Alumina Limited's Financial Audit: Ethical Standards and Analysis

VerifiedAdded on 2023/06/11

|13

|2902

|474

Report

AI Summary

This report provides an overview of audit and ethics concepts, focusing on Alumina Limited's financial analysis. It discusses the importance of auditing in ensuring financial statements present a true and fair view, and the role of ethics in maintaining smooth business operations. The report delves into materiality, both qualitatively and quantitatively, and analyzes Alumina Limited's cash flow statement to identify key inflows and outflows. It also examines the auditor's opinion on the company's annual report and conducts an analytical review using financial ratios to assess the company's performance and associated risks. The analysis includes current ratio, debt-equity ratio, and debt ratio, providing insights into the company's liquidity and financial structure. This document is available on Desklib, a platform providing study tools for students.

Running head: Audit and Ethics

Audit and Ethics

Name of the Student

Name of the University

Author Note

Audit and Ethics

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Audit and Ethics

Executive Summary

The report include about the concept of the audit and ethics. Audit is the process of

examination of the company financial statement and checks whether the financial statement

are showing true and fair view or not. Ethics are the norms which are made by the company

in related to the employees so that it can able to make the business smoothly. The report also

contain about the company name Alumina Limited and consist about it materiality and going

concern concept. It also contains about analytical review of the company and show how the

auditor check the risk associated in the financial statement with the help of the analytical

review. It also contains an analysis of the company cash flow statement and show which

items have most cash inflow and outflow.

Audit and Ethics

Executive Summary

The report include about the concept of the audit and ethics. Audit is the process of

examination of the company financial statement and checks whether the financial statement

are showing true and fair view or not. Ethics are the norms which are made by the company

in related to the employees so that it can able to make the business smoothly. The report also

contain about the company name Alumina Limited and consist about it materiality and going

concern concept. It also contains about analytical review of the company and show how the

auditor check the risk associated in the financial statement with the help of the analytical

review. It also contains an analysis of the company cash flow statement and show which

items have most cash inflow and outflow.

2

Audit and Ethics

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the company......................................................................................................3

Materiality in Financial Reporting.........................................................................................4

Qualitative approach of the Materiality.................................................................................4

Quantitative Aspects of the Materiality.................................................................................5

Cash Flow Analysis of the Company.....................................................................................8

Auditor opinion in the annual report......................................................................................9

Conclusion..................................................................................................................................9

Reference and Bibliography.....................................................................................................11

Audit and Ethics

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the company......................................................................................................3

Materiality in Financial Reporting.........................................................................................4

Qualitative approach of the Materiality.................................................................................4

Quantitative Aspects of the Materiality.................................................................................5

Cash Flow Analysis of the Company.....................................................................................8

Auditor opinion in the annual report......................................................................................9

Conclusion..................................................................................................................................9

Reference and Bibliography.....................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Audit and Ethics

Introduction

Auditing is a process which is been carried by an individual who check the financial

statement of the company and say whether the company financial statement are showing true

and fair view or not (Crigger and Godfrey 2014). This process helps the financial user to

know how the company is performing in the industry and what its growth rate in the industry

is. Audited financial statement help the company to get the confidents of the investors and

other financial users as it is a proof that all the business activity which the company carry are

fair and no fraud is been taken place in the company(D. Carnegie 2014). The auditor do many

test of control and check check each area of the company where the business is concern so

that it can able to judge whether the financial statement have some material misstatement or

not. It also check the internal control of the company and how the company manages its

internal control process as a whole. If the internal control of the company is weak than it

means there will be high risk in the financial statement of the company.

On the other hand ethics are the professional behaviour which every person should

follow while doing their work (Davies 2016). Each organization make some standard for their

employees to follow so that each individual will able to do their work properly as if there will

be some set of principles than it will be easy for the company to run their business smoothly

and effectively. It help the company to achieve its goals more easily as if all the work of the

company will be done in a systematic way than it will able to get the required result easily

and help them to achieve the business goals of the company.

