activity on a daily

basis.

C. Evaluation of benefits of management accounting system and its application in Agmet

Benefits of Cost accounting system:

a tool for measuring and improving efficiency

Throws a light on profitable and non profitable activities

Firm is able to fix the price of its product

Provide guidance for reduction in product price

Provide complete information for proper planning

Information related to stock and various materials are constantly available.

Guides in making decision regarding increase and decrease in production of a particular

product

Cost accounting system assists and guides Agmet in process of decision making in

relation to expansion of production units, cost control, setting up profit margin it needs to earn.

The system also gives an insight in cost bifurcation and relates each part of cost incurred-to

relevant activity.

Benefits of Job costing system:

3

managers take corrective measures for better performance of employees.

Cost report: in a business activity the most important thing is cost, to carry on any

activity, business have to spend first then only it can get returns. To manage the cost is critical

and of key importance. The cost incurred can be calculated by using different costing methods

such as job costing, marginal and absorption costing, standard costing.

Project report: these reports are prepared to evaluate the status of ongoing or finished

projects. In these reports, the performance is evaluated in relation to the use of funds allocated to

them and the level of progress and success of such projects (Fullerton, Kennedy and Widener,

2014). These reports present-detailed information on projects. The report also states further

requisition of resources or material for completion of ongoing projects and measures to be taken

for making a project successful.

Activity report: The report is prepared in relation to activities performed in day-to-day

operation of business. This gives a close eye on actual performance of each activity on a daily

basis.

C. Evaluation of benefits of management accounting system and its application in Agmet

Benefits of Cost accounting system:

a tool for measuring and improving efficiency

Throws a light on profitable and non profitable activities

Firm is able to fix the price of its product

Provide guidance for reduction in product price

Provide complete information for proper planning

Information related to stock and various materials are constantly available.

Guides in making decision regarding increase and decrease in production of a particular

product

Cost accounting system assists and guides Agmet in process of decision making in

relation to expansion of production units, cost control, setting up profit margin it needs to earn.

The system also gives an insight in cost bifurcation and relates each part of cost incurred-to

relevant activity.

Benefits of Job costing system:

3

Control over costs as cost may be ascertain at any stage of completion of a job.

Separate profits earned for each job is known.

Each element of cost, selling price and profits can be compared with estimates for cost

control, on completion of a job.

On the basis of past records in job costing management can estimate cost of a job.

The present job cost can be compared with actual cost of previous job.

On the basis of budgets overhead recovery rates can be predetermined.

Facilitates pricing of each job.

Agmet can use job costing for determination of cost of jobs related to manufacturing of

chemical products and other jobs related to operations of business. This will result in actual

allocation of cost to particular activities.

Benefits of Inventory management system:

Determine exactly the quantity of inventory firm needs.

Keeping the right amount of inventory for seasonal changes.

Proper organisation of warehoused products as per their need and demand.

A time saving tool as it keeps track of all products in hand and in order.

Avoid waste of money on slow moving products when in demand by keeping a stock of

it.

A proper knowledge of inventory in hand can lead to a smarter decision about what to

order and when.

Agmet can keep a good inventory system so that keep a record of what to order and when

to order raw material for production of chemicals (Cooper, Ezzamel and Qu, 2017). It will have a

record regarding how many units it already have as a stock and how much to produce as per the

orders it have.

Benefits of Price optimization system:

achievement of organization objective by maximisation of operating profits.

Proper evaluation of consumer reaction regarding the price of the product.

Visualisation of varying demand at different price points.

Determination of price to meet the corporate goals.

Gives information for formulating and solving constrains related to optimization process.

Determination of pricing structure for initial, promotional and discount price.

4

Separate profits earned for each job is known.

Each element of cost, selling price and profits can be compared with estimates for cost

control, on completion of a job.

On the basis of past records in job costing management can estimate cost of a job.

The present job cost can be compared with actual cost of previous job.

On the basis of budgets overhead recovery rates can be predetermined.

Facilitates pricing of each job.

Agmet can use job costing for determination of cost of jobs related to manufacturing of

chemical products and other jobs related to operations of business. This will result in actual

allocation of cost to particular activities.

Benefits of Inventory management system:

Determine exactly the quantity of inventory firm needs.

Keeping the right amount of inventory for seasonal changes.