Discussion

Overview of the company

The assignment is been based upon the company name Alumina Limited. The

company was found in 23 by the demerger of a big company name Western Mining

Audit and Ethics

Introduction

Auditing is a process which is been carried by an individual who check the financial

statement of the company and say whether the company financial statement are showing true

and fair view or not (Crigger and Godfrey 2014). This process helps the financial user to

know how the company is performing in the industry and what its growth rate in the industry

is. Audited financial statement help the company to get the confidents of the investors and

other financial users as it is a proof that all the business activity which the company carry are

fair and no fraud is been taken place in the company(D. Carnegie 2014). The auditor do many

test of control and check check each area of the company where the business is concern so

that it can able to judge whether the financial statement have some material misstatement or

not. It also check the internal control of the company and how the company manages its

internal control process as a whole. If the internal control of the company is weak than it

means there will be high risk in the financial statement of the company.

On the other hand ethics are the professional behaviour which every person should

follow while doing their work (Davies 2016). Each organization make some standard for their

employees to follow so that each individual will able to do their work properly as if there will

be some set of principles than it will be easy for the company to run their business smoothly

and effectively. It help the company to achieve its goals more easily as if all the work of the

company will be done in a systematic way than it will able to get the required result easily

and help them to achieve the business goals of the company.

Discussion

Overview of the company

The assignment is been based upon the company name Alumina Limited. The

company was found in 23 by the demerger of a big company name Western Mining

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Audit and Ethics

Corporation (Aluminalimited.com 2019). It headquarter is been situated in Southbank

Melbourne, Victoria, Australia. The business activity which is been carried by the company is

mining of bauxite, smelting of the pure alumina and extraction of alumina.

Materiality in Financial Reporting

The error and omission which happen in financial reporting of the company is been

termed as Materiality. This happen when the company does not give more attention to the

accounts and due to that some transaction are been omitted to get record in the financial book

and as a result create a material misstatement in the company account and which can also

affect the financial decision of the financial user of the company (DeFond and Zhang 2014).

The auditor should plan the materiality of the company in both at the time of the planning of

the audit and also at the time of process of the audit. As it help it to get an better view of the

transaction and will help it to know the risk and material misstatement in the company and

able to give a proper and fair opinion of the balance sheet. The materiality can be of two

types as qualitative and quantitative approach.

Qualitative approach of the Materiality

Steps in Qualitative approach:

o If the company have recorded any transaction not properly than it will directly affect

the company balance sheet. As if the company does not record the event properly than

it will overvalued or undervalued account will take place so it will be consider as a

material misstatement and will affect the financial user as it will not able to take

proper decision regarding the company financial position.

o Company should give all the disclosure of the events so if they will not give proper

disclosure in the company financial statement than the shareholder so the company

will not able to know the reason of the required entry as the company may do some

Audit and Ethics

Corporation (Aluminalimited.com 2019). It headquarter is been situated in Southbank

Melbourne, Victoria, Australia. The business activity which is been carried by the company is

mining of bauxite, smelting of the pure alumina and extraction of alumina.

Materiality in Financial Reporting

The error and omission which happen in financial reporting of the company is been

termed as Materiality. This happen when the company does not give more attention to the

accounts and due to that some transaction are been omitted to get record in the financial book

and as a result create a material misstatement in the company account and which can also

affect the financial decision of the financial user of the company (DeFond and Zhang 2014).

The auditor should plan the materiality of the company in both at the time of the planning of

the audit and also at the time of process of the audit. As it help it to get an better view of the

transaction and will help it to know the risk and material misstatement in the company and

able to give a proper and fair opinion of the balance sheet. The materiality can be of two

types as qualitative and quantitative approach.

Qualitative approach of the Materiality

Steps in Qualitative approach:

o If the company have recorded any transaction not properly than it will directly affect

the company balance sheet. As if the company does not record the event properly than

it will overvalued or undervalued account will take place so it will be consider as a

material misstatement and will affect the financial user as it will not able to take

proper decision regarding the company financial position.

o Company should give all the disclosure of the events so if they will not give proper

disclosure in the company financial statement than the shareholder so the company

will not able to know the reason of the required entry as the company may do some

5

Audit and Ethics

manipulation and no disclosure is given so it will create a fraud in the company so the

auditor should check that the company is giving proper disclosure is given related to

all the specific transaction done by the company.

Quantitative Aspects of the Materiality

Steps regarding the Quantitative Aspects are

o Auditor should analysis the industry benchmark as it will give it the amount of

materiality which is very common in the industry and which can be consider as

normal level of materiality in the company. So the auditor should make it sample

size and should do the audit as per the materiality. So the company can have a

materiality of 5-10% of net profit so this will be consider as a proper percentage in

regard of the materiality and that can be normal amount of materiality.

o Auditor should analysis all the necessary account of the company so that it can

know the level of the materiality in the financial account and as a result it will

give them a better overview of the company.

o Auditor should check the liquidity of the company as it will help it to know the

company liquid cash and able to judge the proper level of the materiality.

o Auditor should make a estimate of the company materiality so that it can be held

as the level of the materiality. The estimate of the company materiality should be

done on the basic of the industry benchmark and it also help it to do the compare

the company financial account more easily and effectively.

o Auditor should compare the estimation and actual which is there in the company

so it able to get the real performance of the company and also if the company had

more amount of the materiality in compare of estimation than the auditor should

Audit and Ethics

manipulation and no disclosure is given so it will create a fraud in the company so the

auditor should check that the company is giving proper disclosure is given related to

all the specific transaction done by the company.

Quantitative Aspects of the Materiality

Steps regarding the Quantitative Aspects are

o Auditor should analysis the industry benchmark as it will give it the amount of

materiality which is very common in the industry and which can be consider as

normal level of materiality in the company. So the auditor should make it sample

size and should do the audit as per the materiality. So the company can have a

materiality of 5-10% of net profit so this will be consider as a proper percentage in

regard of the materiality and that can be normal amount of materiality.

o Auditor should analysis all the necessary account of the company so that it can

know the level of the materiality in the financial account and as a result it will

give them a better overview of the company.

o Auditor should check the liquidity of the company as it will help it to know the

company liquid cash and able to judge the proper level of the materiality.

o Auditor should make a estimate of the company materiality so that it can be held

as the level of the materiality. The estimate of the company materiality should be

done on the basic of the industry benchmark and it also help it to do the compare

the company financial account more easily and effectively.

o Auditor should compare the estimation and actual which is there in the company

so it able to get the real performance of the company and also if the company had

more amount of the materiality in compare of estimation than the auditor should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Audit and Ethics

increase its scope of the audit as there will be more amount of risk involve in the

company financial account.