Proper organisation of warehoused products as per their need and demand.

A time saving tool as it keeps track of all products in hand and in order.

Avoid waste of money on slow moving products when in demand by keeping a stock of

it.

A proper knowledge of inventory in hand can lead to a smarter decision about what to

order and when.

Agmet can keep a good inventory system so that keep a record of what to order and when

to order raw material for production of chemicals (Cooper, Ezzamel and Qu, 2017). It will have a

record regarding how many units it already have as a stock and how much to produce as per the

orders it have.

Benefits of Price optimization system:

achievement of organization objective by maximisation of operating profits.

Proper evaluation of consumer reaction regarding the price of the product.

Visualisation of varying demand at different price points.

Determination of price to meet the corporate goals.

Gives information for formulating and solving constrains related to optimization process.

Determination of pricing structure for initial, promotional and discount price.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This system allow Agmet to determine hoe a price will affect its consumer and how they

will react. This helps the firm to determine the initial and promotional price of a new product.

The extent to which price shall be changed of an existing product which will not affect consumer

much.

D. Evaluation of integration of management accounting system and management accounting

reporting

Management accounting system is internal check ion an organisation. It uses its tools and

techniques to evaluate each and every activity performed within an organisation be it related to

finance or employee performance (Ekwue, 2014). This system focuses on evaluating overall

performance of business, monitoring the and taking controlling measures for any deviation or

achievement of organisational goal.

On the other hand the management accounting reports are prepared on the basis of

performance of business activities. These report are evaluation of each activity separately. These

reports are prepared for planning of business goals.

Management accounting report are prepared for various activities of the organisation

separately such as budgets, cost, activity, project reports. It can be said that reports are

individual analysis and management accounting system is an overall analysis of performance of

the firm. So both management accounting system and management accounting reporting go hand

in hand. The reports provide information to accounting system for taking management decision

of the firm Agmet.

TASK 2

A. Marginal costing and absorption costing methods and preparation of income statements on

basis of both methods

A.1 marginal and absorption costing method:

Marginal costing method: in this method, with change in sales volume the fixed cost

remain constant for given time. The marginal cost that is variable is charged from costs and fixed

cost is written off completely against the contribution.

In this method direct material, direct overhead, variable factory overhead are charged to

cost of production and are charged as expenses when goods are sold. Fixed factory and total

selling and distribution overheads are charged as expenses when incurred.

5

will react. This helps the firm to determine the initial and promotional price of a new product.

The extent to which price shall be changed of an existing product which will not affect consumer

much.

D. Evaluation of integration of management accounting system and management accounting

reporting

Management accounting system is internal check ion an organisation. It uses its tools and

techniques to evaluate each and every activity performed within an organisation be it related to

finance or employee performance (Ekwue, 2014). This system focuses on evaluating overall

performance of business, monitoring the and taking controlling measures for any deviation or

achievement of organisational goal.

On the other hand the management accounting reports are prepared on the basis of

performance of business activities. These report are evaluation of each activity separately. These

reports are prepared for planning of business goals.

Management accounting report are prepared for various activities of the organisation

separately such as budgets, cost, activity, project reports. It can be said that reports are

individual analysis and management accounting system is an overall analysis of performance of

the firm. So both management accounting system and management accounting reporting go hand

in hand. The reports provide information to accounting system for taking management decision

of the firm Agmet.

TASK 2

A. Marginal costing and absorption costing methods and preparation of income statements on

basis of both methods

A.1 marginal and absorption costing method:

Marginal costing method: in this method, with change in sales volume the fixed cost

remain constant for given time. The marginal cost that is variable is charged from costs and fixed

cost is written off completely against the contribution.

In this method direct material, direct overhead, variable factory overhead are charged to

cost of production and are charged as expenses when goods are sold. Fixed factory and total

selling and distribution overheads are charged as expenses when incurred.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

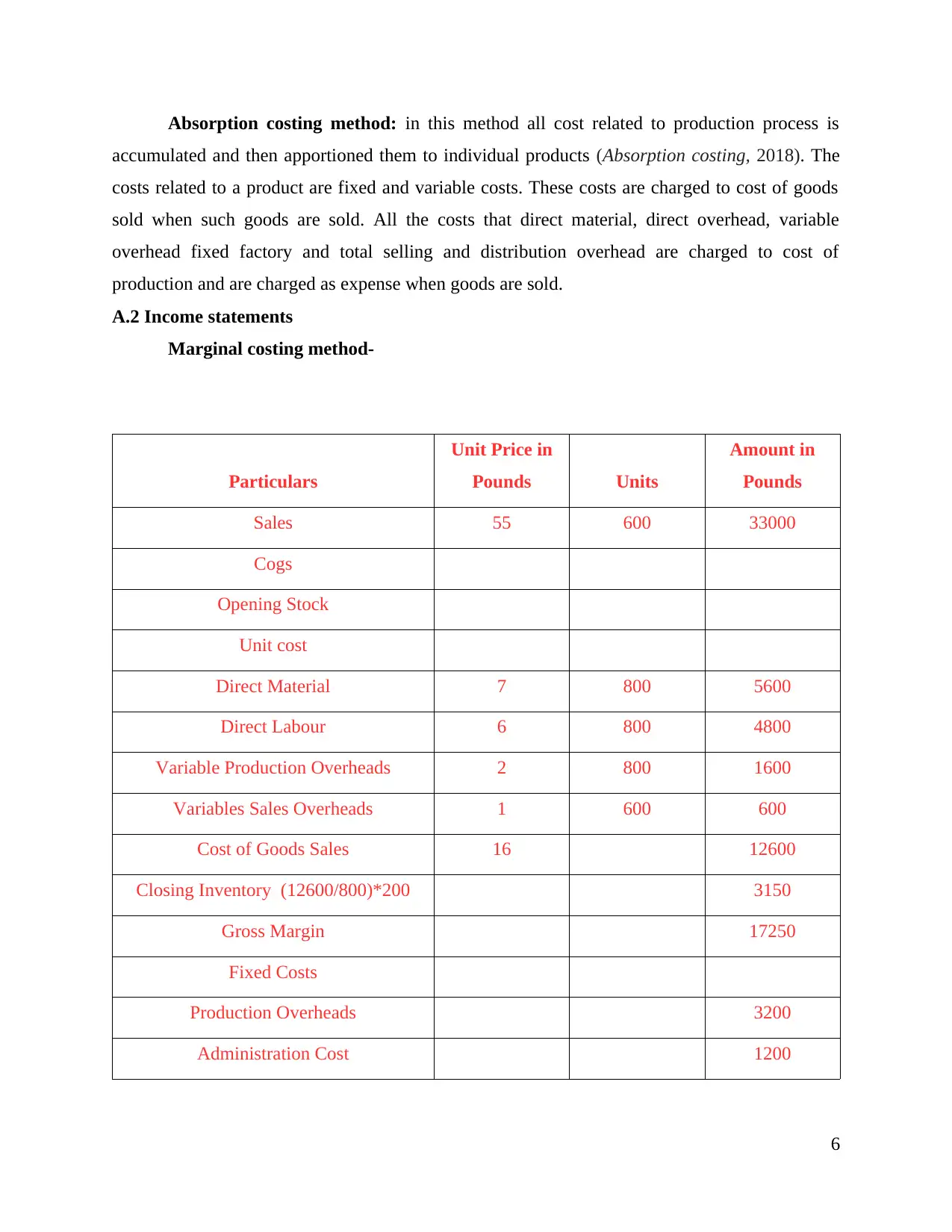

Absorption costing method: in this method all cost related to production process is

accumulated and then apportioned them to individual products (Absorption costing, 2018). The

costs related to a product are fixed and variable costs. These costs are charged to cost of goods

sold when such goods are sold. All the costs that direct material, direct overhead, variable

overhead fixed factory and total selling and distribution overhead are charged to cost of

production and are charged as expense when goods are sold.

A.2 Income statements

Marginal costing method-

Particulars

Unit Price in

Pounds Units

Amount in

Pounds

Sales 55 600 33000

Cogs

Opening Stock

Unit cost

Direct Material 7 800 5600

Direct Labour 6 800 4800

Variable Production Overheads 2 800 1600

Variables Sales Overheads 1 600 600

Cost of Goods Sales 16 12600

Closing Inventory (12600/800)*200 3150

Gross Margin 17250

Fixed Costs

Production Overheads 3200

Administration Cost 1200

6

accumulated and then apportioned them to individual products (Absorption costing, 2018). The

costs related to a product are fixed and variable costs. These costs are charged to cost of goods

sold when such goods are sold. All the costs that direct material, direct overhead, variable

overhead fixed factory and total selling and distribution overhead are charged to cost of

production and are charged as expense when goods are sold.