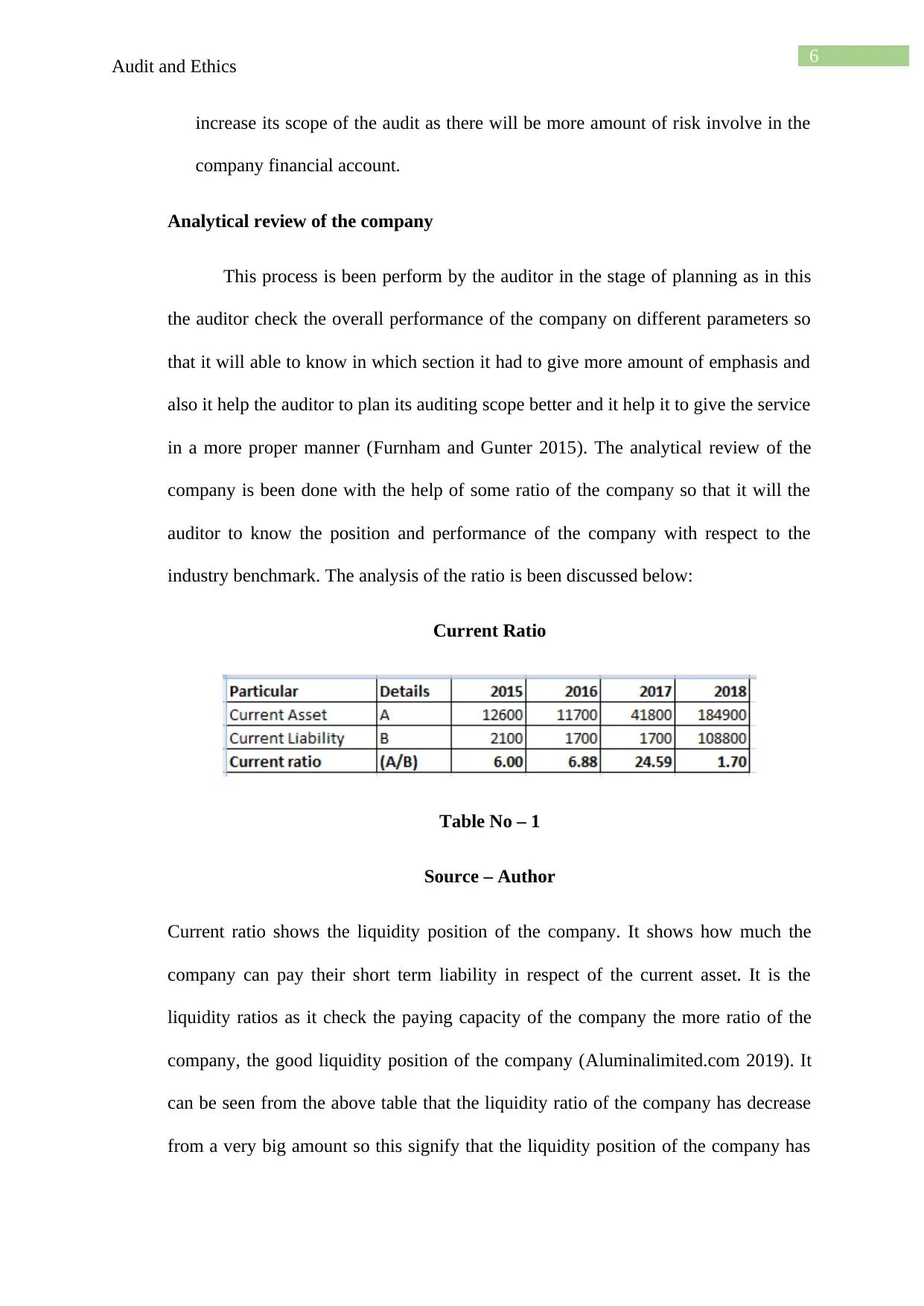

Analytical review of the company

This process is been perform by the auditor in the stage of planning as in this

the auditor check the overall performance of the company on different parameters so

that it will able to know in which section it had to give more amount of emphasis and

also it help the auditor to plan its auditing scope better and it help it to give the service

in a more proper manner (Furnham and Gunter 2015). The analytical review of the

company is been done with the help of some ratio of the company so that it will the

auditor to know the position and performance of the company with respect to the

industry benchmark. The analysis of the ratio is been discussed below:

Current Ratio

Table No – 1

Source – Author

Current ratio shows the liquidity position of the company. It shows how much the

company can pay their short term liability in respect of the current asset. It is the

liquidity ratios as it check the paying capacity of the company the more ratio of the

company, the good liquidity position of the company (Aluminalimited.com 2019). It

can be seen from the above table that the liquidity ratio of the company has decrease

from a very big amount so this signify that the liquidity position of the company has

Audit and Ethics

increase its scope of the audit as there will be more amount of risk involve in the

company financial account.

Analytical review of the company

This process is been perform by the auditor in the stage of planning as in this

the auditor check the overall performance of the company on different parameters so

that it will able to know in which section it had to give more amount of emphasis and

also it help the auditor to plan its auditing scope better and it help it to give the service

in a more proper manner (Furnham and Gunter 2015). The analytical review of the

company is been done with the help of some ratio of the company so that it will the

auditor to know the position and performance of the company with respect to the

industry benchmark. The analysis of the ratio is been discussed below:

Current Ratio

Table No – 1

Source – Author

Current ratio shows the liquidity position of the company. It shows how much the

company can pay their short term liability in respect of the current asset. It is the

liquidity ratios as it check the paying capacity of the company the more ratio of the

company, the good liquidity position of the company (Aluminalimited.com 2019). It

can be seen from the above table that the liquidity ratio of the company has decrease

from a very big amount so this signify that the liquidity position of the company has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Audit and Ethics

fallen. It can be seen from the table that both the asset and short term liability have

been increase in a very high percentage so due to these the overall current asset have

been fallen. So the auditor should check the reason of the increase of the asset and

liability as why the company have increase it by some a big amount and also it should

verify the asset and liability as it may happen company have just did overvaluation of

its amount and also it should check the disclosure is been given properly related to the

asset and liability and what the company have mention in the disclosure so the auditor

should check all the things properly.