A.2 Income statements

Marginal costing method-

Particulars

Unit Price in

Pounds Units

Amount in

Pounds

Sales 55 600 33000

Cogs

Opening Stock

Unit cost

Direct Material 7 800 5600

Direct Labour 6 800 4800

Variable Production Overheads 2 800 1600

Variables Sales Overheads 1 600 600

Cost of Goods Sales 16 12600

Closing Inventory (12600/800)*200 3150

Gross Margin 17250

Fixed Costs

Production Overheads 3200

Administration Cost 1200

6

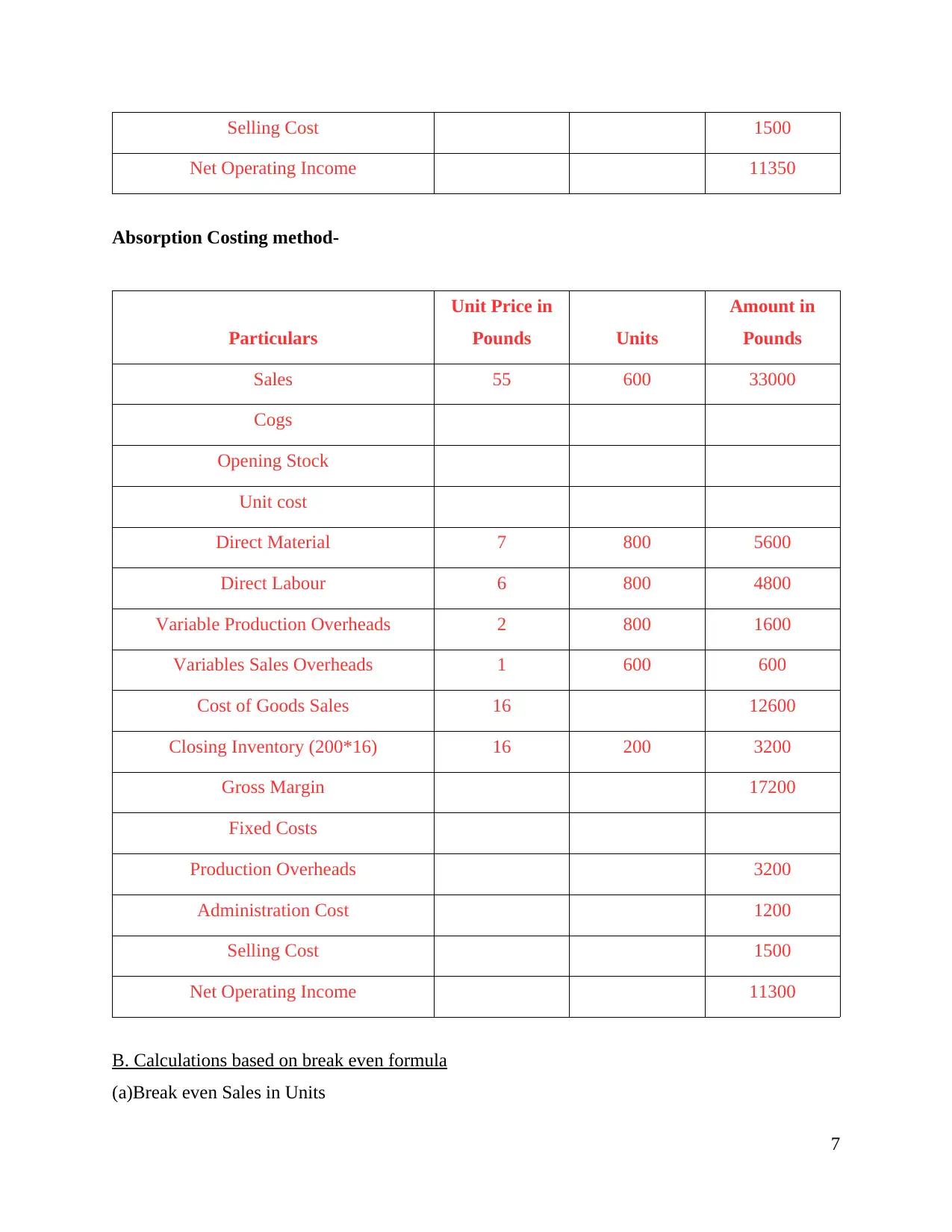

Selling Cost 1500

Net Operating Income 11350

Absorption Costing method-

Particulars

Unit Price in

Pounds Units

Amount in

Pounds

Sales 55 600 33000

Cogs

Opening Stock

Unit cost

Direct Material 7 800 5600

Direct Labour 6 800 4800

Variable Production Overheads 2 800 1600

Variables Sales Overheads 1 600 600

Cost of Goods Sales 16 12600

Closing Inventory (200*16) 16 200 3200

Gross Margin 17200

Fixed Costs

Production Overheads 3200

Administration Cost 1200

Selling Cost 1500

Net Operating Income 11300

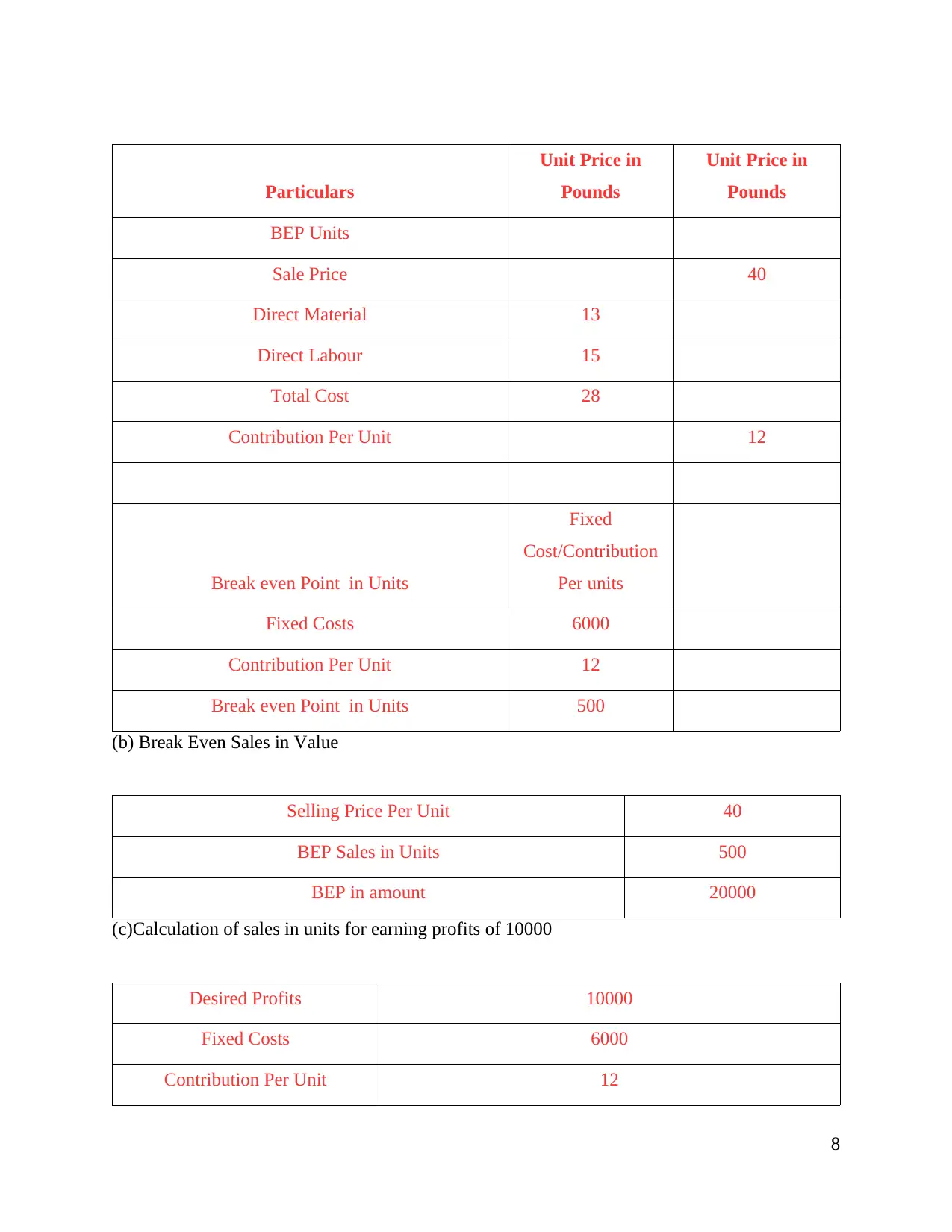

B. Calculations based on break even formula

(a)Break even Sales in Units

7

Net Operating Income 11350

Absorption Costing method-

Particulars

Unit Price in

Pounds Units

Amount in

Pounds

Sales 55 600 33000

Cogs

Opening Stock

Unit cost

Direct Material 7 800 5600

Direct Labour 6 800 4800

Variable Production Overheads 2 800 1600

Variables Sales Overheads 1 600 600

Cost of Goods Sales 16 12600

Closing Inventory (200*16) 16 200 3200

Gross Margin 17200

Fixed Costs

Production Overheads 3200

Administration Cost 1200

Selling Cost 1500

Net Operating Income 11300

B. Calculations based on break even formula

(a)Break even Sales in Units

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars

Unit Price in

Pounds

Unit Price in

Pounds

BEP Units

Sale Price 40

Direct Material 13

Direct Labour 15

Total Cost 28

Contribution Per Unit 12

Break even Point in Units

Fixed

Cost/Contribution

Per units

Fixed Costs 6000

Contribution Per Unit 12

Break even Point in Units 500

(b) Break Even Sales in Value

Selling Price Per Unit 40

BEP Sales in Units 500

BEP in amount 20000

(c)Calculation of sales in units for earning profits of 10000

Desired Profits 10000

Fixed Costs 6000

Contribution Per Unit 12

8

Unit Price in

Pounds

Unit Price in

Pounds

BEP Units

Sale Price 40

Direct Material 13

Direct Labour 15

Total Cost 28

Contribution Per Unit 12

Break even Point in Units

Fixed

Cost/Contribution

Per units

Fixed Costs 6000

Contribution Per Unit 12

Break even Point in Units 500

(b) Break Even Sales in Value

Selling Price Per Unit 40

BEP Sales in Units 500

BEP in amount 20000

(c)Calculation of sales in units for earning profits of 10000

Desired Profits 10000

Fixed Costs 6000

Contribution Per Unit 12

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Desired Sales Fixed Cost + Desired Profit/ Contribution per unit

Desired Sales in units 1333

(d)Calculation of Margin of Safety if 800 units are sold

Margin of Safety Actual Sales- Break even Sales

Actual sales 800

Break Even Sales 500

Margin of safety in Units 300

C. Financial reporting documents

The financial reporting documents includes balance sheet, income statement, cash flow

statement and statements of shareholder's equity (Financial statements, 2018). All these

statements together reveals the financial position of a business. It reveals profitability,

borrowings, position of equity and other financial details of the organisation.

Profit and loss account: another name for this account is income statement. This