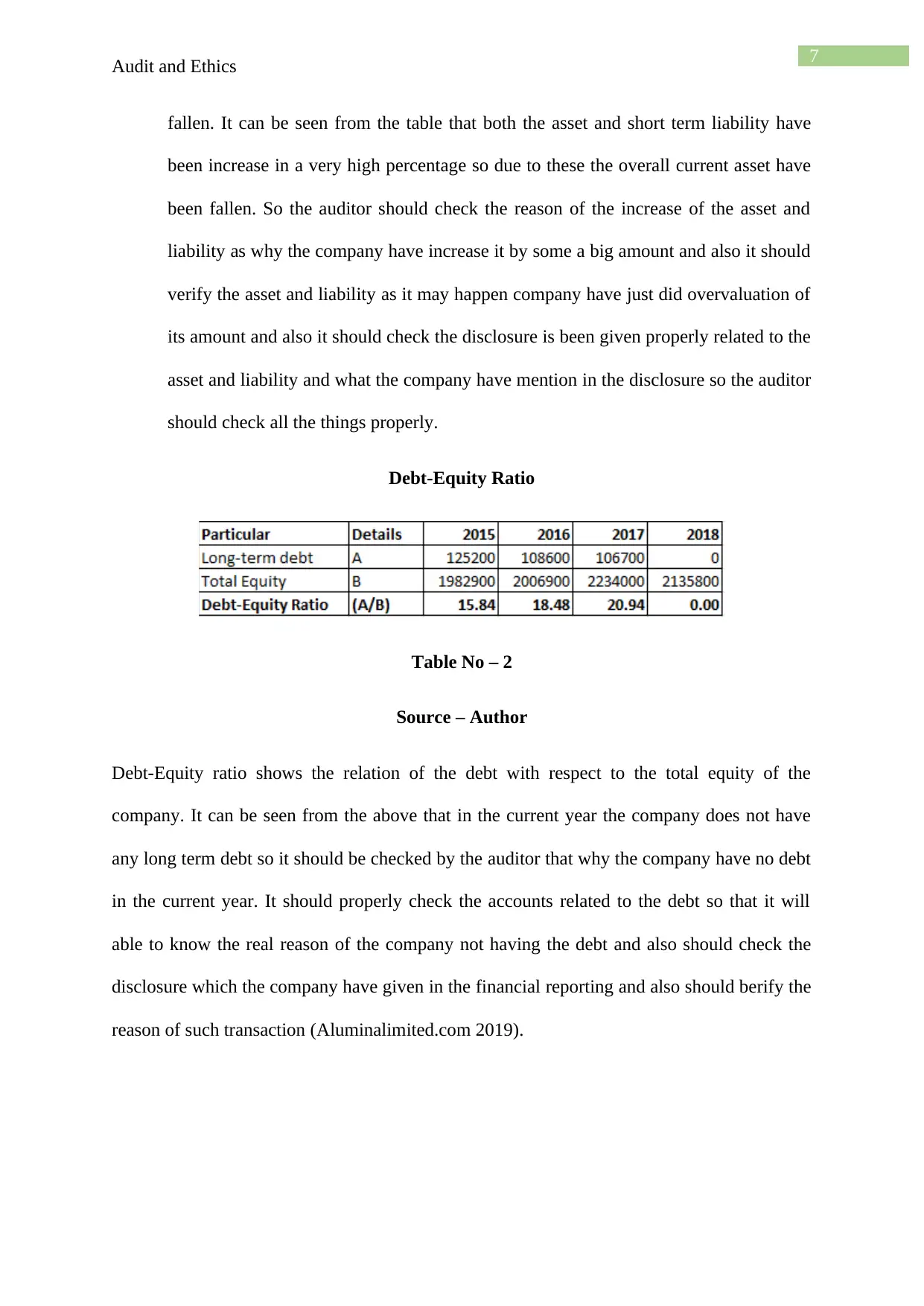

Debt-Equity Ratio

Table No – 2

Source – Author

Debt-Equity ratio shows the relation of the debt with respect to the total equity of the

company. It can be seen from the above that in the current year the company does not have

any long term debt so it should be checked by the auditor that why the company have no debt

in the current year. It should properly check the accounts related to the debt so that it will

able to know the real reason of the company not having the debt and also should check the

disclosure which the company have given in the financial reporting and also should berify the

reason of such transaction (Aluminalimited.com 2019).

Audit and Ethics

fallen. It can be seen from the table that both the asset and short term liability have

been increase in a very high percentage so due to these the overall current asset have

been fallen. So the auditor should check the reason of the increase of the asset and

liability as why the company have increase it by some a big amount and also it should

verify the asset and liability as it may happen company have just did overvaluation of

its amount and also it should check the disclosure is been given properly related to the

asset and liability and what the company have mention in the disclosure so the auditor

should check all the things properly.

Debt-Equity Ratio

Table No – 2

Source – Author

Debt-Equity ratio shows the relation of the debt with respect to the total equity of the

company. It can be seen from the above that in the current year the company does not have

any long term debt so it should be checked by the auditor that why the company have no debt

in the current year. It should properly check the accounts related to the debt so that it will

able to know the real reason of the company not having the debt and also should check the

disclosure which the company have given in the financial reporting and also should berify the

reason of such transaction (Aluminalimited.com 2019).

8

Audit and Ethics

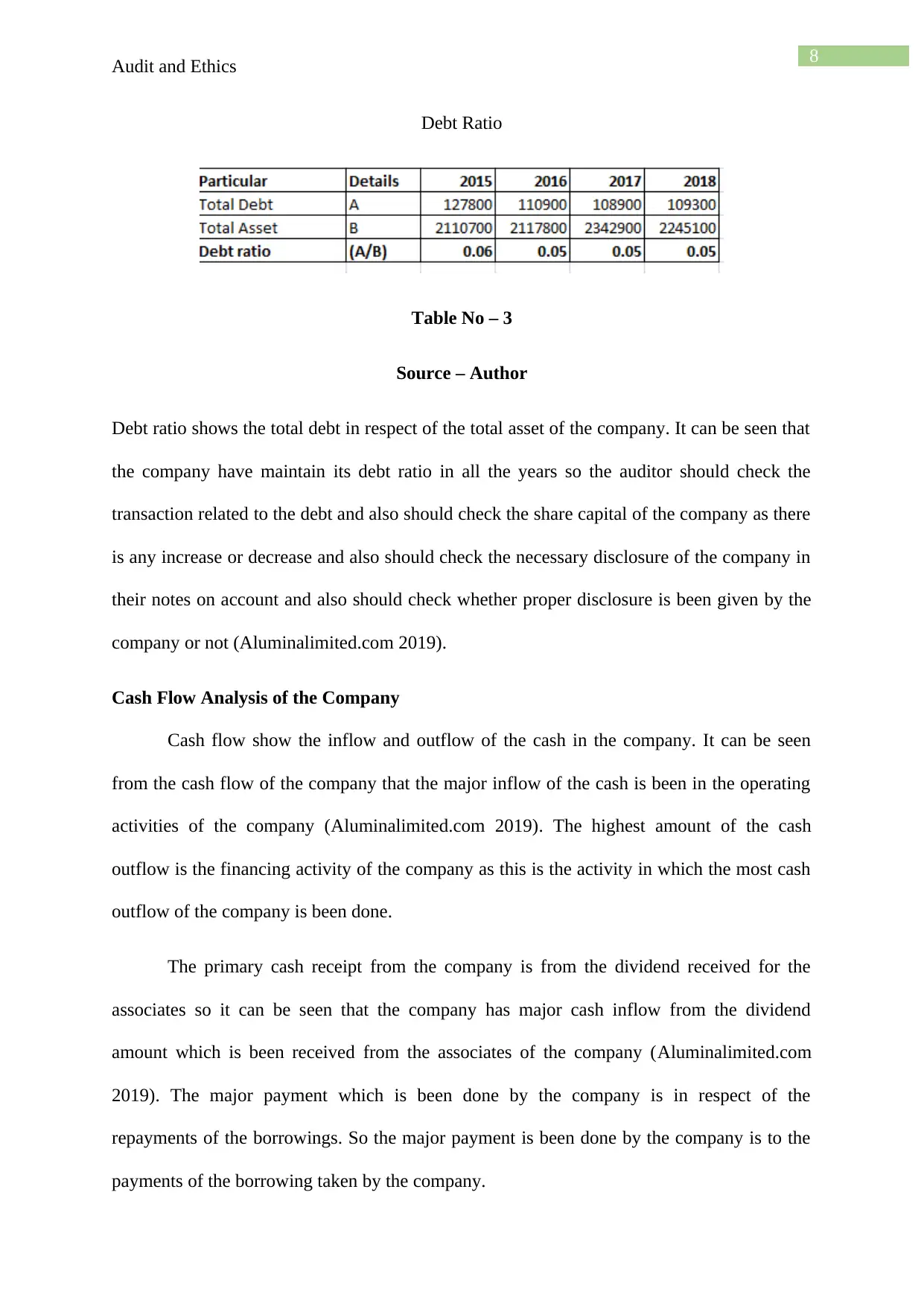

Debt Ratio

Table No – 3

Source – Author

Debt ratio shows the total debt in respect of the total asset of the company. It can be seen that

the company have maintain its debt ratio in all the years so the auditor should check the

transaction related to the debt and also should check the share capital of the company as there

is any increase or decrease and also should check the necessary disclosure of the company in

their notes on account and also should check whether proper disclosure is been given by the

company or not (Aluminalimited.com 2019).

Cash Flow Analysis of the Company

Cash flow show the inflow and outflow of the cash in the company. It can be seen

from the cash flow of the company that the major inflow of the cash is been in the operating

activities of the company (Aluminalimited.com 2019). The highest amount of the cash

outflow is the financing activity of the company as this is the activity in which the most cash

outflow of the company is been done.

The primary cash receipt from the company is from the dividend received for the

associates so it can be seen that the company has major cash inflow from the dividend

amount which is been received from the associates of the company (Aluminalimited.com

2019). The major payment which is been done by the company is in respect of the

repayments of the borrowings. So the major payment is been done by the company is to the

payments of the borrowing taken by the company.

Audit and Ethics

Debt Ratio

Table No – 3

Source – Author

Debt ratio shows the total debt in respect of the total asset of the company. It can be seen that

the company have maintain its debt ratio in all the years so the auditor should check the