statement presents costs, expenses and revenue of an organisation. The P&L statement after

taking into consideration all revenue and capitalised expenses shows the actual income earned by

business. This provides information about profits generate by business, with increment in

revenue and reducing costs and expenditures.

Balance sheet: a balance sheet presents the information of assets, liabilities and

shareholder's equity of a firm. The things owned by a company are called assets. The assets hold

a capacity either to be sold or used by company for production of good or services that can be

sold. Liabilities are amounts that company owes to others (Minnis, and Sutherland, 2017). This is

an obligation that has to be met by company. Shareholder's equity is the net worth of company. It

is the money which will be left if a company sales all its assets and pay all its liabilities.

Cash flow statement: this is a statement of cash inflow and outflow of a company. This

gives information about the cash availability with company. Do company have enough cash and

what amount of cash in hand it needs to purchase assets and pay all expenses.

9

Desired Sales in units 1333

(d)Calculation of Margin of Safety if 800 units are sold

Margin of Safety Actual Sales- Break even Sales

Actual sales 800

Break Even Sales 500

Margin of safety in Units 300

C. Financial reporting documents

The financial reporting documents includes balance sheet, income statement, cash flow

statement and statements of shareholder's equity (Financial statements, 2018). All these

statements together reveals the financial position of a business. It reveals profitability,

borrowings, position of equity and other financial details of the organisation.