transaction related to the debt and also should check the share capital of the company as there

is any increase or decrease and also should check the necessary disclosure of the company in

their notes on account and also should check whether proper disclosure is been given by the

company or not (Aluminalimited.com 2019).

Cash Flow Analysis of the Company

Cash flow show the inflow and outflow of the cash in the company. It can be seen

from the cash flow of the company that the major inflow of the cash is been in the operating

activities of the company (Aluminalimited.com 2019). The highest amount of the cash

outflow is the financing activity of the company as this is the activity in which the most cash

outflow of the company is been done.

The primary cash receipt from the company is from the dividend received for the

associates so it can be seen that the company has major cash inflow from the dividend

amount which is been received from the associates of the company (Aluminalimited.com

2019). The major payment which is been done by the company is in respect of the

repayments of the borrowings. So the major payment is been done by the company is to the

payments of the borrowing taken by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Audit and Ethics

The cash flow of the company is not having any non cash financial item in it. The

investing activities which the company has is one is the outflow of the cash which is related

to the payments made for the investment in the associates and it has one inflow which is

related to the proceeds of the return from the investing activities. So these are two activities

in the cash from investing activities in the company cash flow (Aluminalimited.com 2019).

It can be seen that the cash flow of the company that the company is having a good

financial position so it can be say that the company is having going concern and it will not

shut its business soon (Aluminalimited.com 2019). So the auditor should do test of control so

that it can help it to know more about the company and will able to give more fair opinion to

the financial report

Auditor opinion in the annual report

The auditor of the company is PWC and they have given the company an Unqualified

Report. The company has said in it opinion that the company financial statement are showing

true and fair view and it has maintained all the financial statement in respect of the Australian

accounting standard (Aluminalimited.com 2019). The financial report of the company is not

having any paragraph related to the audit issue so it can be say that the auditor company have

not face any issue while doing the audit of the company.

Conclusion

The report is been concluded about the auditor auditing process and ethics in the

company. Auditing help the user to know whether the financial statement are showing true

and fair view or not. On the other hand ethics are the rules and regulation which are made by

the company for the employees so that it can able to run the business properly and smoothly.