Profit and loss account: another name for this account is income statement. This

statement presents costs, expenses and revenue of an organisation. The P&L statement after

taking into consideration all revenue and capitalised expenses shows the actual income earned by

business. This provides information about profits generate by business, with increment in

revenue and reducing costs and expenditures.

Balance sheet: a balance sheet presents the information of assets, liabilities and

shareholder's equity of a firm. The things owned by a company are called assets. The assets hold

a capacity either to be sold or used by company for production of good or services that can be

sold. Liabilities are amounts that company owes to others (Minnis, and Sutherland, 2017). This is

an obligation that has to be met by company. Shareholder's equity is the net worth of company. It

is the money which will be left if a company sales all its assets and pay all its liabilities.

Cash flow statement: this is a statement of cash inflow and outflow of a company. This

gives information about the cash availability with company. Do company have enough cash and

what amount of cash in hand it needs to purchase assets and pay all expenses.

9

Statement of shareholder's Equity: shareholder equity is the owner's fund. This provide

information about shares, total equity and ownership of company and how that has changed in a

financial year. The change in the shareholdings represents change in equity position of company.

The changes in equity can be in the debentures, equity shares, preference shares, paid up capital

and increase or decrease in capital of the firm.

Reporting analysis based upon above calculation states that if company wants to save tax

they should go with absorption costing and this costing also shows better financial profits and

also absorbs all the cost that are allocated to the product rather than marginal costing.

D. Interpretation of the data by financial reports

Interpretation of income statements:

Net income earned by Agmet from marginal costing method is 17500 and from

absorption costing net income is 17700. it is clear that the abortion costing is a method which

gives a better profitability as compared to marginal costing method (Brierley, 2017). It is

advisable for Agmet to go for absorption costing method to increase its profitability. With a

better sales and better profit the firm can ensures its long term survival in the industry. This also

makes sure the timely availability of working capital for regulating day to day business operation

of the business.

Interpretation of calculation by break even formula:

Break even point is a no profit no loss situation of a business. At this point the cost and

expenses incurred on business operation are equal to revenue generated by business. Agmet id

currently operating at a profit situation. To reach the break even point where cost and expenses

are equal the firm has to sell 222 units. The company has crossed the break even point and the

income earned is more than expenses incurred and this is a profit making situation for the firm,

Agmet has to make sure that its sells does not drop down below 222 as this will lead to a loss

position.

Break even point in sales can be calculated by dividing fixed expenses of company by

contribution margin ratio. The contribution margin is calculated as sales minus variable

10

information about shares, total equity and ownership of company and how that has changed in a

financial year. The change in the shareholdings represents change in equity position of company.

The changes in equity can be in the debentures, equity shares, preference shares, paid up capital

and increase or decrease in capital of the firm.

Reporting analysis based upon above calculation states that if company wants to save tax

they should go with absorption costing and this costing also shows better financial profits and

also absorbs all the cost that are allocated to the product rather than marginal costing.

D. Interpretation of the data by financial reports

Interpretation of income statements:

Net income earned by Agmet from marginal costing method is 17500 and from

absorption costing net income is 17700. it is clear that the abortion costing is a method which

gives a better profitability as compared to marginal costing method (Brierley, 2017). It is

advisable for Agmet to go for absorption costing method to increase its profitability. With a

better sales and better profit the firm can ensures its long term survival in the industry. This also

makes sure the timely availability of working capital for regulating day to day business operation

of the business.

Interpretation of calculation by break even formula:

Break even point is a no profit no loss situation of a business. At this point the cost and

expenses incurred on business operation are equal to revenue generated by business. Agmet id

currently operating at a profit situation. To reach the break even point where cost and expenses

are equal the firm has to sell 222 units. The company has crossed the break even point and the

income earned is more than expenses incurred and this is a profit making situation for the firm,

Agmet has to make sure that its sells does not drop down below 222 as this will lead to a loss

position.

Break even point in sales can be calculated by dividing fixed expenses of company by

contribution margin ratio. The contribution margin is calculated as sales minus variable

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.