The report also concludes about the company name Alumina Limited. It contains the

audit process related to the company. It also have the concept of the materiality and how the

Audit and Ethics

The cash flow of the company is not having any non cash financial item in it. The

investing activities which the company has is one is the outflow of the cash which is related

to the payments made for the investment in the associates and it has one inflow which is

related to the proceeds of the return from the investing activities. So these are two activities

in the cash from investing activities in the company cash flow (Aluminalimited.com 2019).

It can be seen that the cash flow of the company that the company is having a good

financial position so it can be say that the company is having going concern and it will not

shut its business soon (Aluminalimited.com 2019). So the auditor should do test of control so

that it can help it to know more about the company and will able to give more fair opinion to

the financial report

Auditor opinion in the annual report

The auditor of the company is PWC and they have given the company an Unqualified

Report. The company has said in it opinion that the company financial statement are showing

true and fair view and it has maintained all the financial statement in respect of the Australian

accounting standard (Aluminalimited.com 2019). The financial report of the company is not

having any paragraph related to the audit issue so it can be say that the auditor company have

not face any issue while doing the audit of the company.

Conclusion

The report is been concluded about the auditor auditing process and ethics in the

company. Auditing help the user to know whether the financial statement are showing true

and fair view or not. On the other hand ethics are the rules and regulation which are made by

the company for the employees so that it can able to run the business properly and smoothly.

The report also concludes about the company name Alumina Limited. It contains the

audit process related to the company. It also have the concept of the materiality and how the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Audit and Ethics

auditor analysis it and also contain an analytical review of the company and how it help the

auditor to know the risk in the company.

Audit and Ethics

auditor analysis it and also contain an analytical review of the company and how it help the

auditor to know the risk in the company.

11

Audit and Ethics

Reference and Bibliography

Aluminalimited.com (2019). Alumina Limited. [online] Aluminalimited.com. Available at:

https://www.aluminalimited.com/latest-annual-report/ [Accessed 15 May 2019].

Crigger, N. and Godfrey, N., 2014. From the inside out: A new approach to teaching

professional identity formation and professional ethics. Journal of Professional

Nursing, 30(5), pp.376-382.

D. Carnegie, G., 2014. The present and future of accounting history. Accounting, Auditing &

Accountability Journal, 27(8), pp.1241-1249.

Davies, P.W., 2016. Current issues in business ethics. Routledge.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeMartino, G.F. and McCloskey, D.N. eds., 2016. The Oxford handbook of professional

economic ethics. Oxford University Press.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffin, P.A. and Wright, A.M., 2015. Commentaries on Big Data's importance for

accounting and auditing. Accounting Horizons, 29(2), pp.377-379.

Guthrie, J. and D. Parker, L., 2014. The global accounting academic: what

counts!. Accounting, Auditing & Accountability Journal, 27(1), pp.2-14.

Harris, S.E. and Robinson Kurpius, S.E., 2014. Social networking and professional ethics:

Client searches, informed consent, and disclosure. Professional Psychology: Research and

Practice, 45(1), p.11.

Audit and Ethics

Reference and Bibliography

Aluminalimited.com (2019). Alumina Limited. [online] Aluminalimited.com. Available at:

https://www.aluminalimited.com/latest-annual-report/ [Accessed 15 May 2019].

Crigger, N. and Godfrey, N., 2014. From the inside out: A new approach to teaching

professional identity formation and professional ethics. Journal of Professional

Nursing, 30(5), pp.376-382.

D. Carnegie, G., 2014. The present and future of accounting history. Accounting, Auditing &

Accountability Journal, 27(8), pp.1241-1249.

Davies, P.W., 2016. Current issues in business ethics. Routledge.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), pp.275-326.

DeMartino, G.F. and McCloskey, D.N. eds., 2016. The Oxford handbook of professional

economic ethics. Oxford University Press.

Furnham, A. and Gunter, B., 2015. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Griffin, P.A. and Wright, A.M., 2015. Commentaries on Big Data's importance for

accounting and auditing. Accounting Horizons, 29(2), pp.377-379.

Guthrie, J. and D. Parker, L., 2014. The global accounting academic: what

counts!. Accounting, Auditing & Accountability Journal, 27(1), pp.2-14.

Harris, S.E. and Robinson Kurpius, S.E., 2014. Social networking and professional ethics:

Client searches, informed consent, and disclosure. Professional Psychology: Research and

Practice, 45(1), p.11.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.